Finance and

Performance Committee of the Whole - Terms

of Reference

/ Ngā Ārahina Mahinga

|

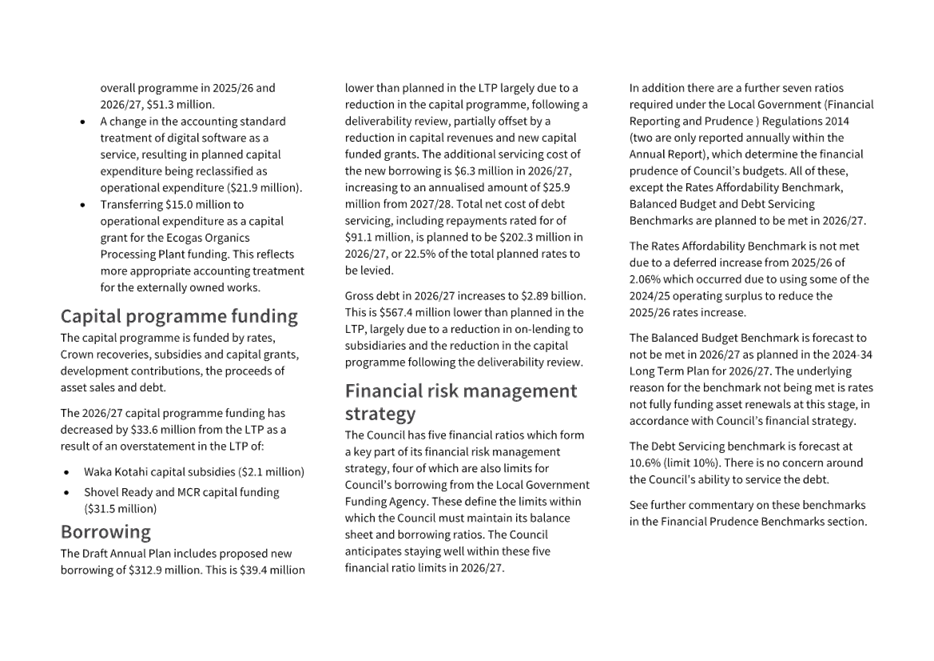

Chair Chair

|

Councillor

MacDonald

|

|

Deputy Chair

|

Councillor

McLellan

|

|

Membership

|

The Mayor and all councillors

are members of

this committee.

|

|

Quorum

|

Half of the members if the number of members (including vacancies) is even, or a majority of members if the number of members (including vacancies) is

odd

|

|

Meeting

Cycle

|

Monthly

|

|

Reports To

|

Council

|

Delegations

The Council delegates to

the Finance

and

Performance Committee authority

to

oversee and make decisions

on the following

matters:

Capital Programme and operational expenditure

·

Monitoring the delivery of the Council’s

Capital Programme and associated operational

expenditure,

including inquiring

into any material discrepancies

from planned expenditure.

·

Approving

amendments to the Capital Programme outside the Long-Term Plan or Annual Plan

processes.

·

Approving

Capital Programme investment cases, and associated operational expenditure, as

agreed in the Council’s Long-Term Plan.

·

Approving

any capital or other carry-forward requests and the use of operating surpluses.

·

Approving

the procurement plans (where applicable), preferred supplier, and contracts for

all capital expenditure where the value of the contract exceeds $15 million

(noting that the Committee may sub-delegate authority for approval of the

preferred supplier and /or contract to the Chief Executive, conditional on

compliance with the procurement plan strategy).

·

Approving the procurement plans (where applicable),

preferred supplier,

and contracts, for

all operational

expenditure

where the value of the contract exceeds $10 million (noting

that

the Committee may sub-delegate

authority for approval of the preferred supplier and/or contract to the Chief Executive, conditional on compliance with the procurement plan strategy).

Non-financial performance

·

Reviewing the delivery of services under

s17A.

·

Amending levels of

service targets, unless the decision is precluded

under section 97 of the Local Government Act 2002.

·

Exercising all of the Council's powers

under section 17A of the Local

Government Act 2002, relating to service

delivery reviews and decisions not to undertake a review.

·

Exercising all of the Council's powers under

section 17A of the Local Government Act 2002, relating to service delivery

reviews and decisions not to undertake a review.

Council Controlled Organisations

·

Monitoring the financial and non-financial

performance of the Council

and Council-controlled Organisations.

·

Making

governance decisions

related to Council

Controlled Organisations under sections 65

to 72 of the

Local Government Act

2002.

·

Exercising the Council’s powers

directly as the shareholder, or through CCHL, or in

respect of an entity

(within

the meaning of section

6(1) of the Local Government Act 2002) in relation to:

-

(without limitation)

the

modification of constitutions and/or trust deeds, and

other governance arrangements,

granting shareholder approval of

major transactions,

appointing directors or trustees, and approving

policies related

to Council Controlled

Organisations; and

-

in relation to

the approval of Statements of Intent and

their modification (if any).

Development

Contributions

·

Exercising all of the Council's powers

in relation to development

contributions,

other than those delegated to the Chief Executive and

Council officers as set out in the Council's Delegations Register.

Property

·

Purchasing or disposing

of property where required for the delivery of the Capital Programme, in accordance with

the

Council’s Long-Term Plan, and where those

acquisitions or disposals

have

not

been delegated to another decision-making body of the

Council or staff.

Loans and debt write-offs

·

Approving debt write-offs where those debt write-offs are not delegated to staff.

·

Approving amendments

to

loans, in accordance with the Council’s Long-Term Plan.

Insurance

·

All insurance matters,

including considering legal

advice from the Council’s

legal and other advisers,

approving further actions

relating

to

the issues, and authorising

the taking of formal actions

(Sub-delegated

to

the Insurance Subcommittee

as per the Subcommittees

Terms of Reference).

Annual Plan and Long Term Plan

·

Providing oversight and monitoring development of the Long Term Plan (LTP) and Annual

Plan.

Submissions

·

The Council

delegates to

the

Committee authority:

-

To consider

and

approve draft

submissions on behalf of the

Council on topics within its

terms of reference. Where the timing of a consultation does

not allow for consideration of a draft submission by the Council

or relevant Committee,

the

draft submission can

be considered and

approved on behalf of the

Council.

Limitations

·

The general delegations to this Committee

exclude any specific decision-making powers that are delegated to a Community

Board, another Committee of Council or Joint Committee. Delegations to staff

are set out in the delegations register.

·

The Council retains the authority to adopt policies, strategies

and bylaws.

The following matters

are prohibited from being subdelegated in accordance with LGA 2002 Schedule 7

Clause 32(1) :

·

the power to make a rate; or

·

the power to make a bylaw; or

·

the power to borrow money, or purchase or

dispose of assets, other than in accordance with the long-term plan; or

·

the power to adopt a long-term plan, annual

plan, or annual report; or

·

the power to appoint a chief executive; or

·

the power to adopt policies required to be

adopted and consulted on under this Act in association with the long-term plan

or developed for the purpose of the local governance statement; or

·

the power to adopt a remuneration and employment

policy.

Chairperson

may refer urgent matters to the Council

As may be necessary from

time to time, the Committee Chairperson is authorised to refer urgent matters

to the Council for decision, where this Committee would ordinarily have

considered the matter. In order to

exercise this authority:

·

The Committee Advisor must inform the

Chairperson in writing of the reasons why the referral is necessary

·

The Chairperson must then respond to the

Committee Advisor in writing with their decision.

·

If the Chairperson agrees to refer the report to

the Council, the Council may then assume decision-making authority for that

specific report.

Urgent

matters referred from the Council

As may be necessary

from time to time, the Mayor is authorised to refer urgent matters to this

Committee for decision, where the Council would ordinarily have considered the

matter, except for those matters listed in the limitations above.

In order to

exercise this authority:

·

The Council Secretary must inform the Mayor and

Chief Executive in writing of the reasons why the referral is necessary

·

The Mayor and Chief Executive must then respond

to the Council Secretary in writing with their decision.

If the Mayor

and Chief Executive agree to refer the report to the Committee, the Committee

may then assume decision-making authority for that specific report.

|

3. Draft

Annual Plan 2026/27

|

|

Reference Te Tohutoro:

|

26/81358

|

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Performance & Planning

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to present to the Committee for consideration and

adoption:

· The Draft Annual Plan

2026/27, including attached documents;

· The Draft Annual Plan

2026/27 draft Consultation Document; and

· The Draft Annual Plan

2026/27 consultation and engagement process to be undertaken.

1.2 The

Council is required to prepare and adopt an Annual Plan for each financial year

(s.95(1) Local Government Act 2002 (LGA)). The purpose of the annual plan is

to:

· contain the proposed

annual budget and funding impact statement for 2026/27;

· identify any variation

from the financial statements and funding impact statement in the

Council’s Long-Term Plan for 2024-34;

· provide integrated

decision-making and co-ordination of the Council’s resources; and

· contribute to the

accountability of the Council to the community.

1.3 The

decisions in this report are of high significance based on the Council’s

Significance and Engagement Policy.

2. Officer

Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Draft Annual Plan 2026/27

Report.

2. Notes that the decisions in this report are

assessed as being of high significance based on the Christchurch City

Council’s Significance and Engagement Policy.

3. Notes the Recommendations of the

Council’s Audit and Risk Management Committee at its meeting on 02

February 2026 (refer Attachment A).

4. Notes that the information and options

provided in the Draft Annual Plan 2026/27 report are as directed by the

resolutions of the Finance and Performance Committee (on behalf of Council) at

its meeting of 17 December 2025.

5. Confirms the staff recommendation as the

preferred option upon which to base development of the Draft Annual Plan

2026/27, noting that key components detailed below result in an average overall

rates increase of 7.95% for 2026/27:

a. the reduction of the planned core capital

expenditure to $586.2 million following a review of the deliverability of the

Council’s capital programme; and

b. the in-housing of the Council’s urban

development functions; and

c. the application of $6.3 million of analytical

savings to debt reduction, by increasing rating for renewals; and

d. the application of $10.0 million of the

forecast 2025/26 operating cash surplus to reduce borrowing in 2025/26,

reducing opening debt for 2026/27; and

e. reducing the Business differential on the

Value Based General Rate from 2.220 to 2.000; and

f. a breach of the balanced budget financial

prudence benchmark for 2026/27 (as indicated in the LTP).

6. Approves and adopts for consultation the information contained or referred to in the

staff report which provides the basis for the Draft Annual Plan 2026/27,

together with any amendments made by resolution at the meeting, and which

includes the following attachments of this report:

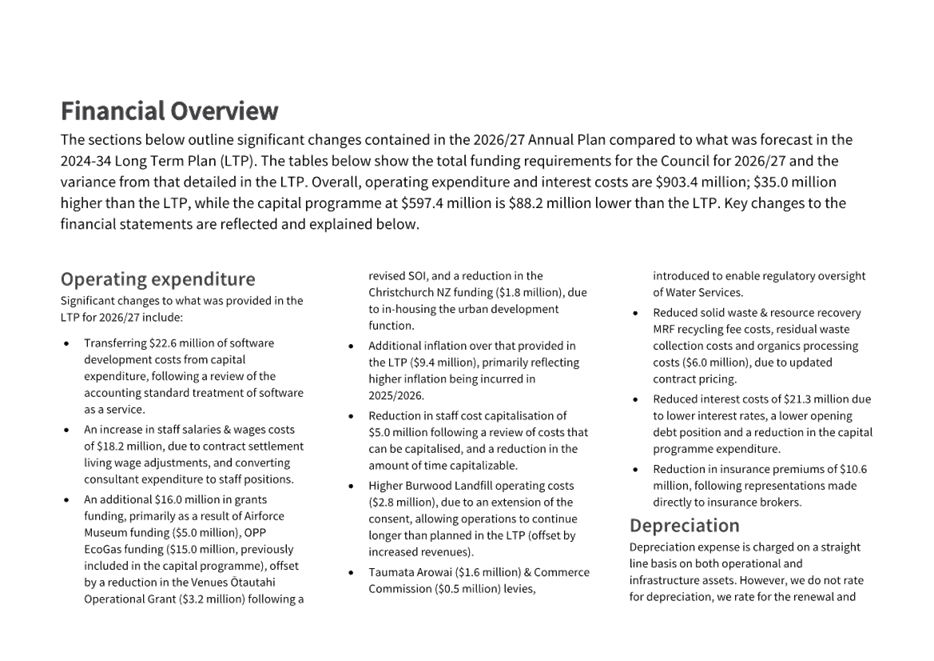

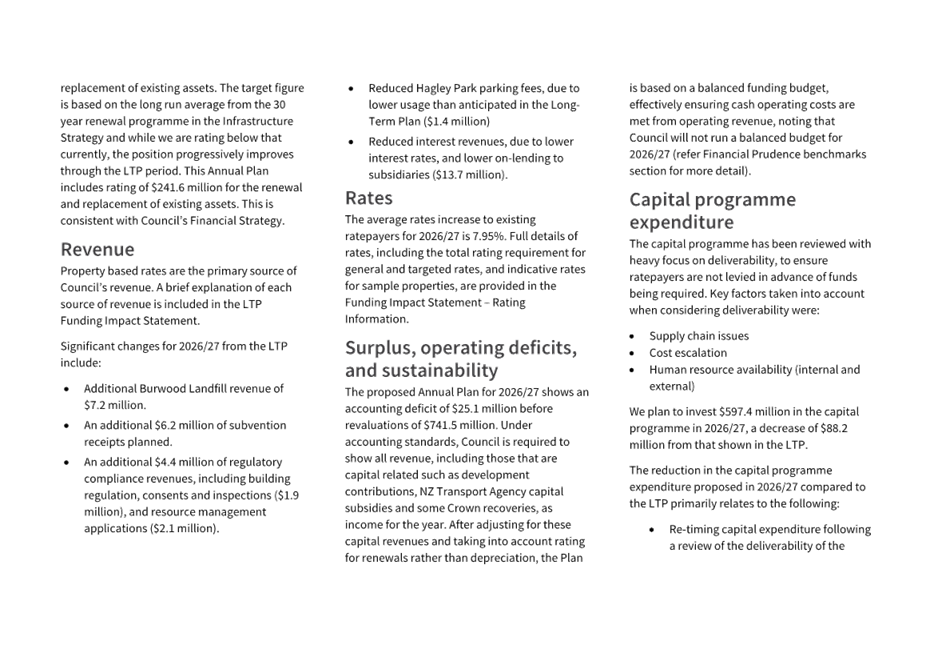

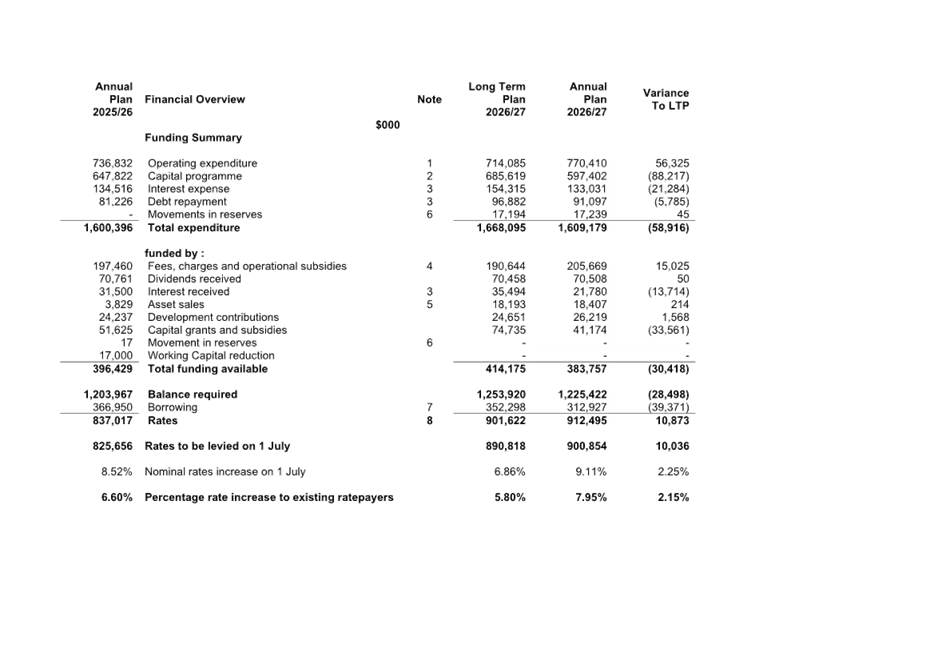

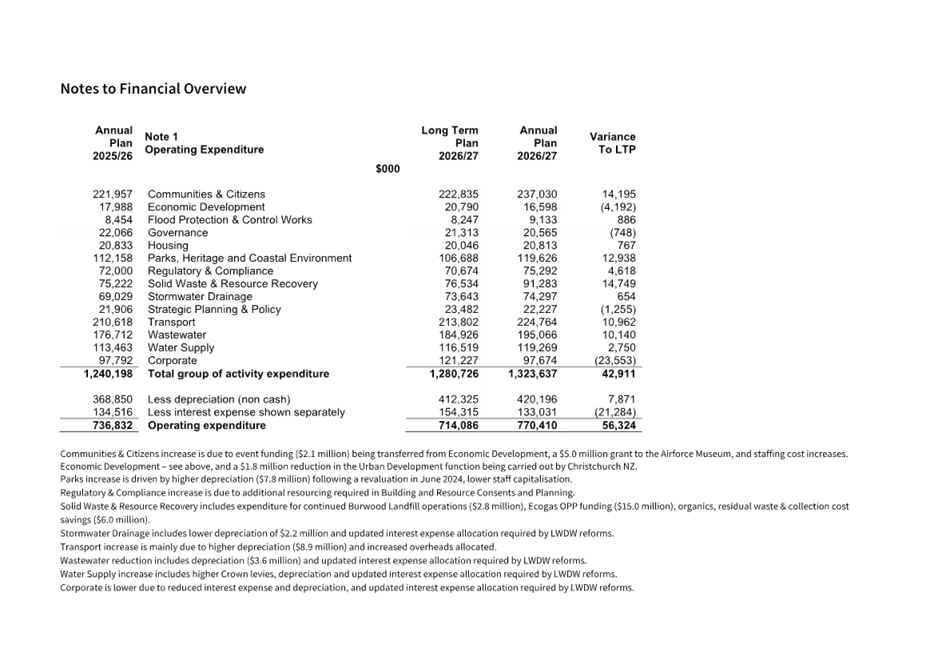

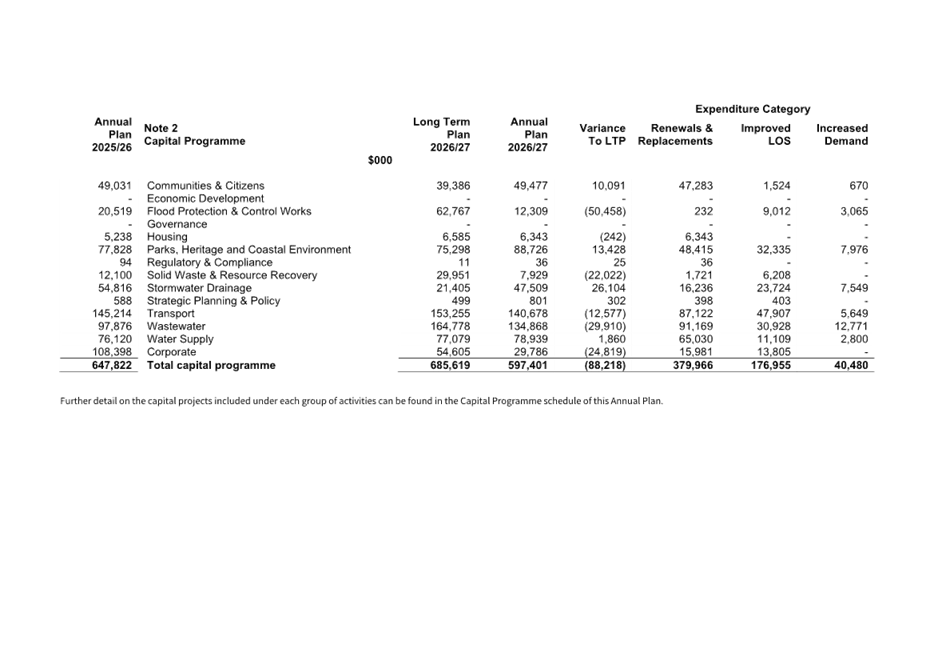

a. Financial Overview, including financial

changes to that contained in the Long-Term Plan 2024-2034 (Attachment B)

b. Funding Impact Statement (Attachment C)

c. Rating Information (Attachment D)

d. Rating Policies (Attachment E)

e. Financial Prudence Benchmarks (Attachment F)

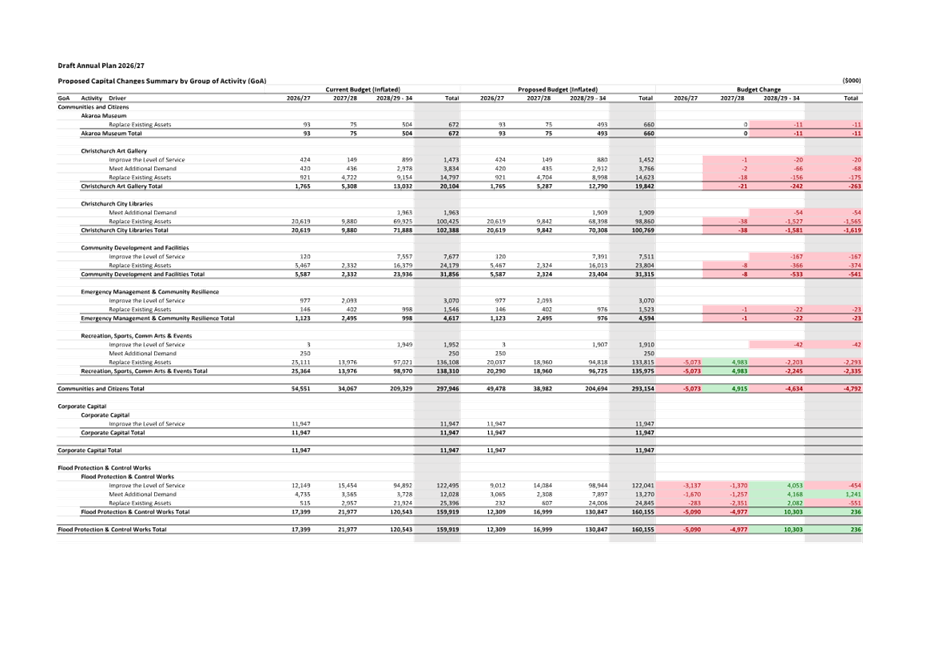

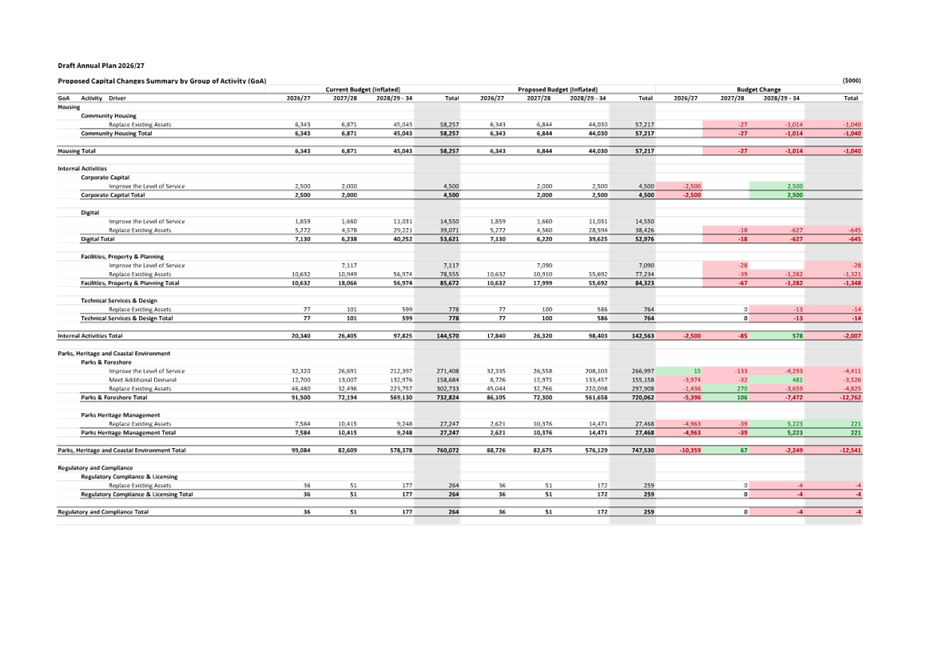

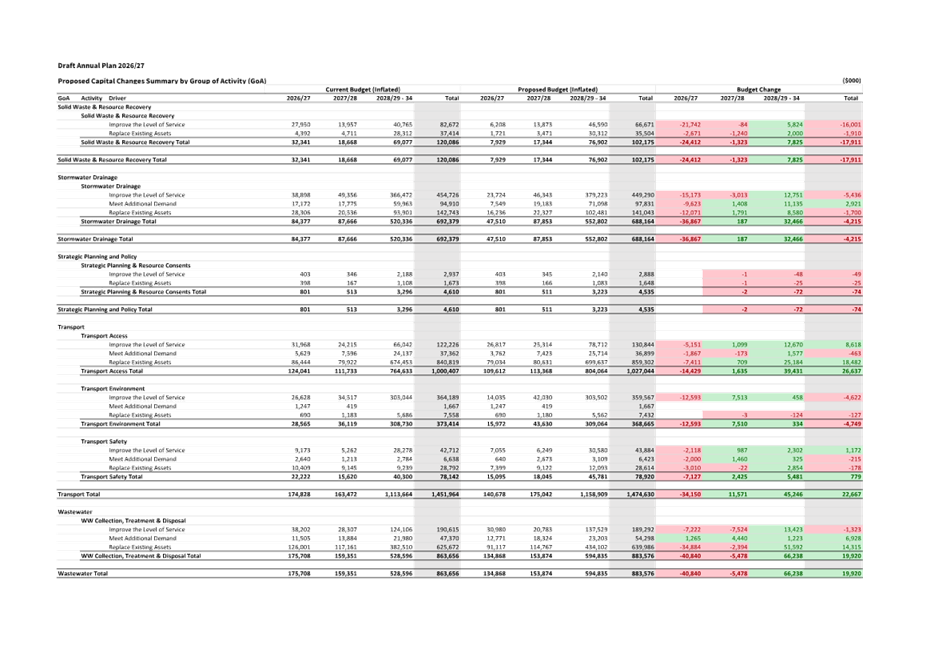

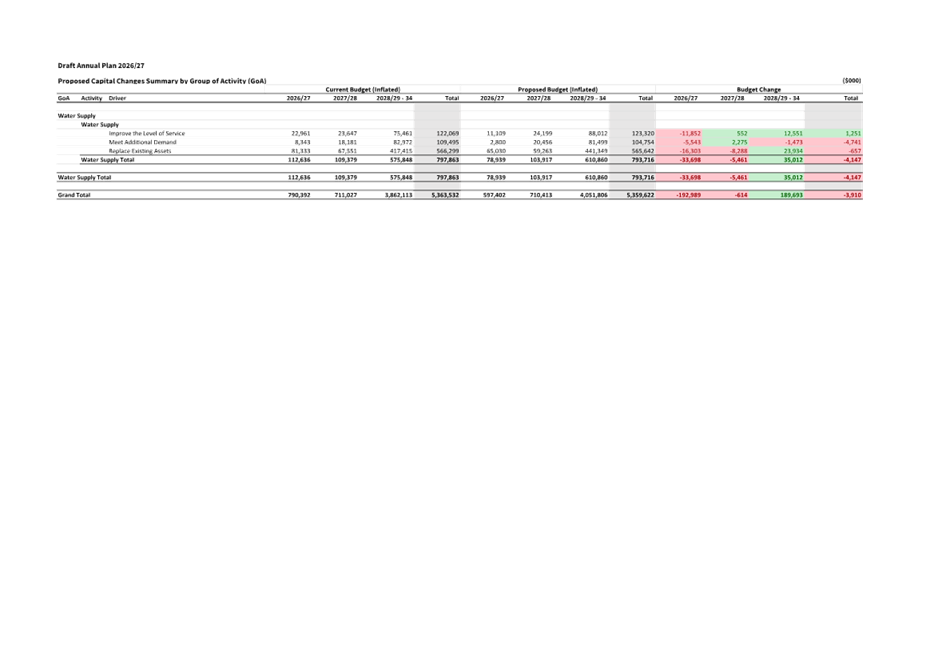

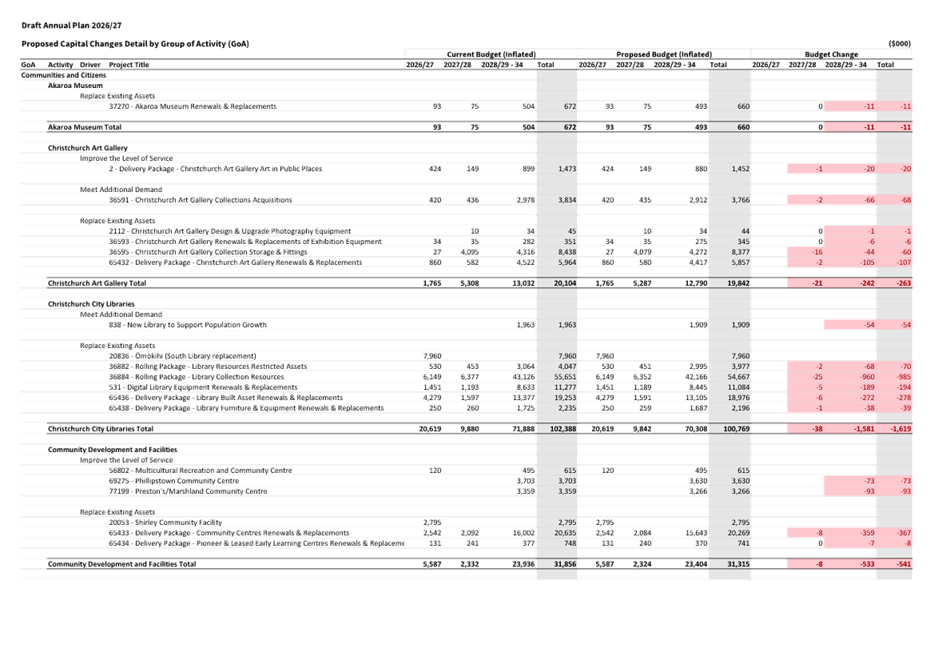

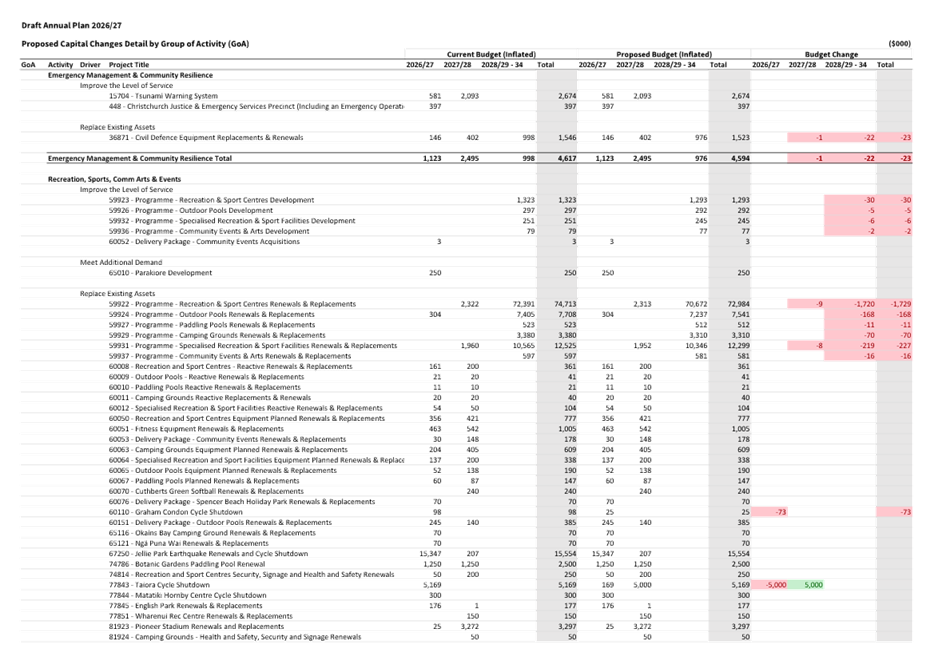

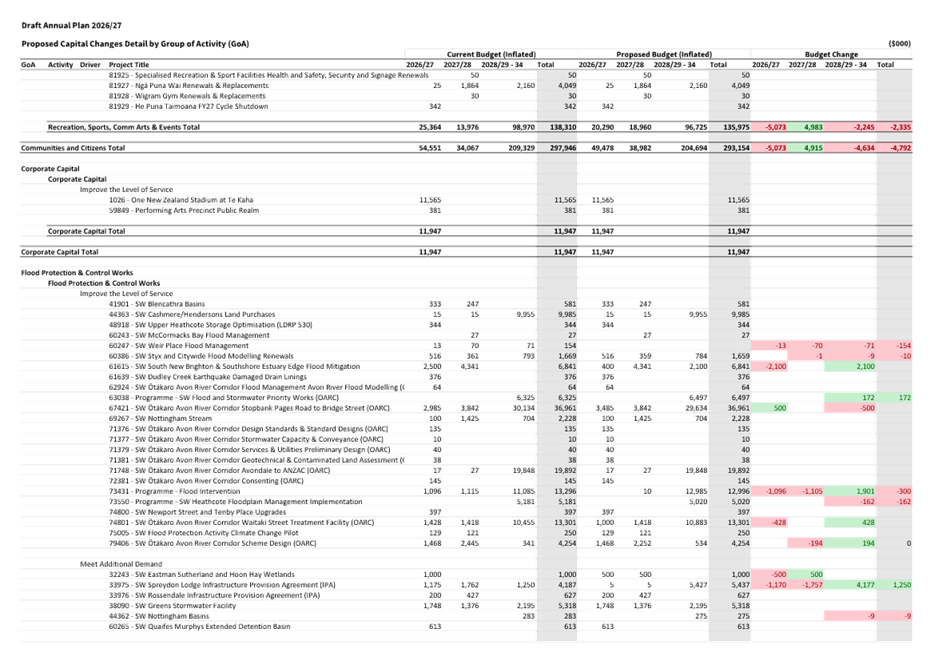

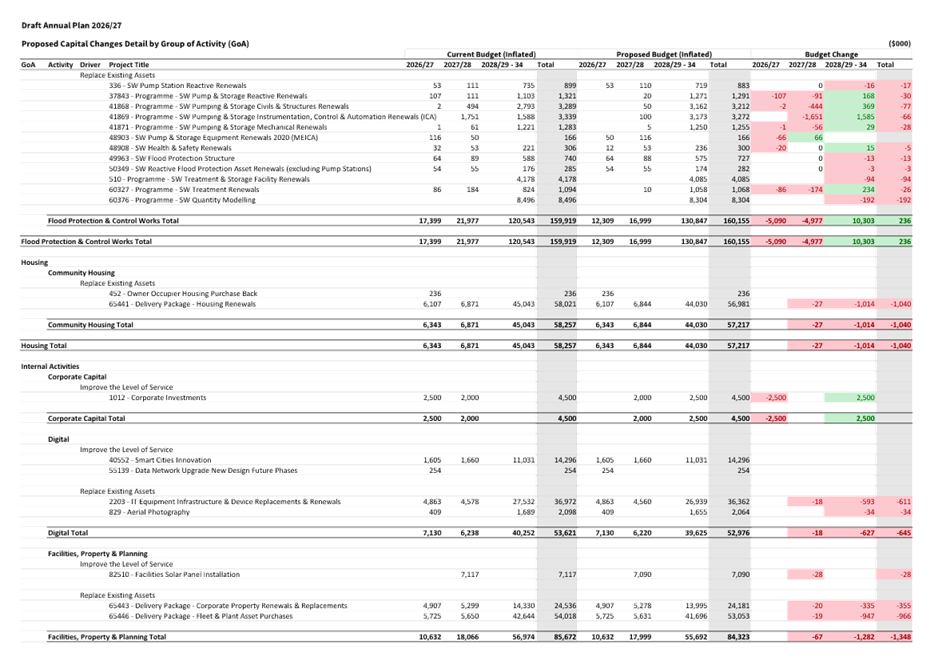

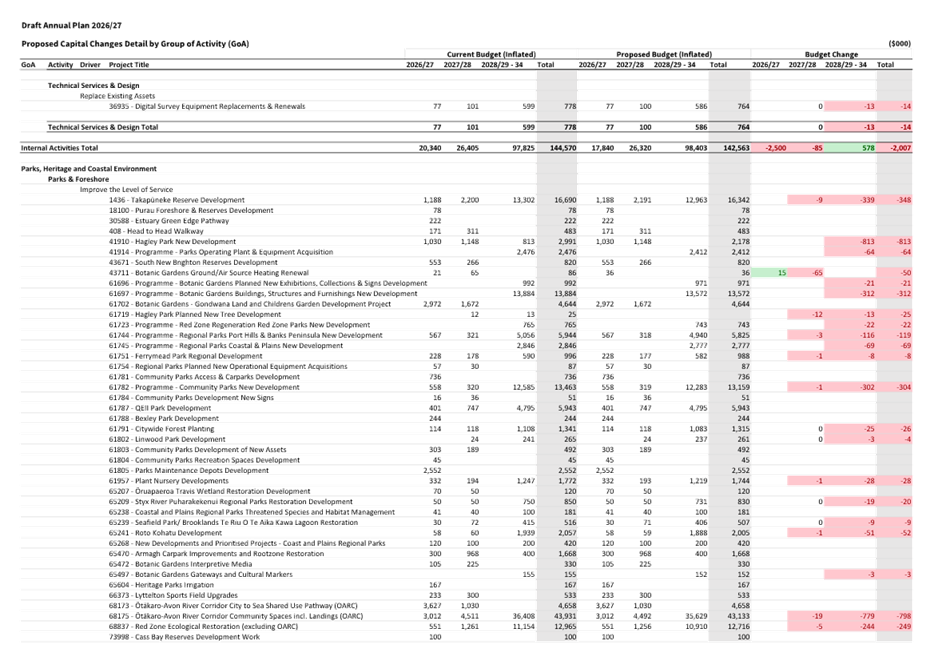

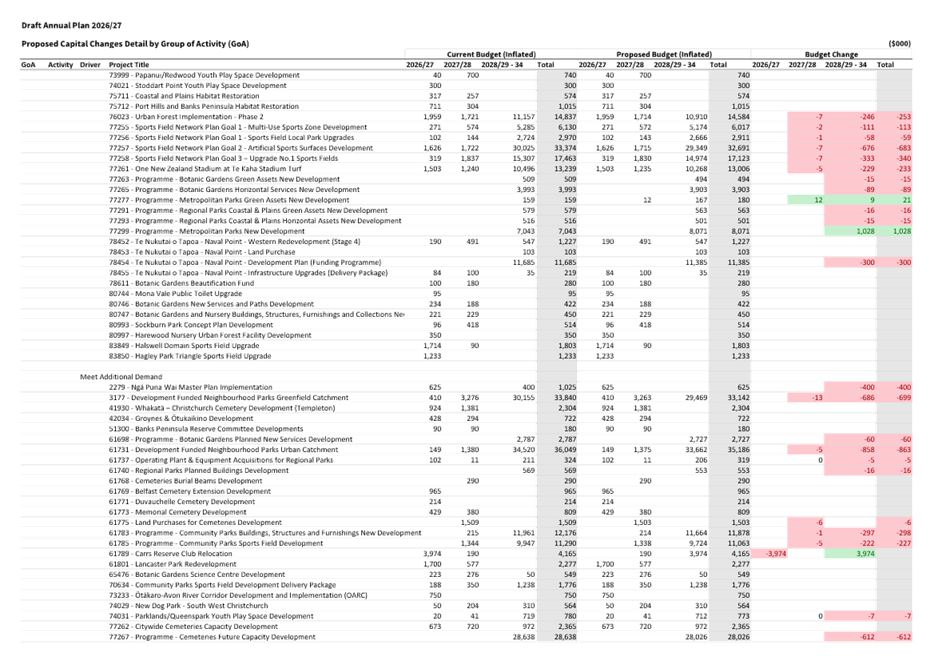

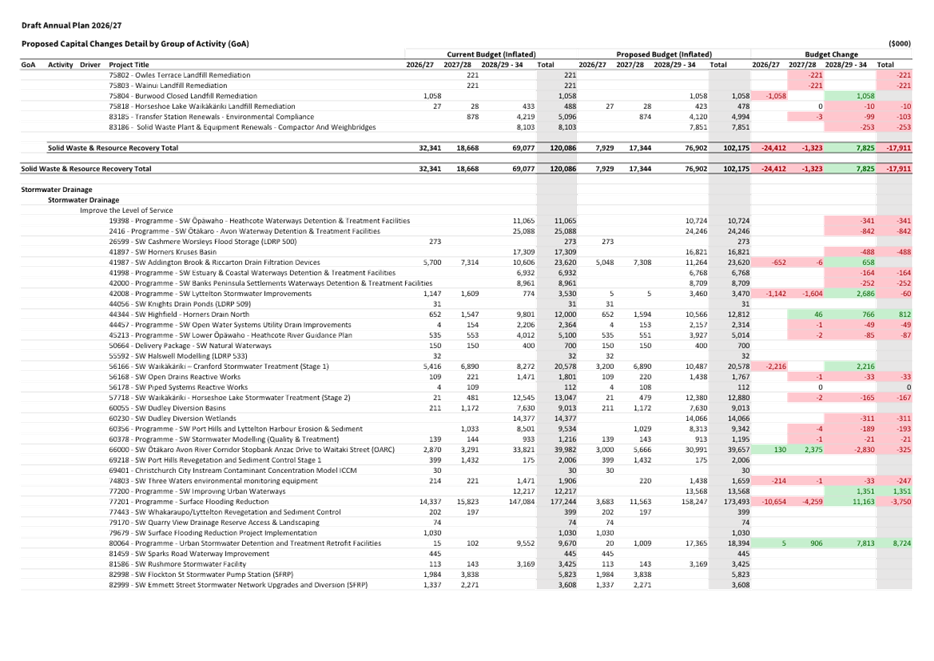

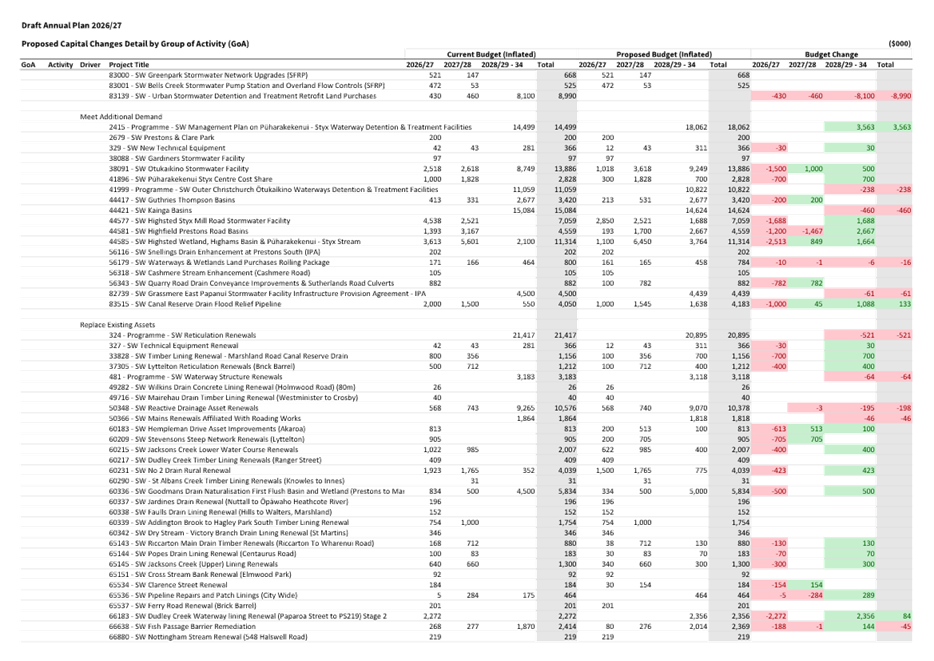

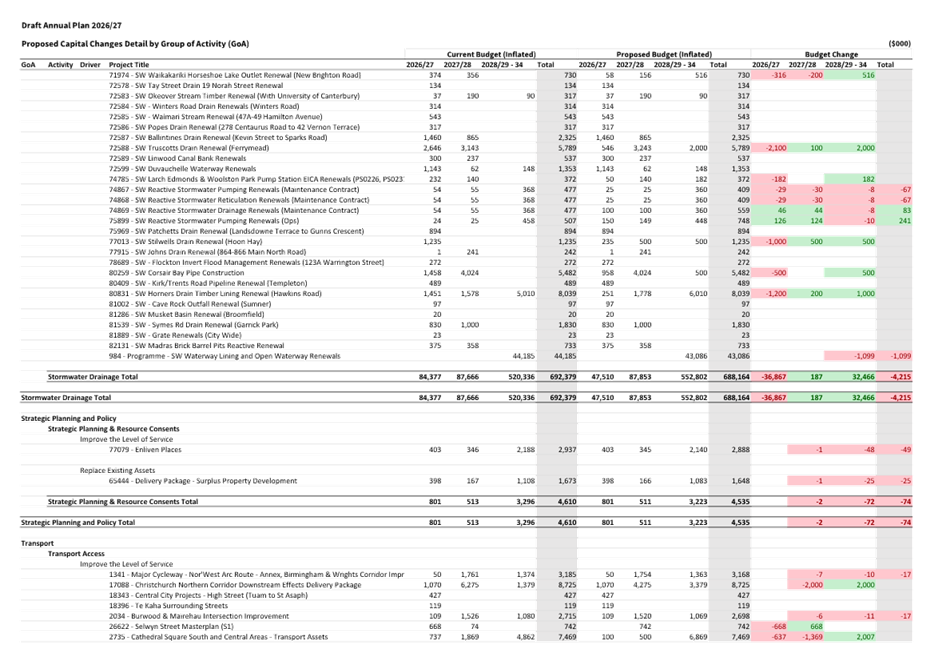

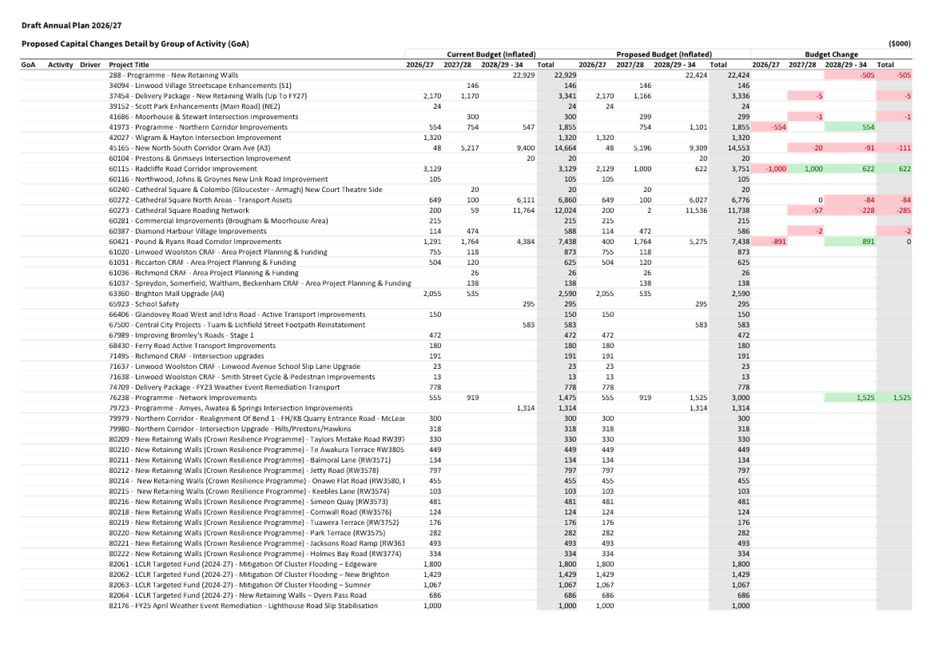

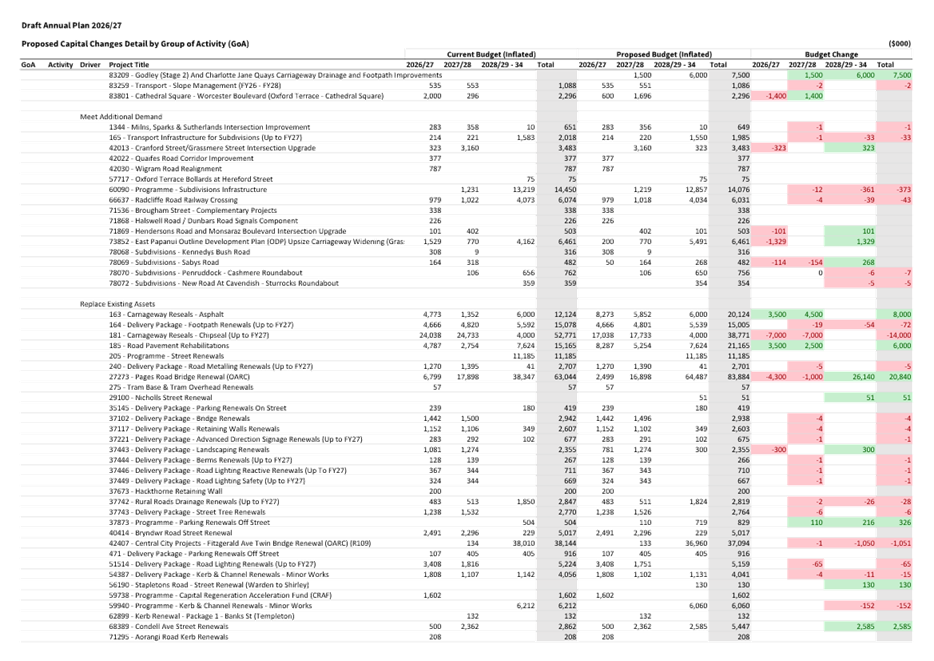

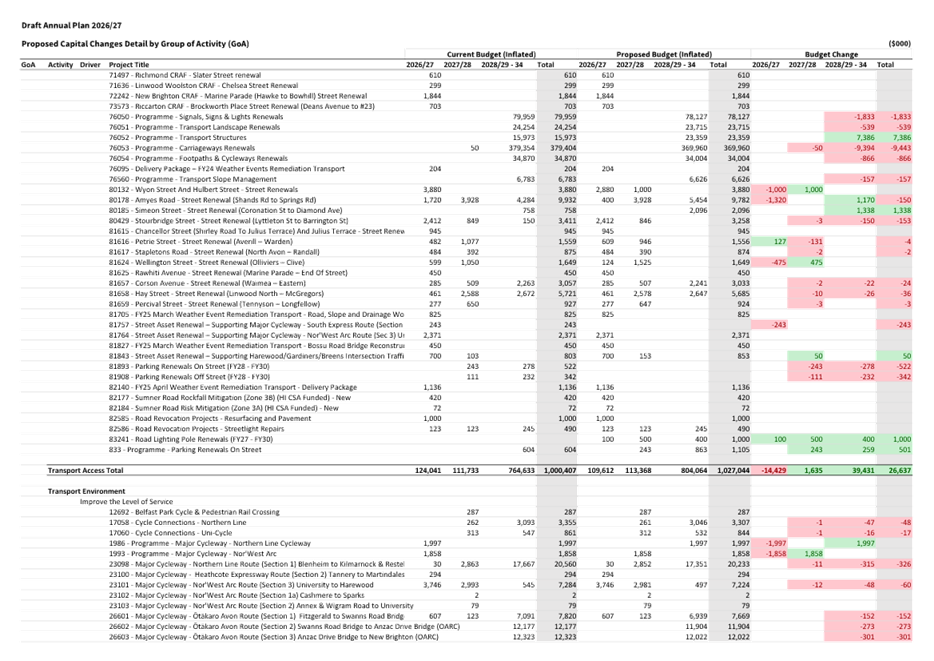

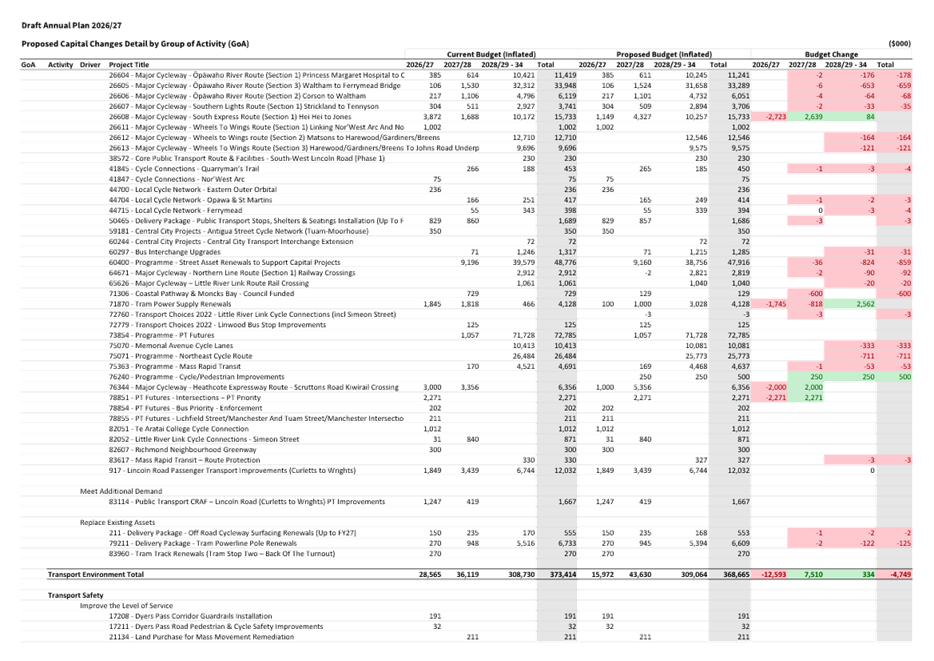

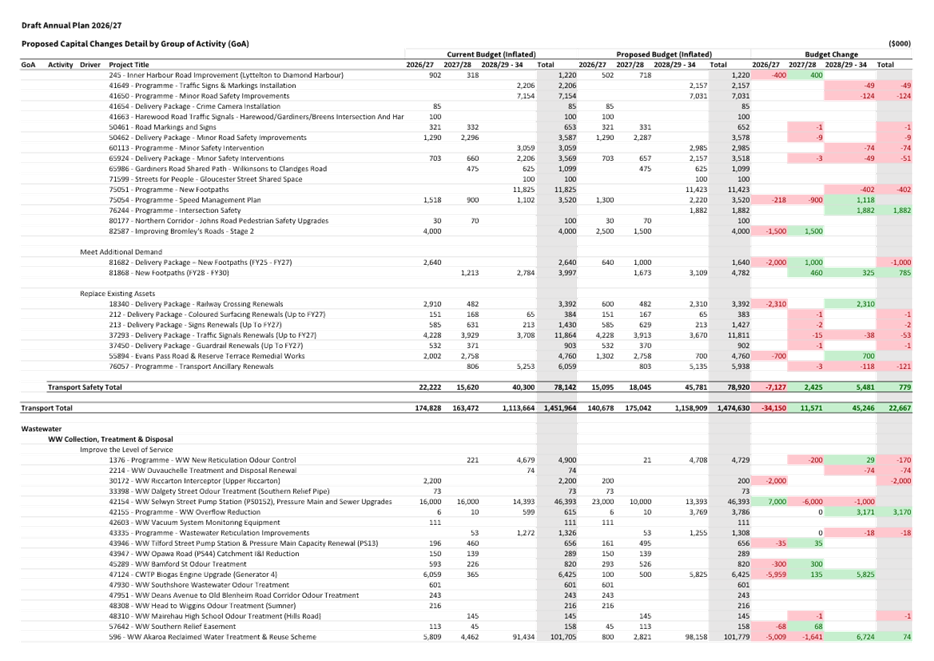

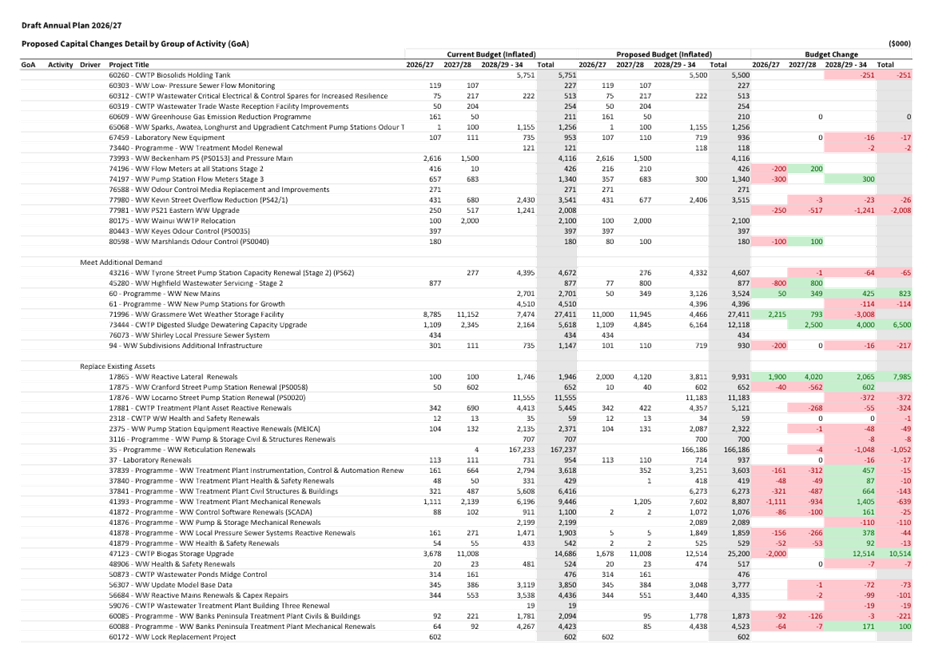

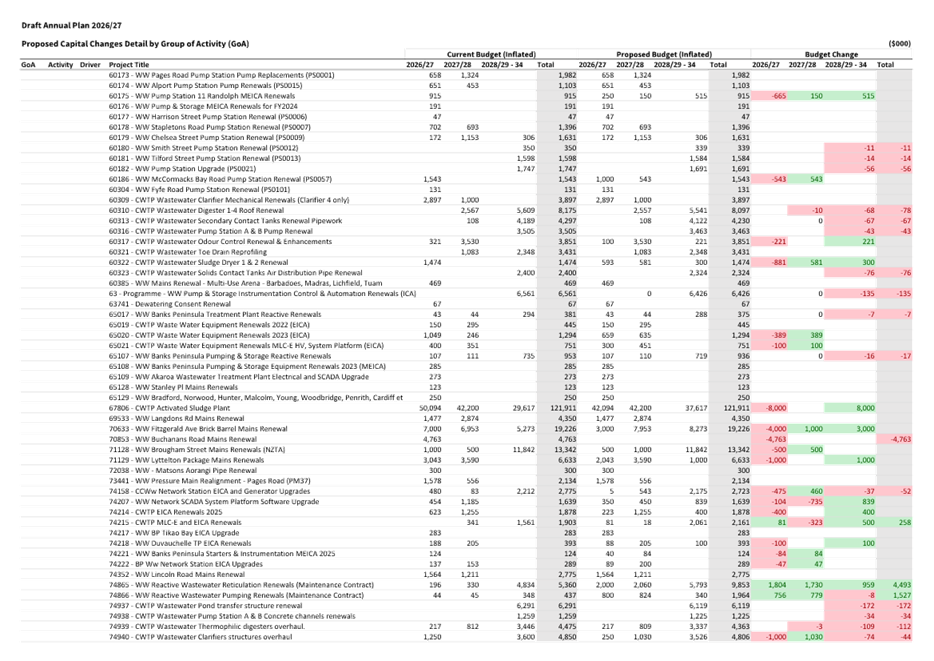

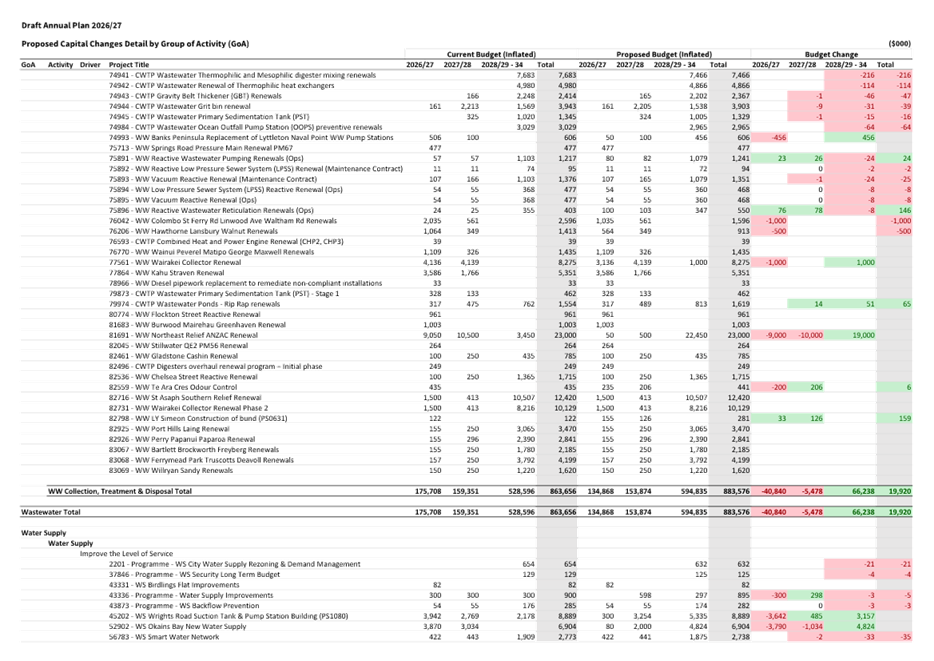

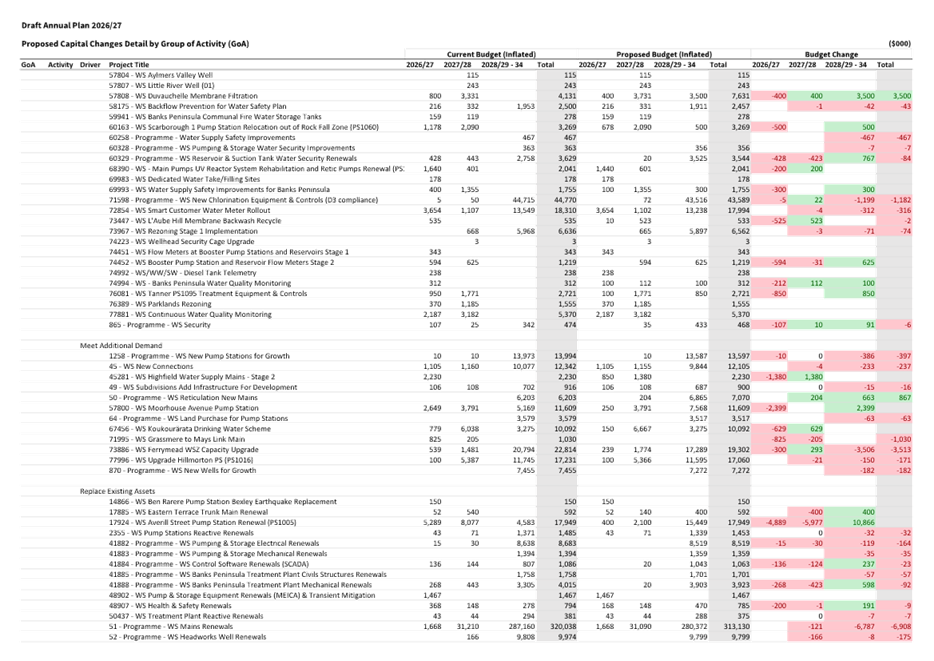

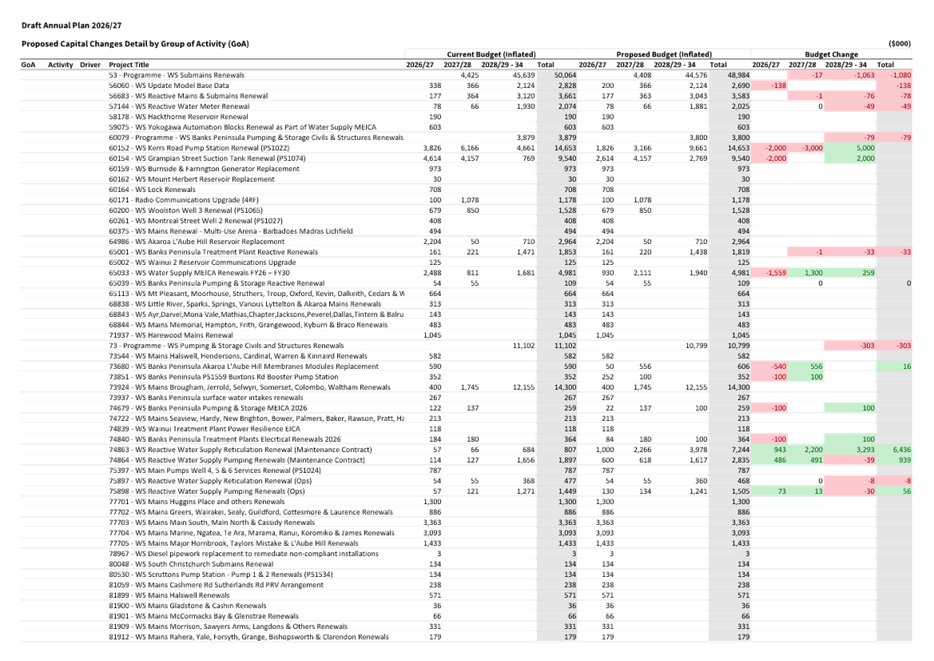

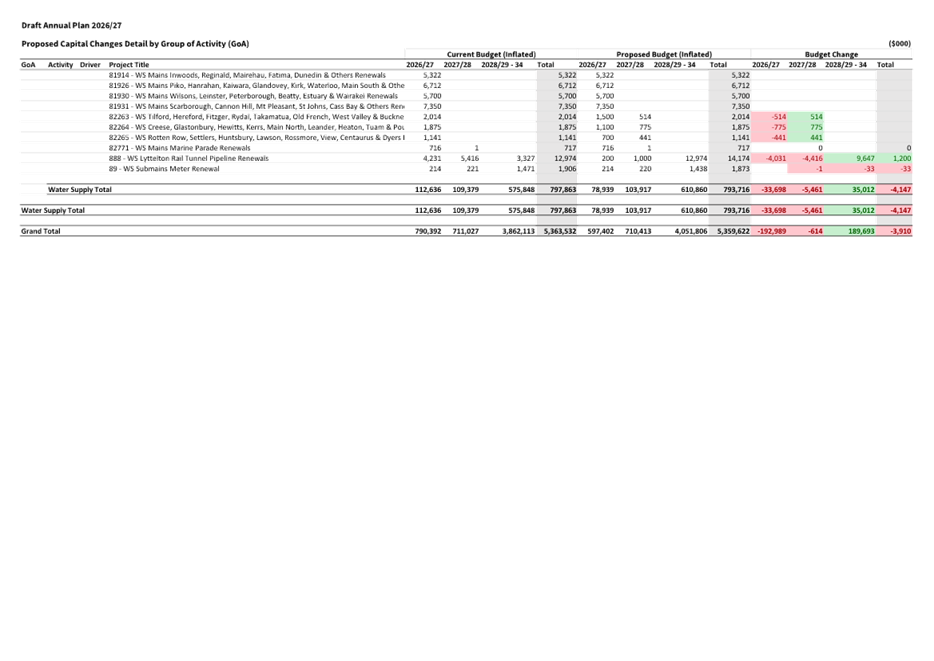

f. Proposed Capital Programme, including schedule

of changes to LTP (Attachment G)

g. Proposed Minor Changes to Levels of Service

(Attachment H)

h. Proposed Fees and Charges (Attachment I)

i. Prospective Financial Statements (Attachment

J)

j. Statement of Significant Accounting Policies

(Attachment K)

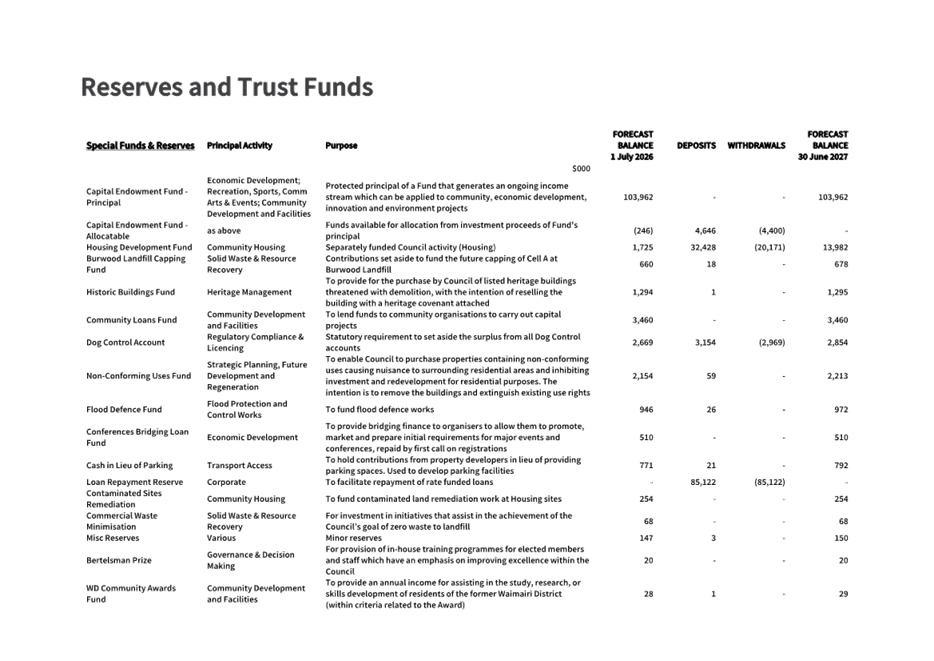

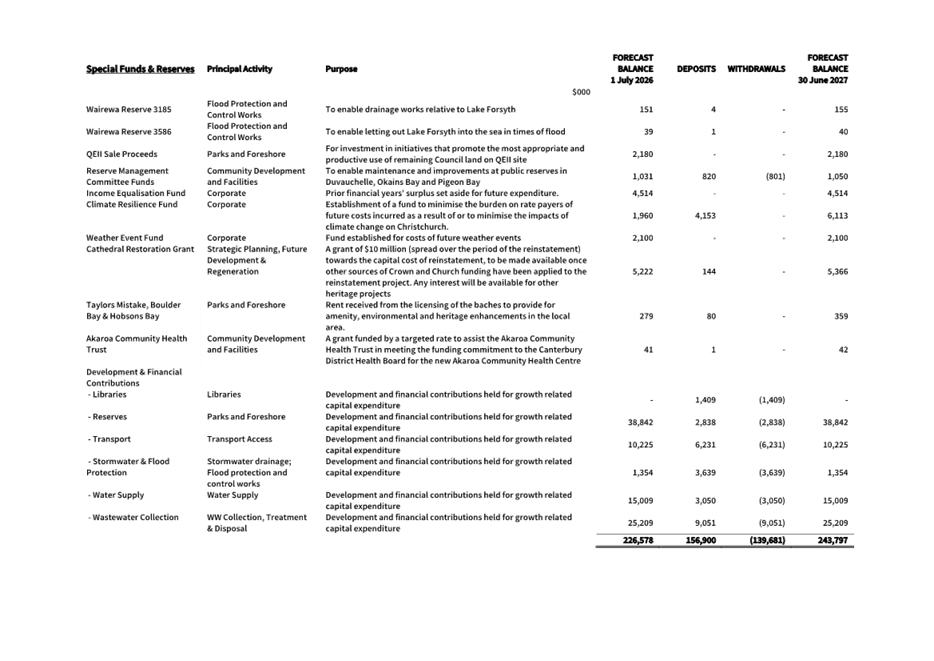

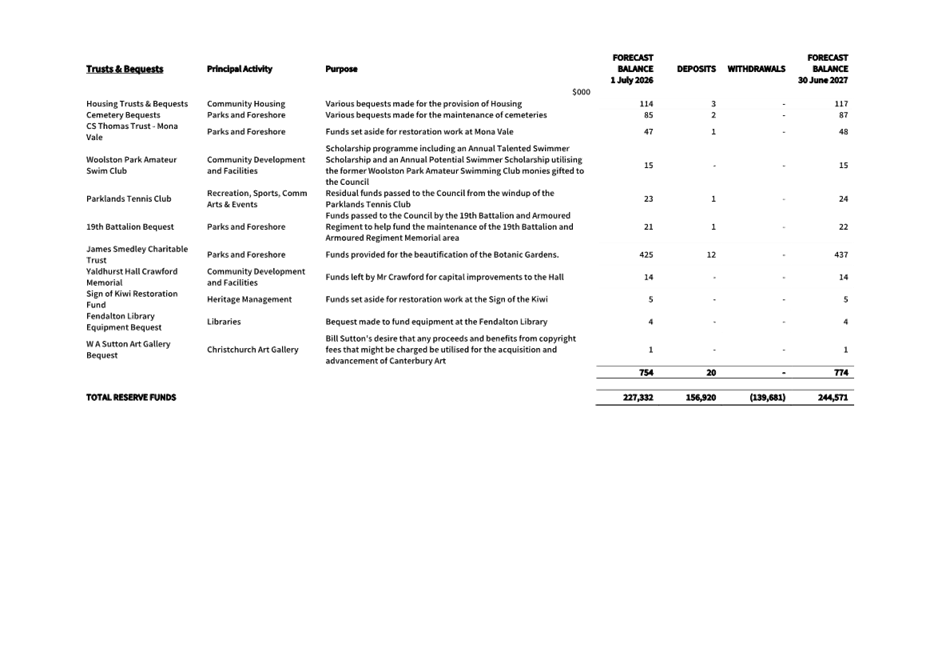

k. Reserves and Trust Funds (Attachment L)

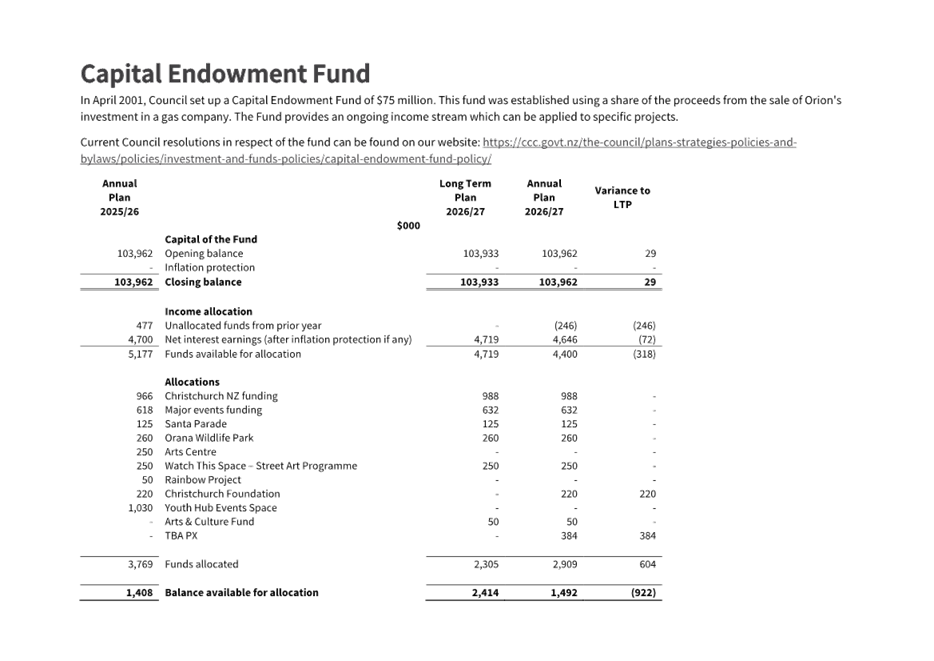

l. Capital Endowment Fund (Attachment M)

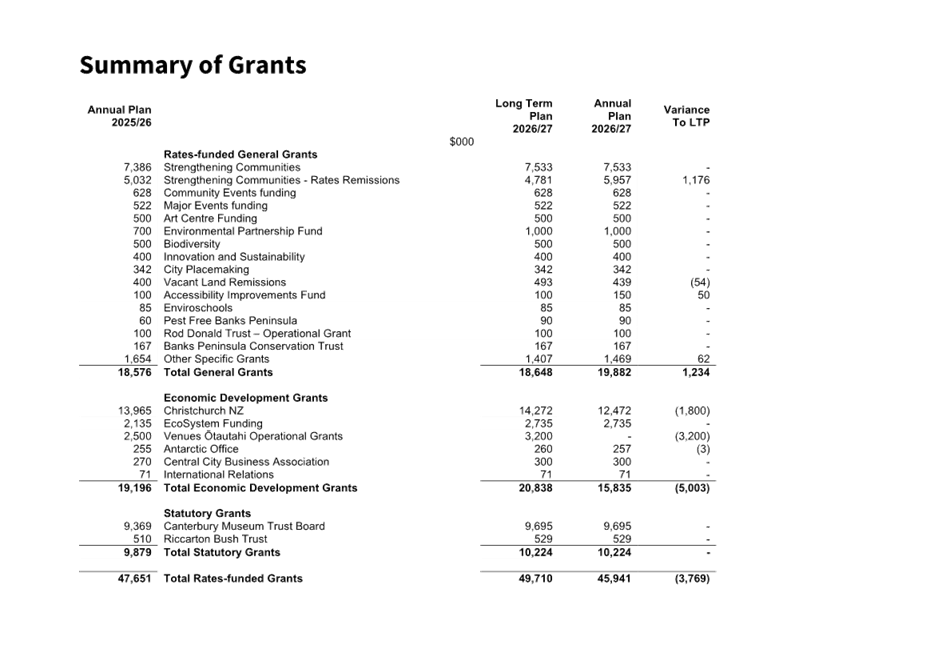

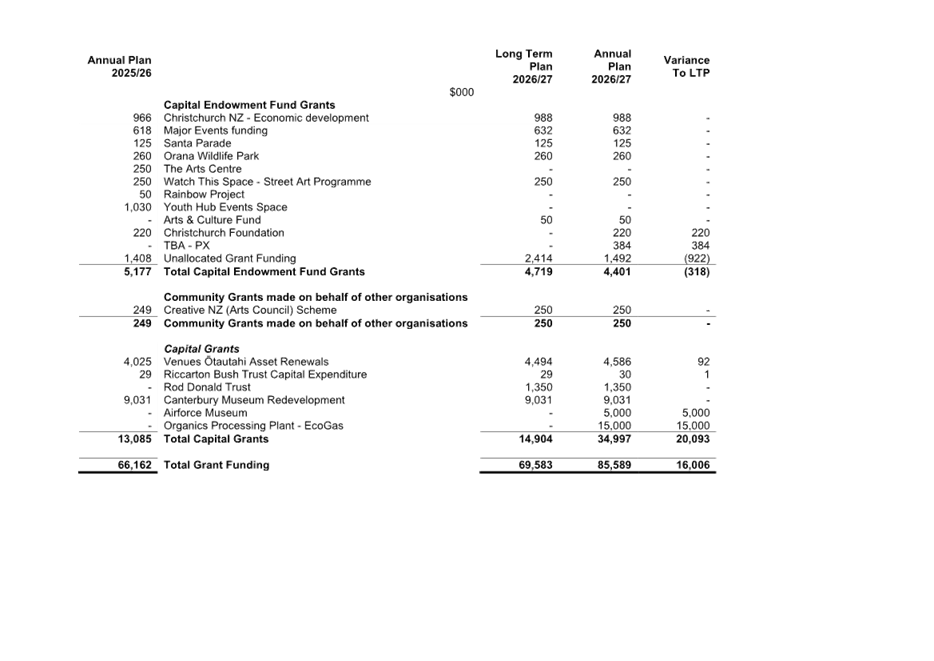

m. Summary of Grants (Attachment N)

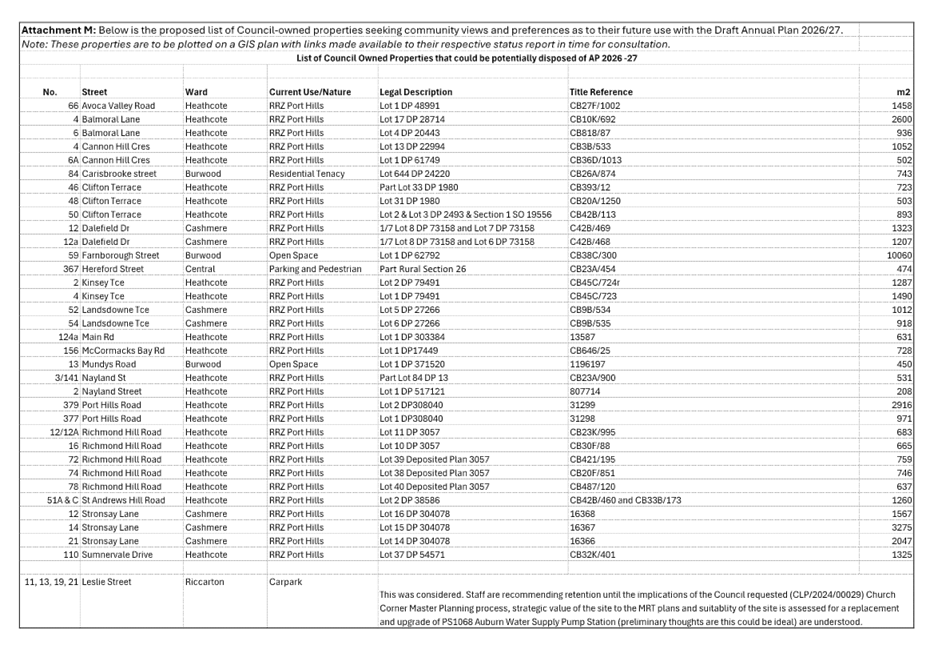

n. List of properties for seeking the community

views and preferences as to their future use (Attachment O)

7. Approves and adopts for public consultation

the draft Consultation Document for the Draft 2026/27 Annual Plan (under

separate cover).

8. Approves the following process for the Draft

Annual Plan 2026/27 consultation:

a. All relevant information and documents,

including the Consultation Document, be made available on the Council’s

website from 27 February 2026.

b. Hard copy information and documents to be made

available at Council libraries and service centres from 27 February 2026.

c. The period for making submissions will run

from 27 February 2026 to 11.59pm on 27 March 2026.

d. For people who indicate they wish to present

oral submissions, hearings will be held from late March to April 2026 (exact

dates will be confirmed and communicated to those submitters closer to the

time), noting that only the name of the submitter is published with the

submissions.

9. Authorises the General Manager Finance, Risk

and Performance/CFO to make any non-material changes to the Draft 2026/27

Annual Plan documents and/or information attached to or referred to in the

staff report.

10. Notes that the Council will meet on 23 June

2026 to adopt its Annual Plan 2026/27.

3. Executive Summary Te Whakarāpopoto Matua

3.1 The

purpose of an Annual Plan is to provide a one-year schedule of updates to the

Long-Term Plan (LTP), if any are required by changing circumstances.

3.2 Annual

Plans are not designed as a mechanism to revisit the entire LTP. To give

effect to the latter requires an amendment to the LTP, and that requires (among

other matters) that the amended LTP is audited.

3.3 Where

that list of updates is not material a local authority may opt to not consult

on its Annual Plan.

3.4 Annual

Plans, being limited in scope relative to an LTP, are not required to be

audited. The options and recommendations set out in this report meet the

criteria for an Annual Plan, in contrast to an amendment of the LTP, and were

workshopped extensively with Council after the 2025 triennial elections.

3.5 The

Council has provided clear direction on the process to be followed. Councillors

advised that the process would be for an Annual Plan, and that the draft Annual

Plan would be consulted on with the community.

3.6 Recent

announcements by central government on local government reform - notably those

concerning a proposed rates capping model will, if enacted, have a significant

impact on the 2027-2037 LTP and future Annual Plans. It should be noted that

these proposals do not directly impact the Annual Plan 2026/27.

4. Background/Context Te Horopaki

Starting Position

4.1 In

accordance with the LGA, the Council adopted its Long-Term Plan 2024-34 in June

2024 (LTP 2024 – 34). The LTP sets out service delivery, capital

programmes and budgets over that ten-year period. The LTP 2024 – 34 was

based on several key Council decisions:

· that levels of service

would not be reduced;

· that the core capital

programme (excluding One New Zealand Stadium at Te Kaha) would increase from

483M in 2023/24 to 668M in 2026/27;

· that the One New Zealand

Stadium at Te Kaha would be completed and hosting events by the beginning of

the 2026/27 financial year;

· staff would be recruited

for the new Parakiore Recreation and Sport Centre;

· asset renewals would be

sustainable; and

· that a variety of climate

resilience and environmental initiatives / grants would be funded.

4.2 The

LTP 2024 – 34 and Annual Plan 2025/26 (AP 2025/26) factored in inflation

based on the BERL Local Government Cost Index (LGCI) forecasts (BERL’s

LGCI is the Cost Price Index (CPI) for local authorities and accepted by Audit

New Zealand as providing a reliable measure of the LGCI).

4.3 Subsequently,

the Council adopted the AP 2025/26 (year two of the LTP 2024 -34) on 26 June

2025.

4.4 The

decisions made when adopting the AP 2025/26 initially put the rates increase

for the Annual Plan 2026/27 at 10.52% as shown below:

|

Major Drivers

|

2026/27

|

|

|

Cost changes – inflation

|

2.96%

|

Based on BERL 3.1% Opex, 3.4% Capex for

2026/27.

|

|

Rating for Renewals

|

2.78%

|

Increase in rating for renewals to

achieve fully funded renewals by 2032 per the Financial Strategy.

|

|

Capital Programme

|

2.78%

|

Planned capital programme expenditure of

$713.0m in 2026/27.

|

|

Use of 2024/25 Surplus

|

2.06%

|

$17.0m of surplus applied to 2025/26

rates reduction in 2025/26 AP.

|

|

Climate Resilience Fund

|

0.25%

|

$2.1m fund contribution increase (total

2026/27 contribution $4.1m).

|

|

Operational Expenditure

|

0.39%

|

|

|

Corporate Revenues & Expenses

|

(0.72%)

|

Subvention receipts, CCO on-lending

interest, dividend projections.

|

|

Rating Growth

|

(1.00%)

|

1% city capital value growth

|

|

Base requirement

|

9.50%

|

|

|

One New Zealand Stadium at Te Kaha

|

1.02%

|

Debt repayment & interest expense

resulting from borrowing to fund One New Zealand Stadium at Te Kaha

completion.

|

|

Initial Position

|

10.52%

|

|

4.5 Since

the adoption of the AP 2025/26 there have been further changes with financial

impacts based on Council direction and updated information becoming available.

These have reduced the current rates increase for the Annual Plan 2026/27 to

7.95%. Material changes include:

|

|

2026/27

|

2027/28

|

2028/29

|

|

2026 Annual Plan Rates Increase above

|

10.52%

|

9.11%

|

5.73%

|

|

|

|

|

|

|

Changes incorporated in the initial

budget build (reduced

insurance, updated subvention receipt forecast, Burwood Landfill extension,

2024/25 reduced capital expenditure)

|

(1.30%)

|

0.40%

|

0.24%

|

|

2026/27 Capital Programme deliverability

review (reducing

the 2026/27 planned core capital expenditure from $778.8m to $586.2m.)

|

(0.71%)

|

(0.89%)

|

0.52%

|

|

In-housing Urban Development functions

|

(0.19%)

|

0.01%

|

0.01%

|

|

Analytical Savings ($6.3m of savings which do not

impact LoS, based on historic performance to the proposed budget)

|

(0.73%)

|

0.06%

|

0.05%

|

|

Additional Rating for Renewals ($6.3m of analytical savings

applied to rating for renewals, reducing interest and debt repayment costs)

|

0.73%

|

(0.11%)

|

(0.09%)

|

|

Draft Annual Plan Build (17 Dec 2025)

|

8.32%

|

8.58%

|

6.46%

|

|

|

|

|

|

|

Additional savings identified ($0.8 million, various minor

adjustments and savings)

|

(0.10%)

|

0.01%

|

0.01%

|

|

Updated opening balance sheet debt ($10.0 million reduction in

2025/26 borrowing based on capex forecast)

|

(0.10%)

|

0.01%

|

0.01%

|

|

Updated opening balance sheet debt ($10.0 million reduction in

2025/26 borrowing based on opex forecast)

|

(0.10%)

|

0.01%

|

0.01%

|

|

Updated rating growth (Rating growth increased $0.6

million based on 2025/26 actual rates strike after adjustments)

|

(0.07%)

|

0.02%

|

0.02%

|

|

Proposed Draft Annual Plan

|

7.95%

|

8.63%

|

6.51%

|

Purpose and

confirmation of process of the Annual Plan

4.6 The

affordability of rates is a key concern for the Council. When considering how

rate increases can be moderated it is important to keep in mind the legal and

administrative mechanisms of the Annual Plan, such as changes to levels of

service and their implementation.

4.7 Following

the election of the new Council in October 2025, staff began a series of

workshops with the Mayor and councillors on the Annual Plan 2026/27. The

following related information session/workshops have taken place for the

members of the meeting:

|

Date

|

Subject

|

|

6th

Nov 2025

|

AP Workshop

1: General update on Annual Plan 2026/27

|

|

12th

Nov 2025

|

AP Workshop

2: Update on Capital Programme review

|

|

19th

Nov 2025

|

AP Workshop

3: Council only day

|

|

27th

Nov 2025

|

AP Workshop

4: Council only day

|

|

4th

Dec 2025

|

AP Workshop

5: Council only day

|

|

9th

Dec 2025

|

AP Workshop

6: Feedback on Council only days and potential savings options

|

|

17th

Dec 2025

|

Finance and

Performance Committee Meeting – Confirmation of content – Draft

Annual Plan 2026/27

|

|

27th

Jan 2026

|

Council

Workshop: General Revaluation and Rates Update

|

4.8 Staff

prepared options on various ways to reduce the rates increase while still

meeting (1) the decisions made by Council in the LTP24-34, (2) the fixed costs

which must also be met, and (3) the Council guidance on the Annual Plan

process.

4.9 It

may be helpful when considering options to note as a quick guide that $8.3m of

rates funded operational expenditure (OPEX) equals a 1% rate increase. A

one-off saving (additional revenue or reduced cost) reduces rates for one year

but has a corresponding increase the following year. To reduce rates on an

ongoing basis the savings must be permanent and not savings identified for a

particular year only.

Capital Programme Deliverability

4.10 Staff

have reviewed the capital programme to ensure it reflects realistic delivery

capacity, aligns with strategic priorities and addresses growing infrastructure

demands. The proposed adjustments reduce the 2026/27 core capital budget from

$778.8 million (including approved carry-forwards from 2024/25) to $586.2

million, focusing on key projects such as transport upgrades, water supply

renewals, wastewater improvements, and stormwater management / flood reduction.

This approach balances affordability and deliverability, lowering the rates

increase by 0.7% and reducing borrowing requirements, while continuing to

invest in essential infrastructure and community facilities.

4.11 Capital

expenditure (Capex) and/or borrowing of approximately $110m equals a 1% rate

increase spread over 2 years (year 1: 0.27%, year 2: 0.73%).

5. Financial Implications Ngā Hīraunga Rauemi

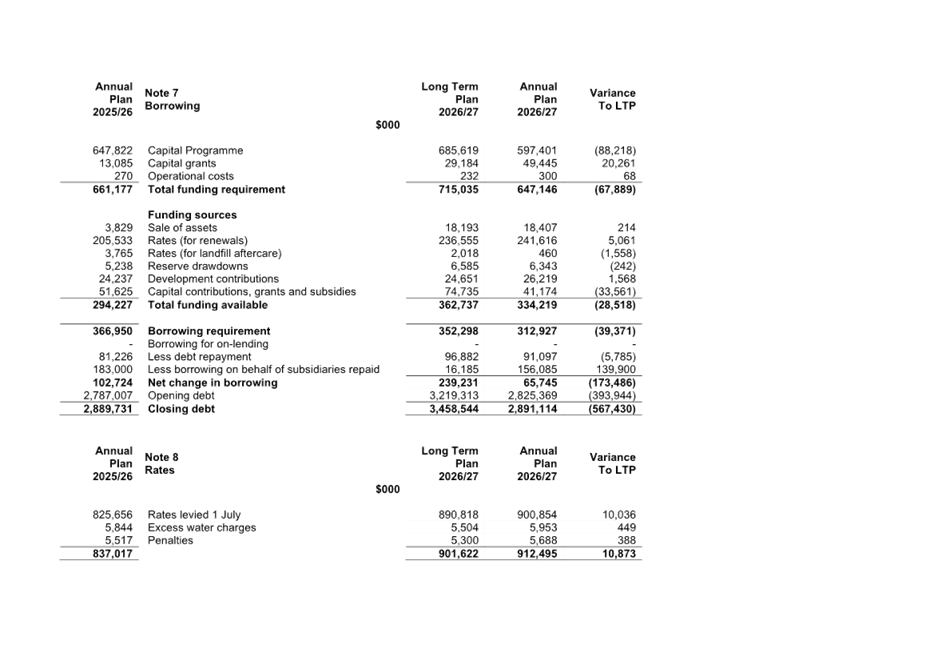

Rates

5.1 The

proposed draft Annual Plan 2026/27 includes an average overall rates increase

of 7.95% for 2026/27, compared to the LTP24-24 average overall rates increase

of 5.80% for 2026/27.

5.2 The

proposed draft Annual Plan 2026/27 average overall cumulative rates increase

since 2024/25 (first year of the LTP) is 26.47%, marginally higher than the

LTP24-34 cumulative rates increase of 26.13% by 2026/27.

5.3 A

general revaluation of rating units for rating purposes occurred as at August

2025 and will be effective for the 2026/27 year.

5.4 The

revaluation has increased overall capital values unevenly between rating

sectors with the overall average increases shown below:

|

Rating sector

|

2022 Average Capital

Value

|

2025 Average Capital Value

|

Overall Average Increase

|

|

Standard (Includes Residential)

|

830,000

|

845,000

|

1.8%

|

|

Business

|

2,490,000

|

2,734,000

|

9.8%

|

|

Remote Rural

|

1,910,000

|

1,905,000

|

-0.3%

|

5.5 Staff

note that many individual properties will have valuation changes that differ

materially from the above overall average.

5.6 As

a result of the above, the draft Annual Plan 2026/27 proposes an adjustment to

the value-based general rate business differential, decreasing the differential

from 2.220 to 2.000, to maintain the proportionality of rates charged to each

sector. Staff note that during the preparation of the 2023/24 Annual Plan,

Council increased the value-based general rate business differential from 1.697

to 2.220 to smooth the rates increase to standard (including residential) rate

payers incurred as a result of the 2022 rating revaluation and to maintain the

proportionality of rates charged to each sector. The recommended change to the

business differential partially reverses the previous change.

5.7 An

average overall rates increase of 7.95% to existing ratepayers is estimated to

translate to the following rating sector increases for an average capital value

property in that sector:

|

|

Existing Business

Differential (2.220)

|

Proposed Business

Differential (2.000)

|

|

Rating sector

|

Rates % Increase

|

Weekly $ Increase

|

Rates % Increase

|

Weekly $ Increase

|

|

Standard (Includes Residential)

|

5.5%

|

$ 4.48

|

7.4%

|

$ 6.05

|

|

Business

|

14.3%

|

$ 53.99

|

8.7%

|

$ 33.09

|

|

Remote Rural

|

4.6%

|

$ 3.54

|

8.0%

|

$ 6.19

|

5.8 Staff

also note that technical updates have been made to the Funding Impact Statement

– Rating Information (Attachment C), updating the definition of

short-term accommodation in relation to the business differential to remove the

minimum 60-day requirement.

5.9 Minor

updates have been made to the Rates Remissions Policy (Attachment E),

affecting the date to which the remission for a new claim on an

earthquake-damaged property will be back dated.

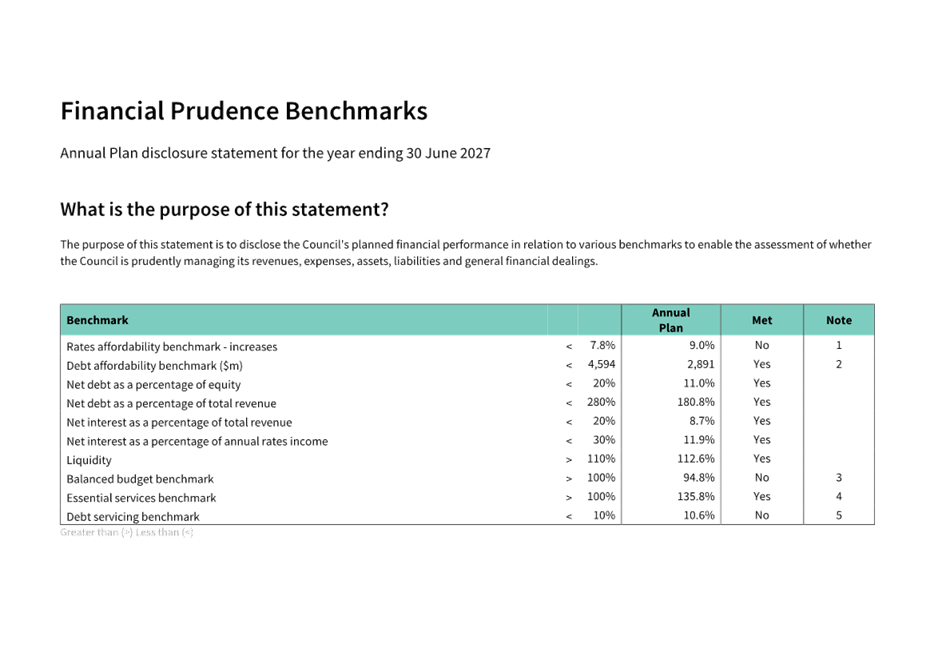

Financial Prudence Benchmarks

5.10 In

relation to the Financial Prudence Benchmarks, the Council will not meet the

following:

5.10.1 The

Rates Affordability benchmark

· Benchmark

<7.8%, Annual Plan 2026/27 9.0%.

· The Council

meets the rates affordability benchmark if its planned rates increase for the

year equals or is less than each quantified limit on rates increases.

· The Council

has not met this benchmark for 2026/27 with the rates increase for 2026/27

being 1.2% higher than the quantified limit. The 2025/26 Annual Plan rates

increase was reduced (2.06%) using some of the 2024/25 operating surplus. This

was a temporary saving which effectively moved the increase to the 2026/27

year.

5.10.2 The

Balanced Budget benchmark in 2026/27 (as indicated in the LTP).

· Benchmark

>100%, Annual Plan 2026/27 94.8%.

· The Council

meets the balanced budget benchmark if its revenue equals or is greater than

its operating expenses.

· The Council

has not met this benchmark for 2026/27 as was forecast in the LTP24/34. This is

a result of the delay in the increase to Rating for Renewals in the Long Term

Plan to assist in managing the level of planned rates increases.

5.10.3 The

Debt Servicing benchmark (as indicated in the LTP)

· Benchmark

<10%, Annual Plan 2026/27 10.6%.

· The Council

meets the debt servicing benchmark if its planned borrowing costs equal or are

less than 10% of its planned revenue.

· The Council

has not met this benchmark for 2026/27 as was forecast in the LTP24/34. This

benchmark includes interest costs relating to debt that is on-lent to

subsidiaries and funded by them, and it accounts for 12.6% of Council’s

interest costs, without which the Council’s ratio would by 9.4%. There is

no concern around Council’s ability to service debt.

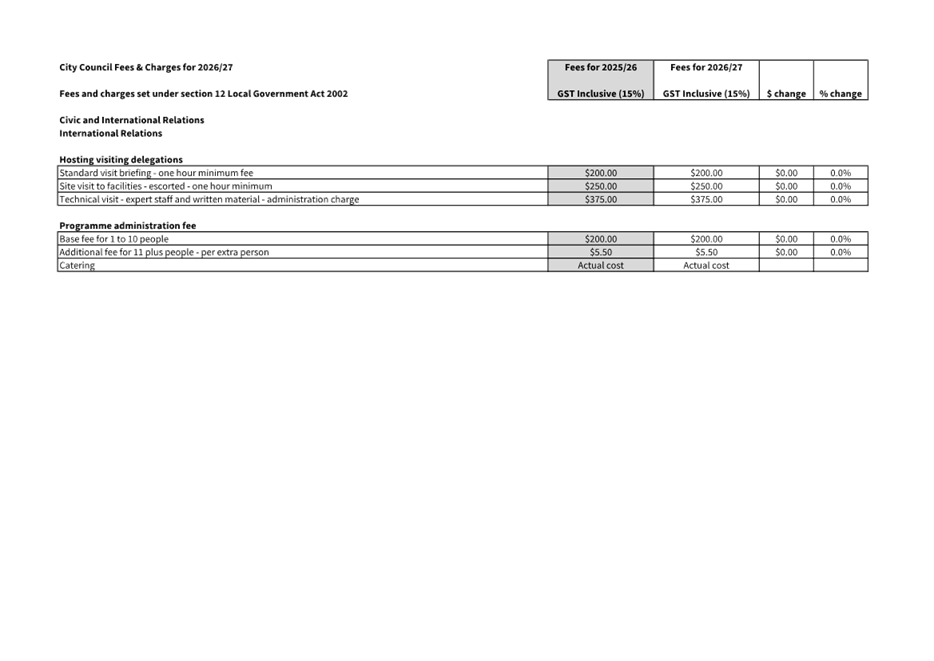

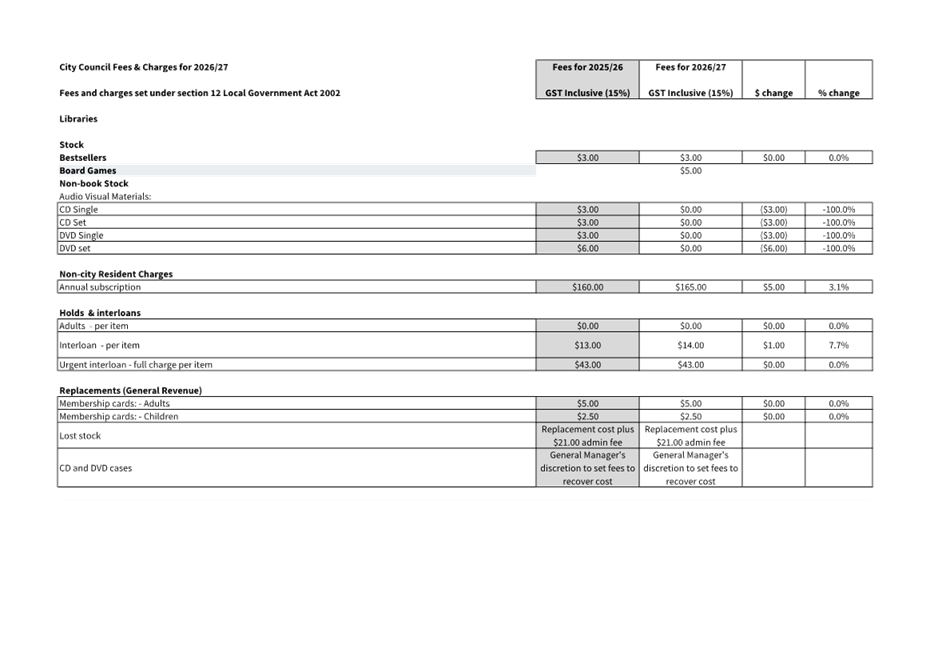

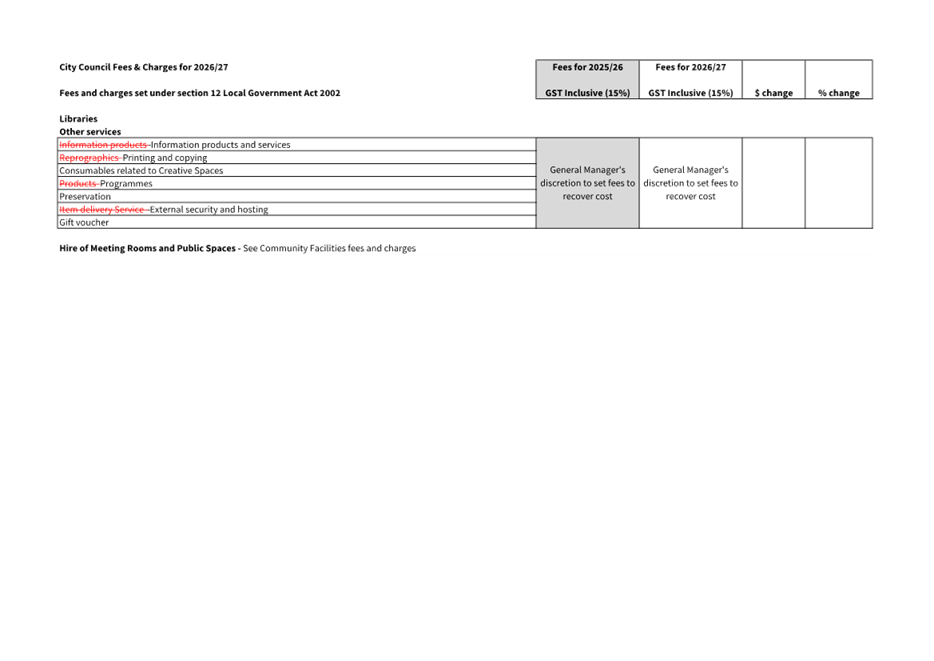

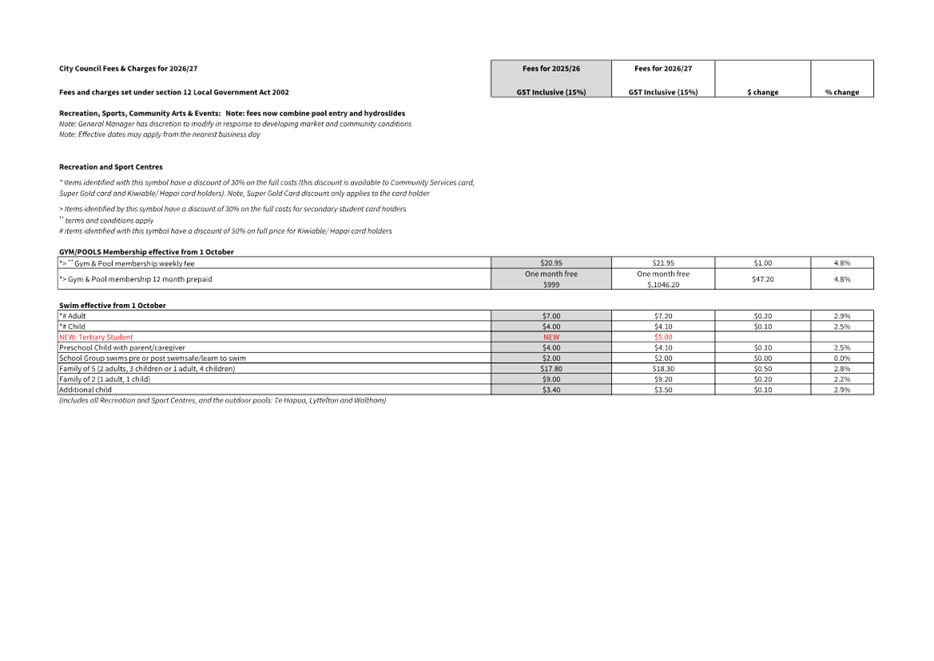

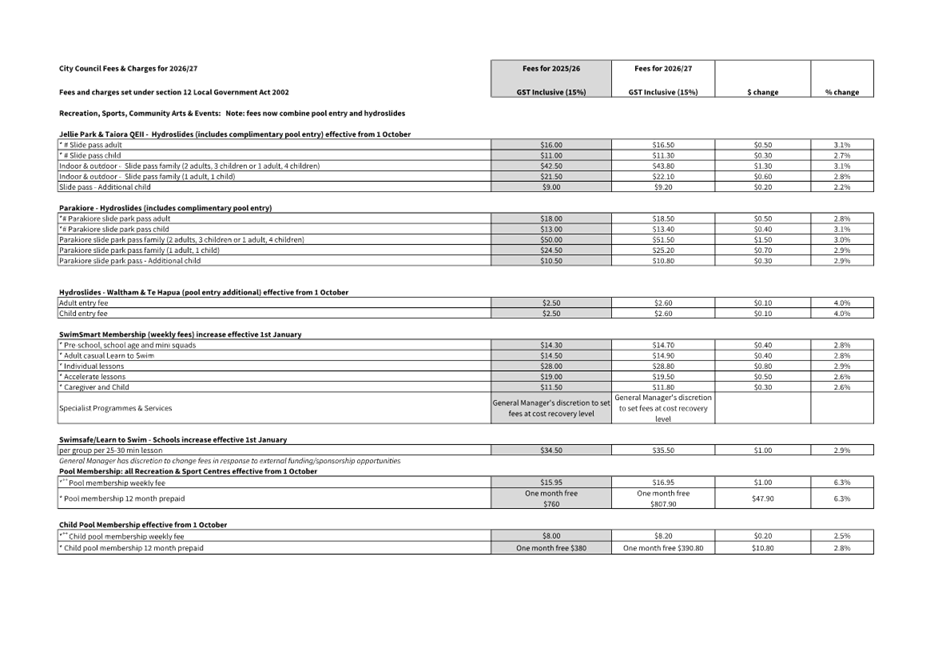

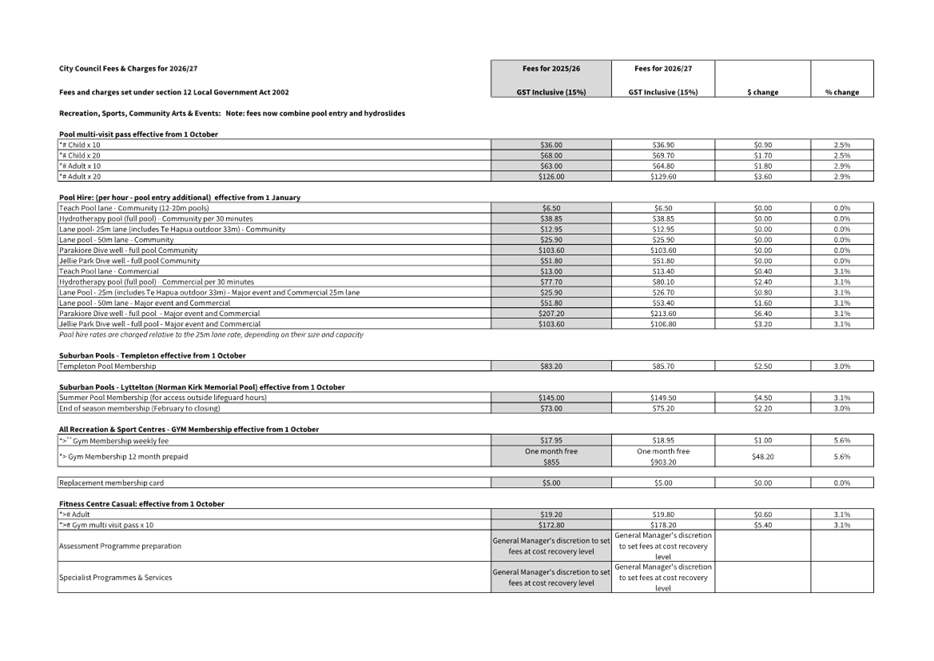

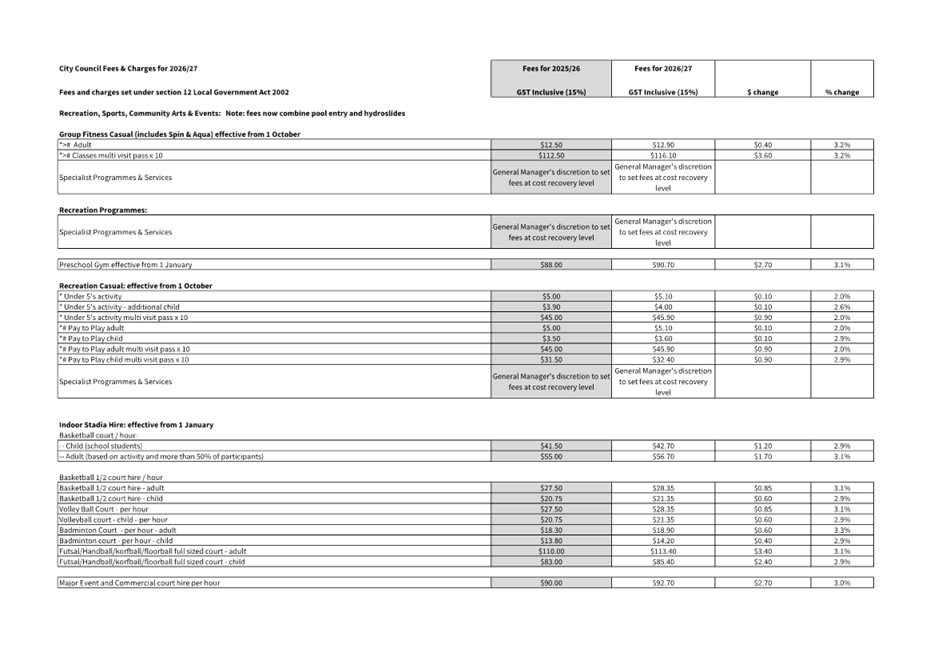

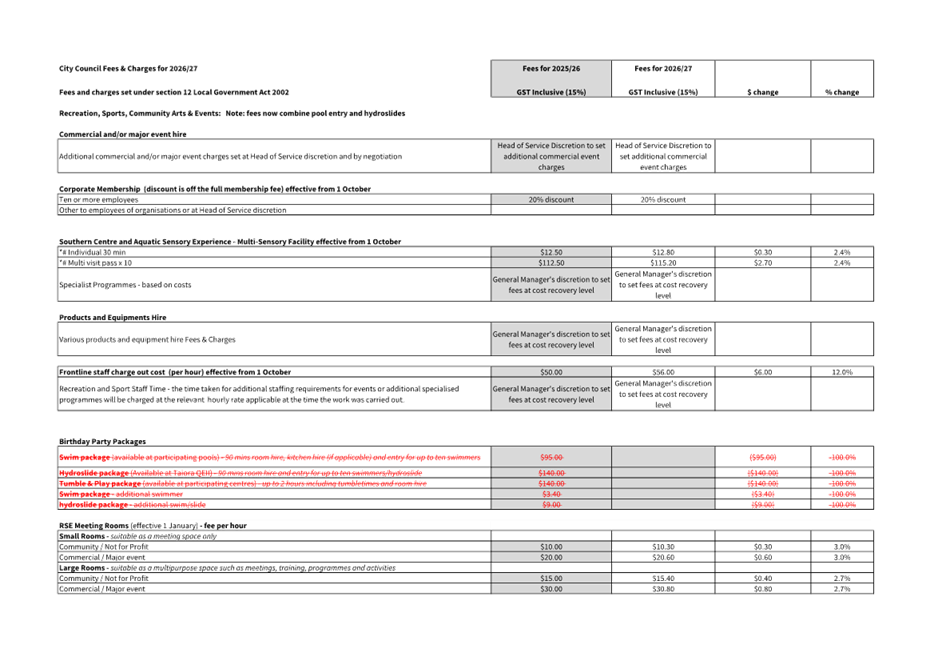

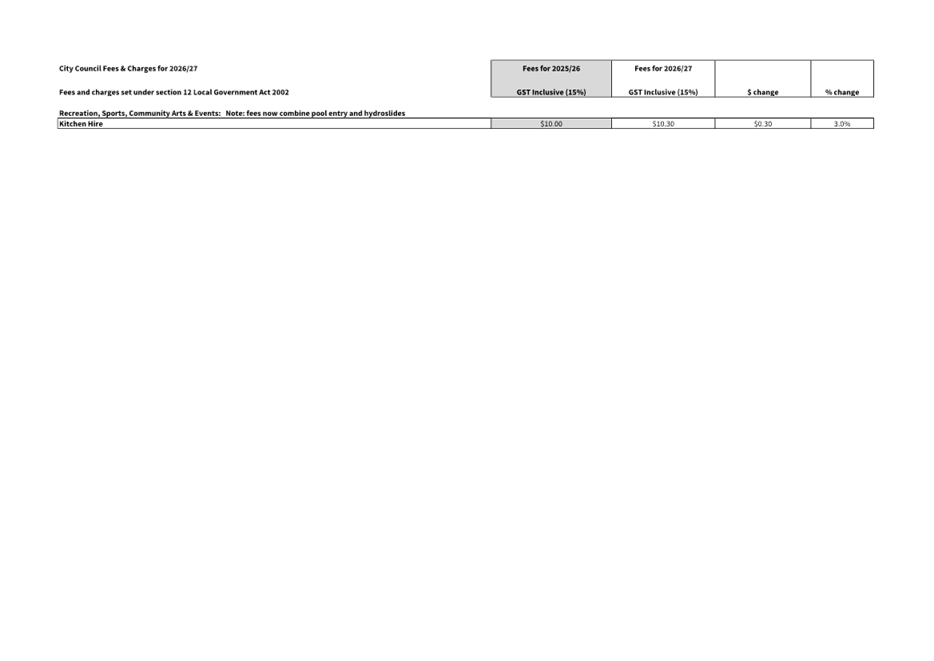

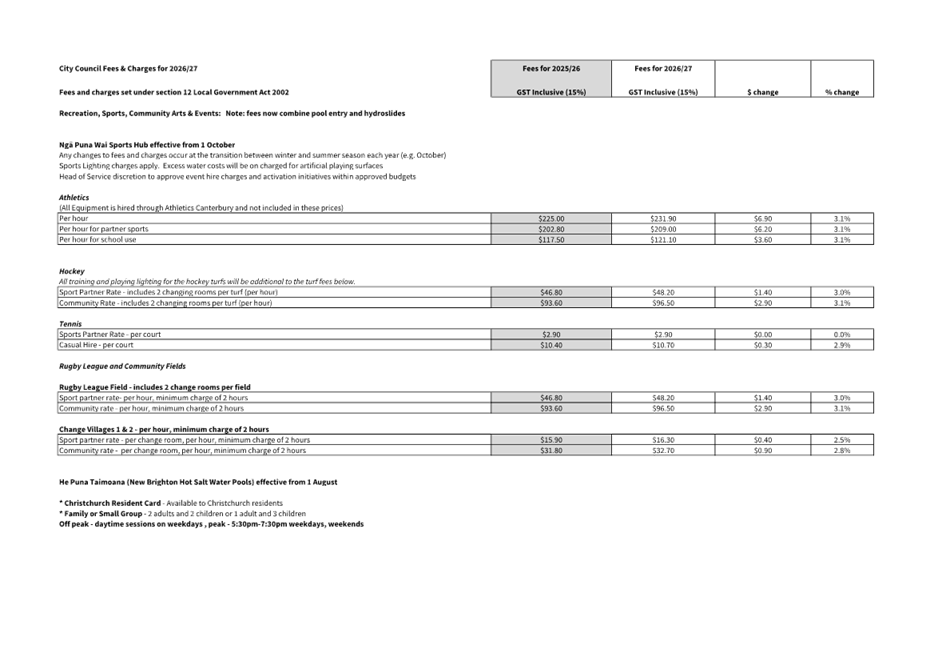

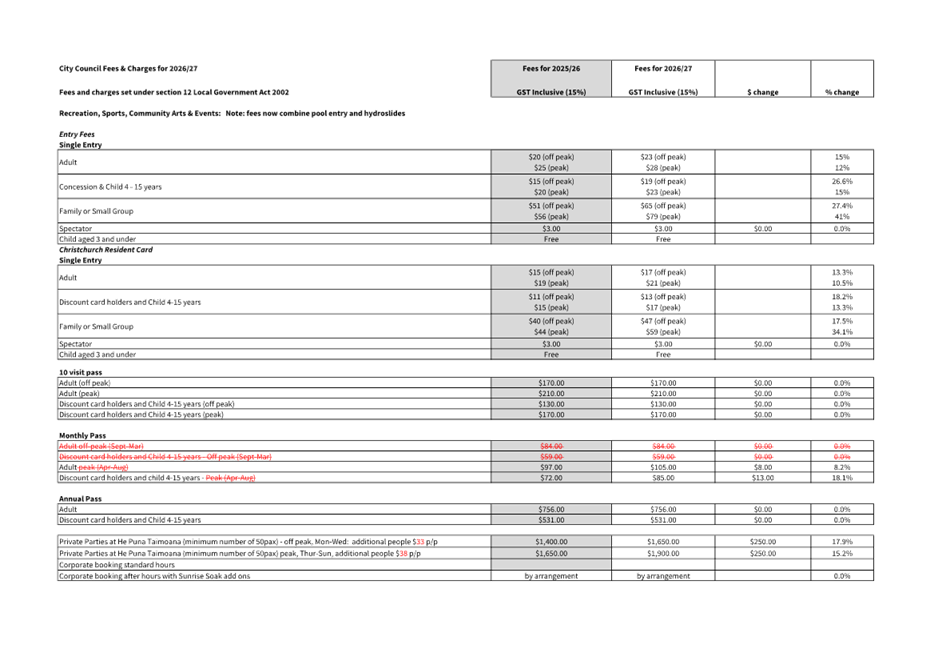

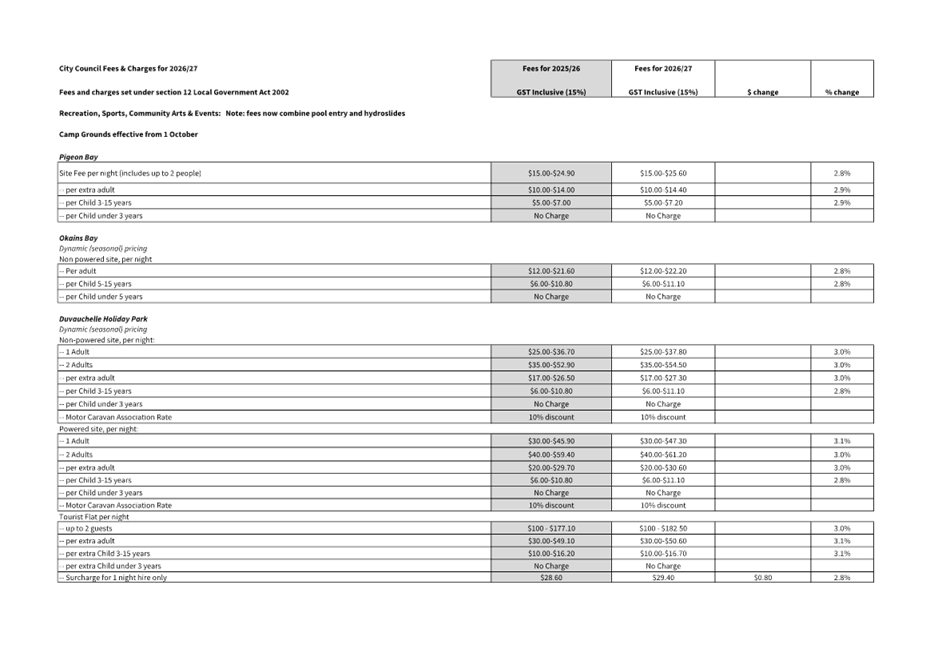

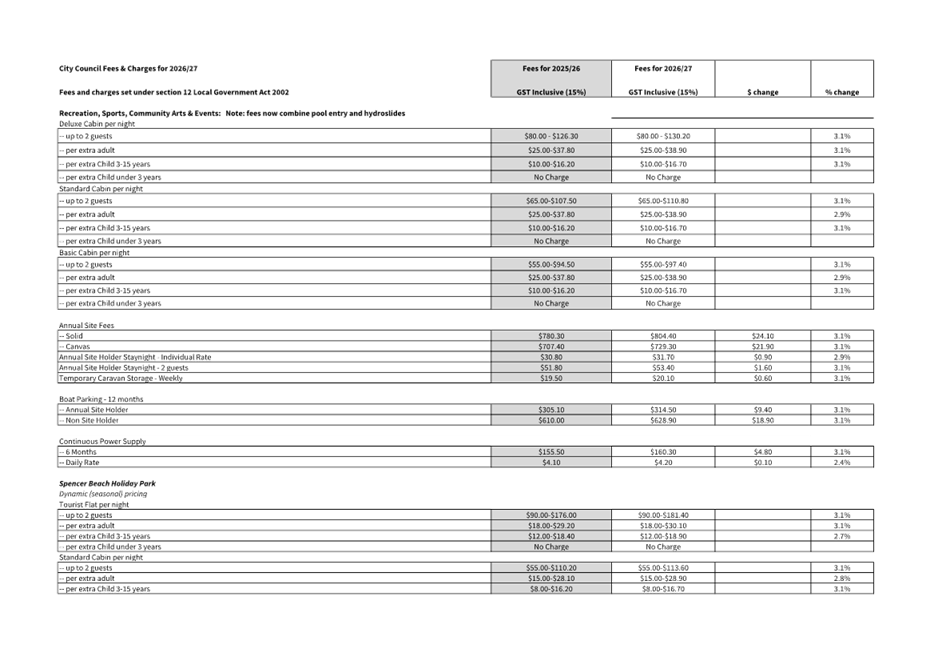

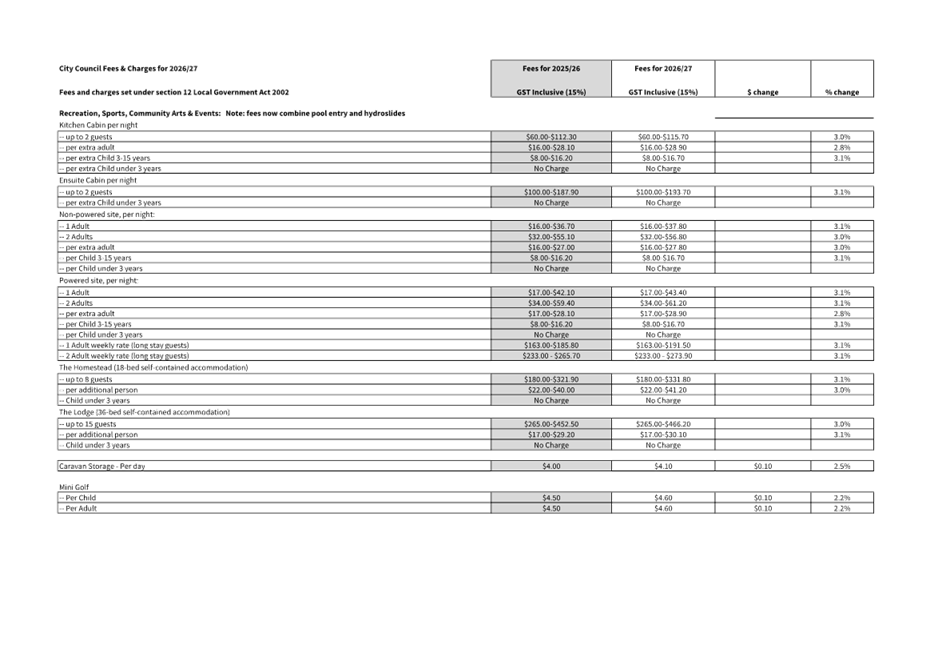

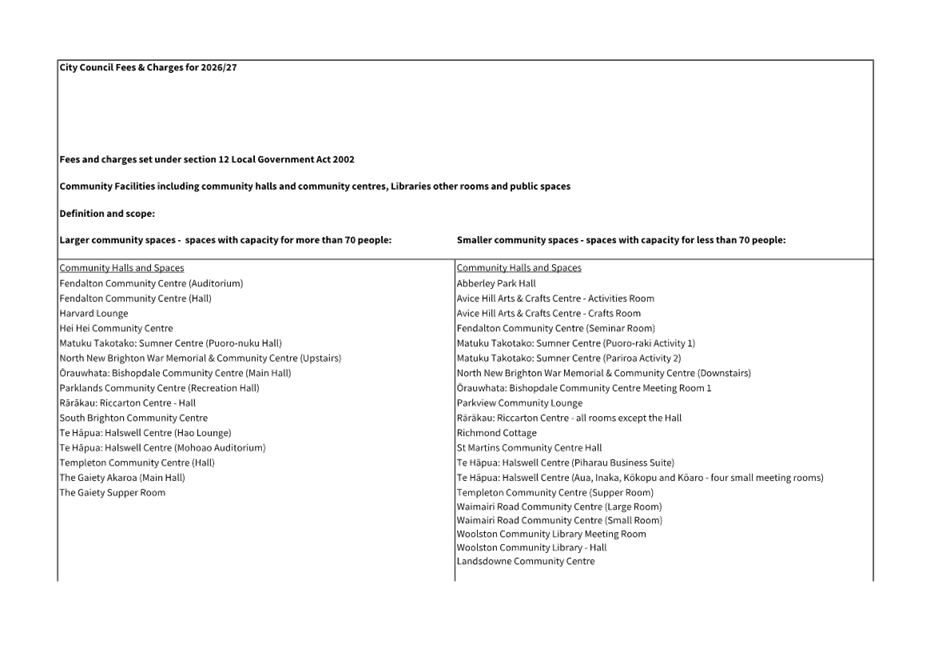

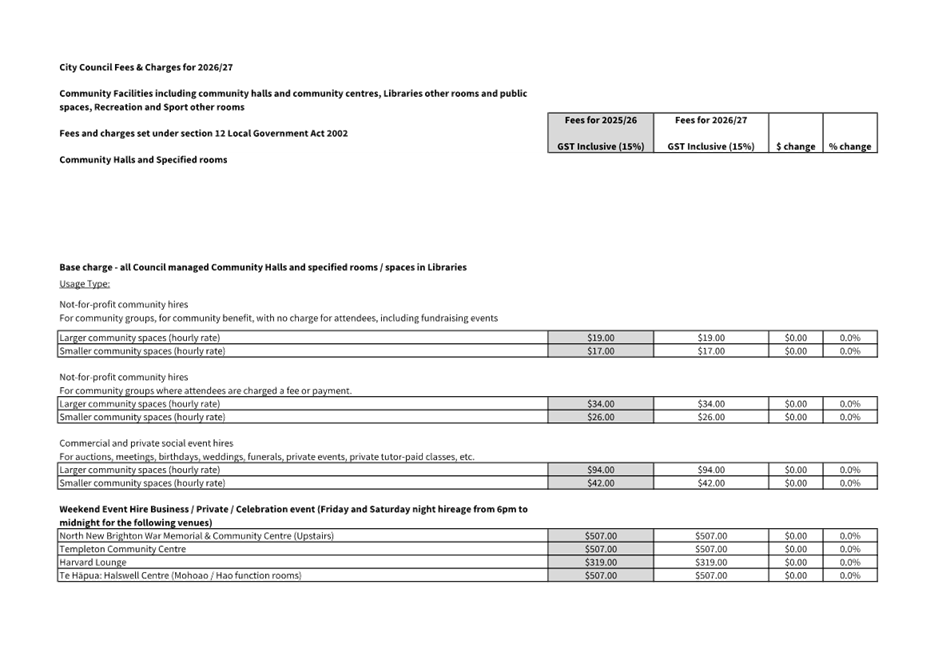

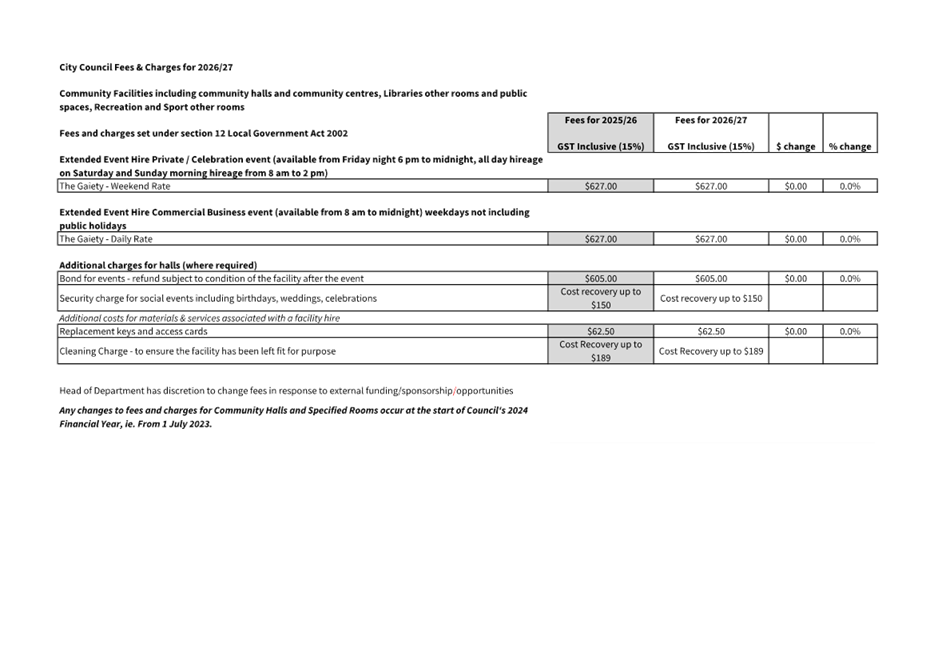

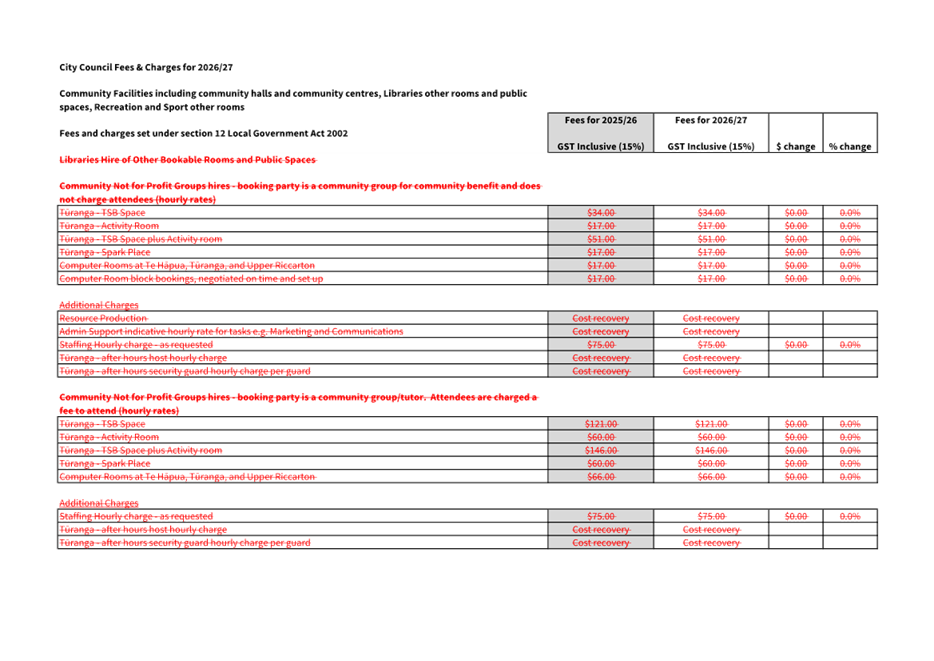

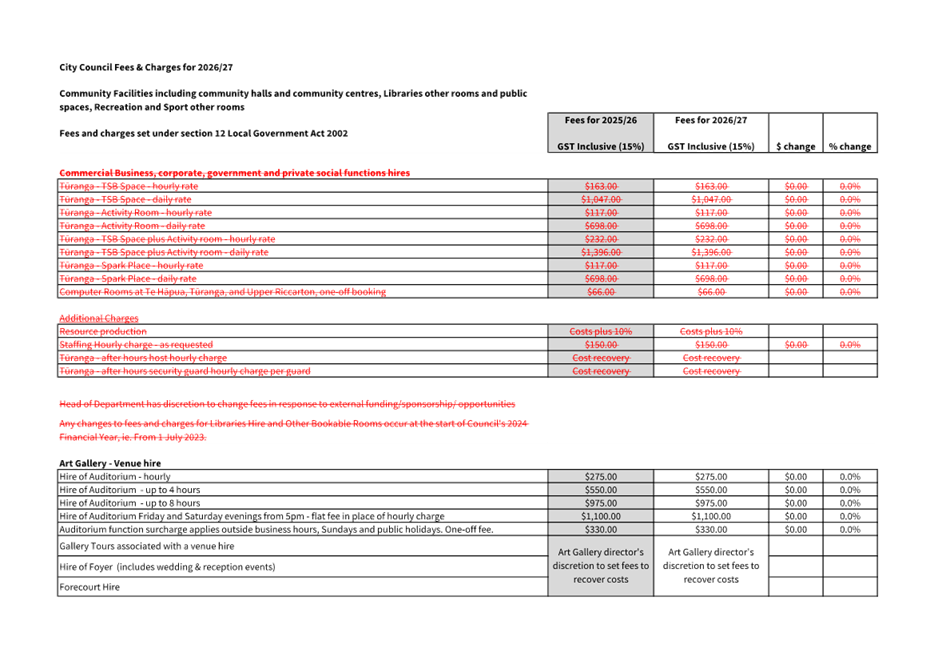

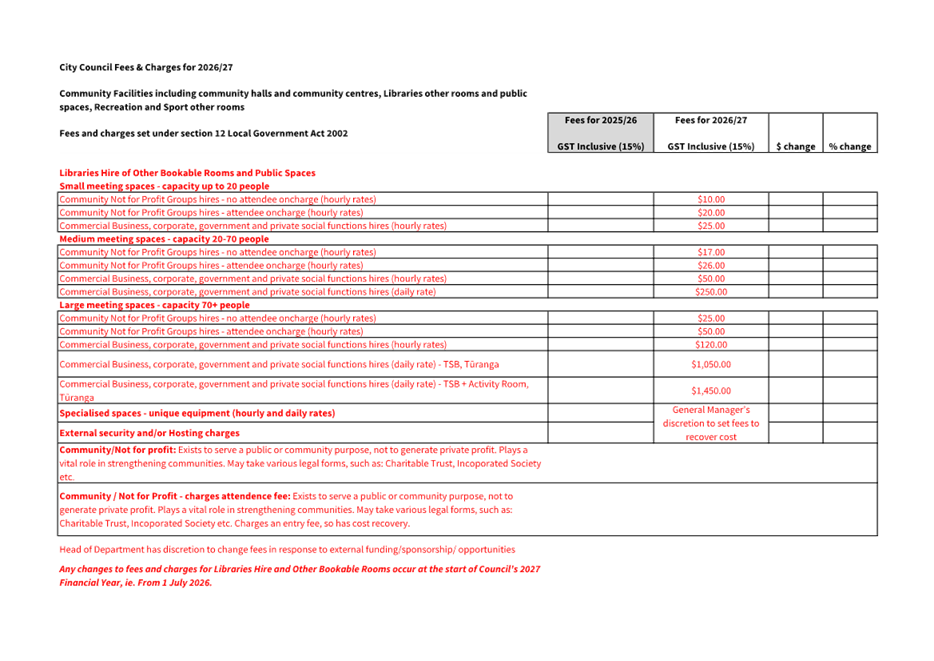

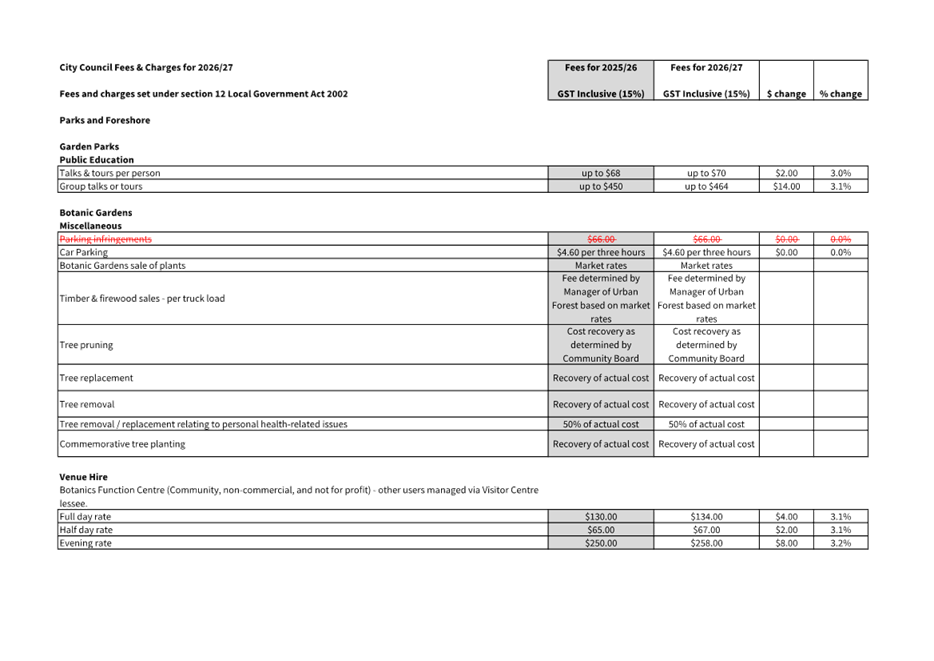

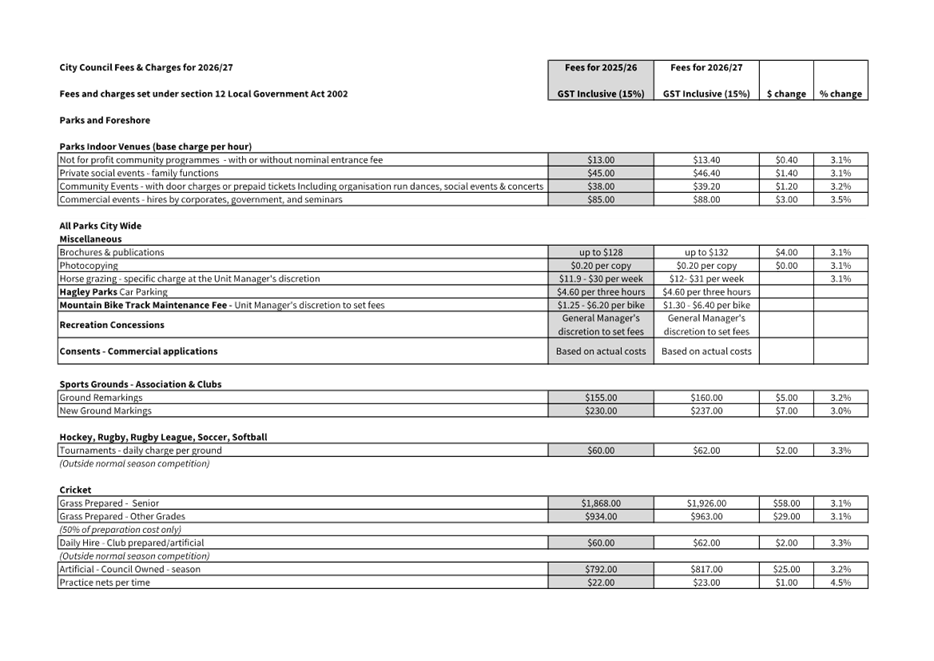

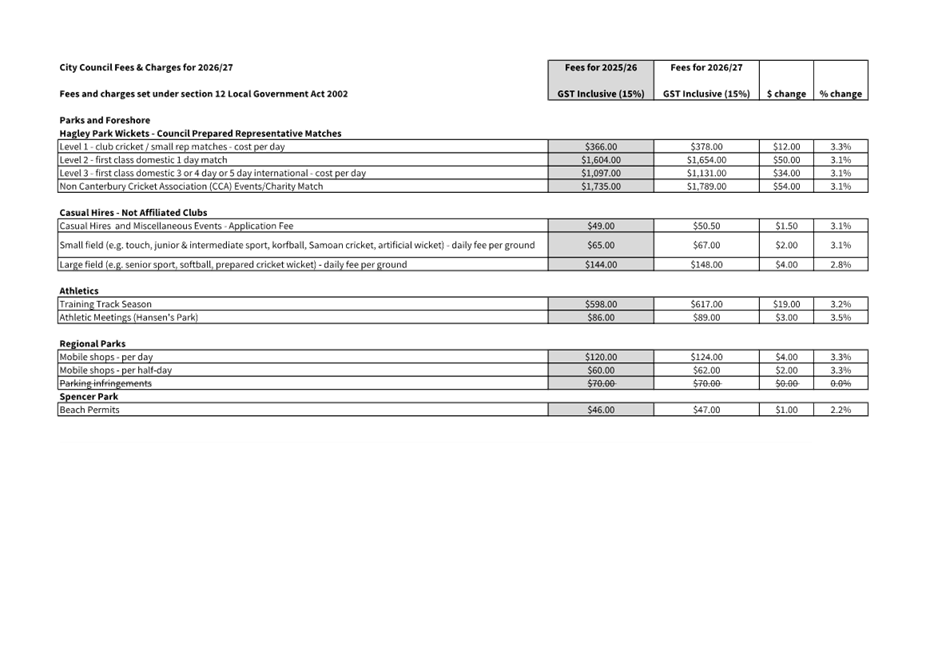

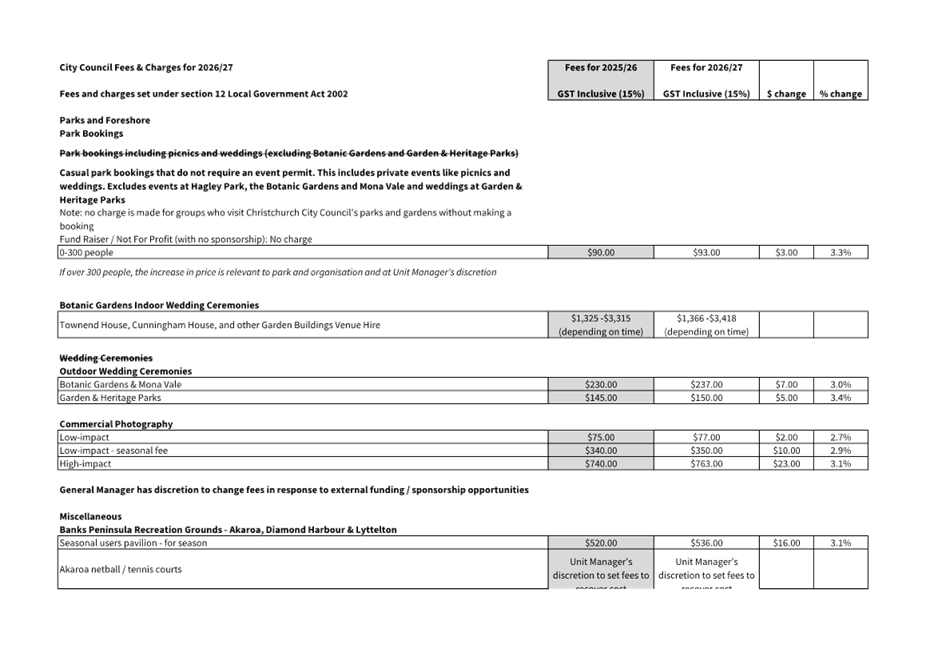

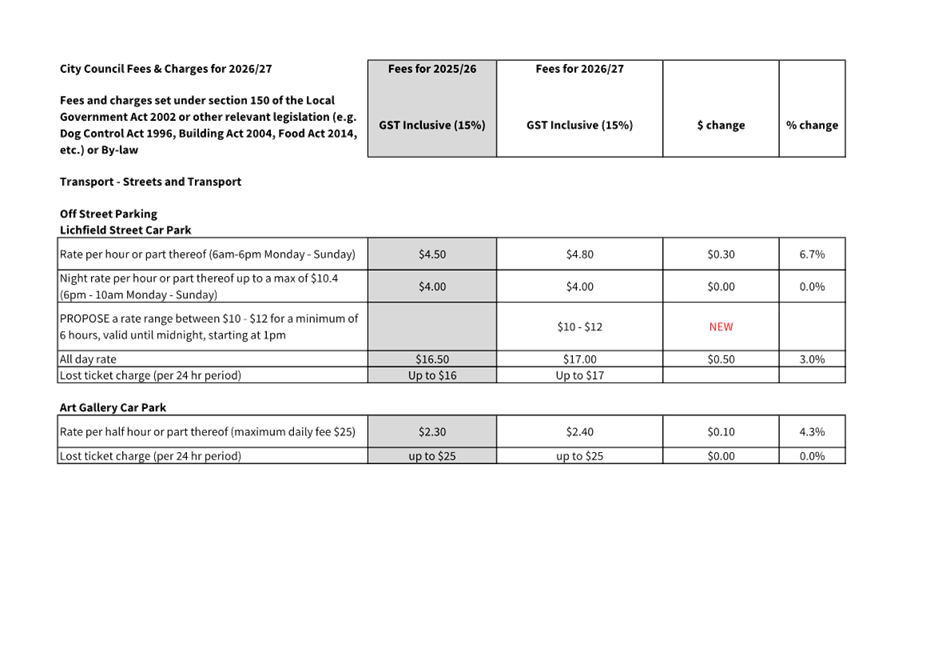

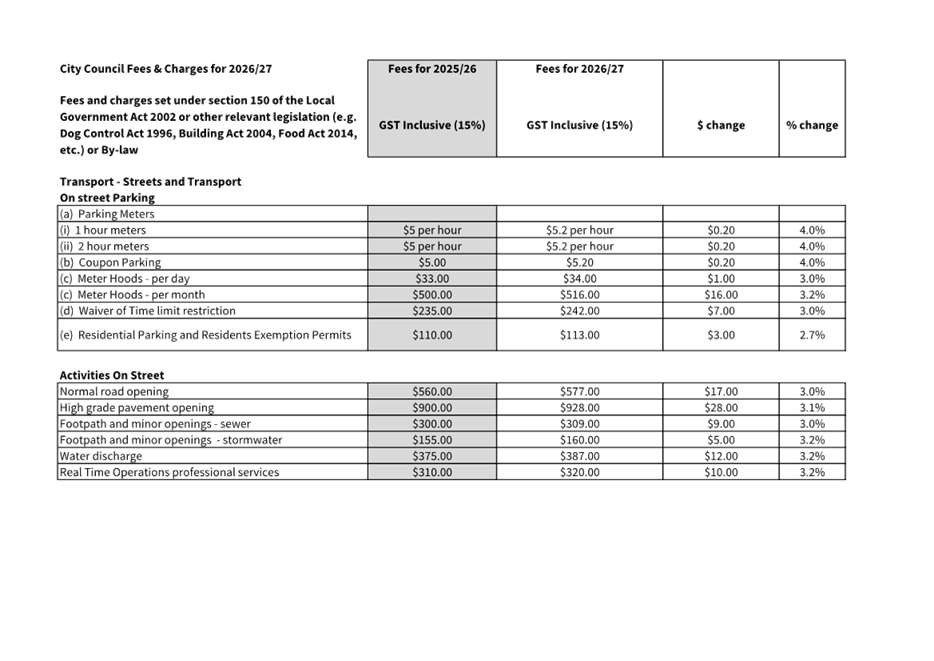

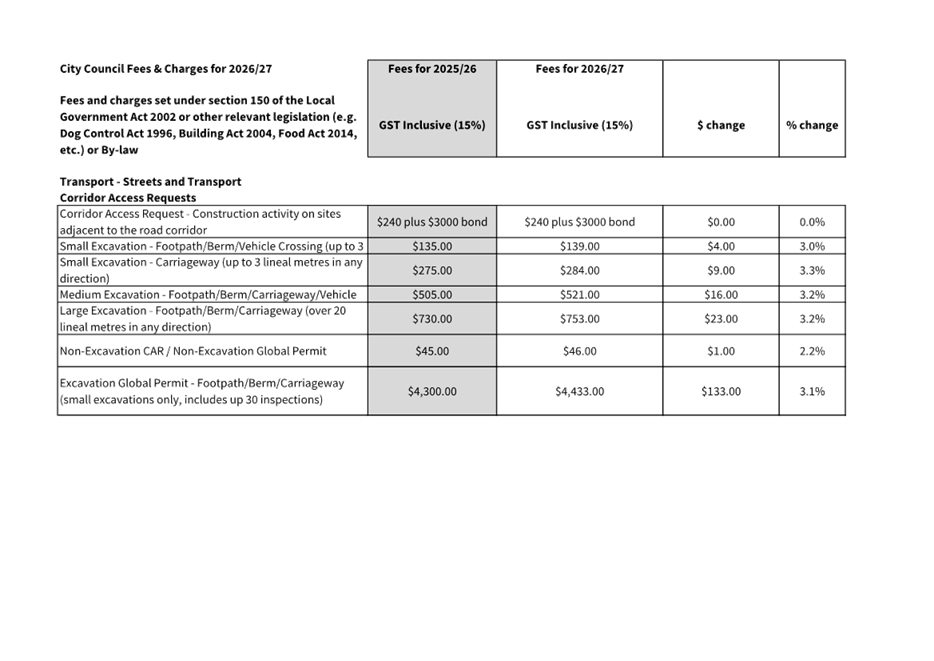

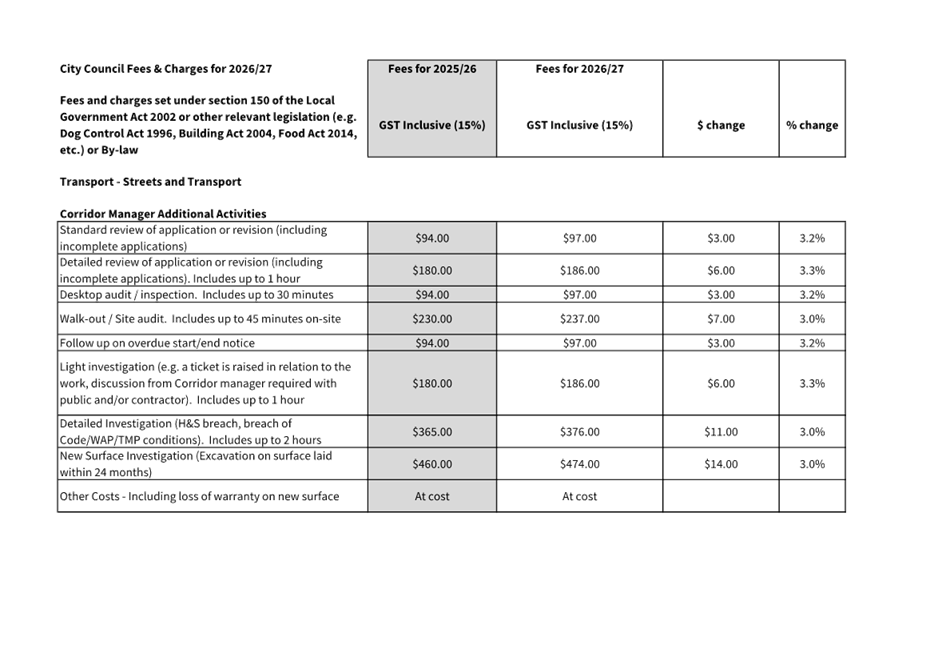

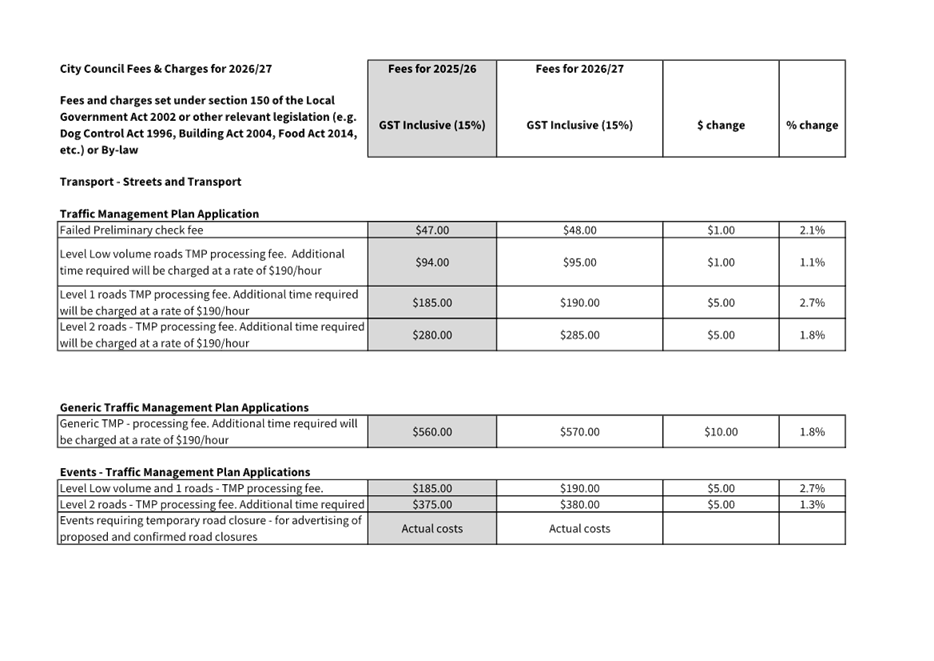

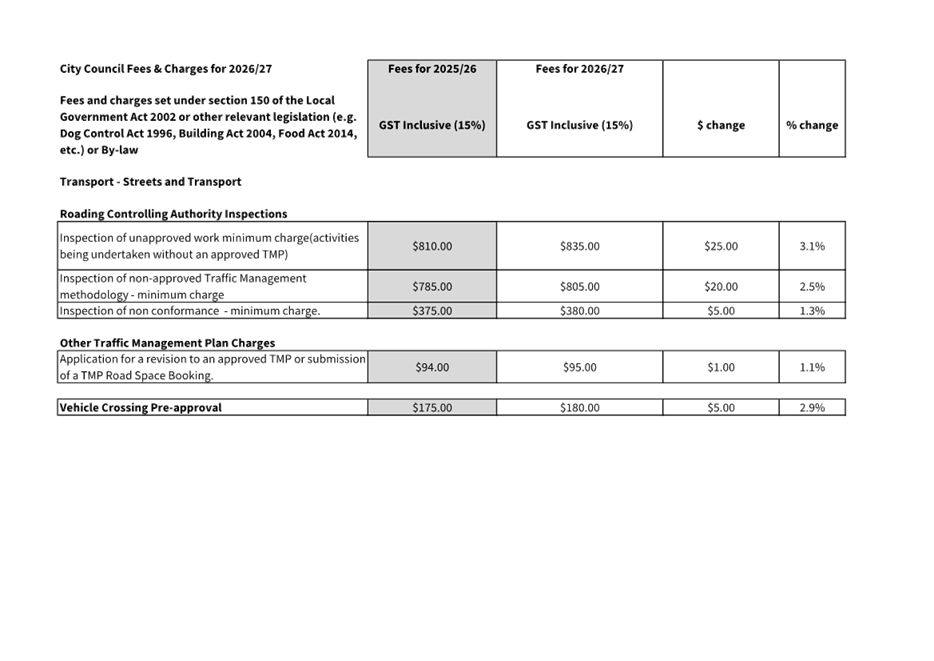

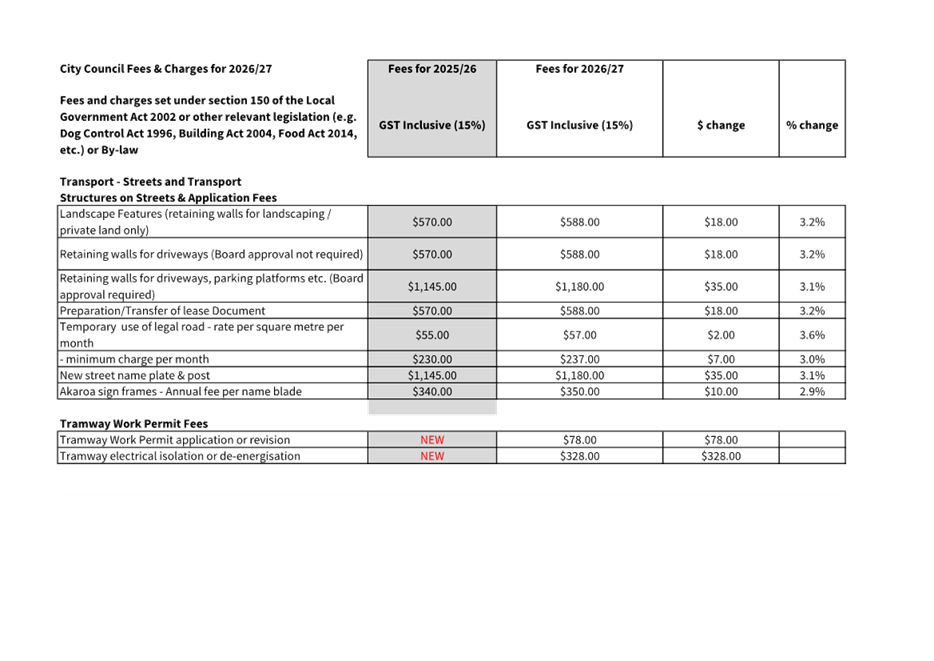

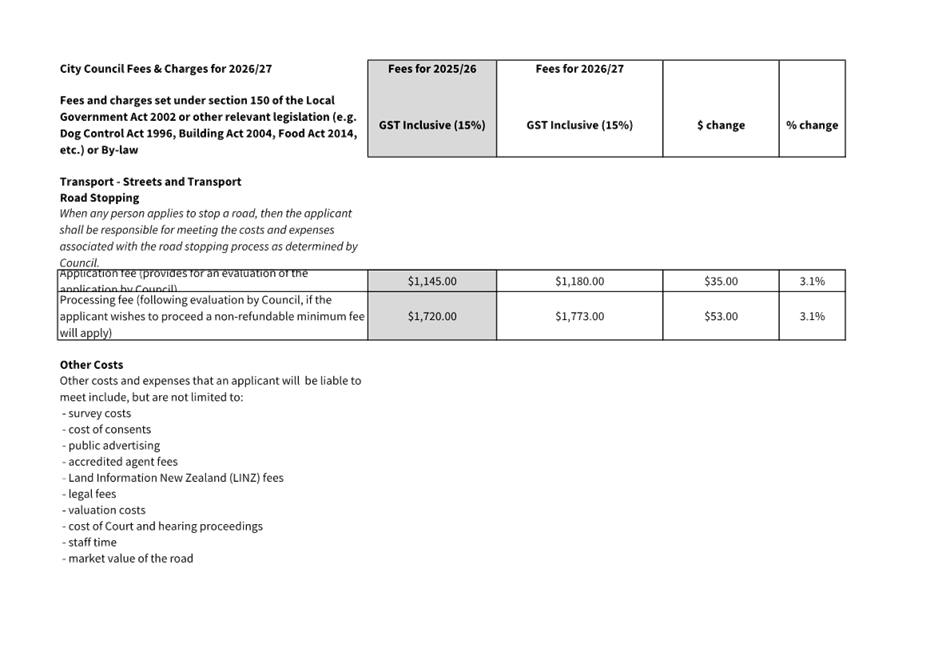

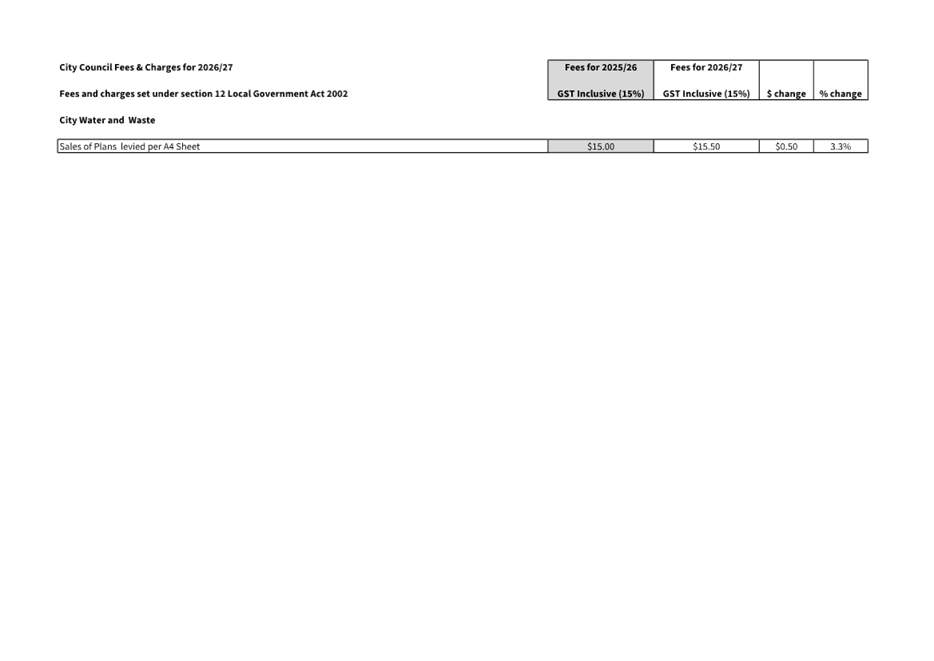

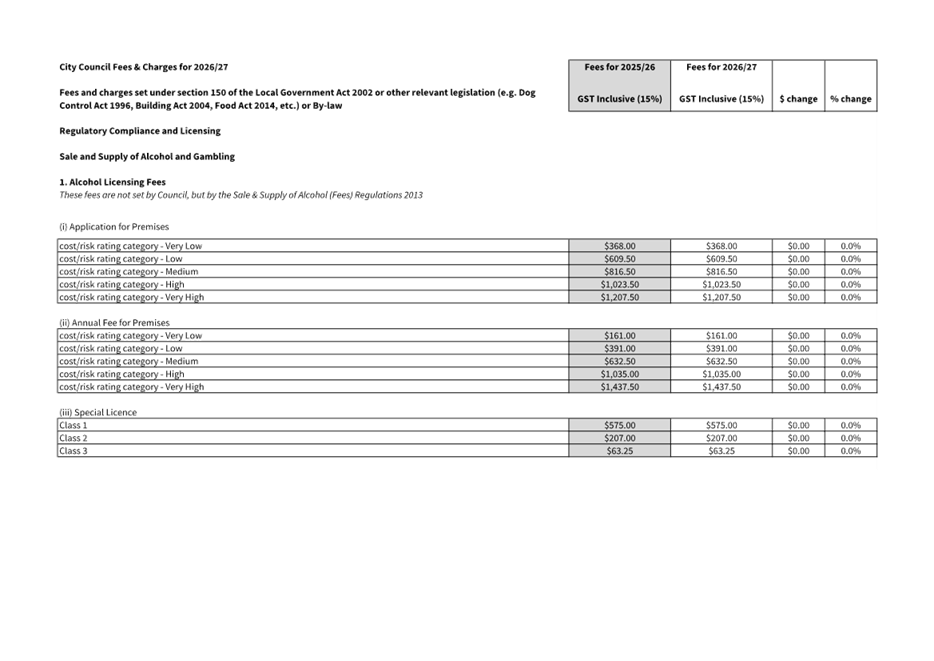

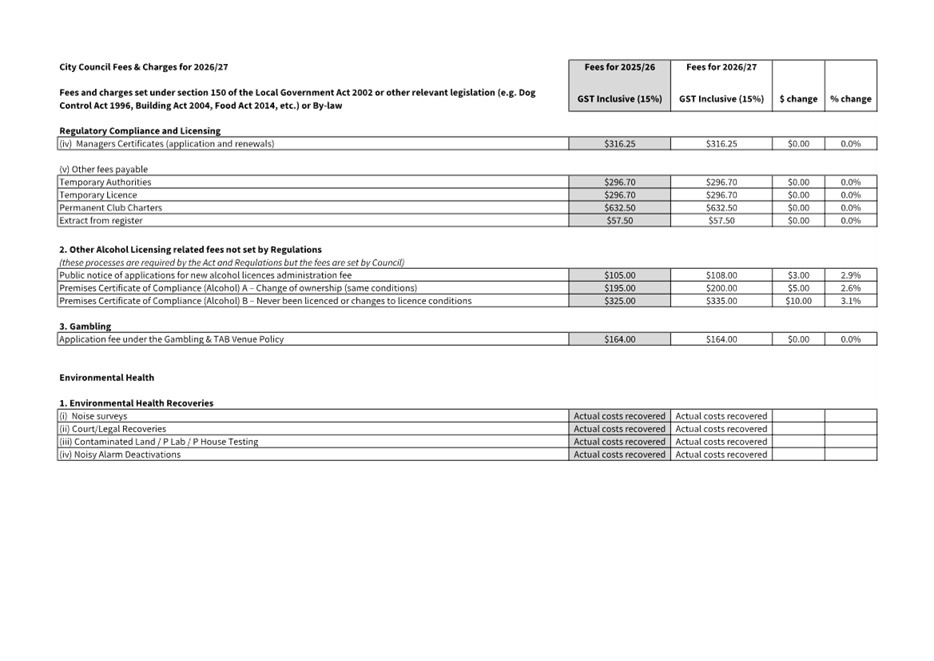

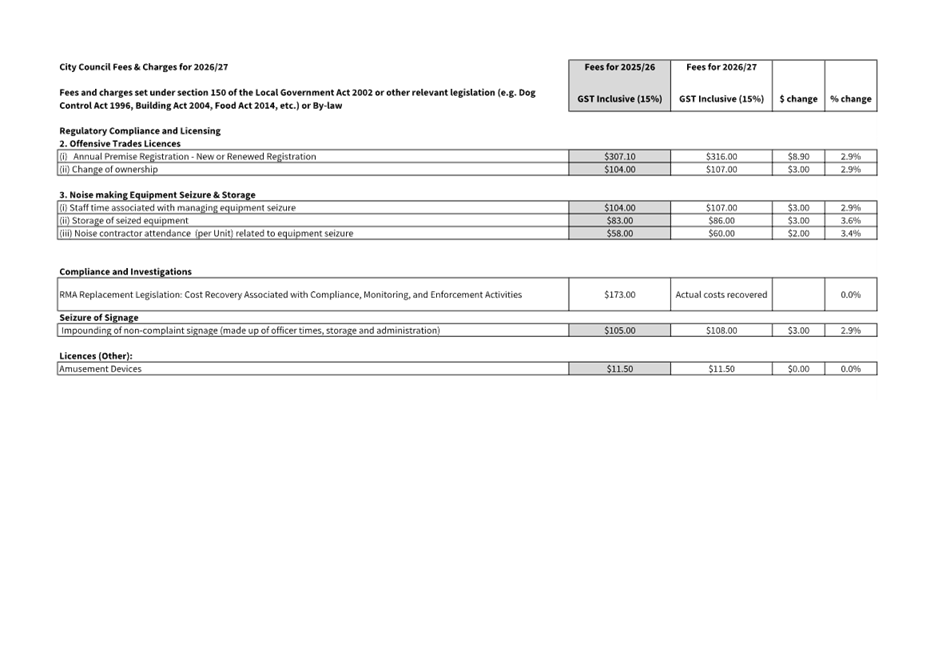

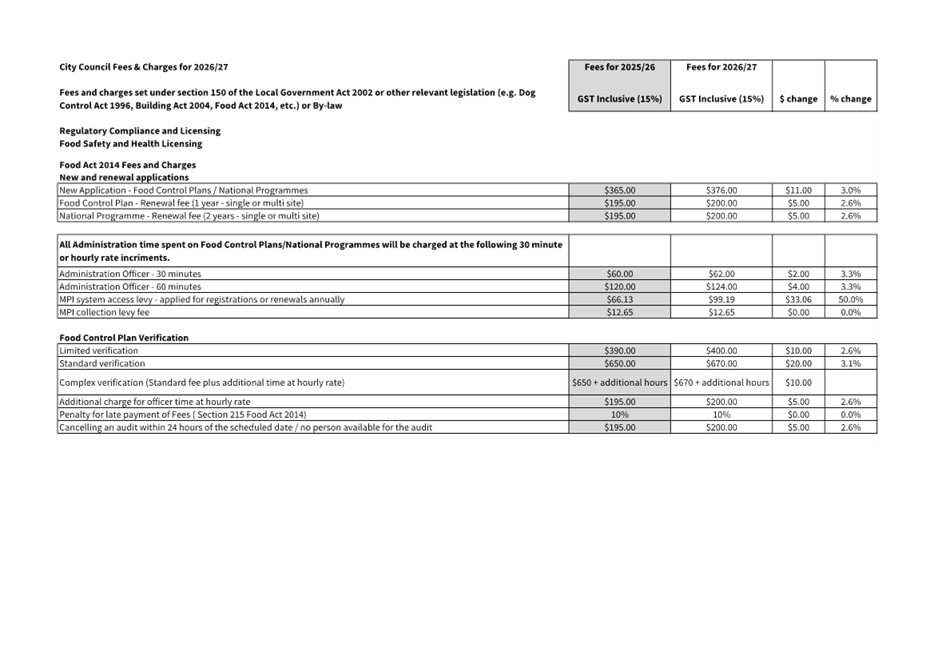

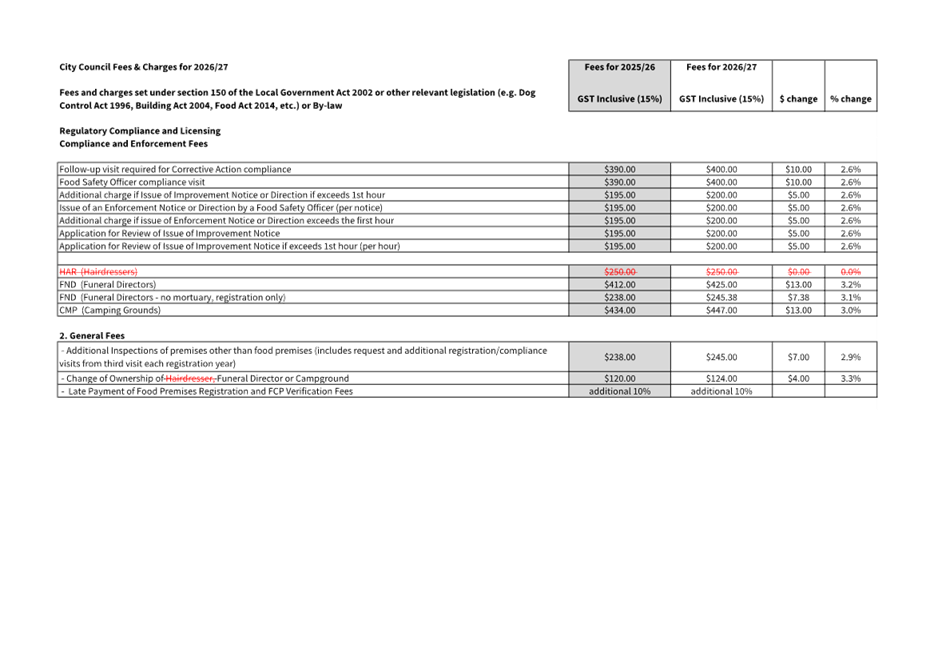

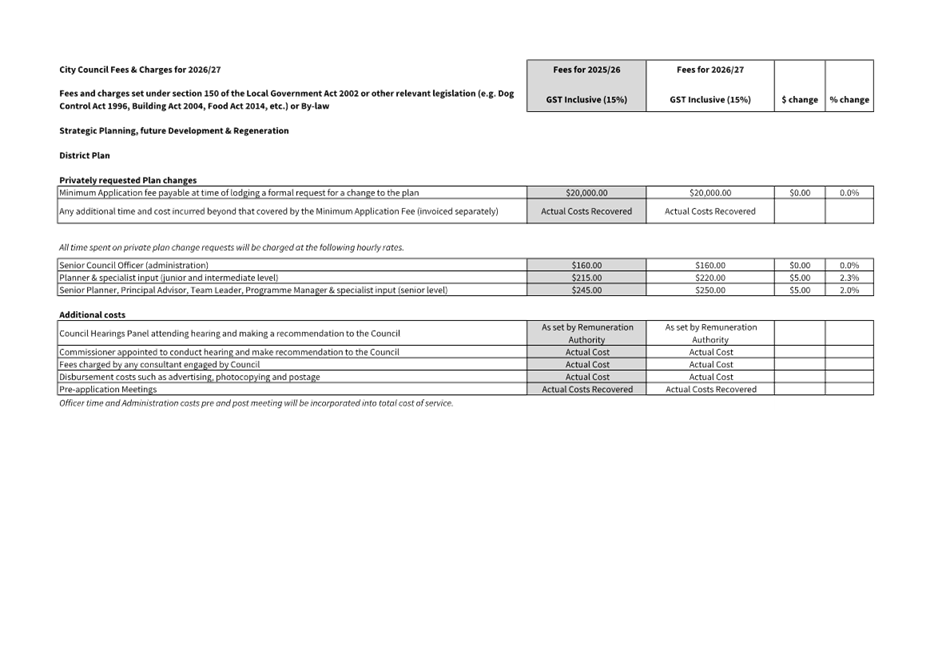

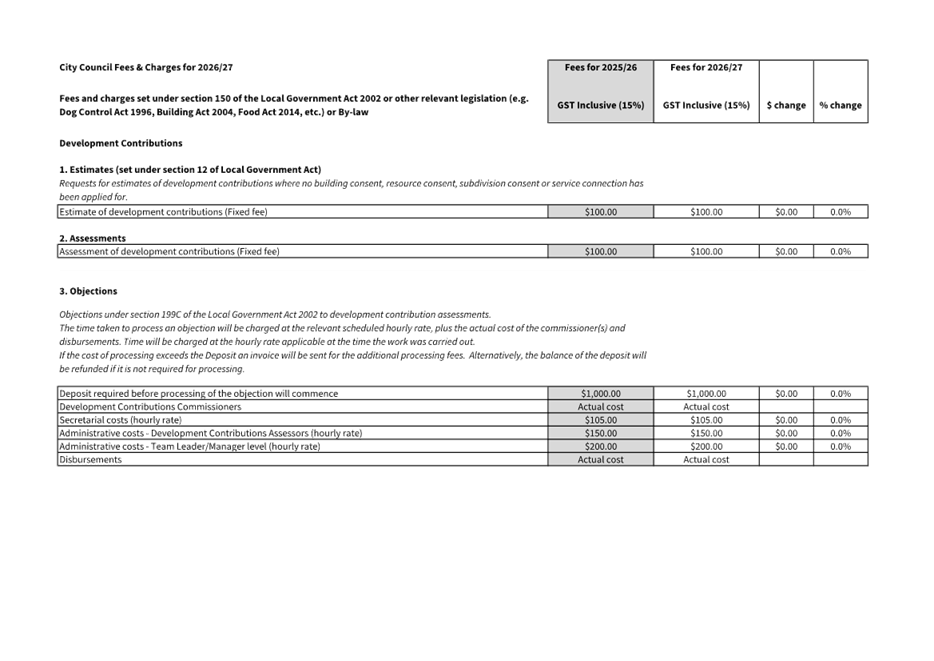

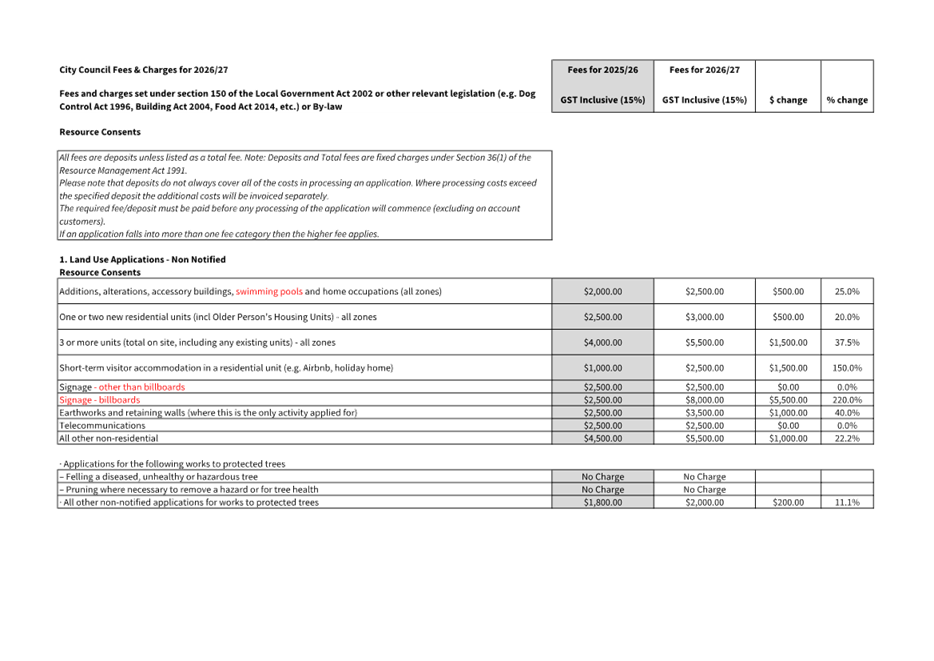

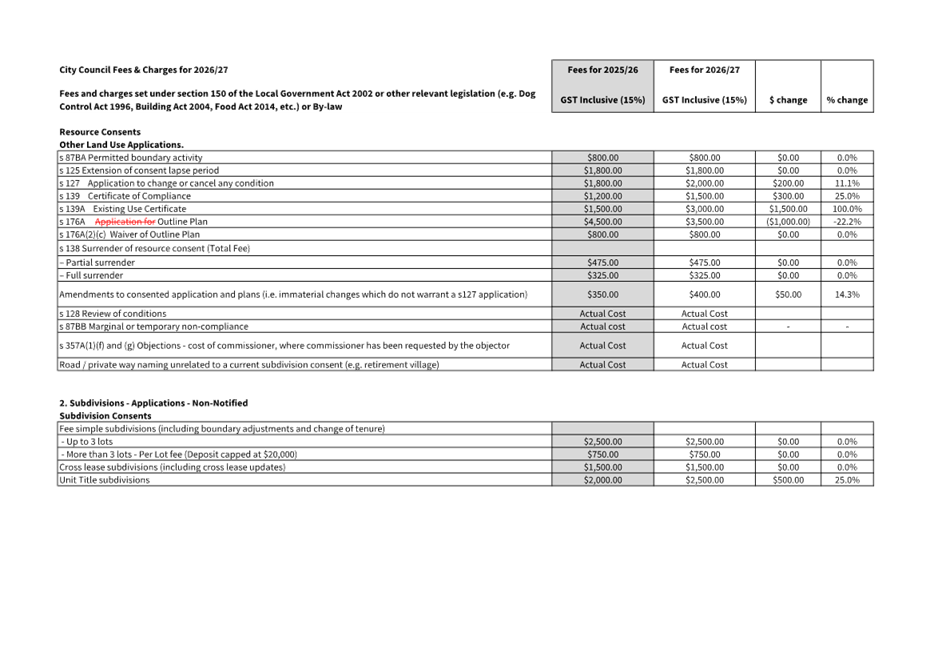

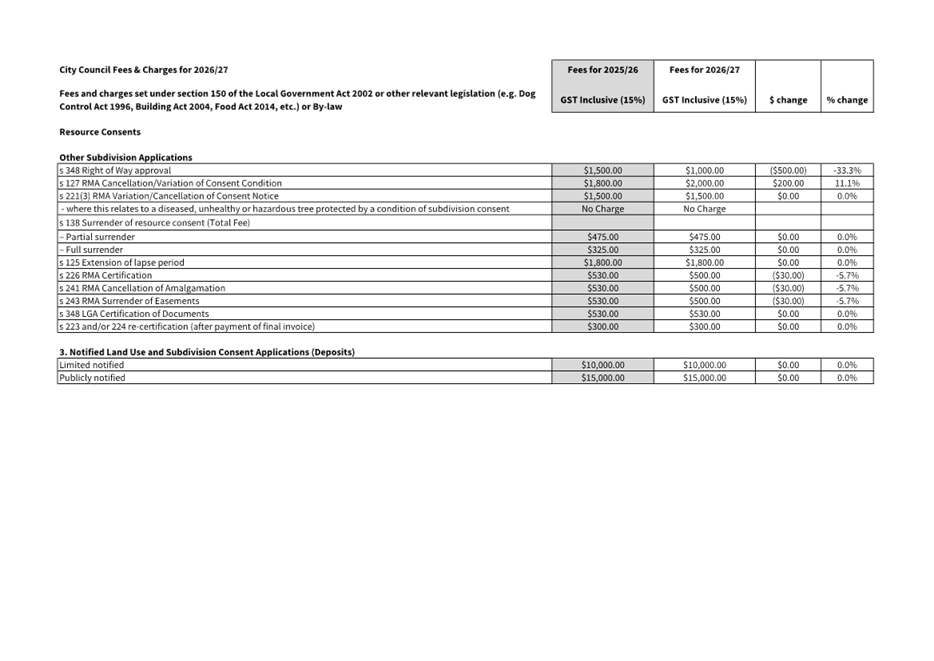

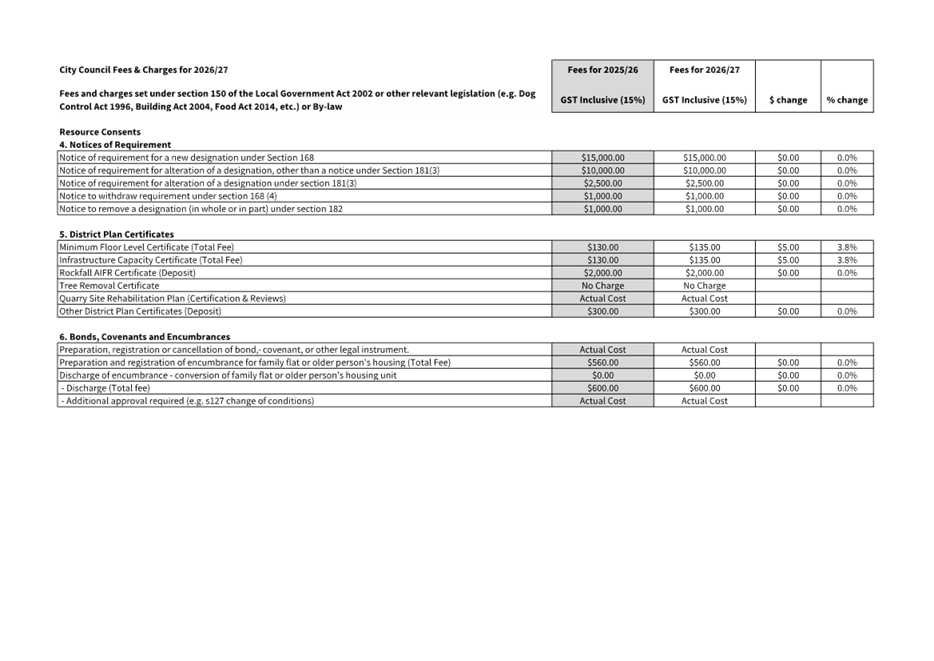

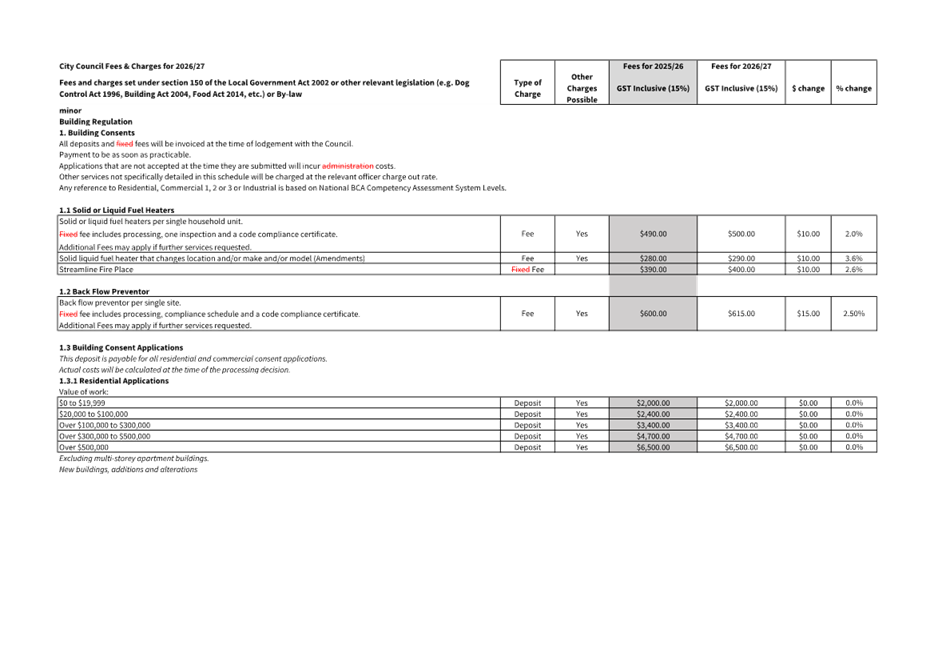

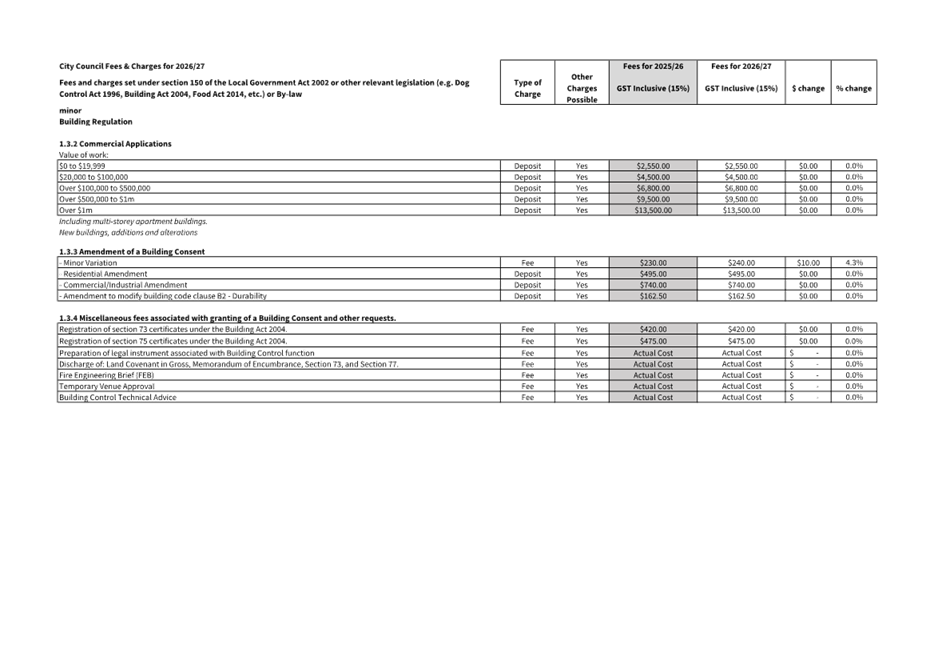

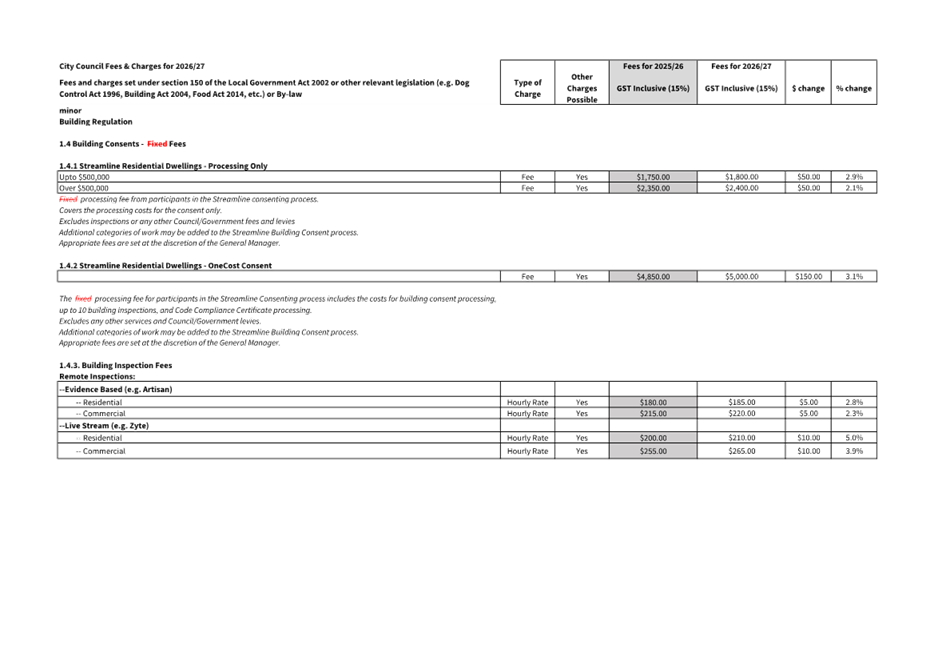

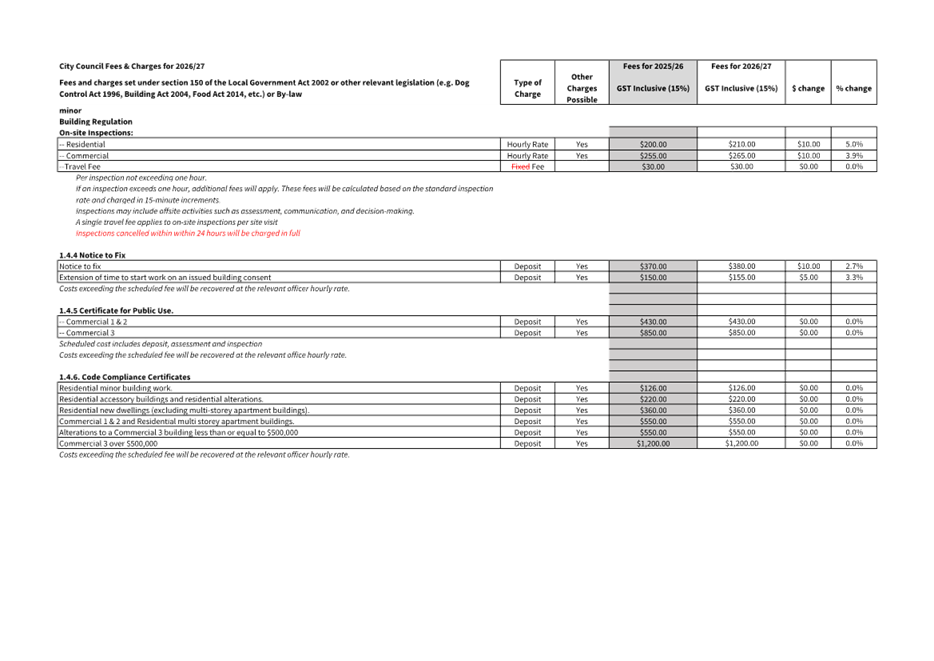

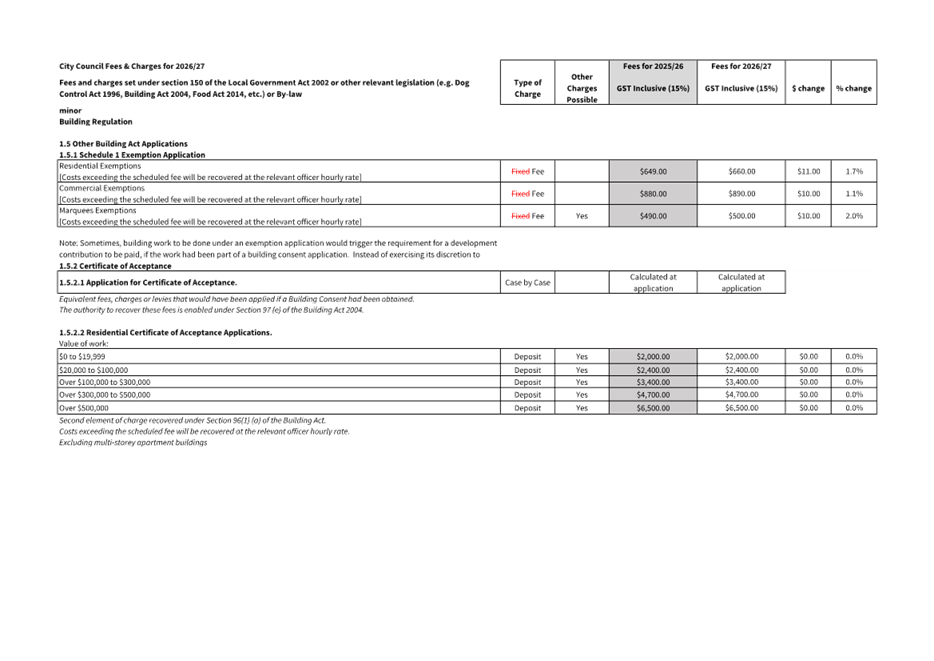

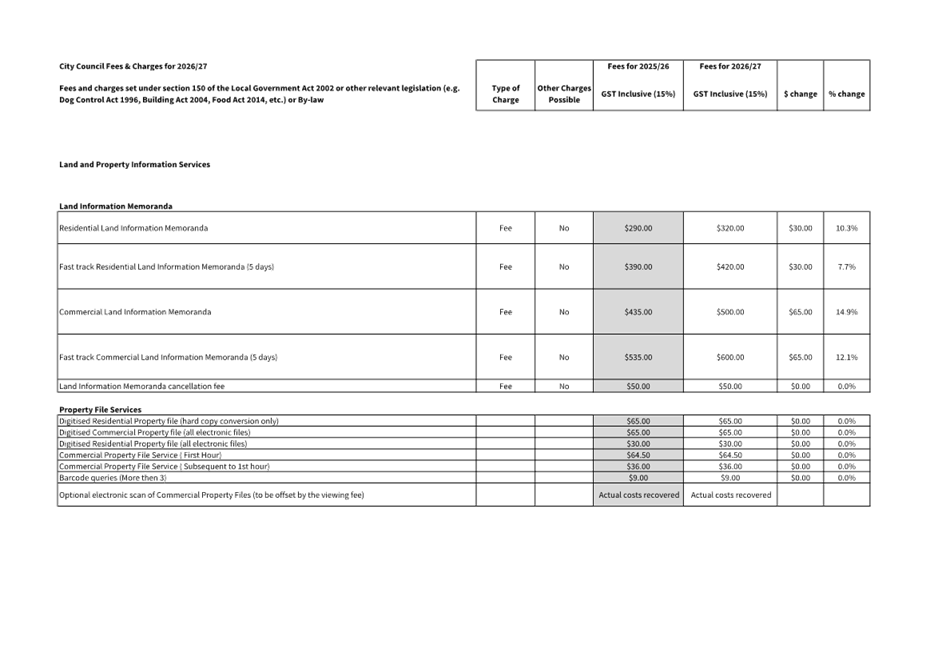

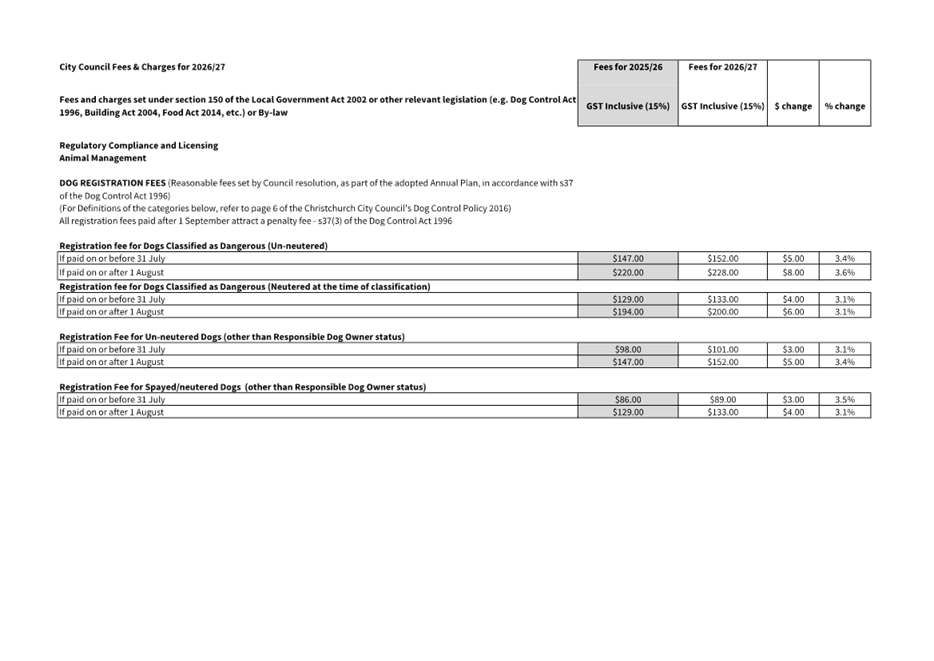

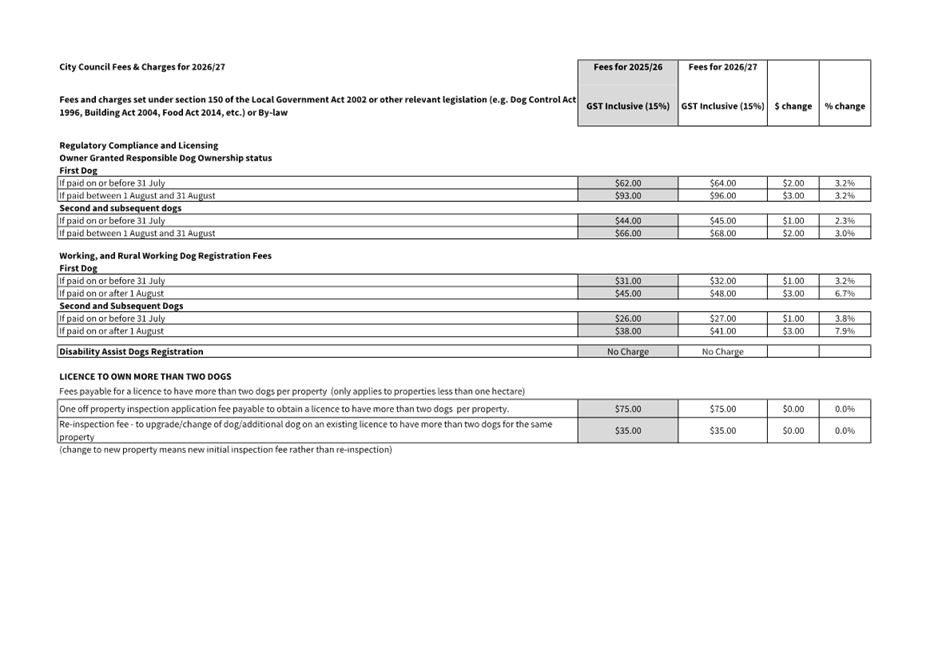

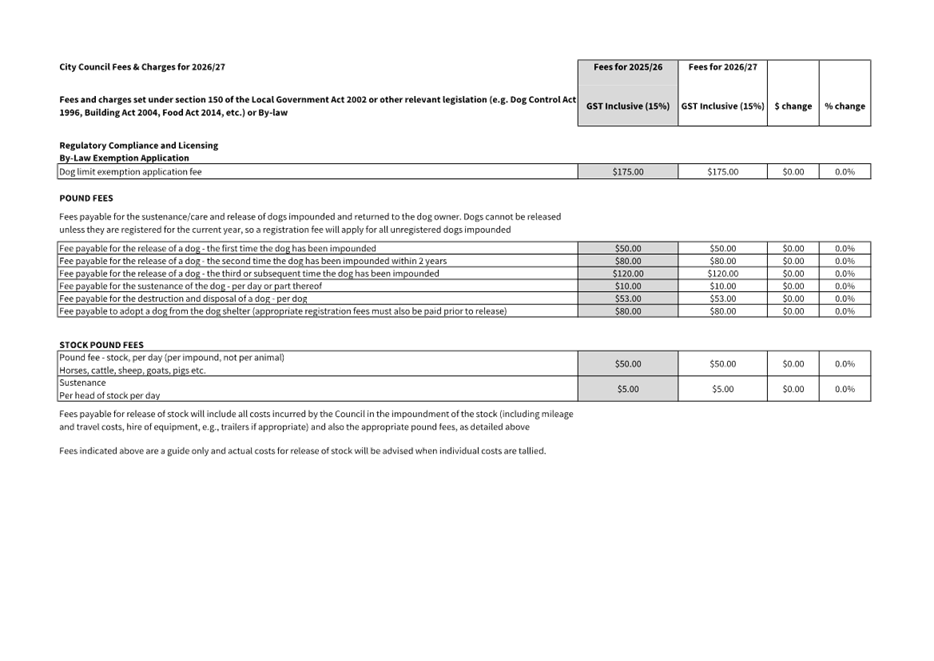

6. Fees and Charges

6.1 A

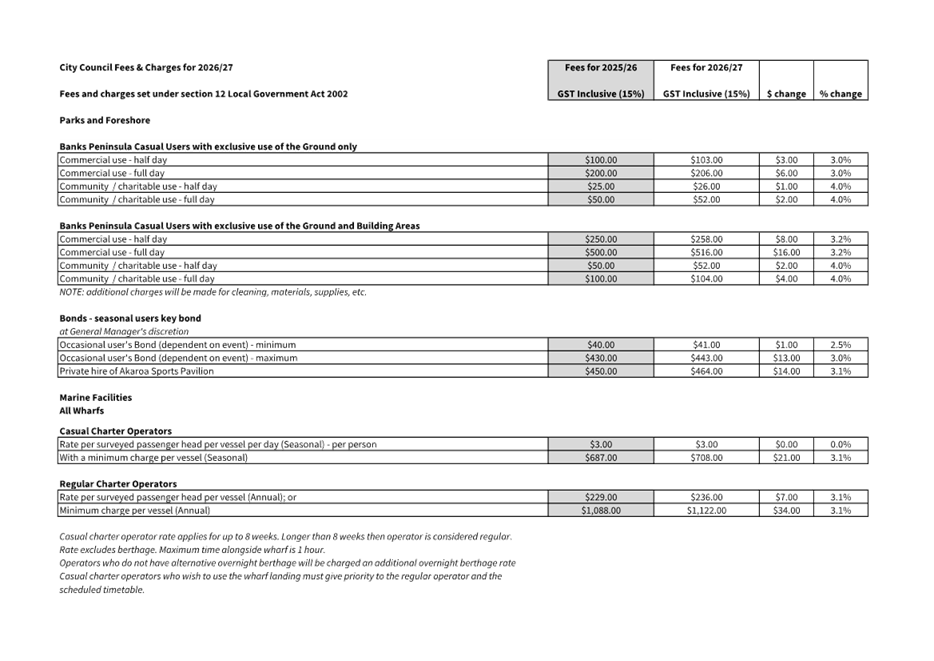

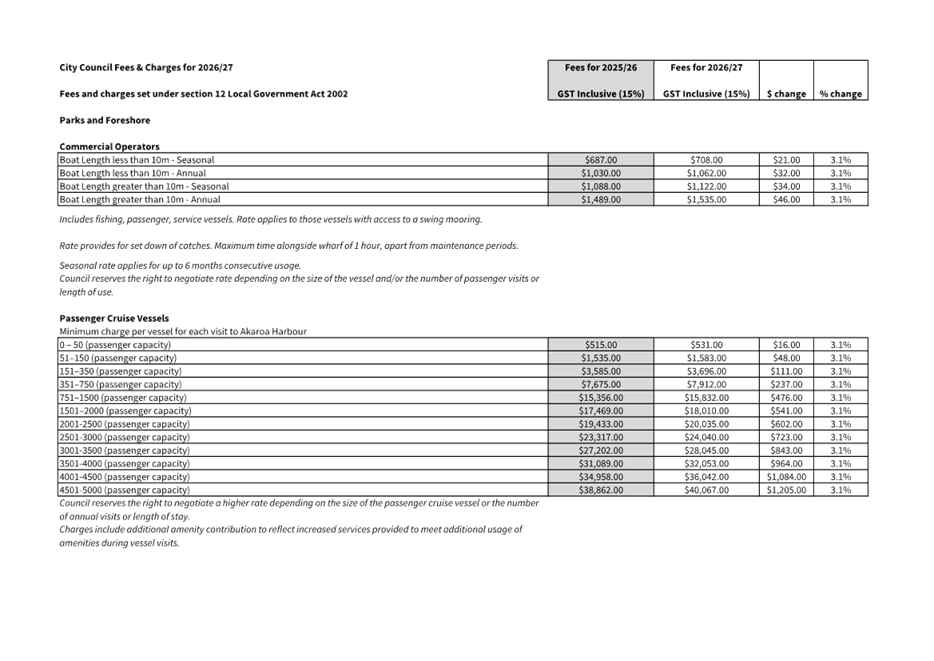

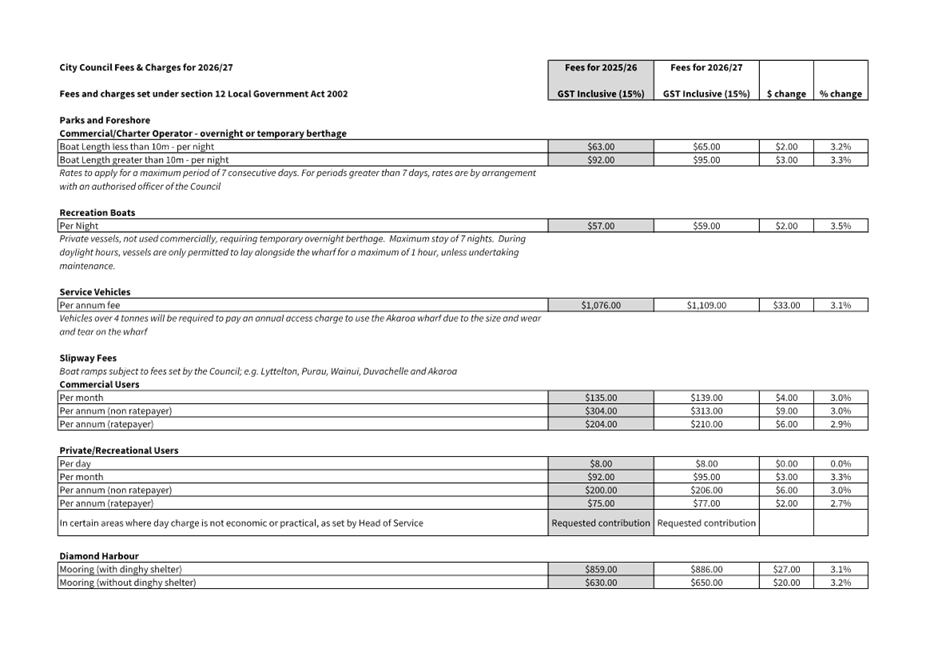

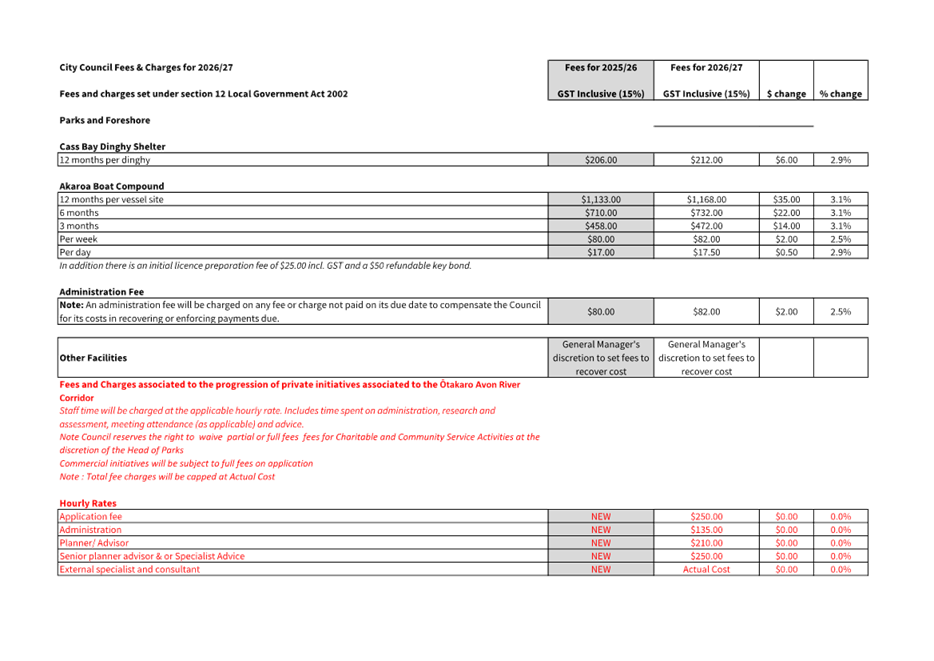

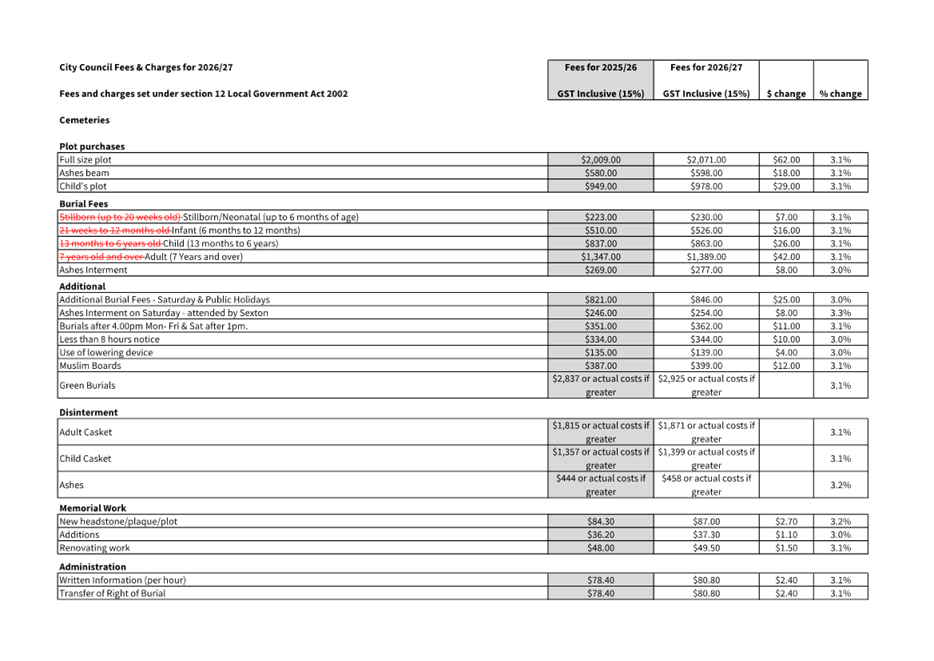

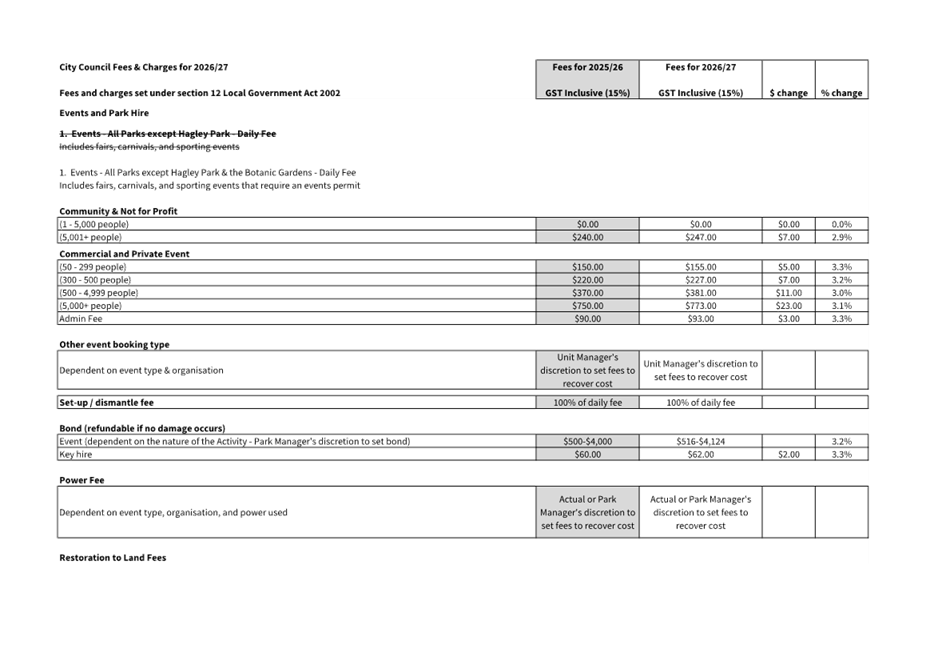

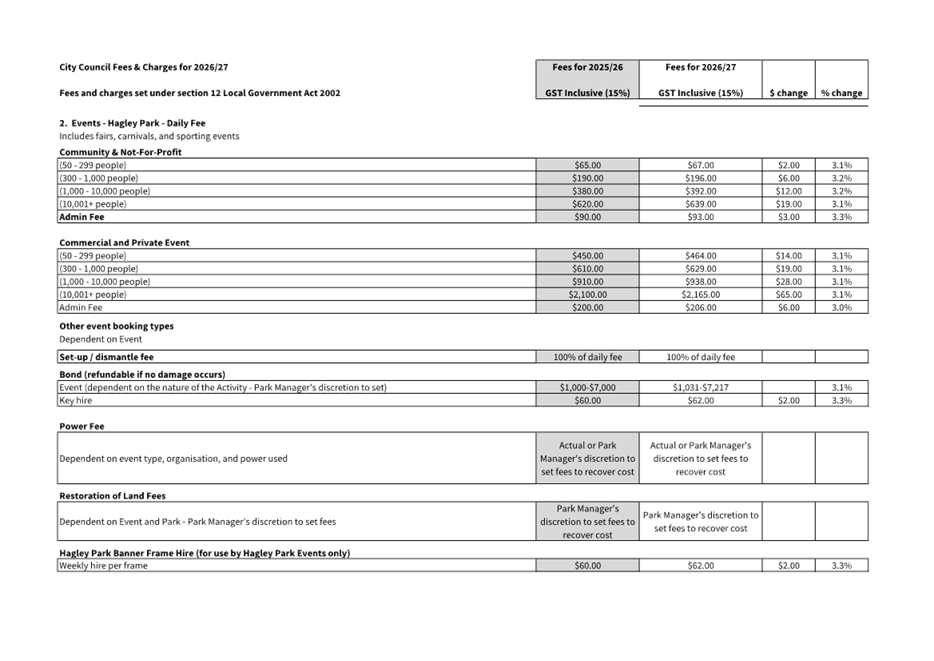

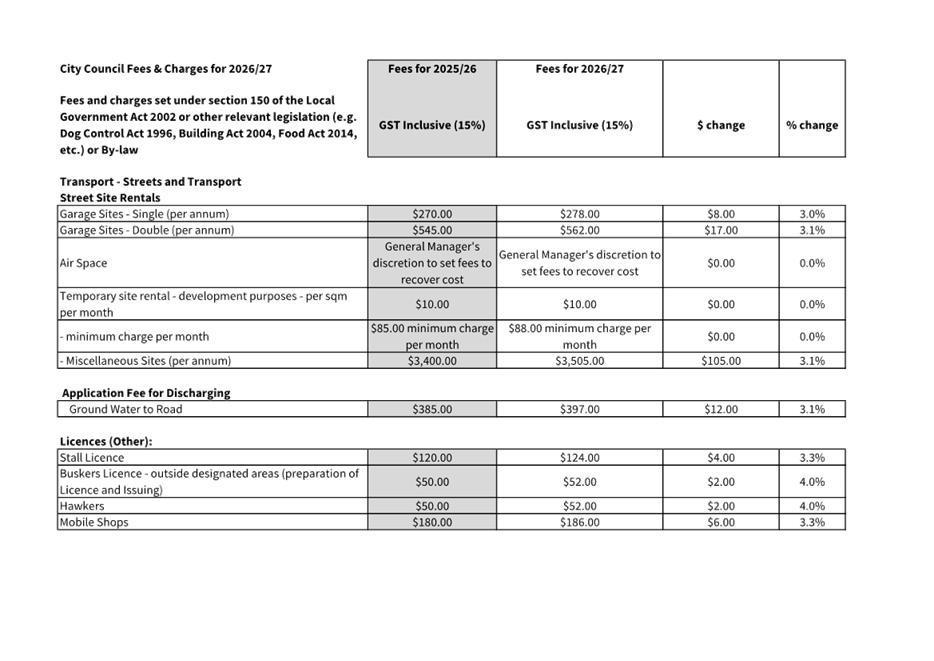

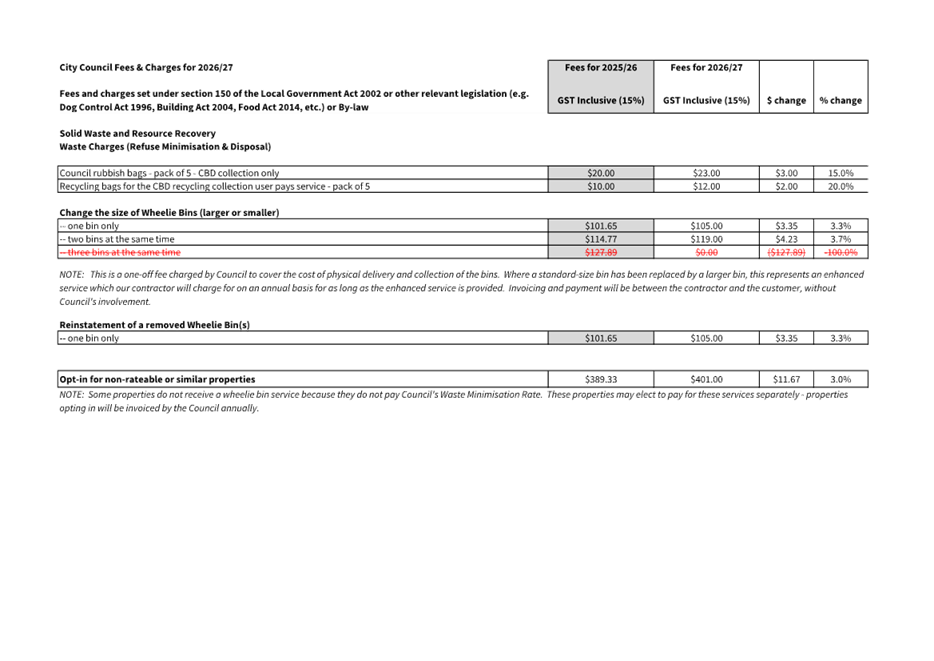

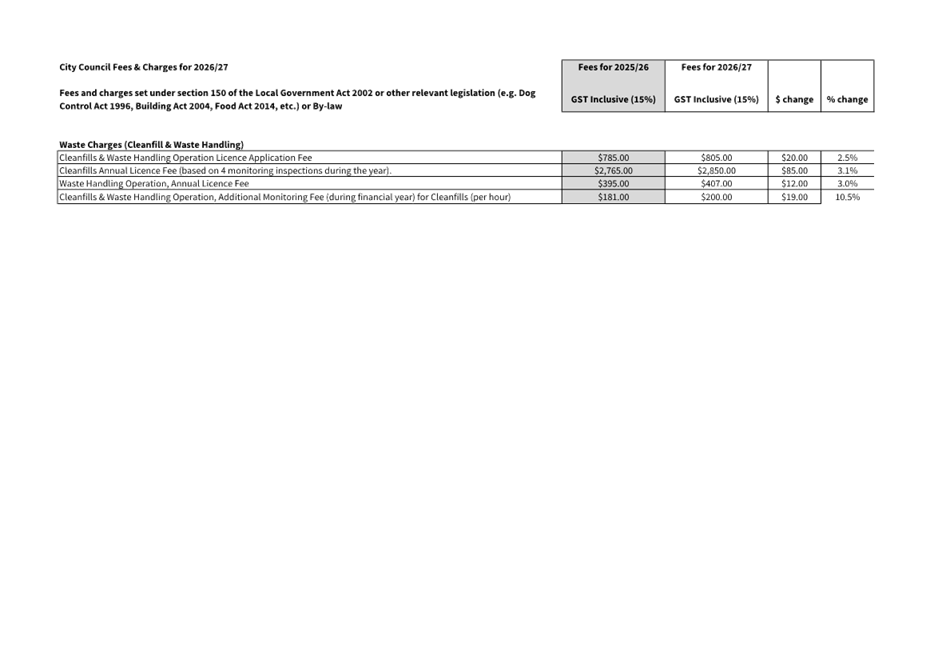

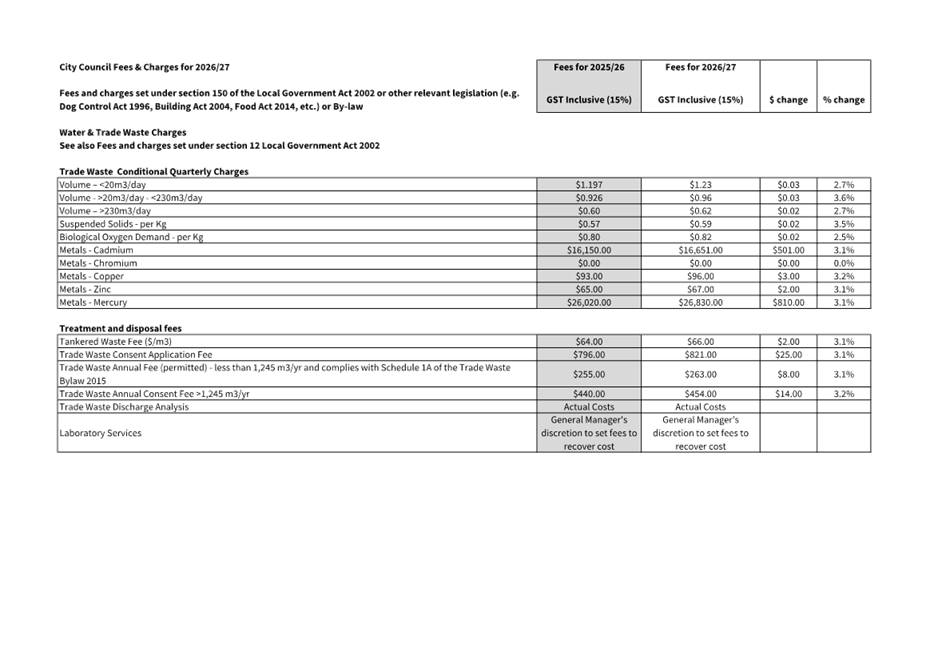

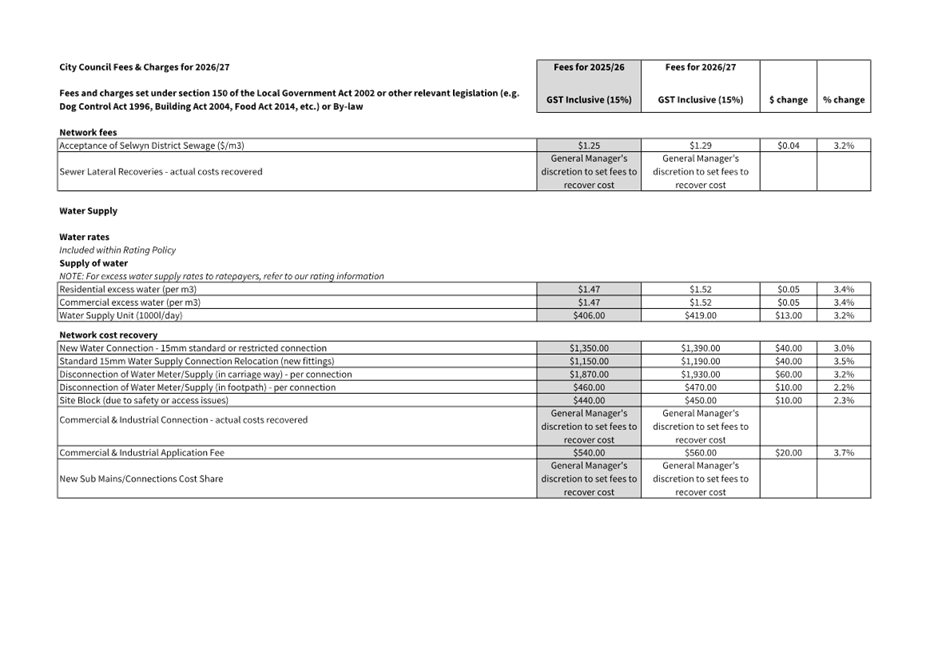

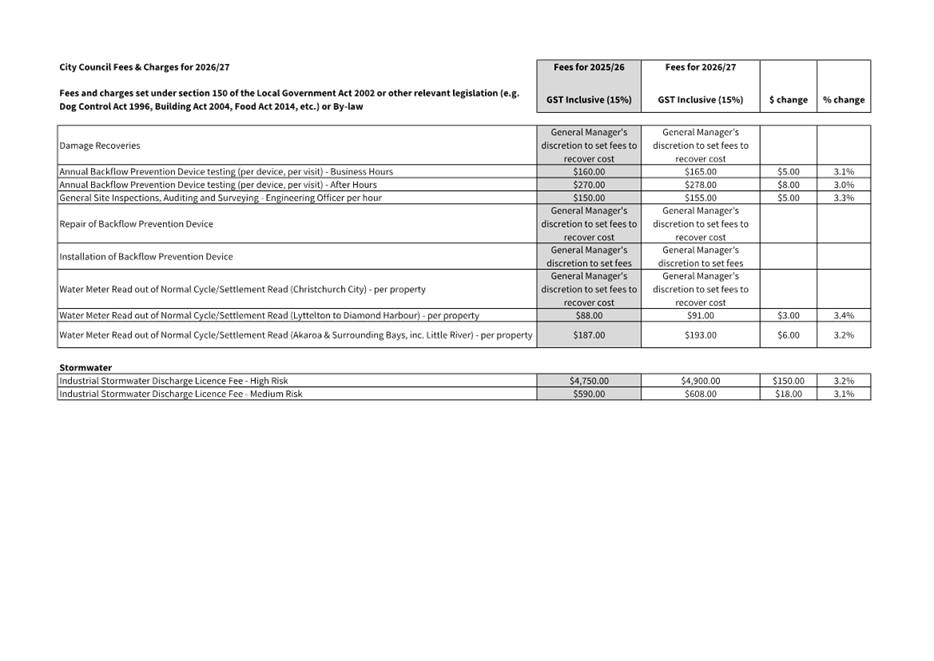

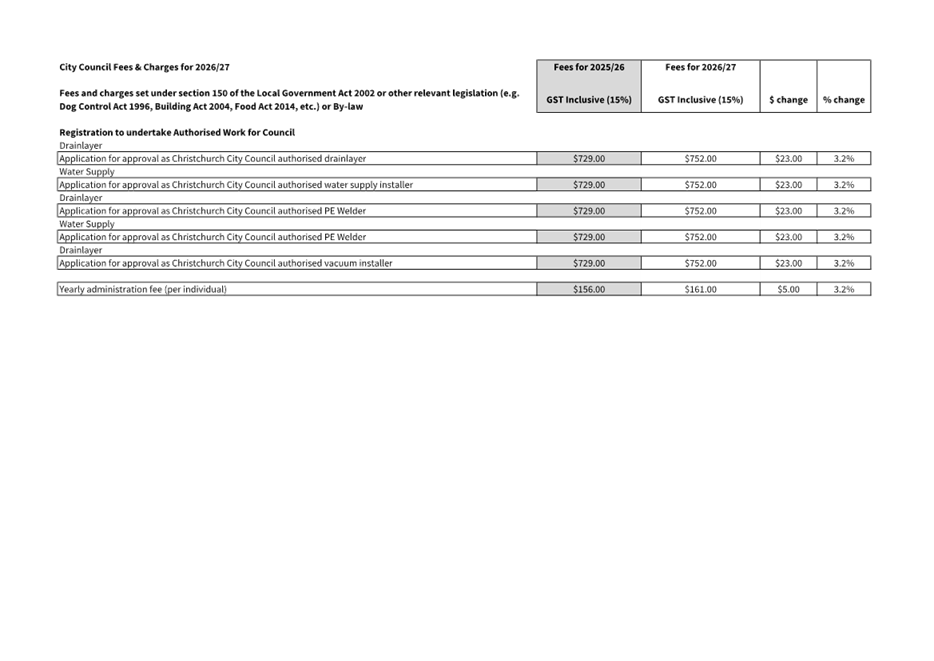

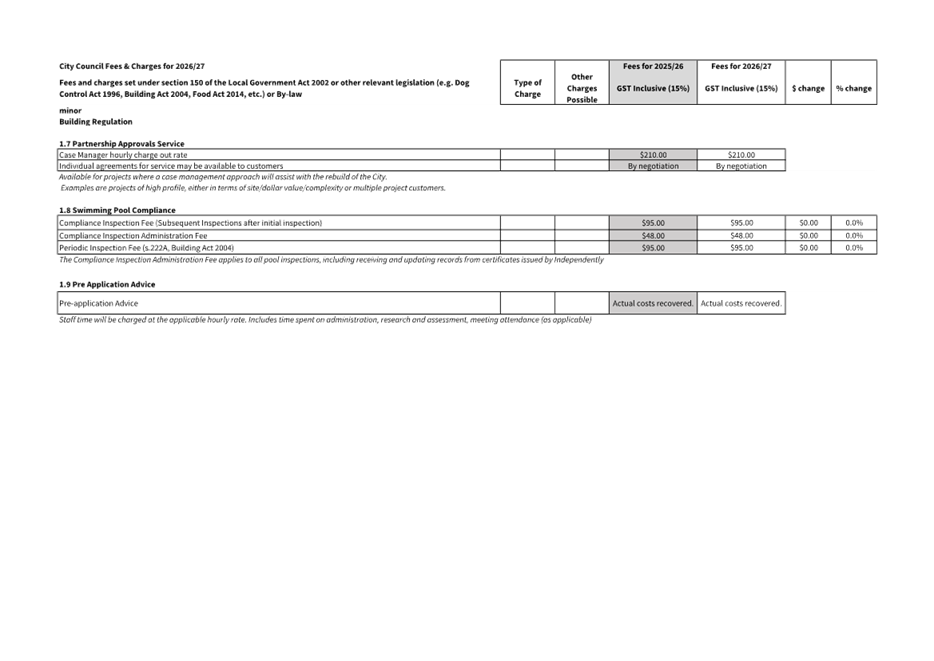

schedule of proposed Fees and Charges is included (refer Attachment I).

In recommending the proposed fees, staff have been conscious of the financial

pressure on residents and ratepayers and have attempted to avoid increases that

would create a barrier to the community’s utilisation of Council’s

services.

6.2 As

a result of the above, limitations imposed by the market, and the varying

inflationary impacts on costs and limits on cost recovery, fee increases

proposed for 2026/27 vary but generally align to expected Council inflation of

3.1%.

6.3 New

fees are proposed in the schedule of proposed Fees & Charges associated to

the progression of private initiatives associated to the Ōtākaro Avon

River Corridor (refer Attachment I, Page 36).

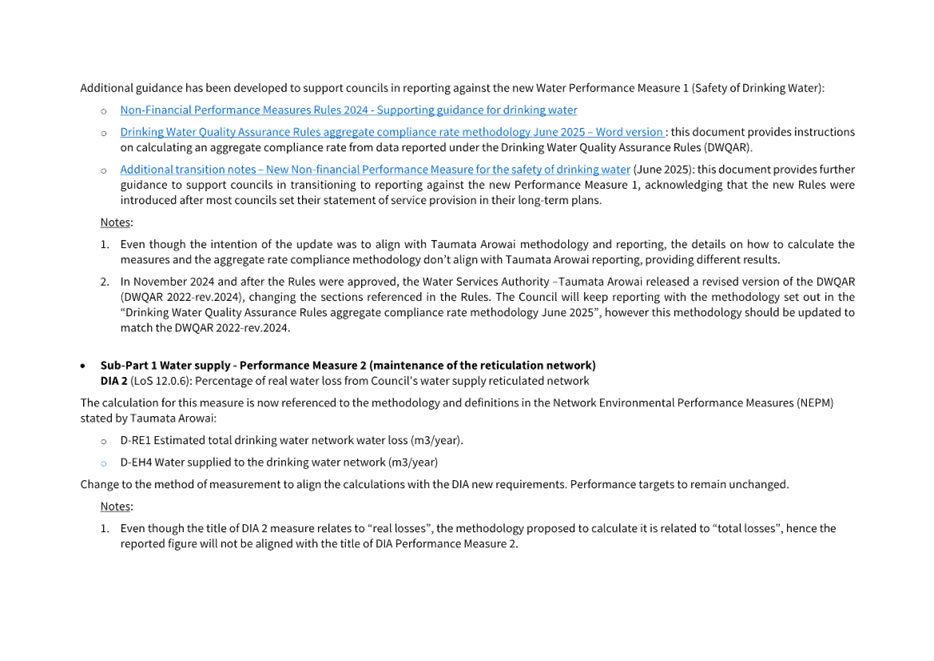

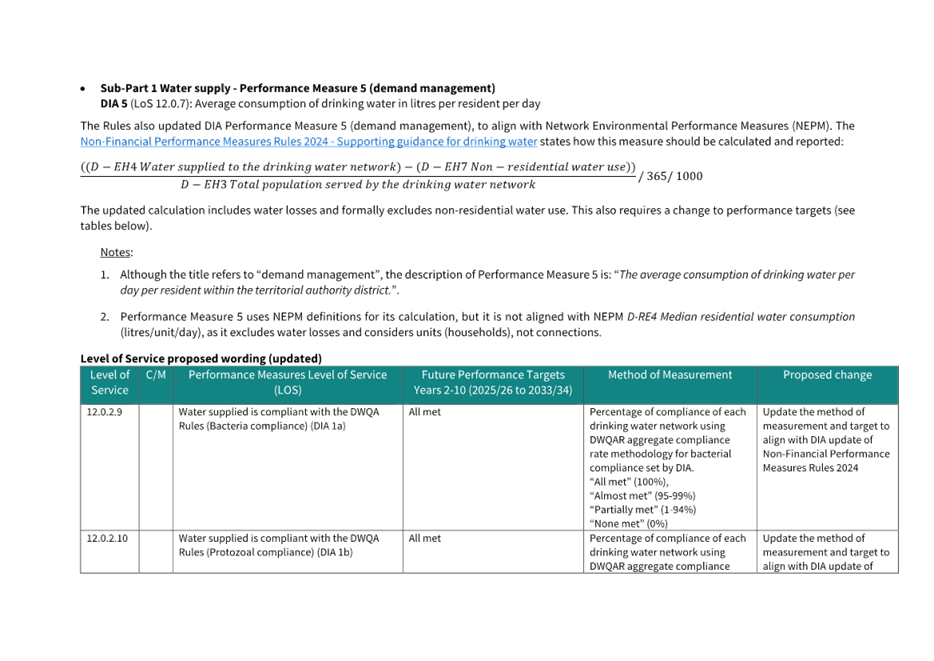

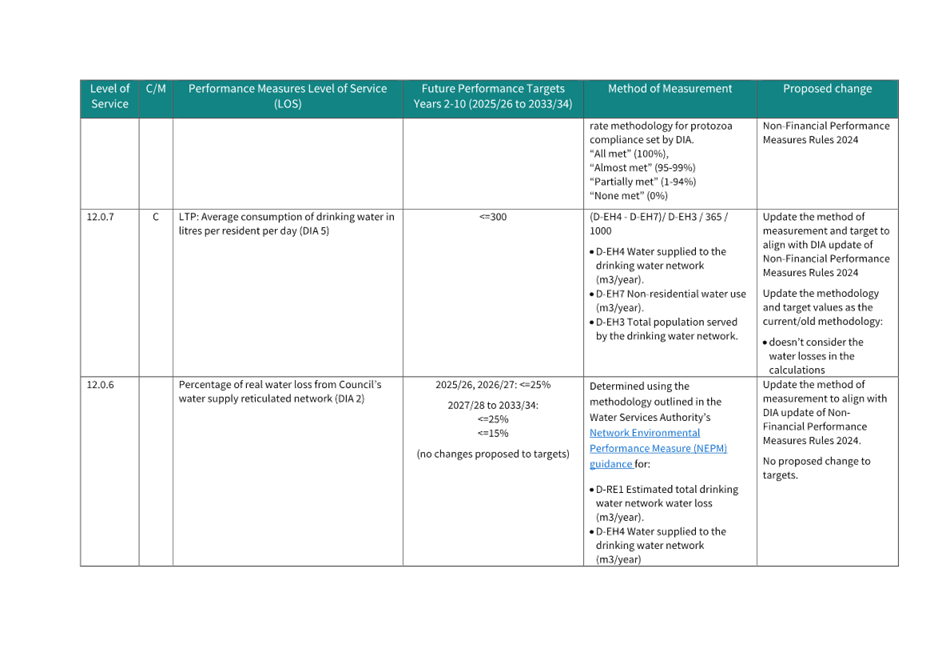

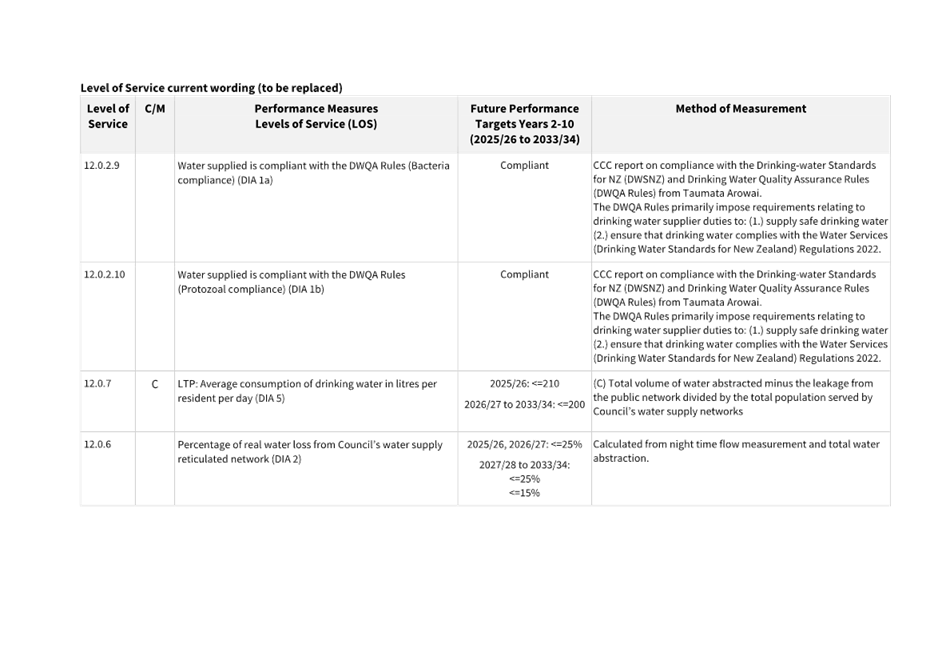

7. Changes to Levels of Service

7.1 There

are proposed minor changes to Measures of Success and targets (levels of

service) for two activities, accompanied by rationale (refer Attachment H).

These are the same as presented to Finance and Performance Committee at the

meeting of 17 December 2025.

7.2 In

summary the changes are;

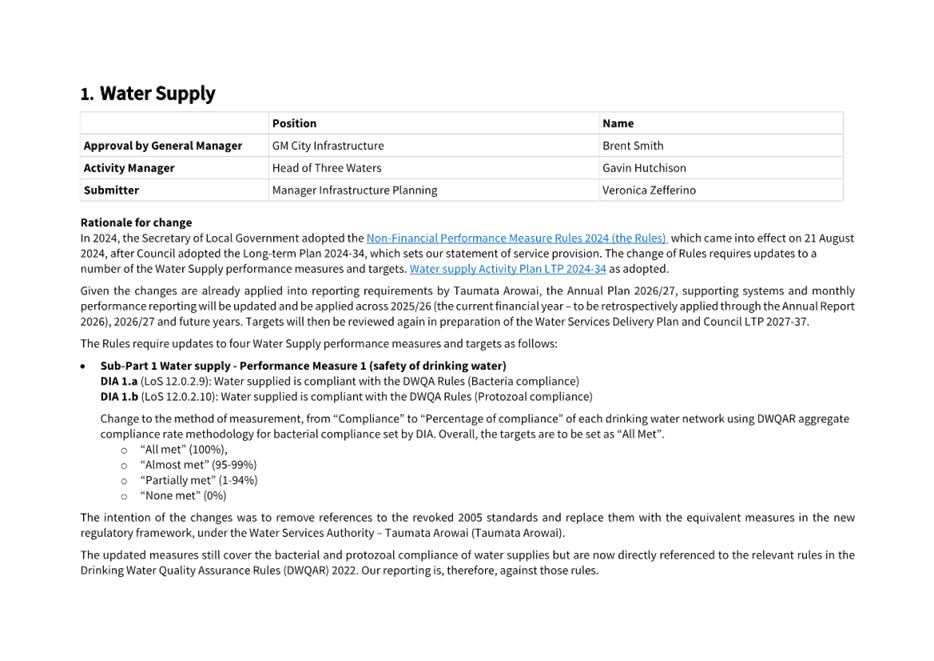

7.2.1 Water

Supply activity: to align methods of measurement and targets with Department of

Internal Affairs (DIA) updates of Non-Financial Performance Measures Rules

2024, including updates to methodology and target values for those with

current/old methodology. Given the changes are already applied into reporting

requirements by Taumata Arowai, the Annual Plan 2026/27, supporting systems and

monthly performance reporting will be updated and will be applied across

2025/26 (the current financial year – to be retrospectively applied

through the Annual Report 2026), 2026/27 and future years.

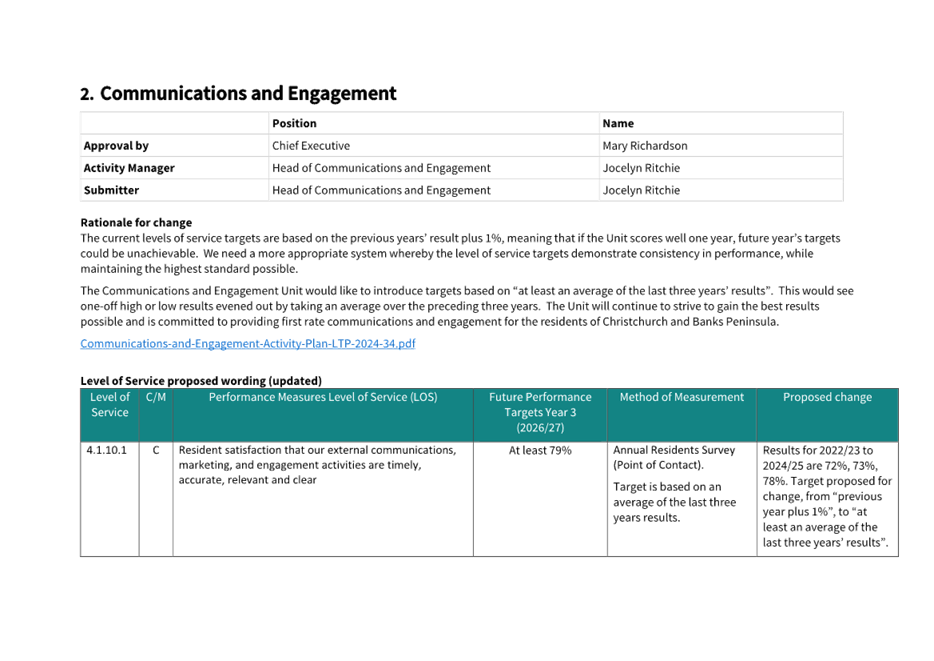

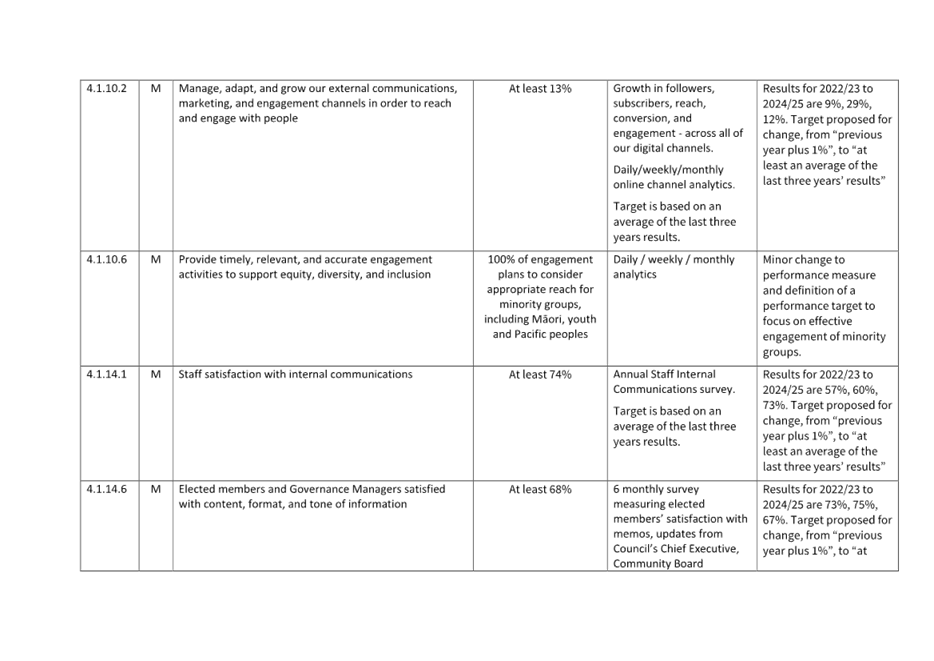

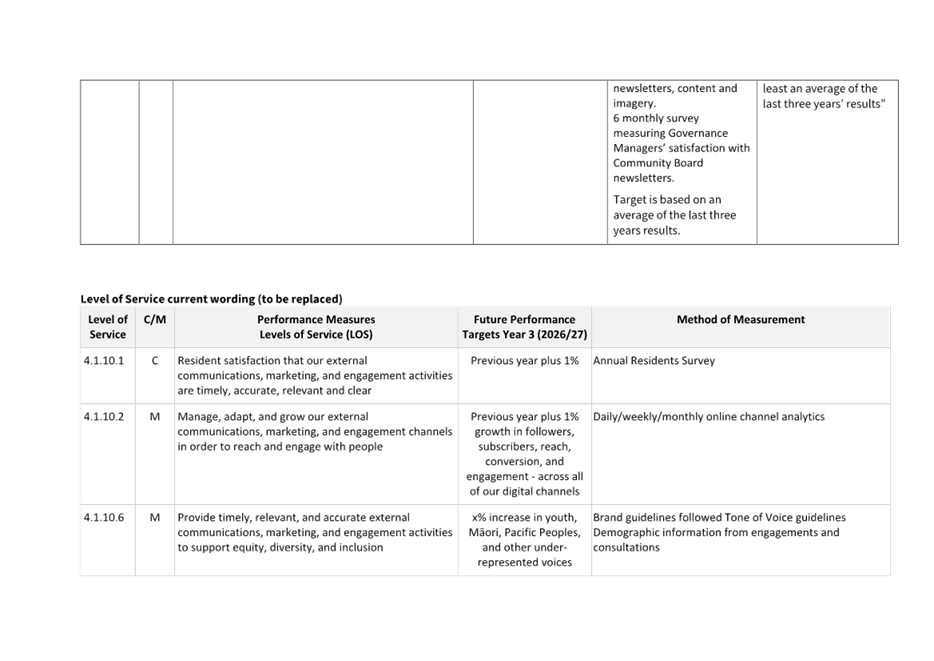

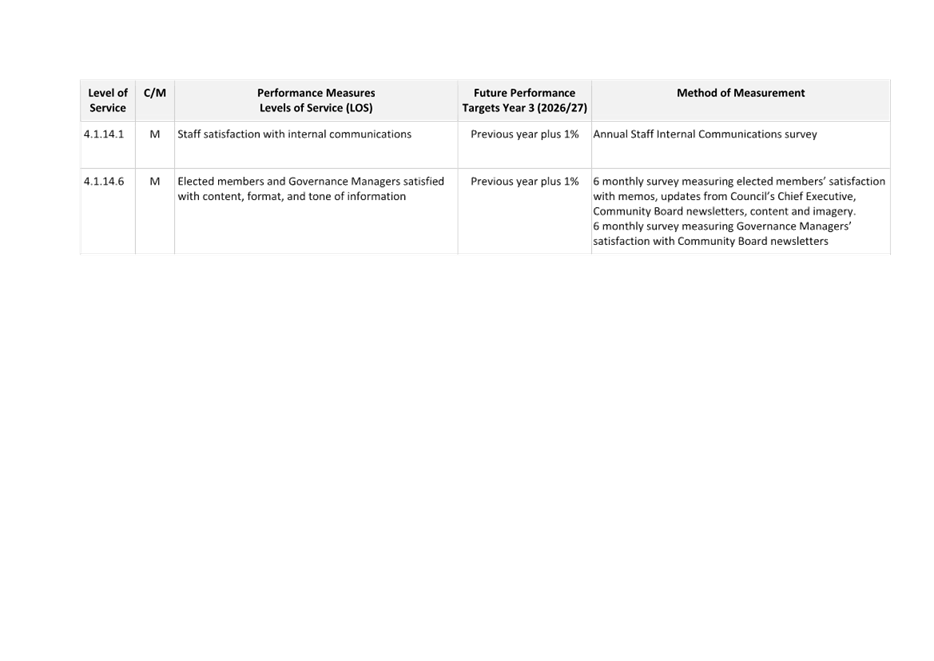

7.2.2 Communications

and Engagement activity: Current levels of service targets are based on the

previous years’ result plus 1%, meaning that if the Unit scores well one

year, future year’s targets could be unachievable. The proposal is

to introduce targets based on “at least an average of the last three

years’ results” plus 1%. Doing so will provide a more appropriate

system whereby the level of service targets demonstrate consistency in

performance (one-off high or low results evened out by taking an average over

the preceding three years), while maintaining the highest standard possible.

7.3 These

minor changes are for administrative purposes and do not require consultation

with the community.

8. Potential Disposal of Council Owned Properties

8.1 The

Council owns many types of properties of varying configurations and sizes.

Owning property comes at a cost, and it is good financial practice to

frequently review the portfolio to ensure it remains fit for purpose. If a

property is no longer fit for purpose, then Council should decide whether to

keep it or release its value for community benefit.

8.2 Since

2021 the Council has when appropriate included in its draft LTPs and Annual

Plans a small portfolio of properties to be considered for disposal. The

properties have been put forward for consideration on the basis they were no

longer delivering the original activity or service for which they were

purchased.

8.3 It

is intended to replicate the process in this Annual Plan for a small number of

properties which have been identified as no longer used for the purpose for

which they were originally acquired. These have been assessed against and are

considered to meet the following criteria adopted by the Council at its meeting

of 10 December 2021:

8.3.1

Is the property still required for the purpose for which it was originally

acquired?

8.3.2

Does the property have special cultural, heritage or environmental values that

can only be protected through public ownership?

8.3.3

Is there an immediate identified alternative public use / work / activity in a

policy, plan or strategy?

8.3.4

Are there any strategic, non-service delivery needs that the property meets and

that can only be met through public ownership?

8.3.5

Are there any identified unmet needs, which the Council might normally address,

that the property could be used to solve? And is there a reasonable pathway to

funding the unmet need?

8.4 A

list of those properties considered suitable to be put forward for

incorporation in this draft Annual Plan for consultation purposes can be seen

at Attachment O.

9. Considerations Ngā Whai Whakaaro

Risks and Mitigations Ngā Mōrearea me

ngā Whakamātautau

9.1 Key

risks for the Annual Plan include:

9.1.1 Failure

to achieve project plan milestones. Mitigation: currently on track due to

direction provided by Council to staff at the meeting of Finance and

Performance Committee at the meeting of 17 December 2025. Adoption of the draft

Annual Plan 2026/27 in February 2026 remains critical to the process.

9.1.2 Not

meeting the decision-making requirements of the LGA due to a large number of

late amendments at the time of adopting the draft Annual Plan.

Mitigation: Workshops with Council to provide opportunity for matters to be

raised as part of the build of the draft Annual Plan.

9.1.3 Attempting

to amend the LTP with insufficient time to do so. Mitigation: Also currently on

track due to clear communication of Council guidance to date, legal and

logistical constraints.

9.1.4 Deliverability

of capital programme. Mitigation: this risk has been mitigated by the

recommended re-phasing of the capital programme. Historically, average

annual capital expenditure has been approximately $500 million, while the

proposed 2026/27 programme is $586.2 million— a 17% increase. This

increase includes $42 million for the Activated Sludge project at the

Wastewater Treatment Plant, delivery of which is now under contract.

· These delivery

risks will be further managed by focussing on key/critical projects,

strengthening oversight through regular performance reviews and working with

contractors to explore ways to increase delivery capacity.

· Looking ahead,

there is still a delivery risk for capital projects for future years (2027/28

to 2033/34) that will need to be addressed as part of the upcoming Long-Term

Plan.

Legal Considerations Ngā Hīraunga

ā-Ture

9.2 Statutory

and/or delegated authority to undertake proposals in the report:

9.2.1 The

Council must, at all times, have an LTP / Annual Plan in place (sections 93 and

95 of the LGA). The Annual Plan is required to be adopted prior to the

year to which it relates (section 95(3) of the LGA).

9.3 Other

Legal Implications:

9.3.1 The

Council has a legal duty to ensure that each year the projected operating

expenses are set to achieve a balanced budget (section 100(1) of the Local

Government Act 2002 (LGA)). Council can approve an unbalanced budget (in final

Annual Plan adoption of June 2026) provided it resolves that it is financially

prudent to do so, having regard to the relevant criteria set out in section

100(2) of the LGA.

9.3.2 There is

no additional legal context, issue or implication relevant to this decision.

Strategy

and Policy Considerations Te

Whai Kaupapa here

9.4 The

required decision aligns with the Strategic Framework adopted with the 2024

Long Term Plan.

9.5 This

report supports the Council's

Long Term Plan (2024 - 2034):

9.6 Internal

Services

9.6.1 Activity: Performance, Finance, and Procurement

· Level of Service: 13.1.1 Implement the Long-Term Plan and

Annual Plan programme plan - Critical path milestone due dates in programme

plans are met

Community

Impacts and Views Ngā Mariu ā-Hāpori

9.7 This

decision affects all existing citizens and ratepayers of Christchurch, and has

implications for future citizens, ratepayers, and Councils.

9.8 The

decision affects all wards/Community Board areas.

Impact

on Mana Whenua Ngā

Whai Take Mana Whenua

9.9 The

LTP 2024–34 saw consultation and engagement with Ngā Papatipu

Rūnanga, which resulted in a wide range of initiatives being undertaken in

the LTP. Those undertakings remain intact and are not proposed to be affected

by the Annual Plan.

9.10 The

decision will not impact on our agreed partnership priorities with Ngā

Papatipu Rūnanga.

Climate

Change Impact Considerations Ngā Whai Whakaaro mā te Āhuarangi

9.11 The

decisions in this report are likely to:

9.11.1 Contribute

to adaptation to the impacts of climate change, in line with decisions for new

initiatives and increases set out in the LTP 2024-34.

9.11.2 Contribute to stability of a whole-of-community climate response by

continuing to provide leadership through the funds established with LTP 2024-34

that will be used in future to mitigate the approaching impacts of climate

change.

10. Next Steps Ngā Mahinga ā-muri

10.1 After

adoption of the draft Annual Plan, consultation with the community will

commence (refer Attachment P to be provided under separate cover for the

draft Consultation Document) beginning on 27 February 2026 and running until

11:59pm, 27 March 2026.

10.2 At

the completion of consultation, Hearings will follow and are planned to be held

from late March to April 2026 (exact dates will be confirmed and communicated

to those submitters closer to the time).

10.3 After

completion of the Hearings, the results of the consultation feedback and

Hearings will be collated to inform Council Information Sessions/Workshops for

April/May/June 2026. (Exact dates will be confirmed and communicated with

Council closer to the time.)

10.4 Any

adjustments to the draft Annual Plan resulting from consultation, Hearings and

Workshops will be completed so that the Annual Plan report preparation process

can be reviewed by ARMC at the meeting of 15 June 2026 and included in the

agenda for the Council meeting of 23 June 2026.

10.5 The

Annual Plan 2026/27 is scheduled for consideration and final adoption at a

meeting of the Christchurch City Council on 23 June 2026.

10.6 Any

delay, impediment, stoppage or indecision in this timeframe is likely to result

in the Annual Plan 2026/27 not being adopted before the end of June, preventing

the striking of the new rates from 1 July 2026. This would result in a

significant loss of revenue and reputational damage until the new Annual Plan

can be adopted.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Audit and Risk

Management Committee Recommendations - 2 February 2026

|

26/230621

|

22

|

|

b ⇩

|

Financial

Overview

|

26/119985

|

23

|

|

c ⇩

|

Funding Impact

Statement

|

26/119977

|

33

|

|

d ⇩

|

Rating

Information

|

26/130005

|

37

|

|

e ⇩

|

Rating

Policies

|

26/131705

|

54

|

|

f ⇩

|

Financial

Prudence Benchmarks

|

26/119961

|

69

|

|

g ⇩

|

Proposed

Capital Programme

|

26/130177

|

71

|

|

h ⇩

|

Proposed Minor

Changes to Levels of Service

|

25/2475018

|

99

|

|

i ⇩

|

Proposed Fees

and Charges

|

26/3302

|

109

|

|

j ⇩

|

Prospective

Financial Statements

|

26/119938

|

193

|

|

k ⇩

|

Statement of

Significant Accounting Policies

|

26/149312

|

202

|

|

l ⇩

|

Reserves and

Trust Funds

|

26/119871

|

218

|

|

m ⇩

|

Capital

Endowment Fund

|

26/119844

|

221

|

|

n ⇩

|

Summary of

Grants

|

26/119945

|

223

|

|

o ⇩

|

List of

properties for consultation seeking the community views and preferences as to

their future use

|

26/116840

|

225

|

|

p

|

Consultation

Document (Under Separate Cover)

|

26/128435

|

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Following the election of the new Council

in October 2025, staff began a series of workshops with the Mayor and

councillors on the Annual Plan 2026/27, to seek Council direction for

development of the draft Annual Plan for adoption. Below are links to the

recordings of the various public workshops and meetings, including agendas

and minutes related to this development:

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Meg Wedlock -

Performance Analyst

Saba Azeem -

Senior Corporate Planning and Performance Analyst

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

Paul Dadson -

Senior Capital Programme Advisor Parks & Facilities

Mitchell Shaw

- Principal Advisor - Finance

Ron Lemm -

Manager Legal Service Delivery

Bruce Moher -

Head of Finance

Peter Ryan -

Head of Corporate Planning & Performance

|

|

Approved By

|

Bruce Moher -

Head of Finance

Peter Ryan -

Head of Corporate Planning & Performance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

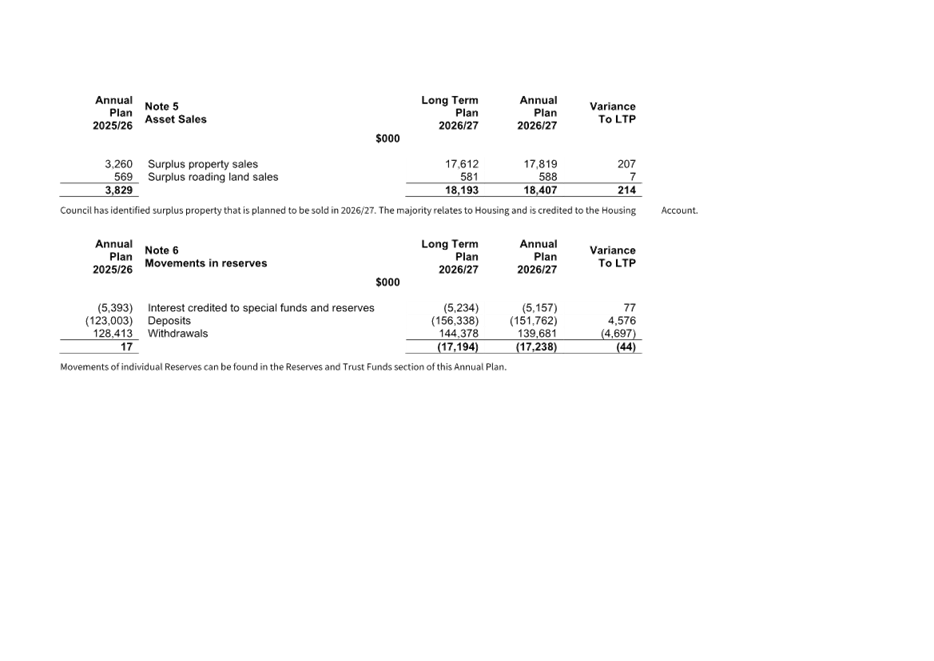

|