|

3. Development

Contributions Policy 2025

|

|

Reference Te Tohutoro:

|

25/994794

|

|

Responsible Officer(s) Te Pou Matua:

|

Ellen

Cavanagh, Senior Policy Analyst

|

|

Accountable ELT Member Pouwhakarae:

|

John

Higgins, General Manager Strategy, Planning & Regulatory Services

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is for the Council to adopt the draft Development

Contributions Policy 2025.

1.2 The Council has previously received the written and oral submissions

on the draft policy and resulting staff advice.

1.3 The Local Government Act 2002 (‘LGA’) requires

all local authorities to have a policy on development contributions or

financial contributions and to review it every three years. As the

Council’s policy was last adopted in 2021, it is due for review.

2. Officer Recommendations Ngā

Tūtohu

That the Council:

1. Receives the information in the Development Contributions

Policy 2025 Report.

2. Notes that the decision in this report is

assessed as medium significance based on the Christchurch City Council’s

Significance and Engagement Policy.

3. Adopts the draft Development Contributions

Policy 2025 (Attachment A to this report).

4. Agrees that the Development Contributions

Policy 2025 will come into force from 1 July 2025.

5. Delegates to staff to correct any

typographical or minor drafting errors in the Development Contributions Policy

2025.

6. Agrees to remit the difference in cost between a development

contributions assessment undertaken under a previous development contributions

policy and the Development Contributions Policy 2025 where the total assessment

is reduced under the 2025 policy.

3. Executive Summary Te Whakarāpopoto Matua

3.1 Section

102 of the LGA requires all

local authorities to have a policy on development contributions or financial

contributions. The Development Contributions Policy (‘the policy’)

must comply with the requirements of section 106 and sections 197AA to 211 of

the LGA. This includes the policy being reviewed at least once every three

years.

3.2 The

policy has been under review since mid-2023. On 19 February 2025, the Council

resolved to commence public consultation on the draft policy[1].

Consultation ran from 25 February to 26 March 2025 and submitters were heard

between 3 and 15 April 2025 as part of the draft Annual Plan 2025/26 process.

3.3 A

post-consultation workshop was held with the Council on Monday 19 May where

submitter feedback and staff advice were discussed. The workshop focused on

issues where submitters requested changes to the policy. Elected member

feedback has informed the final draft policy that is presented for adoption.

Policy changes

reflect principle of averages

3.4 Many

of the key policy changes proposed are designed to ensure the development contribution assessment

provisions are aligned with the overarching principle of averaging.

3.5 The LGA provides for averaging or grouping of different development

types. The policy is built on the assumed average demand for a range of

development types and for most developments this averaging will be sufficient

to determine a development contribution requirement.

3.6 The policy should only look to adjust when actual demand is either

half or double assumed demand. This threshold aligns

with the Ryman Healthcare v Auckland Council objection decision. In this

decision, the Commissioner accepted that that a 50% threshold was appropriate

for demonstrating a substantial reduction in demand.

3.7 The current (2021) policy, however, provides several discounts when

this threshold has not been met. The policy does not do the same for

developments where actual demand is slightly higher than the averages. This approach has caused revenue leakages because the Council is

reducing the development contribution requirements within the averages built

into the policy. This means ratepayers are currently subsidising the cost

of growth.

Growth projections and charges

reflect a return to ‘normal’

3.8 Another

change between the current and draft policies is the per-Household Unit

Equivalent (‘HUE’) development contributions charges.

Development contribution charges are calculated by dividing cost to deliver the

growth component of an asset by the number of new or additional households.

3.9 Overall,

the charges in the draft policy have increased compared to the 2021 policy,

however the 2021 charges were unusually low primarily due to a high rate of

growth projected due to post-earthquake population shifts and

changes in the district. The growth modelling that underpins the draft policy

reflects a ‘return to normal’ growth patterns in the district.

Consequently, the draft charges reflect a return to more normal development

contributions charges and are in line with the pre-2021 charges.

Clear split in opinions between developers and

non-developers

3.10 Forty-four

submissions were received on the policy, most from developers or those

associated with the development sector. With respect to the policy changes,

there is a clear split in views between those submitters who have (developers)

and those who have not (non-developers) paid development contributions before.

This reflects the choice that the Council must make in deciding whether or not

ratepayers should subsidise growth development or growth should pay for growth.

Incorporation of feedback into the draft

policy

3.11 Staff

have made changes to the draft policy as a result of feedback received from

submitters and elected members. The proposed post-consultation changes are

outlined in section 10 of this report. A track changes version of the final

draft policy is included as Attachment B.

4. Background/Context Te Horopaki

4.1 Under

the LGA the Council is required to have a policy on development contributions

(s102(2)(d)) and to review it every three years (s106(6)). The current policy

was adopted in July 2021 and a review of the policy is required.

4.2 Development

contributions enable the Council to recover a fair share of the cost of

providing infrastructure to service growth development from those who benefit

from the provision of that investment.

4.3 Development

contributions are a cost recovery tool for the growth component of

projects agreed to in the capital programme. If the Council did not recover

these costs from development contributions, the costs would be recovered from

rates.

4.4 The

policy details the methodology used to establish development contribution

charges per HUE, the resulting cost of those charges, the methodology used to

assess a development for the level of development contributions required and

various process requirements associated with operating a fair and consistent

development contributions process.

5. Policy review process

5.1 Development

contribution charges are derived directly from the cost the Council incurs to

provide infrastructure to service growth development. The revenue is used to

pay down debt taken out to initially fund the investment in growth

infrastructure.

5.2 The

policy has many discrete inputs, all of which must be reviewed as part of any

policy review process. These include residential growth model, business growth

model, transport growth model, capital expenditure programmes related to

growth, interest and inflation rate forecasts and reviews of the numerous

methodologies used as the basis for the calculation and assessment of

development contributions.

5.3 In

addition, this review process has included reviewing the use of catchments to

calculate and assess development contributions. This review has also been an

opportunity to evaluate the content and structure of the policy to improve

clarity and legibility.

5.4 Ten information sessions/workshops have taken place for the members

of the meeting:

6. Community Views and Preferences

6.1 In

June 2024, early conversations with the Halswell Residents Association were had

at their Councillor’s request. This particularly concerned how catchments

work and growth components within transport projects.

6.2 Later

that month, staff presented to the Property Council New Zealand South Island

Regional Committee on all main policy changes. This was to give them a chance

to ask questions face-to-face prior to public consultation opening.

6.3 Staff

presented on or discussed the draft policy at several Developers’ Forums

(as well as sending emails about consultation delays) from mid-2024 until

consultation opened. At these meetings there was clear concern about the

increase in development contribution costs.

6.4 Public

consultation started on 25 February and ran until 26 March 2025.

6.5 Consultation

details, including links to the project information shared on the Kōrero

mai | Let’s talk webpage were advertised via:

· An email sent to over 420

identified stakeholders, including residents’ associations, developers,

interest-groups, and Kōrero mai subscribers who requested to be notified

when projects like this opened for feedback. A follow-up email one week before

consultation closed was also sent to these stakeholders.

· A

Newsline story was published, receiving 469 views. This was shared to

Council’s Facebook page, where 10,741 accounts were reached and 1,153

users interacted (commented, interacted, clicked etc.).

· Consultation documents

were available at all libraries and service centres.

6.6 The

Kōrero mai

| Let’s talk page had 1, 504 views throughout the consultation

period.

6.7 Staff

hosted a webinar on

the consultation that was attended by 10 people at the time and has been viewed

126 times since.

Hearing of submissions

6.8 Submissions

on the draft policy were heard alongside submissions on the draft Annual Plan

2025/26 in April 2025.

6.9 Submissions

were heard by the full Council, chaired by the Mayor. The hearing was open to

the public and livestreamed on the Council’s website.

Overview of submissions

6.10 Submissions

were made by 11 recognised organisations, 18 businesses and 15 individuals. All

submissions will be available on the Kōrero mai webpage.

6.11 Of

the 44 submitters, 24 (55%) have previously paid development contributions or

anticipate paying them within the next three years. 20 (45%) haven’t paid

them and don’t expect to.

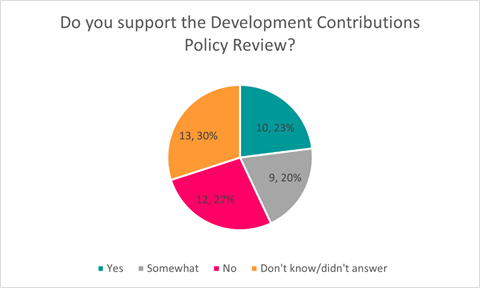

6.12 Overall,

when asked whether submitters supported the Development Contributions Policy

Review, 23% (10) said yes, 20% (9) somewhat, 27% (12) said no, and the

remaining 30% (13) didn’t know or didn’t answer this question.

6.13 Submitters

who have never paid development contributions and don't anticipate doing so

were nearly twice as likely to support the policy review. Specifically, 30% of

these submitters (6 out of 20) expressed support, compared to 17% of those who

have paid (4 out of 24).

6.14 A

thematic analysis of submissions is available in section 8.

Council workshop on consultation feedback

6.15 A

workshop was held on submissions and proposed post-consultation changes on

Monday 19 May.

6.16 At

the workshop, elected members were informed on matters related to consultation,

feedback from submitters on the draft policy and resulting staff advice.

Elected members had the opportunity to provide feedback to staff as to their

preferred policy positions and to ask questions and seek clarification on the

policy and associated issues.

7. Principles of Setting and Calculating Development Contributions

Background -

principles of averaging

7.1 The

LGA allows for the use of averaging by development types. This means

developments within a development type category will be assessed as having the

same level of demand, regardless of individual variations.

7.2 A

HUE is the unit of demand used in the policy to calculate development

contributions charges and determine the development contributions requirement

for each development. A HUE represents the average demand a household places on

Council infrastructure and it is assumed that all single households place this

level of demand on Council infrastructure. This is an efficient method of

assessing development contributions for residential development.

Non-residential developments are assessed as a proportion of the HUE.

7.3 The

policy assumes the average household contains 2.6 people, which is consistent

with the growth modelling used in the Long-Term Plan (‘LTP’)

2024-34.

7.4 The

base unit measures for the HUE are outlined in clause 3.2.1 of the draft policy

and are summarised below. The base units are updated as part of each policy

review to ensure an accurate reflection of average household demand.

|

Activity

|

Demand per

HUE

|

|

Water supply

|

644.30 litres

per day

|

|

Wastewater

|

572 litres

per day

|

|

Stormwater

and Flood Protection

|

367 m2 impervious

surface area (ISA)

|

|

Transport

|

6.35 vehicle

trips per day

|

Background -

Special assessments

7.5 The

policy is based on average demand for a range of development types. Development

contributions required for non-residential development are calculated as a

multiple of the HUE. For the transport, water supply and wastewater

activities the development contribution requirement is calculated according to

the average demand on infrastructure per square metre of gross floor area

(‘GFA’) by business type. For stormwater and flood

protection the development contribution is calculated according to the

impervious surface area (‘ISA’) of the development. The non-residential HUE equivalences (also referred to as HUE

multipliers) are detailed in Part 8 of the draft policy.

7.6 For

most developments, the use of the HUE equivalences will be appropriate to

determine a development contribution requirement. There will be some

developments, however, where actual demand is significantly different to the

demand assumptions built into the policy. In these instances, the Council will

undertake a special assessment or an actual demand assessment.

7.7 The

threshold for a special assessment is when actual demand is half or double what

is built into the policy. This aligns with the Ryman Healthcare v Auckland

Council objection decision. In this decision, the Commissioner accepted

that that a 50% threshold was appropriate for demonstrating a substantial

reduction in demand.

7.8 The

draft policy did not propose to remove the special assessment provision from

the policy. Some submitters appeared to confuse special assessments and

remissions, but these are quite different issues in the policy. Issues

related to remissions are detailed below.

8. Submission feedback and

workshop discussion

Residential unit adjustments

8.1 The

Council assesses each residential unit at a base rate of 1 HUE. However, there

will be circumstances where actual demand is half or double assumed demand and

therefore it is appropriate to provide a residential unit adjustment.

8.2 Providing

some kind of adjustment for small and/or large residential units is common

across development contributions policies. Councils across New Zealand have

taken a range of approaches to providing these adjustments.

8.3 The

Council has used GFA to make small residential unit adjustments since 2007.

However, there is no data that correlates the GFA of a residential unit with

number of usual residents or with demand on infrastructure. In 2024, 45%

of building consents were for homes less than 100m2. This means the

Council is providing a discount for close to half of all new homes, which is

not what the policy is intended to do.

8.4 Census

data shows that the greater the number of bedrooms in a residential unit the

more people are likely living in it. The more usual residents in a residential

unit, the greater level of demand on Council services.

Average

number of usual residents per dwelling type as at Census 2023

|

Dwelling type

|

One bedroom

|

Two bedrooms

|

Three bedrooms

|

Four bedrooms

|

Five bedrooms

|

Six bedrooms

|

Seven bedrooms

|

Eight bedrooms

|

|

Average residents

|

1.36

|

1.82

|

2.56

|

3.19

|

3.83

|

4.80

|

5.07

|

5.10

|

8.5 The draft policy proposes to move to bedroom-based adjustments as a

result.

Small residential unit adjustment

8.5.1 What

was consulted on: The draft policy proposed moving to a residential unit adjustment based on bedrooms

and keeping a small unit adjustment for one-bedroom residential units only.

This will ensure that the Council only adjusts for developments that fall

outside the assumptions built into the policy.

8.5.2 Feedback from submitters: There were

mixed views on change to small unit adjustment. Five submitters supported the

change, eight were opposed and three expressed mixed views. Several submitters

also requested the Council introduce an adjustment for two-bedroom units. Two

submitters asked that the small unit adjustment just be applied to developments

in the central city.

8.5.3 Staff

advice in workshop: 2023 Census data shows that the average one-bedroom

residential unit in Christchurch has 1.36 usual residents living in it. As an

average household is 2.6 people, this dwelling type is assumed to put half the

average demand on Council infrastructure.

8.5.4 With respect to a two-bedroom adjustment, 2023

Census data confirms that the average two-bedroom residential unit in

Christchurch has 1.82 people, which does not meet the threshold for a special

assessment under the policy. If a change were to be

made, the large residential unit adjustment would need to come down, either to

four or five bedrooms, to reflect that an adjustment has been made within the

averages and ensure the Council continues to recover the cost of growth from

new development. This would increase the administrative complexity of the

policy and staff do not recommend making this change.

8.5.5 There is no data that would support having a one-bedroom adjustment

just for central city developments.

8.5.6 Workshop discussion: At the 19 May 2025

workshop, councillors provided no further guidance on the small

residential unit adjustment as proposed.

8.5.7 Recommendation for final policy:

One-bedroom residential units will be assessed at 0.6 HUE for all activities.

Large

residential unit adjustment

8.5.8 What

was consulted on: The draft policy introduced a large residential unit adjustment for dwelling

types of seven or more bedrooms assessed at 1.4 HUE. This was intended to

ensure the development contribution charge better reflects the usually higher

demand on infrastructure from larger homes.

8.5.9 Feedback from submitters: There were

mixed views on the change to the large residential unit adjustment with two

supporting, four opposed and three expressing mixed views. Some submitters

questioned whether the threshold should be lower or whether the adjustment

should increase with each additional bedroom.

8.5.10 Staff

advice in workshop: 2023 Census data shows that the average seven-bedroom

residential unit in Christchurch has 5.07 usual residents living in it. As an

average household is 2.6 people, this dwelling type is assumed to put double

the average demand on Council infrastructure.

8.5.11 Some

submitters also asked whether the adjustment could be for 0.4 per additional

room. 0.4 HUE is effectively the equivalent of one person so the Council could

add 0.4 per additional room for seven bedrooms and over. However, census data

does not support this change; eight-bedroom homes have only a slightly higher

number of residents compared to seven-bedroom homes. The overall impact of a

change like this is likely to be minimal given the small number of dwellings of

this size in the district. Therefore, staff did not recommend this change.

8.5.12 Workshop discussion: At the 19 May 2025

workshop, councillors provided no further guidance on the large

residential unit adjustment as proposed.

8.5.13 Recommendation for final policy: Houses

with seven or more bedrooms are charged an additional 0.4 HUE for all

activities except for stormwater.

Stormwater discounts

8.6 The

Council currently provides two reductions for stormwater activity. Both are out

of alignment with the special assessment threshold in the policy and the draft

proposed changes to bring the assessment of the stormwater activity back into

line with the overall principle of averages as discussed in section 7.

Developer provided infrastructure

8.6.1 What

was consulted on: The draft

policy provides that stormwater reductions will only be provided in instances

where developers provide on-site stormwater mitigation and the resulting demand

on Council infrastructure is less than half of the average assumed demand as

detailed in the policy. This would see relatively minor adjustments (such as

for the installation of a rainwater tank) cease.

8.6.2 Feedback from submitters: There were

mixed views on the proposal to bring stormwater adjustments for developer

provided infrastructure into line with the special assessment provisions of the

policy as outlined in paragraphs 7.5 – 7.7. Four submitters supported the change, six were opposed and two

expressed mixed views

8.6.3 Staff

advice in workshop: The change is intended to bring

stormwater adjustments into line with the rest of the policy. The Council

will still undertake a special assessment if the development exerts a level of

demand on infrastructure that will be significantly different from the level of

assumed demand in the policy for that type of development.

8.6.1 Staff follow a set methodology to determine degree to which demand

on the Council's network has been mitigated by the developer provided

infrastructure. Each relevant development is reviewed using this

methodology.

8.6.2 Staff note that on occasion, developer-provided infrastructure is

vested with the Council, but the assessment receives a stormwater discount of

less than 50% due to the level of mitigation provided. Council may consider it

fair to include a provision for these sites to still receive a stormwater

adjustment due to the asset being vested.

8.6.3 Workshop discussion: At the 19 May

workshop, councillors expressed concern about increased flood risk as a result

of infill development. Staff discussed the strategies, standards and programmes

in place to manage stormwater in infill areas.

8.6.4 Recommendation for final policy: In

instances where developers provide stormwater infrastructure, a special

assessment will be done only when the demand on Council stormwater

infrastructure is less than half of the average assumed demand as detailed in

the policy.

8.6.5 An

additional provision is proposed to allow for a reduction in the stormwater

development contributions assessment for developments where stormwater

infrastructure is vested with the Council regardless of whether the mitigation

provided has reached the threshold for a special assessment. This is wording is

outlined in section 10 of this report.

Stormwater

discount for attached multi-unit developments

8.6.6 What

was consulted on: The draft

policy proposed the Council cease providing a stormwater discount for

developments with at least two attached multi-units on this basis that the ISA

averages built into the policy already takes into account smaller residential

units and changing development patterns.

8.6.7 All base unit demand assumptions have been updated as part of this

review. Average ISA per site (parcel) has been reduced from 427m2 to

367m2 as a result. This reflects the changing development patterns

and increased intensification.

8.6.8 A special assessment would still be triggered if the threshold is

met in line with the special assessment provisions of the policy.

8.6.9 Feedback from submitters: Ten submitters

commented on the proposal to remove the multi-unit adjustment for stormwater.

Submitters presented mixed views - two supported the change, five opposed it

and three expressed a mixed view.

8.6.10 Workshop discussion: At the 19 May

workshop, councillors expressed concern about increased flood risk as a result

of infill development and questioned whether there should be any discounts

provided for multi-unit developments.

8.6.11 Staff advice in workshop: Staff noted

that under the broader principles of the policy, the Council would still need

to provide some kind of actual demand assessment for developments where actual

ISA was less than half of the ISA assumptions built into the policy. Staff

suggested a compromise would be to change the provision so that if the special

assessment threshold is met, multi-unit developments will be assessed as though

the entire site is impervious (as opposed to using the ISA stated on the

plans).

8.6.12 Recommendation for final policy: The

assessment for the stormwater activity will be undertaken using the HUE

multipliers outlined in paragraph 7.4 of this report. If the assessment results

in assumed demand (ISA) that is more than double the area of the development

site, the development site will instead be assessed as though it is 100%

impervious. This is wording is outlined in section 10 of this report.

Remissions

8.7 What

was consulted on: The current policy includes a clause that provides for

the Council to remit some or all development contribution charges for a

development in “unique and compelling circumstances”. The original

intent of this clause was to allow for the Council to address a matter directly

associated with the development contributions charge. The clause is being used

more widely with developers appealing to the Council to remit development

contributions charges for a range of reasons including that the organisation

applying provides services to the community.

8.8 The

remission provision was removed from the draft policy.

8.9 An

alternative remission provision was also drafted and included in the

consultation material. The alternative clause clarified that it is the

development itself (not the developer or future occupier of the site) that must

be unique, and that the development must be sufficiently distinct from other

developments that remitting a development contribution requirement does not

create a new precedent.

8.10 Feedback from submitters: Thirteen

submitters commented on the removal of the remissions provision. There were

mixed views on removing remission clause with some submitters confusing

remissions and special assessments, and some confusing remissions and

rebates. Submitters did not express a preference for one remission clause

over the other.

8.11 Staff advice in workshop: The term ‘remission’ is used differently by different

councils in their development contributions policies. The Council's policy uses

the term ‘remission’ to refer to the Council intervening on a

development contributions assessment when there is something about the

development that has not been considered in drafting the policy and therefore

the Council considers it necessary to address an aspect of the assessment via a

remission.

8.12 However,

many councils use the term 'remission' to refer to an actual demand remission -

where demand is materially different to the assumed demand built into the

policy. The Council's policy refers to this as a special assessment.

8.13 There

is no proposal to remove the ability for developers to seek a special

assessment (or actual demand assessment) provided that the threshold is met (of

actual demand being half assumed demand).

8.14 Noting

the feedback received on remissions, more generally, staff proposed the Council

adopt the inclusion of the alternative remission clause.

8.15 Workshop discussion: At the 19 May 2025

workshop, councillors provided no further guidance on the proposal to use the

alternative remission clause.

8.16 Recommendation for final policy: The

alternative remission clause be included in the policy. This is wording is outlined in section 10 of this report.

Life of existing demand credits

8.17 What

was consulted on: The Council position has been to limit the life of

existing use credits to ten years from when the site last exerted demand on

Council infrastructure. Many credits have expired in the last four years on

buildings and sites of former buildings damaged in the 2010/11 earthquakes

– particularly in the central city. This issue was reconsidered as part

of this review and the policy retained the ten-year life of existing demand

credits.

8.18 Feedback from submitters: Ten submitters

commented on the life of existing demand credits. Eight submitters asked that

the life of credits clause be extended either to 20 years or indefinitely. Two

submitters supported retention of the current provision.

8.19 Staff advice in workshop: There

is no explicit requirement under the LGA to provide existing demand credits.

The purpose of existing demand credits is to recognise that development may not

result in additional demand on infrastructure. Therefore, only net additional

demand attracts a development contribution requirement.

8.20 The Council

provides credits to assess for net additional demand, promote equity and

encourage timely redevelopment.

8.21 The LGA requires

the Council to manage its infrastructure assets in a way that promotes prudent

stewardship and efficient and effective use of assets. Providing existing

demand credits requires the Council to effectively “reserve”

infrastructure capacity and guarantee infrastructure capacity for the life of

the credits. This creates increased risk for Council the longer the credit is

in place but unused.

8.22 Managing

that risk would require the Council to operate its infrastructure in such a way

as to always carry capacity sufficient to honour the credits. This means

infrastructure would need to have a high level of unused capacity sitting

waiting for redevelopment to again take up capacity once used at some point in

the past. This is not an efficient or prudent way to manage infrastructure and

will result in other ratepayers carrying the cost of having that capacity

available.

8.23 The

current policy setting, where existing demand credits expire after ten years

strikes a balance between managing infrastructure capacity wisely, being fair

to ratepayers in that a liability to provide infrastructure to service these

lots is not in place forever and being fair to developers in recognising that

development has occurred on a site previously.

8.24 Workshop discussion: At the 19 May 2025

workshop, a question was asked about the rationale to limit the life of

existing demand credits and what approaches were taken by other councils.

Staff advised that other councils have taken a range of approaches from

providing no existing demand credits through to providing for credits to have a

perpetual life.

8.25 Staff

also noted that walking back a change to existing demand credits would be very

difficult and advised that a rebate scheme would be a sensible way to deal with

central city sites. Work on a rebate for existing demand credits is being

progressed separately.

8.26 Recommendation for final policy:

Existing demand credits expire 10 years after a site last exerts demand on

Council infrastructure.

Fee for development contributions assessments

8.27 What

was consulted on: The draft policy included a provision for the Council to charge a fee for development

contributions assessments.

8.28 Feedback from submitters: Submitters

presented mixed views on the Council charging a fee for development

contributions assessments. Seven submitters were opposed, although several

submitters appear to be mistaking the fee for the Development Contributions

Team to complete an assessment with development contributions charges. Six were

supportive of the proposal.

8.29 Staff advice in workshop: The proposed

fee for development contributions assessments is a one-off, flat fee charged at

invoicing. It was included in the draft Annual Plan 2025/26 fees and charges

and is $100 including GST.

8.30 The fee remains the same regardless of how many times a developer or

their agent contacts the Development Contributions Team or whether the

assessment is amended or revised. The Development Contributions Team time

is not charged for as part of a building and/or resource consent application;

it is currently paid for by rates only.

8.31 It is fair that the cost of preparing a

development contributions assessment is funded by the developer because they

both benefit from the assessment of their development and cause the assessment

to be required through submitting their development for consent.

8.32 Workshop discussion: At the 19 May 2025

workshop, councillors provided no further guidance on the fee for

development contributions assessments as proposed.

8.33 Recommendation for final policy: At the time of invoicing, a fee to cover the cost for the Council to

administer the development contribution assessment will be invoiced alongside

the development contribution requirement. The development contribution

assessment fee is set out in the Council’s schedule of fees and charges.

HUE equivalences/multipliers

8.34 What

was consulted on: A range of changes have been made to the HUE equivalences

or HUE multipliers, most notably the policy reverts to using a land or

activity-based methodology for transport activities. The HUE equivalences cover

a range of land-use types and are outlined in Part 8 of the policy (Tables 4, 6

and 8).

8.35 Feedback from submitters: Three

submitters opposed the proposed HUE equivalences for residential units and care

suites in retirement villages. One submitter opposed the changes to

activity-based HUE multipliers. Another submitter requested all non-residential

assessments be conducted as actual demand assessments.

8.36 Staff advice in workshop: The retirement

village HUE equivalences are based on stated average occupancy of 1.3 in a unit

in an objection to the Council in addition to the Ryman objection

decision. Staff have previously completed a survey of

all retirement villages and confirmed the average water use was accurate and

are therefore comfortable with this HUE equivalence.

8.37 It

was also noted the retirement village community facilities are not assessed for

development contributions and these facilities are assessed as ancillary to the

residential spaces.

8.38 Staff agreed with submitters that residential units in retirement

villages could be assessed at 0.1 HUE for the reserves activity.

8.39 Workshop discussion: At the 19 May 2025 workshop, staff were asked why industrial, and

warehousing and logistics development types were separated in the policy. Staff

advised the decision was made to separate the industrial and

warehousing/logistics categories, recognising the growth in warehouse-based

activities and the differing demands these sectors place on land use and

Council services.

8.40 Recommendation for final policy:

Residential units to be assessed at 0.1 HUE for the reserves activity. Several

clarifications are recommended for Table 4 of the policy; these are outlined in

section 10 of the report. No other changes recommended for the HUE equivalence

or land-use types.

Active Travel and Public Transport catchments

8.41 What

was consulted on: No changes were proposed to the Active Travel and Public

Transport catchments between the current and draft policies.

8.42 Feedback from submitters: One submitter requested the public transport catchment be amended

to include Marshland Road. One submitter requested that Templeton be included

in the active travel catchment.

8.43 One

submitter felt that Lyttleton should be excluded from active travel.

8.44 Workshop discussion: At the 19 May workshop, councillors asked why Marshlands Road was

excluded from the Active Travel catchment and why Templeton was not part of the

Public Transport catchment.

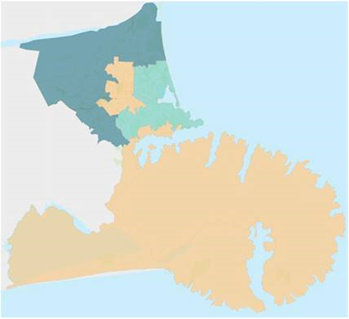

8.45 Recommendation for final policy: Staff have made small changes to the Active Travel and Public

Transport catchments to reflect submitter and elected member feedback. The

final catchment maps are included in Appendix 3 of the policy.

8.46 As

active travel includes footpaths and cycleways, it is fair Lyttleton is

included in this catchment.

Development contributions charges

8.47 Feedback from submitters: Some developers submitted that the increase in charges may impact

the viability of developments and affordability of new homes.

8.48 Staff

advice: Development contributions is a cost recovery tool

for the growth component of projects that are in the Council’s capital

programme. Development contribution charges are calculated by dividing cost to

the growth component of an asset by projected growth.

8.49 The overall capital programme increased from $5.78B in 2021 to

$6.51B in 2024. The

cost of the growth component of those projects also increased

– from $730M in 2021 to $923M in 2024.

8.50 The

2024 growth forecast has a slower rate of growth in all aspects compared to

2021 (an average 0.52% per annum over 30 years compared to 2.06% in 2021). Growth projections that informed the 2021 policy were significantly

higher than in the previous policies due to post-earthquake population shifts

and changes in the district. Statistics New Zealand’s projections that

have informed the 2025 policy reflect the ‘return to normal’ growth

patterns in the district.

8.51 The increase in

growth capital expenditure, combined with slower growth projections compared to

the 2021 LTP, has resulted in development contributions charges that are higher

than in the 2021 policy. These charges are, however, in line with pre-2021 charges.

8.52 While the charges

in the 2025 policy have increased compared to the 2021 policy, the 2021 charges

were unusually low. If Council were to set development contributions lower than

what is contained in this policy this would require ratepayers

across the district to meet the cost of the foregone revenue.

8.53 Workshop discussion: At the 19 May 2025

workshop, councillors provided no feedback on the development contributions charges.

8.54 Recommendation for final policy:

Development contributions charges are outlined in Appendix 1 of the policy.

9. Submitter feedback on issues not discussed at workshop

Neighbourhood

Parks and Road Network catchments

9.1 What was consulted on: The policy

proposed to move the neighbourhood parks and road network catchments from a

concentric configuration to localised catchments.

9.2 Feedback from submitters: There was overall support for the move to localised

catchments, but some submitters requested that the catchments be made smaller.

9.3 Staff

advice: Smaller catchments increase the complexity of developing and

operating the policy and the range of per-HUE charges across those catchments

also tends to increase, which may have unintended consequences for funding

growth. Some small catchments may pay very high, targeted contributions, while

others may pay very low contributions, depending on how the catchments are

drawn.

9.4 Additionally,

the risk of under-recovering the cost of growth infrastructure increases with

smaller catchments especially if modelling has not allocated growth in the

correct places. Overall, the smaller the catchments, the greater the risk of

error in the policy. This risk is reflected in the number and size of the

catchments for these activities.

9.5 Recommendation for final policy: No

changes to Neighbourhood Parks and Road Network catchments

Three

Waters catchments

9.6 What was consulted on: The policy

proposed to move to fewer and larger catchments for the three waters

activities.

9.7 Feedback from submitters: There was mixed support for these

catchments, with two opposed, two supportive and one suggesting sub-catchments

may be required.

9.8 Staff

advice: Before 2021, water supply and wastewater

activities were grouped into a district-wide catchment. The 2025 policy

proposes to return to larger catchments for these activities to address several

issues.

9.8.1 Nature

of water infrastructure in the district: The Council has a unique

integrated water network which isn’t necessarily reflected in our current

catchments. The new catchments better reflect the Council’s

integrated delivery of water services. Additionally, infrastructure within the

urban catchment is interconnected within the city and three waters projects

generally benefit the related wider infrastructure network.

9.8.2 Unpredictable

growth and need to be responsive: The Council’s capital spending

for growth-related three waters infrastructure will need to become more

dynamic, reacting to patterns of intensification. Around two-thirds of all new

residential development is occurring in infill areas, and it is likely this

trend will continue. There is a lack of certainty with respect to where that

growth is going to occur

9.8.3 Whilst

three waters infrastructure plans consider growth for the next 50 years, LTP

growth funding is allocated 10 years in advance with specific projects

identified every three years. Development contributions based on smaller

catchments may cause under collection for growth provision not yet ring-fenced

in the LTP. Furthermore, because infrastructure plans are not fully

aligned with the LTP funding period, there may be misalignment when LTP

provision has not yet been made for development triggering upgrades. A

grouped catchment will ensure that development contributions are collected from

all new development on a fair and equitable basis.

9.9 Recommendation for final policy: No

changes to Three Waters catchments

Pause review

9.10 Feedback from submitters: A number of submitters suggested the Council pause the review the of

the Development Contributions Policy with some submitters stating development

levies would be coming in in September 2025 and implying the draft policy, if

adopted, would only be in effect for a few months. This is not correct. The

Government has indicated legislation will be introduced in September 2025 and

will be enacted by mid-2026. Levies will come into effect from mid-2027.

9.11 Staff

advice: Until new legislation is enacted, councils have a

legislative requirement to have a policy on development contributions and to

review it every three years. The Council’s current Development

Contributions Policy was adopted in July 2021, and it is due for review.

9.12 The

current policy does not reflect the Council’s actual costs to deliver

growth infrastructure. Developers are currently paying development

contributions based on significantly outdated costs and are not contributing

towards additional projects approved in the 2024 LTP. As development

contributions are a one-off payment and councils cannot require other

developers to pay for infrastructure capacity that has been taken up by a

development that has not paid for it, the difference in revenue becomes

ratepayer funded.

9.13 Recommendation for review: Staff do not recommend the

policy review be paused.

Other comments made during hearing of

submissions

Accuracy

of technical inputs

9.14 During

the hearing of submissions, some submitters questioned the accuracy of the cost

allocations/capital programme.

Growth

projections

9.14.1 The

growth inputs for the policy are based on the Statistics New Zealand medium

population and household growth scenarios. This is consistent with past

development contributions policies. Christchurch has historically tracked very

closely to the medium projections, and they remain a good indication of future

growth.

9.14.2 The

Council’s growth models are used to distribute future growth to a

sub-city level. These models are all connected and talk to each other, to tell

a consistent growth story. The growth models have been peer-reviewed by

external agencies and have been found to be fit for purpose

9.14.3 The

models consider both intensification and greenfield development. The capacity

inputs into the model include a picture of both infill and greenfield capacity.

Cost

allocations for capital projects

9.14.4 The cost allocation process, which identifies the growth component

of each asset is outlined in Part 6 of the draft policy. Council staff review

each capital project and determine the allocation of cost drivers: renewal,

backlog, increase in current level of service or growth. Only the cost of

infrastructure to service growth is funded from development contributions. The

cost allocation methodology takes account of causation (the reason the asset is

being provided), as well as who benefits from the project. The methodology to

determine the exact allocation between the cost drivers varies between the

activities.

9.14.5 The capital programme, and the projects to be delivered for which

the Council collects development contributions, has been informed by the 2024

growth model. The cost allocations for projects not yet delivered, therefore,

reflect projected growth. Projects that have already been delivered (that is,

are noted as 'complete' in the Schedule of Assets) remain unchanged.

Trigger to

assess for development contributions

9.15 One

submitter commented that the Council has an incorrect trigger to assess for

development contributions in the draft policy.

9.16 Section

198(2A) of the LGA requires councils assess for development contributions under

the policy in force at the time the consent/authorisation application was

submitted, accompanied by all required information. Section 4.1.3

confirms the Council will assess using the policy in force at the time the

complete application for consent is received.

9.17 The

developer will be formally notified of their development contribution

requirement as part of the granting of the consent application.

10. Incorporation of feedback into the draft policy

10.1 The consultation and hearing

process allowed submitters to share their insights, comments and suggestions

with the Council about the policy proposals. As a result of these

considerations, staff have incorporated the following items into the draft

policy:

10.1.1 Clause

3.2.4 (4): “The development provides infrastructure to be vested

with the Council, which reduces the impact of the development’s demand on

Council stormwater infrastructure, prior to discharge into the Council

network”.

10.1.2 Clause

3.2.5: “Residential units in retirement villages and care

suites are assessed for development contributions as set out in Table 4”.

10.1.3 Clause 5.6: “The Council

considers that there may be a development that is so unique it has not been

anticipated by the policy, so much so that the Council considers the full

development contribution assessment to be unfair and unable to be remedied

under the provision of a special assessment.

The development, itself, must be

sufficiently distinct from other developments that remitting a development

contribution requirement would not create a new precedent in terms of the

Council’s current interpretation and application of the policy.

In these cases, the Council may, at

its sole discretion, consider and grant a full or partial remission of

development contributions in cases where it is satisfied this threshold has

been met.

The developer must write to the Chief

Executive seeking a remission and explaining how the development has met this

threshold and why the Council should grant a full or partial remission in the

interest of fairness. The explanation must be specific to the development (not

the developer or intended future occupier) and the features of the development

that make it unique”.

10.1.4 Table

4: Footnote: “Community facilities within a retirement village for

the predominant use of residents and their guests are not subject to a

development contribution requirement”.

10.1.5 Table

4: 0.1 HUE reserve assessment for retirement units.

10.1.6 Table

4: Care suites are not charged for the community infrastructure

activity.

10.2 At

the 19 May 2025 workshop, elected members expressed concern about providing

discounts for attached multi-unit developments, citing the importance of

stormwater infrastructure in managing the impact of increased intensification

in infill areas. The following has been added to the draft policy:

10.2.1 3.2.2.5:

“Developments of two or more attached residential units on a single

lot will be assessed for the stormwater and flood protection based on the HUE

rates outlined in section 3.2.1 and 3.2.2. If assessed HUEs result in ISA that

is more than double the area of the development site, the development site will

instead be assessed as though it is 100% impervious”.

10.3 On

review of the final draft policy, staff considered the wording of 3.2.4 could

be amended to better reflect the description of the tables contained in Part 8

of the policy.

10.3.1 Clause

3.2.4: Where a development is not consistent with the land use or

business type as detailed in Part 8 of the policy the Council may require a

special assessment for development contributions for the activities considered

to be outside the expected demand. Situations where this may be required

include:

1. Where

the type of development proposed is not adequately covered by Tables 4, 6 and

8.

2. Where

the demand for an activity from the development is expected to be more than

double the value identified as average for that type of development as set out

in Tables 4, 6 and 8.

……

A developer may ask the Council to consider

undertaking a special assessment if:

The

development is expected to place less than half the assumed demand on

infrastructure for the value identified as average for that type of development

as set out in Tables 4, 6 and 8.

11. Transitional provision

11.1 Staff

note the policy may result in lower development contributions charges for some

Akaroa Harbour developments compared to the 2021 policy. Charges for Akaroa

Harbour under the 2021 policy are $68,189.73 including GST compared to

$44,083.25 including GST under the 2025 policy.

11.2 Section

198 (2A) of the LGA requires the Council to undertake its assessment of

development contribution requirement under the development contributions policy

in place at the time it receives a complete application for resource consent,

building consent or authorisation to connect to Council infrastructure.

11.3 Given

the difference in the development contributions requirements in Akaroa between

the two policies, there is risk that developers may surrender consents and then

reapply for consent to trigger a new development contribution assessment under

the 2025 policy. This is an inefficient use of Council consenting resources.

11.4 Clause

4.1.5 of the policy provides for a remission of the difference in cost between

a development contributions assessment undertaken under a previous policy and

the 2025 policy where the charge is less under the 2025 policy. A remission is

only available where the developer could lawfully surrender a resource consent

or building consent and reapply for consent and thereby trigger a requirement

for a new development contribution assessment under the 2025 policy.

11.5 The

development would still be assessed under the provisions of the relevant policy

in accordance with section 198(2A) of the LGA, it would just receive the

benefit of the lower per-HUE charge.

12. Options Considered Ngā

Kōwhiringa Whaiwhakaaro

12.1 The

following reasonably practicable options were considered and are assessed in

this report:

12.1.1 Adopt

the draft policy.

12.1.2 Decline

to adopt the policy.

Options Descriptions Ngā Kōwhiringa

12.2 Preferred

Option: Adopt the draft policy.

12.2.1 Option

Description: The Council would resolve to adopt the draft policy.

12.2.2 Option

Advantages

· Complies with

legislative requirements and ensures development contributions charges

accurately reflect current capital costs required to service growth

development. It also provides an opportunity to make updates to the policy

provisions.

12.2.3 Option

Disadvantages

· Charges would

increase for most development types under the new charges. However, these new

charges accurately reflect the cost to Council to service growth

infrastructure.

12.3 Decline

to adopt the policy.

12.3.1 Option

Description: The Council would resolve to not adopt the draft policy and

direct staff to continue working on the review.

12.3.2 Option

Advantages

· This option

would benefit developers who would continue to be assessed for development

contributions under the 2021 policy, which contains significantly lower than

average charges.

12.3.3 Option

Disadvantages

· The 2021

development contributions charges do not accurately reflect the Council’s

current costs to service growth development. This option therefore

disadvantages ratepayers who would cover the difference between the

Council’s actual costs to provide growth infrastructure and the charges

developers are paying under the current policy.

· This does not

comply with the legislative requirement to review the policy every three years.

13. Financial Implications Ngā Hīraunga Rauemi

Capex/Opex Ngā Utu Whakahaere

13.1 Cost

to Implement – The cost of reviewing the policy and undertaking community

engagement is funded through existing operational budgets. This work has been

undertaken over more than one year and is funded as a general cost of business

rather than a discrete cost attributed to the project.

13.2 Maintenance/Ongoing

costs - Annual policy and administration costs vary depending on the policy

work required and the level of development needing to be assessed.

13.3 Funding

Source – The cost of preparing and administering the policy comes from

the general rate. The policy proposes to charge an administration fee at

invoicing stage to cover some of the costs associated with administering this

policy. In the previous 12 months, 900 development contributions invoices were

issued, so the anticipated revenue associated with this fee is around $90,000.

14. Considerations Ngā Whai Whakaaro

Risks and Mitigations Ngā Mōrearea me

ngā Whakamātautau

14.1 Development

contributions can be a litigious area of local government activity often with

significant financial implications for developers and councils. Because of this

there is a significant body of case law regarding what can and cannot be done

under the provisions of a development contributions policy.

14.2 As

with any decision made by the Council, there is a risk of judicial review. The

policy (or parts of it) could be quashed by the High Court if the policy is

challenged and the Court finds the decisions made relating to the policy are

unlawful or procedurally unfair. This is a risk of any decision made by

Council, but one that can be minimised as much as possible by ensuring that the

policy has been through a stringent review process and that the Council adheres

to an appropriate and fair consultation process.

14.3 The

Council’s Legal Services Team has provided advice throughout the policy

development process including full review of the proposed policy to ensure the

review and resulting policy reflect legislative requirements.

Legal Considerations Ngā Hīraunga

ā-Ture

14.4 Statutory

and/or delegated authority to undertake proposals in the report:

14.4.1 Section

102 of the LGA requires all local authorities to have a policy on development

contributions and financial contributions.

14.4.2 The

policy must comply with the requirements of section 106 and sections 197AA to

211 of the LGA. Section 106(6) of the LGA requires the Council to review its

development contributions policy at least once every three years.

14.5 Other Legal Implications:

14.5.1 This

report and the policy have been reviewed and approved by the Council’s

Legal Services Team.

Strategy

and Policy Considerations Te

Whai Kaupapa here

14.6 The

required decisions:

14.6.1 Do

align with the Christchurch

City Council’s Strategic Framework, particularly the strategic

priorities to manage ratepayers' money wisely and actively balance

the needs of today's residents with the needs of future generations.

14.6.2 Are

assessed as medium significance based on the Christchurch City Council’s

Significance and Engagement Policy. The level of significance was

determined by importance of the policy to the wider community who are largely

unaffected (low significance) and to property developers of Christchurch

district (medium significance) who are directly affected through the

requirement to pay development contributions.

14.6.3 Are

consistent with Council’s Plans and Policies. In particular the decisions

support the Council’s approach to funding the provision of infrastructure

to service growth development outlined in the Council’s Revenue and

Financing Policy.

14.7 This

report supports the Council's

Long Term Plan (2024 - 2034):

14.8 Strategic Planning and Policy

14.8.1 Activity: Strategic Policy and Resilience

· Level of Service: 17.0.1.2 Advice meets emerging needs and

statutory requirements, and is aligned with governance expectations in the

Strategic Framework - Carry out policy reviews in accordance with Unit work

programme and provide advice to meet emerging needs and statutory requirements

Community

Impacts and Views Ngā Mariu ā-Hāpori

14.9 Consultation

on the draft policy was undertaken in in accordance with sections 82 and 82A of

the LGA. Consultation and submitter feedback is outlined in section 6 of this

report.

14.10 The

decision affects all wards/Community Board areas.

Impact

on Mana Whenua Ngā

Whai Take Mana Whenua

14.11 The decisions

in this report do not involve a significant decision in relation to

ancestral land or a body of water or other elements of intrinsic value,

therefore this decision does not specifically impact Mana Whenua,

their culture, and traditions.

14.12 The

decision is not a matter of interest to Mana Whenua and will

not impact on our agreed partnership priorities with Ngā

Papatipu Rūnanga.

14.13 This is a

funding policy. The Council had a development contributions rebate scheme

for Papakāinga/Kāinga Nohoanga developments, but the rebate

scheme sits outside the scope of this policy.

Climate

Change Impact Considerations Ngā Whai Whakaaro mā te Āhuarangi

14.15 The proposals in this report

are unlikely to contribute significantly to adaptation to the impacts of

climate change or emissions reductions.

14.16 The policy details

how the Council will fund infrastructure to service growth development. Climate

change considerations are dealt with outside the scope of this policy.

15. Next Steps Ngā Mahinga ā-muri

15.1 If

adopted by the Council, the policy will come into effect from 1 July 2025.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a

|

Draft

Development Contributions Policy 2025 (Under Separate Cover)

|

25/1145731

|

|

|

b

|

Draft

Development Contributions Policy 2025 (with track changes) (Under Separate

Cover)

|

25/1145732

|

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Ellen Cavanagh

- Senior Policy Analyst

Hannah

Ballantyne - Senior Engagement Advisor

Andrew

Campbell - Legal Counsel

|

|

Approved By

|

David

Griffiths - Head of Strategic Policy & Resilience

John Higgins -

General Manager Strategy, Planning & Regulatory Services

|

|

4. Annual Plan 2025/26

|

|

Reference Te Tohutoro:

|

25/245303

|

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning and Performance

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to present to the Council for its consideration and

adoption:

1.1.1 An

analysis of the submissions and hearings made through the 2025/26 Annual Plan

consultation process;

1.1.2 The

outcome of the Council’s considerations to date before it adopts its

Annual Plan 2025/26; and

1.1.3 The

Annual Plan 2025/26, including any attached documents.

1.2 The

Council is required to prepare and adopt an Annual Plan for each financial year

(s.95(1)) Local Government Act 2002 (LGA)). The purpose of the plan is to:

1.2.1 provide

integrated decision-making and co-ordination of the Council’s resources;

and contribute to the accountability of the Council to the community;

1.2.2 identify

any variation from the financial statements and funding impact statement in the

Council’s Long Term Plan for 2025/26;

1.2.3 contain

the annual budget and funding impact statement for 2025/26.

1.3 The

decisions in this report are of high significance in relation to the

Christchurch City Council’s Significance and Engagement Policy.

2. Officer Recommendations Ngā

Tūtohu

That the Council:

Noting provisions

and financial prudence

1. Receives the information in the Annual Plan 2025/26 Report and

the attachments to this report.

2. Notes that the decision in this report is

assessed as high significance based on the Christchurch City Council’s

Significance and Engagement Policy.

3. Notes the recommendations of the

Council’s Audit and Risk Management Committee at its meeting held on 13

June 2025, as set out in Attachment A of this report.

4. Notes the Thematic Analysis of the Annual Plan

2025/26 Submissions, set out in Attachment B of this report.

5. Notes the Annual Plan 2025/26 - Management

Sign-off for Process set out in Attachment C of this report; and

6. Notes the Annual Plan 2025/26 - Management

Sign-off for Significant Forecasting Assumptions set out in Attachment D

of this report.

7. Resolves that in accordance with section

100(2) of the Local Government Act 2002, it is financially prudent not to set

the Council’s projected operating revenues at a level sufficient to meet

the projected operating expenses in the 2025-26 financial year, having regard

to:

a. The ratio, which is forecast to be 96% in the

2025-26 year; and

b. The estimated expenses of achieving and

maintaining the predicted levels of service provision set out in the long-term

plan, including the estimated expenses associated with maintaining the service

capacity and integrity of the Council’s assets; and

c. The projected revenue available to fund the

estimated expenses associated with maintaining the service capacity and

integrity of the Council’s assets throughout their useful life; and

d. The equitable allocation of responsibility for

funding the provision and maintenance of the Council’s assets and

facilities; and

e. The Council's funding and financial policies.

Climate

Resilience Fund Policy

8. Adopts the Climate Resilience Fund Policy as

set out in Attachment K of this report.

9. Resolves to hold the Climate Resilience Fund

in accordance with the Investment Policy adopted by the Council with the

2024-2034 Long Term Plan.

Draft Annual

Plan – Adoption of Attachments

10. Adopts the summary of the financial, rates,

and benchmark impacts including proposed operational changes for 2025/26 set

out in Attachment E of this report.

11. Adopts the changes to the Council’s

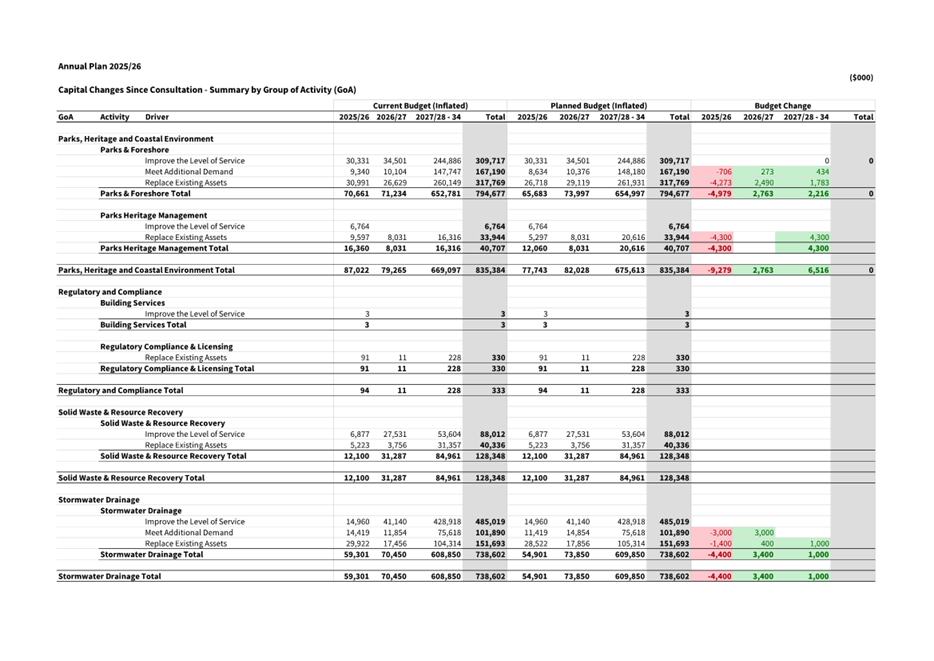

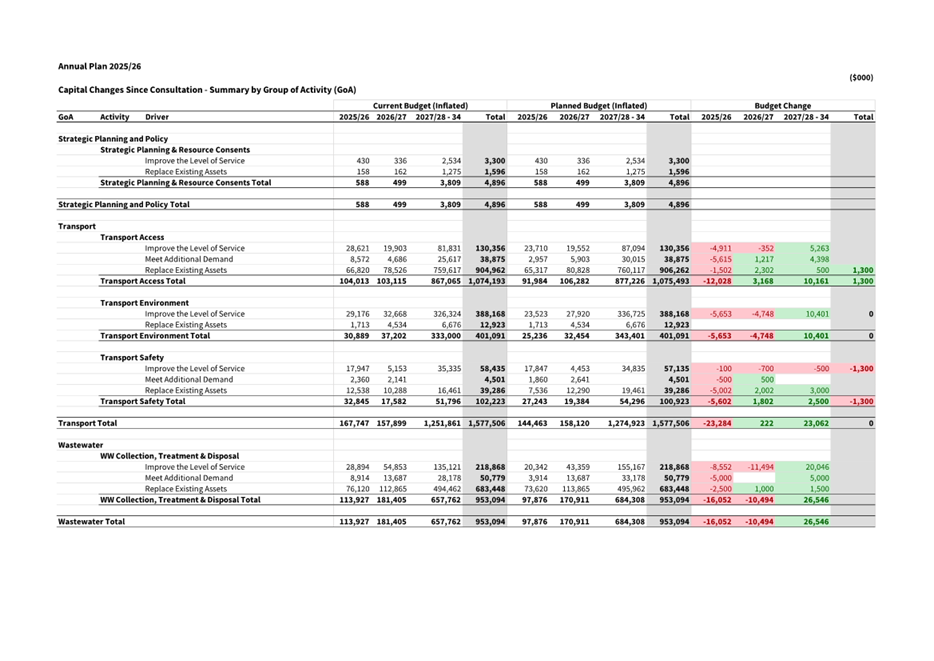

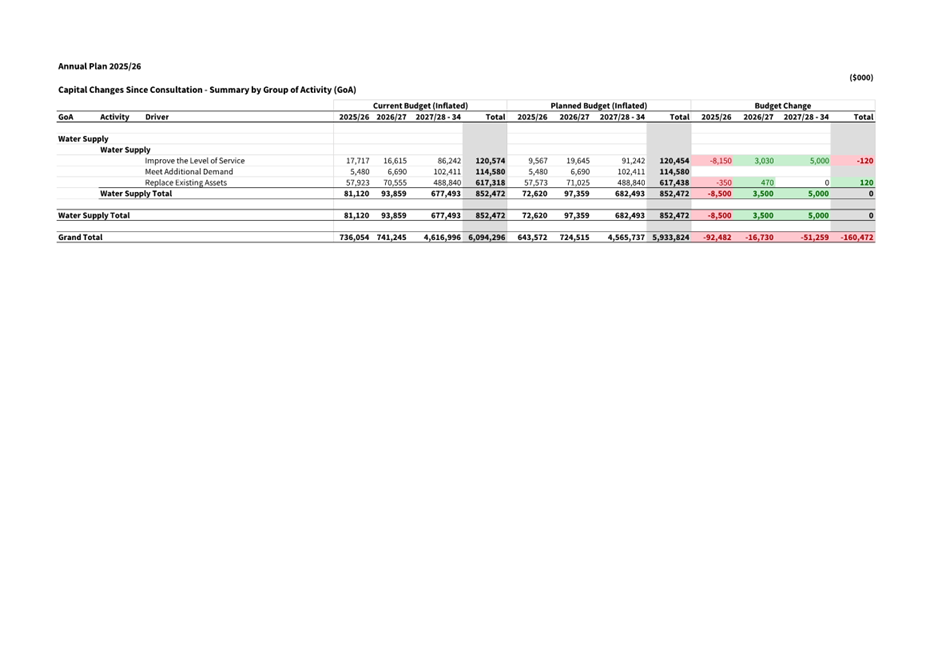

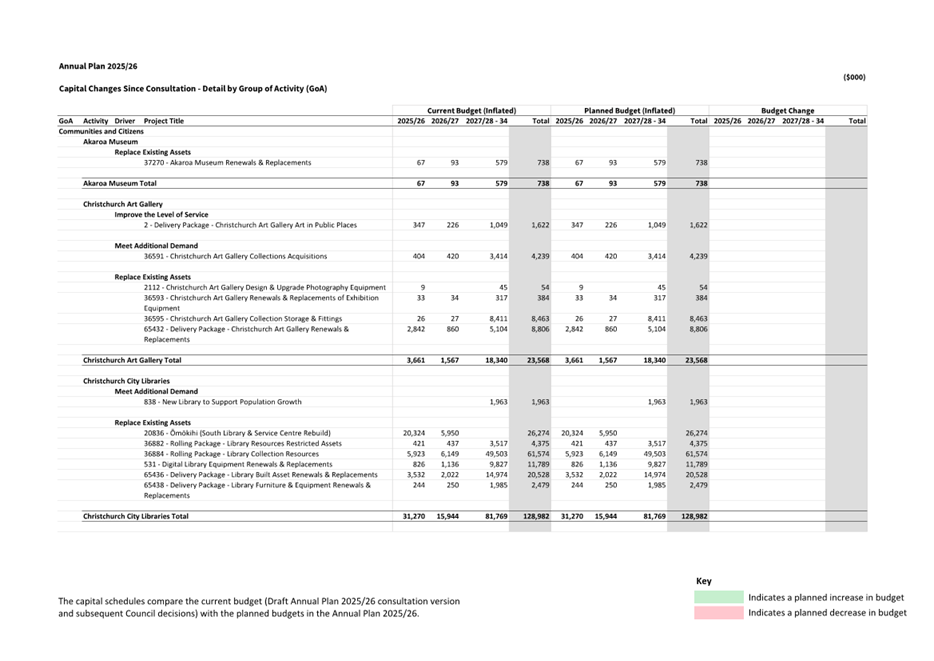

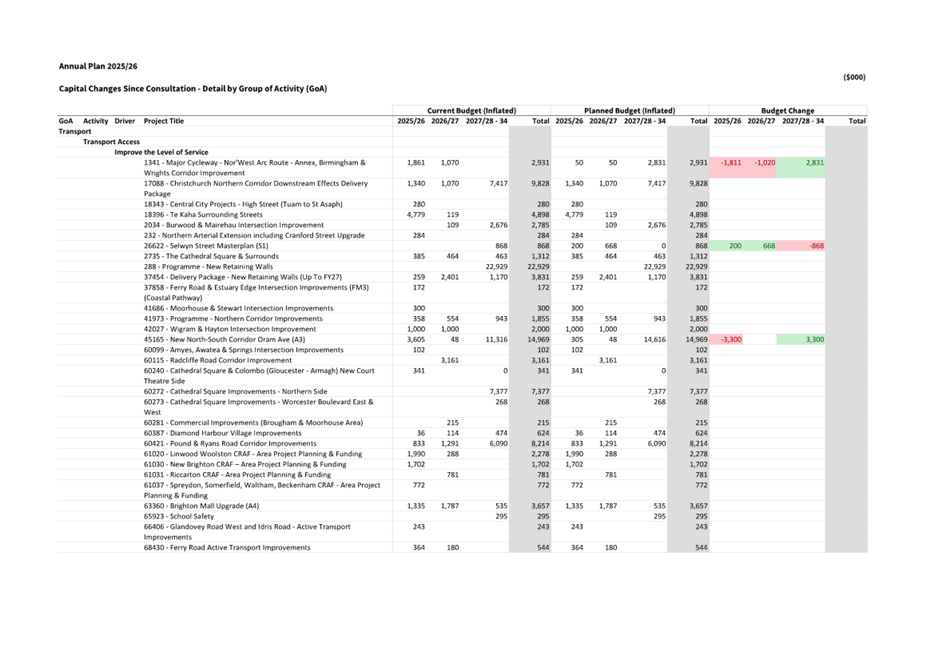

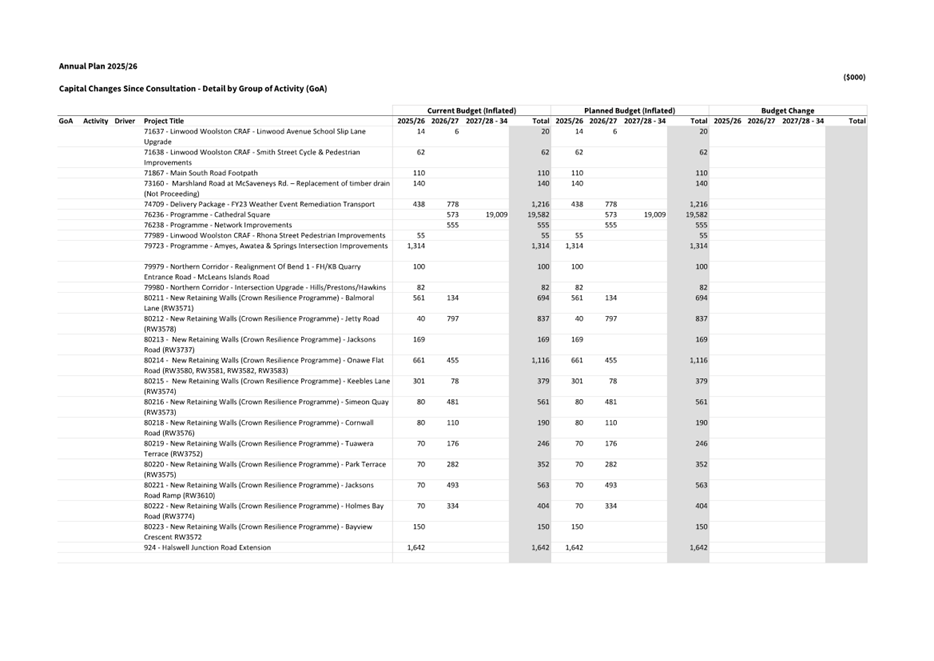

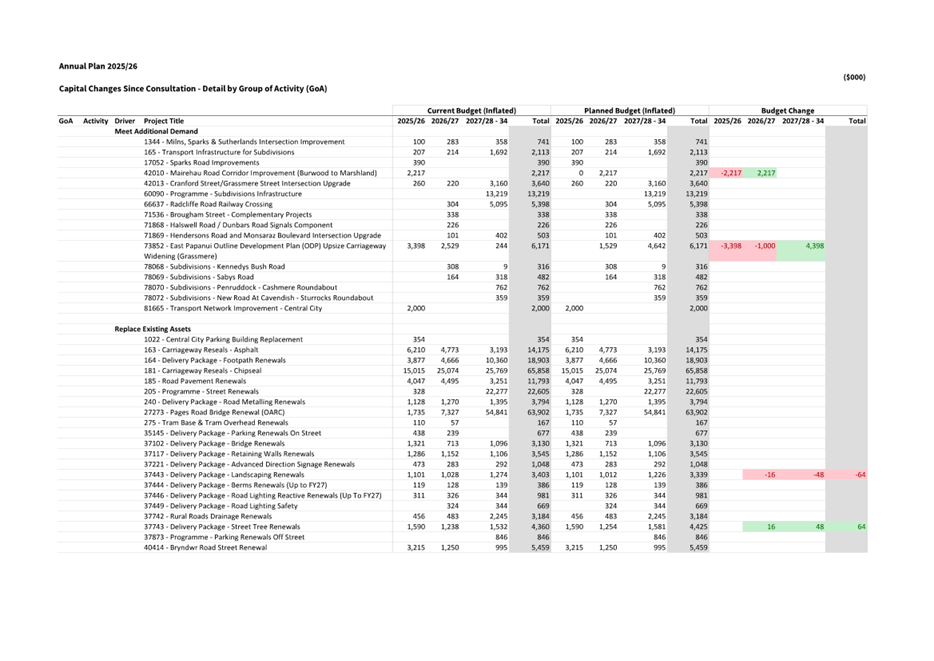

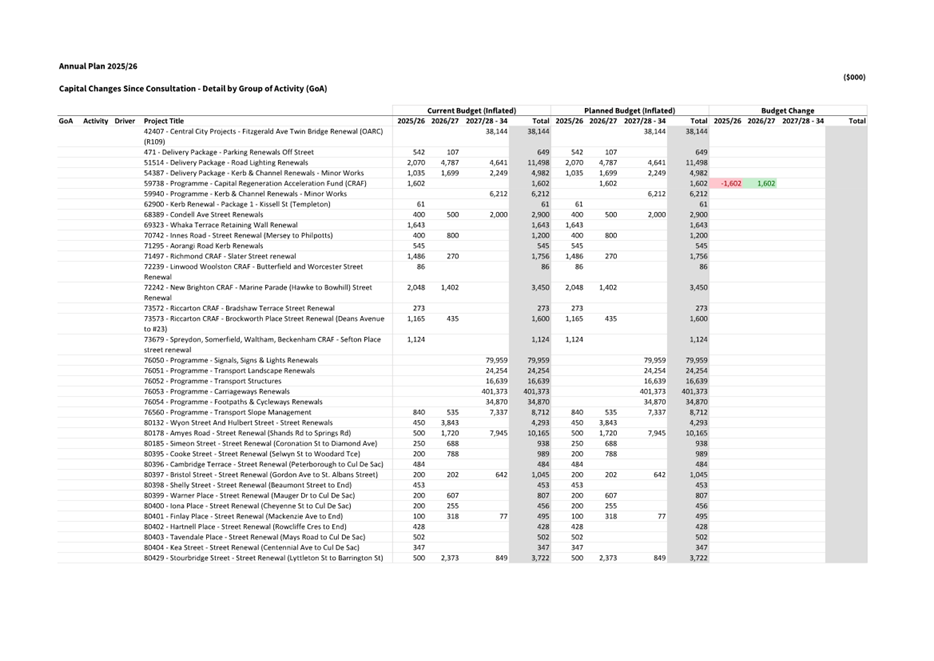

capital programme for 2025/26 set out in Attachment F of this report.

12. Adopts the proposed Funding Impact Statement

– Rating Information set out in Attachment G of this report.

13. Adopts a minor change to a level of service

identified since the publication of the draft Annual Plan 2025/26, set out in Attachment H of this report.

14. Adopts minor changes to the Fees and Charges

schedule identified since the publication of the draft Annual Plan 2025/26, set

out in Attachment I of this report.

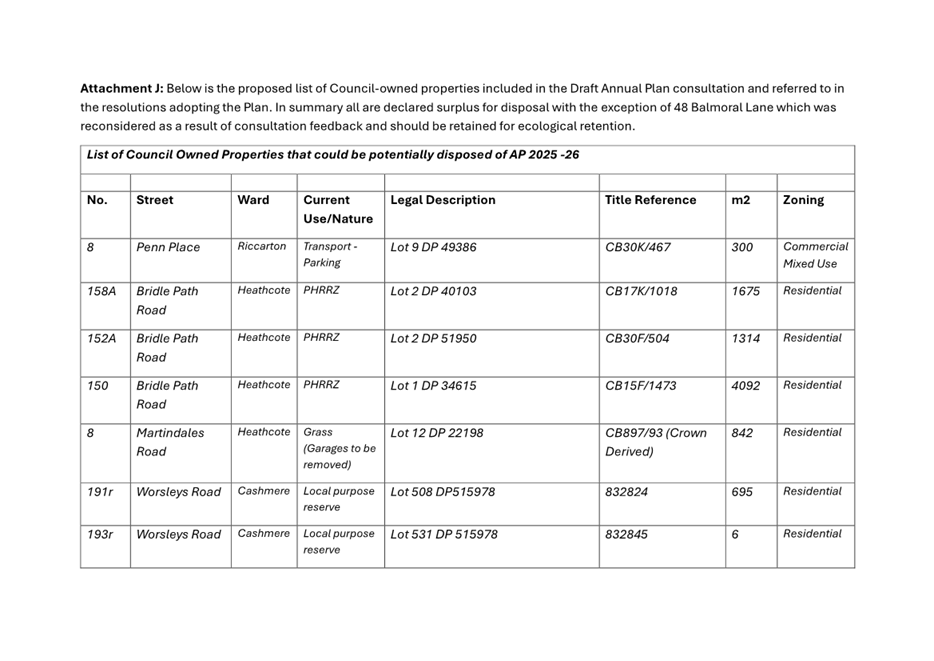

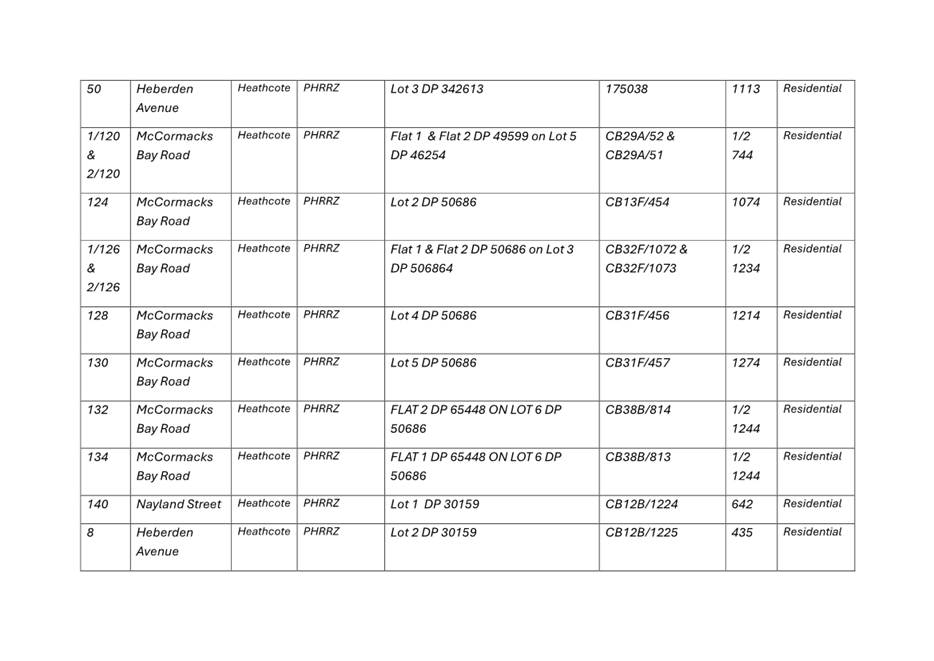

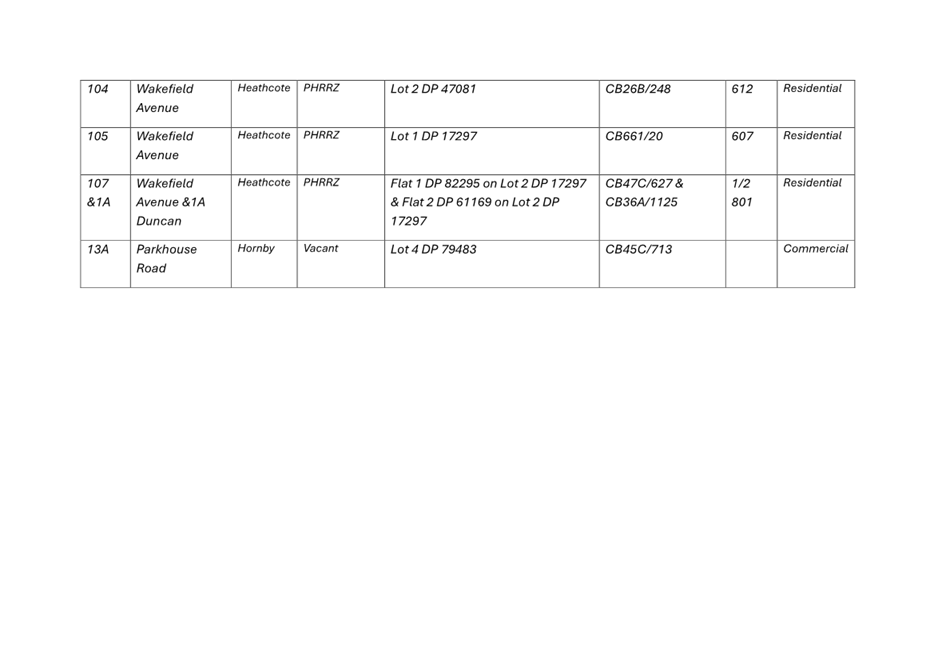

Disposal of Council-owned properties

15. Notes the following in respect of the disposal

of Council-owned properties consulted on as part of the 25/26 draft Annual Plan

process:

a. Separate advertising was undertaken to satisfy

the requirements of section 138 of the Local Government Act and section 24 of

the Reserves Act in respect of the following properties:

· 44 Canada Drive and Sir James Wattie Drive (no

title/street number) reserves subject to the Reserves Act 1977.

· 8 Penn Place and 38 Bexley Road considered to be a

‘Park’ pursuant to section 138 of the Local Government Act 2002.

· 8 Martindales Road, 191r Worsleys Road and 193r Worsleys

Road reserves subject to the Reserves Act 1977 and are also considered a

‘Park’ pursuant to section 138 Local

Government Act 2002 for disposal

purposes.

b. Advertising comprised public notices in the Press on 8

and 15 March 2025 for each property and publication on the

council main public notice page. Any resulting submissions have been

incorporated into the overall draft 2025/26 Annual Plan submissions (refer Attachment B of

this report, Thematic Analysis of Submissions) to

inform the Council’s decision.

c. Fair and reasonable consideration has been given to all

submissions/objections and all information in accordance with section 78 and

138 of the Local Government Act 2002 and section 24 of the Reserves Act 1977 to

inform the Council’s decision.

16. Resolves that all

of the properties on the list in the draft 2025/26 Annual Plan, except 48

Balmoral Lane, as set out in Attachment J of this report, do not meet

the Council’s retention criteria and are therefore declared surplus and

to be disposed of.

17. Resolves that 48 Balmoral Lane shall be

retained due to its ecological restoration potential.

18. Authorises that the reserve revocation process for the

following listed properties is commenced in accordance with the Reserves Act

1977:

a. 44 Canada Drive and Sir James Wattie Drive (no

title).

b. 8 Martindales Road.

c. 191r Worsleys Road.

d. 193r Worsleys Road.

19. Authorises the Manager

Property Consultancy to implement

resolutions 15-18 above and in doing so make any reasonable decisions necessary

at their sole discretion to effect the sale of these properties in accordance

with Council normal practises and Policies and subject to applicable

legislation.

Draft Annual

Plan - Adoption

20. Adopts the Annual Plan 2025/26 comprising the

information and underlying documents adopted by the Council at the meeting

dated 12 February 2025 (the draft Annual Plan 2025/26), as amended by

resolutions 10 to 19 above and Attachments E-I and K of this report and

including any carried amendments made at this meeting.

Draft Annual

Plan – Authorisations and setting the rates

21. Authorises the General Manager Finance, Risk

& Performance/Chief Financial Officer to make the amendments required to

ensure the published 2025/26 Annual Plan aligns with the Council’s

resolutions of 24 June 2025 and to make any other minor changes that may be

required.

22. Authorises the Chief Executive to borrow, in

accordance with the Liability Management Policy, sufficient funds to enable the

Council to meet its funding requirements as set out in the 2025/26 Annual Plan.

23. Having set out rates information in the

Funding Impact Statement – Rating Information contained in the Annual

Plan 2025/26 (adopted as Attachment G by the above resolutions),

resolves to set the following rates under the Local Government (Rating) Act

2002 for the 2025/26 financial year, commencing on 1 July 2025 and ending on 30

June 2026 (all statutory references are to the Local Government (Rating) Act

2002).

a. A uniform annual general charge under section 15(1)(b) of $193.00 (incl. GST) per

separately used or inhabited part of a rating unit;

b. a general rate under sections 13(2)(b)

and 13(3)(a)(ii) set differentially based on property type, and capital value

as follows:

|

Differential Category

|

Basis for Liability

|

Rate Factor (incl. GST) (cents/$ of capital value)

|

|

Standard

|

Capital Value

|

0.256336

|

|

Business

|

Capital Value

|

0.569065

|

|

City Vacant

|

Capital Value

|

1.159406

|

|

Remote Rural

|

Capital Value

|

0.192252

|

c. a sewerage targeted rate under sections

16(3)(b) and 16(4)(a) on all rating units in the serviced area of 0.088232

cents per dollar of capital value (incl. GST);

d. a land drainage targeted rate under

sections 16(3)(b) and 16(4)(a) on all rating units in the serviced area of

0.045166 cents per dollar of capital value (incl. GST);

e. a water supply targeted rate under

section 16(3)(b) and 16(4)(b) set differentially depending on whether a

property is connected or capable of connection to the on-demand water

reticulation system, as follows:

|

Differential Category

|

Basis for Liability

|

Rate Factor (incl. GST) (cents/$ of capital value)

|

|

Connected (full charge)

|

Capital Value

|

0.073750

|

|

Serviceable (half charge)

|

Capital Value

|

0.036875

|

f. a restricted water supply targeted rate

under sections 16(3)(b) and 16(4)(a) on all rating units with one or more

connections to restricted water supply systems of $406.00

(incl. GST) for each standard level of service received by a rating unit;

g. a water supply fire connection targeted rate under sections 16(3)(b) and 16(4)(a) on all

rating units receiving the benefit of a water supply fire connection of $135.00

(incl. GST) per connection;

h. an excess water supply commercial targeted

rate under section 19(2)(a) set for all rating units which receive a

commercial water supply as defined in the Water Supply, Wastewater and

Stormwater Bylaw 2022 plus boarding houses, motels, and rest

homes, of $1.47 (incl. GST) per m3 or any part of a m3 for consumption in excess of the rating unit’s

water supply targeted rate daily allowance:

· where the rating unit’s water supply

targeted rate daily allowance is an amount of cubic meters per day, calculated

as the total amount payable under the water supply targeted rate (above),

divided by the cubic meter cost ($1.47), divided by 365;

· provided that all properties will be entitled to a minimum consumption

of 0.6986 cubic metres per day.

i. an excess water supply residential

targeted rate under section 19(2)(a) set for the following:

· all metered residential rating units where the

meter records usage for a single rating unit;

· a rating unit where the meter records usage

for multiple rating units where there is a special agreement in force

specifying which rating unit / ratepayer is responsible for payment,

of $1.47 (incl.

GST) per m3 or any part of a m3 for consumption in excess

of 900 litres per day, per separately used or inhabited part of the rating

unit;

j. a waste minimisation targeted rate under

sections 16(3)(b) and 16(4)(b) set differentially depending on whether a full

or partial service is provided, as follows:

|

Differential Category

|

Basis for Liability

|

Rate Factor (incl. GST)

|

|

Full service

|

Per separately used or inhabited part of a rating unit

|

$176.49

|

|

Partial service

|

Per separately used or inhabited part of a rating unit

|

$132.36

|

k. an active travel targeted rate under

section 16(3)(a) and 16(4)(a) of $20.00 (incl. GST) per separately used or

inhabited part of a rating unit;

l. a special heritage (Arts Centre)

targeted rate under section 16(3)(a) and 16(4)(a) of 0.000277

cents per dollar of capital value (incl. GST);

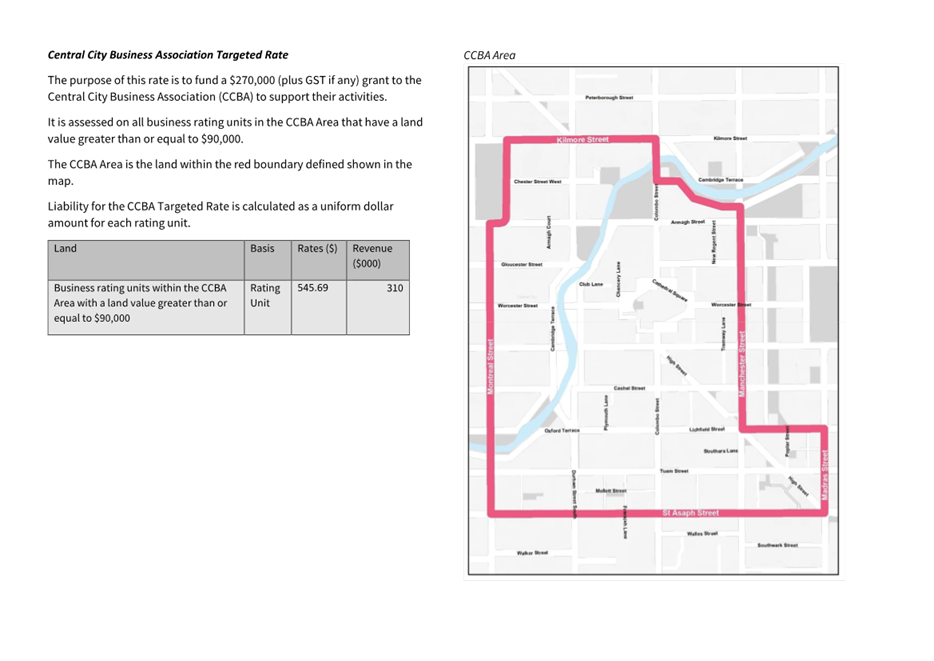

m. a Central City Business Association

targeted rate under section 16(3)(b) and 16(4)(a) of $545.69 (incl.

GST) per business rating unit in the Central City Business Association Area,