Finance and Performance Committee

Agenda

Notice of Meeting Te Pānui o te Hui:

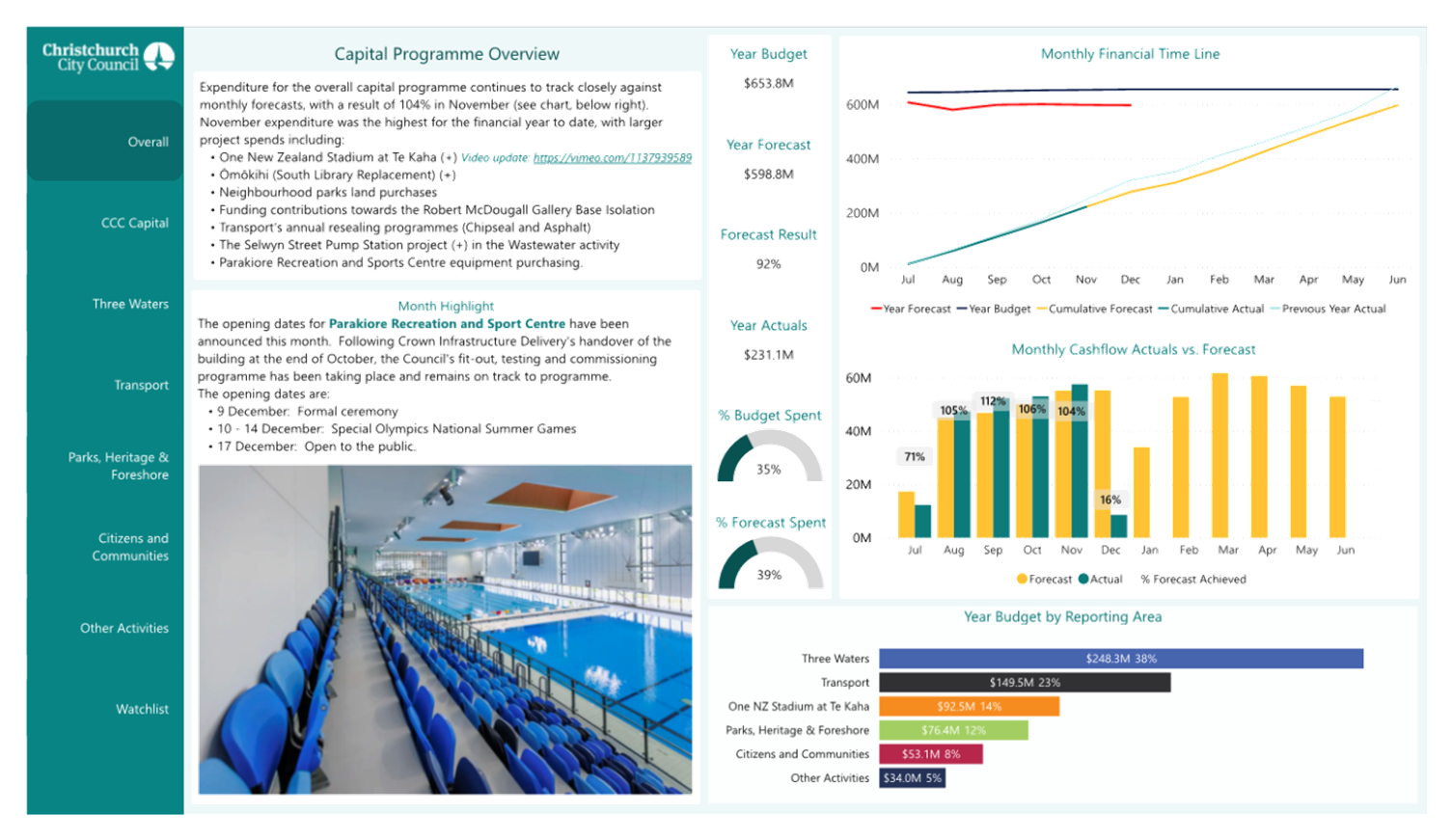

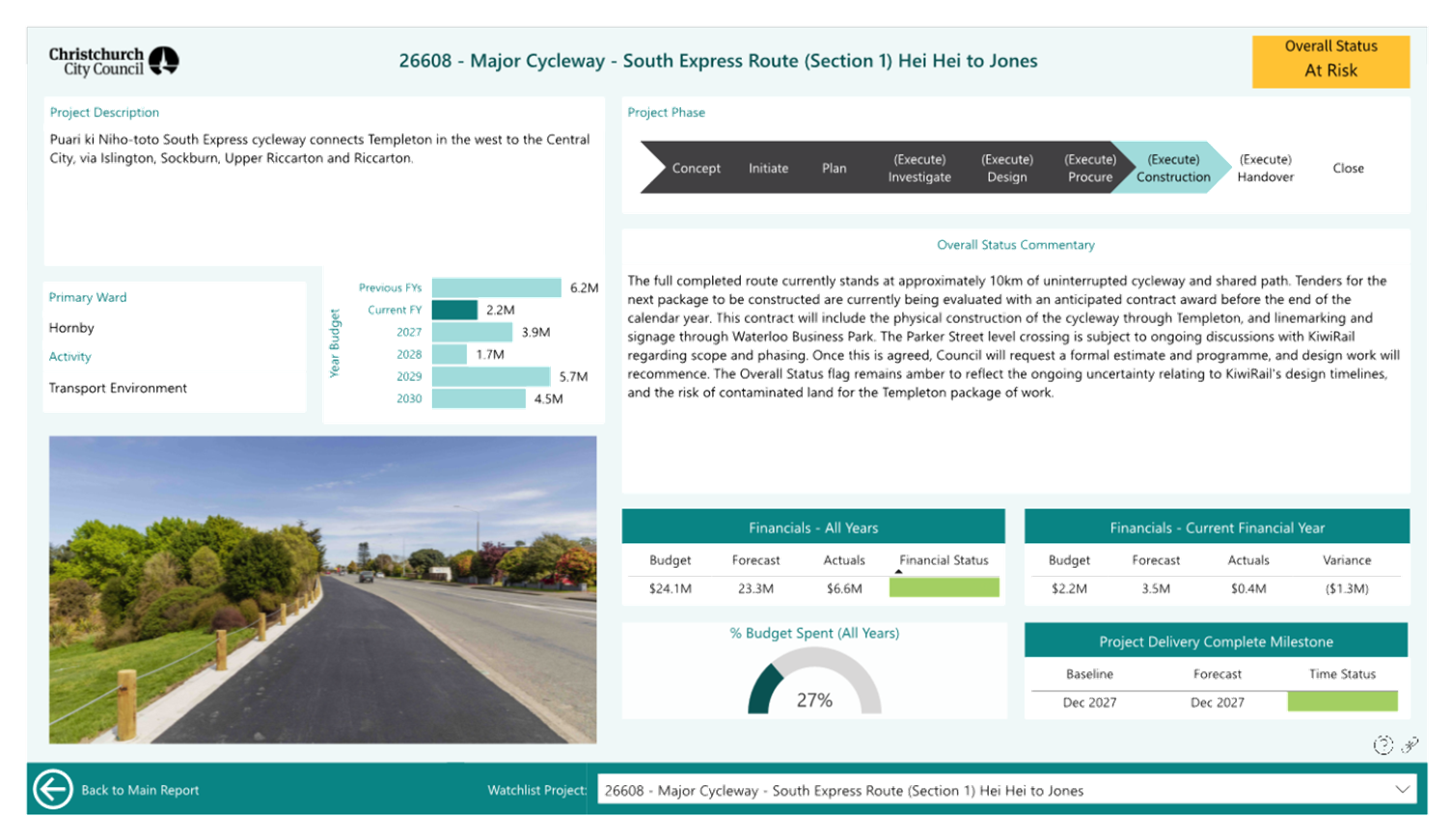

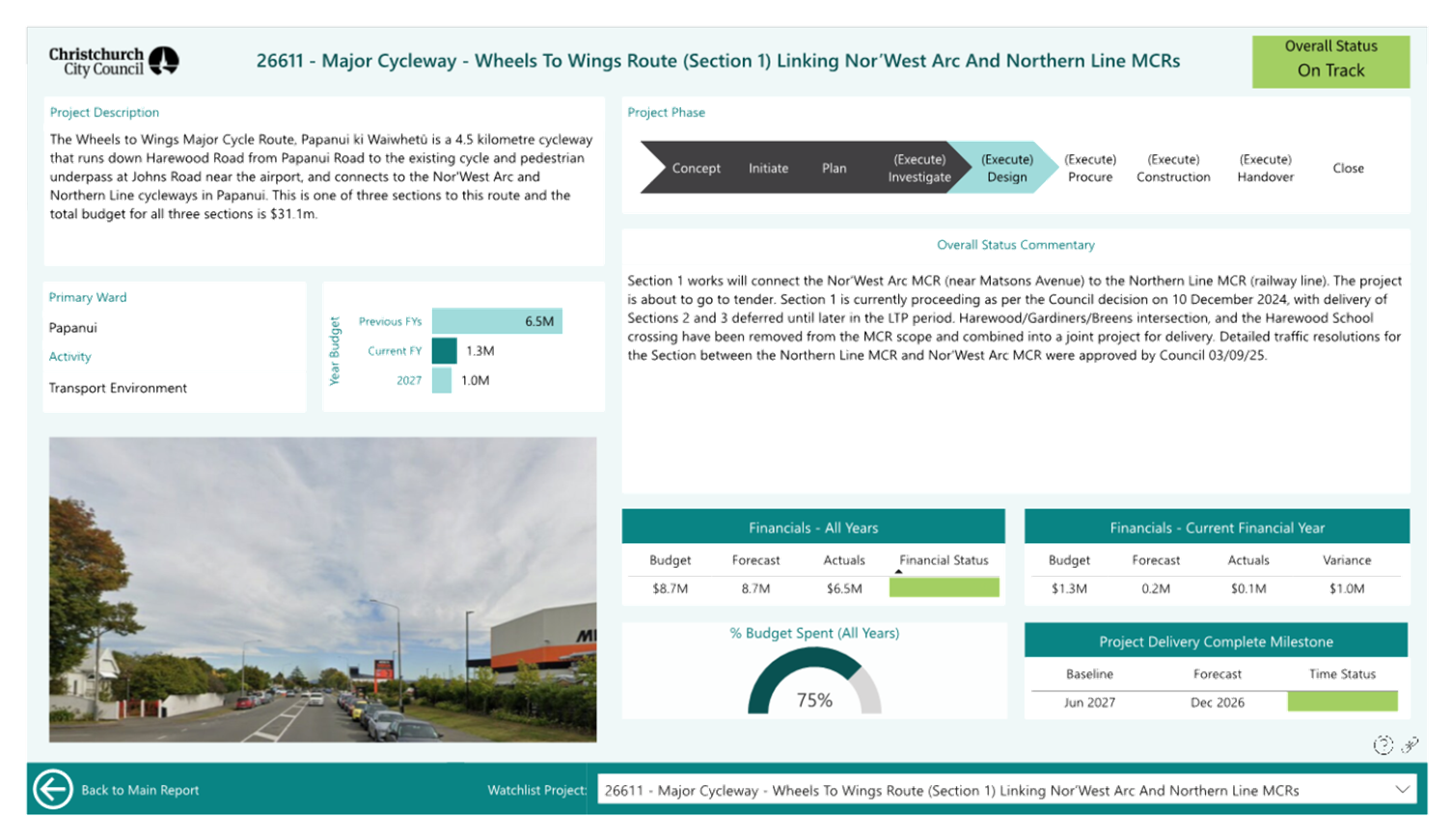

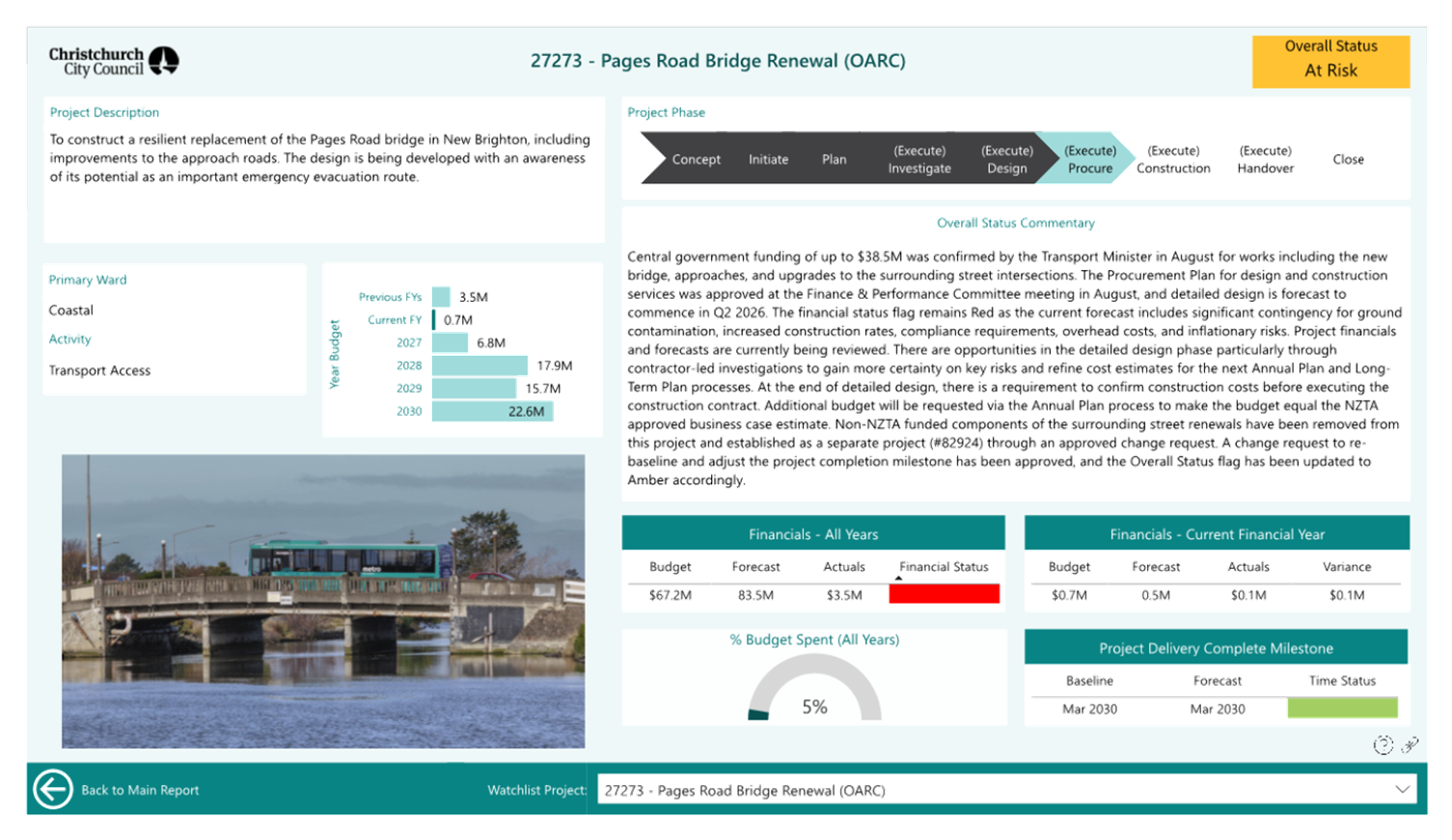

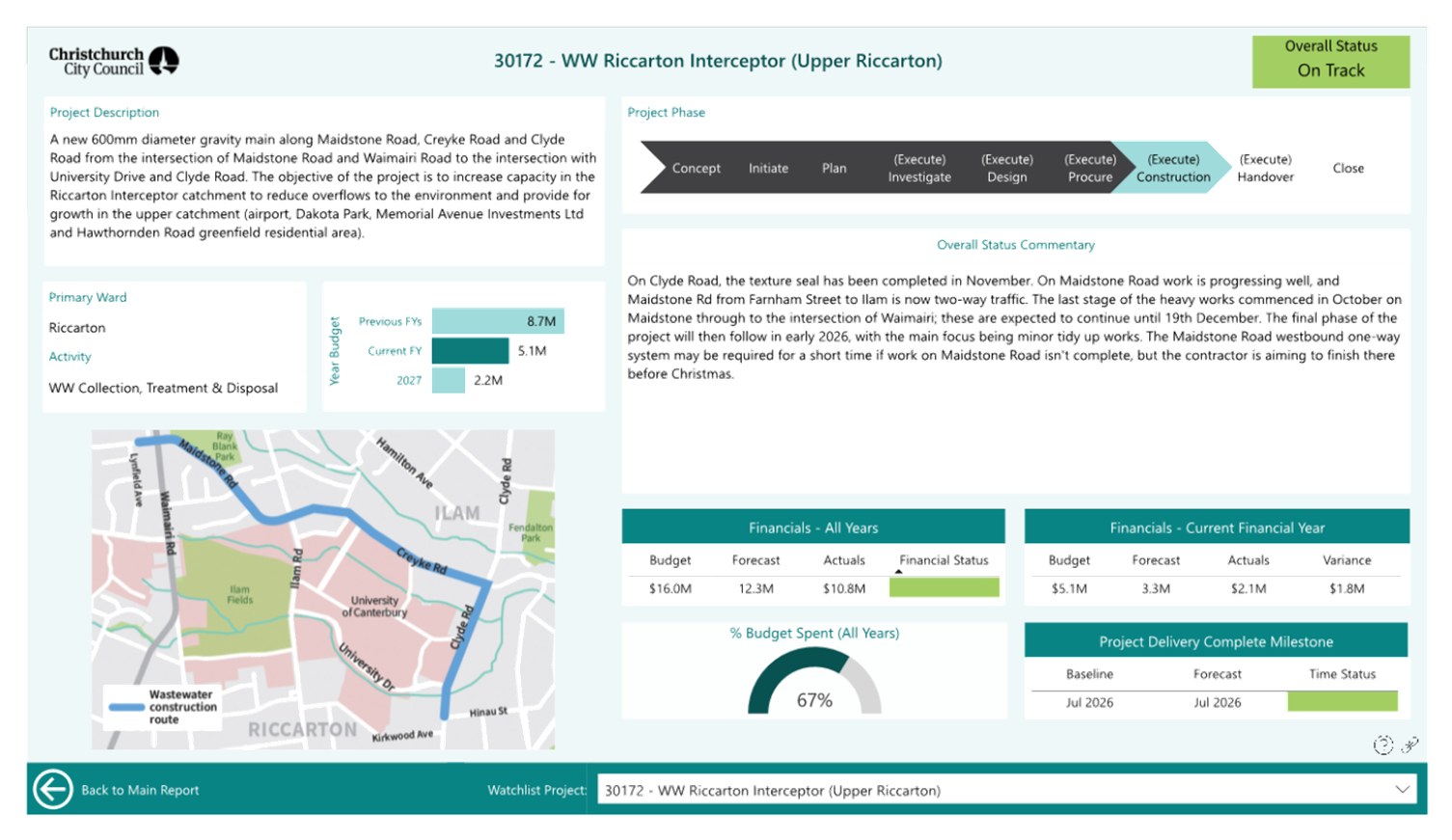

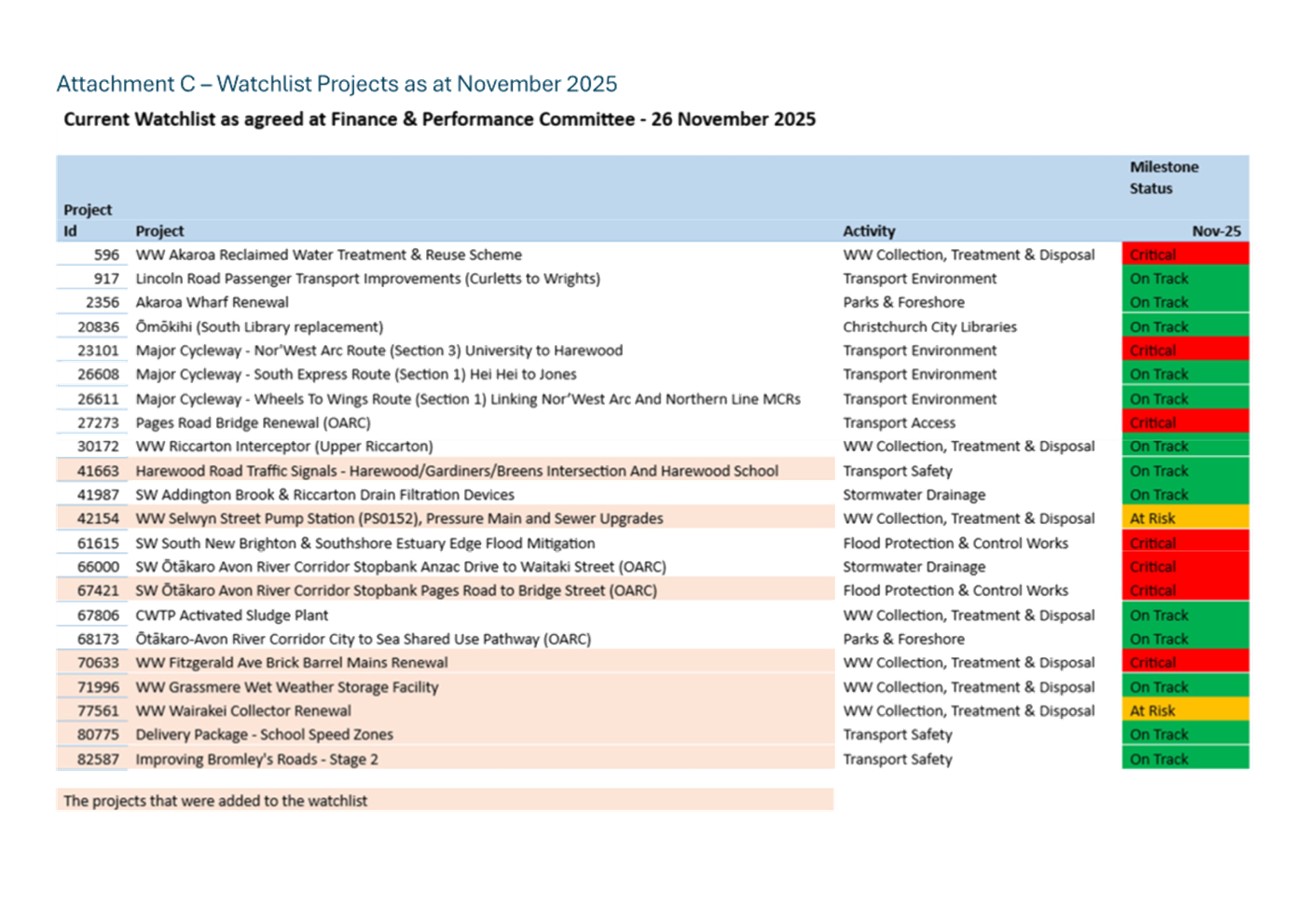

An ordinary meeting of the Finance &

Performance Committee will be held on:

Date: Wednesday 17 December 2025

Time: 9.30 am

Venue: Camellia Chambers, Civic Offices,

53 Hereford Street, Christchurch

Membership

|

Chairperson

Deputy Chairperson

Members

|

Councillor Sam MacDonald

Councillor Jake McLellan

Mayor Phil Mauger

Deputy Mayor Victoria Henstock

Councillor David Cartwright

Councillor Melanie Coker

Councillor Pauline Cotter

Councillor Kelly Barber

Councillor Celeste Donovan

Councillor Tyrone Fields

Councillor Tyla Harrison-Hunt

Councillor Nathaniel Herz Jardine

Councillor Yani Johanson

Councillor Aaron Keown

Councillor Andrei Moore

Councillor Mark Peters

Councillor Tim Scandrett

|

11 December 2025

Website: www.ccc.govt.nz

Finance and

Performance Committee of the Whole - Terms

of Reference

/ Ngā Ārahina Mahinga

|

Chair Chair

|

Councillor

MacDonald

|

|

Deputy Chair

|

Councillor

McLellan

|

|

Membership

|

The Mayor and all councillors

are members of

this committee.

|

|

Quorum

|

Half of the members if the number of members (including vacancies) is even, or a majority of members if the number of members (including vacancies) is

odd

|

|

Meeting

Cycle

|

Monthly

|

|

Reports To

|

Council

|

Delegations

The Council delegates to

the Finance

and

Performance Committee authority

to

oversee and make decisions

on the following

matters:

Capital Programme and operational expenditure

· Monitoring the delivery of the Council’s

Capital Programme and associated operational

expenditure,

including inquiring

into any material discrepancies

from planned expenditure.

· Approving amendments to

the Capital Programme outside the Long-Term Plan or Annual Plan

processes.

· Approving Capital

Programme investment cases, and associated operational expenditure, as agreed

in the Council’s Long-Term Plan.

· Approving any capital or

other carry-forward requests and the use of operating surpluses.

· Approving the procurement

plans (where applicable), preferred supplier, and contracts for all capital

expenditure where the value of the contract exceeds $15 million (noting that

the Committee may sub-delegate authority for approval of the preferred supplier

and /or contract to the Chief Executive, conditional on compliance with the

procurement plan strategy).

· Approving

the

procurement plans (where applicable),

preferred supplier,

and contracts, for

all operational

expenditure

where the value of the contract exceeds $10 million (noting

that

the Committee may sub-delegate

authority for approval of the preferred supplier and/or contract to the Chief Executive, conditional on compliance with the procurement plan strategy).

Non-financial performance

· Reviewing the delivery of services

under s17A.

· Amending

levels of service

targets, unless the decision is precluded

under section 97 of the Local Government Act 2002.

· Exercising all of the Council's powers

under section 17A of the Local

Government Act 2002, relating to service

delivery reviews and decisions not to undertake a review.

·

Exercising all of the Council's powers under

section 17A of the Local Government Act 2002, relating to service delivery

reviews and decisions not to undertake a review.

Council Controlled Organisations

· Monitoring the financial and non-financial

performance of the Council

and Council-controlled Organisations.

· Making governance decisions

related to Council

Controlled Organisations under sections 65

to 72 of the

Local Government Act

2002.

· Exercising the

Council’s powers directly as the shareholder, or through CCHL, or in

respect of an entity

(within

the meaning of section

6(1) of the Local Government Act 2002) in relation to:

-

(without limitation)

the

modification of constitutions and/or trust deeds, and

other governance arrangements,

granting shareholder approval of

major transactions,

appointing directors or trustees, and approving

policies related

to Council Controlled

Organisations; and

-

in relation to

the approval of Statements of Intent and

their modification (if any).

Development

Contributions

· Exercising all of the Council's powers

in relation to development

contributions,

other than those delegated to the Chief Executive and

Council officers as set out in the Council's Delegations Register.

Property

· Purchasing or disposing of property where required for the delivery of the Capital Programme, in accordance with

the

Council’s Long-Term Plan, and where those

acquisitions or disposals

have

not

been delegated to another decision-making body of the

Council or staff.

Loans and debt write-offs

· Approving

debt write-offs

where those debt write-offs

are not delegated

to

staff.

· Approving

amendments to

loans, in accordance with the Council’s Long-Term Plan.

Insurance

· All insurance matters, including considering

legal advice from the Council’s legal and

other advisers, approving further actions

relating

to

the issues, and authorising

the taking of formal actions

(Sub-delegated

to

the Insurance Subcommittee

as per the Subcommittees

Terms of Reference).

Annual Plan and Long Term Plan

· Providing

oversight and monitoring

development of the Long Term Plan (LTP) and Annual

Plan.

Submissions

· The Council delegates to

the

Committee authority:

-

To consider

and

approve draft

submissions on behalf of the

Council on topics within its

terms of reference. Where the timing of a consultation does

not allow for consideration of a draft submission by the Council

or relevant Committee,

the

draft submission can

be considered and

approved on behalf of the

Council.

Limitations

·

The general delegations to this Committee

exclude any specific decision-making powers that are delegated to a Community

Board, another Committee of Council or Joint Committee. Delegations to staff

are set out in the delegations register.

· The

Council retains the authority to adopt policies, strategies and bylaws.

The following matters

are prohibited from being subdelegated in accordance with LGA 2002 Schedule 7

Clause 32(1) :

· the power to make a rate; or

· the power to make a bylaw; or

· the power to borrow money, or purchase or dispose of assets, other

than in accordance with the long-term plan; or

· the power to adopt a long-term plan, annual plan, or annual report;

or

· the power to appoint a chief executive; or

· the power to adopt policies required to be adopted and consulted on

under this Act in association with the long-term plan or developed for the

purpose of the local governance statement; or

·

the power to adopt a remuneration and employment

policy.

Chairperson

may refer urgent matters to the Council

As may be necessary from

time to time, the Committee Chairperson is authorised to refer urgent matters

to the Council for decision, where this Committee would ordinarily have

considered the matter. In order to

exercise this authority:

· The Committee Advisor must inform the Chairperson in writing of the

reasons why the referral is necessary

· The Chairperson must then respond to the Committee Advisor in

writing with their decision.

· If the Chairperson agrees to refer the report to the Council, the

Council may then assume decision-making authority for that specific report.

Urgent

matters referred from the Council

As may be necessary

from time to time, the Mayor is authorised to refer urgent matters to this

Committee for decision, where the Council would ordinarily have considered the

matter, except for those matters listed in the limitations above.

In order to

exercise this authority:

·

The Council Secretary must inform the Mayor and

Chief Executive in writing of the reasons why the referral is necessary

·

The Mayor and Chief Executive must then respond

to the Council Secretary in writing with their decision.

If the Mayor

and Chief Executive agree to refer the report to the Committee, the Committee

may then assume decision-making authority for that specific report.

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

TABLE OF CONTENTS NGĀ IHIRANGI

Karakia Tīmatanga.................................................................. 7

C 1. Apologies Ngā Whakapāha...................................... 7

B 2. Declarations of Interest Ngā Whakapuaki Aronga..... 7

C 3. Confirmation of Previous Minutes Te Whakaāe o te

hui o mua............................................................... 7

B 4. Public Forum Te Huinga Whānui.............................. 7

B 5. Deputations by Appointment Ngā Huinga

Whakaritenga......................................................... 7

B 6. Presentation

of Petitions Ngā

Pākikitanga............... 7

Staff Reports

B 7. Key

Organisational Performance Results - November 2025............................................ 17

B 8. Financial

Performance Report - November 2025 67

B 9. Capital

Programme Performance Report November 2025............................................ 71

C 10. Draft Council

submissions on Building and Construction Sector Amendment Bills.......... 105

C 11. Ōtautahi

Community Housing Trust: Request to Approve Subsidiary..................................... 113

C 12. Confirmation of

content - Draft Annual Plan 2026/27...................................................... 123

B 13. Christchurch

City Holdings Ltd - Quarter 1 2025/26 Performance Report....................... 149

C 14. Appointment of

an Elected Member to the Board of Christchurch City Holdings Ltd....... 167

Governance Items

C 15. Notice of

Motion - Letter to Central Government regarding paying rates on Crown owned

properties.................................................. 175

C 16. Resolution to

Exclude the Public.................. 178

Karakia Whakamutunga

Actions Register Ngā Mahinga Tuwhera

Karakia Tīmatanga

Whakataka te hau ki te uru

Whakataka te hau ki te tonga

Kia mākinakina ki uta

Kia mātaratara ki tai

E hī ake ana te atakura

He tio, he huka, he hau hū

Tihei mauri ora

1. Apologies Ngā Whakapāha

Apologies will

be recorded at the meeting.

2. Declarations of Interest Ngā

Whakapuaki Aronga

Members are

reminded of the need to be vigilant and to stand aside from decision-making

when a conflict arises between their role as an elected representative and any

private or other external interest they might have.

3. Confirmation of Previous Minutes Te

Whakaāe o te hui o mua

That the

minutes of the Finance and Performance Committee meeting held on Wednesday, 26 November 2025 be

confirmed (refer page 8).

4. Public Forum Te Huinga Whānui

A period of up

to 30 minutes will be available for people to speak for up to five minutes on

any issue that is not the subject of a separate hearing process.

|

4.1

|

Harrison McEvoy

Harrison McEvoy will speak on rates

capping.

|

5. Deputations by Appointment Ngā Huinga Whakaritenga

Deputations may

be heard on a matter or matters covered by a report on this agenda and approved

by the Chairperson.

Deputations will

be recorded in the meeting minutes.

6. Presentation of Petitions Ngā

Pākikitanga

There were no petitions

received at the time the agenda was prepared.

To present to the Committee,

refer to the Participating in decision-making webpage or

contact the meeting advisor listed on the front of this agenda.

Finance and Performance Committee

Open Minutes

Date: Wednesday 26 November 2025

Time: 9.30 am

Venue: Camellia Chambers, Civic Offices,

53 Hereford Street, Christchurch

Present

|

Chairperson

Deputy Chairperson

Members

|

Councillor Sam MacDonald

Councillor Jake McLellan

Mayor Phil Mauger

Deputy Mayor Victoria Henstock

Councillor David Cartwright

Councillor Melanie Coker

Councillor Pauline Cotter

Councillor Kelly Barber

Councillor Celeste Donovan

Councillor Tyla Harrison-Hunt

Councillor Nathaniel Herz Jardine

Councillor Yani Johanson

Councillor Aaron Keown

Councillor Andrei Moore

Councillor Mark Peters

Councillor Tim Scandrett

|

Website: www.ccc.govt.nz

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

1. Apologies

Ngā Whakapāha

Part C

|

Committee Resolved FPCO/2025/00143

That the apologies from Deputy Mayor

Henstock for lateness and Councillor Fields for absence be accepted.

Councillor

MacDonald/Councillor McLellan Carried

|

Councillor Moore joined the meeting at 9.31

am during Karakia Tīmatanga.

Karakia Tīmatanga

2. Declarations

of Interest Ngā Whakapuaki Aronga

Part B

There were no

declarations of interest recorded.

3. Public

Forum Te Huinga Whānui

Part B

There were no public forum presentations.

4. Deputations

by Appointment Ngā Huinga Whakaritenga

Part B

There were no deputations by appointment.

5. Presentation

of Petitions Ngā Pākikitanga

Part B

There was no presentation of petitions.

Mayor Mauger joined the meeting at 9.34 am

during consideration of Item 6.

Deputy Mayor Henstock joined the meeting at

9.43 am during consideration of Item 6.

|

6. Key

Organisational Performance Results - October 2025

|

|

|

Committee Resolved FPCO/2025/00144

Officer Recommendation accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives the information in the Key

Organisational Performance Results - October 2025 Report.

Mayor/Councillor

McLellan Carried

|

For

|

16

|

Councillor Barber, Councillor

Cartwright, Councillor Coker, Councillor Cotter, Councillor Donovan,

Councillor Harrison-Hunt, Councillor Herz Jardine, Councillor Johanson,

Councillor Keown, Councillor MacDonald, Councillor McLellan, Councillor

Moore, Councillor Peters, Councillor Scandrett, Deputy Mayor Henstock,

Mayor Mauger

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

16

|

|

|

|

|

|

|

Absent

|

1

|

Councillor Fields

|

|

|

7. Financial

Performance Report - October 2025

|

|

|

Committee Resolved FPCO/2025/00145

Officer Recommendation accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives the information in the Financial

Performance Report - October 2025 Report.

Councillor

MacDonald/Councillor McLellan Carried

|

For

|

16

|

Councillor Barber, Councillor

Cartwright, Councillor Coker, Councillor Cotter, Councillor Donovan,

Councillor Harrison-Hunt, Councillor Herz Jardine, Councillor Johanson,

Councillor Keown, Councillor MacDonald, Councillor McLellan, Councillor

Moore, Councillor Peters, Councillor Scandrett, Deputy Mayor Henstock,

Mayor Mauger

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

16

|

|

|

|

|

|

|

Absent

|

1

|

Councillor Fields

|

|

|

|

|

|

8. Capital

Programme Performance Report October 2025

|

|

|

Committee Resolved FPCO/2025/00146

Officer Recommendations accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives the information in the Capital

Programme Performance Report October 2025.

2. Confirms the draft set of FY26 Watchlist

projects (as set out in Attachment B).

Deputy

Mayor/Councillor Donovan Carried

|

For

|

16

|

Councillor Barber, Councillor

Cartwright, Councillor Coker, Councillor Cotter, Councillor Donovan,

Councillor Harrison-Hunt, Councillor Herz Jardine, Councillor Johanson,

Councillor Keown, Councillor MacDonald, Councillor McLellan, Councillor

Moore, Councillor Peters, Councillor Scandrett, Deputy Mayor Henstock,

Mayor Mauger

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

16

|

|

|

|

|

|

|

Absent

|

1

|

Councillor Fields

|

|

|

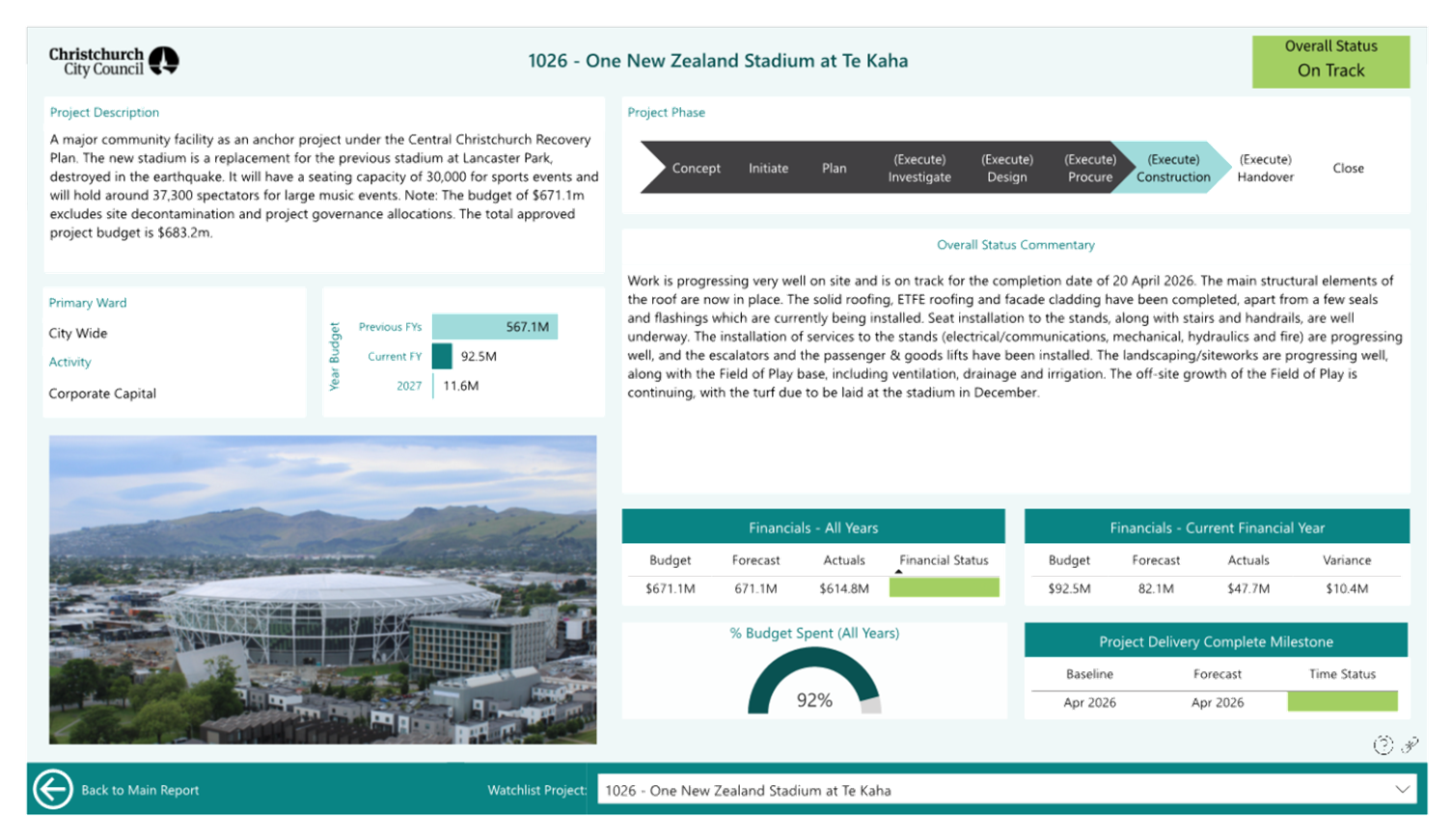

9. One

New Zealand Stadium at Te Kaha - Elected Members' Update

|

|

|

Committee Resolved FPCO/2025/00147

Officer Recommendation accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives the information in the One New

Zealand Stadium at Te Kaha - Elected Members' Update Report.

Councillor

Peters/Mayor Carried

|

For

|

16

|

Councillor Barber, Councillor

Cartwright, Councillor Coker, Councillor Cotter, Councillor Donovan,

Councillor Harrison-Hunt, Councillor Herz Jardine, Councillor Johanson,

Councillor Keown, Councillor MacDonald, Councillor McLellan, Councillor

Moore, Councillor Peters, Councillor Scandrett, Deputy Mayor Henstock,

Mayor Mauger

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

16

|

|

|

|

|

|

|

Absent

|

1

|

Councillor Fields

|

|

Mayor Mauger left the meeting at 10.44 am

during consideration of Item 10.

|

10. Christchurch

City Holdings Ltd - Annual Report 2024/25

|

|

|

Committee Resolved FPCO/2025/00148

Officer Recommendation accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives Christchurch City Holdings Ltd -

Annual Report 2024/25.

Councillor

Keown/Councillor MacDonald Carried

|

For

|

15

|

Councillor Barber, Councillor

Cartwright, Councillor Coker, Councillor Cotter, Councillor Donovan,

Councillor Harrison-Hunt, Councillor Herz Jardine, Councillor Johanson,

Councillor Keown, Councillor MacDonald, Councillor McLellan, Councillor

Moore, Councillor Peters, Councillor Scandrett, Deputy Mayor Henstock

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

15

|

|

|

|

|

|

|

Absent

|

2

|

Councillor Fields, Mayor Mauger

|

|

|

|

Attachments

a Item

10 - Christchurch City Holdings Ltd Presentation to Committee

|

Councillor Barber left the meeting at 10.55

am and returned at 10.58 am during consideration of Item 11.

Councillor Cotter left the meeting at 10.58

am and returned at 11.01 am during consideration of Item 11.

|

11. ChristchurchNZ

Holdings Ltd - Annual Report 2024/25

|

|

|

Committee Resolved FPCO/2025/00149

Officer Recommendation accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives the information in the ChristchurchNZ

Holdings Ltd - Annual Report 2024/25 and Quarter 1

2025/26 Performance Report.

Councillor Herz

Jardine/Councillor Scandrett Carried

|

For

|

15

|

Councillor Barber, Councillor

Cartwright, Councillor Coker, Councillor Cotter, Councillor Donovan,

Councillor Harrison-Hunt, Councillor Herz Jardine, Councillor Johanson,

Councillor Keown, Councillor MacDonald, Councillor McLellan, Councillor

Moore, Councillor Peters, Councillor Scandrett, Deputy Mayor Henstock

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

15

|

|

|

|

|

|

|

Absent

|

2

|

Councillor Fields, Mayor Mauger

|

|

|

|

Attachments

a Item

11 - ChristchurchNZ Holdings Ltd Presentation to Committee

|

The meeting adjourned at 11.19 am and

reconvened at 11.39 am.

The Mayor returned to the meeting at this

time. Councillors Barber and Johanson were not present at this time.

|

12. Council-controlled

Organisations - Annual Reports 2024/25

|

|

|

Committee Resolved FPCO/2025/00150

Officer Recommendations accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives the Annual Reports for 2024/25 with audited financial

statements for the following Council-controlled Organisations:

· Transwaste

Canterbury Ltd;

· Riccarton Bush

Trust;

· Rod Donald Banks

Peninsula Trust; and

· Te Kaha Project

Delivery Ltd.

2. Notes that all the above entities received unmodified audit

opinions.

3. Receives the Quarter 1 2025/26 Performance Report for Te Kaha

Project Delivery Ltd; and

4. Receives the Half Year Report 2025 for Civic Financial Services.

Councillor

MacDonald/Councillor Moore Carried

|

For

|

14

|

Councillor Cartwright, Councillor Coker,

Councillor Cotter, Councillor Donovan, Councillor Harrison-Hunt, Councillor

Herz Jardine, Councillor Keown, Councillor MacDonald, Councillor McLellan,

Councillor Moore, Councillor Peters, Councillor Scandrett, Deputy Mayor

Henstock, Mayor Mauger

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

14

|

|

|

|

|

|

|

Absent

|

3

|

Councillor Barber, Councillor Fields,

Councillor Johanson

|

|

|

|

|

Councillor Johanson returned to the meeting

at 11.40 am during consideration of Item 13.

|

13. Council-controlled

organisations - Annual General Meetings by Written Resolution

|

|

|

Committee Resolved FPCO/2025/00151

Officer Recommendations accepted without

change

Part C

That the

Finance and Performance Committee:

1. Agrees to pass shareholder resolutions for the 2025 annual

meetings of the following Council-controlled organisations:

a. non-trading

‘shelf’ companies - CCC One Ltd, CCC Five Ltd, CCC Seven Ltd and

Ellerslie International Flower Show Ltd; and

b. trading

companies –Te Kaha Project Delivery Ltd and Venues Ōtautahi Ltd;

and

2. Notes that the decisions in this report are assessed as low

significance based on the Christchurch City Council’s Significance and

Engagement Policy.

Councillor

MacDonald/Councillor Moore Carried

|

For

|

15

|

Councillor Cartwright, Councillor Coker,

Councillor Cotter, Councillor Donovan, Councillor Harrison-Hunt, Councillor

Herz Jardine, Councillor Johanson, Councillor Keown, Councillor MacDonald,

Councillor McLellan, Councillor Moore, Councillor Peters, Councillor

Scandrett, Deputy Mayor Henstock, Mayor Mauger

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

15

|

|

|

|

|

|

|

Absent

|

2

|

Councillor Barber, Councillor Fields

|

|

|

14. Resolution

to Exclude the Public Te whakataunga kaupare hunga tūmatanui

|

|

|

Committee Resolved FPCO/2025/00152

Part C

That at

11.40 am the resolution to exclude the public set out on pages 521 to 522 of

the agenda be adopted.

Councillor

MacDonald/Councillor Moore Carried

|

For

|

15

|

Councillor Cartwright, Councillor Coker,

Councillor Cotter, Councillor Donovan, Councillor Harrison-Hunt, Councillor

Herz Jardine, Councillor Johanson, Councillor Keown, Councillor MacDonald,

Councillor McLellan, Councillor Moore, Councillor Peters, Councillor

Scandrett, Deputy Mayor Henstock, Mayor Mauger

|

|

Against

|

0

|

|

|

Abstain

|

0

|

|

|

Total

|

15

|

|

|

|

|

|

|

Absent

|

2

|

Councillor Barber, Councillor Fields

|

|

The public were re-admitted to the meeting

at 11.52 am.

Karakia

Whakamutunga

Meeting

concluded at 11.53 am.

CONFIRMED THIS 17th DAY OF

DECEMBER 2026

Councillor Sam MacDonald

Chairperson

|

7. Key

Organisational Performance Results - November 2025

|

|

Reference Te Tohutoro:

|

25/2438129

|

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 To

provide Council with an overview of organisational performance that is tracking

progress towards delivering the second year of its Long-Term Plan 2024-34

(LTP), our ‘contract with the community’. This report is for

the five months ended 30 November 2025.

1.2 This

is a staff generated report presented monthly to the Committee.

2. Officer Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Key Organisational Performance Results -

November 2025 Report.

3. Background/Context Te Horopaki

3.1 This

is a standing report focused on a suite of the ‘vital few’

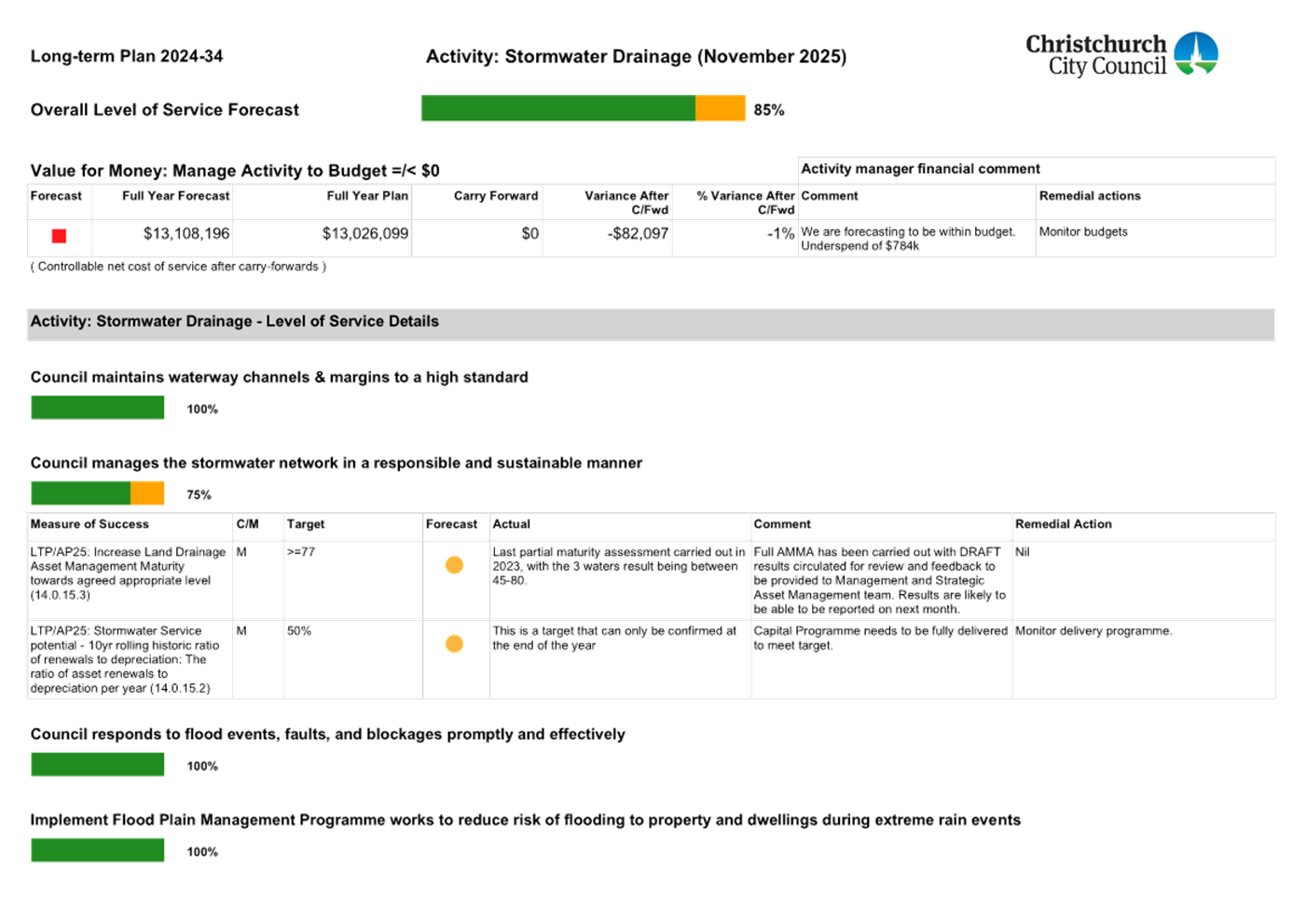

organisational performance targets and is a key component of the

Council’s Performance Framework and its reporting.

4. Considerations Ngā Whai Whakaaro

4.1 The

key organisational performance targets include:

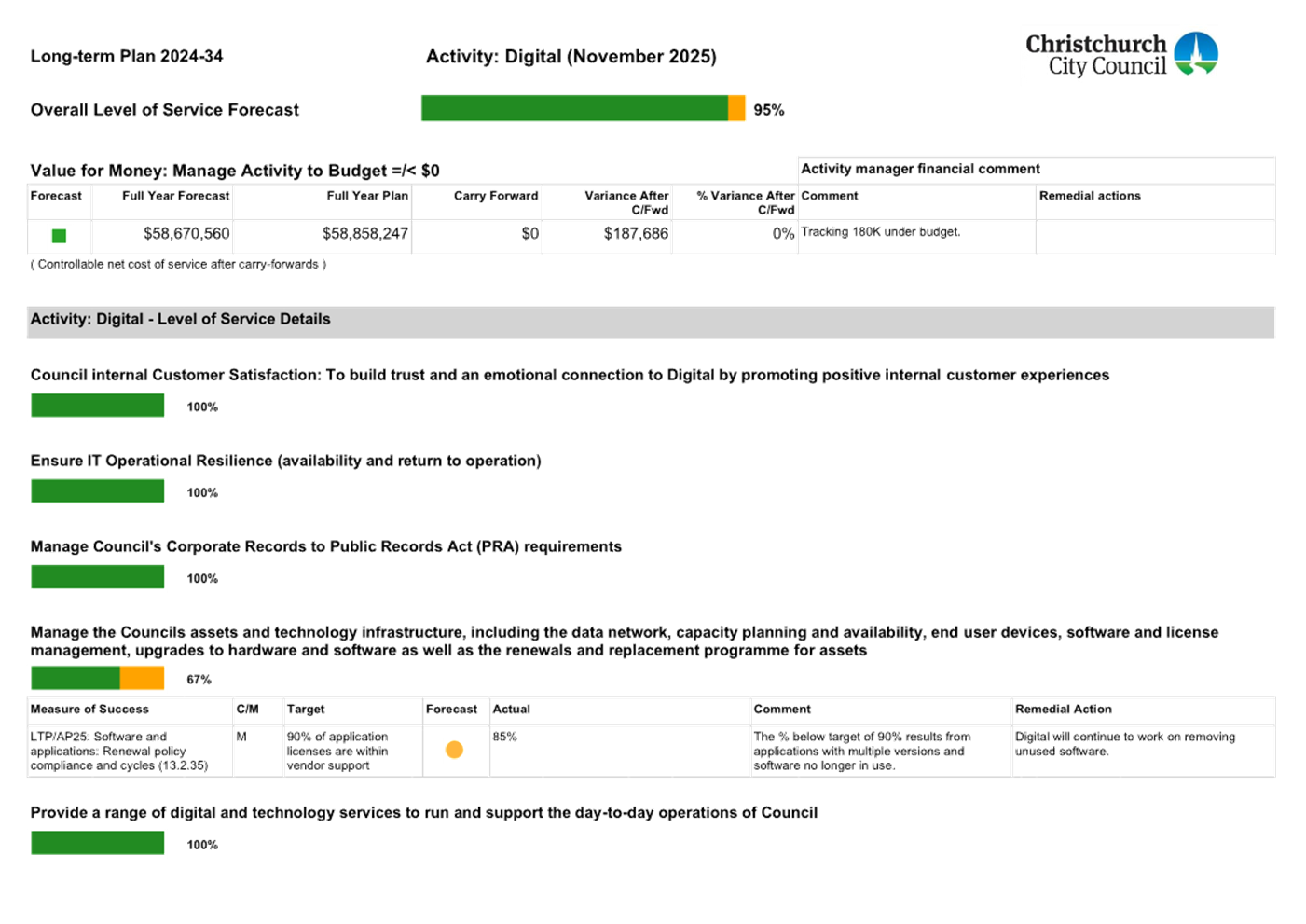

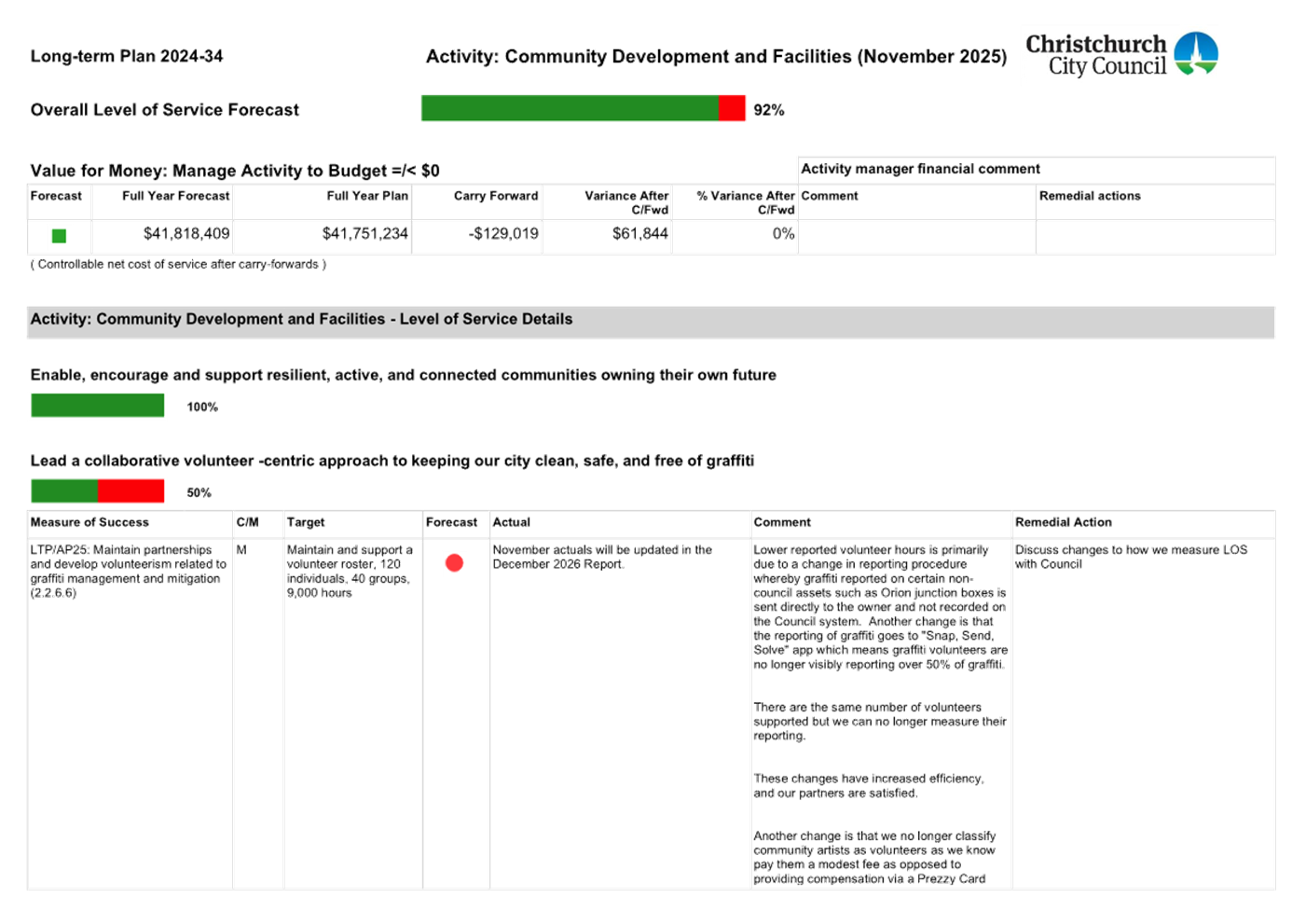

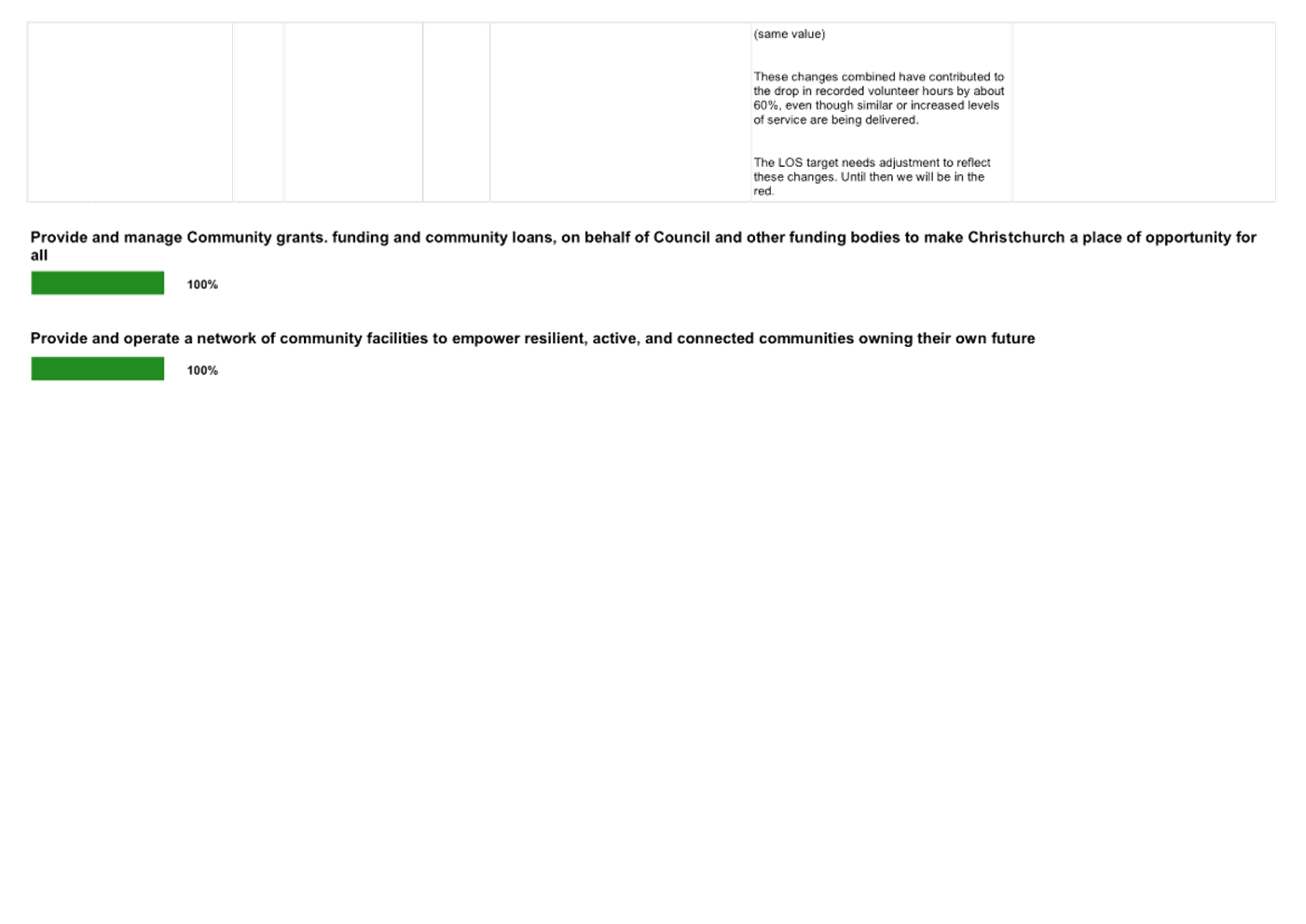

· Service Delivery (levels of service (LOS)).

· Capital Projects (both milestone delivery and planning).

· Value for Money (finance – activity budgets and capital programme budgets).

4.2 This

report provides, as at the end of November 2025, the year-end performance

forecasts against the Executive Leadership Team’s (ELT) performance

priority targets for year two of the LTP 2024-34.

4.3 The

table below summarises performance against the targets.

4.4 Community Level of Service

delivery is forecast at 89.6%, it is showing improvement from reporting for

October and is slightly ahead of the year end (YE) position for 2024/25 and is

tracking to achieve the ELT performance target of 85%.

4.4 Community Level of Service

delivery is forecast at 89.6%, it is showing improvement from reporting for

October and is slightly ahead of the year end (YE) position for 2024/25 and is

tracking to achieve the ELT performance target of 85%.

4.5 Management

Level of Service delivery is forecast at 90.1%, it is showing a slight increase

from reporting for October and is also slightly ahead of the YE position for

2024/25 and is tracking to achieve the ELT performance target of 85%.

4.6 Watchlist

project milestone delivery is forecast at 59.1%, showing a decrease from

October reporting of 72.2%. The significance difference is due to changes

to the Watchlist projects agreed with the Committee at the November meeting

(refer paragraph 6.3 and Attachment B for further detail). Presently

this measure is behind the combined YE result for 2024/25 (80.2%), the target

of 85% is forecast to not be met.

4.7 Non

watchlist project milestone delivery is forecast at 79.8%, remaining generally

stable from October reporting, and slightly behind the previous YE position

(80.2%). This measure is also forecast to not achieve the ELT performance

target of 85%.

4.8 FY2027 Capital programme

planning is forecast at 89.6%. It is expected the

ELT performance target of 90% will be met.

4.9 FY2028/2029

Capital programme planning is forecast at 81.3%, a reduction from reporting for

October due to revised calculations (see paragraphs 6.8 - 6.9 below for more

information).

4.10 Activity

budgets, actively managed to budget is forecast at 92.3%, an improvement on

reporting for October. While some activities are

unfavourable against budget, overall Council is within budget.

4.11 Deliver

Capital Programme within approved budget is forecast at -10.9%, consistent with

October, and is presently forecast to not achieve the ELT target of 0% to -10%.

4.12 Further detail and explanation of forecast

performance against each of ELT’s targets is provided below.

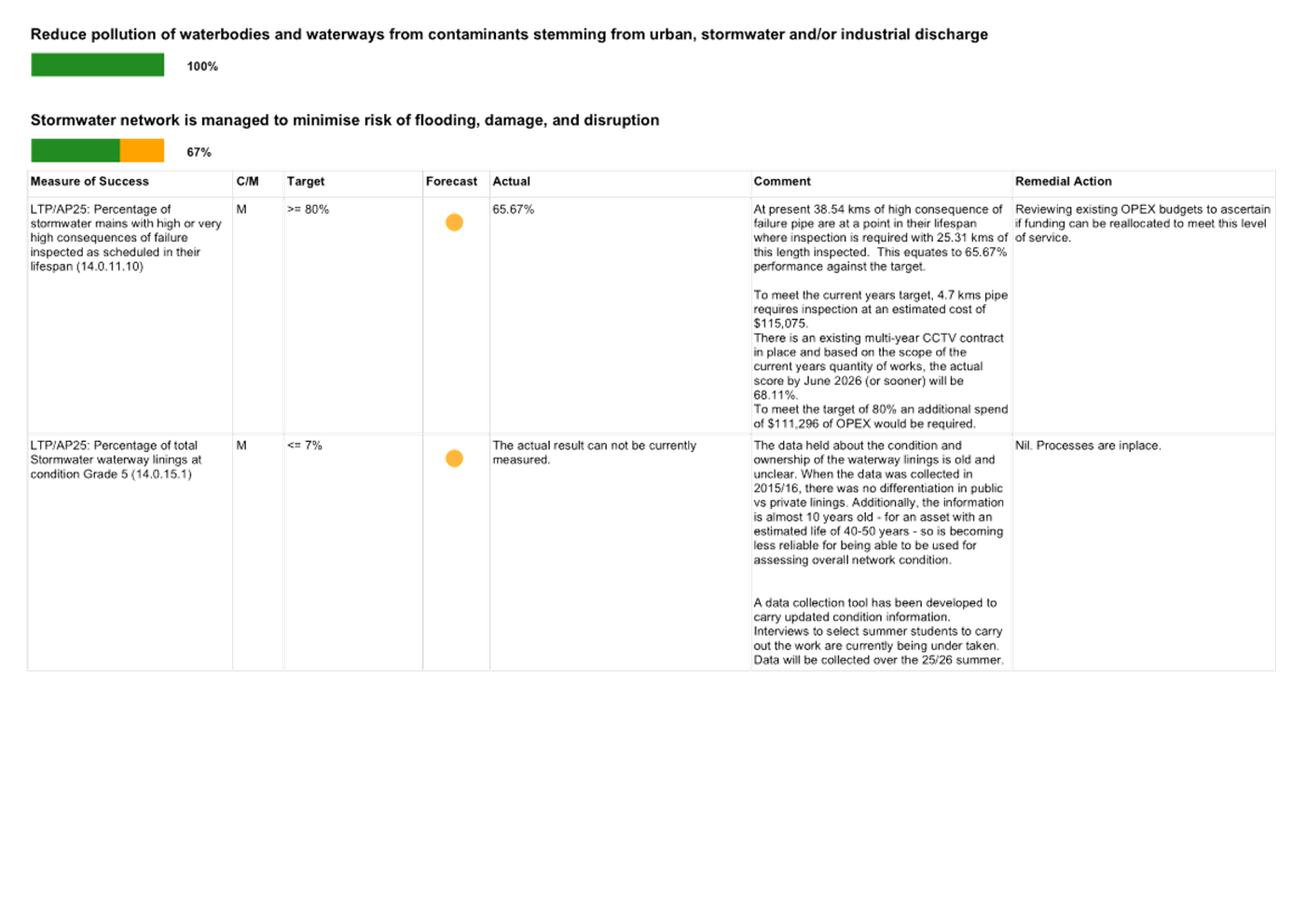

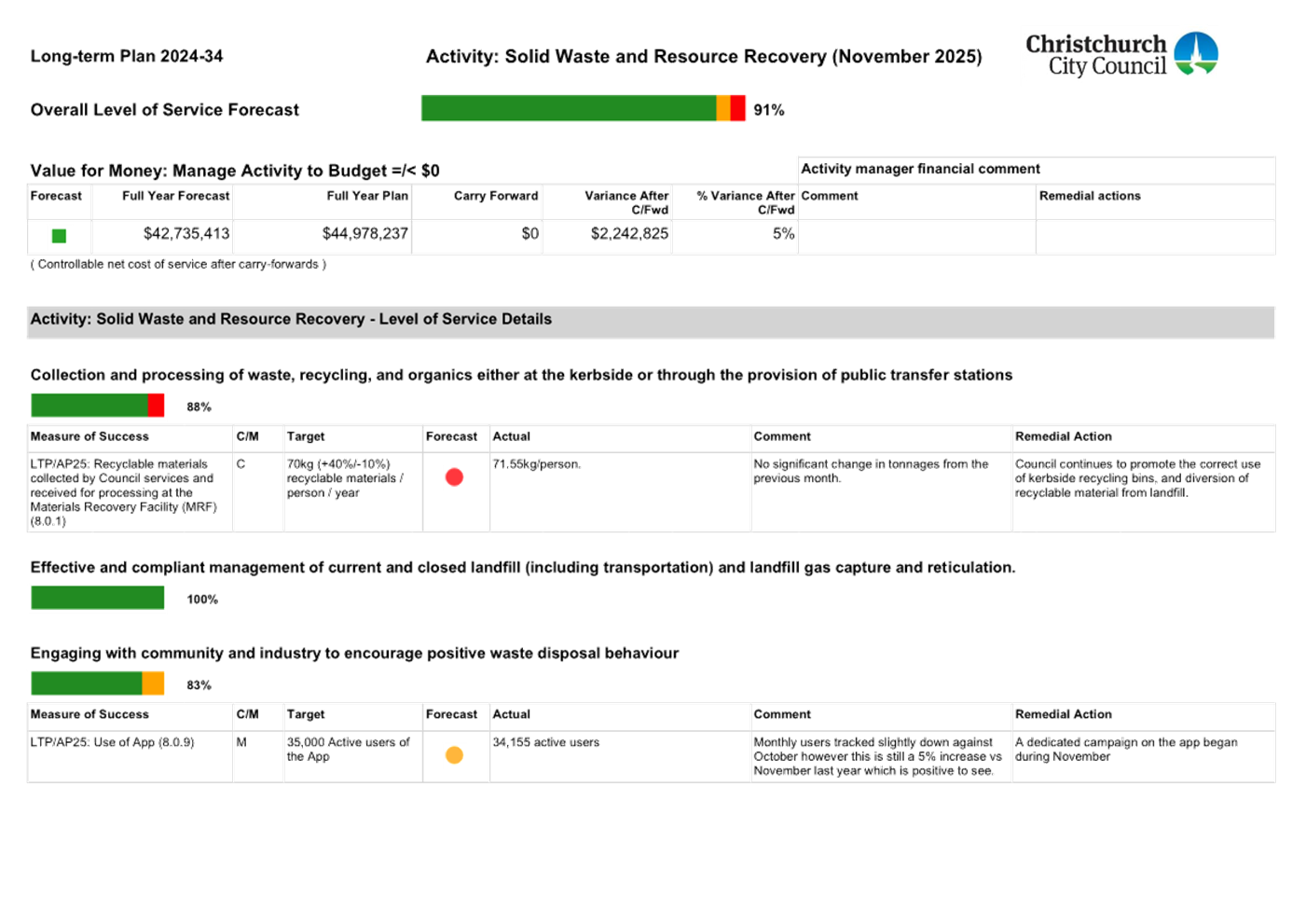

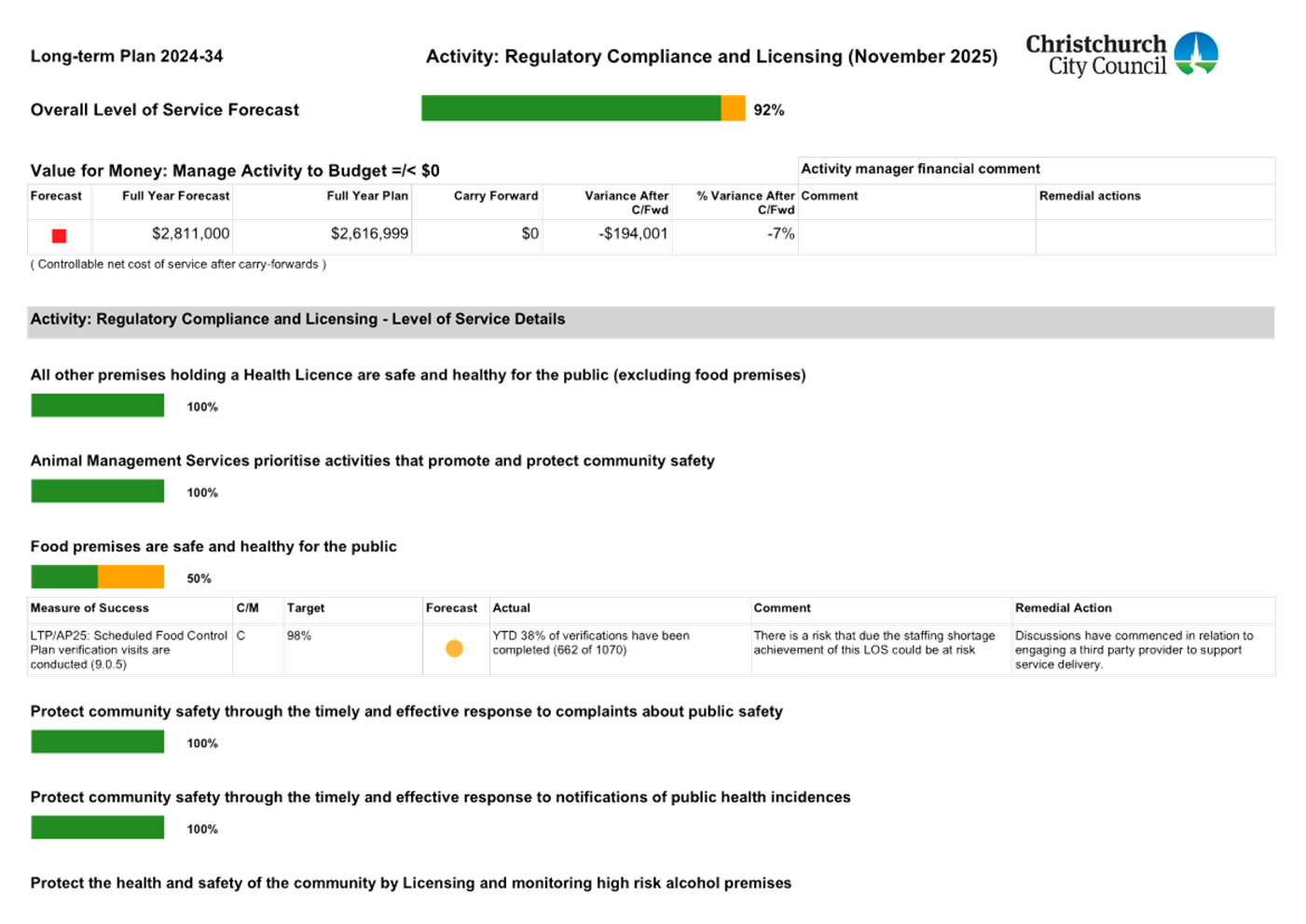

5. Service Delivery

5.1  The table below provides a summary of forecast level of service

achievement for the organisation (all activities) against the performance

targets. Additional information provides context and background; whether the

target is forecast to be met, percentage forecast variance and relative

movement compared to the previous reporting period, a count of levels of

service, and the last three years year-end performance results.

The table below provides a summary of forecast level of service

achievement for the organisation (all activities) against the performance

targets. Additional information provides context and background; whether the

target is forecast to be met, percentage forecast variance and relative

movement compared to the previous reporting period, a count of levels of

service, and the last three years year-end performance results.

*B = Black, no data. R = Red, will miss

target. A = Amber, requires intervention. G = Green, will achieve target.

5.2 Community

Level of Service delivery is forecast at 89.6%, an increase of 1.0% from

reporting for October and ahead of the year-end June 2025 result, 87.5%.

5.3 Management

Level of Service delivery is forecast at 90.1%, an increase of 0.7% from

reporting for October. The forecast remains consistent with the year-end

position for 2024/25 (89.1%).

5.4 Both

targets are forecast to be met.

5.5 Attachment

A, provides details for levels of service exceptions, including manager

comments and remedial actions.

5.6 The

scatter-diagram below shows forecast activity LOS delivery performance

(Community and Management LOS), against forecast activity budget performance

(over- or under-spend), noting:

· across all listed

activities, level of service delivery forecasts ranges from 67.7% to 100%

· the vertical y-axis shows

forecast service delivery (LOS) performance.

· the horizontal x-axis shows forecast budget over/underspend (scaled

to relative budget).

· while some activities are unfavourable against budget overall

Council is within budget.

5.7 The

table below provides further detail on all of Council’s activities, and

their forecast level of service delivery against budget.

5.7 The

table below provides further detail on all of Council’s activities, and

their forecast level of service delivery against budget.

6. ELT

Performance Priority: Capital Projects delivery

6. ELT

Performance Priority: Capital Projects delivery

6.1  The table below provides a summary of the capital project delivery

against milestones. Note, information relating to spend against budget is shown

at paragraph 7.4 below (also referenced in the Financial Performance and the

Capital Programme Performance Reports).

The table below provides a summary of the capital project delivery

against milestones. Note, information relating to spend against budget is shown

at paragraph 7.4 below (also referenced in the Financial Performance and the

Capital Programme Performance Reports).

6.2 Capital

Watchlist project milestone delivery performance is forecast at 59.1%, a drop

from the 72.7% reported in October. This measure is forecast to not achieve the ELT target of 85%.

6.3 The

reason for the change is that the list of Watchlist projects was reviewed with

the Committee at the November meeting which saw eight projects removed (7 of

these forecast green/on track) and eight projects added (of which 4 are

forecast green/on track). While the overall number of reported projects remains

the same (22) the specific status of the selected projects is what has led to

the change in overall delivery forecast (decrease of 13.6% from 72.7% to

59.1%). Refer to Attachment B for the list of projects added and

removed.

6.4 Capital

Non-Watchlist projects milestone delivery performance is forecast at 79.8%,

which is also forecast to not achieve the ELT

target of 85%.

6.5 Both

forecasts are presently behind the overall combined capital project milestone

delivery result for 2024/25, 80.2%.

Capital project planning

6.6 Council

monitors capital project planning as lead indicators of future capital project

delivery. The table below summarises the forward view of project planning for

2027 and 2028/2029.

6.7 Capital projects planning %

for FY2027 is forecast at 89.6%, an increase of

1.5% from October reporting and remains forecast close to the ELT target of

90%. There is sufficient time remaining this financial year for this ELT

performance target to be met if current progress is maintained.

6.8 Capital

projects planning % for FY2028/2029 is forecast at 81.3%, a decrease of 8.6%

from what was reported in October. When preparing the

November reporting, a calculation error was identified for this ELT goal. The

calculations have been corrected in this month’s reporting. Adjusting for

the error and presenting the correct amounts for the previous three months the

results that would have been reported are as set out below:

|

|

August

|

September

|

October

|

|

Reported - in error

|

88.4%

|

88.0%

|

89.0%

|

|

Actual

|

79.2%

|

79.4%

|

80.5%

|

6.9 Noting the revised starting

point (79.2%), and progress to date (to 81.3% between August and November

2025), continued focus will be applied for the remainder of the financial year

for the 2028/2029 ELT planning target to be met.

6.10 For

further information and underlying project detail, refer to the Capital

Programme Performance Report.

7. ELT Performance Priority: Value for Money

7.1 A

key financial performance goal is Value for Money, used for monitoring both

operational and capital budget performance.

7.2  The table below summarises the year end position for all activities

(operational, whether activities are operating within the budgets for

controllable costs).

The table below summarises the year end position for all activities

(operational, whether activities are operating within the budgets for

controllable costs).

7.3 92.3%

(36/39) of activities are forecast to achieve budget (nett controllable cost,

after carry-forwards). While some activities are

unfavourable against budget, overall Council is within budget. Attachment A (summary of performance targets for

major Council activities, with detailed levels of service results, exceptions,

activity budget results, with manager commentary) and the Financial Performance

Report provide analysis of the exceptions and variances.

7.4 Monitoring

capital programme budget performance is also part of the Value for Money goal.

The table below summarises the forecast capital spend and indicates that

capital expenditure is forecast to not meet the ELT target of between 0% to

-10%.

7.5 Reporting

against the performance target includes Council’s core and externally

funded work, regardless of funding source, but excludes One New Zealand Stadium

at Te Kaha.

7.6 The

current year forecast variance of -10.9% remains generally consistent with

reporting for last month (October). This is based on the current year budget of

$561.3M against a forecast of $500M (underspend -$61.3M).

7.7 This

compares with the prior year’s year end, budget of $553.7M with

underspend of -$73.4M, a calculated unfavourable variance of -13.3%. More detailed information is available in the Financial and

Capital Programme Performance reports.

7.8 Set out below is the forward view of capital delivery performance for the LTP 2024-34

(financial), which looks at commitments for the first few years of the LTP

2024-34, accompanied by confirmed capital delivery in preceding LTP-cycles

against plan.

7.9 This view includes the

adopted capital programme from the LTP 2024-34 as updated through the 2025/26

Annual Plan.

7.10 The

view does include adjustments to budgets for years 2025/26 to 2027/28 for

carry-forwards (-$57.4M) as approved through the Financial Performance Report – June

2025, by Finance and Performance Committee, Part C

(3)), noting however that the forecast capital programme for outer years do not

yet incorporate the updates from the PMO’s review of deliverability.

7.11 The

extended black line is the full planned delivery budget including One New

Zealand Stadium at Te Kaha (as adopted through the Annual Plan 2025/2026),

including confirmed carry forwards.

7.12 The extended blue line shows the full Council

planned delivery budget (excluding One New Zealand Stadium at Te Kaha,

including confirmed carry forwards):

· from a consistent $488M to

$483M planned budget for the previous three years (2021-2024);

· to $554M for 2025, to

between $561M to $775M (back to $711M) planned budget for the years

(2026-2028).

7.13 The Council capital delivery (green line) for

2025/2026 is forecasted at $500M against the programme budget of $561M

(rounded) (blue line). This equates to 89.1% of budget spent.

7.14 A

review of capital programme future years’ deliverability has been

undertaken with Council through a series of workshops, in preparation for the

Annual Plan 2026/27. Updates to the forecast capital programme will be

applied once Council formally adopt the changes (generally at the draft AP

and/or final AP adoption stage).

7.15 Figures

align with the Financial and Capital Programme Performance reports.

8. Responses to questions from Councillors

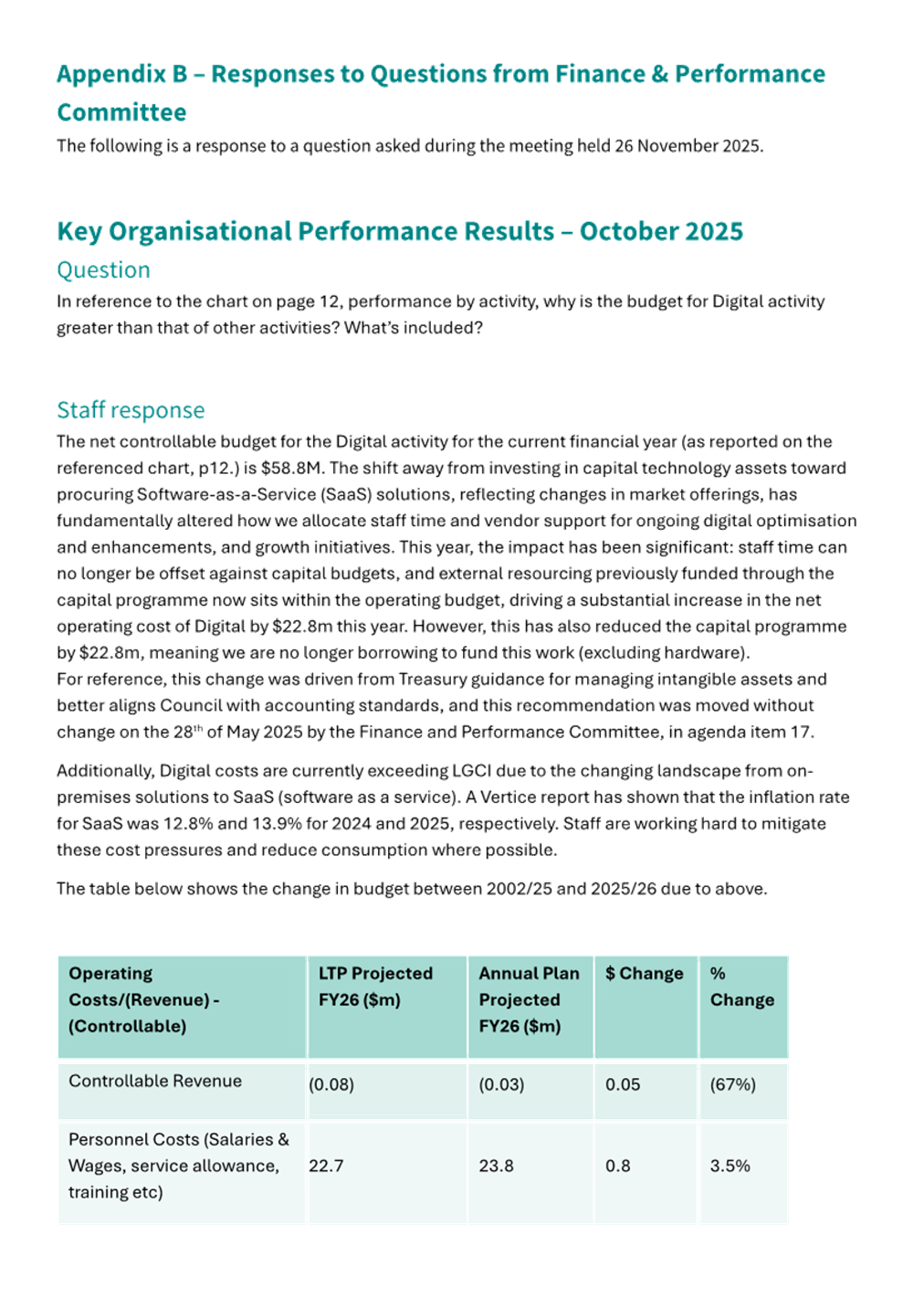

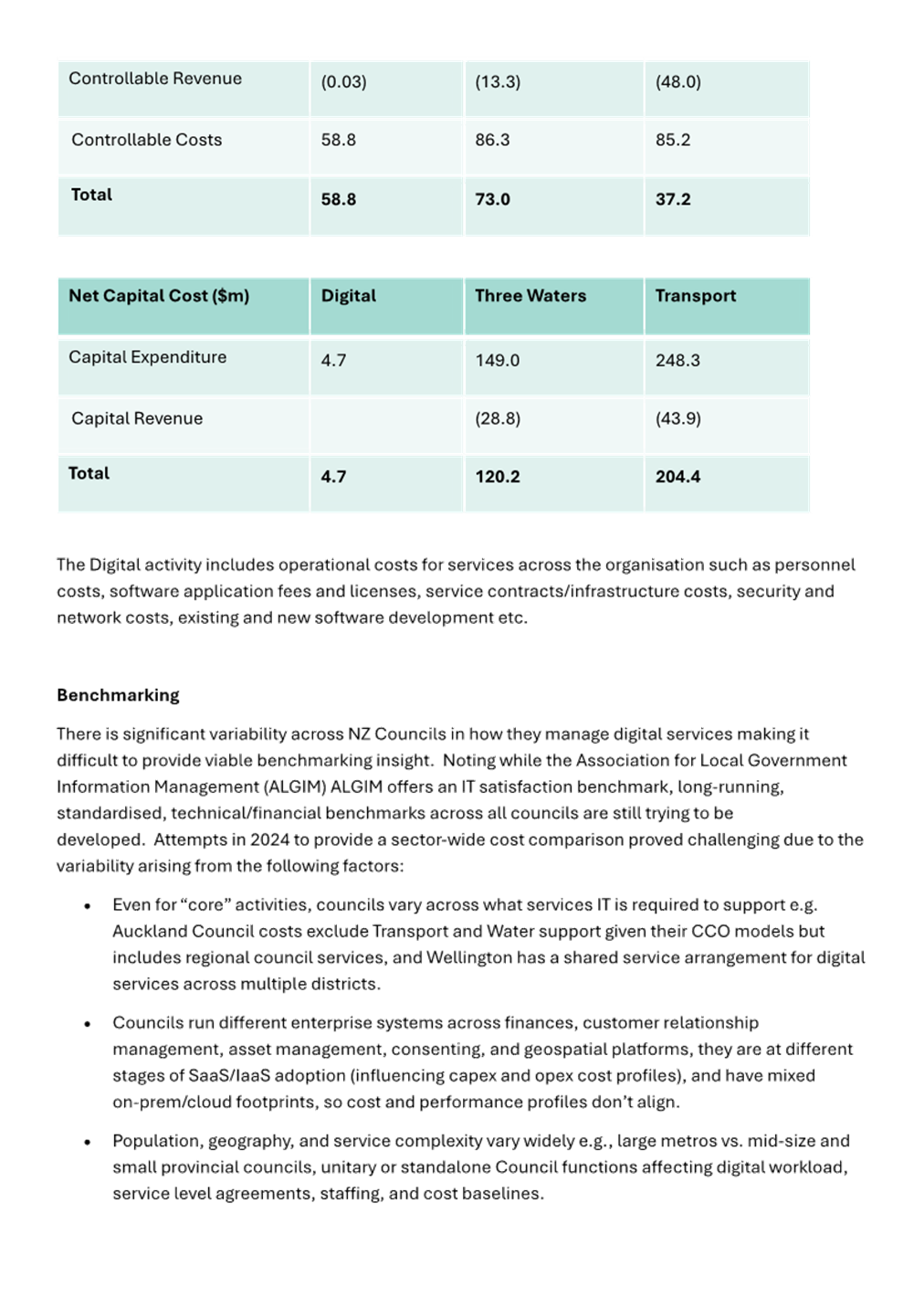

8.1 A

question was raised regarding the Digital spend at the last meeting: staff

responses to questions from Councillors asked at the Committee meeting of 26

November 2026 can be found in Attachment C.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Service

Delivery Summary (Levels of Service)

|

25/2511323

|

26

|

|

b ⇩

|

Watchlist

Projects as agreed with Finance and Performance Committee 26 November 2026

|

25/2559892

|

60

|

|

c ⇩

|

Staff

responses to Councillor questions

|

25/2533490

|

62

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Amber Tait -

Performance Analyst

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

|

|

8. Financial

Performance Report - November 2025

|

|

Reference Te Tohutoro:

|

25/2451456

|

|

Responsible Officer(s) Te Pou Matua:

|

Bruce

Moher, Head of Finance

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to inform

the Committee on Council's financial performance to 30 November 2025, which

includes providing an updated year-end forecast.

1.2 This is a standing report that is presented to

the Committee.

2. Officer Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Financial Performance Report - November 2025 Report.

3. Executive Summary Te Whakarāpopoto Matua

3.1 This is the second report for 2025/26 and the new triennium. There is no material change from the October report

regarding the year to date or forecast Opex and Capex position.

3.2 The

year-to-date operational surplus of $12.9 million is $30.2 million greater than

budget, slightly higher than the $27.7 million reported last month. This is

driven by: savings in insurance costs, reduced personnel costs due to staff

vacancies, lower than budgeted landfill and resource recovery operations

expenditure, a stronger than forecast building market increasing consenting

revenue, increased recreation and sports participation revenues, reduced

reactive infrastructure maintenance and late 24/25 rating growth.

3.3 The

forecast year end operating surplus is currently $16.9 million, a small

improvement from the $14.3 million reported in October. The forecast is driven

by: $2.3 million additional revenue, primarily related to interest earnings,

rates and rates penalties, and Land Information Memorandum (LIM) and property

files income. The improved year end forecast also reflects lower forecast

costs of approximately $15.8 million, mainly due to $7.1 million of insurance

renewal savings, $1.9 million of personnel cost savings due to vacancies, $2.3

million in landfill and resource recovery operations and reduced rates of $1.9

million on Council owned properties due to the rates reductions arising after

budgets had been set. $1.2 million of the surplus relates to and is retained in

the Housing Account.

3.4 Capital

expenditure is $46.8 million under budget year to date ($37.5 million in

October) primarily due to Transport ($18.1 million) and Three Waters ($18.1

million) projects. The Project Management Office (PMO) forecasts the underspend

to extend to $71.7 million by year end.

4. Operational Revenue and Expenditure

4.1 Operational

revenue and expenditure covers day to day spend on staffing, operations and

maintenance, and revenues to fund the operational spend.

4.2 Operational

revenue exceeds expenditure as it includes rates revenue for capital renewals

and debt repayment. This revenue is referred to below as ‘Funds not

available for Opex’ and is removed to show the year to date and forecast

cash operational surplus or deficit.

|

Year to Date Results

|

Forecast Year End Results

|

After Carry Forward

|

|

$m

|

Actual

|

Budget

|

Var

|

|

Forecast

|

Budget

|

Var

|

|

C/

fwd

|

Var

|

|

|

Operational

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenues

|

(519.7)

|

(515.2)

|

4.5

|

|

(1,146.8)

|

(1,144.5)

|

2.3

|

|

-

|

2.3

|

|

|

Expenditure

|

370.3

|

396.9

|

26.6

|

|

876.3

|

892.1

|

15.8

|

|

(0.1)

|

15.9

|

|

|

Funds not

available for Opex

|

136.5

|

135.6

|

(0.9)

|

|

253.6

|

252.4

|

(1.2)

|

|

0.1

|

(1.3)

|

|

|

Operating

(Surplus)/Deficit

|

(12.9)

|

17.3

|

30.2

|

|

(16.9)

|

-

|

16.9

|

|

-

|

16.9

|

|

4.3 After

five months the year to date operating surplus variance is $30.2 million and

forecast to reduce to $16.9 million by financial year end. Summaries of the

material revenue and expenditure variances and changes are highlighted below.

4.4 Revenue is $4.5 million more than budget year to date and

forecast to be $2.3 million more than budget at year end.

4.5 Key

drivers of actual and forecast revenue variances to budget include: [amounts in

() are unfavourable variances, i.e. revenues below budget]

|

Revenue Variance ($m)

|

Annual Budget

|

YTD

Variance

|

Forecast Variance

|

|

Building & Planning consent volumes

(refer also to cost variances)

|

37.2

|

2.8

|

-

|

|

Transport – NZTA, parking &

commercial rent

|

48.4

|

0.4

|

-

|

|

Recreation & Sports –

additional community participation

|

26.3

|

0.7

|

(0.3)

|

|

Interest earnings

|

38.4

|

0.1

|

1.0

|

|

Rates penalties

|

5.5

|

0.4

|

1.0

|

|

Rates – additional late growth

|

825.7

|

0.5

|

0.6

|

|

LIM & Property file volumes –

strong property market

|

3.3

|

0.5

|

0.8

|

|

Transwaste dividend – SOI update

|

5.6

|

0.1

|

(0.2)

|

|

Water Billing and Trade Waste revenue

|

12.8

|

(1.0)

|

-

|

|

Resource Recovery transfer stations,

organics processing and landfills

|

24.4

|

(0.5)

|

(0.9)

|

|

Other revenues

|

116.9

|

0.5

|

0.3

|

|

Total

|

1,144.5

|

4.5

|

2.3

|

4.6 Expenditure

is $26.6 million under budget year to date and forecast to be $15.9 million

(1.8%) under budget, after carry forwards, at year end.

4.7 Key

drivers of actual and forecast expenditure variances to budget include:

[amounts in () are unfavourable variances, i.e. expenses are greater than

budget]

|

Expenditure Variance ($m)

|

Annual Budget

|

YTD

Variance

|

Forecast Variance

|

|

Insurance – renewal savings

|

37.3

|

9.1

|

7.1

|

|

Personnel costs (units with vacancies which were

planned to be filled)

|

293.7

|

2.4

|

1.9

|

|

Waste Management lower recycling processing fees and

organic processing fees, and landfill costs

|

67.7

|

4.5

|

3.2

|

|

Three Waters – timing of reactive maintenance

& operating works and higher capitalisation rates

|

60.6

|

2.9

|

2.1

|

|

Parks – timing of activity

(pre-Spring) and no major fire or flooding events

|

20.7

|

1.0

|

0.3

|

|

Rates on Council owned properties

|

39.9

|

1.1

|

1.7

|

|

Digital – timing of software renewals and

portfolio delivery

|

35.0

|

0.9

|

-

|

|

Transport – timing of maintenance works

|

68.1

|

2.6

|

(0.6)

|

|

Riskpool insurance call

|

-

|

(0.4)

|

(0.4)

|

|

Governance – timing of remaining election

costs vs budget phasing

|

6.5

|

0.6

|

0.1

|

|

Other expenditure variances

|

262.6

|

1.9

|

0.4

|

|

Total

|

892.1

|

26.6

|

15.8

|

5. Capital Expenditure and Revenue

5.1 This

section covers the capital programme spend and funding relating to it (details

on the delivery of capital projects is contained in the Capital Programme

Performance Report).

|

Year to Date Results

|

Forecast Year End Results

|

After Carry Forwards

|

|

$m

|

Actual

|

Budget

|

Var

|

|

Forecast

|

Budget

|

Var

|

|

Carry Fwd

|

Var

|

|

|

Core Programme

|

174.9

|

220.3

|

45.4

|

|

516.8

|

561.3

|

44.5

|

|

30.5

|

14.0

|

|

|

Less unidentified

Carry Forwards

|

-

|

-

|

-

|

|

(16.8)

|

-

|

16.8

|

|

30.8

|

(14.0)

|

|

|

Core Programme

|

174.9

|

220.3

|

45.4

|

|

500.0

|

561.3

|

61.3

|

|

61.3

|

-

|

|

|

One New Zealand

Stadium at Te Kaha

|

47.6

|

49.0

|

1.4

|

|

82.1

|

92.5

|

10.4

|

|

10.4

|

-

|

|

|

Total Capital

Programme

|

222.5

|

269.3

|

46.8

|

|

582.1

|

653.8

|

71.7

|

|

71.7

|

-

|

|

|

Revenues and

Funding

|

(140.4)

|

(151.4)

|

(11.0)

|

|

(310.4)

|

(310.4)

|

-

|

|

-

|

-

|

|

|

Borrowing

required

|

82.1

|

117.9

|

35.8

|

|

271.7

|

343.4

|

71.7

|

|

71.7

|

-

|

|

Capital Expenditure

5.2 Capital expenditure is $46.8

million under budget year to date primarily due to Transport ($18.1 million)

and Three Waters ($18.1 million) projects.

5.3 The

PMO’s current core programme year end forecast is $500 million. This is

$61.3 million (11%) lower than budget, most of which

will likely be requested to be carried forward to future years. The project

managers’ forecast is currently $16.8 million higher than PMO’s at

$516.8 million. The primary reason for the variance is that the project

managers forecast on a project-by-project basis. In contrast the PMO

forecasts using a programme level analytical review and historic delivery

trends of prior years.

5.4 The

project managers core programme end of year forecast is $44.5 million (8%)

under budget before carry forwards due to underspends on three waters ($28.2

million, 11% of its total capex) and mainly related to delays arising from

dependencies on other project work proceeding, transport ($13.5 million, 9% of

its total capex) and landfill and transfer station projects ($6.9 million, 62%

of its total capex).

Capital Revenues and Funding

5.5 Capital revenues and funding is $11.0 million lower than budget year

to date. This is largely due to the timing of New Zealand Transport Agency

capex payments ($9.8 million), Parakiore and Court Theatre capital grant

receipts ($4.2 million), offset by higher Development Contributions (DCs) of

$2.9 million.

5.6 Capital

revenues and funding are forecast to align with budget by year end.

Attachments Ngā Tāpirihanga

There are no

attachments for this report.

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Mitchell Shaw

- Principal Advisor - Finance

Nick Dean -

Finance Business Partner

|

|

Approved By

|

Bruce Moher -

Head of Finance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

|

|

9. Capital Programme Performance

Report November 2025

|

|

Reference Te Tohutoro:

|

25/2445128

|

|

Responsible Officer(s) Te Pou Matua:

|

Paul

Dadson - Senior Capital Programme Advisor Parks & Facilities

|

|

Accountable ELT Member Pouwhakarae:

|

Brent

Smith, General Manager City Infrastructure

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to present the Finance and Performance Committee with

the Capital Programme Performance Report for November

2025. This report provides Elected Members with oversight on the

performance of the Capital Programme.

1.2 This

report has been prepared by the Programme Management Office.

2. Officer Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Capital Programme Performance Report November

2025.

3. Background/Context Te Horopaki

3.1 As

of November month-end, the FY26 year-end forecast for the overall capital

programme is $582.1m, or 89% of budget. This is based on the PMO

Forecast for CCC Capital, and the year-end forecast for One New Zealand Stadium

at Te Kaha.

3.2 For

CCC Capital (excluding One New Zealand Stadium at Te Kaha):

3.2.1 The

PMO Forecast for FY26 year-end remains at $500m, or 89% of budget, which

is 3% lower than the aggregated project management forecast of $516.8m.

3.2.2 Year-to-date

expenditure is closely aligned with monthly forecasts and consistent with the

prior year’s expenditure profile.

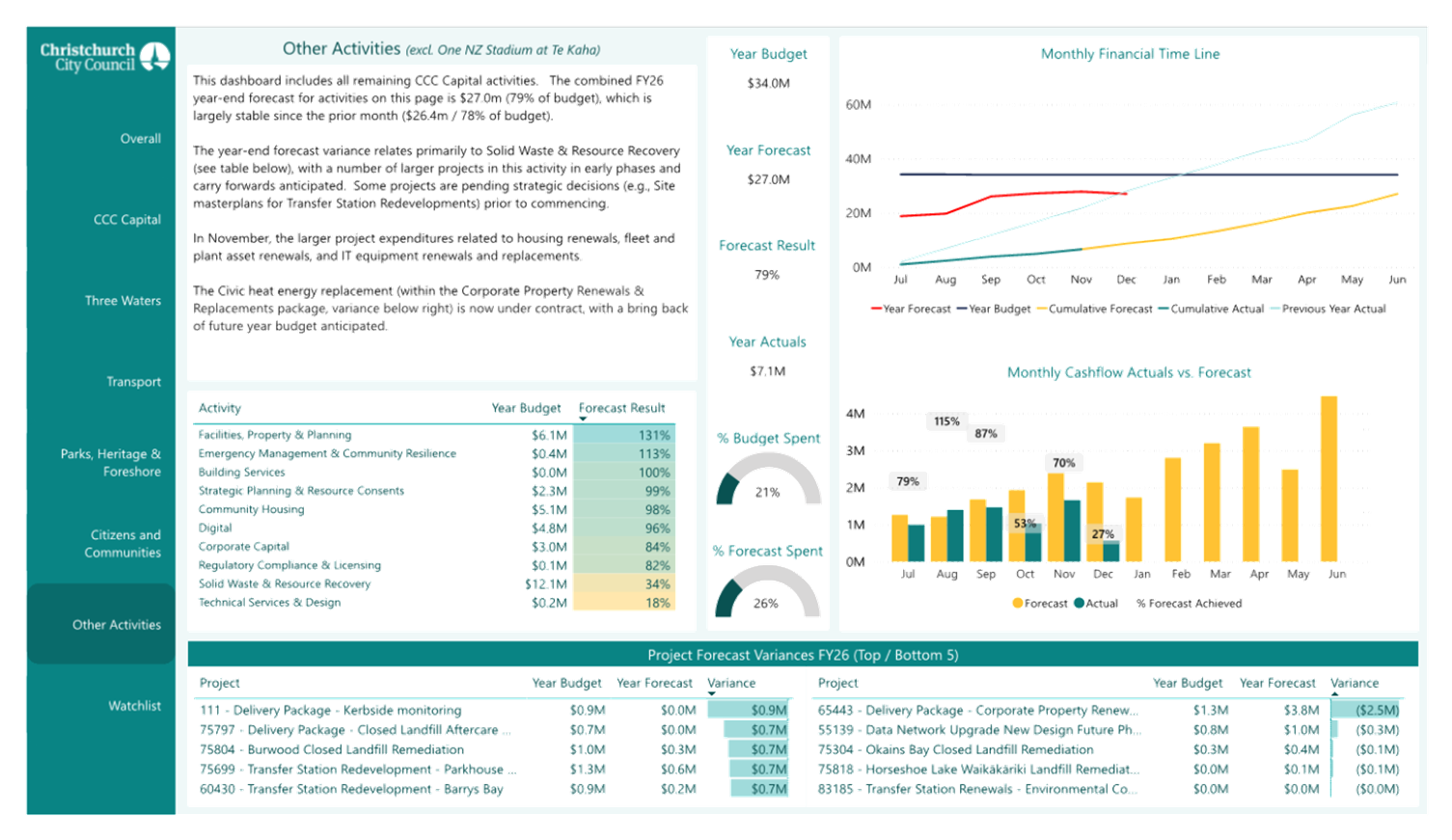

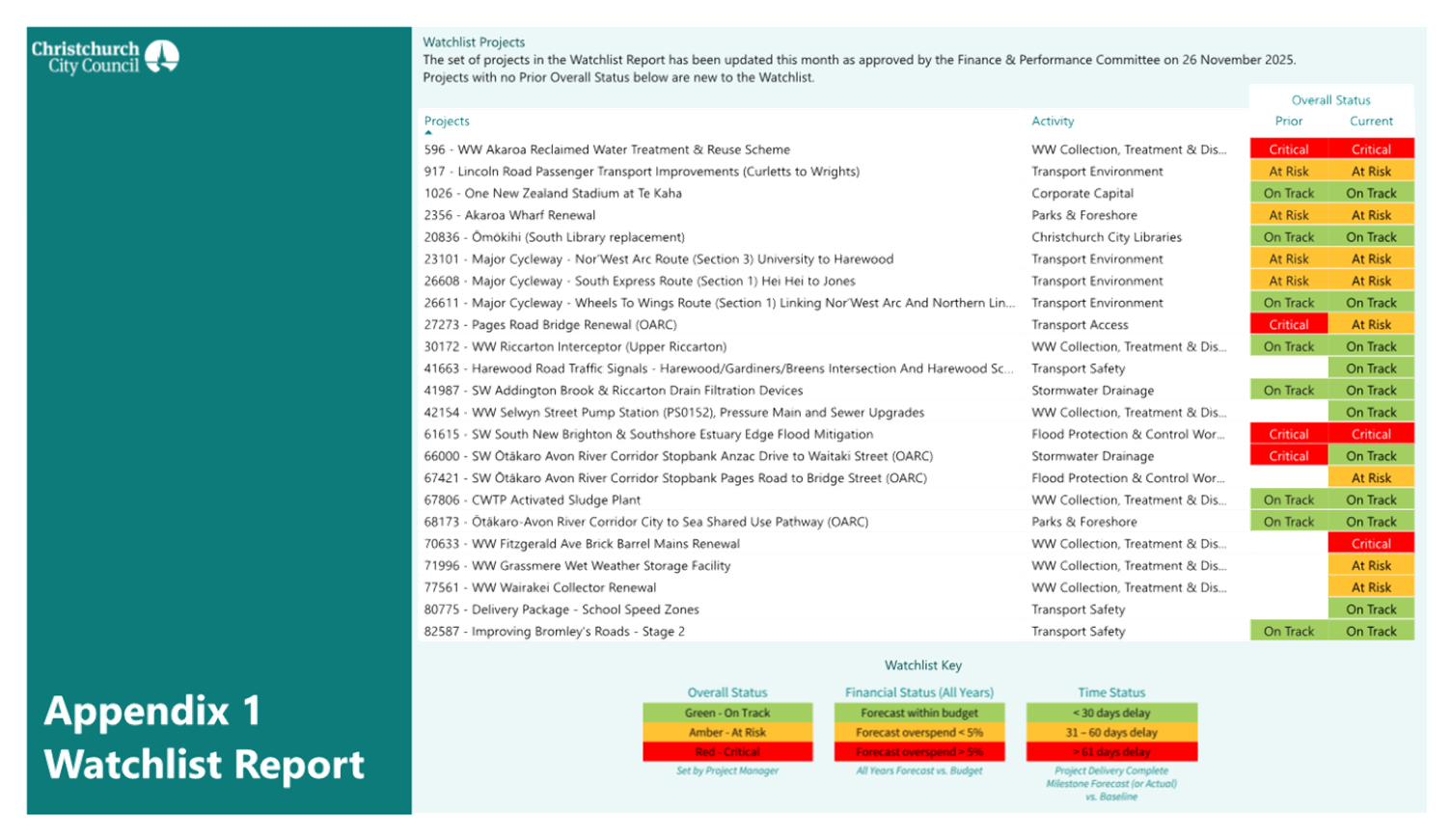

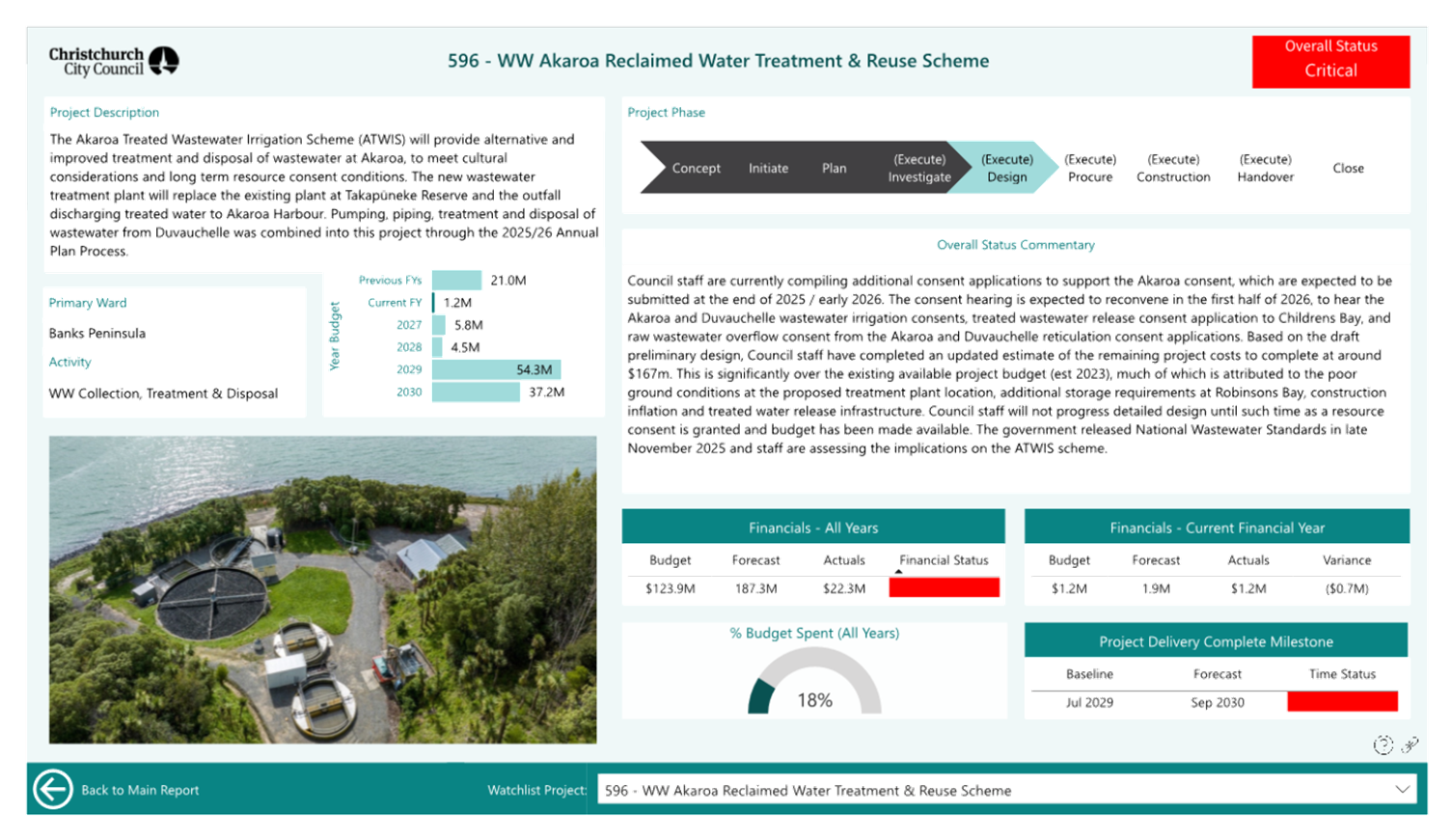

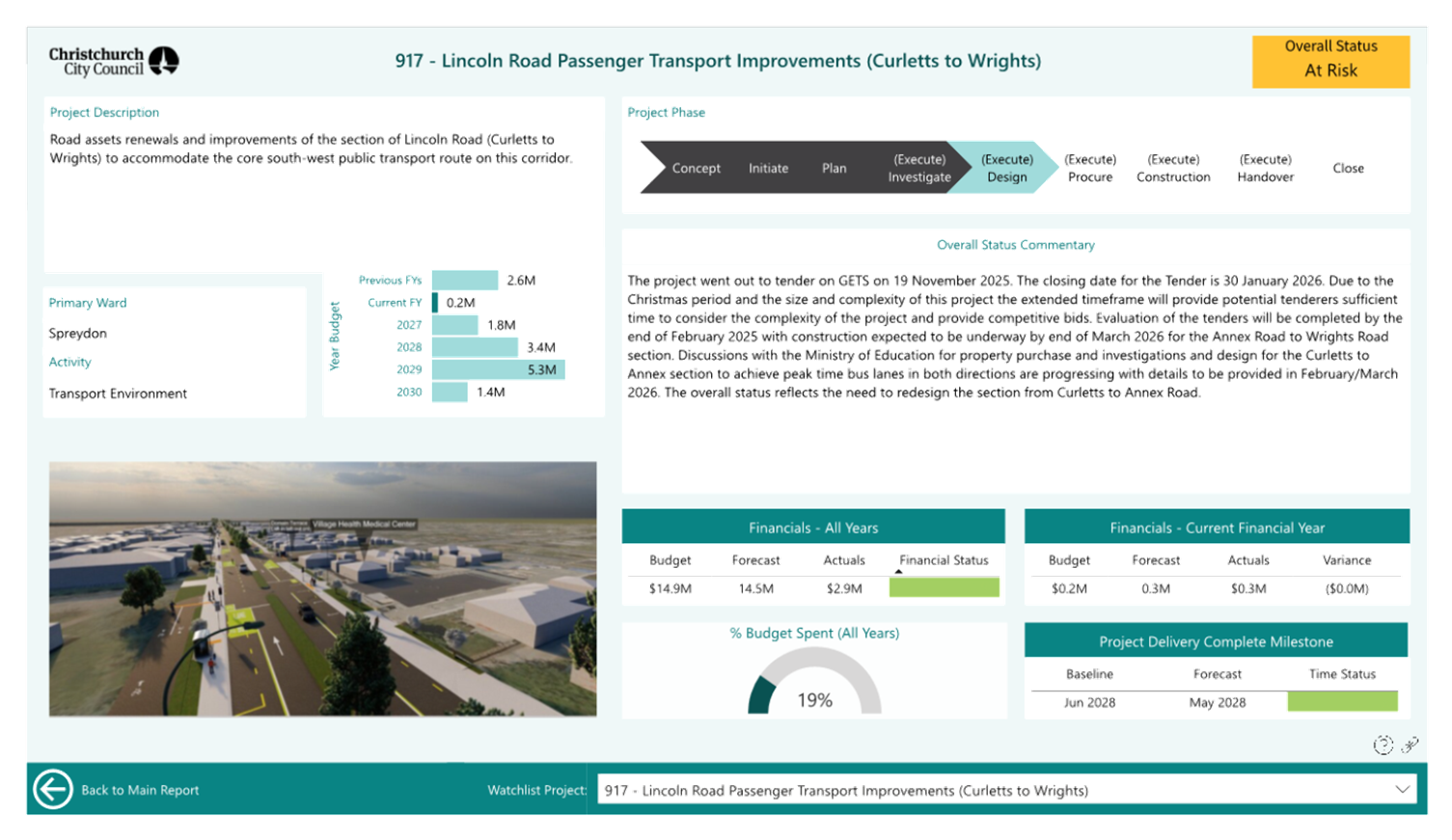

3.3 Full

results are provided in the Capital Programme Performance Report for November

2025 (Attachment A). This includes the Watchlist Report as Appendix

1.

3.4 The

set of projects in the Watchlist Report has been updated this month as agreed

at the Finance and Performance Committee Meeting on 26 November 2025.

3.5 Active

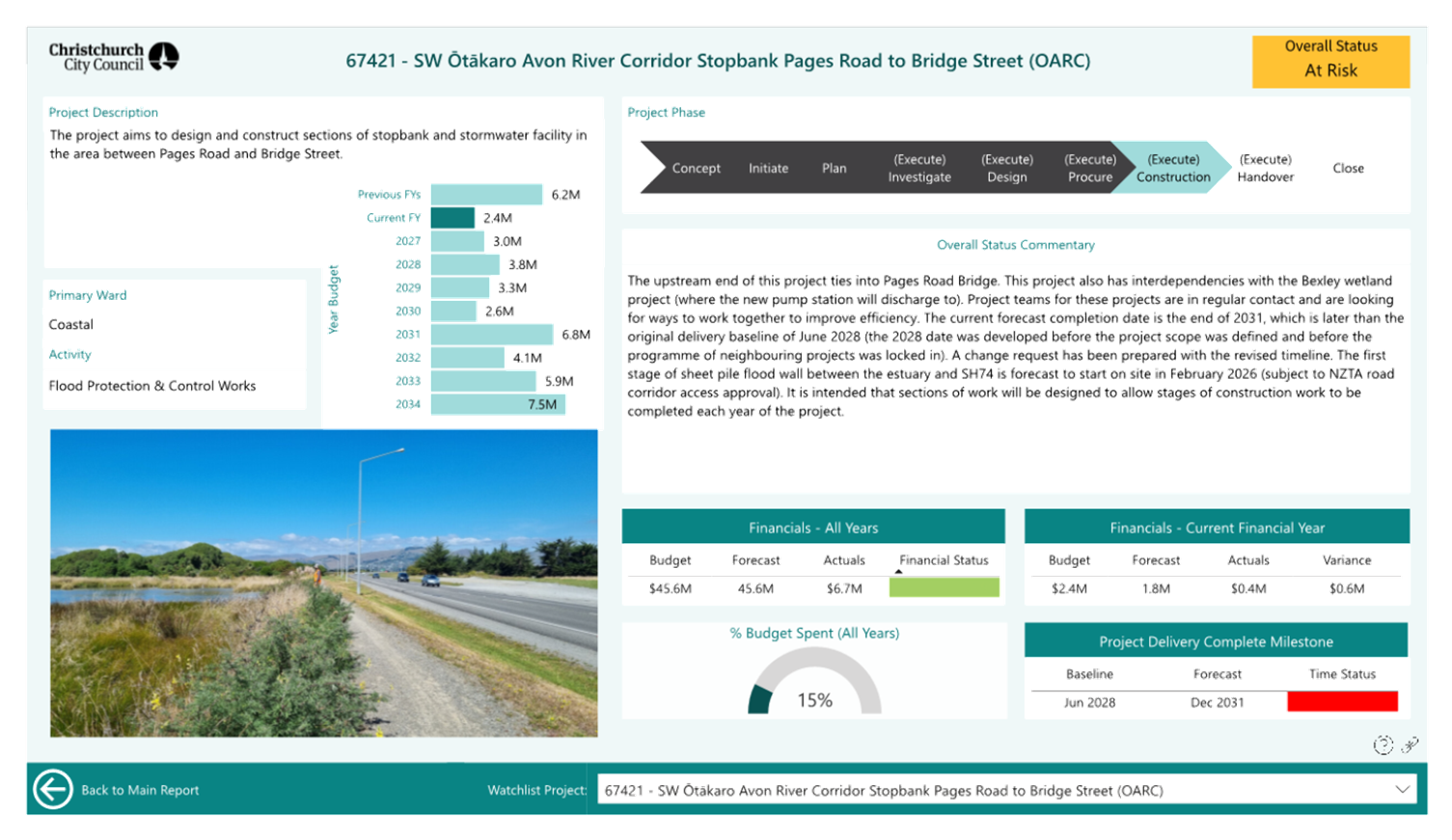

risks / issues affecting Watchlist projects include budget risks and

shortfalls, consenting timelines and uncertainty, some programme delays,

challenging ground conditions, contaminated land, and third-party

interdependencies.

3.6 Two

Watchlist projects have had a change in Overall Status flag since the prior

report, following the re-baselining of the delivery timelines via Change

Request:

- 27273 - Pages Road Bridge

Renewal: Updated from ‘Red –

Critical’ to ‘Amber – At Risk’

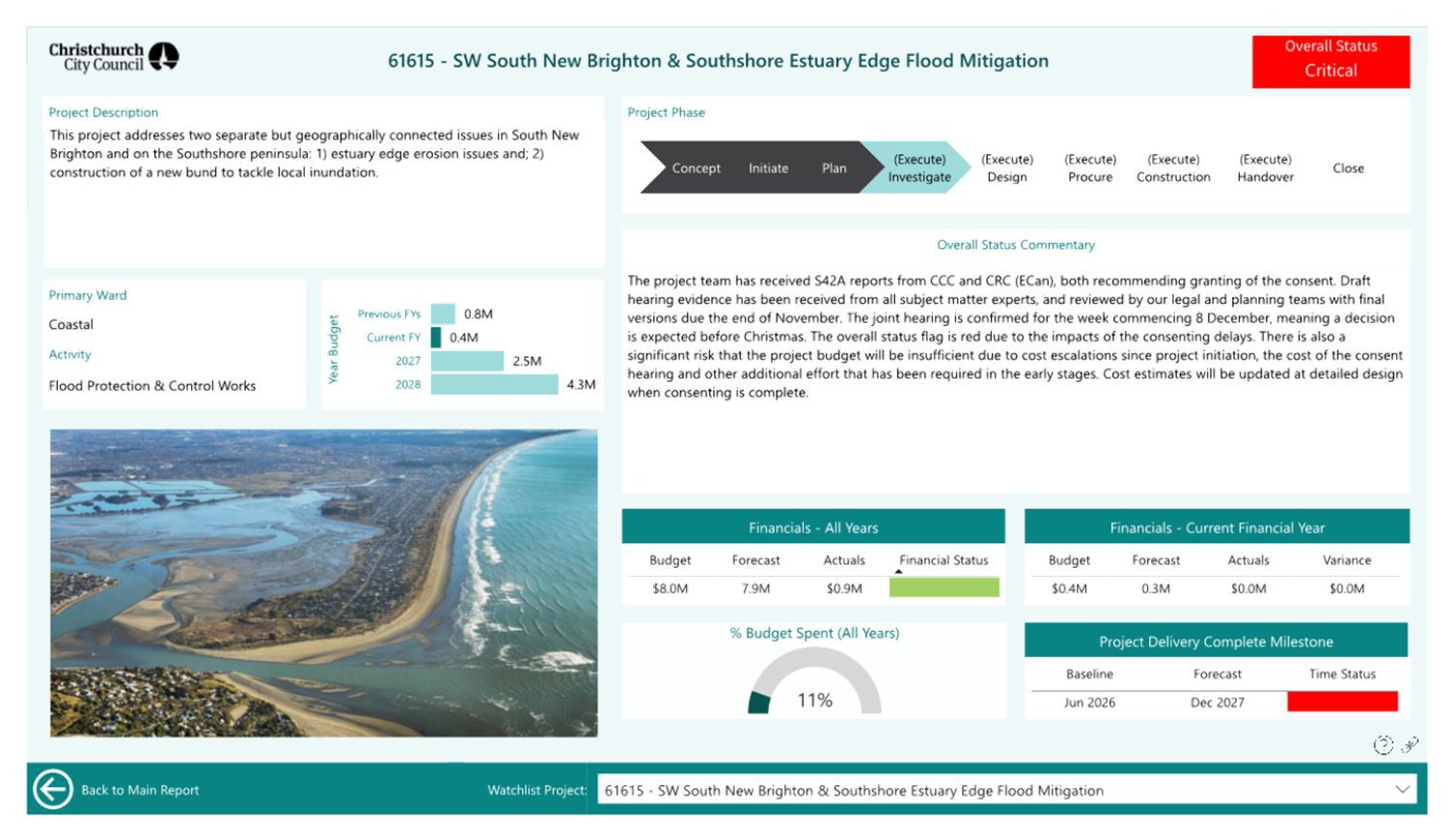

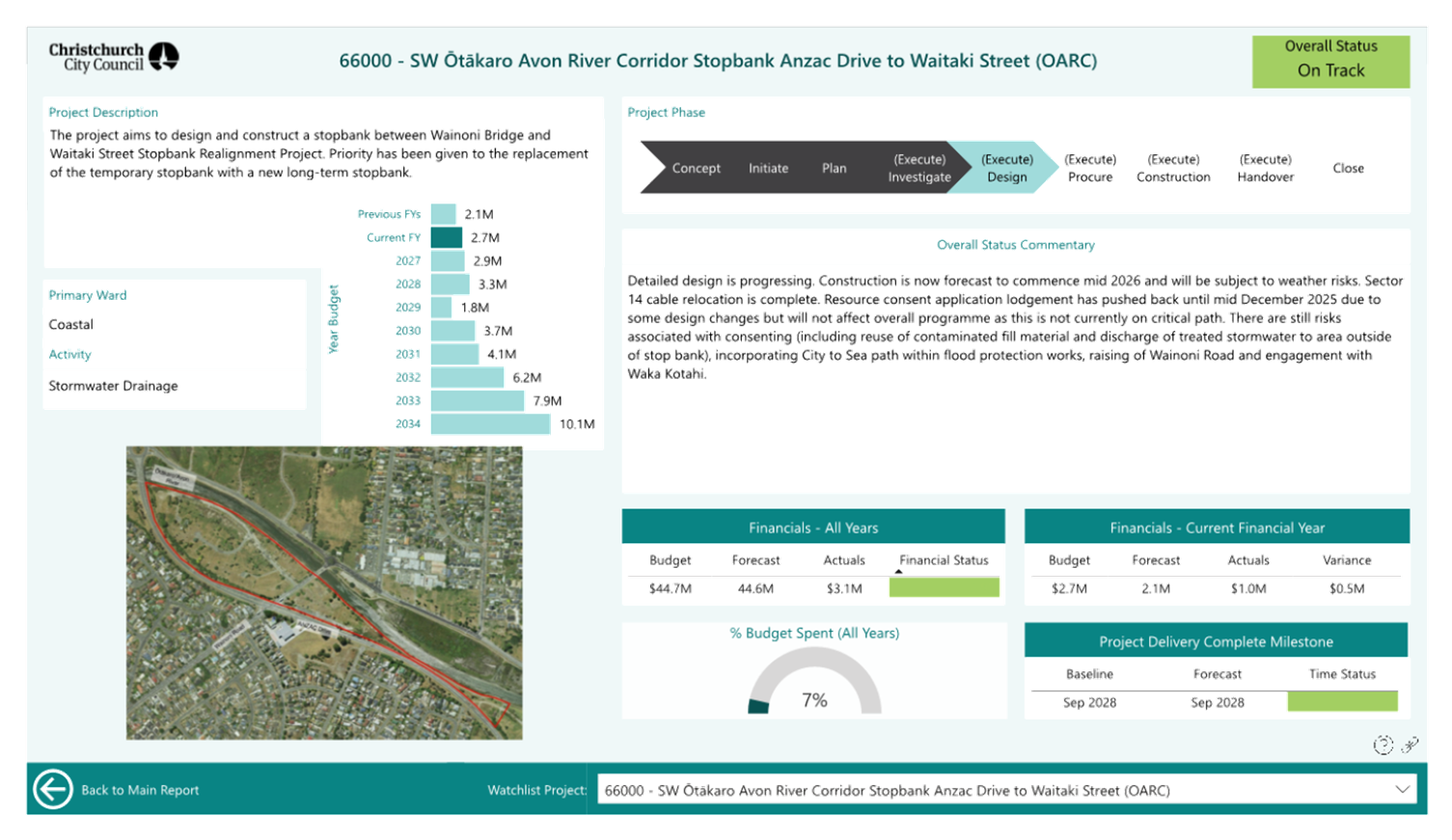

- 66000 - SW Ōtākaro Avon River Corridor Stopbank Anzac Drive to Waitaki Street (OARC):

Updated from ‘Red – Critical’ to

‘Green – On Track’.

3.7 The

Monthly Change Report is included in the public

excluded section due to contract commercial sensitivity.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Attachment to

report 25/2445154 (Title: Capital Programme Performance Report - November

2025 - Final)

|

25/2530574

|

73

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Lauren Barry -

Senior PMO Business Analyst

Paul Dadson -

Senior Capital Programme Advisor Parks & Facilities

|

|

Approved By

|

Brent Smith -

General Manager City Infrastructure

|

|

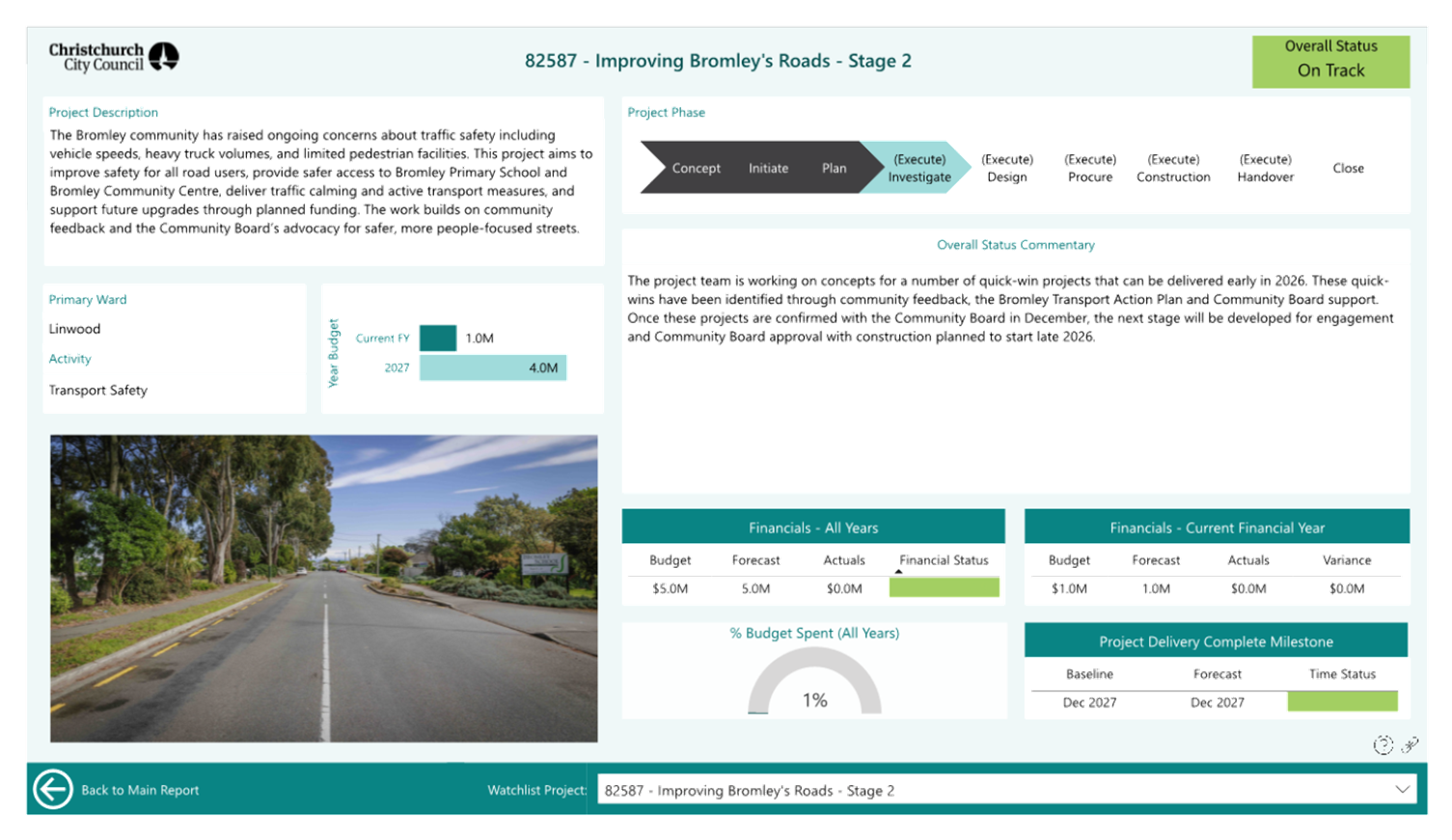

10. Draft Council

submissions on Building and Construction Sector Amendment Bills

|

|

Reference Te Tohutoro:

|

25/2455928

|

|

Responsible Officer(s) Te Pou Matua:

|

Steffan

Thomas, Head of Building Consenting

|

|

Accountable ELT Member Pouwhakarae:

|

David

Griffiths, Acting General Manager Strategy, Planning & Regulatory

Services

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to seek approval from the Finance and Performance

Committee to lodge the joint submission on the:

1.1.1 Building

and Construction Sector (Strengthening Occupational Licensing Regimes)

Amendment Bill.

1.1.2 Building

and Construction Sector (Self-certification by Plumbers and Drainlayers)

Amendment Bill.

1.2 The Transport and Infrastructure Select Committee is calling for

feedback on the bills, with submissions due on Thursday 8 January 2026.

2. Officer Recommendations Ngā

Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Draft Council submissions on

Building and Construction Sector Amendment Bills Report.

2. Approves lodging the Council submission on the

Building and Construction Sector Amendment Bills (Attachment A).

3. Notes that the decision in this report is

assessed as low significance based on the Christchurch City Council’s

Significance and Engagement Policy.

4. Delegates authority to the General Manager

Strategy, Planning and Regulatory Services to oversee final editorial changes

to correct any typographical or formatting errors in the submission.

3. Executive Summary Te Whakarāpopoto Matua

3.1 The

Government has proposed legislative changes intended to speed up building work

and take pressure off building consent authorities.

Currently, all building work requiring consent must be inspected by the

relevant building consent authority.

3.2 The

first bill, Building and Construction Sector (Self-certification by Plumbers

and Drainlayers) Amendment Bill will allow building professionals such as

plumbers, drainlayers and builders the ability to self-certify

‘low-risk’ building work.

3.3 A

second bill, Building and Construction Sector (Strengthening Occupational

Licensing Regimes) Amendment Bill is being progressed in tandem and looks

to raise standards and improve accountability for building professionals.

3.4 As

the bills are interlinked and part of the same area of reform, a submission has been drafted dealing with

both pieces of legislation.

4. Background/Context Te Horopaki

Building and Construction Sector (Strengthening

Occupational Licensing Regimes) Amendment Bill

4.1 The

bill strengthens occupational licensing regimes in the building and

construction sector. The bill:

4.1.1 clarifies

the functions of regulatory boards and registrars, and expanding registrars'

powers to deal with complaints

4.1.2 enables

codes of ethics for licensed plumbers, gasfitters, and drainlayers

4.1.3 allows

the Building Practitioners Board to enforce training orders

4.1.4 improves

the licence renewal process for licensed building practitioners

4.1.5 increases

the membership of the Plumbers, Gasfitters, and Drainlayers Board

4.2 As

an omnibus bill, it amends the Building Act 2004, the Plumbers, Gasfitters, and

Drainlayers Act 2006, and the Electricity Act 1992.

Building and Construction Sector (Self-certification by

Plumbers and Drainlayers) Amendment Bill

4.3 The

bill introduces an opt-in scheme to allow qualified plumbers and drainlayers to

self-certify that their work complies with the terms of a building consent.

This is intended to remove the need for a building consent authority to inspect

the work itself.

4.4 As

an omnibus bill, it amends the Building Act 2004 and the Plumbers, Gasfitters,

and Drainlayers Act 2006.

4.5 Regulations

are expected to be released in early 2026 and will detail which types of

plumbing and drainlaying work can be self-certified.

Key submission points

4.6 The

draft submission makes the following points:

4.6.1 The strengthening of occupational licencing

is appropriate and is supported by the Council.

4.6.2 With respect to the self-certification of plumbers and drainlayers,

while the Council considers that the bill itself is generally appropriate,

we do not believe that the savings anticipated will be realised, and

there is likely to be long-term issues with the quality of buildings. The submission notes that while many Licensed Building

Practitioners (LBPs) are competent and reliable, it only takes a small number

to create large, complex and costly issues, the resolution of which will fall

on homeowners.

4.6.3 The

Council is concerned that many plumbers and drainlayers

may not be consistent enough to self-certify their work

with no third-party overview. The Council observed substantial non-compliant

work carried out or supervised by LBPs after the Canterbury earthquake sequence

where there was no third-party overview.

4.6.4 The

Council is also concerned about high failure rates of inspections for work

carried out by certifying plumbers and drainlayers, even for work that would be

considered “simple” under these proposed changes. We have

particular concerns with plumbing within concrete raft slabs as drains within

or under a concrete slab can impact the structure of the building.

4.7 The following related memos/information were circulated to the

meeting members:

|

Date

|

Subject

|

|

9

December 2025

|

Draft Council submissions on Building and

Construction Sector Amendment Bills

|

Options Considered Ngā Kōwhiringa Whaiwhakaaro

4.8 The

only reasonably practicable option considered and assessed in this report is

that the Council prepares a submission on the bills. It is important to submit

on these bills as they impact our roles and responsibilities as a building

consent authority.

4.9 The

Council regularly makes submissions on proposals which may significantly impact

Christchurch residents or Council business. Submissions are an important

opportunity to influence thinking and decisions through external

agencies’ consultation processes.

4.10 The

alternative option would be to not submit on the proposed changes. This course

of action is not recommended in this case, as Council would miss an opportunity

to provide feedback and influence government policy that directly relates to

the role of the Council.

5. Financial Implications Ngā Hīraunga Rauemi

Capex/Opex Ngā Utu Whakahaere

|

|

Recommended Option

|

Option 2 – do not submit

|

|

Cost to Implement

|

Met from existing operational budgets.

|

No cost.

|

|

Maintenance/Ongoing Costs

|

No cost.

|

No cost.

|

|

Funding Source

|

Met from existing operational budgets.

|

No cost.

|

|

Funding Availability

|

Available.

|

No cost.

|

|

Impact on Rates

|

No impact on rates.

|

No cost.

|

6. Considerations Ngā Whai Whakaaro

Risks and Mitigations Ngā Mōrearea me

ngā Whakamātautau

6.1 The

decision to lodge a Council submission is low risk.

Legal Considerations Ngā Hīraunga

ā-Ture

6.2 Statutory

and/or delegated authority to undertake proposals in the report:

6.2.1 Any

person or organisation can submit on Government Bills during the select

committee process.

6.3 Other Legal Implications:

6.3.1 There

is no legal context, issue, or implication relevant to this decision. The Legal

Services team was involved in the development of the submission.

Strategy

and Policy Considerations Te

Whai Kaupapa here

6.4 The

required decision:

6.4.1 Aligns

with the Christchurch

City Council’s Strategic Framework.

6.4.2 Are

assessed as low significance based on the Christchurch City Council’s

Significance and Engagement Policy. This recognises that while there may be

community interest in the proposed direction, the specific decision (to approve

the draft submission) is of a lower level of significance

6.4.3 Are consistent with Council’s Plans and

Policies.

6.5 This

report supports the Council's

Long Term Plan (2024 - 2034):

6.6 Strategic Planning and Policy

6.6.1 Activity: Strategic Policy and Resilience

· Level of Service: 17.0.1.1 Advice meets emerging needs and

statutory requirements, and is aligned with governance expectations in the

Strategic Framework - Triennial (every three years) reconfirmation of the

Strategic Framework and Infrastructure Strategy

Community

Impacts and Views Ngā Mariu ā-Hāpori

6.7 The

decision of the Council to make a submission on the Bill does not directly

impact the community and community views have not been sought by staff.

Impact

on Mana Whenua Ngā

Whai Take Mana Whenua

6.8 The

decision to make a submission on these bills does not involve

a significant decision in relation to ancestral land, a body of water or other

elements of intrinsic value, therefore this decision does not

specifically impact Mana Whenua, their culture, and traditions.

6.9 The

decision does not involve a matter of interest to Mana Whenua and will not impact on our agreed partnership priorities

with Ngā Papatipu Rūnanga.

Climate

Change Impact Considerations Ngā Whai Whakaaro mā te Āhuarangi

6.15 A

decision to make a Council submission on the bills is unlikely to contribute

significantly to adaptation to the impacts of climate change or emissions

reductions.

7. Next Steps Ngā Mahinga ā-muri

7.1 Subject

to approval, the draft submission on the bills will be lodged with the

Transport and Infrastructure Select Committee before Thursday 8 January 2026.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Draft Council

submissions on Building and Construction Sector Amendment Bills

|

25/2544958

|

110

|

In addition to the attached documents, the following background

information is available:

Signatories Ngā Kaiwaitohu

|

Authors

|

Ellen Cavanagh

- Senior Policy Analyst

Sharna O'Neil

- Policy Analyst

|

|

Approved By

|

Steffan Thomas

- Head of Building Consenting

David

Griffiths - Acting General Manager Strategy, Planning & Regulatory

Services

|

|

11. Ōtautahi Community Housing Trust: Request to

Approve Subsidiary

|

|

Reference Te Tohutoro:

|

25/2092580

|

|

Responsible Officer(s) Te Pou Matua:

|

Bruce

Rendall, Head of Facilities and Property

|

|

Accountable ELT Member Pouwhakarae:

|

Anne

Columbus, General Manager Corporate Services/Chief People Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The purpose of this report is to seek the Council’s approval,

as a lender, to a request by Ōtautahi Community Housing Trust (OCHT) to

set up a charitable subsidiary, allowing it to start undertaking the provision

of community housing services outside Christchurch and Banks Peninsula.

1.2 The report is officer generated in response to a request from OCHT.

2. Officer Recommendations Ngā

Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Ōtautahi Community Housing

Trust: Request to Approve Subsidiary Report.

2. Notes that the decision in this report is

assessed as low significance based on the Christchurch City Council’s

Significance and Engagement Policy.

3. Approves, as required by the terms of the

Financing Agreements, Ōtautahi Community Housing Trust’s

request to establish a subsidiary, being a charitable company, that can develop

social and affordable housing outside of Christchurch and Banks Peninsula.

4. Notes that this is a contingency measure

allowing for the take up of housing opportunities while Coucnil’s

previously approved changes to the Ōtautahi Community Housing Trust’s trust

deed are implemented via a Private Bill.

3. Executive Summary Te Whakarāpopoto Matua

3.1 The subject matter of this report is associated with matters

approved by Council on 11 December 2024 (reference: 25/2092580) whereby the Council, among other matters:

Approve[d], as required by the terms of

the Financing Agreements, a material change to the Ōtautahi Community Housing

Trust’s Trust Deed, being the removal of the geographic restriction on

operations, expanding the definition of ‘affordable’ to allow for

ownership products, and increasing the focus to be on all those with low incomes

that are currently contained in the Purpose of the Trust Deed.

Note[d] that the mechanism for the

change to the Trust Deed’s Purpose is an Ōtautahi Community Housing

Trust initiated Private Bill.

Approve[d], as required under the terms

of the Financing Agreements, a material change to Ōtautahi Community

Housing Trust’s business to allow it to:

· provide tenancy

management services, lease or own property, and/or to develop social and

affordable housing other than in Christchurch and Banks Peninsula with the

prior written agreement of Council in its role as lender, such agreement not to

be unreasonably withheld; and

· provide paid

advice and professional development services elsewhere.

3.2 As the Ōtautahi Community Housing Trust (OCHT) is a

charitable trust, the proposed extension of its current geographic parameters

is being considered by a Private Bill (Bill) is currently before

Parliament.

3.3 While OCHT is not a Council Controlled Organisation, Council has

lent OCHT $55,670.000 in relation to various projects. Council and OCHT

have entered into financing agreements and securities in relation to this

lending/borrowing. It is a condition of the finance agreements and the

security agreements that Council’s consent be sought prior to certain

actions being taken by OCHT.

3.4 While the Bill is progressing through the Parliamentary process,

OCHT has requested the Council’s approval to establish a wholly owned

charitable subsidiary to enable operations beyond Christchurch and Banks

Peninsula. The subsidiary would remain inactive initially but would allow

OCHT to respond to opportunities with central government and neighbouring

councils.

3.5 The proposal aligns with Council’s housing policy objectives

and supports OCHT’s bid to become a strategic partner with the Crown,

potentially improving housing outcomes for Christchurch and the wider region.

The subsidiary structure includes safeguards to ringfence financial risk and

maintain oversight, ensuring OCHT’s core obligations to the Council are

protected.

3.6 The key risks include potential financial exposure if the subsidiary

underperforms and concerns about OCHT losing focus on Christchurch operations.

However, these risks are mitigated by structural separations, legal reviews,

and the scale of Christchurch’s existing housing portfolio. Opportunities

include retaining skilled staff, expanding housing delivery, and strengthening

regional partnerships.

3.7 The recommendation to proceed reflects a strategic investment in

OCHT’s long-term sustainability and the Council-OCHT partnership. It

supports Council policy, enhances regional housing resilience, and positions

Christchurch to benefit from future government housing initiatives without

compromising local priorities.

4. Background/Context Te Horopaki

4.1 OCHT is formally requesting the Council's written consent to

establish a subsidiary in the form of a charitable company. OCHT would

wholly own the subsidiary. The Council’s consent is required under clause

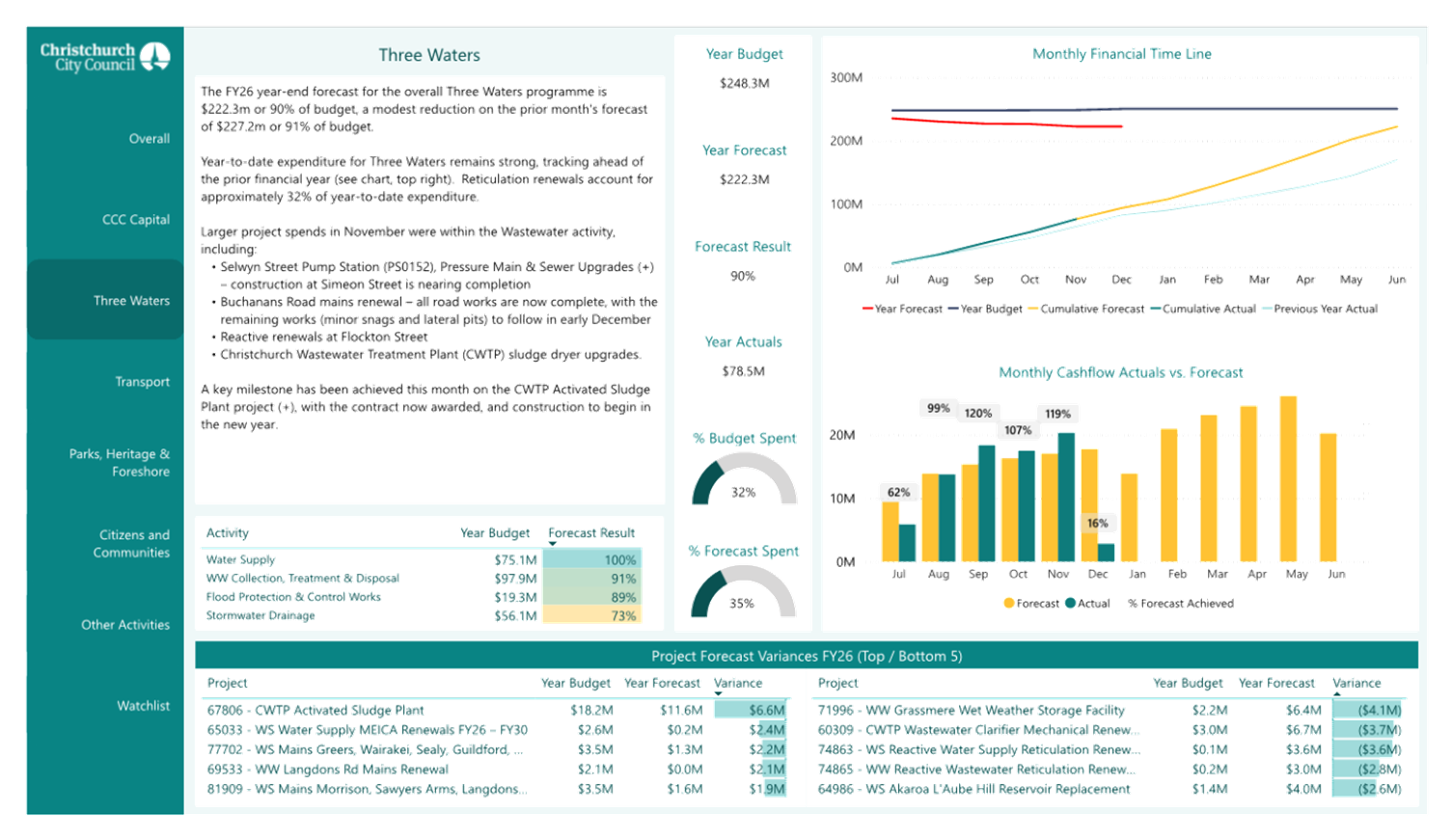

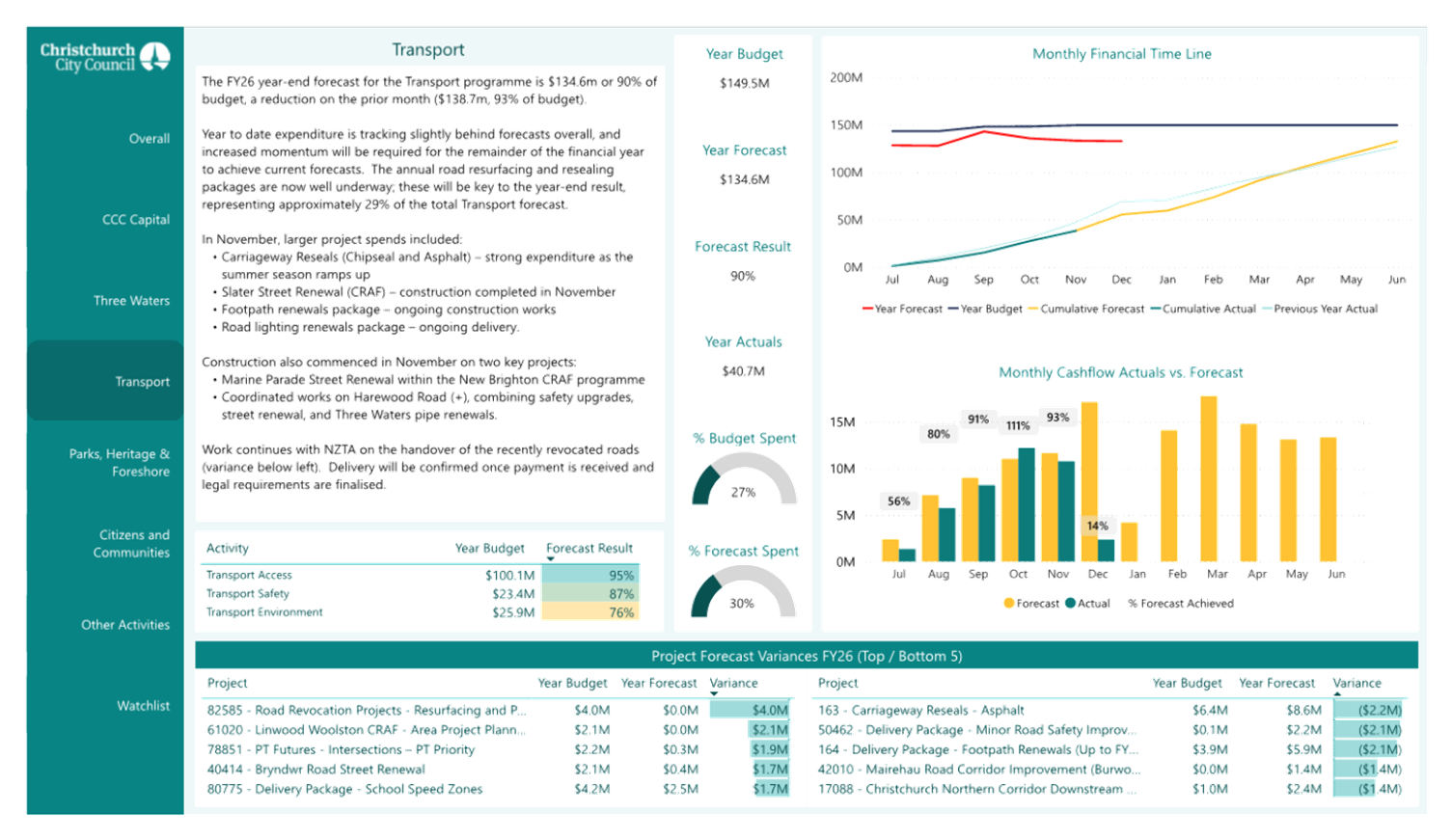

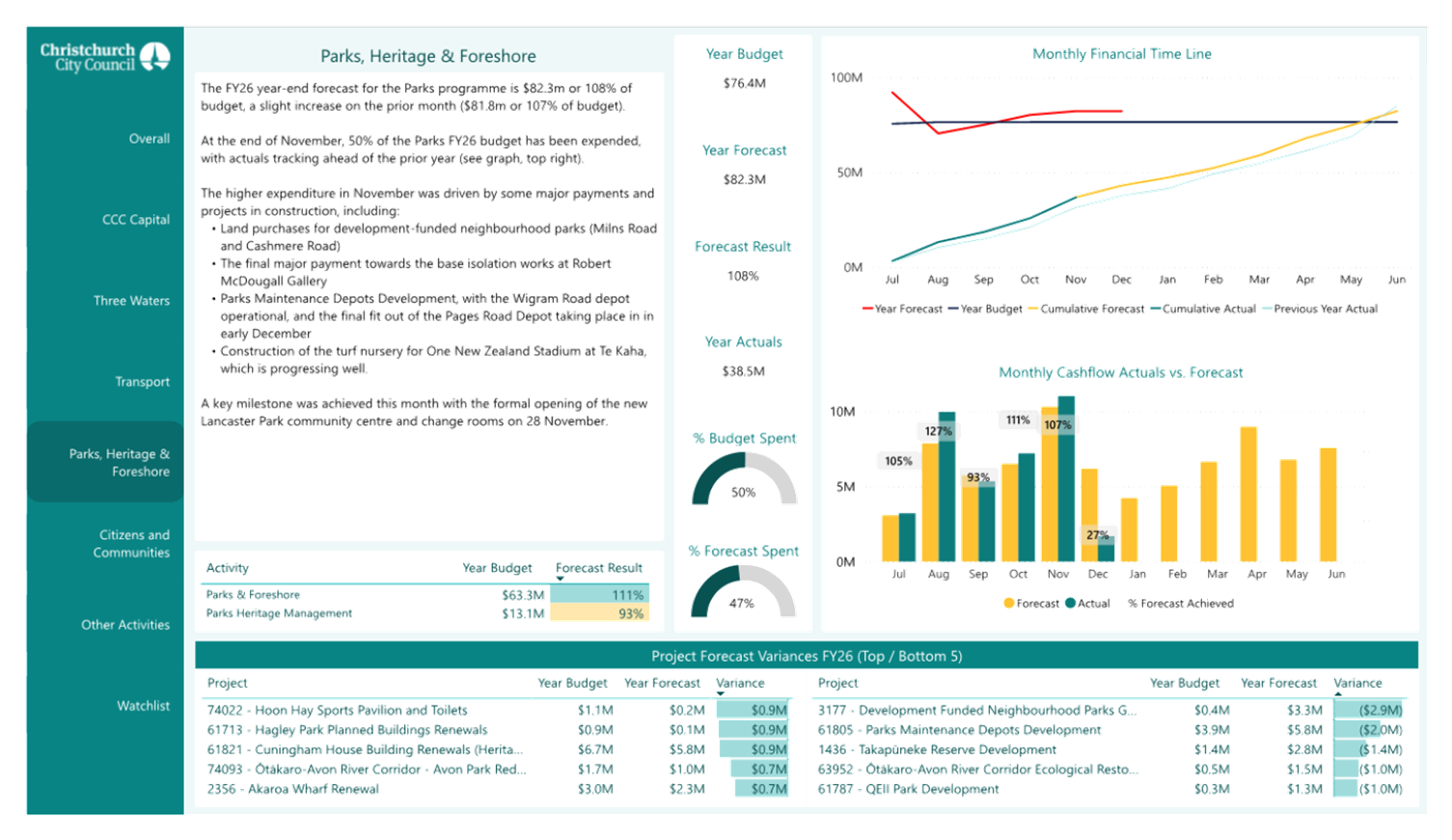

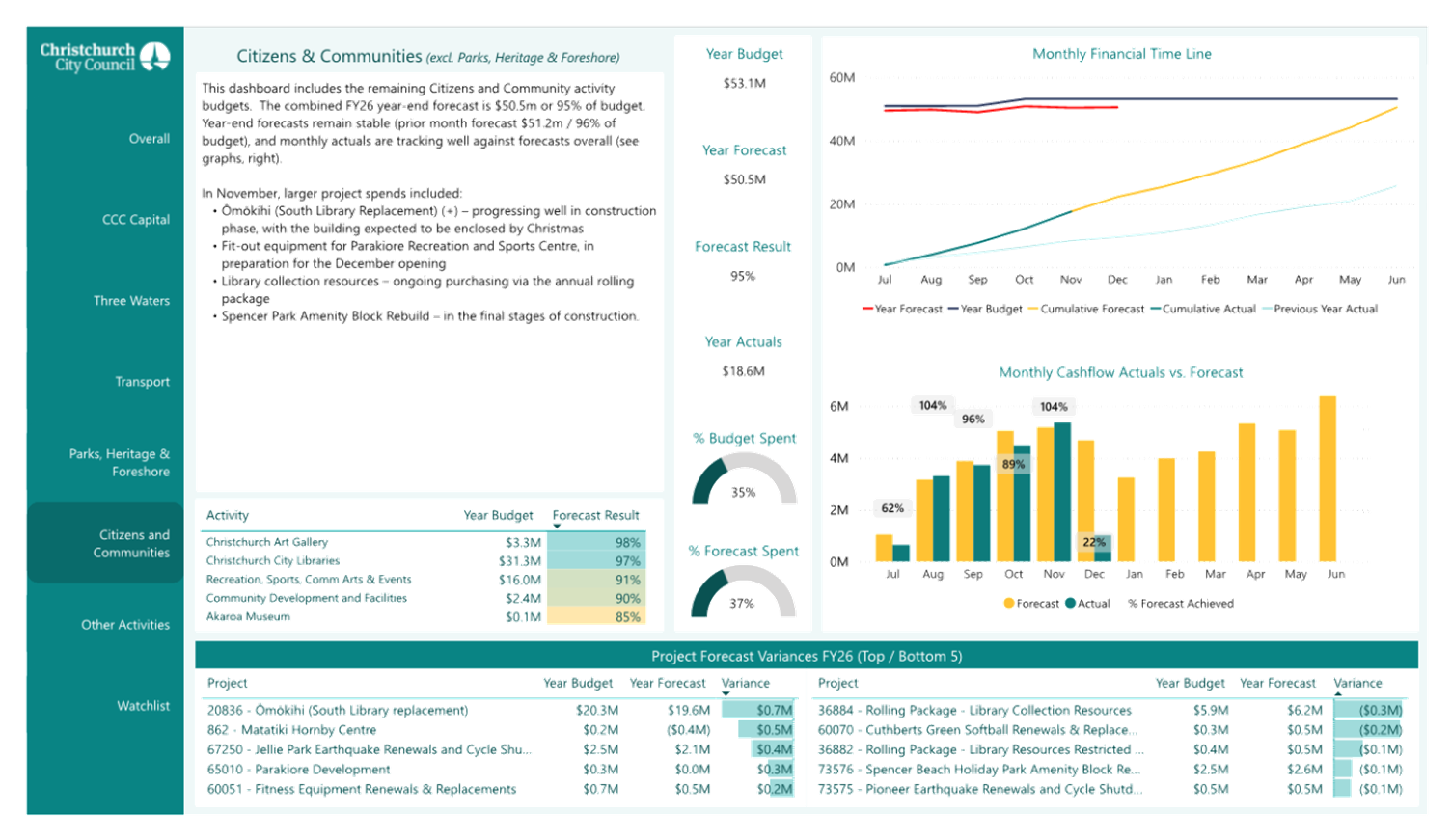

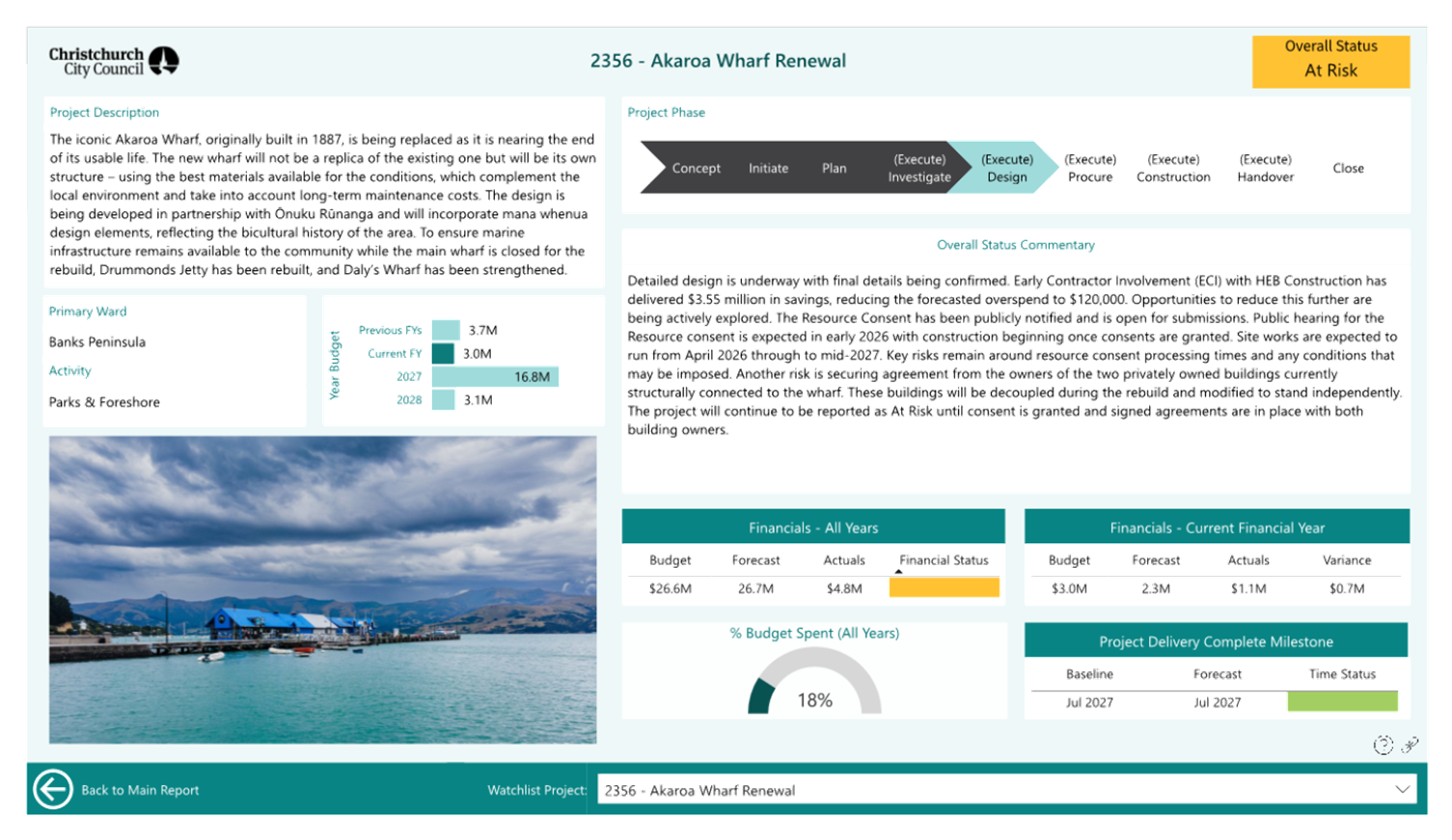

10.3 (c) of the Development Funding Agreement (DFA).