Audit and Risk Management Committee

Agenda

Notice of Meeting:

An ordinary meeting of the Audit and Risk

Management Committee will be held on:

Date: Monday 10 February 2025

Time: 9.30 am

Venue: Council Chambers, Level 2, Civic Offices,

53 Hereford Street, Christchurch

Membership

|

Chairperson

Deputy Chairperson

Members

|

Mr Bruce Robertson

Councillor Jake McLellan

Councillor Tyrone Fields

Councillor Sam MacDonald

Councillor Tim Scandrett

Mrs Hilary Walton

Mr Michael Wilkes

|

4 February 2025

Website: www.ccc.govt.nz

Audit

and Risk Management Committee - Terms of Reference Ngā Ārahina Mahinga

|

Chair

|

Mr Bruce Robertson

|

|

Deputy Chair

|

Councillor McLellan

|

|

Membership

|

Councillor Fields

Councillor MacDonald

Councillor Scandrett

External Members:

Mrs Hilary Walton

Mr Michael Wilkes

|

|

Quorum

|

Half of the members if the

number of members (including vacancies) is even, or a majority of members if

the number of members (including vacancies) is odd.

|

|

Meeting

Cycle

|

Quarterly and

as required

|

|

Reports

To

|

Council

|

Purpose

To assist the Council to discharge

its responsibility to exercise

due care, diligence and skill in relation to the oversight of:

·

the robustness of the internal control framework;

·

the integrity and appropriateness of external reporting, and

accountability arrangements within the organisation for these functions;

·

the robustness of risk management systems, process and practices;

·

internal and external audit;

·

accounting policy and practice;

·

compliance with applicable laws, regulations, standards and best

practice guidelines for public entities; and

·

the establishment and maintenance of controls to safeguard the

Council’s financial and non-financial assets.

The foundations on which this

Committee operates, and as reflected in this Terms of Reference, includes:

independence; clarity of purpose; competence; open and effective relationships

and no surprises approach.

Procedure

·

In order to give effect to its advice the Committee should make recommendations to the Council and to

Management.

·

The Committee should meet the internal and the external auditors

without Management present as a standing agenda item at each meeting where

external reporting is approved, and at other meetings if requested by any of

the parties.

·

The external auditors,

the internal audit manager and the co-sourced internal audit firm should meet

outside of formal meetings as appropriate with the Committee Chair.

·

The Committee Chair

will meet with relevant members of Management before each Committee meeting and

at other times as required.

Responsibilities

Internal Control Framework

·

Consider the adequacy and effectiveness of internal controls and

the internal control framework including overseeing privacy and cyber security.

·

Enquire as to the steps management has taken to embed a culture

that is committed to probity and ethical behaviour.

·

Review the processes or systems in place to capture and

effectively investigate fraud or material litigation should it be required.

·

Seek confirmation annually and as necessary from internal and

external auditors, attending Councillors, and management, regarding the

completeness, quality and appropriateness of financial and operational

information that is provided to the Council.

Risk Management

·

Review and consider Management’s risk management framework

in line with Council’s risk appetite, which includes policies and

procedures to effectively identify, treat and monitor significant risks, and

regular reporting to the Council.

·

Assist the Council to determine its appetite for risk.

·

Review the principal risks that are determined by Council and

Management, and consider whether appropriate action is being taken by

management to treat Council’s significant risks. Assess the effectiveness

of, and monitor compliance with, the risk management framework.

·

Consider emerging significant risks and report these to Council

where appropriate.

Internal Audit

·

Review and approve the annual internal audit plan, such plan to

be based on the Council’s risk framework. Monitor performance against the

plan at each regular quarterly meeting.

·

Monitor all internal audit reports and the adequacy of

management’s response to internal audit recommendations.

·

Review six monthly fraud reporting and confirm fraud issues are

disclosed to the external auditor.

·

Provide a functional reporting line for internal audit and ensure

objectivity of internal audit.

·

Oversee and monitor the performance and independence of internal

auditors, both internal and co-sourced. Review the range of services provided

by the co-sourced partner and make recommendations to Council regarding the

conduct of the internal audit function.

·

Monitor compliance with the delegations policy.

External Reporting and

Accountability

·

Consider the appropriateness of the Council’s existing

accounting policies and practices and approve any changes as appropriate.

·

Contribute to improve the quality, credibility and objectivity of

the accounting processes, including financial reporting.

·

Consider and review the draft annual financial statements and any

other financial reports that are to be publicly released, make recommendations

to Management.

·

Consider the underlying quality of the external financial

reporting, changes in accounting policy and practice, any significant

accounting estimates and judgements, accounting implications of new and

significant transactions, management practices and any significant

disagreements between Management and the external auditors, the propriety of

any related party transactions and compliance with applicable New Zealand and

international accounting standards and legislative requirements.

·

Consider whether the external reporting is consistent with

Committee members’ information and knowledge and whether it is adequate

for stakeholder needs.

·

Recommend to Council the adoption of the Financial Statements and

Reports and the Statement of Service Performance and the signing of the Letter

of Representation to the Auditors by the Mayor and the Chief Executive.

·

Enquire of external auditors for any information that affects the

quality and clarity of the Council’s financial statements, and assess

whether appropriate action has been taken by management.

·

Request visibility of appropriate management signoff on the

financial reporting and on the adequacy of the systems of internal control;

including certification from the Chief Executive, the Chief Financial Officer

and the General Manager Corporate Services that risk management and internal

control systems are operating effectively;

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

·

Review and consider the Summary Financial Statements for

consistency with the Annual Report.

External Audit

·

Annually review the independence and confirm the terms of the

audit engagement with the external auditor appointed by the Office of the

Auditor General. Including the adequacy of the nature and scope of the audit,

and the timetable and fees.

·

Review all external audit reporting, discuss with the auditors

and review action to be taken by management on significant issues and

recommendations and report to Council as appropriate.

·

The external audit reporting should describe: Council’s

internal control procedures relating to external financial reporting, findings

from the most recent external audit and any steps taken to deal with such

findings, all relationships between the Council and the external auditor,

Critical accounting policies used by Council, alternative treatments of

financial information within Generally Accepted Accounting Practice that have

been discussed with Management, the ramifications of these treatments and the treatment

preferred by the external auditor.

·

Ensure that the lead audit engagement and concurring audit

directors are rotated in accordance with best practice and NZ Auditing

Standards.

Compliance with Legislation,

Standards and Best Practice Guidelines

·

Review the effectiveness of the system for monitoring the

Council’s compliance with laws (including governance legislation,

regulations and associated government policies), with Council’s own

standards, and Best Practice Guidelines.

Appointment of Independent Members

·

Identify skills required for Independent Members of the Audit and

Risk Management Committee. Appointment panels will include the Mayor or

Deputy Mayor, Chair of Finance & Performance Committee and Chair of Audit

& Risk Management Committee. Council approval is required for all

Independent Member appointments.

·

The term of the Independent members should be for three

years. (It is recommended that the term for independent members begins on

1 April following the Triennial elections and ends 31 March three years

later. Note the term being from April to March provides continuity for

the committee over the initial months of a new Council.)

·

Independent members are eligible for re-appointment to a maximum

of two terms. By exception the Council may approve a third term to ensure

continuity of knowledge.

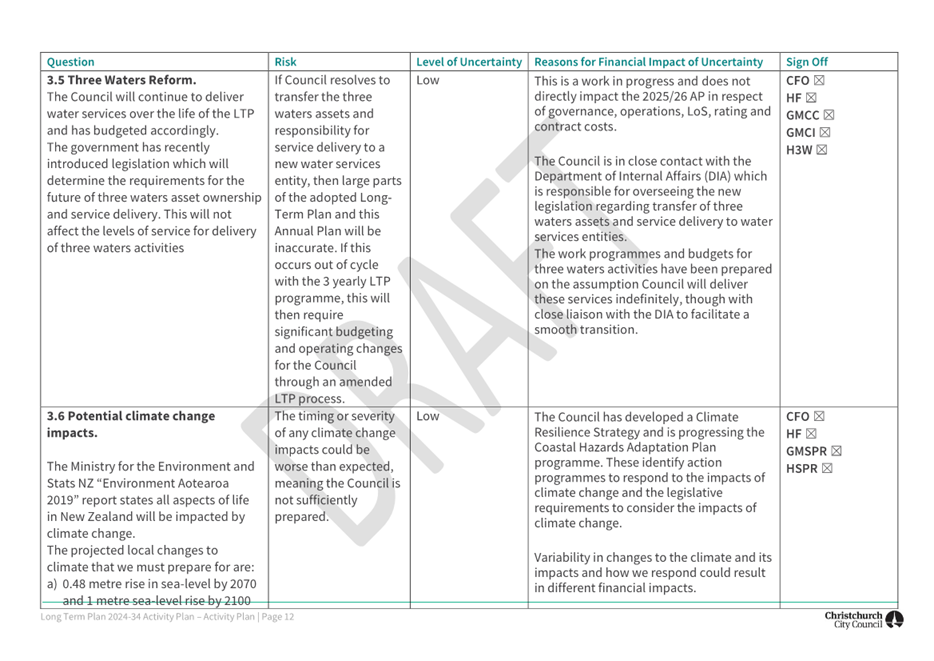

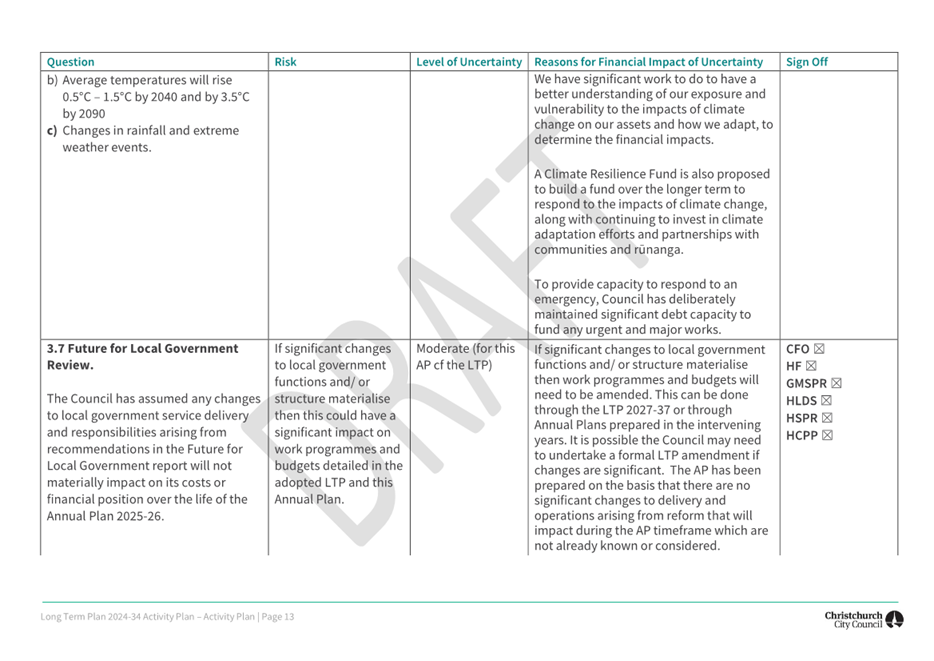

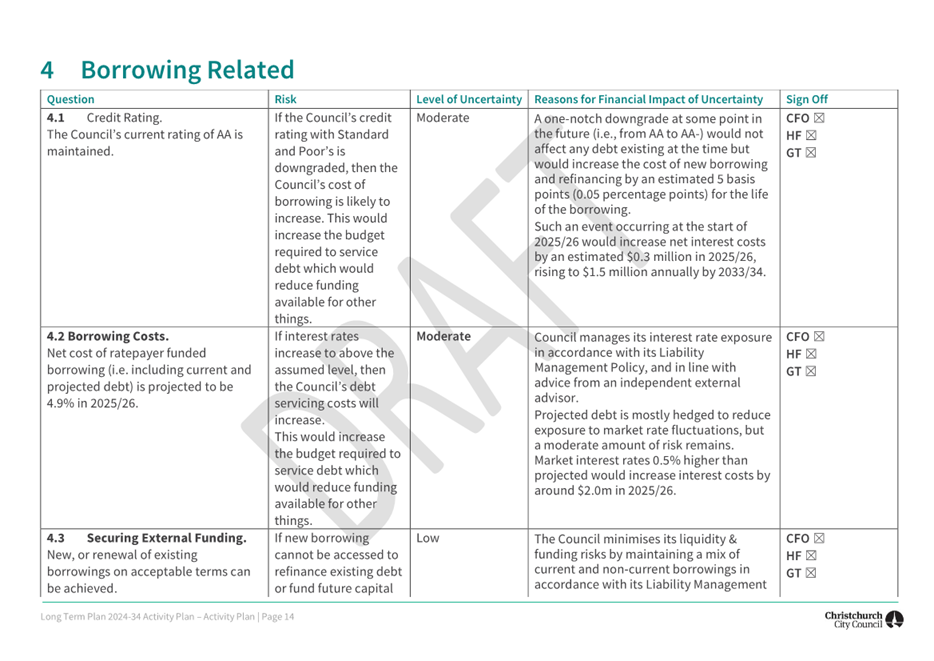

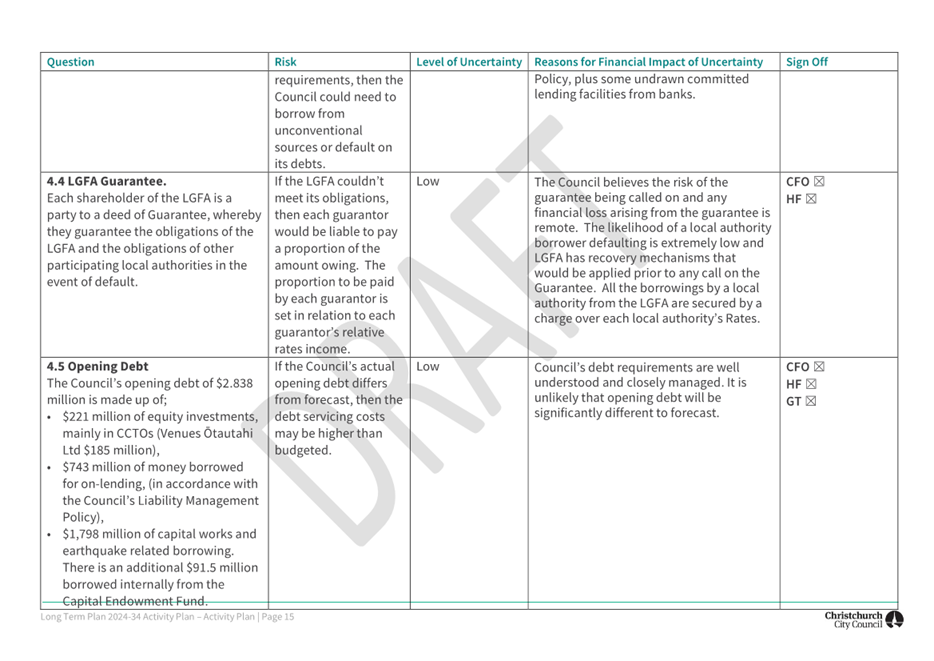

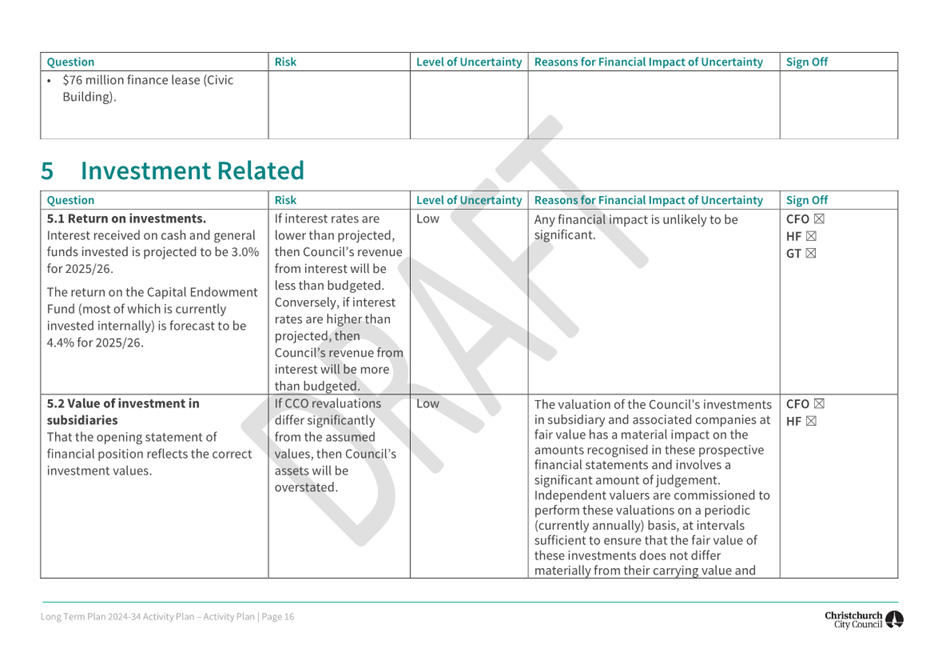

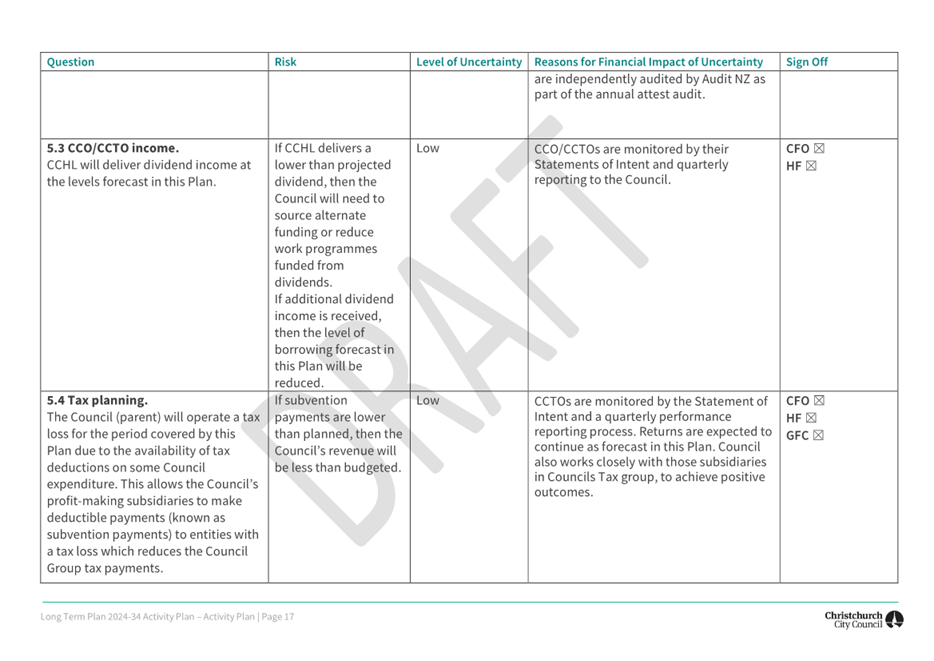

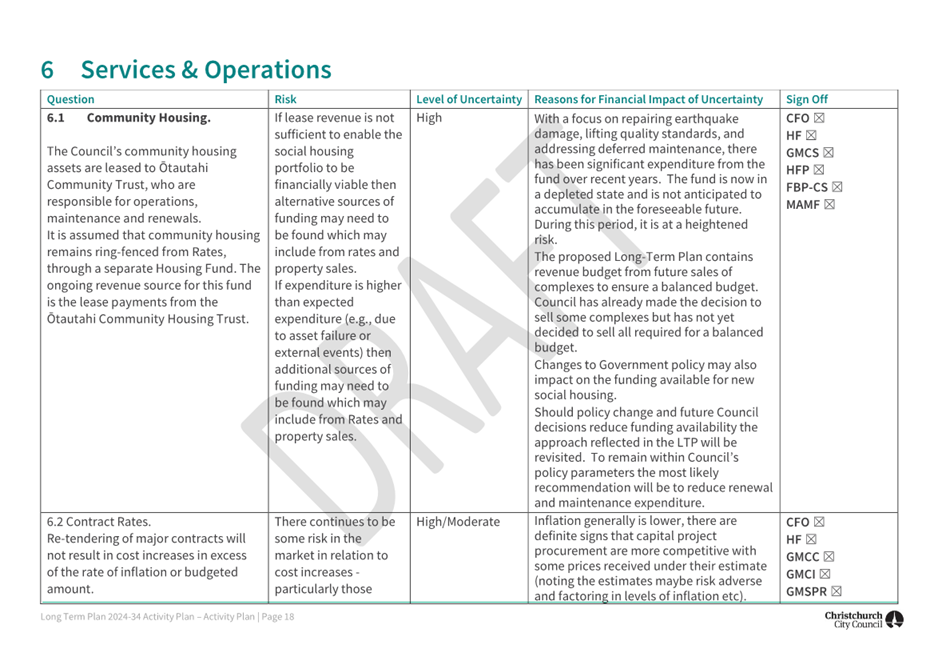

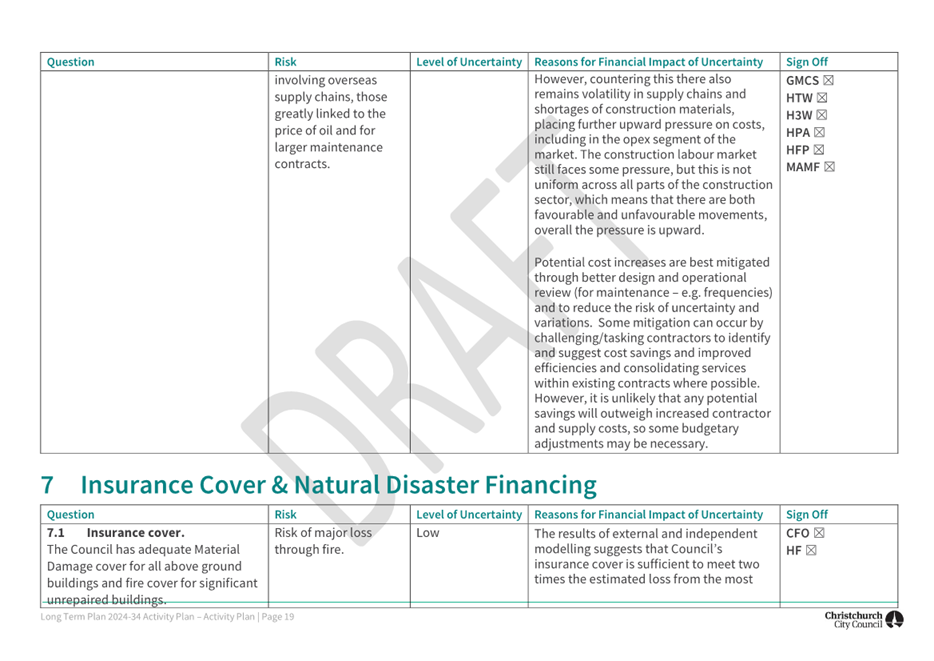

Long Term Plan Activities

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

Audit and Risk Management Committee

Forward Work Programme 2025

|

2025

|

Feb 10

|

Apr 4

|

Jun 17

|

Aug 15

|

Annual Report

Oct 6

|

Dec

|

|

Update Reports

|

·

Risk

and Assurance

·

Cyber

Security Report

·

Parakiore

Update

|

·

Risk

and Assurance

·

Procurement

|

· Risk and Assurance

|

· Risk and Assurance

· Procurement

·

Cyber

Security

|

|

· Risk and Assurance

· Procurement

· Health, Safety & Wellbeing

|

|

Other Reports

|

·

Insurance

Update

|

·

|

· Kiwi Rail Update

· Te Kaha Update

|

|

|

·

Kiwi

Rail Update

|

|

Annual Report

|

·

Audit

Management Report 2024

|

·

External

Reporting and Audit Programme for 2022/23 Update

|

·

External

Reporting and Audit Programme Update

·

Audit

NZ Management Letter for current year interim audit

|

· Update on critical judgments, estimates

& assumptions

· Financial Statements Update - Valuations

|

·

Financial Statements

and Annual Report

|

·

Audit NZ Management

Letter from prior year’s audit

|

|

Annual Plan

|

·

Draft

Annual Plan

|

|

·

Final

Annual Plan

|

|

|

|

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

TABLE OF CONTENTS NGĀ IHIRANGI

C 1. Apologies Ngā Whakapāha.......................................................................... 9

B 2. Declarations of Interest Ngā Whakapuaki Aronga........................................... 9

C 3. Confirmation of Previous Minutes Te Whakaāe o te

hui o mua.......................... 9

B 4. Public Forum Te Huinga Whānui.................................................................. 9

B 5. Deputations by Appointment Ngā Huinga

Whakaritenga................................. 9

B 6. Presentation

of Petitions Ngā

Pākikitanga.................................................... 9

Staff Reports

C 7. Consideration

of the Council's Draft Annual Plan 2025/26.............................. 13

C 8. Resolution

to Exclude the Public................................................................ 53

1. Apologies Ngā Whakapāha

Apologies will

be recorded at the meeting.

2. Declarations of Interest Ngā

Whakapuaki Aronga

Members are

reminded of the need to be vigilant and to stand aside from decision-making

when a conflict arises between their role as an elected representative and any

private or other external interest they might have.

3. Confirmation of Previous Minutes Te

Whakaāe o te hui o mua

That the

minutes of the Audit and Risk Management Committee meeting held on Friday, 6 December 2024 be confirmed

(refer page 10).

4. Public Forum Te Huinga Whānui

A period of up

to 30 minutes may be available for people to speak for up to five minutes on

any issue that is not the subject of a separate hearing process.

Public Forum presentations will be

recorded in the meeting minutes

5. Deputations by Appointment Ngā Huinga

Whakaritenga

Deputations will

be recorded in the meeting minutes.

6. Petitions Ngā Pākikitanga

There were no

petitions received at the time the agenda was prepared.

Audit and Risk Management Committee

Open Minutes

Date: Friday 6 December 2024

Time: 9.32am

Venue: Council Chambers, Level 2, Civic Offices,

53 Hereford Street, Christchurch

Present

|

Chairperson

Members

|

Mr Bruce Robertson

Councillor Sam MacDonald

Councillor Tim Scandrett

Mrs Hilary Walton

Mr Michael Wilkes

|

Website: www.ccc.govt.nz

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

The agenda was dealt with in the following

order.

1. Apologies

Ngā Whakapāha

Part C

|

Committee Resolved ARCM/2024/00029

That the apologies from Councillor Fields

and Councillor McLellan for absence be accepted.

Mr

Robertson/Councillor Scandrett Carried

|

2. Declarations

of Interest Ngā Whakapuaki Aronga

Part B

There were no

declarations of interest recorded.

3. Confirmation

of Previous Minutes Te Whakaāe o te hui o mua

Part C

|

Committee Resolved ARCM/2024/00030

That the

minutes of the Audit and Risk Management Committee meeting held on Thursday,

17 October 2024 be confirmed.

Mr Robertson/Mr

Wilkes Carried

|

4. Public

Forum Te Huinga Whānui

Part B

There were no public forum presentations.

5. Deputations

by Appointment Ngā Huinga Whakaritenga

Part B

There were no deputations by appointment.

6. Presentation

of Petitions Ngā Pākikitanga

Part B

There was no presentation of petitions.

|

7. Procurement

& Contracts FY25 Q1

|

|

|

Committee Resolved ARCM/2024/00031

Officer Recommendation accepted without

change

Part C

That the Audit

and Risk Management Committee:

1. Receive the information in the Procurement & Contracts FY25 Q1 Report.

Mr

Robertson/Councillor Scandrett Carried

|

|

8. Resolution

to Exclude the Public Te whakataunga kaupare hunga tūmatanui

|

|

|

Committee Resolved ARCM/2024/00032

Part C

That Chantelle Gernetzky of Audit New Zealand remain after the

public have been excluded for Items 9 to 12 in the public excluded agenda as

they have knowledge that is relevant to those Items and will assist the

Council.

AND

That at 9.44am the resolution to exclude the public set out on

pages 19 to 21 of the agenda be adopted.

Mr

Robertson/Councillor MacDonald Carried

|

The public were re-admitted to the meeting

at 11.16am.

Meeting

concluded at 11.17am.

CONFIRMED THIS 10th DAY OF FEBRUAY

2025

Bruce Robertson

Chairperson

|

7. Consideration

of the Council's Draft Annual Plan 2025/26

|

|

Reference Te Tohutoro:

|

24/2209871

|

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance Peter.Ryan@ccc.govt.nz

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 Under

their Terms of Reference, Audit and Risk Management Committee considers and

reviews the Long Term and Annual Plans before adoption by the Council.

1.2 The

purpose of this report is to enable the Audit and Risk Management Committee to

review the process for preparation of the Draft Annual Plan 2025/26.

1.3 The

Council is required to prepare and adopt a Draft Annual Plan for each financial

year (s.95(1)) Local Government Act 2002). The purpose of the plan is to:

1.3.1 contain the proposed

annual budget and funding impact statement for 2025/26;

1.3.2 identify any

variation from the financial statements and funding impact statement in the

Council’s Long Term Plan for 2025/26;

1.3.3 provide integrated

decision-making and co-ordination of the Council’s resources; and

1.3.4 contribute to the

accountability of the Council to the community.

1.4 The

decisions in this report are not of high significance in relation to the

Christchurch City Council’s Significance and Engagement Policy.

This is largely as it reports on the process for development of the Annual

Plan. It is important to distinguish between a review of the process for

development of the Draft Annual Plan and the Draft Annual Plan itself.

The Council’s Draft Annual Plan 2025/26 is of high significance as it

contains information that varies to some degree from the information contained

in the Long Term Plan 2024-34 (LTP) for that year. Individually, these

changes may not be regarded as being significant or material, collectively they

are considered significant and as such Council will consult on its Draft Annual

Plan.

2. Officer Recommendations Ngā Tūtohu

That the Audit and

Risk Management Committee:

1. Receives the information in the Consideration of the Council's Draft Annual

Plan 2025/26 Report.

2. Notes that it has reviewed the general

checklists and sign-offs by management, including Significant Forecasting

Assumptions, in respect of the information that

provides the basis for the Draft Annual Plan 2025/26.

3. Advises the Council that in the

Committee’s opinion, an appropriate process has been followed in the

preparation of the information that provides the basis for the Draft Annual

Plan 2025/26.

4. Notes that the Draft Annual Plan 2025/26 will

be released when it is published in the Council Agenda for its meeting

commencing 12 February 2025.

3. Background/Context Te Horopaki

3.1 The

purpose of this report is to enable the Audit and Risk Management Committee to

review the process for preparation of the Draft Annual Plan 2025/26.

3.2 The

LTP was approved by Council in June 2024. That approval followed a

comprehensive process that reviewed operational expenditure, levels of service

and the capital programme in a highly detailed way.

3.3 The

purpose of the Draft Annual Plan 2025/26 is to identify any changes that need

to be made to the LTP to keep it current. The draft Annual Plan has been

developed from the information contained in the LTP for the 2025/26 financial

year, as well as recent guidance from the Mayor and Councillors.

3.4 As

the draft Annual Plan evolved between August 2024 and December 2024, council

staff held a series of workshops with the Mayor and Councillors to obtain

overall guidance on what to include in the Draft Annual Plan and to update

specific details with current information. The workshops included open

(public and live-streamed) and public-excluded briefings on the following

dates: 27 August, 24 September, 1 October, 15 October, 22 October, 29 October,

5 November, 12 November, 19 November, and 26 November 2024.

3.5 This

approach (public and live-streamed briefings) followed feedback from similar

public briefings held as part of the previous LTP development, and provides

Councillors an opportunity to discuss Annual Plan choices and priorities in a

public, non-decision-making setting. In addition, it provided

opportunities for Councillors to discuss their expectations for matters such as

rates increases and level of debt. The draft Annual Plan contains no

significant changes to levels of service.

3.6 During

these workshops, discussions and questions were considered relating to many

factors relevant to the Annual Plan, including:

3.6.1 The

scope of the Annual Plan 2025/26.

3.6.2 Actions

that were carried over from the LTP that were to be considered as part of the

Annual Plan 2025/26.

3.6.3 The

structure of the Capital Programme, particularly relating to the major

infrastructure areas of Transport, Three Waters, and Parks.

3.6.4 New

financial information that came to hand during the development process,

including:

· Changes to

revenue.

· Increased

staff costs.

· Changes to

insurance costs.

· An insurance settlement

resulting from the Wastewater Treatment Plant fire.

· Changes to

central government funding for infrastructure and cycleways.

· New central

government levies to fund the changes resulting from repeal of the Three Waters

legislation.

· Increased

operational costs for several activities.

· Changes in the

BERL inflation forecasts.

3.6.5 The

likely quantum of rates rises for 2025/26.

3.6.6 Previous

decisions by Council during the LTP and in previous years that had

significantly increased rates for the 2025/26 year.

3.6.7 Potential

financial methods (levers) for reducing rates increases.

3.6.8 The

funding strategy for renewals.

3.6.9 Properties

proposed for disposal.

3.7 During

the development and workshop process, the Q+A Tool that was developed during

the LTP was used to collate and respond to Councillor questions on the

development of the Annual Plan. The tool is another mechanism that Councillors

can utilise to contribute to the development of the Annual Plan.

3.7.1 Some

24 queries/questions were received from Councillors on the Annual Plan. All of

these queries have been resolved/closed.

3.7.2 In

comparison, during the period of the LTP development, several hundred questions

were received from Councillors and responded to by staff.

3.8 A

further Council meeting was held on 10 December 2024 to obtain clear direction

on what to include in the Draft Annual Plan. At the 10 December meeting, the

Council considered and made decisions on content to include in the Draft Annual

Plan, including:

3.8.1

Rates increase of 8.93%, comprising 8.48% as per year 2 of the 2024-34

Long-Term Plan, a further 0.28% being Central Government imposed costs for

water services regulators, and increased capacity to support amendments to the

District Plan at a cost of $1.125 million p.a.

3.8.2 The

use of $6 million of subvention receipts to reduce rates increases; and

3.8.3 The

use of $6 million of forecast current year (2024/25) operating surplus to

reduce rates increases ($3.35 million) and reduce debt ($2.65 million).

3.8.4 Acknowledgement

of a breach of the balanced budget financial prudence benchmark for 2025/26

(and 2026/27, as indicated in the LTP).

3.8.5 Inclusion

of additional rating of $5/10/15 million (plus inflation) over the next three

years to enable the balanced budget prudence benchmark to be met by 2027/28.

While the LTP showed the 2026/27 benchmark as not met, latest modelling shows

that without this increase the next four years are at risk. The additional

rates will be applied to funding asset renewals in lieu of borrowing to reduce

interest and debt repayment costs. It should be noted that the benchmark is one

of a number of regulatory measures that indicates financial prudence.

3.9 Council

also decided that the following topics would be explored further/consulted upon

as part of the Draft Annual Plan 2025/26 consultation process:

· Cathedral Targeted Rate - Given the situation with the Cathedral reconstruction, the draft

Plan proposes pausing the collection of the remaining three years of the

Cathedral targeted rate (a fixed charge of $6.52 per annum). The existing

ringfenced funds held will continue to earn interest in the interim. As

previously advised, the community should be consulted about this proposed

change.

· Postponing the

completion of the Wheels to Wings cycleway in favour of implementing selected

portions of the project.

3.10 Having

received this specific direction from Councillors, staff proceeded to build the

report and attachments for the Draft Annual Plan 2025/26. The process for

preparing this information has been the subject of a detailed series of

management sign offs – including signoffs by members of the Executive

Leadership Team - that demonstrate compliance with the Council’s

statutory, financial, and legal obligations. The management process and

significant assumptions checklists and sign-off schedules are attached to this

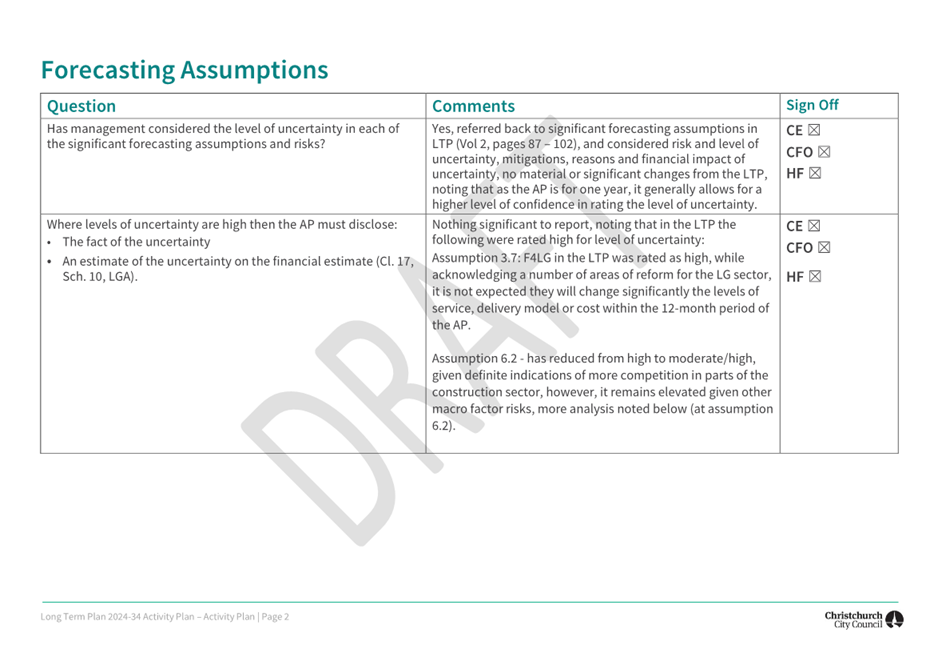

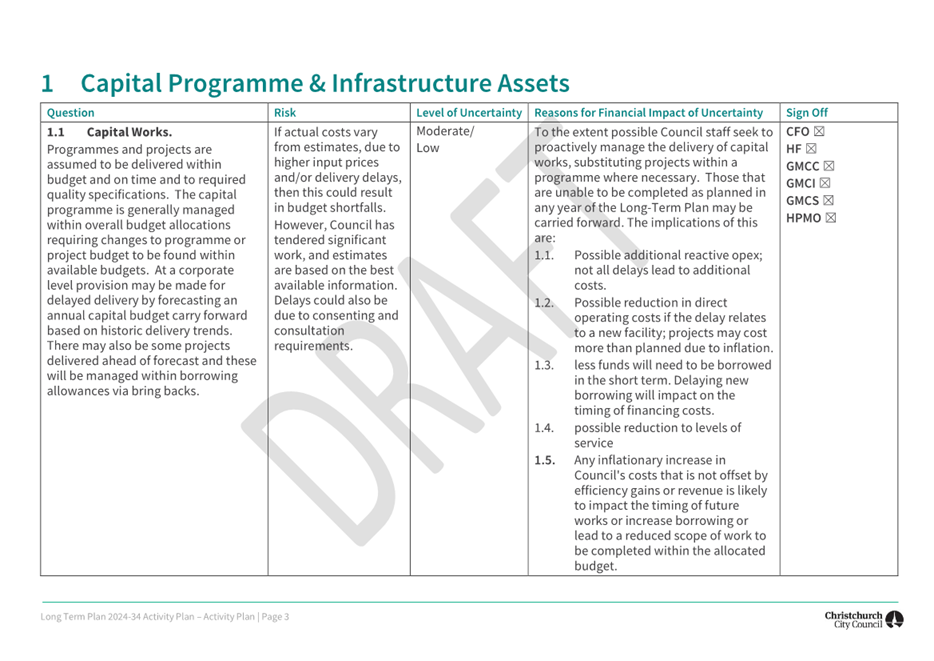

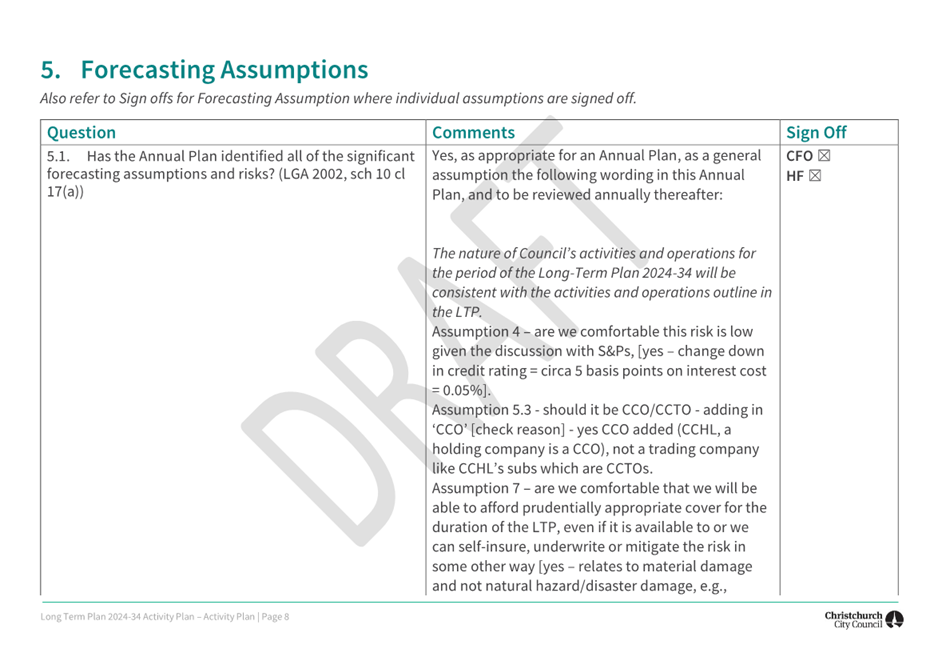

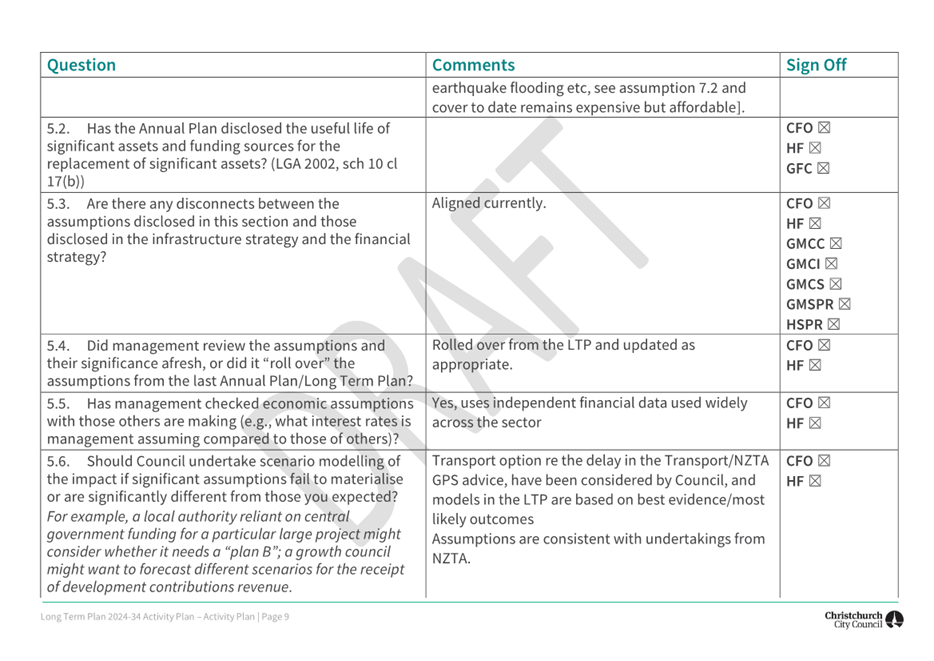

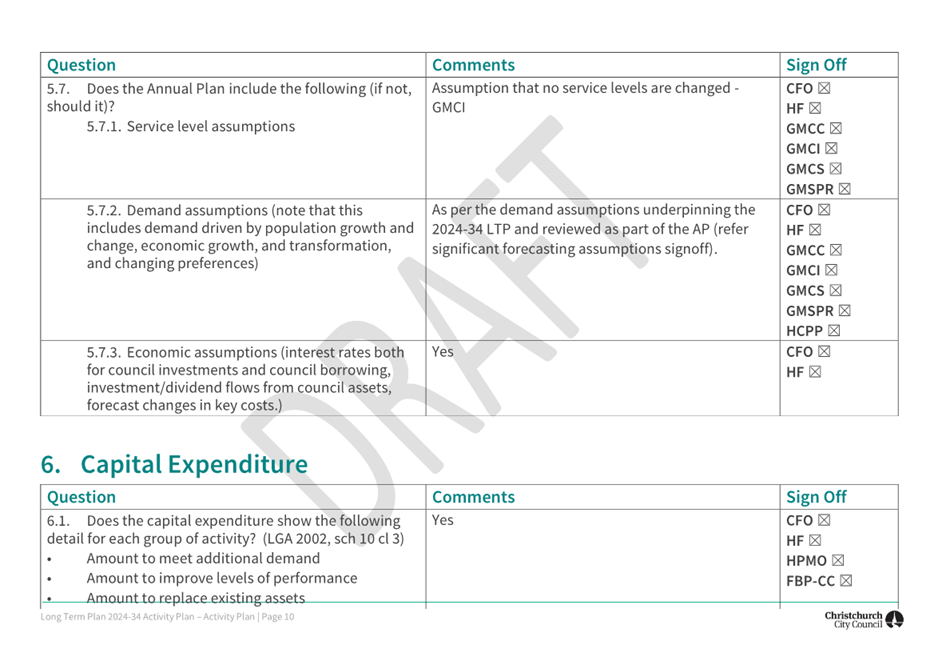

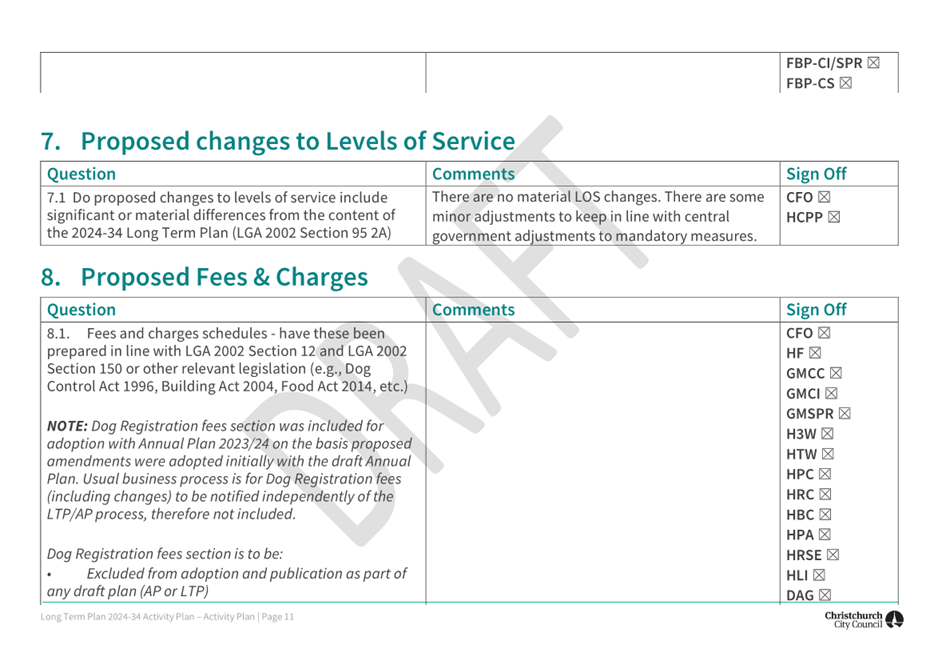

report (refer Attachments A and B).

3.11 Current

drafts of Council’s Annual Plan adoption documents are in Attachment C

(to be under separate cover and public-excluded until the Draft Annual Plan

2025/26 agenda to Council is released).

3.12 Staff

do not anticipate any significant or material changes between the release of

the ARMC agenda and attachments for this meeting of 10 February and the release

of the Council Annual Plan agenda for their meeting of 12 February 2025.

3.13 Council

will meet to consider and adopt the Draft Annual Plan on 12 February 2025, to

be followed by community consultation. The Consultation Document is the primary

mechanism for this and will reflect the decisions made on 12 February.

3.14 Consultation

will include the traditional submissions process as well as feedback generated

on social media. There will also be the opportunity for members of the

community to present directly to Councillors. More information on the

consultation process and timings is included in the Council report.

4. Considerations Ngā Whai Whakaaro

4.1 The Council is required to prepare and adopt a Draft Annual

Plan for each financial year (s.95(1)) Local Government Act 2002).

4.2 This report supports the Council’s Long Term Plan 2024-34:

4.2.1 Activity: Performance Management and Reporting

· Level of Service: 13.1.1 Implement the Long Term

Plan and Annual Plan programme plan – ensure that critical path milestone

due dates in programme plans are met.

4.3 This

report is consistent with Council’s Plans and Policies.

4.4 This report affects all wards and Community Board areas.

4.5 There

is no legal context, issue or implication relevant to this decision, other than

that which has been considered as part of the regular Annual Plan management

process and sign-offs.

4.6 Risks

have been identified and managed through the general checklists and sign-offs

by management, including significant forecasting assumptions.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Significant

Forecasting Assumptions for the Annual Plan 2025/26

|

25/179890

|

18

|

|

b ⇩

|

Management

Process Sign-offs for the Annual Plan 2025/26

|

25/179892

|

39

|

|

c

|

Draft Annual

Plan 2025/26 Report 12 February 2025 (this attachment is to be

public-excluded until after the publication of the Council Draft Annual Plan

2025/26 agenda) (Under Separate Cover) - Confidential

|

24/2254465

|

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Tim Ward -

Senior Corporate Planning & Performance Analyst

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

|

|

8. Resolution to Exclude the Public

|

Section

48, Local Government Official Information and Meetings Act 1987.

Note: The

grounds for exclusion are summarised in the following table. The full wording from

the Act can be found in section

6 or section

7, depending on the context.

I move that the public be excluded from the

following parts of the proceedings of this meeting, namely the items

listed overleaf.

Reason for passing this resolution: a good

reason to withhold exists under section 7.

Specific grounds under section 48(1) for

the passing of this resolution: Section 48(1)(a)

Note

Section 48(4) of the Local Government

Official Information and Meetings Act 1987 provides as follows:

“(4) Every resolution to exclude the

public shall be put at a time when the meeting is open to the public, and the

text of that resolution (or copies thereof):

(a) Shall

be available to any member of the public who is present; and

(b) Shall

form part of the minutes of the local authority.”

This resolution is made in reliance on

Section 48(1)(a) of the Local Government Official Information and Meetings Act

1987 and the particular interest or interests protected by Section 6 or Section

7 of that Act which would be prejudiced by the holding of the whole or relevant

part of the proceedings of the meeting in public are as follows:

|

ITEM NO.

|

GENERAL SUBJECT OF EACH MATTER TO BE CONSIDERED

|

SECTION

|

SUBCLAUSE AND REASON UNDER THE ACT

|

PUBLIC INTEREST CONSIDERATION

|

Potential Release Review Date and

Conditions

|

|

7.

|

Consideration of the Council's Draft Annual Plan 2025/26

|

|

|

|

|

|

|

Attachment c - Draft Annual Plan 2025/26

Report 12 February 2025 (this attachment is to be public-excluded until after

the publication of the Council Draft Annual Plan 2025/26 agenda)

|

s7(2)(b)(ii)

|

Prejudice Commercial Position

|

The information in the current draft version of the Council's

Annual Plan remains subject to change. Premature release of this information

could prejudice those people and entities that may be affected by any changes

made which would not be in the public interest.

|

12 February 2025

The Draft Annual Plan will be published in the Council Agenda for

its meeting commencing 12 February 2025.

|

|

9.

|

Public Excluded Audit and Risk Management

Committee Minutes - 6 December 2024

|

|

|

Refer to the previous public excluded reason in the agendas for

these meetings.

|

|

|

10.

|

Cyber Security Report

|

s7(2)(c)(i)

|

Protection of Source of Information

|

Disclosure of our approach to cyber security will increase the

risk of Council being a target, resulting in potential service disruptions

and / or information breaches that will not be in the public interest.

|

30 March 2026

This report may only be released if the Chief Executive Officer

has determined that there are no longer any reasons under the Local

Government Official Information and Meeting Act to withhold the information.

|

|

11.

|

Insurance update

|

s7(2)(b)(ii), s7(2)(h), s7(2)(i)

|

Prejudice Commercial Position, Commercial Activities, Conduct

Negotiations

|

Council's insurance strategy must remain confidential in order to

protect our position when undertaking annual policy renewals. Release of this

information would put Council at a disadvantage when seeking insurance cover

at a reasonable cost And will not be in the public interest.

|

30 June 2027

This report may be released after the end of the 2026/27 cover

year, however specific details around financials and terms must remain

confidential.

|

|

12.

|

Parakiore

|

s7(2)(i)

|

Conduct Negotiations

|

The report contains specific information pertaining to ongoing

negotiations between Council and external parties and putting the information

in the public domain could compromise the negotiations and will not be in the

public interest.

|

31 December 2026

With the approval of the Chief Executive at the conclusion of the

defect liability period for Parakiore Recreation and Sports Centre

|

|

13.

|

Risk and Assurance Quarterly Update

|

s7(2)(a), s7(2)(e)

|

Protection of Privacy of Natural Persons, Prevention of Material

Loss

|

Disclosure of the Council’s approach to remedial actions

could result in service disruptions and or / the breach the privacy of

natural persons which outweighs the public interest.

|

1 August 2025

Once the remedial actions have been implemented and appropriate

redactions have been made which protect the privacy of individuals.

|

|

14.

|

Audit Management Report 2024

|

s7(2)(c)(i)

|

Protection of Source of Information

|

Disclosing the information in this report will unreasonably expose

information on the Christchurch City Council’s internal systems and

could compromise the supply of similar information and it is in the public

interest that this information continues to be supplied.

|

10 February 2026

After the conclusion of the review of CCC internal systems.

|