Audit

and Risk Management Committee - Terms of Reference Ngā Ārahina Mahinga

|

Chair

|

Mr Bruce Robertson

|

|

Deputy Chair

|

Councillor McLellan

|

|

Membership

|

Councillor Fields

Councillor MacDonald

Councillor Scandrett

External Members:

Mrs Hilary Walton

Mr Michael Wilkes

|

|

Quorum

|

Half of the members if the

number of members (including vacancies) is even, or a majority of members if

the number of members (including vacancies) is odd.

|

|

Meeting

Cycle

|

Quarterly and

as required

|

|

Reports

To

|

Council

|

Purpose

To assist the Council to discharge

its responsibility to exercise

due care, diligence and skill in relation to the oversight of:

·

the robustness of the internal control framework;

·

the integrity and appropriateness of external reporting, and

accountability arrangements within the organisation for these functions;

·

the robustness of risk management systems, process and practices;

·

internal and external audit;

·

accounting policy and practice;

·

compliance with applicable laws, regulations, standards and best

practice guidelines for public entities; and

·

the establishment and maintenance of controls to safeguard the

Council’s financial and non-financial assets.

The foundations on which this

Committee operates, and as reflected in this Terms of Reference, includes:

independence; clarity of purpose; competence; open and effective relationships

and no surprises approach.

Procedure

·

In order to give effect to its advice the Committee should make recommendations to the Council and to

Management.

·

The Committee should meet the internal and the external auditors

without Management present as a standing agenda item at each meeting where

external reporting is approved, and at other meetings if requested by any of

the parties.

·

The external auditors,

the internal audit manager and the co-sourced internal audit firm should meet

outside of formal meetings as appropriate with the Committee Chair.

·

The Committee Chair

will meet with relevant members of Management before each Committee meeting and

at other times as required.

Responsibilities

Internal Control Framework

·

Consider the adequacy and effectiveness of internal controls and

the internal control framework including overseeing privacy and cyber security.

·

Enquire as to the steps management has taken to embed a culture

that is committed to probity and ethical behaviour.

·

Review the processes or systems in place to capture and

effectively investigate fraud or material litigation should it be required.

·

Seek confirmation annually and as necessary from internal and

external auditors, attending Councillors, and management, regarding the

completeness, quality and appropriateness of financial and operational

information that is provided to the Council.

Risk Management

·

Review and consider Management’s risk management framework

in line with Council’s risk appetite, which includes policies and

procedures to effectively identify, treat and monitor significant risks, and

regular reporting to the Council.

·

Assist the Council to determine its appetite for risk.

·

Review the principal risks that are determined by Council and

Management, and consider whether appropriate action is being taken by

management to treat Council’s significant risks. Assess the effectiveness

of, and monitor compliance with, the risk management framework.

·

Consider emerging significant risks and report these to Council

where appropriate.

Internal Audit

·

Review and approve the annual internal audit plan, such plan to

be based on the Council’s risk framework. Monitor performance against the

plan at each regular quarterly meeting.

·

Monitor all internal audit reports and the adequacy of

management’s response to internal audit recommendations.

·

Review six monthly fraud reporting and confirm fraud issues are

disclosed to the external auditor.

·

Provide a functional reporting line for internal audit and ensure

objectivity of internal audit.

·

Oversee and monitor the performance and independence of internal

auditors, both internal and co-sourced. Review the range of services provided

by the co-sourced partner and make recommendations to Council regarding the

conduct of the internal audit function.

·

Monitor compliance with the delegations policy.

External Reporting and

Accountability

·

Consider the appropriateness of the Council’s existing

accounting policies and practices and approve any changes as appropriate.

·

Contribute to improve the quality, credibility and objectivity of

the accounting processes, including financial reporting.

·

Consider and review the draft annual financial statements and any

other financial reports that are to be publicly released, make recommendations

to Management.

·

Consider the underlying quality of the external financial

reporting, changes in accounting policy and practice, any significant

accounting estimates and judgements, accounting implications of new and

significant transactions, management practices and any significant

disagreements between Management and the external auditors, the propriety of

any related party transactions and compliance with applicable New Zealand and

international accounting standards and legislative requirements.

·

Consider whether the external reporting is consistent with

Committee members’ information and knowledge and whether it is adequate

for stakeholder needs.

·

Recommend to Council the adoption of the Financial Statements and

Reports and the Statement of Service Performance and the signing of the Letter

of Representation to the Auditors by the Mayor and the Chief Executive.

·

Enquire of external auditors for any information that affects the

quality and clarity of the Council’s financial statements, and assess

whether appropriate action has been taken by management.

·

Request visibility of appropriate management signoff on the

financial reporting and on the adequacy of the systems of internal control;

including certification from the Chief Executive, the Chief Financial Officer

and the General Manager Corporate Services that risk management and internal

control systems are operating effectively;

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

·

Review and consider the Summary Financial Statements for

consistency with the Annual Report.

External Audit

·

Annually review the independence and confirm the terms of the

audit engagement with the external auditor appointed by the Office of the

Auditor General. Including the adequacy of the nature and scope of the audit,

and the timetable and fees.

·

Review all external audit reporting, discuss with the auditors

and review action to be taken by management on significant issues and

recommendations and report to Council as appropriate.

·

The external audit reporting should describe: Council’s

internal control procedures relating to external financial reporting, findings

from the most recent external audit and any steps taken to deal with such

findings, all relationships between the Council and the external auditor,

Critical accounting policies used by Council, alternative treatments of

financial information within Generally Accepted Accounting Practice that have

been discussed with Management, the ramifications of these treatments and the treatment

preferred by the external auditor.

·

Ensure that the lead audit engagement and concurring audit

directors are rotated in accordance with best practice and NZ Auditing

Standards.

Compliance with Legislation,

Standards and Best Practice Guidelines

·

Review the effectiveness of the system for monitoring the

Council’s compliance with laws (including governance legislation,

regulations and associated government policies), with Council’s own

standards, and Best Practice Guidelines.

Appointment of Independent Members

·

Identify skills required for Independent Members of the Audit and

Risk Management Committee. Appointment panels will include the Mayor or

Deputy Mayor, Chair of Finance & Performance Committee and Chair of Audit

& Risk Management Committee. Council approval is required for all

Independent Member appointments.

·

The term of the Independent members should be for three

years. (It is recommended that the term for independent members begins on

1 April following the Triennial elections and ends 31 March three years

later. Note the term being from April to March provides continuity for

the committee over the initial months of a new Council.)

·

Independent members are eligible for re-appointment to a maximum

of two terms. By exception the Council may approve a third term to ensure

continuity of knowledge.

Long Term Plan Activities

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

|

7. Long

Term Plan 2027 - Risk Assessment and Project Update

|

|

Reference Te Tohutoro:

|

25/1705241

|

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance Peter.Ryan@ccc.govt.nz

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to provide an analysis of workstreams required and

risks likely to impact upon the Long-term Plan 2027 – 2037 (LTP)

process. The report also provides proposed mitigations for consideration

by the Committee (refer Attachment A).

1.2 A

similar report was considered by the Finance and Performance Committee on 27

August 2025 (F&P meeting). The Committee endorsed a series of high-level

recommendations aimed at mitigating process risks for the LTP.

2. Officer

Recommendations Ngā Tūtohu

That the Audit and

Risk Management Committee:

1. Receives the Long Term Plan 2027 - Risk Assessment and Project

Update report.

2. Notes the Long-term Plan 2027 Project Update and Risk Assessment

report, recommendations and phasing’s approved by the Finance &

Performance Committee at its meeting on 27 August 2025 (refer Attachment A).

3. Endorses the high-level plans set out in Attachment B as an

early step in clarifying and managing process risks to key Long-term Plan

2027-37 (LTP) workstreams.

4. Notes that staff have detailed the key component parts of the LTP in

the report.

5. Notes that a full and detailed LTP project plan will follow

following receipt of the new Council’s Letter of Expectation.

6. Agrees to provide advice to Finance & Performance Committee on

the risks (and the effectiveness of their proposed mitigations) at regular

intervals throughout the preparation of the Long-Term Plan 2027, in line with

its Terms of Reference.

3. Background/Context Te Horopaki

3.1 Under

its Terms of Reference, the Audit and Risk Management Committee (ARMC)

considers and reviews LTP processes during the LTP development and prior to its

adoption by the Council.

3.2 LTPs

are large and complex documents. The process of compiling them is an

organisational wide exercise carried out over an 18-24 month period with a

significant number of risks to be identified and managed. Risks are set

out in Attachment A and can be briefly summarised as arising from:

· a markedly uncertain geopolitical and economic environment;

· the central government elections during the 2026 LTP

‘build’ year;

· a variety of legislative reforms currently being progressed, e.g.

Resource Management reform, the Local Government (Systems Improvement) Bill and

Water Services reform, with the full impact for Council and the sector

remaining uncertain;

· the potential introduction of a rates cap, although there is

considerable uncertainty on the shape and form of any rates capping; and

· a failure of Council internal processes, e.g. the relationship

between the LTP process and other overlapping internal processes is not

established early, accountabilities and milestones for completion not agreed in

advance and adhered to throughout the LTP’s development.

3.3 On

27 August 2025 the F&P meeting approved a range of staff recommendations

designed to mitigate process risks, which are more readily managed than risks

arising from external events. These recommendations originated from a Heads

of Service / ELT meeting on 15 May 2025 and were agreed with the Chief

Executive and ELT. They were developed as learnings from past LTPs and can be

summarised as:

· ‘One Team’ – there

will be a single LTP process and single governance structure. This means one

Steering Group (ELT), LTP Project Sponsor (CFO), LTP Project Manager (Head of

Corporate Planning & Performance) and single LTP project delivery team;

the

community outcomes, financial strategy, infrastructure strategy, activity and

asset plans, budget process and capital programme development must stay aligned

within the LTP project plan in terms of process, mandated content and timings.

· ‘Making It Happen’ –

once the single project plan is agreed, changes must be approved by the LTP

Steering Group or LTP Project Team. Teamwork, which is part of a ‘no

surprises’ policy.

· ‘We have listened’ –

preparation of an integrated LTP process may commence, but LTP content must be

built on guidance from the new (post-election) Council via its Letter of

Expectation (LoE).

3.4 This

means that work currently underway on asset planning, level of service review,

future budgets or capital programmes is on essential and statutory components

of the LTP and remains subject to content change based on LTP decision-making directions

from the new Council.

3.5 At

the same Heads of Service / ELT meeting the Chief Executive emphasised that all

components of an LTP currently exist in both approved and audited form.

Consequently, the focus of the LTP 2027 process must be on review and updating

not starting over from scratch.

3.6 The

F&P meeting identified three specific risks as focus areas:

· internal misalignment and duplication across LTP processes and

components are key risks to effective LTP preparation, to address this the LTP

project plan and accountabilities must address internal coordination issues so

that accountabilities are clear and milestones are fully aligned;

· rates cap: the LTP project plan to develop a scenario containing

options to model the effect of a rates cap (assuming this becomes a legislative

requirement); and

· transparency: the full suite of LTP documentation will remain

transparent to the Mayor, Councillors and the community through the development

of the LTP and thereafter.

3.7 The

F&P meeting requested a draft of a full project plan (full project plan) from

the Project Sponsor and Manager that sets out a ‘single source of

truth’ on all key LTP processes and their timings. It will contain a RACI

model

that confirms all key process accountabilities. The RACI model has been

used as it is a relatively well understood and applied in terms of clarifying

accountabilities in large complex projects.

3.8 Prior

to developing the full project plan, staff believe it is important to set out

the major workstreams, their accountabilities, risks and how it is proposed to

mitigate them (refer Attachment B). This is so the Committee can test the

process that staff are undertaking as part of the LTP’s

development. Once those matters have been framed to the satisfaction of

the ARMC, the full project plan in readiness for the new Council can be

completed and presented.

3.9 Early

direction on the process staff are following to develop the full project plan will

be beneficial to the LTP project, as post 7 October 2025 both the Finance &

Performance Committee and the ARMC will not reconvene until (nominally) late

November and mid-December respectively.

3.10 The summary of

key workstream in the full project plan including the risks, deliverables and

scope is attached (refer Attachment B). This summary has been built using

phasings, deliverables and principles already established with LTP project

team, ELT and Finance & Performance Committee.

3.11 To supplement

the summary of workstreams (Attachment B) key points for ARMC to note on LTP

components are set out below. The components below and the workstreams

referenced in Attachment B form the basis for developing the full project plan

requested at the F&P meeting.

3.12 Letter of

Expectation

3.12.1 Recent LTPs have

benefited from an LoE shortly after the new Council has been elected. Development

of the LoE provides an opportunity for Council to workshop its long-term

objectives, and to clarify priorities and trade-offs. The LoE also means that

staff can develop draft LTP content during the ‘build’ period with

confidence. As with any LoE, the key risks are that it does not provide

clear direction or arrives late which means that major changes in direction are

problematic.

3.12.2 Staff note that the LoE

would normally be finalised around late November or early December.

However, given that central government has signalled an announcement on rates

capping by the ‘end of the calendar year’ some flexibility may be

required to reflect a potentially significant change in government policy

affecting the sector.

3.13 Community

Outcomes

3.13.1 Community outcomes are a

legislative component and sub-set of the LTP project. They describe the

outcomes that a local authority aims to achieve to promote the social,

economic, environmental, and cultural well-being of its district in the present

and for the future.

3.13.2 Community outcomes should

describe desired end states for the community (an outward view) not for the

Council organisation (an inward view). If not carefully framed they may

be expressed in vague or theoretical language, or as operational workstreams or

capital projects. If community outcomes are not clearly defined or

genuinely reflective of what matters, it becomes difficult to use them

effectively in service level reviews and capital delivery prioritisation. This

can undermine the development of an integrated LTP that aligns with the

Council’s priorities for the community.

3.13.3 Broadly, development of

the community outcomes occurs in stages. The first is for Council to have

a ‘free range’ discussion on the outcomes its wishes to achieve

including its priorities and projects. Consideration could be given to

external facilitation for this exercise.

3.13.4 Secondly, a

cross-functional team of staff takes the Councillor guidance in terms of its

outcomes, priorities and projects and frames these as community outcomes.

These are then presented back to Council for it to consider and adopt if they

meet its expectations. It is envisaged this cross-functional staff team

would be made up of key stakeholders representing Infrastructure, Citizens

& Communities, Planning, Strategic Policy, Communications, and potentially

the Principal Policy Advisor.

3.14 Financial

Strategy (FS)

3.14.1 The FS is a legislative

component and sub-set of the LTP project. The purposes of the FS are to:

(a) facilitate prudent financial management by providing a

guide to consider proposals for funding and expenditure against; and

(b) provide a context for consultation on Council’s

proposals for funding and expenditure by making transparent the overall effects

of those proposals on the local authority’s services, rates, debt, and

investments.

3.14.2 Early input from Council

on key parameters will be important for the development of the FS, particularly

if the foreshadowed rates cap eventuates with significant rating constraints.

3.14.3 The statutory

requirements for the FS are set out in section 101A of the LGA, and it and the

infrastructure strategy (IS) need to be aligned and integrated.

3.14.4 Having subject matter

experts as part of the FS development is a key control to ensure the section

101A statutory requirements are met. In terms of integration with the IS,

continuous liaison will help manage this risk, and staff advise that it would

be prudent for a subject matter expert member of each team (FS and IS) to be

represented on the other respective workstream.

3.14.5 Staff also note that some

preliminary modelling has been commenced to understand the effects of a rates

cap on future budgets.

3.15 Infrastructure

Strategy (IS)

3.15.1 The IS is a legislative

component and sub-set of the Long-Term Plan project, covering a minimum 30-year

period, with the statutory requirements set out in section 101B of the LGA. Its

purpose is to identify significant infrastructure issues facing Council over

that timeframe, and to outline the principal options for managing those issues

along with their implications.

3.15.2 The IS must explain how

Council will manage its infrastructure assets, including the renewal or

replacement of existing assets, responding to changes in demand (growth or

decline), adjusting levels of service, protecting public health and the

environment, mitigating adverse effects, and improving resilience by managing

risks from natural hazards and making appropriate financial provisions.

3.15.3 The IS must outline the

most likely scenario for infrastructure asset management, including projected

capital and operating expenditure for each of the first 10 years and each

subsequent 5-year period, significant capital decisions (including timing,

options, and estimated costs), and the key assumptions underpinning the

scenario, such as asset life cycles, changes in demand and service levels, and

the impact of uncertainty.

3.15.4 The IS is a critical

component of LTP as it sets out the major drivers for managing assets and these

must align with both asset management plans, the development of the capital

programme and the FS. To manage the risks of misalignment between the IS

and other components of the LTP, staff advise that a small, well-rounded

cross-functional team is best suited to framing the IS. This group would

have representatives from key infrastructure stakeholders, eg Infrastructure

Group, Citizens and Community, along with Strategic Policy, Planning &

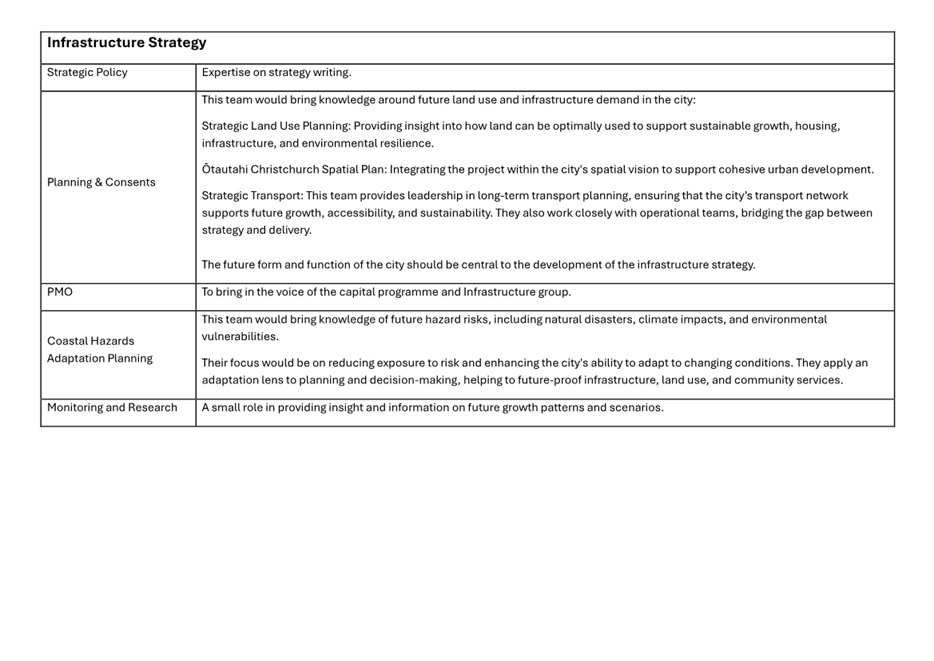

Consents, PMO, Coastal Hazards Adaption Planning, Monitoring & Research and

Finance to support continuous liaison with the FS workstream.

3.16 Opex

Budgeting

3.16.1 As with previous LTPs

this is both a ‘business as usual’ (BAU) function of Council and an

LTP workstream. It relies on a clear LoE, particularly around levels of

service and early FS parameters as operating expenditure is a primary driver of

rates increases.

3.17 Capital

programme development

3.17.1 As with previous LTPs

this is both a BAU function of Council and an LTP workstream.

3.17.2 As part of the Annual

Plan 2025/26 development, significant work was carried out by Council’s

Project Management Office (PMO) to determine a ‘deliverable’

capital programme for the 2025/26 year. This resulted in a significant

reduction in the core capital programme (excluding Te Kaha) of circa $70m from

what was forecast in the LTP 2024-34 (down from $620m to $550m). A

similar exercise to determine what is deliverable is being conducted for the

2026/27 annual plan (currently under development).

3.17.3 As part of the LTP

development, the PMO will continue to work on what is a deliverable 10 year

capital programme. This work is informed from multiple sources including

the LoE, the asset management plans and both the FS and IS. It is cross

organisational involving Heads of Service, project managers and finance team

members.

3.17.4 With the current work on

deliverability, it is expected the PMO will be able to largely mitigate the

risk that emerged in the 2024 LTP where the capital programme began with a Y1

(unprioritised) budget of $1.3B. An inflated undeliverable capital budget

risks delay and confusion for the development of a rigorous deliverable final

capital programme to be adopted as part of the LTP.

3.18 Asset planning

(alignment)

3.18.1 As with previous LTPs

this is both a BAU function of Council and – in terms of alignment only -

an LTP workstream. Asset plans (which drive the majority of capital programme

spend through renewals and replacements) are currently being developed before

community outcomes, IS, FS parameters or LoS review results are known.

3.18.2 However, this work is

proceeding on the basis that asset plans will be modified to align with LTP

decisions made by Council. This is important as asset plans are

scrutinised as part of the LTP audit, usually by a specialist asset planning

auditor, to assess alignment with other core LTP documents. Areas

examined include:

(a) whether the asset data on condition, performance and life

cycle are fit for purpose;

(b) whether the asset plans align with the guidance on

renewing and/or replacing existing assets in the IS; and

(c) whether the asset plans align with the levels of service,

budgets etc set in the LTP.

3.18.3 Audit has noted in the

past that there have been issues with unnecessary duplication and different

levels of service in asset plans and other LTP documents such as activity

plans, hence the focus on alignment across and within the various LTP component

documents.

3.19 Activity plans

/ level of service review

3.19.1 Following work with ELT

and Heads of Service a structured approach is being developed that will enable

a level of service review if that is a decision of Council and which

would be directed through the LoE (and potentially also initiated by central

government announcements on a rates cap).

3.19.2 Broadly, the plan is to

map the levels of service to the agreed community outcomes (when they are

finalised by Council) and test the alignment between them. Staff note

that where there are mandatory levels of services these will need to be

excluded from a level of service review, acknowledging that in some instances

the performance target for some mandatory measures can be adjusted.

3.20 Consultation document

(CD)

3.20.1 This is a legislative

component and sub-set of the LTP project. The purpose and statutory

requirements for the CD are set out in sections 93B -93D of the LGA 2002.

Lessons from earlier CDs highlight the importance of a single lead

‘holding the pen.’ This mitigates significantly the risk of

inconsistent facts, messages, language, delivery and layout. Management of the

CD under a single, unifying voice and process lead is considered important.

3.20.2 Key risks for a CD

include excessive length, complexity and lack of clear, easily understood

options for consideration by the community of significant issues.

3.21 Specific

risks from LTP audit

3.21.1 The effect and

implications of central government reforms and their implementation in the LTP

process will receive scrutiny from Audit NZ. Audit NZ has indicated that up to

$80K in extra funding for the audit process may be needed for the 2027 LTP.

Staff note this is in keeping with an $80K cost overrun for the 2024 LTP.

3.21.2 As noted above Audit NZ

has previously identified misalignment and duplication across Council processes

as key risks to effective LTP preparation. These have cost escalation

implications and has been referenced by Audit NZ when seeking a higher fee

recovery.

3.21.3 Where the LTP does not

provide adequately for the implementation of reforms or there is unresolved

misalignment of component documents, eg between asset plans and the IS and/or

FS, there is an increased risk of a qualified LTP. This has potential

implications for Council’s reputation and likely increased and unbudgeted

costs.

3.22 Risk around

conflating the purpose of an annual plan with LTP

3.22.1 In general the purpose of

an annual plan is to make transparent variations to the LTP, that are neither

material nor significant, and which is why annual plans are not audited.

An annual plan can include specific amendments to the LTP, provided they are

not deemed significant (section 97 of the LGA).

3.22.2 However, if the aim is to

significantly alter the intended level of service for any significant activity

(including a decision to commence or cease any such activity) or transfer the

ownership or control of a strategic asset to or from the local authority, then

those decisions must be taken within an LTP.

3.22.3 Unlike the one-year

horizon of an annual plan, LTPs cover a 10-year period and require

significantly more time and resources to prepare, as well having extensive

audit requirements. There is a high degree of risk around attempting to

prepare an LTP in the much shorter timeframes typically available to an annual

plan.

3.22.4 There needs to be a clear

distinction made between what are non-material variations to an LTP within the

annual plan process, having regard to the LGA and Council’s Significance

and Engagement Policy, and changes which require an LTP to be undertaken.

Having discussions with the Council early in the new triennium on the

distinction is important so that it is well informed on the implications of any

decision it makes to undertake an LTP rather than an annual plan process.

3.23 Special focus

areas identified by the Finance and Performance Committee

3.23.1 These have been addressed

in Attachment B but in summary the concerns raised were:

· internal misalignment and duplication across LTP processes and

components are key risks to effective LTP preparation, the LTP project plan and

accountabilities are the controls to address internal coordination risks and

issues;

· rates cap: the LTP project plan must develop a scenario containing

options that would address a rates cap, if legislation to that effect is

introduced;

· transparency: the full suite of LTP documentation will remain

transparent to the Mayor, Councillors and the community through the development

of the LTP and thereafter.

3.24 LTP Project

Governance and Decision-making

3.24.1 The governance model

approved by Finance & Performance Committee follows a clear and direct

approach:

· LTP Governance - All decisions on the content of the Consultation

Document and supporting LTP documents (FS, IS, activity plans (incl LoS), asset

plans, capital programme) rest with Council, or the Finance & Performance

Committee as delegate;

· LTP Steering Group (ELT) provides direction to staff on strategic

aspects of the LTP during development of draft components (for example, capital

programme deliverability, budget prioritisation decisions, CD options);

· LTP Project Team assists the Project Sponsor and Manager in project

co-ordination at operational level;

· The LTP Project Sponsor (CFO) has executive accountability for the

LTP process and advising the CE;

· The LTP Project Manager (Head of Corporate Planning &

Performance) is responsible for programme management of the LTP –

workstream phasing and milestones, deliverables, quality and risk assurance and

reporting, all materials for LTP workshops with Council to be managed and

coordinated by the Project Manager as a single point of contact.

4. Considerations Ngā Whai Whakaaro

4.1 The

Finance and Performance Committee endorsed the attachments to the LTP report of

27 August 2025, including key principles, phasings, deliverables and governance

structure.

4.2 If

the high-level work stream plans for the LTP development set out in Attachment

B along with the key component parts referenced above are approved by the ARMC

as fit for purpose, a detailed project plan and RACI matrix of accountabilities

will be developed by the LTP Manager for approval by the Project Sponsor.

This will be presented to both the Finance & Performance and Audit &

Risk Management Committees to provide assurance appropriate internal processes

are in place for the efficient and timely development and delivery of the LTP

and its component parts.

4.3 It

is proposed that this will occur at their next meetings, nominally set down for

late November (F&P Committee) and mid-December 2025 (ARMC).

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Finance and

Performance Committee Long Term Plan 2027 - Project Update and Risk

Assessment 27 August 2025 Report

|

25/1844900

|

23

|

|

b ⇩

|

Summary of

Workstream Plans

|

25/1999975

|

35

|

In addition to the attached documents, the following background

information is available:

Signatories Ngā Kaiwaitohu

|

Authors

|

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

Peter Ryan -

Head of Corporate Planning & Performance

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

Mary

Richardson - Chief Executive

|