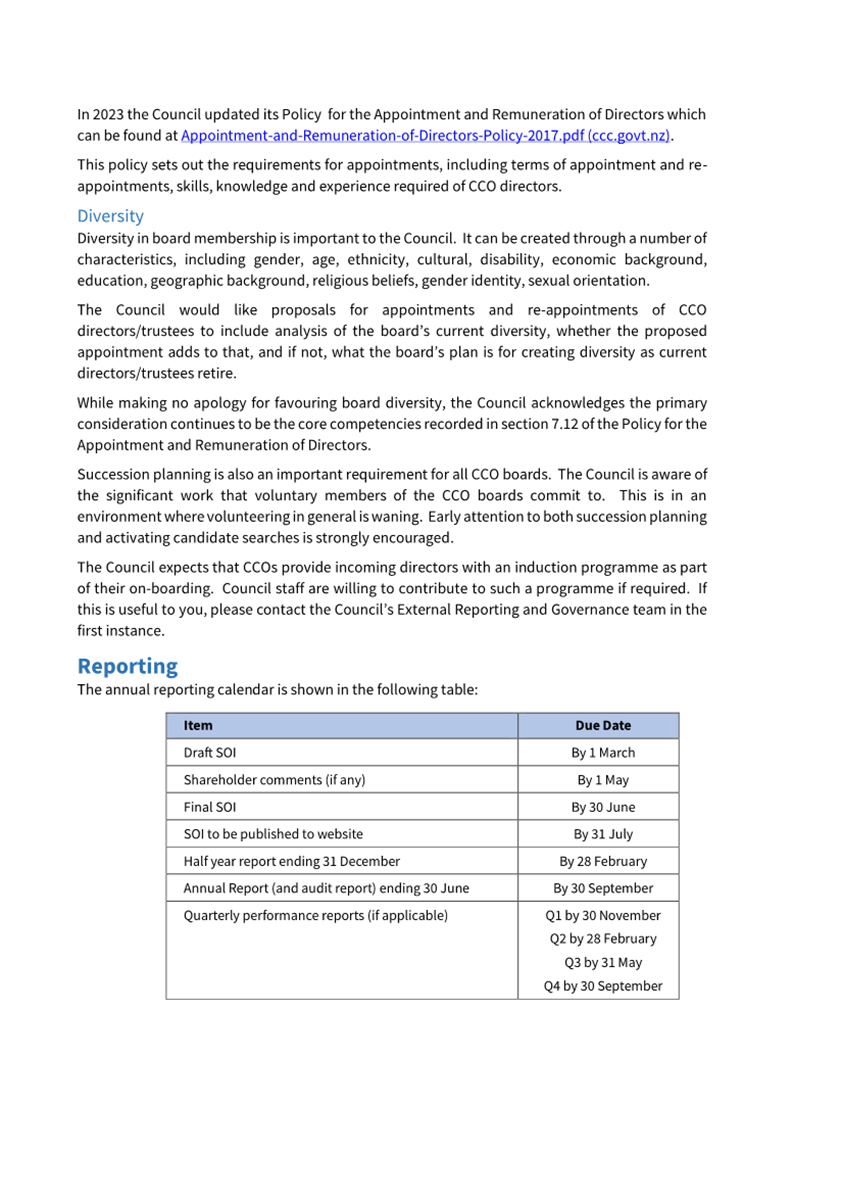

Finance and Performance Committee

Agenda

Notice of Meeting:

An ordinary meeting of the Finance &

Performance Committee will be held on:

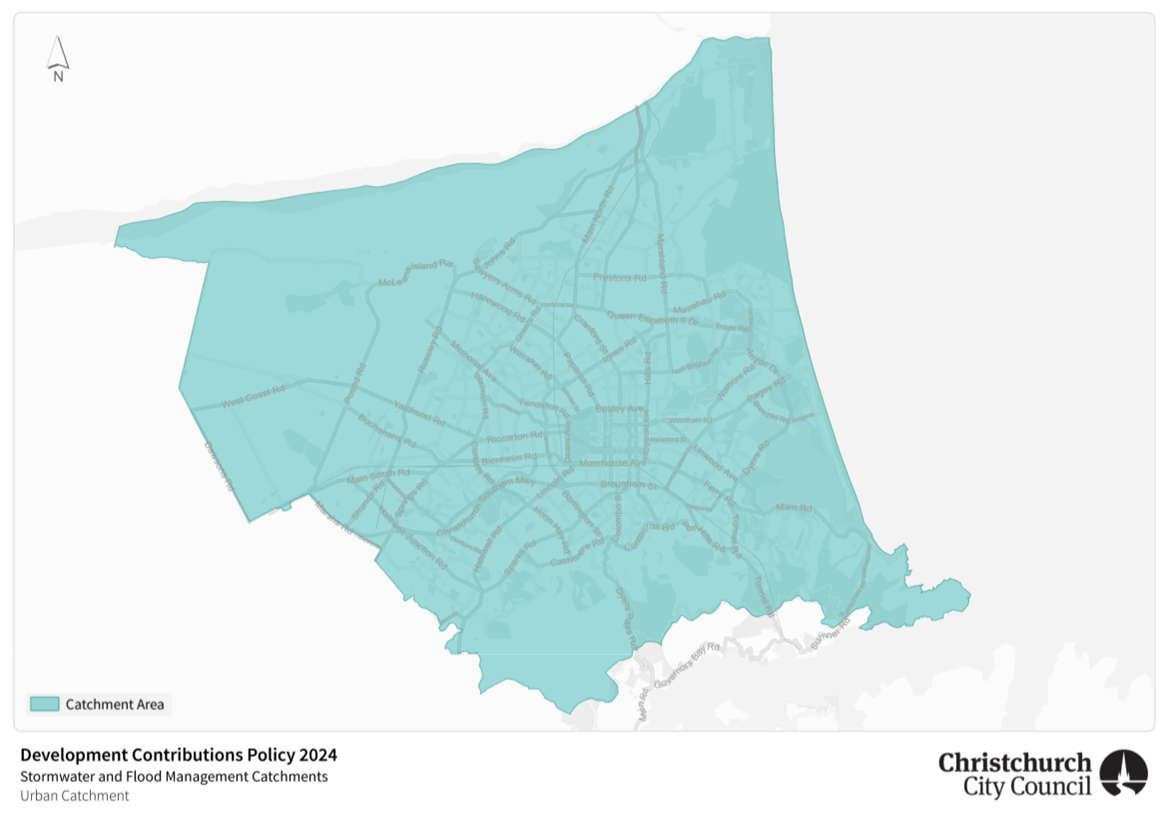

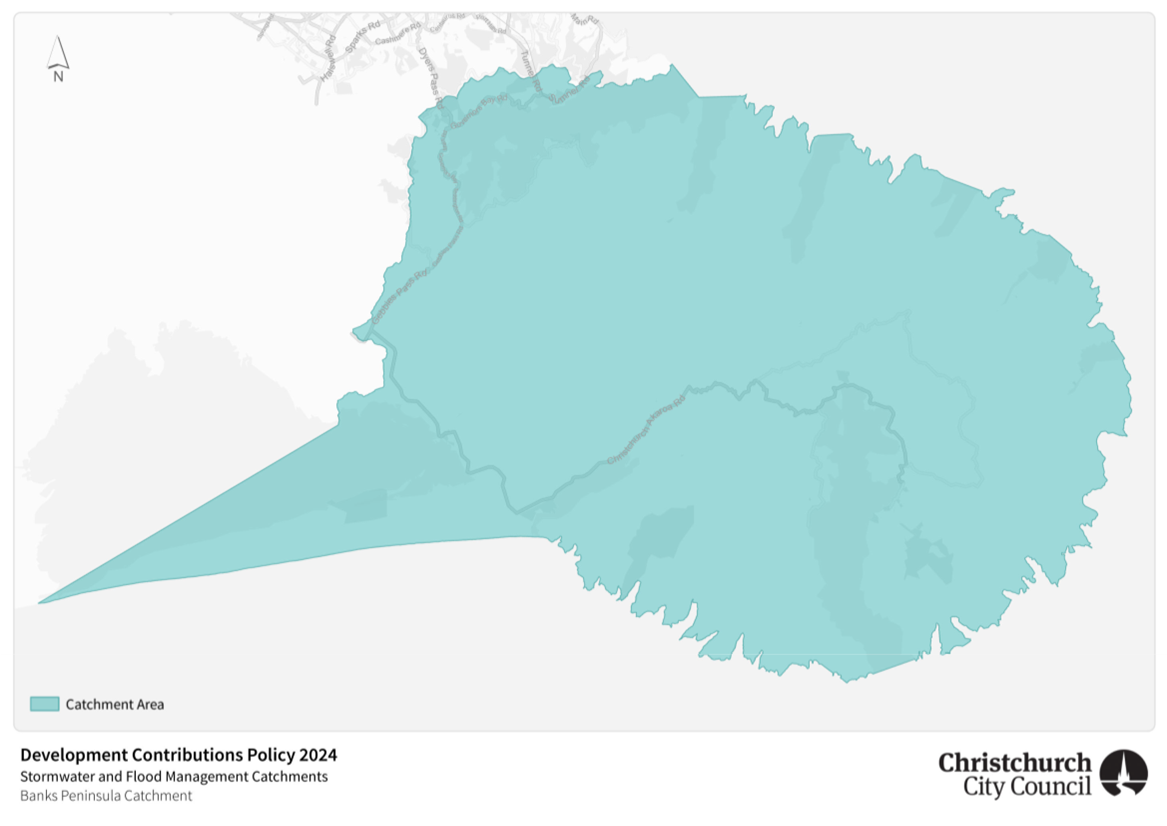

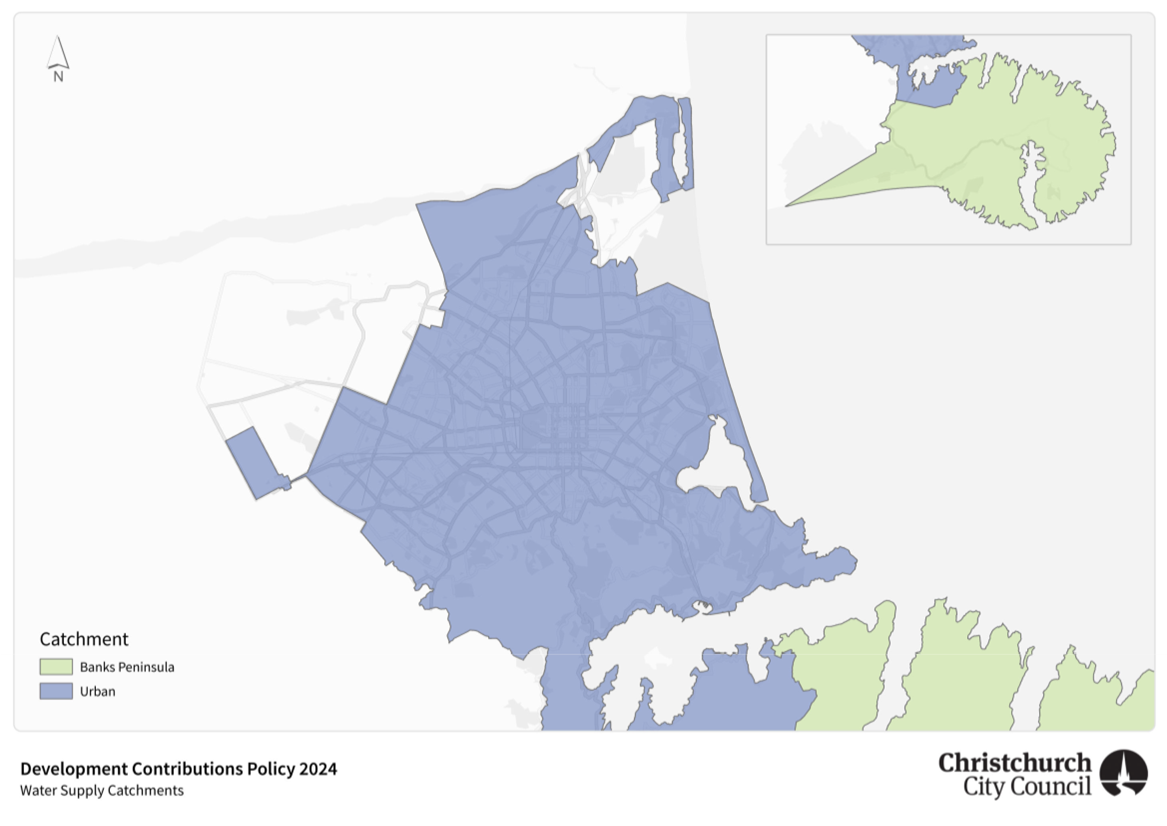

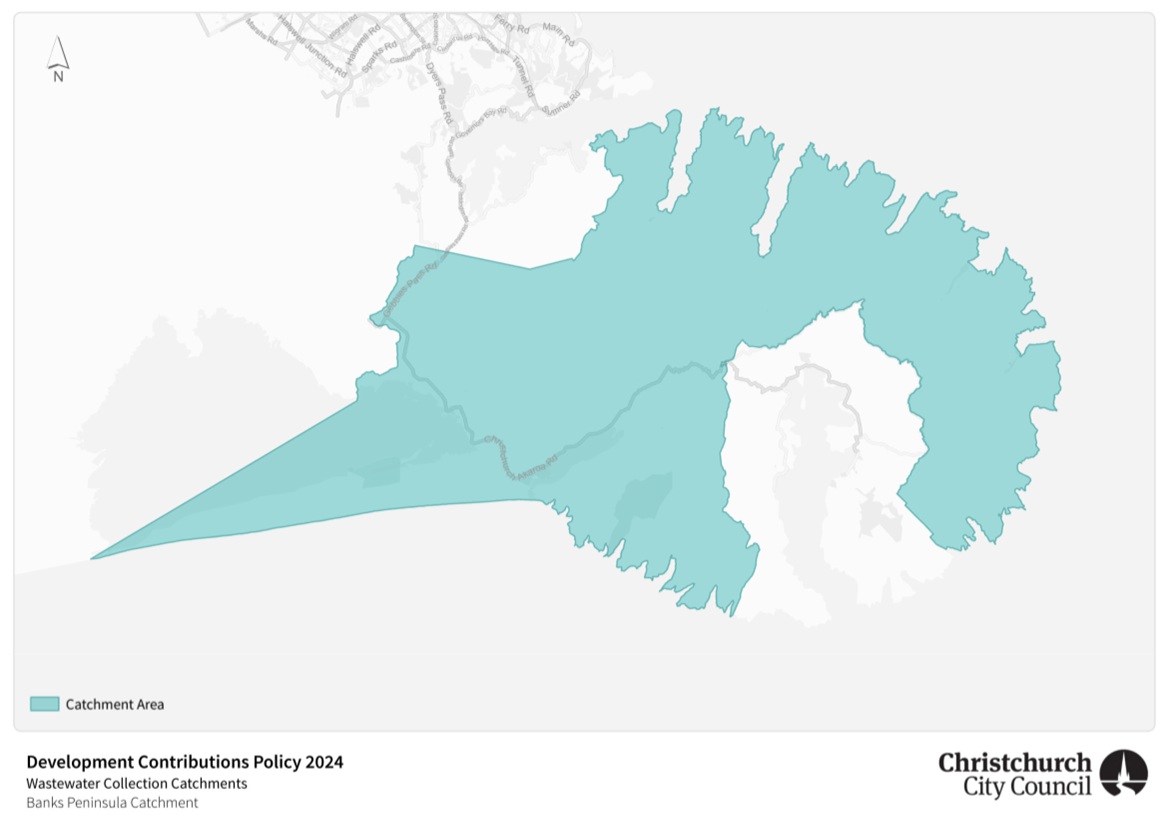

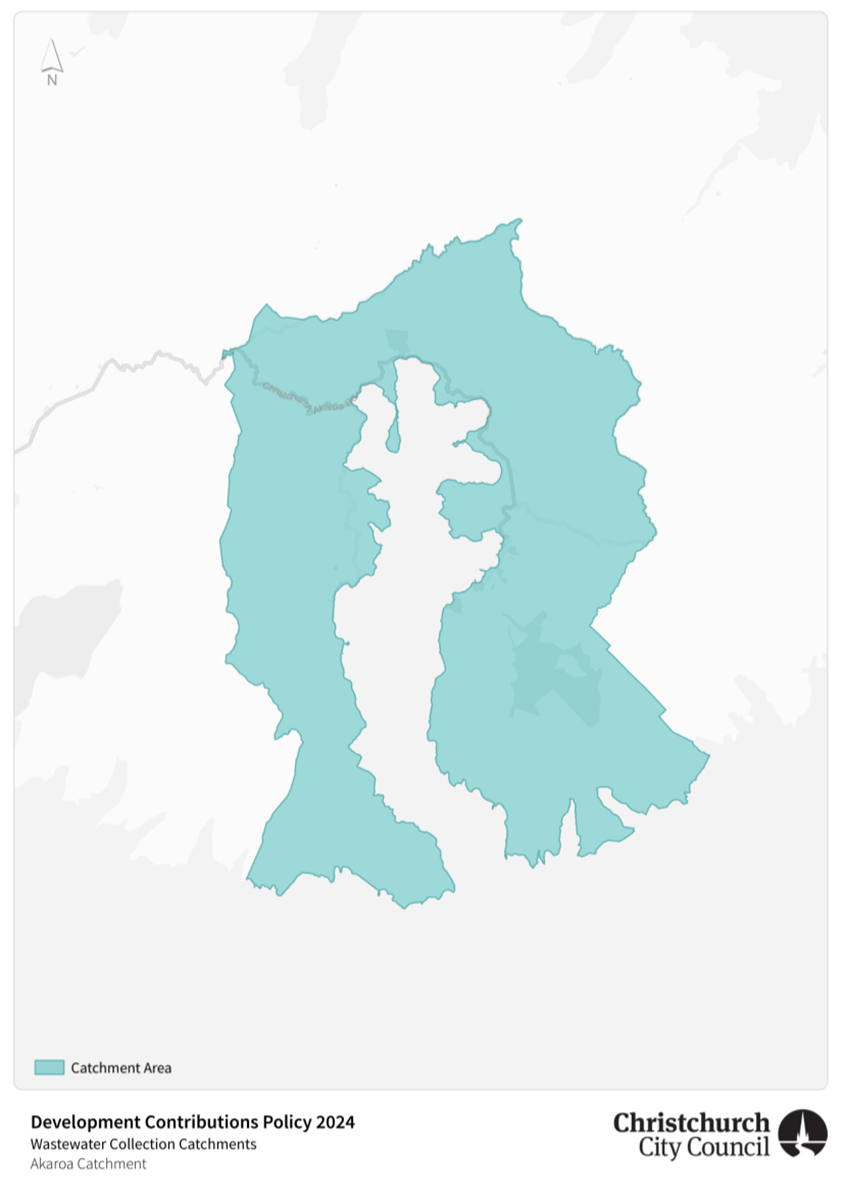

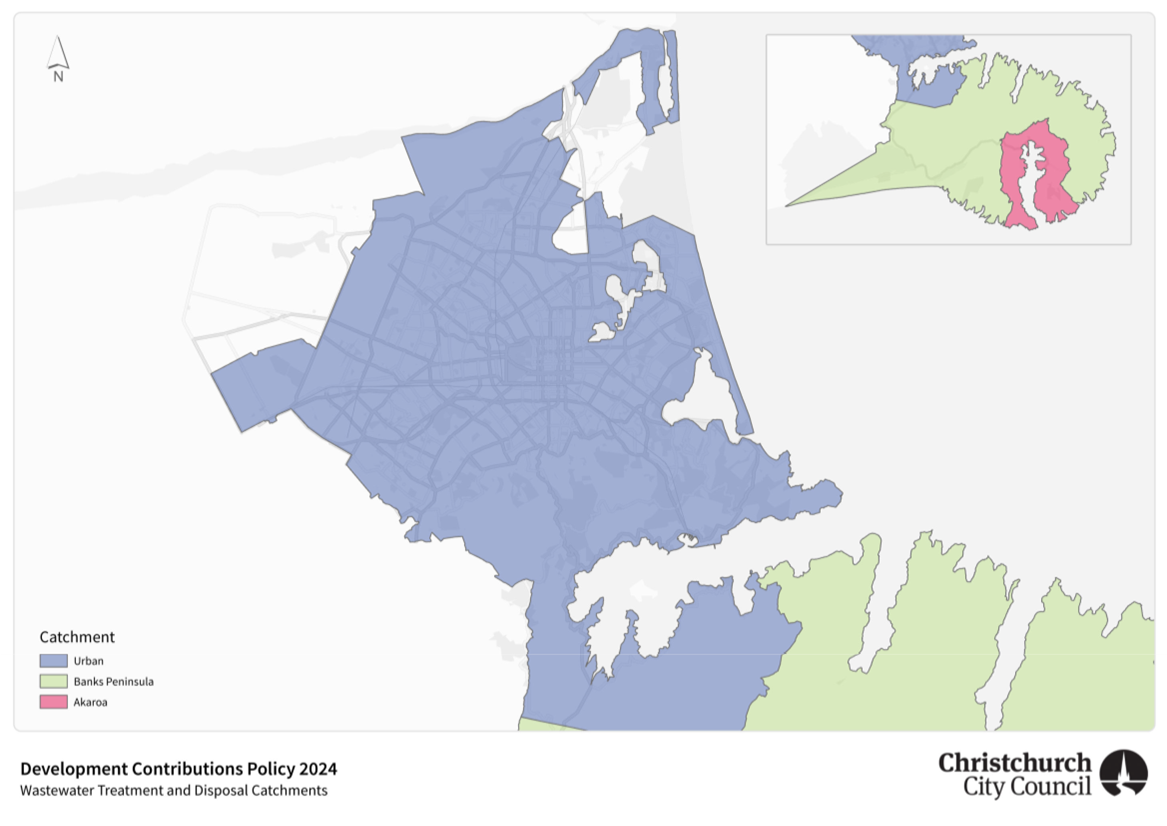

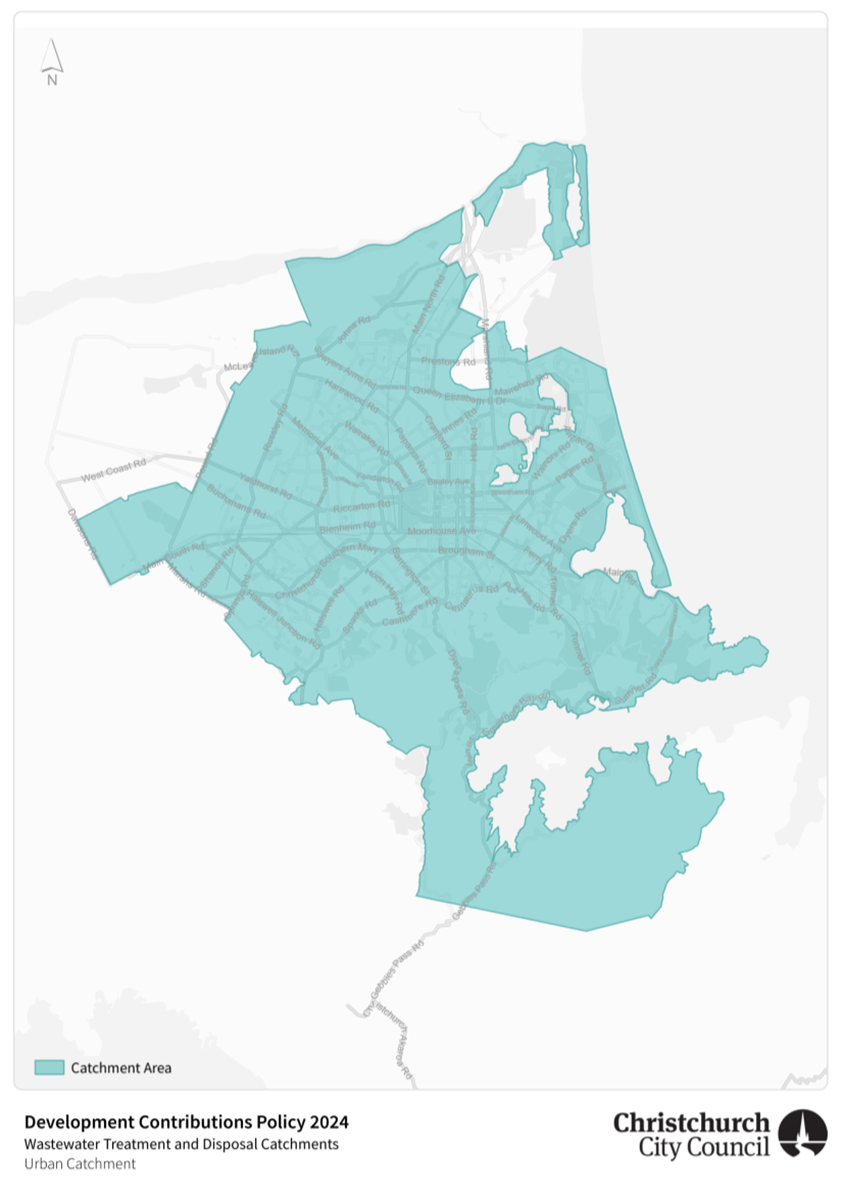

Date: Wednesday 18 December 2024

Time: 9.30 am

Venue: Council Chambers, Civic Offices,

53 Hereford Street, Christchurch

Membership

|

Chairperson

Deputy Chairperson

Members

|

Councillor Sam MacDonald

Councillor Melanie Coker

Mayor Phil Mauger

Deputy Mayor Pauline Cotter

Councillor Kelly Barber

Councillor Celeste Donovan

Councillor Tyrone Fields

Councillor James Gough

Councillor Tyla Harrison-Hunt

Councillor Victoria Henstock

Councillor Yani Johanson

Councillor Aaron Keown

Councillor Jake McLellan

Councillor Andrei Moore

Councillor Mark Peters

Councillor Tim Scandrett

Councillor Sara Templeton

|

12 December 2024

Website: www.ccc.govt.nz

Finance and Performance

Committee of the whole - Terms of Reference Ngā

Ārahina Mahinga

|

Chair

|

Councillor MacDonald

|

|

Deputy Chair

|

Councillor Coker

|

|

Membership

|

The Mayor and all Councillors

|

|

Quorum

|

Half of the members if the

number of members (including vacancies) is even, or a majority of members if

the number of members (including vacancies) is odd

|

|

Meeting Cycle

|

Monthly

|

|

Reports To

|

Council

|

Delegations

The Council delegates to the Finance and Performance

Committee authority to oversee and make decisions on:

Capital Programme and operational

expenditure

·

Monitoring the delivery of the Council’s

Capital Programme and associated operational expenditure, including inquiring

into any material discrepancies from planned expenditure.

·

As may be necessary from time to time, approving

amendments to the Capital Programme outside the Long-Term Plan or Annual Plan

processes.

·

Approving Capital Programme business and

investment cases, and any associated operational expenditure, as agreed in the

Council’s Long-Term Plan.

·

Approving any capital or other carry forward

requests and the use of operating surpluses as the case may be.

·

Approving the procurement plans (where

applicable), preferred supplier, and contracts for all capital expenditure

where the value of the contract exceeds $15 Million (noting that the Committee

may sub delegate authority for approval of the preferred supplier and /or

contract to the Chief Executive provided the procurement plan strategy is

followed).

·

Approving the procurement plans (where

applicable), preferred supplier, and contracts, for all operational expenditure

where the value of the contract exceeds $10 Million (noting that the Committee

may sub delegate authority for approval of the preferred supplier and/or

contract to the Chief Executive provided the procurement plan strategy is

followed).

Non-financial performance

·

Reviewing the delivery of services under s17A.

·

Amending levels of service targets, unless the

decision is precluded under section 97 of the Local Government Act 2002.

·

Exercising all of the Council's powers under

section 17A of the Local Government Act 2002, relating to service delivery

reviews and decisions not to undertake a review.

Council Controlled Organisations

·

Monitoring the financial and non-financial

performance of the Council and Council Controlled Organisations.

·

Making governance decisions related to Council

Controlled Organisations under sections 65 to 72 of the Local Government Act

2002.

·

Exercising the Council’s powers directly

as the shareholder, or through CCHL, or in respect of an entity (within the

meaning of section 6(1) of the Local Government Act 2002) in relation to

–

o

(without limitation) the

modification of constitutions and/or trust deeds, and other governance

arrangements, granting shareholder approval of major transactions, appointing

directors or trustees, and approving policies related to Council Controlled

Organisations; and

o

in relation to the approval of Statements of

Intent and their modification (if any).

Development Contributions

·

Exercising all of the Council's powers in

relation to development contributions, other than those delegated to the Chief

Executive and Council officers as set out in the Council's Delegations

Register.

Property

·

Purchasing or disposing of property where

required for the delivery of the Capital Programme, in accordance with the

Council’s Long-Term Plan, and where those acquisitions or disposals have

not been delegated to another decision-making body of the Council or staff.

Loans and debt write-offs

·

Approving debt write-offs where those debt

write-offs are not delegated to staff.

·

Approving amendments to loans, in accordance

with the Council’s Long-Term Plan.

Insurance

·

All insurance matters, including considering

legal advice from the Council’s legal and other advisers, approving

further actions relating to the issues, and authorising the taking of formal

actions (Sub-delegated to the Insurance Subcommittee as per the Subcommittees

Terms of Reference)

Annual Plan and Long Term Plan

·

Provides oversight and monitors development of

the Long Term Plan (LTP) and Annual Plan.

·

Approves the appointment of the Chairperson and

Deputy Chairperson of the External Advisory Group for the LTP 2021-31.

Submissions

·

The Council delegates to the Committee

authority:

·

To consider and approve draft submissions on

behalf of the Council on topics within its terms of reference. Where the timing

of a consultation does not allow for consideration of a draft submission by the

Council or relevant Committee, that the draft submission can be considered and

approved on behalf of the Council.

Limitations

·

The general delegations to this Committee

exclude any specific decision-making powers that are delegated to a Community

Board, another Committee of Council or Joint Committee. Delegations to staff

are set out in the delegations register.

·

The Council retains the authority to adopt policies, strategies

and bylaws.

The following matters

are prohibited from being subdelegated in accordance with LGA 2002 Schedule 7

Clause 32(1) :

·

the power to make a rate; or

·

the power to make a bylaw; or

·

the power to borrow money, or purchase or

dispose of assets, other than in accordance with the long-term plan; or

·

the power to adopt a long-term plan, annual

plan, or annual report; or

·

the power to appoint a chief executive; or

·

the power to adopt policies required to be

adopted and consulted on under this Act in association with the long-term plan

or developed for the purpose of the local governance statement; or

·

the power to adopt a remuneration and employment

policy.

Chairperson

may refer urgent matters to the Council

As may be necessary from

time to time, the Committee Chairperson is authorised to refer urgent matters

to the Council for decision, where this Committee would ordinarily have

considered the matter. In order to

exercise this authority:

·

The Committee Advisor must inform the

Chairperson in writing the reasons why the referral is necessary

·

The Chairperson must then respond to the

Committee Advisor in writing with their decision.

·

If the Chairperson agrees to refer the report to

the Council, the Council may then assume decision making authority for that

specific report.

Urgent matters referred from the Council

As may be necessary

from time to time, the Mayor is authorised to refer urgent matters to this

Committee for decision, where the Council would ordinarily have considered the

matter, except for those matters listed in the limitations above.

In order to

exercise this authority:

·

The Council Secretary must inform the Mayor and

Chief Executive in writing the reasons why the referral is necessary

·

The Mayor and Chief Executive must then respond

to the Council Secretary in writing with their decision.

If the Mayor

and Chief Executive agrees to refer the report to the Committee, the Committee

may then assume decision-making authority for that specific report.

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

TABLE OF CONTENTS NGĀ IHIRANGI

Karakia Tīmatanga..................................................................................... 7

C 1. Apologies Ngā Whakapāha........................................................... 7

B 2. Declarations of Interest Ngā Whakapuaki Aronga.......................... 7

C 3. Confirmation of Previous Minutes Te Whakaāe o te

hui o mua........ 7

B 4. Public Forum Te Huinga Whānui................................................... 7

B 5. Deputations by Appointment Ngā Huinga

Whakaritenga................ 7

B 6. Presentation

of Petitions Ngā

Pākikitanga.................................... 7

Staff Reports

B 7. Key

Organisational Performance Results - November 2024... 19

B 8. Financial

Performance Report - November 2024.................. 69

B 9. Capital

Programme Performance Report November 2024..... 73

C 10. Draft

Development Contributions Policy 2024................... 109

C 11. Climate

Resilience Fund: Policy........................................ 311

C 12. ChristchurchNZ

Holdings Ltd - Draft Letter of Expectations 2025/26.......................................................................... 333

B 13. Venues Otautahi

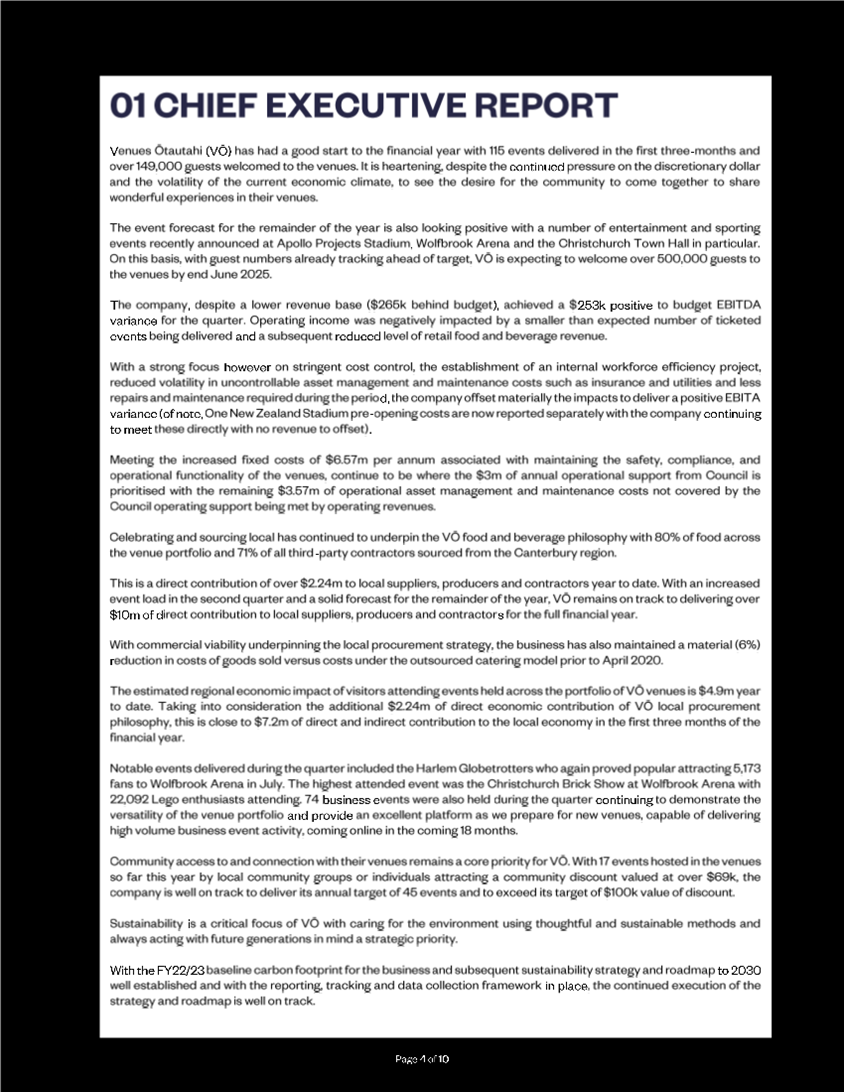

- Quarter 1 2024/25 Performance Report.. 357

C 14. Venues

Ōtautahi - Draft Letter of Expectations for 2025/26. 369

B 15. Christchurch

City Holdings Ltd - Quarter 1 2024/25 Performance Report........................................................ 393

C 16. Christchurch

City Holdings Ltd - Draft Letter of Expectation for 2025/26.......................................................................... 409

C 17. Resolution to

Exclude the Public...................................... 435

Karakia Whakamutunga

Karakia Tīmatanga

Whakataka te hau ki te uru

Whakataka te hau ki te tonga

Kia mākinakina ki uta

Kia mātaratara ki tai

E hī ake ana te atakura

He tio, he huka, he hau hū

Tihei mauri ora

1. Apologies Ngā Whakapāha

Apologies will

be recorded at the meeting.

2. Declarations of Interest Ngā

Whakapuaki Aronga

Members are

reminded of the need to be vigilant and to stand aside from decision-making

when a conflict arises between their role as an elected representative and any

private or other external interest they might have.

3. Confirmation of Previous Minutes Te

Whakaāe o te hui o mua

That the

minutes of the Finance and Performance Committee meeting held on Wednesday, 27 November 2024 be

confirmed (refer page 8).

4. Public Forum Te Huinga Whānui

A period of up

to 30 minutes will be available for people to speak for up to five minutes on

any issue that is not the subject of a separate hearing process.

Public Forum presentations will be

recorded in the meeting minutes

5. Deputations by Appointment Ngā Huinga

Whakaritenga

Deputations may

be heard on a matter or matters covered by a report on this agenda and approved

by the Chairperson.

Deputations will

be recorded in the meeting minutes.

6. Presentation of Petitions Ngā

Pākikitanga

There were no petitions

received at the time the agenda was prepared.

I

Finance and Performance Committee

Open Minutes

Date: Wednesday 27 November 2024

Time: 9.30 am

Venue: Council Chambers, Civic Offices,

53 Hereford Street, Christchurch

Present

|

Chairperson

Deputy Chairperson

Members

|

Councillor Sam MacDonald

Councillor Melanie Coker

Mayor Phil Mauger

Deputy Mayor Pauline Cotter

Councillor Kelly Barber

Councillor Celeste Donovan

Councillor Tyrone Fields

Councillor James Gough

Councillor Tyla Harrison-Hunt

Councillor Victoria Henstock

Councillor Yani Johanson

Councillor Aaron Keown

Councillor Jake McLellan

Councillor Andrei Moore

Councillor Mark Peters

Councillor Tim Scandrett

Councillor Sara Templeton – via

audio/visual link

|

Website: www.ccc.govt.nz

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

Karakia Tīmatanga

The agenda was dealt with in the following

order.

1. Apologies

Ngā Whakapāha

Part C

|

Committee Resolved FPCO/2024/00066

That the apologies from The Mayor and

Councillor Gough for lateness, and Deputy Mayor Cotter for partial absence,

be accepted.

Councillor

Coker/Councillor MacDonald Carried

|

2. Declarations

of Interest Ngā Whakapuaki Aronga

Part B

Councillors Henstock and McLellan declared an interest in

Item 11 – ChristchurchNZ

Holdings Ltd – Annual Report 2023/24 and Quarter 1 Performance Report

2024/25.

Councillors

McLellan, Gough and MacDonald (Civic Building Ltd), Peters (Riccarton Bush

Trust), and Fields (Rod Donald Banks Peninsula Trust) declared an interested in

Item 12 - Council-controlled Organisations - Annual Reports 2023/24.

Councillors

McLellan, Gough and MacDonald (Civic Building Ltd), and Barber and Scandrett

(Venues Ōtautahi) declared an interest in Item 13 - Council-controlled

Organisations - Annual General Meetings by Written Shareholder Resolutions.

3. Confirmation

of Previous Minutes Te Whakaāe o te hui o mua

Part C

|

Committee Resolved FPCO/2024/00067

That the

minutes of the Finance and Performance Committee meeting held on Wednesday,

23 October 2024 be confirmed.

Councillor

MacDonald/Councillor Peters Carried

|

Councillors Johanson and McLellan joined

the meeting at 9.33 am during consideration of Item 4.1.1.

4. Public

Forum Te Huinga Whānui

Part B

|

4.1.1 Ōtākaro

Orchard Project

|

|

Hayley Guglietta spoke and

provided a presentation to provide a financial update to the Ōtākaro

Orchard Project.

|

|

|

|

Attachments

a Ōtākaro

Orchard Project - Presentation to Council

|

5. Deputations

by Appointment Ngā Huinga Whakaritenga

Part B

There were no deputations by appointment.

6. Presentation

of Petitions Ngā Pākikitanga

Part B

There was no presentation of petitions.

Councillor Templeton joined the meeting via

audio/visual link at 9.39 am during consideration of Item 7.

|

8. Financial

Performance Report - October 2024

|

|

|

Committee Resolved FPCO/2024/00069

Officer Recommendations accepted without

change

Part C

That the Finance

and Performance Committee:

1. Receives the information in the Financial

Performance Report - October 2024 Report.

2. Confirms that the Treasury section of the Financial Performance

Report, which covers policy compliance, borrowing and advances to related

parties, funding requirements and interest rates will be reported quarterly

other than if there is a breach or likely breach of Council’s Liability Management Policy and/or Investment Policy in which case

it will be included in the next Financial Performance

Report.

Councillor

Scandrett/Councillor Harrison-Hunt Carried

|

Councillor Keown left the meeting at 10.09

am and returned at 10.11 am during consideration of Item 9.

Councillor Barber left the meeting at 10.17

am during consideration of Item 9.

Councillor Gough joined the meeting at

10.21 am during consideration of Item 10.

The Mayor joined the meeting at 10.23 am

during consideration of Item 10.

Councillor Barber returned to the meeting

at 10.24 am during consideration of Item 10.

|

10. Advice on

the Infrastructure Working Group

|

|

|

Officer Recommendations Ngā

Tūtohu

That the

Finance and Performance Committee:

1. Receives the information in the Advice on the Infrastructure

Working Group report.

2. Agrees to establish an Infrastructure Working Group reporting to

the Finance & Performance Committee for matters relating to

infrastructure project delivery.

3. Notes that the Infrastructure Working Group will be governed by

the Terms of Reference (ToR) in Attachment A to this report.

4. Agrees that the membership of the Infrastructure Working Group

will consist of the following elected members:

a. Chairperson [insert name]

b. Deputy Chairperson [insert name]

c. [insert name]

d. [insert name]

e. [insert name]

f. [insert name]

5. Notes that the decision in this report is of low significance in

relation to the Christchurch City Council’s Significance and Engagement

Policy.

|

|

|

Committee Resolved FPCO/2024/00071

Part C

That the

Finance and Performance Committee:

1. Receives the information in the Advice on the Infrastructure

Working Group report.

2. Agrees to establish an Infrastructure Working Group reporting to

the Finance & Performance Committee for matters relating to

infrastructure project delivery.

3. Notes that the Infrastructure Working Group will be governed by

the Terms of Reference (ToR) in Attachment A to this report.

5. Notes that the decision in this report is of low significance in

relation to the Christchurch City Council’s Significance and Engagement

Policy.

Deputy

Mayor/Councillor MacDonald Carried

|

|

|

Committee Resolved FPCO/2024/00072

4. Agrees that the membership of the Infrastructure Working Group

will consist of the following elected members:

a. Chairperson Councillor Keown

b. Deputy Chairperson Councillor Coker

c. The Mayor

The division was declared carried

by 10 votes to 7 votes the voting being as follows:

For: Councillor MacDonald, Mayor Mauger, Deputy Mayor Cotter,

Councillor Barber, Councillor Gough, Councillor Henstock, Councillor Keown,

Councillor Moore, Councillor Peters and Councillor Scandrett

Against: Councillor Coker, Councillor Donovan, Councillor Fields,

Councillor Harrison-Hunt, Councillor Johanson, Councillor McLellan and

Councillor Templeton

Deputy Mayor/Councillor

MacDonald Carried

|

Councillor Templeton left the meeting at

10.31 am during consideration of Item 11 and did not return.

Councillor Cotter left the meeting at 10.32

am during consideration of Item 11.

Councillor Gough left the meeting at 10.56

am and returned at 10.59 am during consideration of Item 11.

|

11. ChristchurchNZ

Holdings Ltd - Annual Report 2023/24 and Quarter 1 Performance Report 2024/25

|

|

|

The Mayor spoke to acknowledge the retirement of Dr.

Therese Arseneau from the ChristchurchNZ Board and expressed gratitude for

the significant contributions she has made to Christchurch during her 8 years

of service as Chair of ChristchurchNZ.

|

|

|

Officer Recommendations Ngā

Tūtohu

That the Finance

and Performance Committee:

1. Receives ChristchurchNZ Holdings Ltd’s Annual Report for

2023/24;

2. Receives ChristchurchNZ Holdings Ltd’s Quarter 1 2024/25

Performance Report; and

3. Notes that the Chair of ChristchurchNZ Holdings Ltd is to retire

from the board at ChristchurchNZ Holdings Ltd’s Annual General Meeting

on 28 November 2024.

|

|

|

Committee Resolved FPCO/2024/00073

Part C

That the Finance

and Performance Committee:

1. Receives ChristchurchNZ Holdings Ltd’s Annual Report for

2023/24;

2. Receives ChristchurchNZ Holdings Ltd’s Quarter 1 2024/25

Performance Report; and

3. Notes that the Chair of ChristchurchNZ Holdings Ltd is to retire

from the board at ChristchurchNZ Holdings Ltd’s Annual General Meeting

on 28 November 2024 and records with appreciation Dr Therese Arseneau’s

contribution.

Mayor/Councillor

Coker Carried

Councillors

Henstock and McLellan declared an interest in Item 11 and took no part

in the debate or voting on the matter.

|

|

|

Attachments

a ChristchurchNZ

Holdings Ltd - Presentation to Council

|

The meeting adjourned at 11.09 am and

reconvened at 11.26 am. The Mayor, Deputy Mayor, and Councillors Barber,

Fields and Gough were not present at this time.

Councillor Coker assumed the Chair for

consideration of Items 12, 13 and 14.

The Mayor and Councillor Barber returned to

the meeting at 11.26 am during consideration of Item 12.

|

12. Council-controlled

Organisations - Annual Reports 2023/24

|

|

|

Officer Recommendations Ngā

Tūtohu

That the Finance

and Performance Committee:

1. Receives the Annual Reports for the year ending 30 June 2024 for the following Council-controlled organisations:

a. Civic Building Ltd;

b. Riccarton Bush Trust;

c. Rod Donald Banks Peninsula Trust; and

d. Te Kaha Project Delivery Ltd.

2. Receives the Half Year Report to 30 June 2024 for Civic Financial

Services.

|

|

|

Committee Resolved FPCO/2024/00074

Part C

That the Finance

and Performance Committee:

1. Receives the Annual Reports for the year ending 30 June 2024 for

the following Council-controlled organisations:

a. Civic Building Ltd;

b. Riccarton Bush Trust;

c. Rod Donald Banks Peninsula Trust; and

d. Te Kaha Project Delivery Ltd.

2. Receives the Half Year Report to 30 June 2024 for Civic Financial

Services.

Councillor

Scandrett/Councillor Donovan Carried

Councillors

Gough, MacDonald, McLellan and Peters declared an interested in Item 12 and took no part in the debate or voting on the matter. Councillor

Fields declared an interest in Item 12 and was not present at the time this

Item was discussed.

|

Councillor Fields returned to the meeting

at 11.28 am during consideration of Item 13.

Councillor Gough returned to the meeting at

11.29 am during consideration of Item 13.

|

13. Council-controlled

Organisations - Annual General Meetings by Written Shareholder Resolutions

|

|

|

Officer Recommendations Ngā

Tūtohu

That the

Finance and Performance Committee:

1. Agrees to pass shareholder resolutions for the 2024 annual

meetings of the following Council-controlled organisations:

a. non-trading ‘shelf’ companies - CCC One Ltd, CCC Five

Ltd, CCC Seven Ltd and Ellerslie International Flower Show Ltd; and

b. trading companies – Civic Building Ltd, Te Kaha Project

Delivery Ltd and Venues Ōtautahi; and

2. Notes that the decisions in this report are assessed as low

significance based on the Christchurch City Council’s Significance and

Engagement Policy.

|

|

|

Committee Resolved FPCO/2024/00075

Part C

That the

Finance and Performance Committee:

1. Agrees to pass shareholder resolutions for the 2024 annual

meetings of the following Council-controlled organisations:

a. non-trading ‘shelf’ companies - CCC One Ltd, CCC Five Ltd,

CCC Seven Ltd and Ellerslie International Flower Show Ltd; and

b. trading companies – Civic Building Ltd, Te Kaha Project

Delivery Ltd and Venues Ōtautahi; and

2. Notes that the decisions in this report are assessed as low

significance based on the Christchurch City Council’s Significance and

Engagement Policy.

Councillor

Keown/Councillor Moore Carried

Councillors

Barber, Gough, MacDonald, McLellan, and Scandrett declared an interest in

Item 13 and took no part in the debate or voting on

the matter.

|

|

14. Resolution

to Exclude the Public Te whakataunga kaupare hunga tūmatanui

|

|

|

Committee Resolved FPCO/2024/00076

Part C

That at 11.31 am the resolution to exclude the public set out on

pages 359 to 360 of the agenda be adopted.

Councillor

Coker/Councillor Harrison-Hunt Carried

Councillor

Johanson requested his vote against the resolution be recorded.

|

The public were re-admitted to the meeting

at 11.54 am.

Karakia

Whakamutunga

Meeting

concluded at 11.54 am.

CONFIRMED THIS 18TH DAY

OF DECEMBER 2024

Councillor Sam MacDonald

Chairperson

|

7. Key

Organisational Performance Results - November 2024

|

|

Reference Te Tohutoro:

|

24/1957169

|

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance Peter.Ryan@ccc.govt.nz

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 To provide Council with an overview of

performance towards delivering year one of our Long-term Plan 2024-34 (LTP),

our ‘contract with the community.’

2. Officer Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Key Organisational Performance Results -

November 2024 Report.

2. Notes that the section ‘Responses to questions from Councillors’ will be included as an Appendix to the

report from the next meeting.

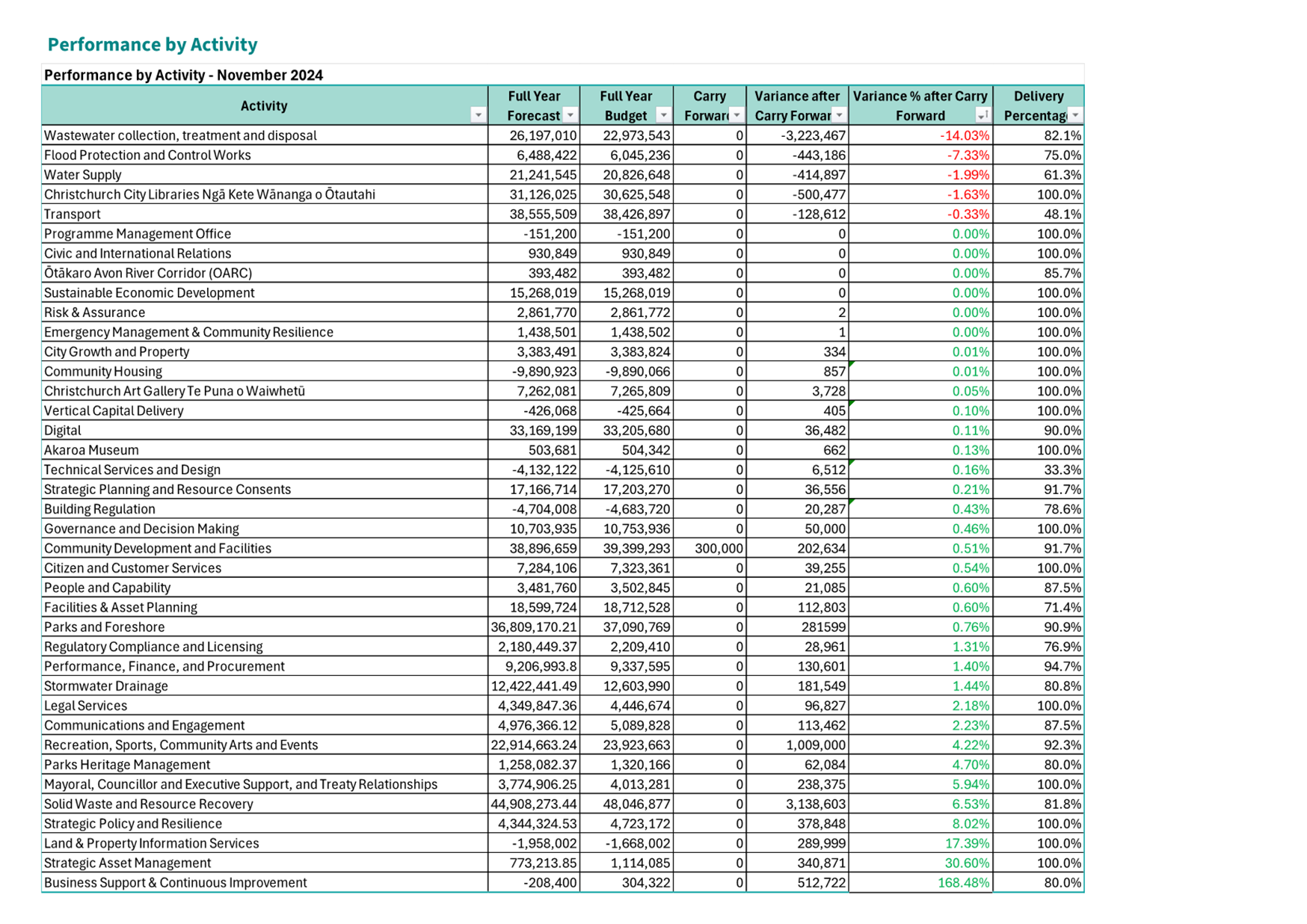

3. Background/Context Te Horopaki

3.1 This

is a regular report focused on a suite of the ‘vital few’

organisational performance targets and forms a key component of the Performance

Framework and its reporting.

3.2 Levels

of service (LOS) are now in consolidated format, which means that exceptions

are put in perspective against those performance measures that are on track.

This report, as well as all supporting activity reports, have been extensively

reworked to achieve this.

4. Considerations Ngā Whai Whakaaro

4.1 The

key organisational performance targets include:

· Service Delivery (levels

of service)

· Capital Projects (both

delivery and planning)

· Value for Money (finance

– activity budgets and capex)

4.2  This report provides November monthly

performance forecasts against ELT performance priority targets for the LTP

2024-34.

This report provides November monthly

performance forecasts against ELT performance priority targets for the LTP

2024-34.

4.3 Overall

organisational performance priority forecasts are mixed, but all retain the

ability to be achieved this financial year.

4.4 Community

Level of Service delivery (83.9%) sees a slight improvement of 0.6% from

October. Level of Service (LOS) performance remains forecast fractionally below

ELTs performance target (85%).

4.5 Management

Level of Service delivery (86.4%) sees a decline of 1.0% from October. LOS

performance remains forecast just above the ELT performance target (85%).

4.6 Due

to truncated preparation timeframes for this reporting period responses to

questions about Service Delivery exceptions from the committee meeting of 27th

November 2024 are being collated and will form part of the Key Organisational

Performance Results for December 2024 at the meeting of 29th January

2025.

4.7 Capital

Project milestone delivery (84.3%) saw a small decline of 0.5% from

October. Capital Programme milestone delivery remains fractionally below the

ELT target (85%).

4.8 Capital

planning performance forecasts each show good progress for this time of

year, against the ELT target of 90% as follows:

· Funding programme budgets

allocated for FY2026 by 31st March 2025 are currently reported at 87%.

· Budget drawdowns for

FY2027 and 2028 by 30th June 2025 are currently reported at 79%.

4.9 Activity

budgets, actively managed to budget (87.2%), saw no

percentage change from October, though there has been movement for some

individual activities. The

organisational target set by ELT is 100% of activities are actively

managed to budget.

4.10 Deliver

Capital Programme within approved budget (-$37.4M), saw a minimal movement

of -$0.1M from October. Deliver Capital Programme within approved budget

remains within the ELT target (=/< $0).

5. Service Delivery

5.1 Community

Level of Service delivery (83.9%) sees a slight

improvement of 0.6% (one LOS) from October. LOS

performance remains below the ELT performance target (85%).

5.2 Management

LOS delivery (86.4%) sees a decline of 1.0% (three

LOS) from October. LOS performance remains just above

the ELT performance target (85%).

5.3 Both

forecasts are in line with the standing Audit and Risk Management Committee

(ARMC) request for all LOS that did not meet target the previous year to

continue to be reported as an amber exception until evidence is provided the

target will or has been met. This provides for conservative forecasts at the

beginning of a financial year.

5.4 The

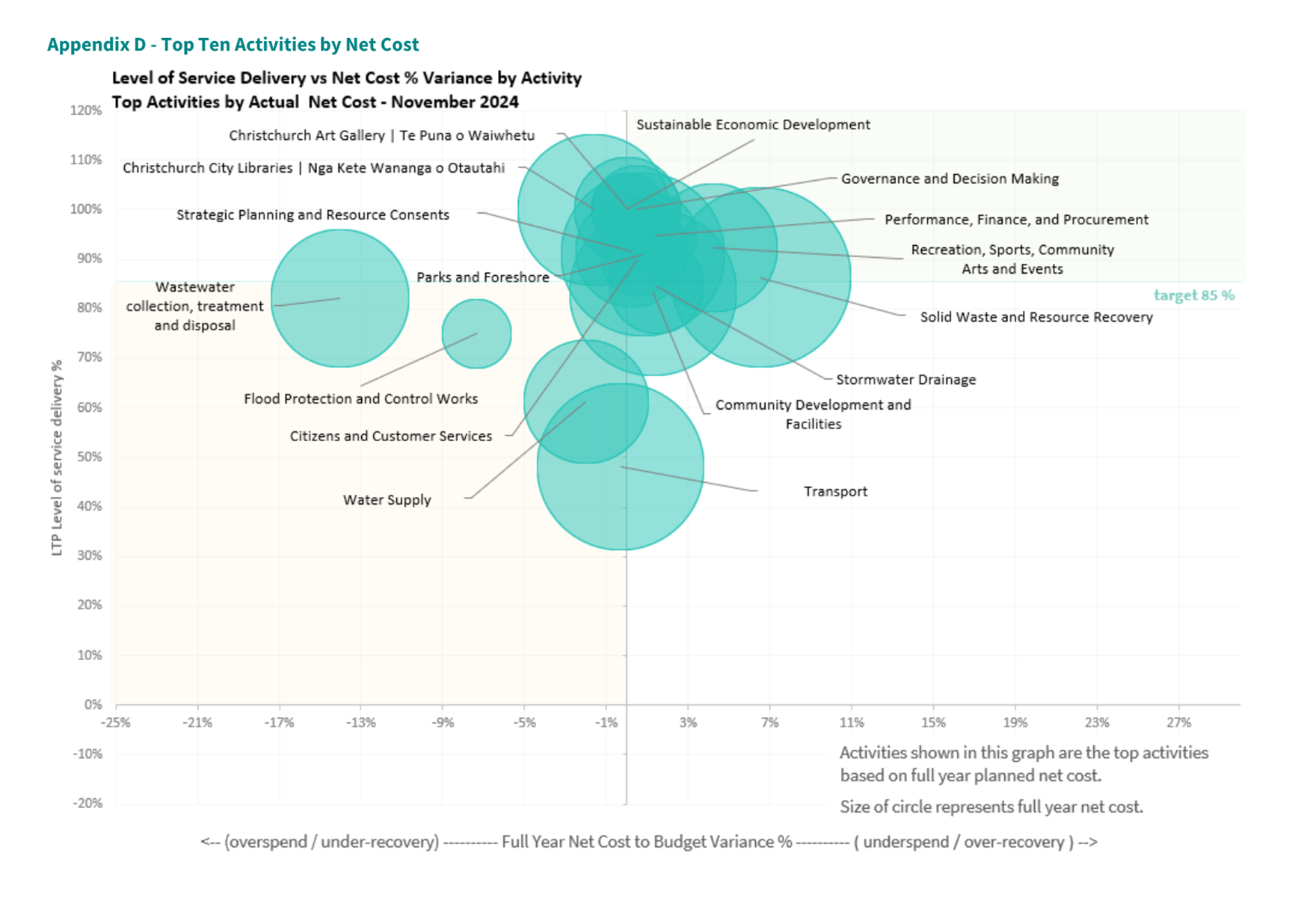

scatter-diagram below (also Attachment A) shows forecast activity LOS

delivery performance (Community and Management LOS), against forecast activity

budget performance (over- or under-spend).

· Activities variously

report level of service delivery forecasts ranging from 48.1% to 100%

achievement, while all but 5 activities are presently forecast on budget.

· The vertical y-axis shows

forecast service delivery (LOS) performance.

· The horizontal x-axis shows forecast budget over/underspend

(scaled to relative budget).

5.5 The

updated view of Service Delivery exceptions is attached to this report (Attachment

B). It is:

· a visual summary of

activity overall service delivery and activity budget performance,

· underpinned by a more

granular LOS summary across the activity, before

·  listing specific exceptions detail and business commentary.

listing specific exceptions detail and business commentary.

6. Responses to questions from Councillors

6.1 At

the committee meeting of 27 November 2024 Councillors asked questions about

several Service Delivery exceptions. The question responses are being collated

and will form part of the Key Organisational Performance Results for December

2024 at the meeting of 29 January 2025. The early in the month timing of

the meeting has made it difficult for staff to collate and then check the

responses for accuracy and completeness.

6.2 Looking

ahead it is proposed that the questions from councillors (and the responses

from staff) will form an appendix to future reports.

7. Capital Projects – Delivery and Planning

7.1 Capital

project milestone delivery performance is forecasting 84.3%, minimal

change from October (a further 0.5% decline). This remains forecast below the

ELT target of 85%.

7.2 The

capital delivery target relates to projects Council is responsible for

delivering, including Council-funded and externally funded projects.

7.3 Capital

planning performance forecasts both show good progress for this time of

year, against the ELT target of 90% as follows:

· Funding programme budgets

allocated for FY2026 by 31st March 2025 currently at 87%.

· Budget drawdowns for FY2027 and 2028 by 30th June 2025 is currently

at 79%.

7.4 For

further information and underlying project detail, refer to the Capital

Programme Performance Report.

8. Value for Money

8.1 87.2%

of activities are forecast to meet budget (nett

controllable cost, after carry-forwards), against the ELT target 100%.

34 of the 39 activities are forecast on budget.

8.2 For

more information refer to Attachments A & B and to the Financial

Performance Report.

8.3 Overall capital programme

budget expenditure is forecast at -$37.4m, against ELT’s

target of within approved budget (= < $0). This applies

a consistent PMO forecast of $510m against the current programme of $547.7m,

approx. -6.9%. The forecast includes core and externally funded work but

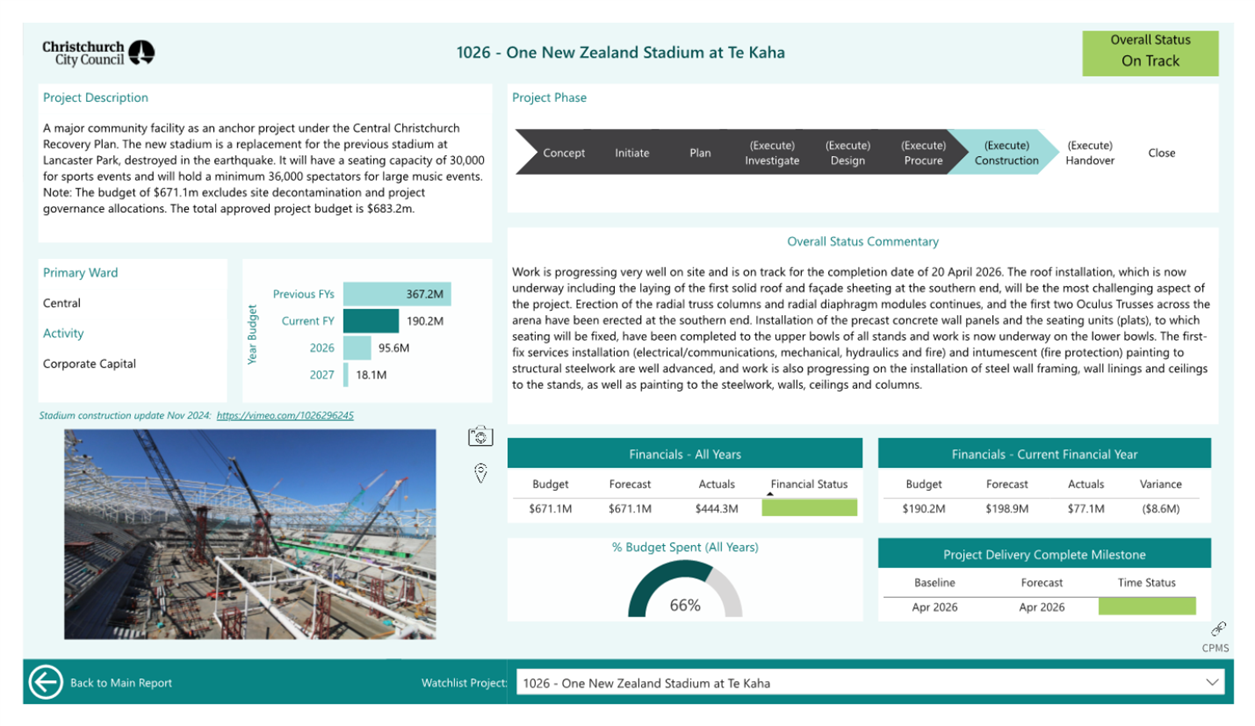

excludes One New Zealand Stadium at Te Kaha.

8.4 More

detailed information is available in the Capital Programme Performance Report.

8.5 Following

is the forward view of capital delivery performance for the LTP 2024-34

(financial).

8.6 The

forward view of capital delivery performance (financial) looks at commitments

for the first three years of the LTP 2024-34, accompanied by confirmed capital

delivery in preceding LTP-cycles against plan.

8.7 This

view takes into account revised year-end budget delivery figures for 2023/24,

and the adopted capital programme from the LTP 2024-34 (approved future years

planned expenditure for 2024/25, 2025/26 and 2026/27).

8.8 The

extended black line is the full planned delivery budget including One New

Zealand Stadium at Te Kaha.

8.9 The

extended blue line shows the full Council planned delivery budget (excluding

One New Zealand Stadium at Te Kaha, and before any confirmed carry forwards):

· from a consistent $488m to

$483m planned budget for the three years (2021-24);

· to between $548m to $668m

planned budget for the future three years (2024-27).

8.10 It

is accepted these future planned delivery budgets for capital meet

Council’s expectations as being both deliverable and affordable.

8.11 Currently, Council capital delivery (green

line) for 2024/25 (year one of the LTP 2024) is forecast at $510m

against the current programme budget of $548m (blue line). This equates

to -$37.4m, or 93.1% forecast delivery.

8.12 This

forecast delivery value is in line with the year-end actual value for 2023/24,

$502m.

8.13 The

ELT performance goal for capital delivery is based on all delivery Council is

accountable for (excluding One New Zealand Stadium at Te Kaha), regardless of

funding source.

8.14 Figures

align with the Financial and Capital Programme Performance reports.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Top Activities

(service delivery and budget)

|

24/2209488

|

26

|

|

b ⇩

|

Service

delivery (level of service) exceptions

|

24/2203231

|

28

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Amber Tait - Performance

Analyst

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

|

|

8. Financial Performance Report -

November 2024

|

|

Reference Te Tohutoro:

|

24/2074300

|

|

Responsible Officer(s) Te Pou Matua:

|

Russell

Holden, Head of Finance

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is for the

Finance and Performance Committee to be updated on Council's financial

performance to 30 November 2024 including the current year forecast.

1.2 This is a regular monthly report that is presented to the

Committee. Debtor, treasury and general insurance claims information is

reported quarterly.

2. Officer Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Financial

Performance Report - November 2024 Report.

3. Executive Summary

3.1 The

year-to-date operational surplus of $19.0m is $21.8m higher than budget year to

date, driven by savings in insurance costs, reduced personnel costs due to

staff vacancies and lower than budgeted solid waste recycling / organics

processing fees.

3.2 The

forecast operating surplus for the year is currently $12.2m, compared to $11.8m

last month. The improvement of $0.4m has been driven by improvement of solid

waste and resource recovery costs relating to the Burwood Landfill and

recycling/organics processing costs, additional revenue from recreation and

sports from higher than planned participation at facilities, and savings of

personnel cost across various activities.

3.3 The

capital programme delivery is marginally above budget year to date

(0.7%). The total capital programme, before signalled

carry forwards, is forecast to be under spent by $29.0 million. This comprises

a forecast under spend of $37.7 million on the core programme and a forecast

overspend of $8.6 million on the One New Zealand Stadium at Te Kaha. Both

variances will be managed via carry-forward / bring-back requests.

3.4 On

the 4 December, Standard & Poor’s (S&P) affirmed the Credit

Rating for Council and CCHL at “AA” but revised their Outlook for

both entities from “Stable” to “Negative”.

3.4.1 The primary driver

for this revision is S&P’s view that the institutional settings for

the local government sector are weakening – they emphasise that New

Zealand’s institutional settings are among the strongest in the world,

but rising spending needs, high levels of planned indebtedness, and elevated

uncertainty around government policy (particularly related to waters) is

exerting downward pressure on this underlying strength. S&P are

likely to review their assessment of sector settings annually, which raises

some risk of a future downgrade to “AA-”, but this will not be

known until their sector review is completed (possibly in the first quarter of

2025).

3.4.2 A secondary factor in

S&P’s revision is Council’s high level of planned new borrowing

and suspension of progress towards full renewals funding, both of which are

expected to be temporary factors driven by the Te Kaha project.

3.4.3 S&P emphasises

the improved management stability at Council and Christchurch City Holdings

Limited with the appointment of permanent Chief Executives, Council’s

credible and well-established fiscal processes, resilient local economy, and

relatively new infrastructure asset base.

3.4.4 The revised Rating

will not affect the availability or cost of debt at Council or CCHL. Of

the 19 councils rated by S&P, only Auckland and Whangarei remain at

“AA (Stable)”.

4. Operational Revenue and Expenditure

4.1 This covers day to day spend on

staffing, operations and maintenance, and revenues to fund the operational

spend.

4.2 Operational revenue exceeds

expenditure as it includes rates revenue for capital renewals and debt

repayment. This ‘capital’ revenue is referred to below as

‘Funds not available for Opex’ and is removed to show the year to

date and forecast cash operational surplus or deficit.

|

Year to Date Results

|

Forecast Year End Results

|

After Carry Forwards

|

|

$m

|

Actual

|

Budget

|

Var

|

|

Forecast

|

Budget

|

Var

|

|

Carry Fwd

|

Var

|

|

|

Revenues

|

(485.9)

|

(485.9)

|

0.8

|

|

(1,085.4)

|

(1,079.4)

|

6.0

|

|

-

|

6.0

|

|

|

Expenditure

|

344.9

|

354.7

|

19.8

|

|

821.0

|

827.9

|

6.9

|

|

0.3

|

6.6

|

|

|

Funds not

available for Opex

|

132.0

|

133.2

|

1.2

|

|

252.2

|

251.5

|

(0.7)

|

|

(0.3)

|

(0.4)

|

|

|

Operating

(Surplus)/Deficit

|

(19.0)

|

2.8

|

21.8

|

|

(12.2)

|

-

|

12.2

|

|

-

|

12.2

|

|

4.3 The

current operating surplus variance of $21.8 million declines to a forecast

$12.2 million by year end due to timing, trends and work patterns. Brief summaries of the material revenue and expenditure variances

and changes are highlighted below.

4.4 Revenues are $0.8 million ahead of budget year to date and are

forecast to be $6.0 million higher at year end. Key

drivers of actual and forecast variances to budget include (amounts in brackets

are revenues below budget):

|

Variance

|

YE Budget

|

YTD

|

YE Forecast – above / (below) budget

|

|

Building & Planning consent volumes

|

35.0m

|

1.6m

|

2.7m

|

|

Recreation & Sports pools and fitness

centres increased participation

|

21.4m

|

1.2m

|

0.9m

|

|

Rates overstrike

|

760.8m

|

0.5m

|

0.9m

|

|

Transwaste dividend

|

7.3m

|

-

|

0.4m

|

|

Otautahi Community Housing Trust (OCHT)

revenues

|

16.3m

|

(0.1m)

|

0.7m

|

|

Hagley Park parking fees – new

parking meters delayed

|

2.2m

|

(0.8m)

|

(0.9m)

|

|

Excess Water – Residential

|

2.3m

|

(0.4m)

|

-

|

|

Excess Water – Commercial

|

2.9m

|

(0.3m)

|

-

|

|

Other revenues

|

230.2m

|

(0.9m)

|

1.3m

|

|

Total

|

1,078.4m

|

0.8m

|

6.0m

|

4.5 The

rates overstrike arises as Council needs to estimate the City’s rateable

capital value for the 24/25 rates strike prior to receiving final changes for

the 23/24 year from Quotable Values.

4.6 Expenditure is $19.8 million lower than budget year to date and

forecast to be $6.6 million under budget after carry forwards at year

end. Key drivers of actual and forecast variances to budget include:

|

Variance

|

YE Budget

|

YTD

|

YE Forecast

(after c/f)

|

|

Insurance costs

|

38.3m

|

7.9m

|

7.9m

|

|

Personnel Costs (Full corporate increases

not yet applied (only staff on collective agreements), units with vacancies

which were planned to be filled)

|

266.4m

|

4.1m

|

2.2m

|

|

Waste Management lower recycling

processing fees and organic processing fees, and landfill costs

|

69.7m

|

4.1m

|

3.9m

|

|

Transport – Timing of maintenance

costs

|

55.2m

|

2.1m

|

(0.3m)

|

|

Parks - timing of maintenance costs,

costs expected to increase in summer months

|

16.3m

|

1.7m

|

-

|

|

Rates on Council owned properties

|

36.8m

|

0.3m

|

1.0m

|

|

OCHT Community Housing increased

operating and maintenance costs (partially offset by increased revenue)

|

6.0m

|

0.0m

|

(0.7m)

|

|

Transport – increased cost of

illegal fly tipping.

|

-

|

(0.7m)

|

(1.0m)

|

|

Three Waters – continued high City

Care reactive maintenance volumes.

|

37.3m

|

(0.1m)

|

(1.6m)

|

|

Three Waters – Staff time

capitalisations

|

(7.8m)

|

(0.3m)

|

(1.4m)

|

|

Building Consenting & Planning

Consenting – additional costs outsourcing consent processing to meet

LoS, due to volumes and staff shortages (offset by increased revenue).

|

14.9m

|

(1.0m)

|

(2.2m)

|

|

Other minor variances

|

294.8m

|

1.7m

|

(1.2m)

|

|

Total

|

827.9m

|

19.8m

|

6.6m

|

5. Capital Expenditure and Revenue

5.1 This

section covers the capital programme spend and funding relating to it.

|

Year to Date Results

|

Forecast Year End Results

|

After Carry Forwards

|

|

$m

|

Actual

|

Budget

|

Var

|

|

Forecast

|

Budget

|

Var

|

|

Carry Fwd

|

Var

|

|

|

Core Programme

|

162.6

|

171.4

|

8.7

|

|

507.6

|

521.9

|

14.4

|

|

(1.3)

|

15.7

|

|

|

External Funded

Programme

|

10.2

|

9.5

|

(0.7)

|

|

24.3

|

25.7

|

1.4

|

|

(1.3)

|

2.7

|

|

|

Less unidentified

Carry Forwards

|

0.0

|

0.0

|

0.0

|

|

(21.9)

|

-

|

21.9

|

|

40.1

|

(18.2)

|

|

|

Core/External

Funded Programme

|

172.8

|

180.8

|

8.0 8.0

|

|

510.0

|

547.7

|

37.7

|

|

37.5

|

0.2

|

|

|

One New Zealand

Stadium at Te Kaha

|

77.0

|

67.3

|

(9.7)

|

|

198.9

|

190.2

|

(8.6)

|

|

(8.6)

|

-

|

|

|

Total Capital

Programme

|

249.8

|

248.1

|

(1.7)

|

|

708.9

|

737.9

|

29.0

|

|

28.8

|

0.2

|

|

|

Revenues and

Funding

|

(182.9)

|

(126.9)

|

56.0

|

|

(355.3)

|

(330.8)

|

24.5

|

|

-

|

24.5

|

|

|

Borrowing

required

|

66.8

|

121.2

|

54.4 54.4

|

|

353.6

|

407.1

|

53.5

|

|

28.8

|

24.7

|

|

Capital

Expenditure

5.2 Gross capital expenditure of

$249.8 million has been incurred against a year-to-date budget of $248.1

million.

5.3 Overall, total capital expenditure

of $708.9 million is forecast (based on the PMO forecast of $510 million for

CCC Capital-Core/External Funded), to be spent against the annual budget of

$737.9 million. Of the $29.0 million forecast variance, the majority is

forecast to be requested to be carried forward at year end.

Capital

Revenues and Funding

5.4 Capital revenues and funding is $56.0m

higher than budget year to date. This is largely due to the insurance recovery

from the CWTP, higher development contributions being collected, partially

offset by lower crown revenues and NZTA capital subsidies.

5.5 The capital revenue and funding

forecast has increased by $17.2m to $24.5m due to receipt of $55.0m of

insurance recoveries for the CWTP Fire, offset by a $37.3m reduction in

expected crown capital revenues due to a budget overstatement in the LTP.

Attachments Ngā Tāpirihanga

There are no

attachments for this report.

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Mitchell Shaw

- Reporting Accountant

Karthik MG -

Reporting Accountant

Bruce Moher -

Manager Corporate Reporting

Steve Ballard

- Group Treasurer

|

|

Approved By

|

Russell Holden

- Head of Finance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

|

|

9. Capital Programme Performance

Report November 2024

|

|

Reference Te Tohutoro:

|

24/2094806

|

|

Responsible Officer(s) Te Pou Matua:

|

Nicky

Palmer, Head of Programme Management Office

|

|

Accountable ELT Member Pouwhakarae:

|

Brent

Smith, Acting General Manager City Infrastructure

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to present to the Finance and Performance Committee

meeting with the monthly Capital Programme Performance Report for November 2024.

1.2 This

report provides Elected Members with oversight on the performance of the

Capital Programme.

2. Officer Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Capital

Programme Performance Report November 2024.

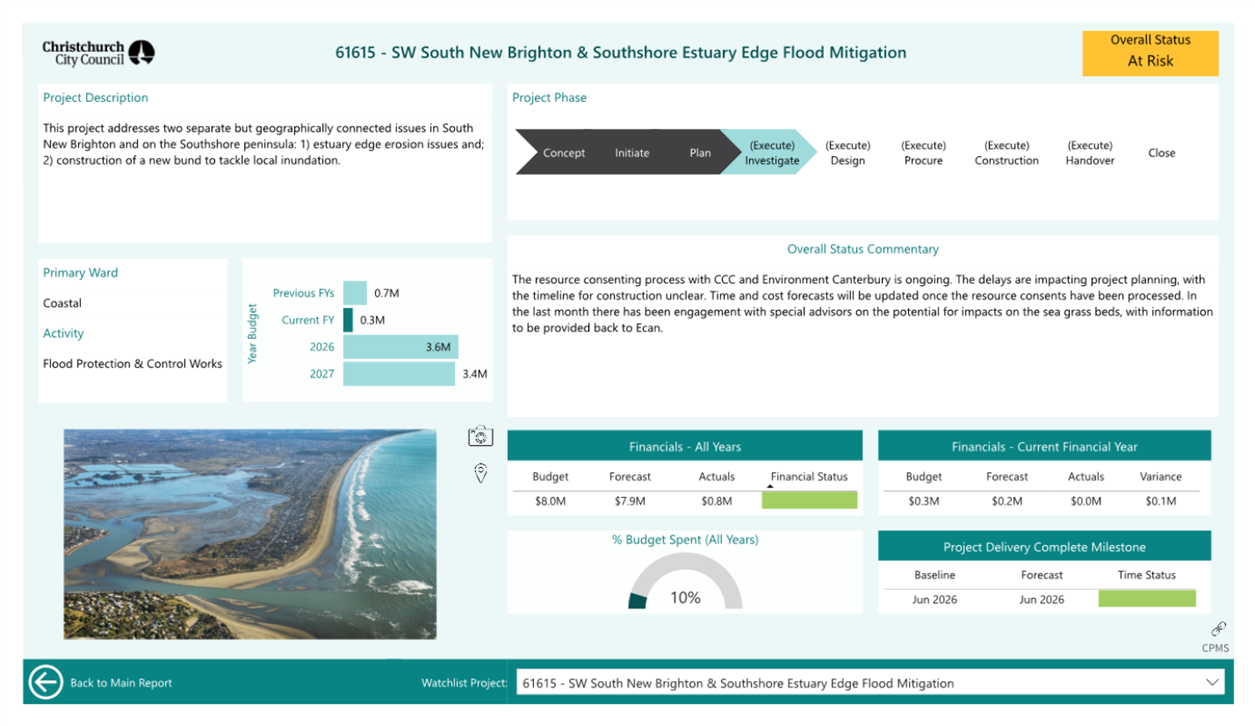

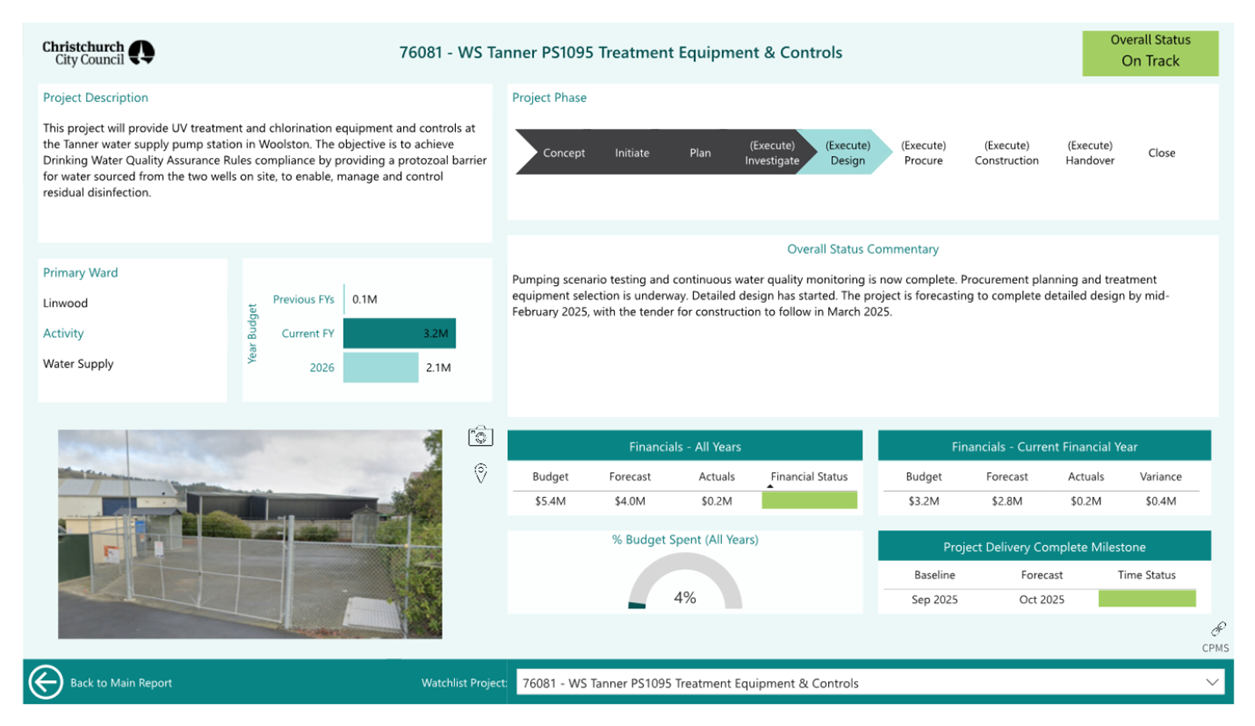

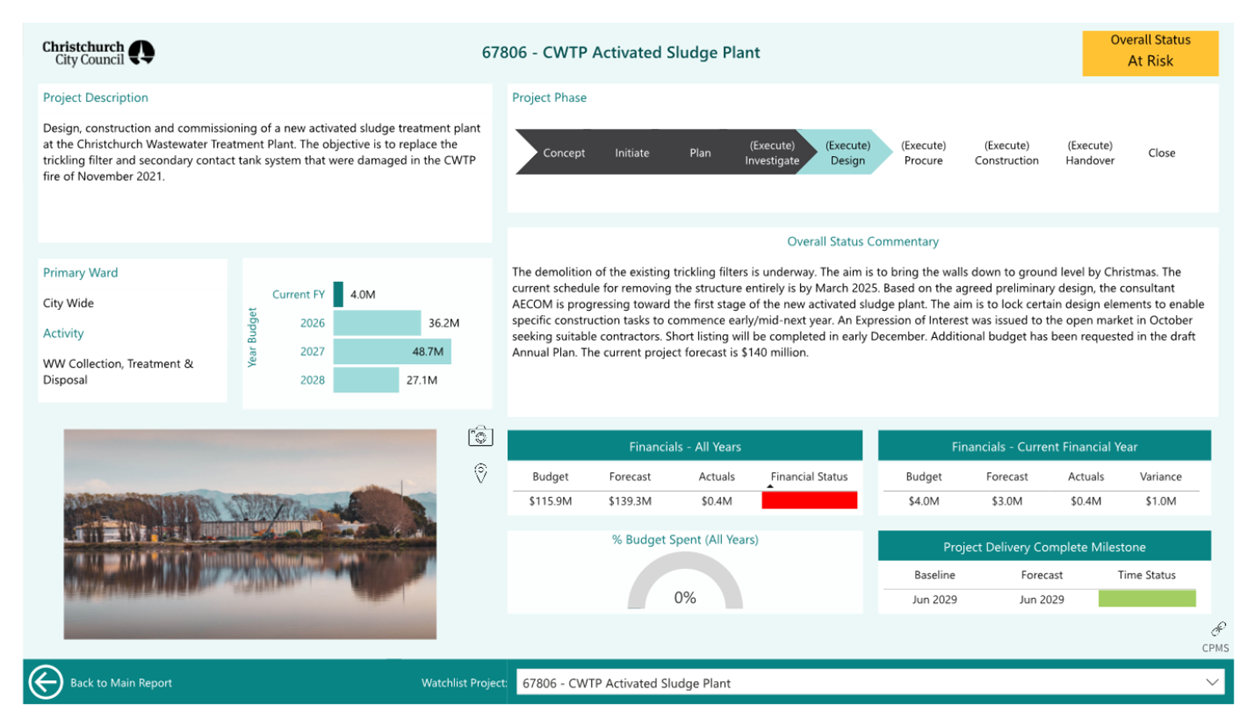

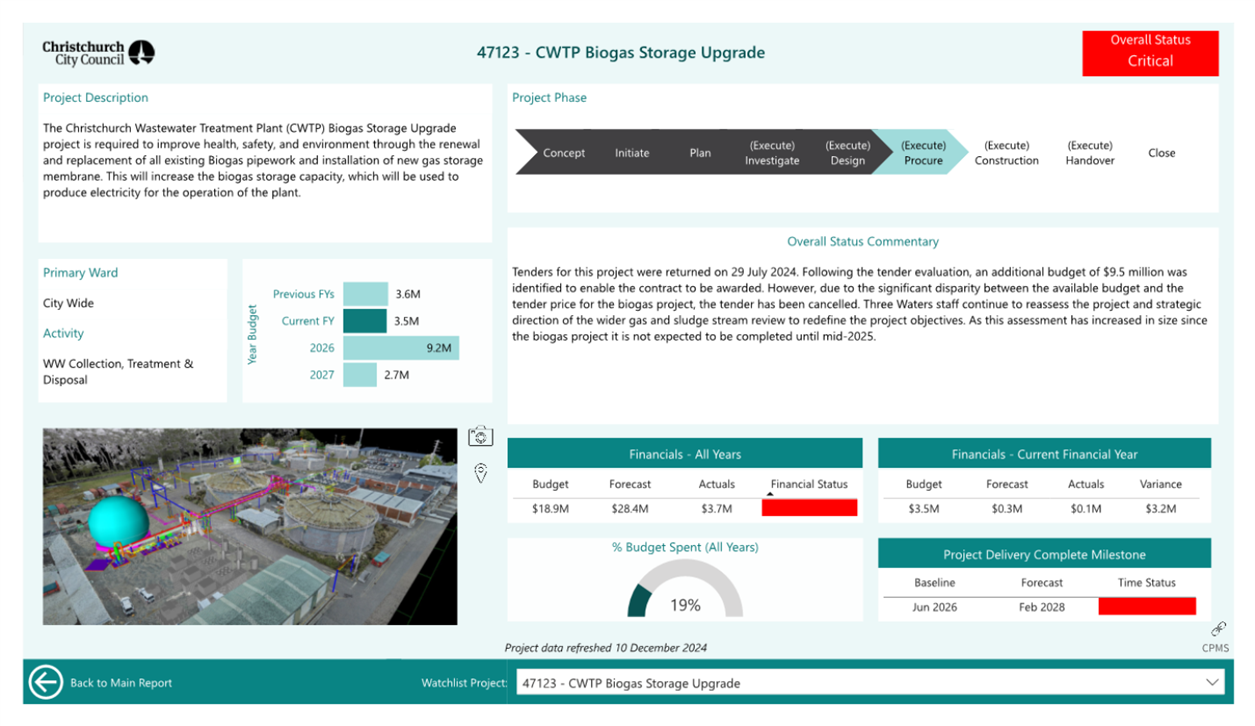

2. Approves the addition of project 67806

– CWTP Activated Sludge Plant (Christchurch Wastewater Treatment Plant

Trickling Filter Replacement) to the FY25 Watchlist.

3. Approves the removal of project 47123 – CWTP Biogas Storage

Upgrade from the FY25 Watchlist.

3. Background/Context Te Horopaki

3.1 At the end of November, the

overall capital programme (including One New Zealand Stadium at Te Kaha) has a

current FY25 forecast of $727.5m (99% of budget), based on Project Managers' consolidated forecasts.

3.2 The

year-end forecast for CCC Capital (excluding One New Zealand Stadium at Te

Kaha) as reported by Project Managers is $528.6m (97%

of budget). This is within 4% of the PMO Forecast, which remains at $510m

this month.

3.3 Full results are provided in the

Capital Programme Performance Report for November 2024 (Attachment A).

This includes the Watchlist Report as Appendix 1.

3.4 Approval is sought from the

Finance and Performance Committee on two changes to the Watchlist this month:

3.4.1 The

addition of project 67806 – CWTP Activated Sludge Plant to the

FY25 Watchlist Report. This project, which

will replace the fire-damaged trickling filter at the Christchurch Wastewater

Treatment Plant, is recommended for inclusion in the Watchlist based on public

profile, scale and significance, and cost. The addition is in alignment

with the draft set of FY25 Watchlist projects that was confirmed by the Finance

and Performance Committee in August 2024. This included a recommendation

that the project be added to the Watchlist once initiated and ready for

delivery.

3.4.2 The removal of

project 47123 – CWTP Biogas Storage Upgrade from the FY25

Watchlist Report. The tender for the project was cancelled due to the

disparity between the available budget and tender price ($9.5m budget

shortfall). Time is required to reassess the project and strategic direction of

the wider gas and sludge stream review (although mandatory health and safety

activities are still being delivered). As this work is not expected to be

completed until mid-2025, it is proposed to remove the project from Watchlist

reporting for the remainder of the financial year, and reconsider it for

inclusion in the FY26 Watchlist Report.

3.5 The Monthly Change Report is included in the public excluded section due to contract commercial

sensitivity.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

Attachment to

report 24/2094633 (Title: Capital Programme Performance Report - November

2024 - Final)

|

24/2224312

|

75

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Lauren Barry -

Senior PMO Business Analyst

Greer Hill -

Administrator Officer

Nicky Palmer -

Head of Programme Management Office

|

|

Approved By

|

Brent Smith -

Acting General Manager City Infrastructure

|

|

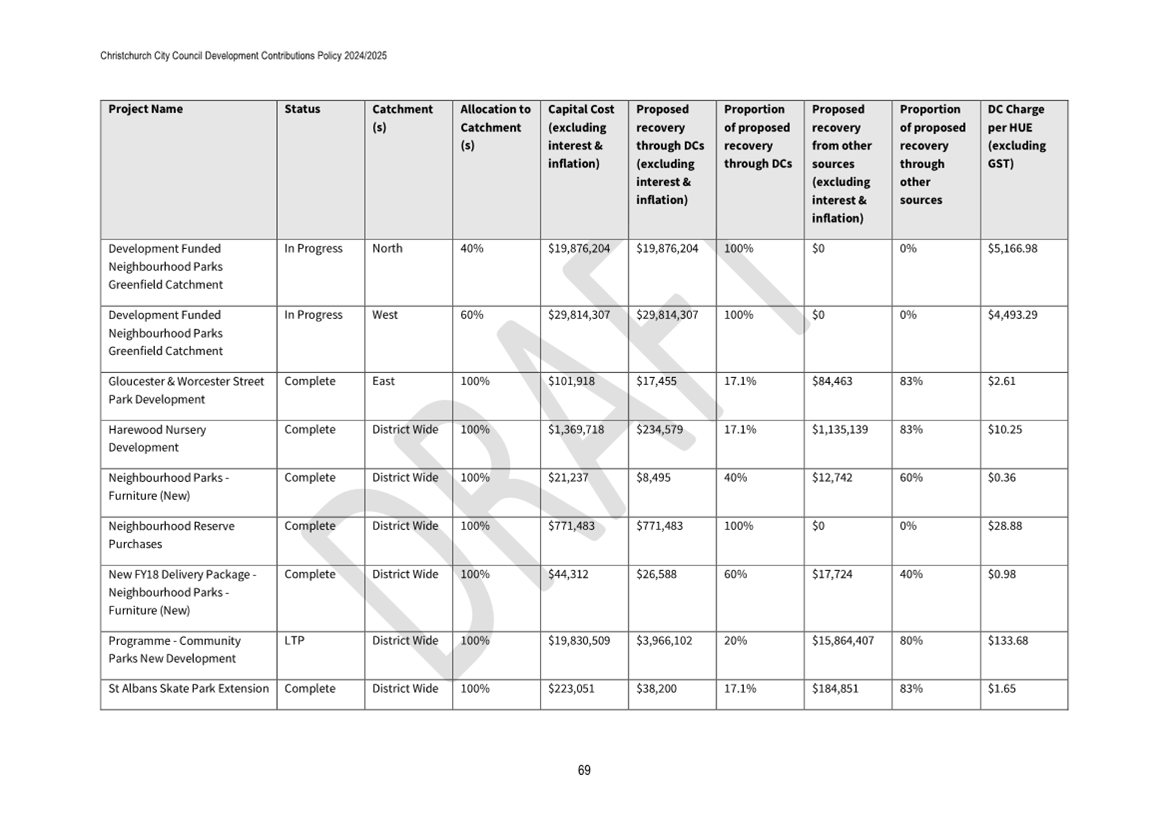

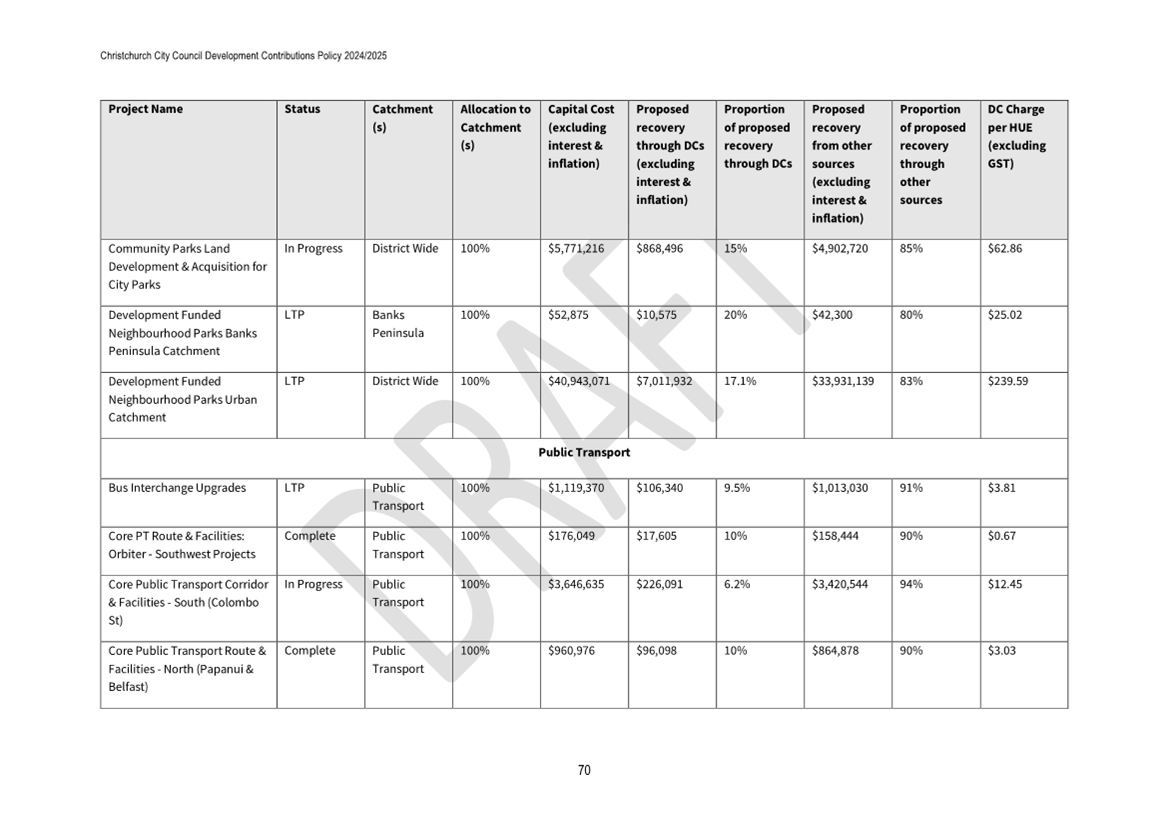

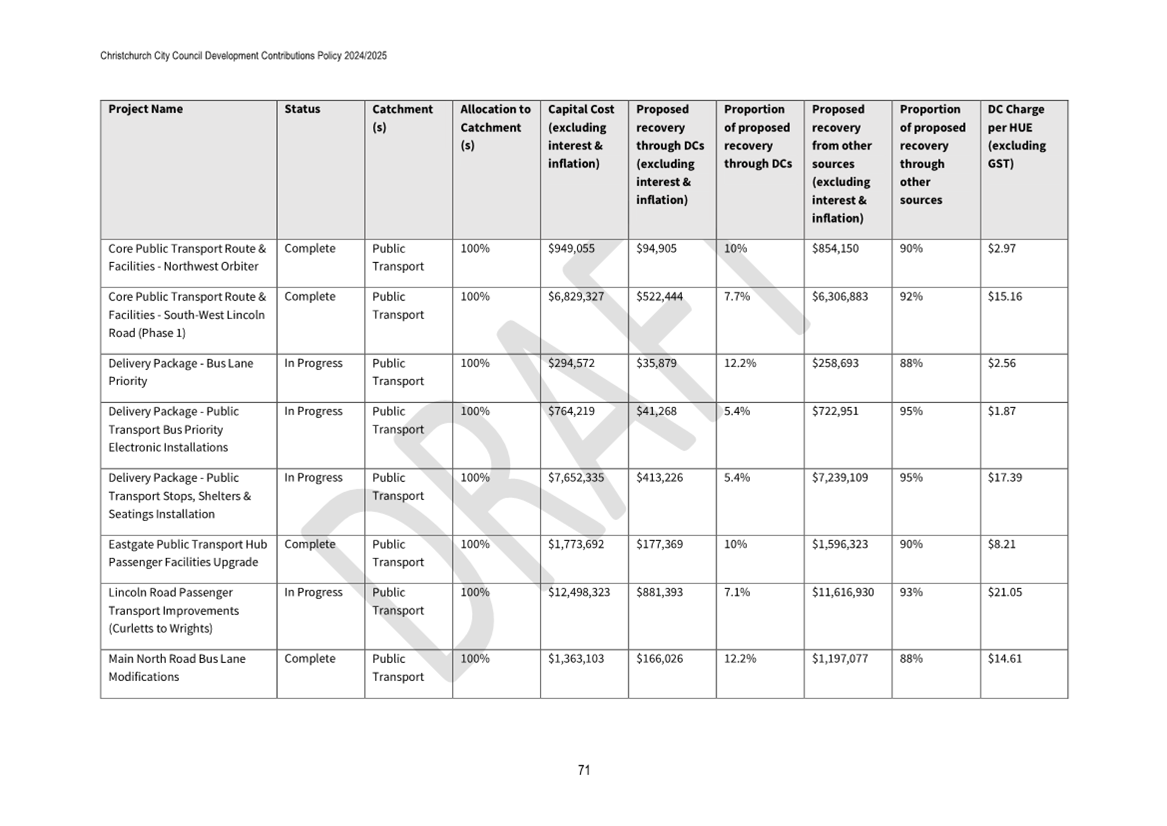

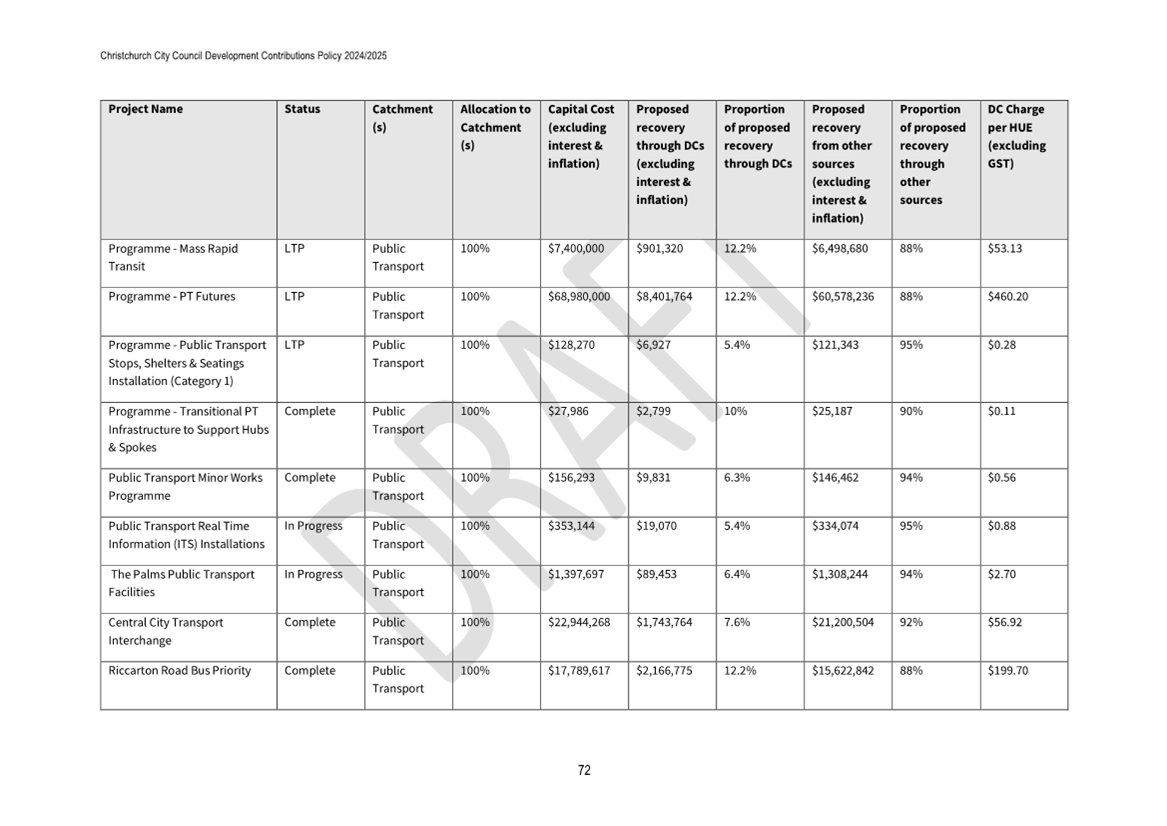

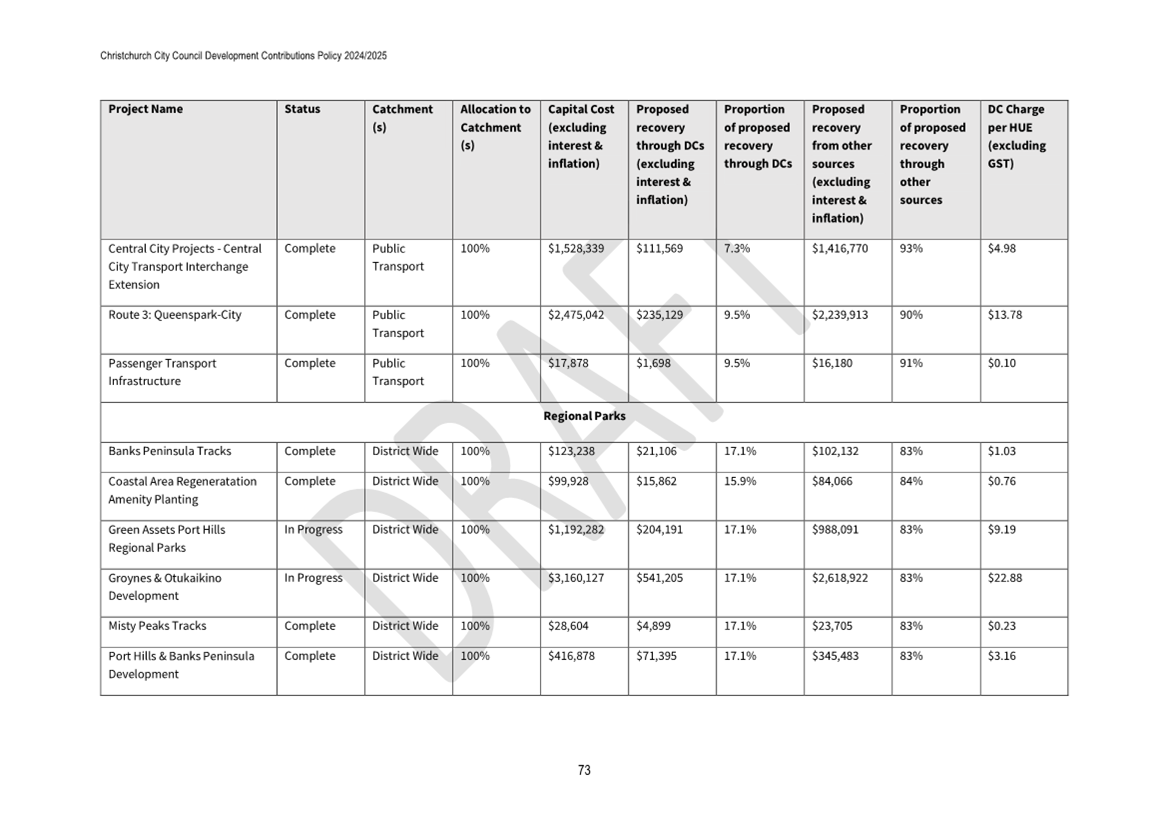

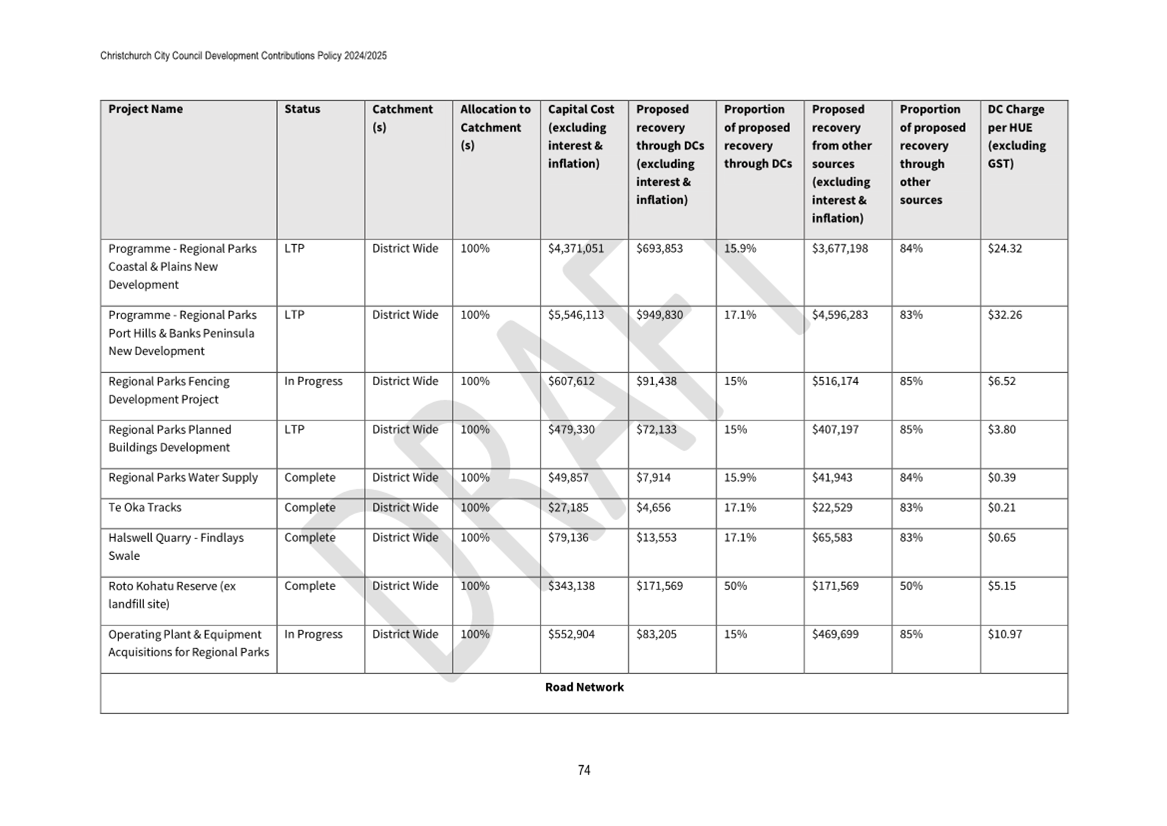

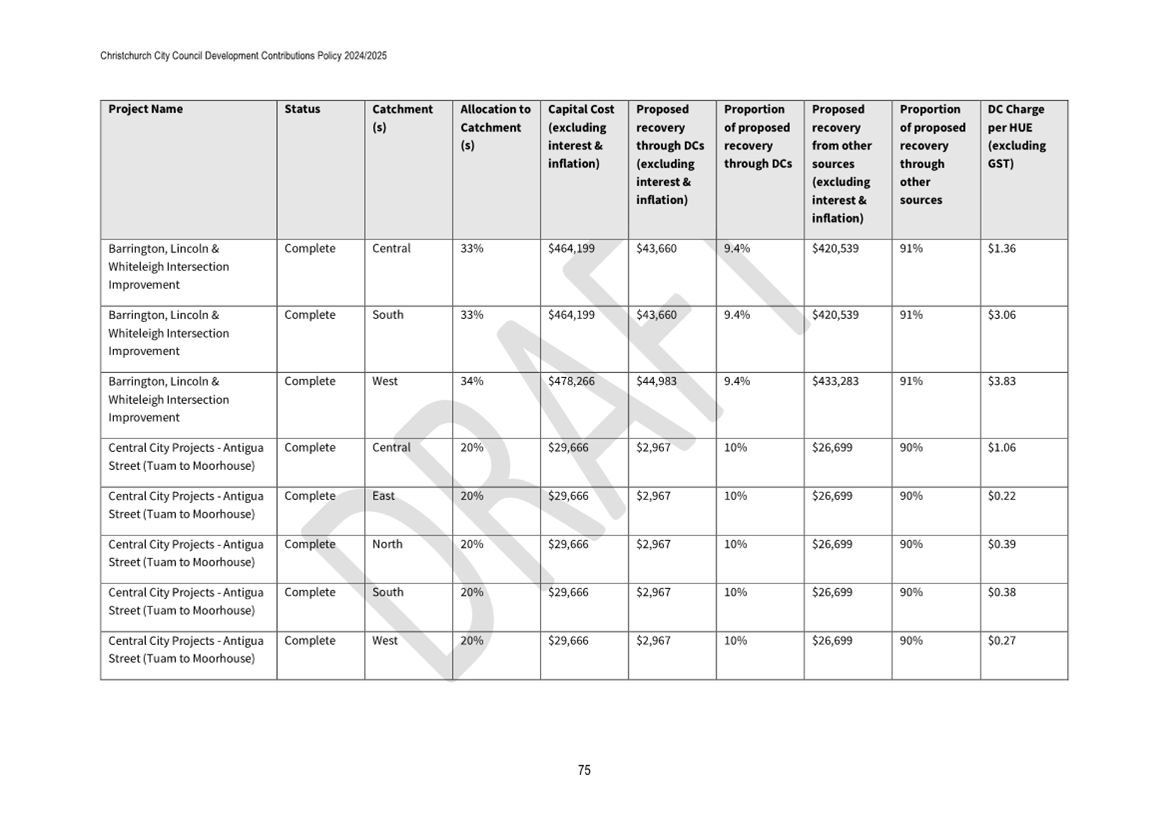

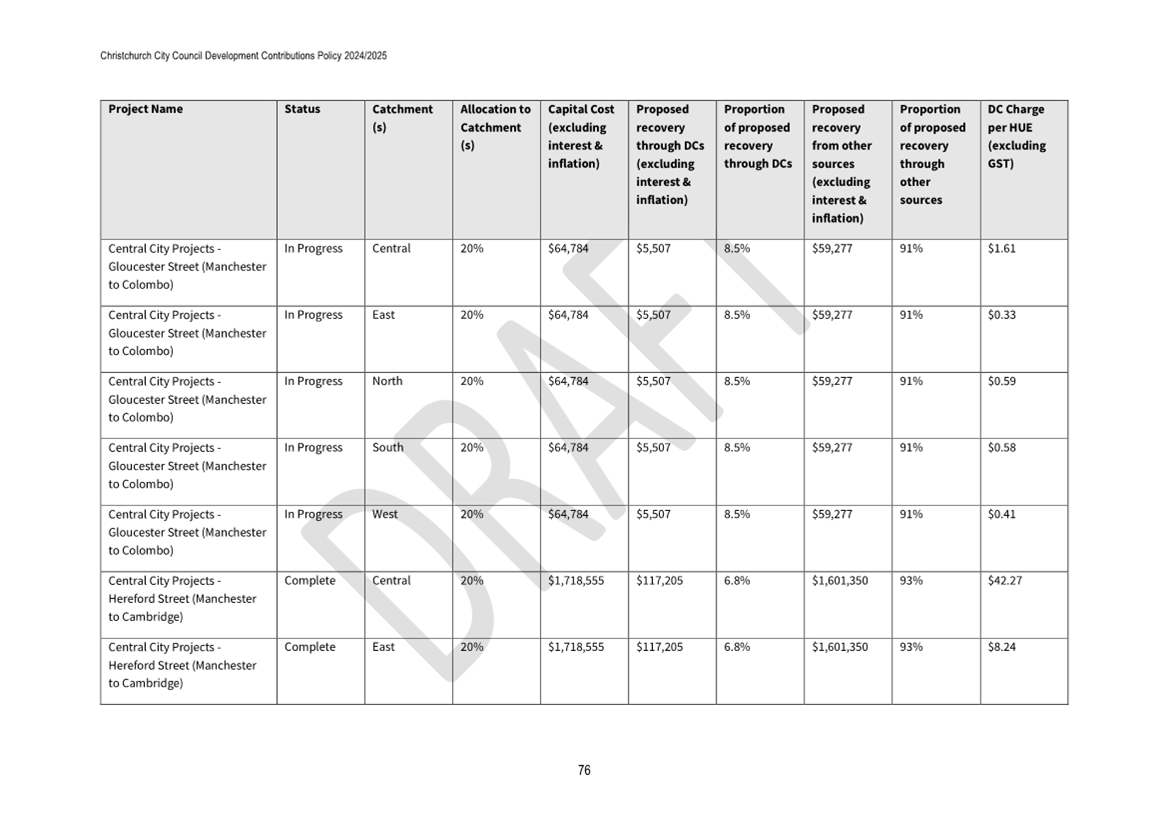

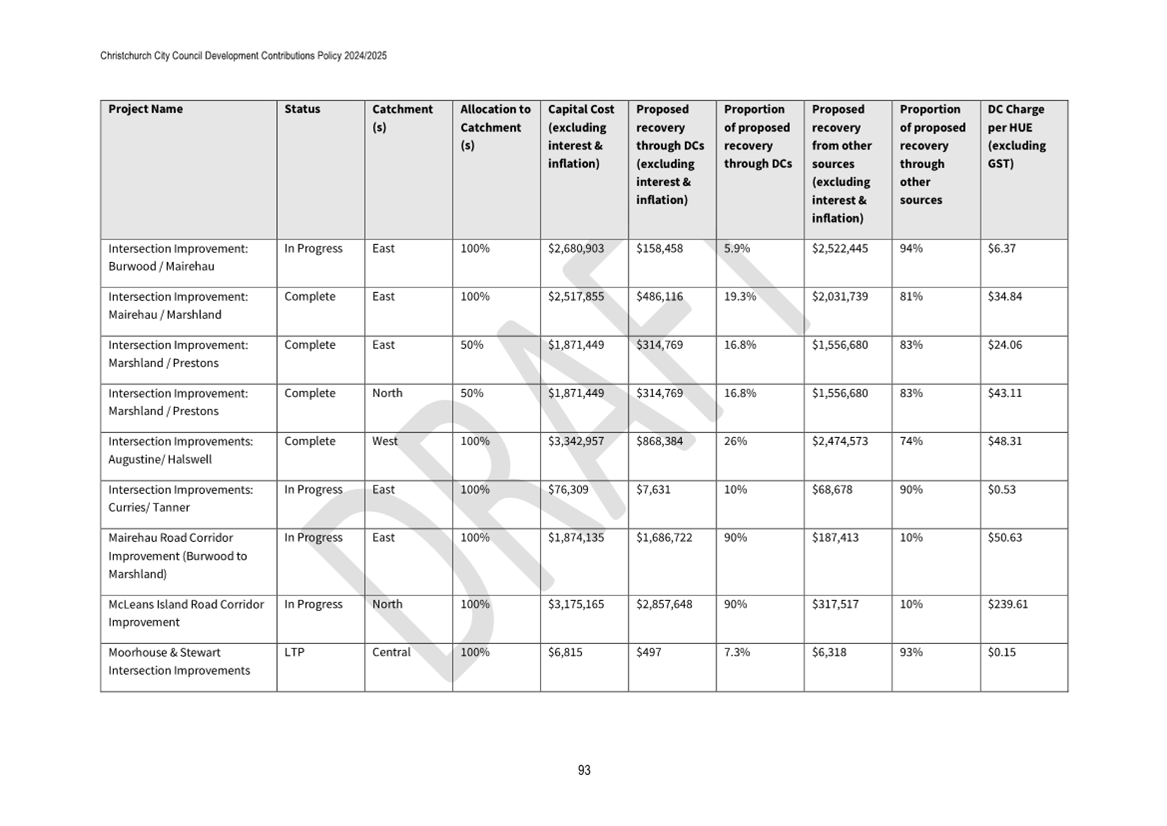

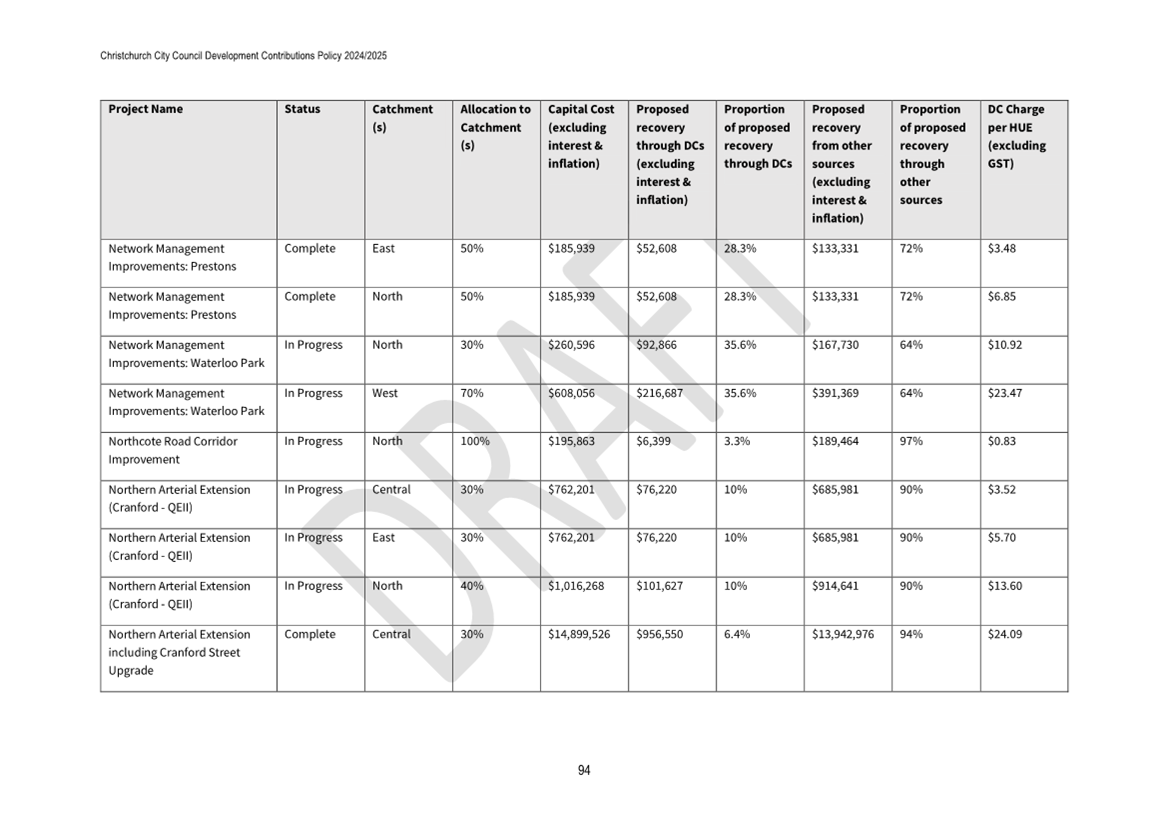

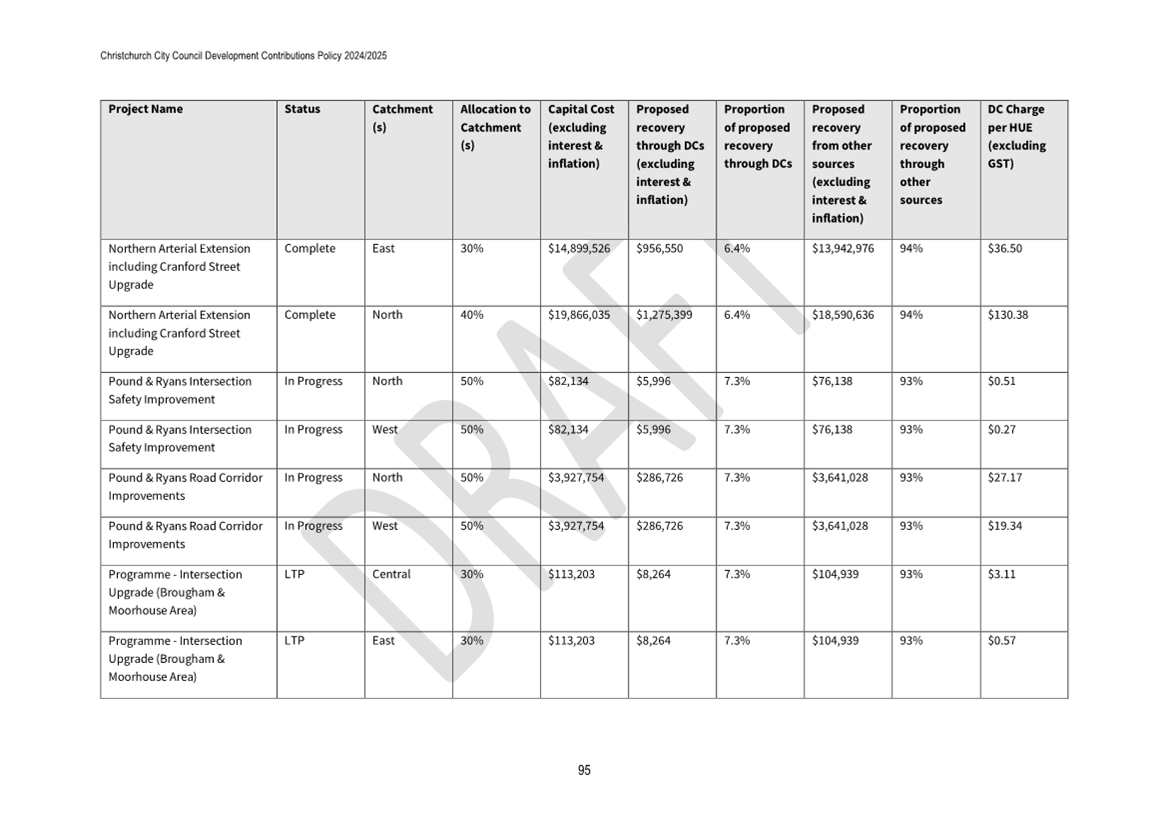

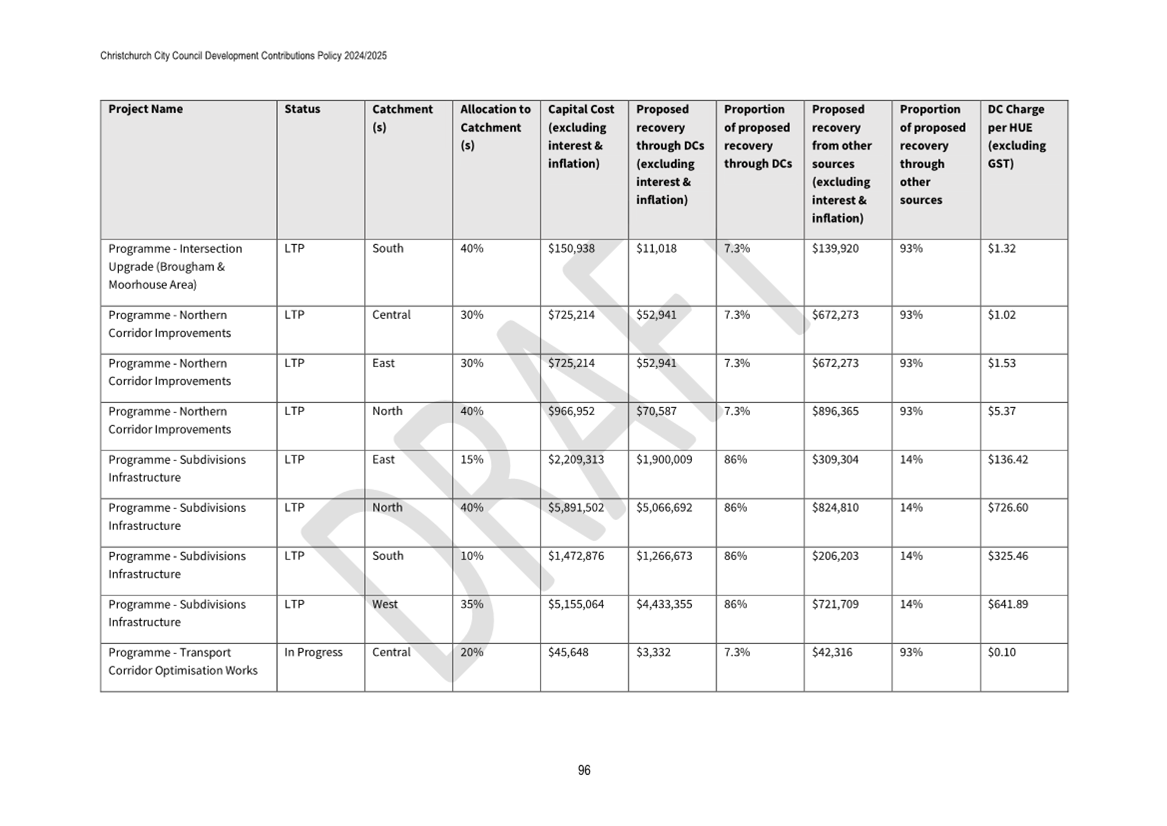

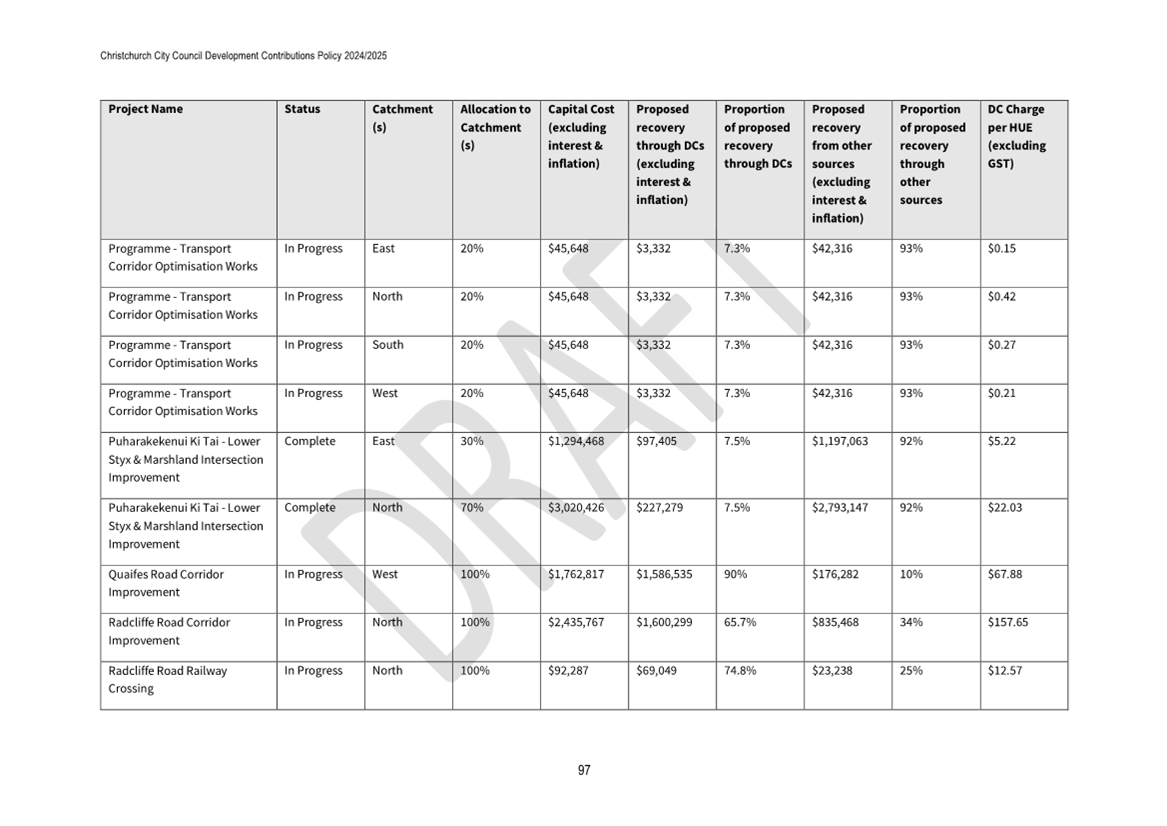

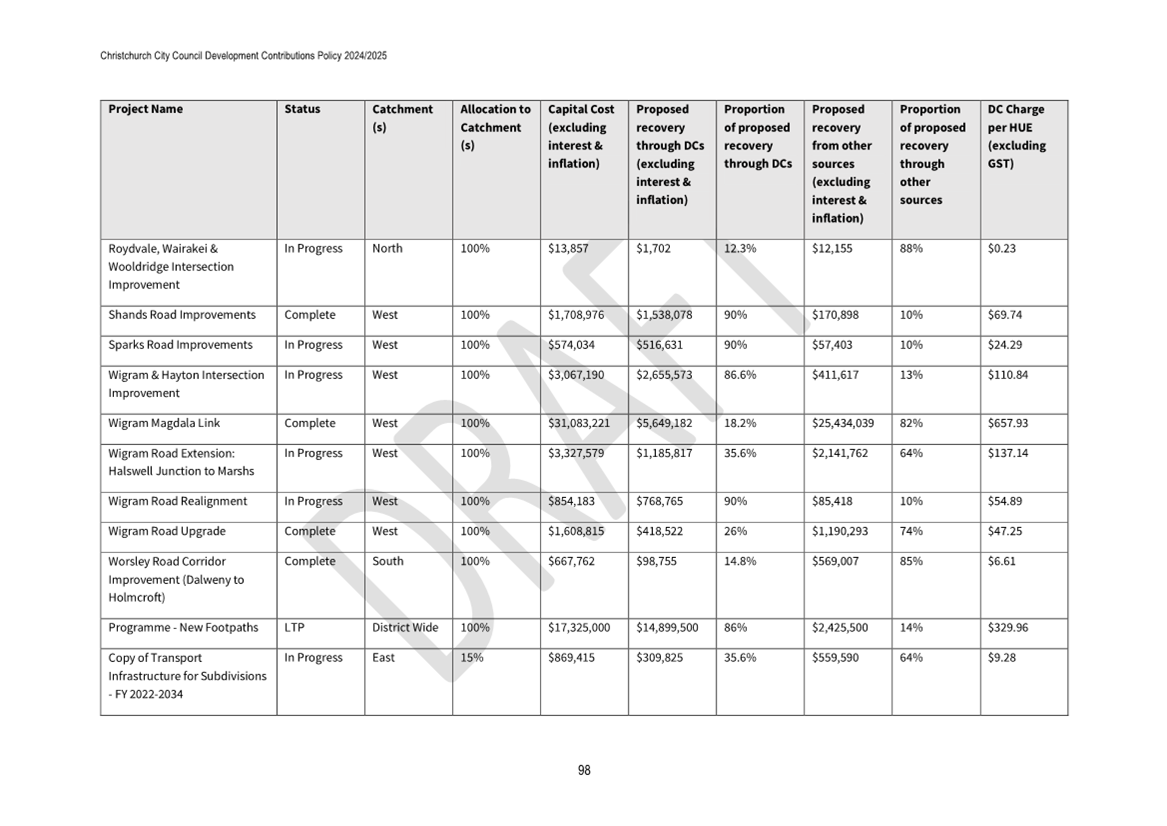

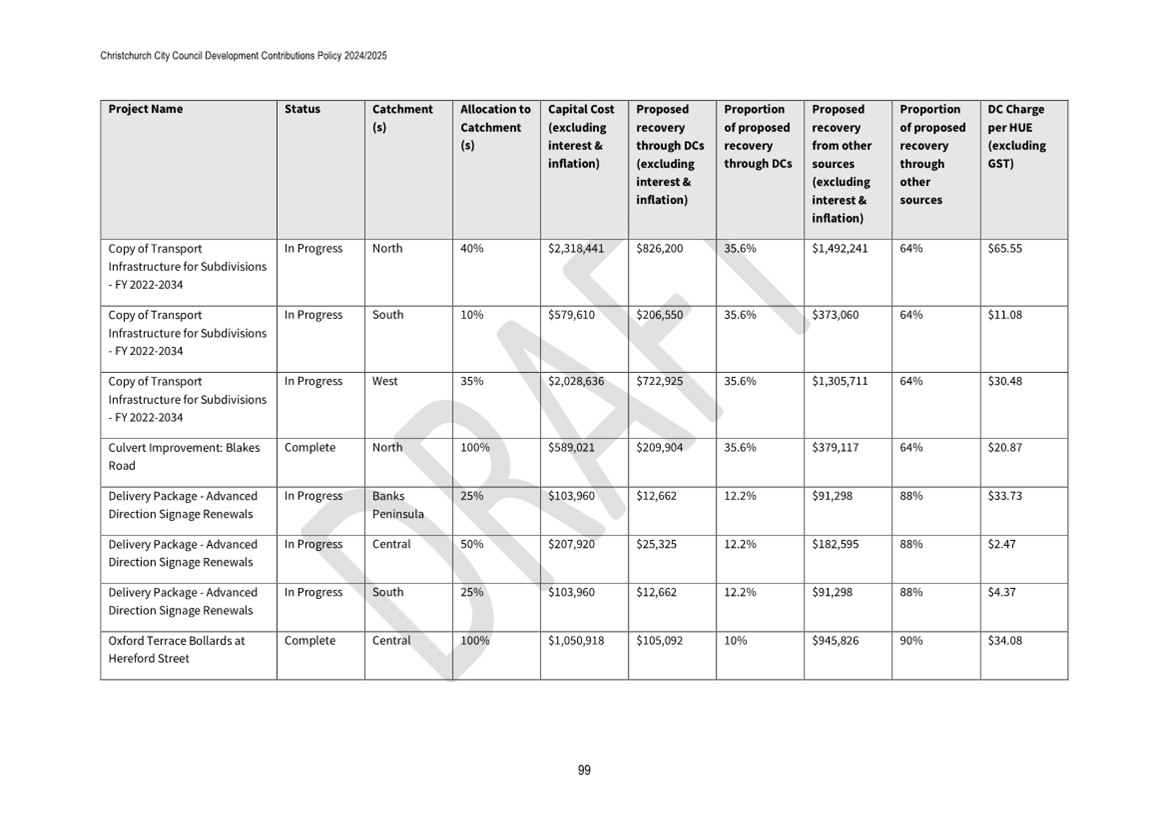

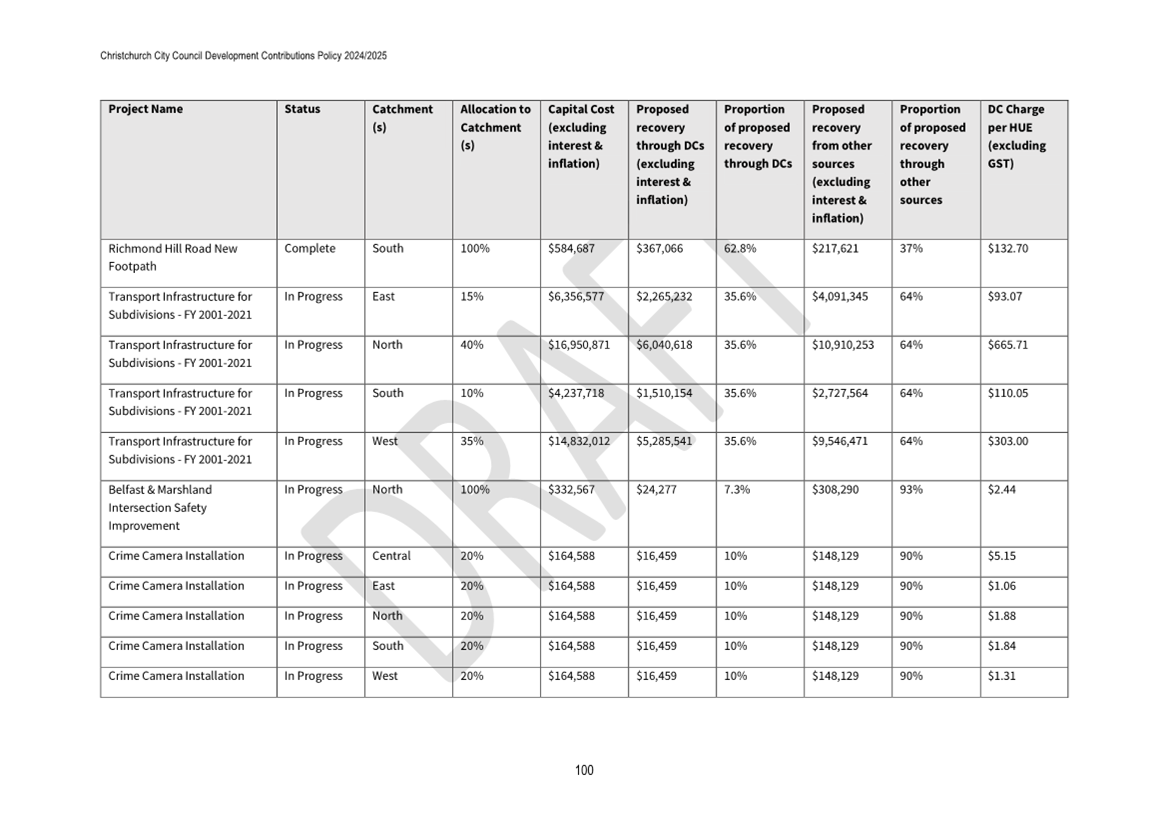

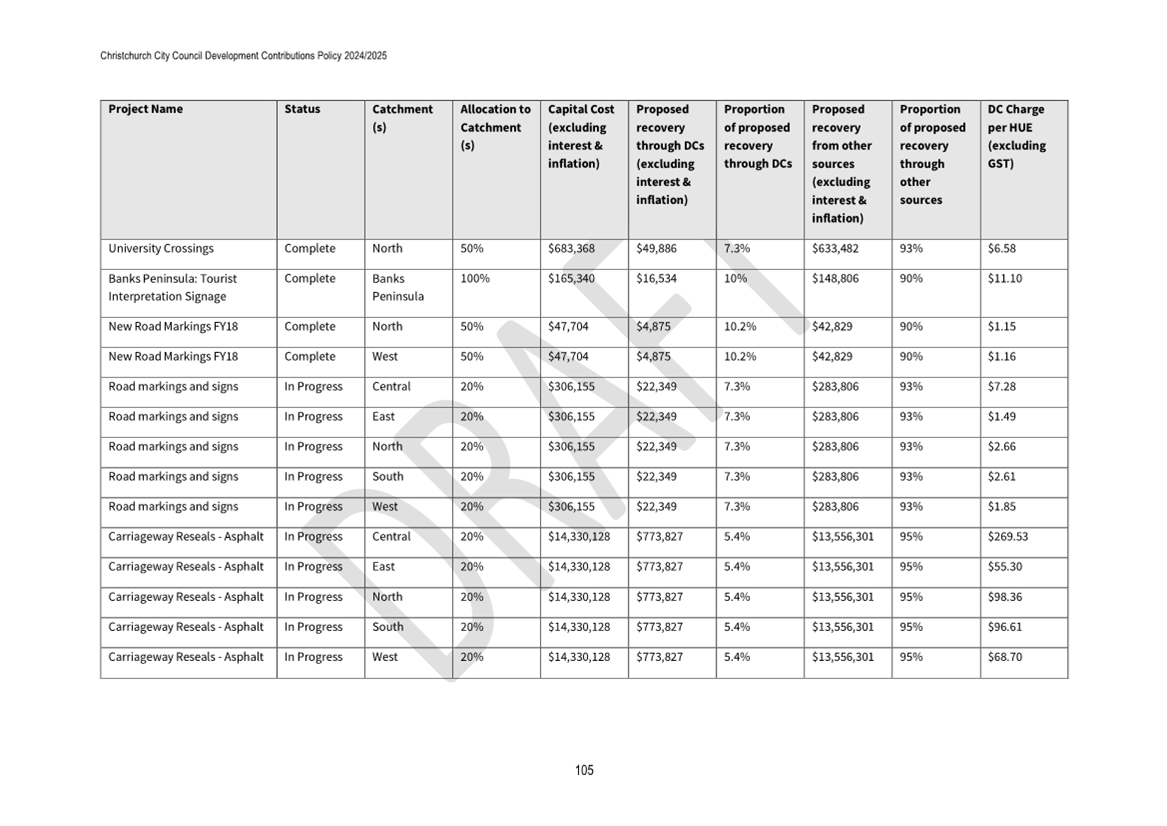

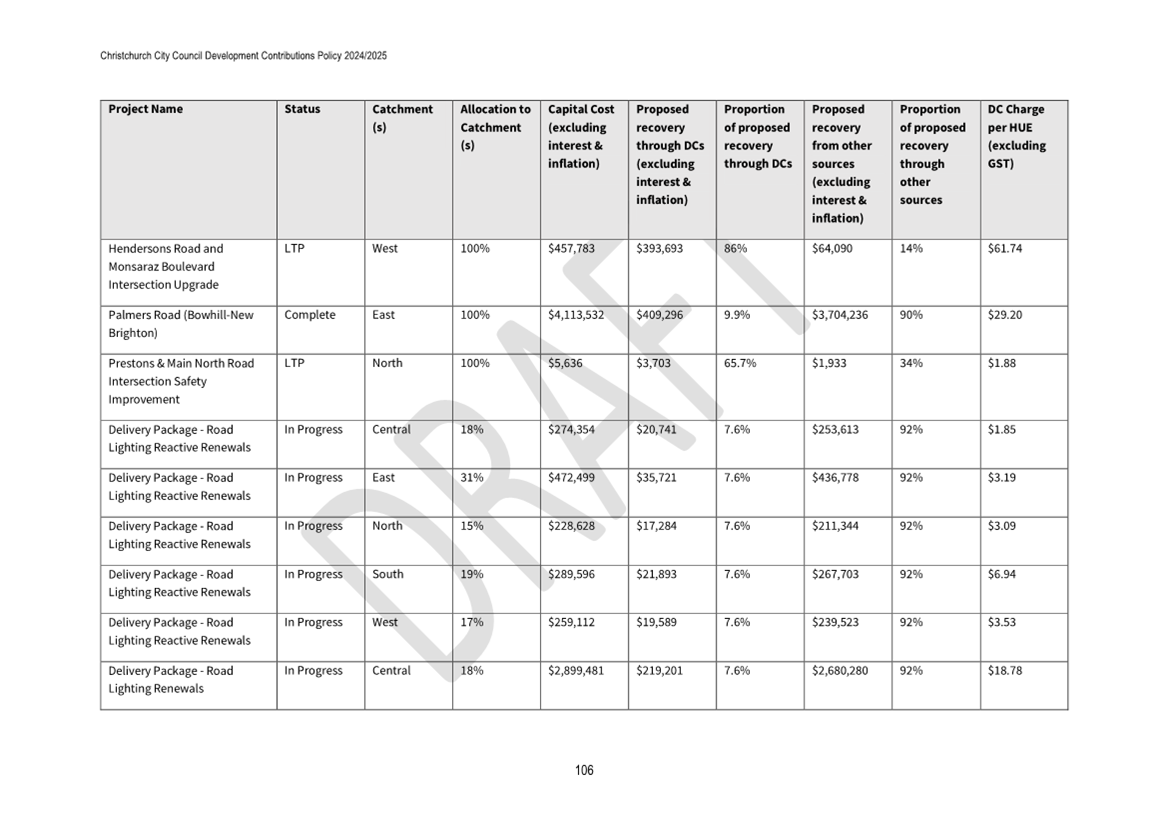

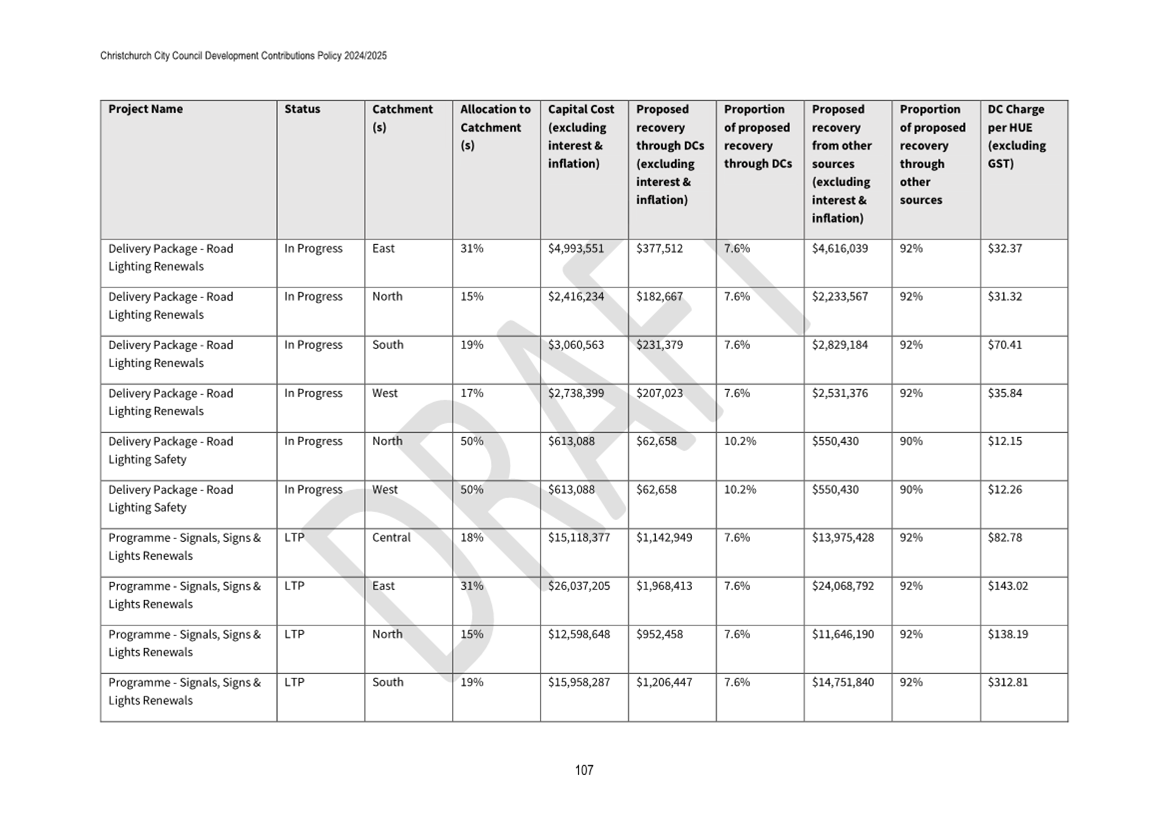

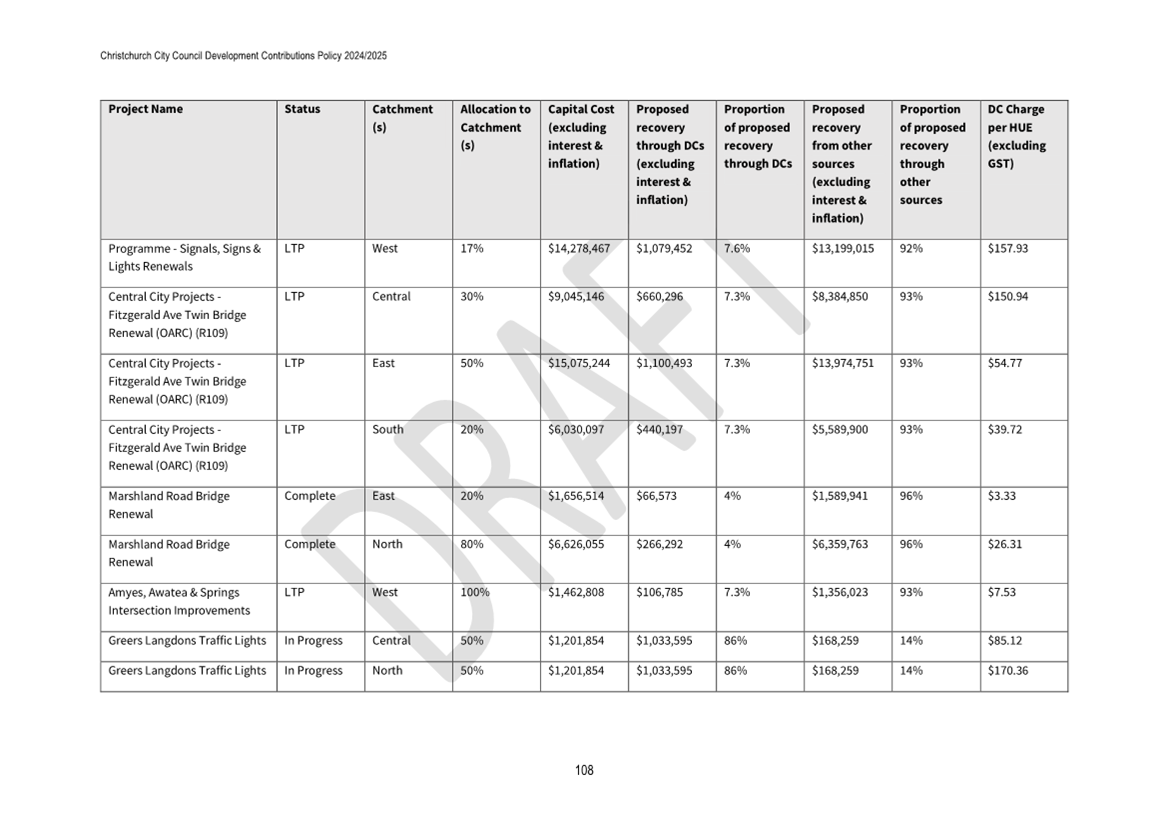

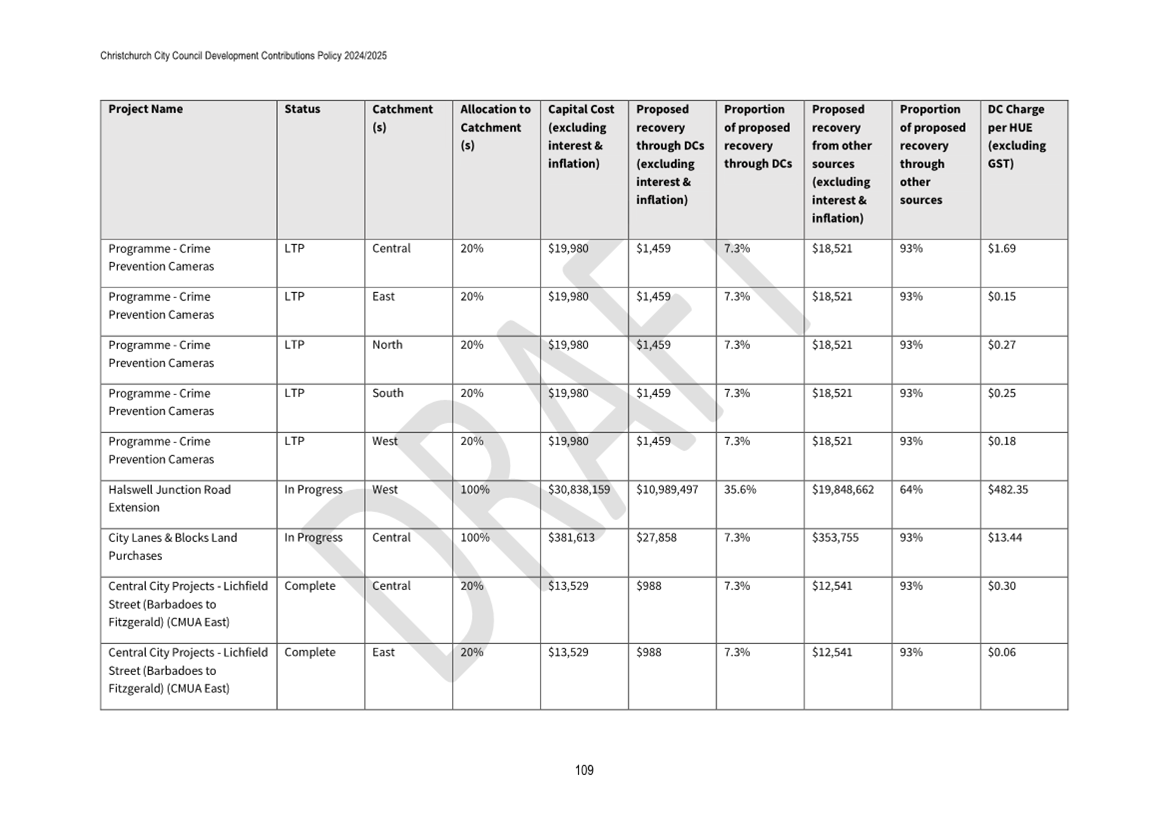

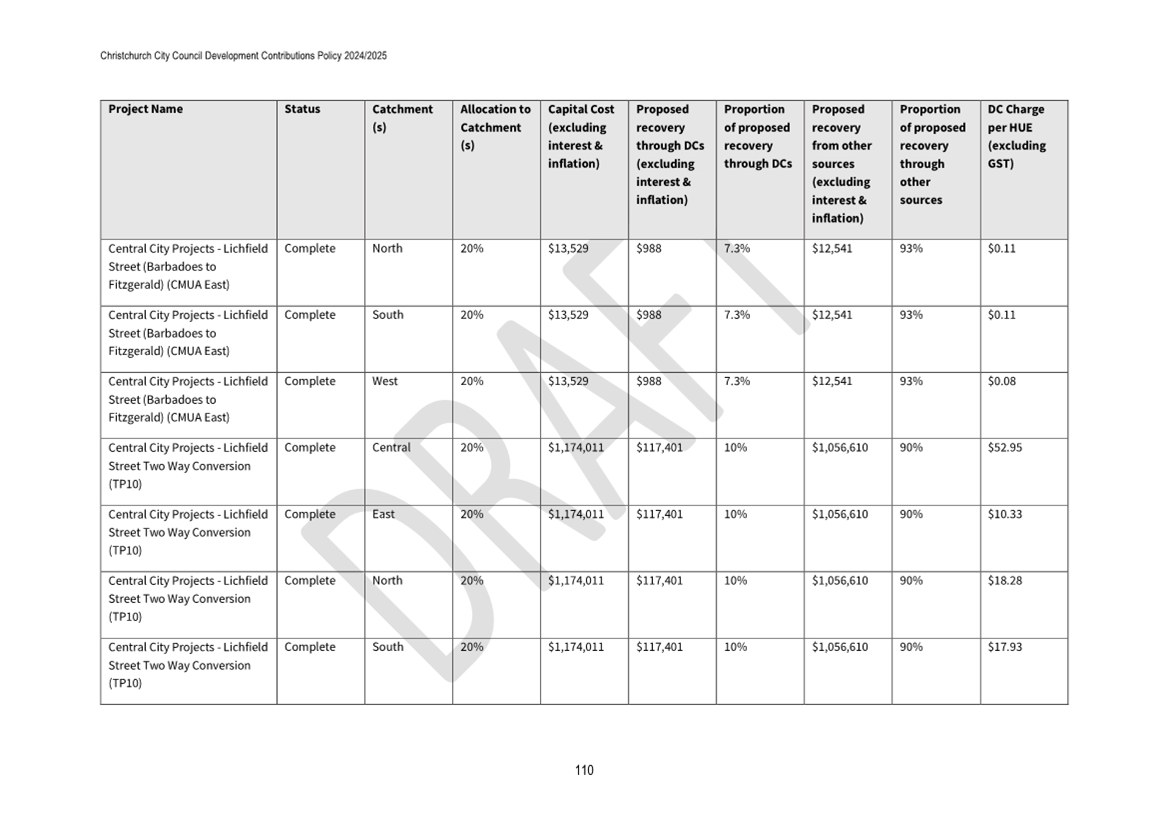

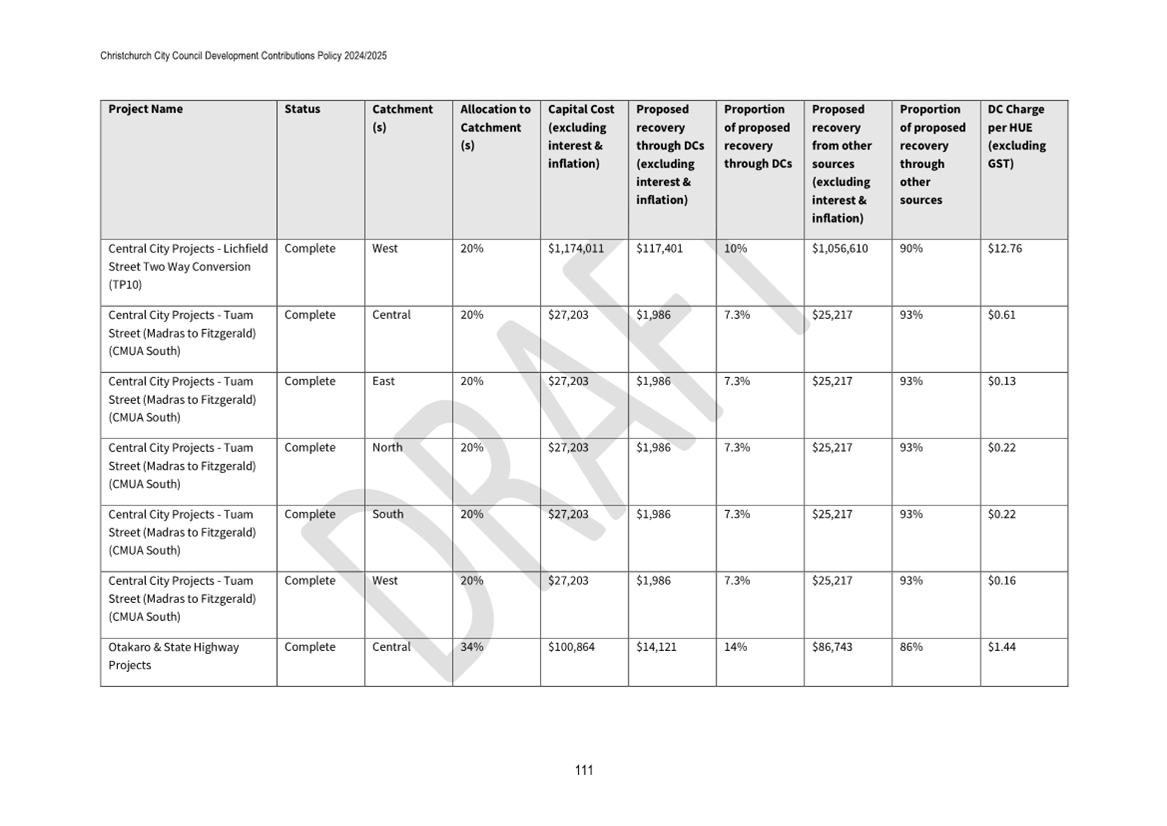

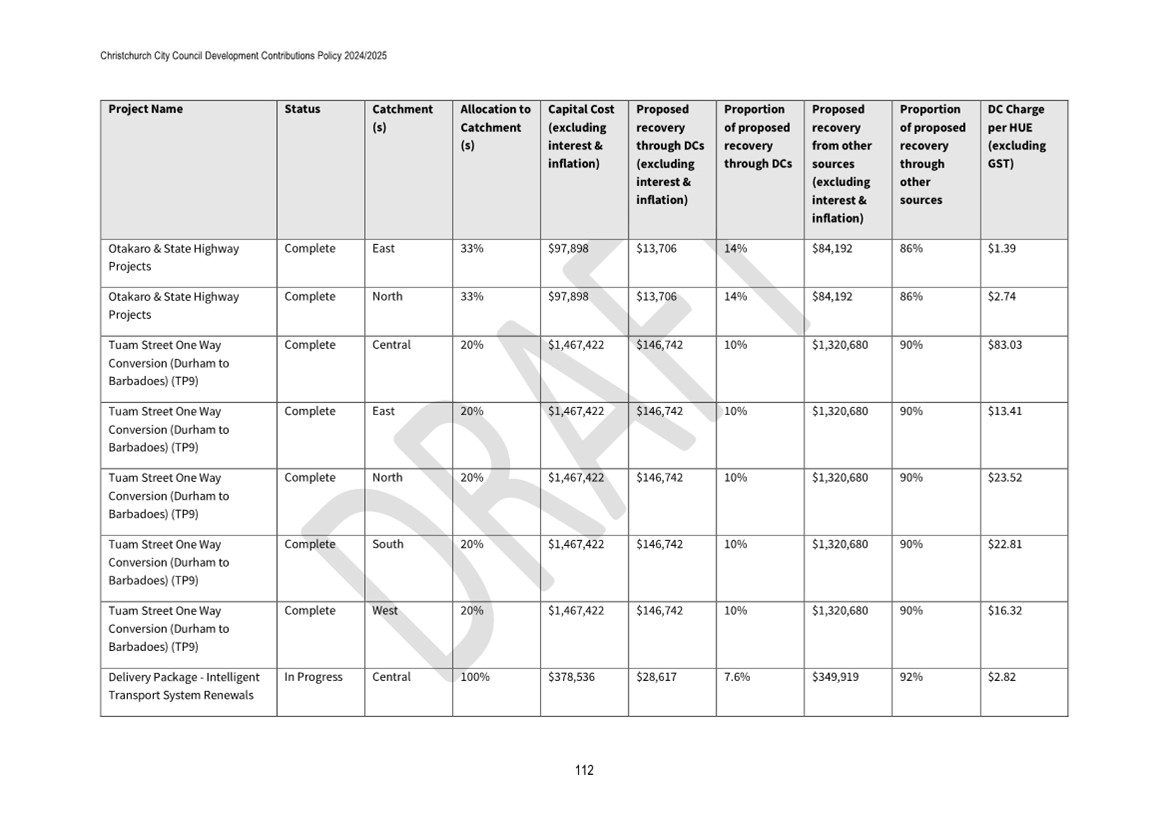

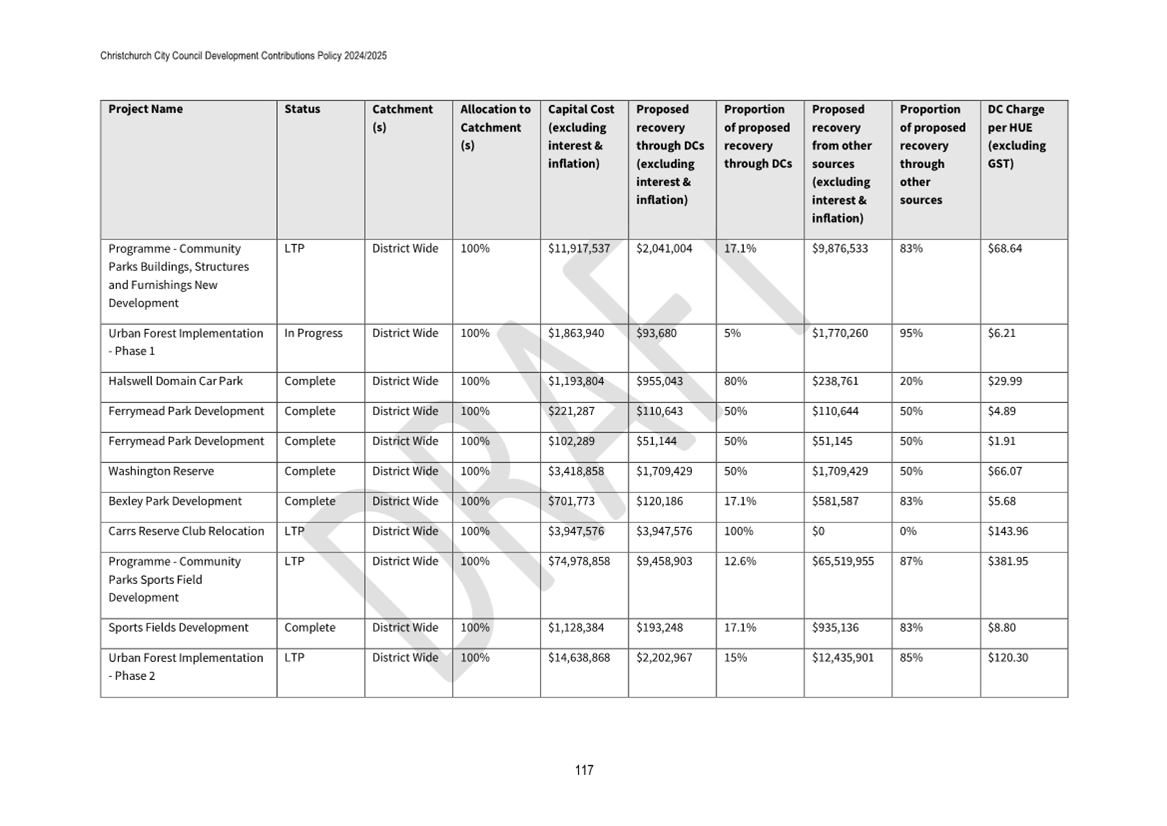

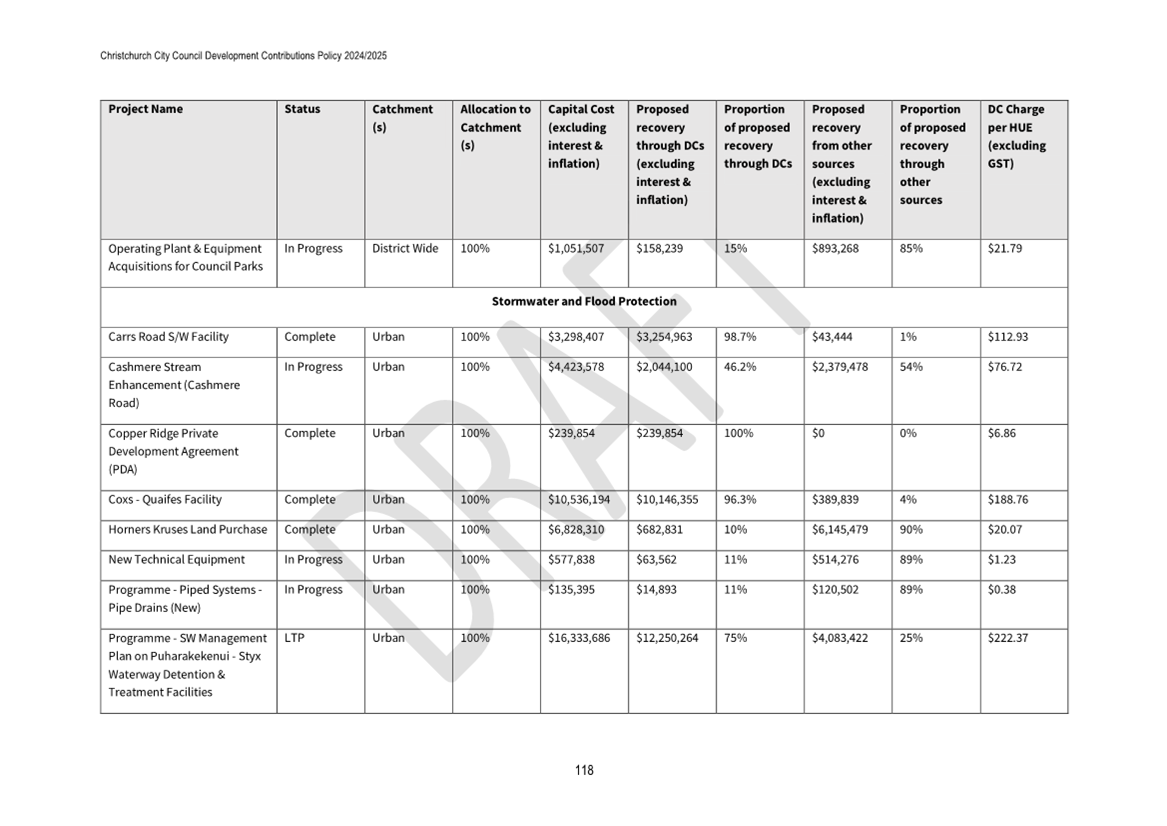

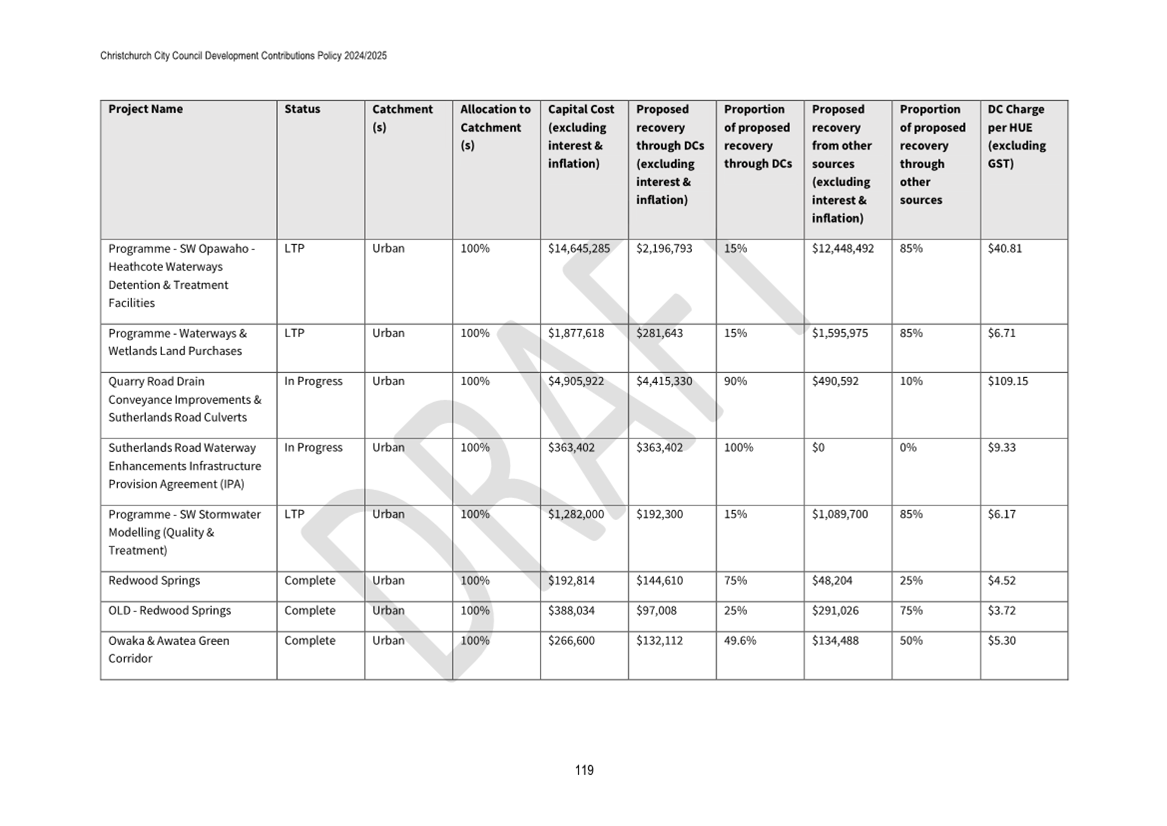

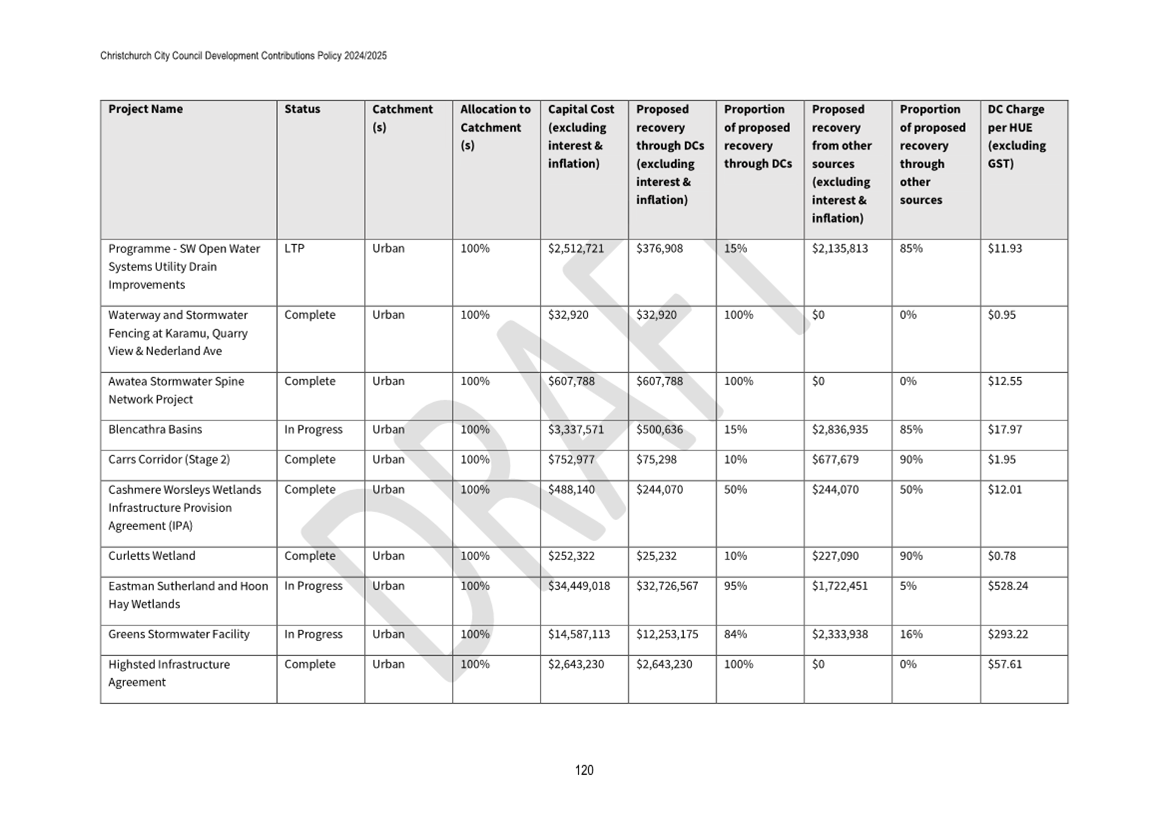

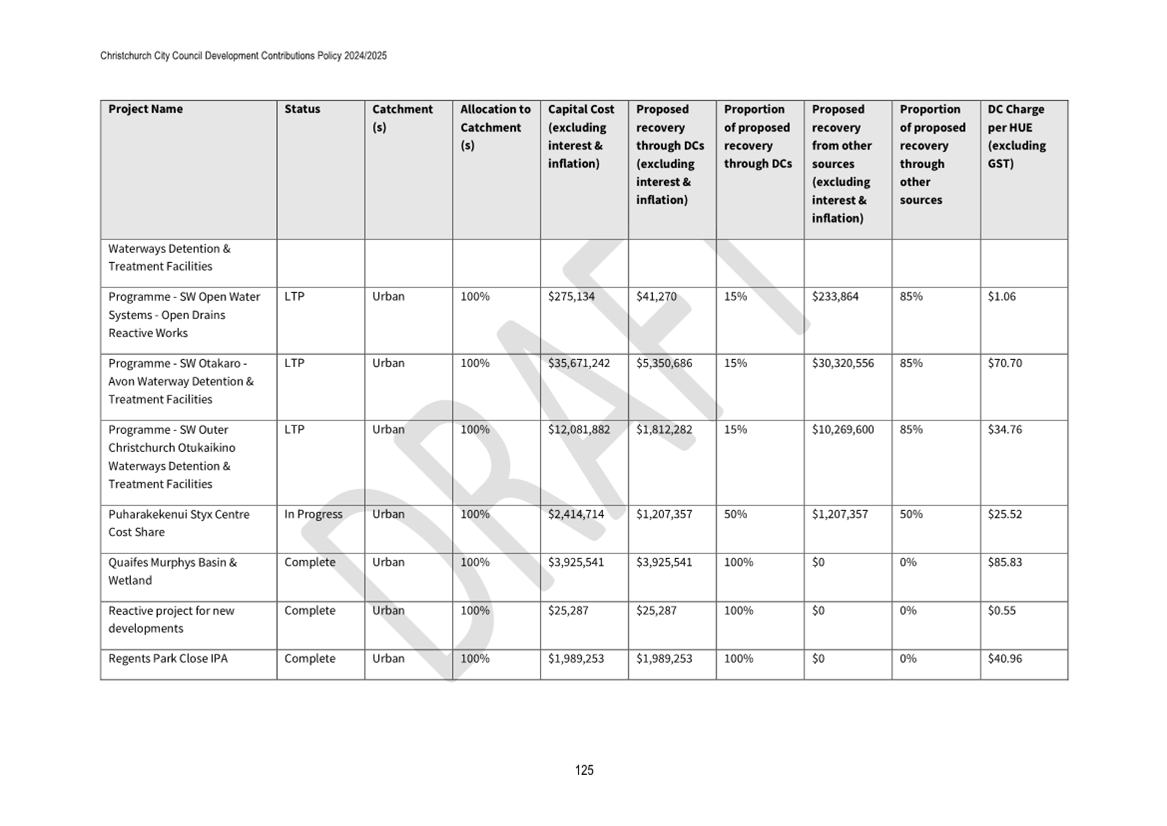

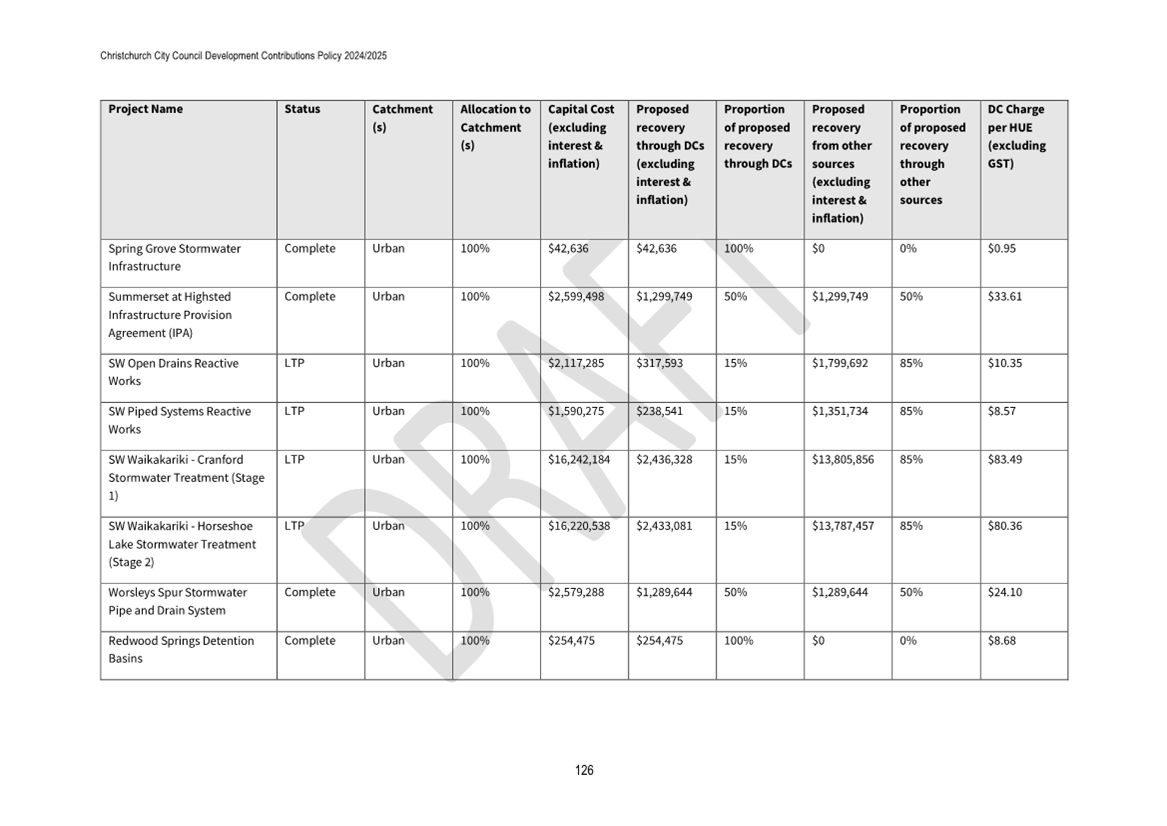

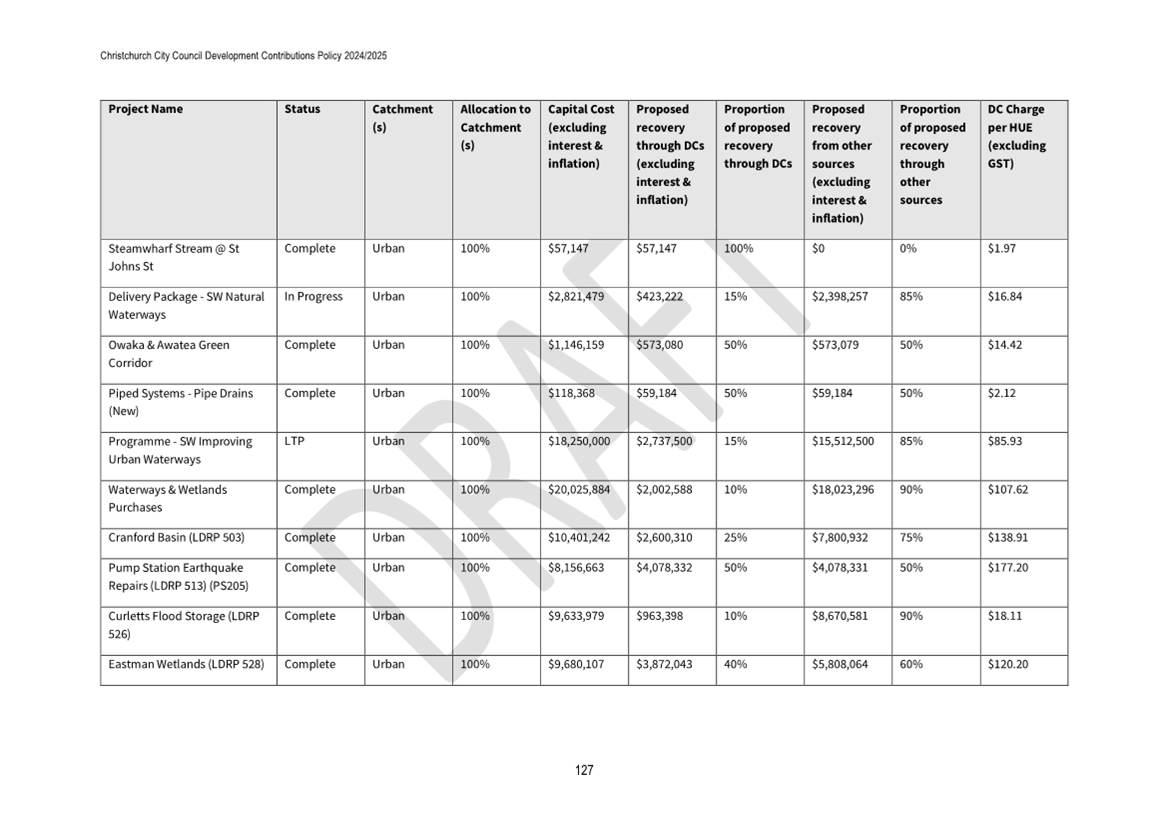

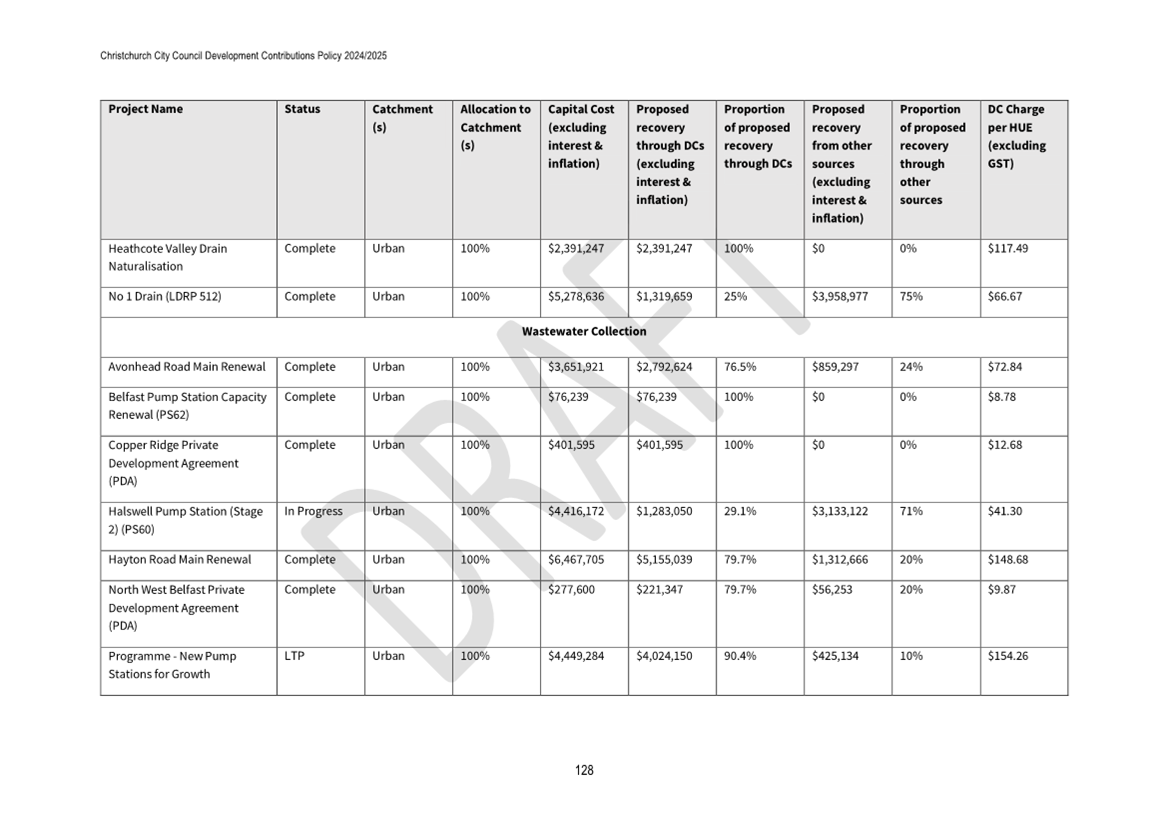

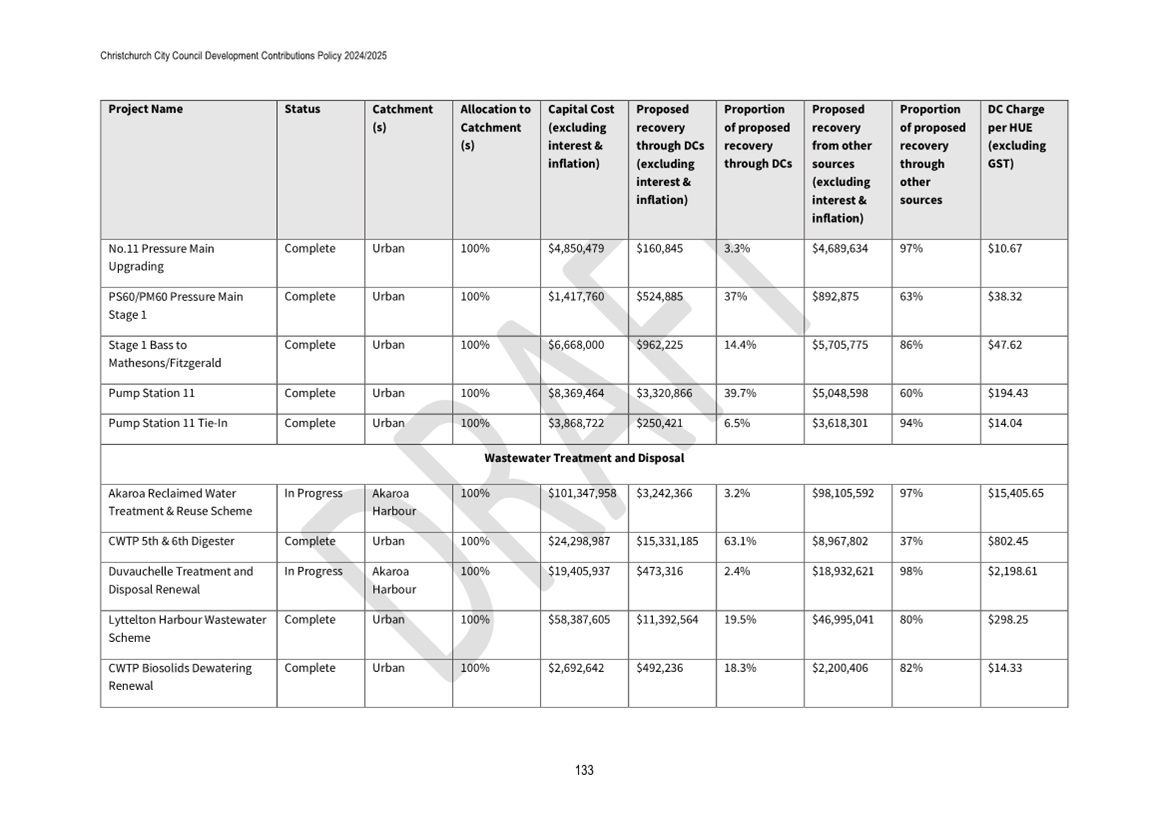

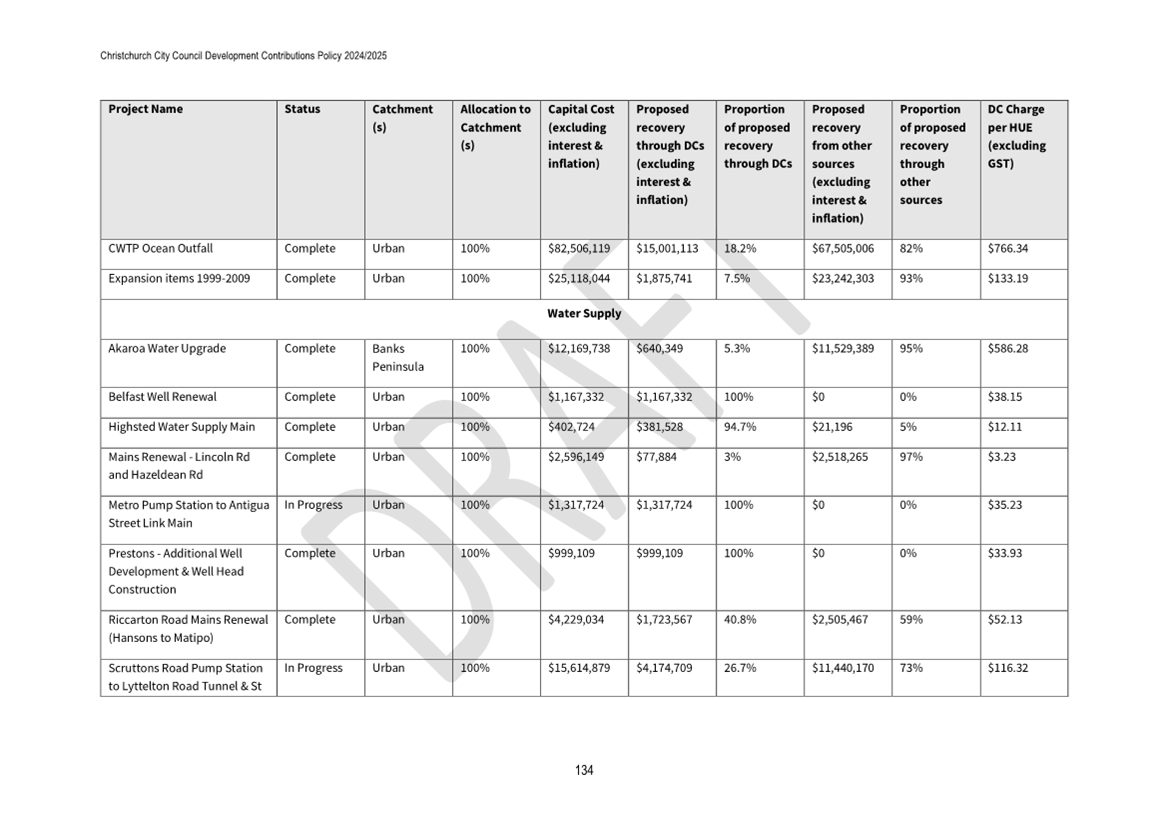

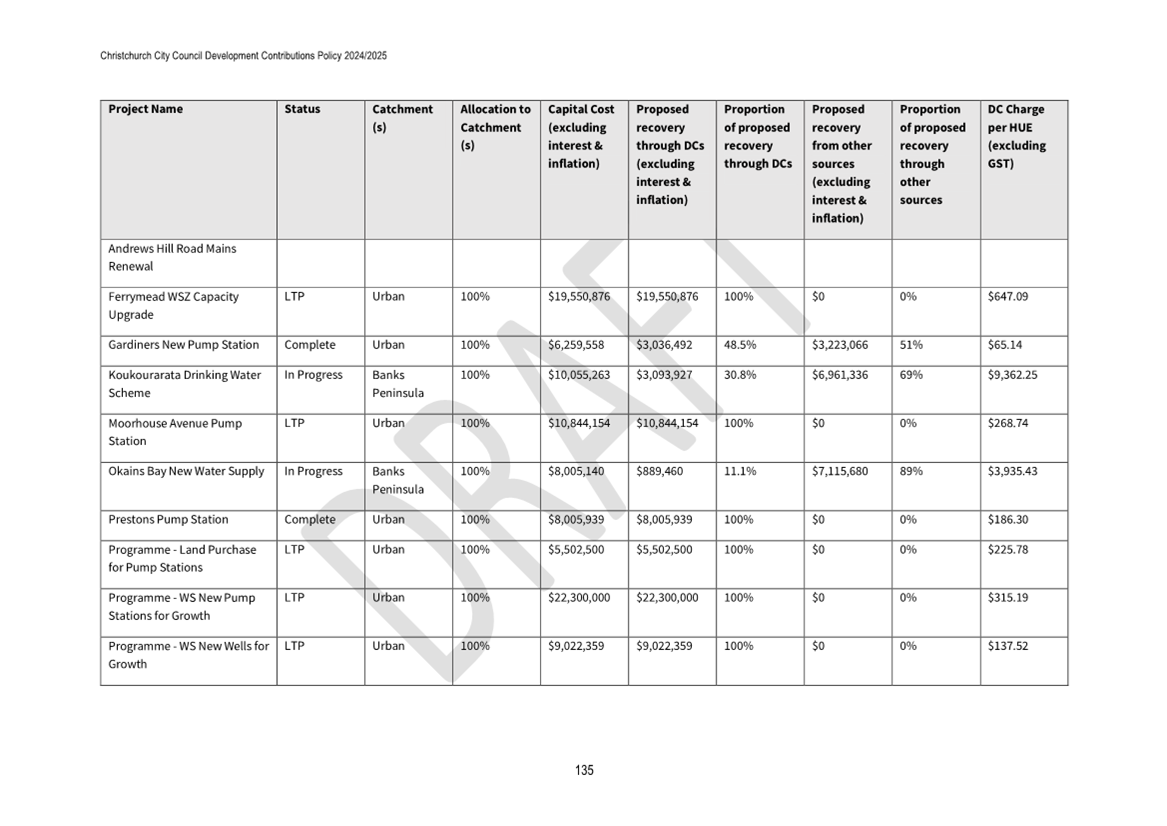

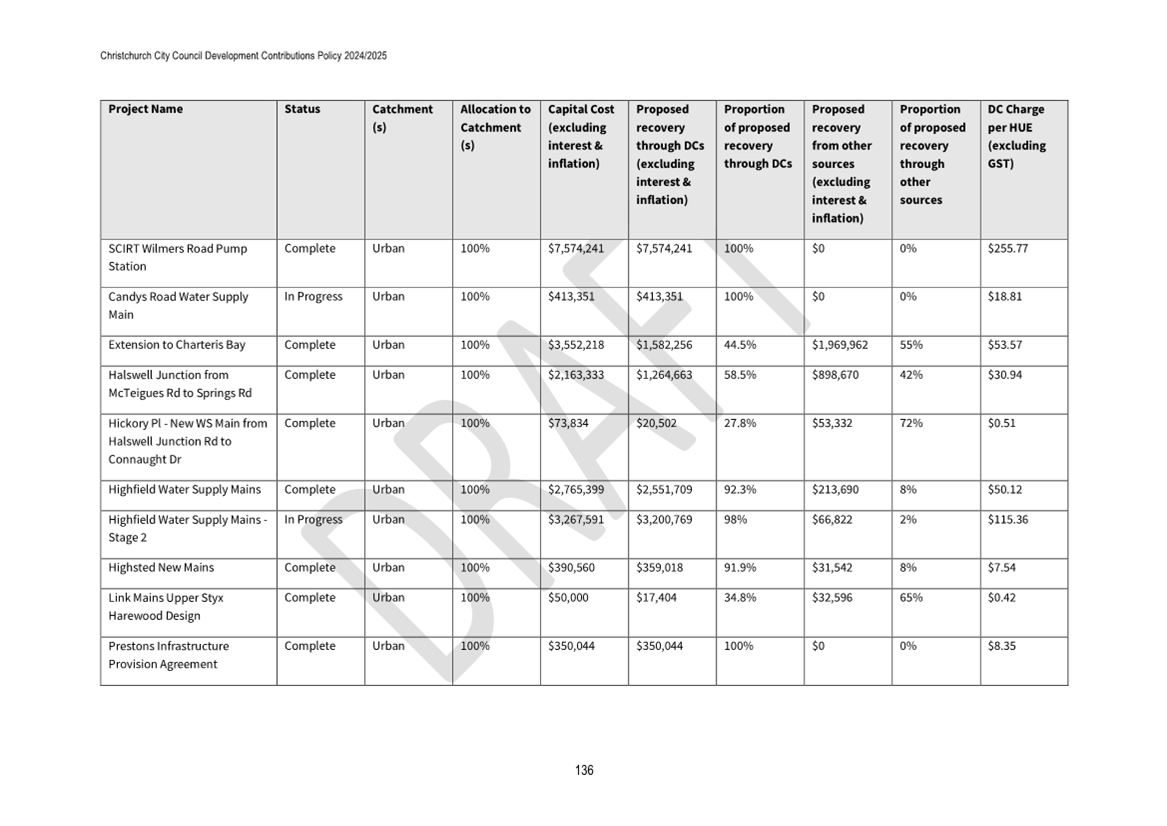

10. Draft Development Contributions Policy 2024

|

|

Reference Te Tohutoro:

|

24/628249

|

|

Responsible Officer(s) Te Pou Matua:

|

Ellen

Cavanagh, Senior Policy Analyst

|

|

Accountable ELT Member Pouwhakarae:

|

John

Higgins, General Manager Strategy, Planning & Regulatory Services

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report for the Finance and Performance Committee to resolve to

consult on the draft Development Contributions Policy.

1.2 The

Local Government Act 2002 (LGA) requires all local authorities to have a policy

on development contributions and financial contributions and to review it every

three years. As the Council’s policy was last adopted in 2021, it is due

for review this year.

2. Officer

Recommendations Ngā Tūtohu

That the Finance and

Performance Committee:

1. Receives the information in the Draft

Development Contributions Policy 2024 Report.

2. Approves the draft Development Contributions Policy 2024 (Attachment

A) for consultation in accordance with section 82 of the Local Government

Act 2002.

3. Agrees that prior to consultation commencing staff may make changes

to the draft Development Contributions Policy 2024 to correct minor drafting

errors.

4. Notes that the decision in this report is assessed as medium

significance based on the Christchurch City

Council’s Significance and Engagement Policy. The

level of significance was determined by consideration of the importance of the

policy to the wider community who are largely unaffected (low significance) and

to property developers of Christchurch district (medium significance) who are

directly affected through the requirement to pay development contributions.

3. Executive Summary Te Whakarāpopoto Matua

3.1 The

LGA requires all local authorities to have a policy on development

contributions and financial contributions. The Development Contributions Policy

(policy) must comply with the requirements of section 106 and sections 197AA to

211 of the LGA. This includes the policy being reviewed at least once every

three years using a consultation process that gives effect to section 82 of the

LGA.

3.2 The

Council’s policy was last reviewed in 2021 and is now due for review.

3.3 The

draft policy contains an updated schedule of capital projects (Schedule of

Assets) and schedule of charges alongside a number of proposed changes to the

policy detail. These policy changes are outlined in Attachment B to this

report. The new development contributions charges are outlined in Attachment

C.

3.4 Subject

to the Committee’s approval, consultation on the draft policy will run

from mid-January to mid-February 2025 with a Hearings Panel to follow.

4. Background/Context Te Horopaki

4.1 Development

contributions enable the Council to recover a fair share of the cost of

providing infrastructure to service growth development from those who benefit

from the provision of that investment. The Council has had a development

contributions policy since 2004 with this being the tenth review of the policy

over that time.

4.2 The

policy details the methodology used to establish development contribution

charges per household unit equivalent (HUE), the resulting cost of those

charges, the methodology used to assess a development for the level of

development contributions required and various process requirements associated

with operating a fair and consistent development contributions process.

4.3 Development

contribution charges are derived directly from the cost the Council incurs to

provide infrastructure to service growth development. The revenue is used to

pay down debt taken out to initially fund the investment in growth

infrastructure.

4.4 Development

contribution charges are calculated per HUE on a per project basis, by dividing

cost to deliver the growth component of an asset by the number of new or

additional households. Overall, development contribution charges have

increased for most parts of the city compared to the 2021 policy. This has been

caused by an increase in the cost to deliver infrastructure to service growth

and revised growth projections that indicate a slower rate of growth compared

to 2021.

4.5 The

charges by activity and catchment are outlined in Attachment C. This

attachment also provides an overview of how development contribution charges

have changed between the 2016, 2021 and 2024 (draft) policy.

4.6 The

policy has many discrete inputs, all of which must be reviewed as part of any policy

review process. These include residential growth model, business growth model,

transport growth model, capital expenditure programmes related to growth,

interest and inflation rate forecasts and reviews of the numerous methodologies

used as the basis for the calculation and assessment of development

contributions.

4.7 In

addition, this review process has included reviewing the use of catchments to

calculate and assess development contributions.

4.8 This

review has also been an opportunity to review the content and structure of the

policy to improve clarity and legibility. The specific policy changes are

outlined in section 5 of this report.

4.9 The

review has been overseen by a Steering Group and undertaken by a Working Group

comprised of relevant staff from across the Council.

4.10 The following related information session/workshops have taken place

for the members of the meeting:

|

Date

|

Subject

|

|

18 July 2023

|

Development Contributions Policy Review

|

|

28 November 2023

|

Development Contributions Policy Workshop

|

|

30 April 2024

|

Development Contributions Policy Workshop

|

|

13 August 2024

|

Council's Growth Model: Ōtautahi

Christchurch Planning Programme, Parks Network Planning, and Development

Contributions

|

|

29 October 2024

|

Development Contributions Policy

|

|

26 November 2024

|

Draft Development Contributions Policy

– Draft Charges

|

Options Considered Ngā

Kōwhiringa Whaiwhakaaro

4.11 Legislation

requires the policy to be reviewed every three years. On this basis, the

following reasonably practicable options were considered:

4.11.1 update the policy and undertake

consultation in accordance with section 82 of the LGA

4.11.2 only update the Schedule

of Assets and development contributions charges and undertake

consultation in accordance with section 82 of the LGA

4.12 The preferred

option is to update and improve the policy. Staff

consider that a full review to update the policy and undertake consultation

more closely complies with our legislative requirement and ensures development

contributions charges accurately reflects current capital costs. Updating only

the schedule of assets would be a missed opportunity to update the policy

detail.

Options Descriptions Ngā

Kōwhiringa

4.13 Preferred

Option: update the policy and undertake consultation

4.13.1 Option Description: This

option involves an update to the schedule of capital projects and charges as

well as changes to the policy framework. These changes are outlined in section

5 of this report.

4.13.2 Option Advantages

· Complies with legislative requirements and ensures development

contributions charges accurately reflects current capital costs required to

service growth development. It also provides an opportunity to make updates to

the policy provisions.

4.13.3 Option Disadvantages

· None. Legislation requires the review and requires consultation,

whether any changes are proposed or not.

4.14 Retain the

policy with no changes to policy framework, but update schedule of assets and

development contributions charges and consult.

4.14.1 Option Description: This

option would involve only updating the schedules of development contribution

charges and capital programme information (Schedule of Assets).

4.14.2 Option Advantages

· Fulfils minimum requirement that the policy be reviewed every three

years.

4.14.3 Option Disadvantages

· Legislation requires a review, and updates are required to the

policy. Not proposing any changes to the policy would be a missed opportunity

to make improvements to the policy.

5. Policy Detail

5.1 The

key proposed changes have been arrived at following assessment of options on

each issue. Attachment B provides an analysis of options considered and reasons

why those being proposed are the preferred options.

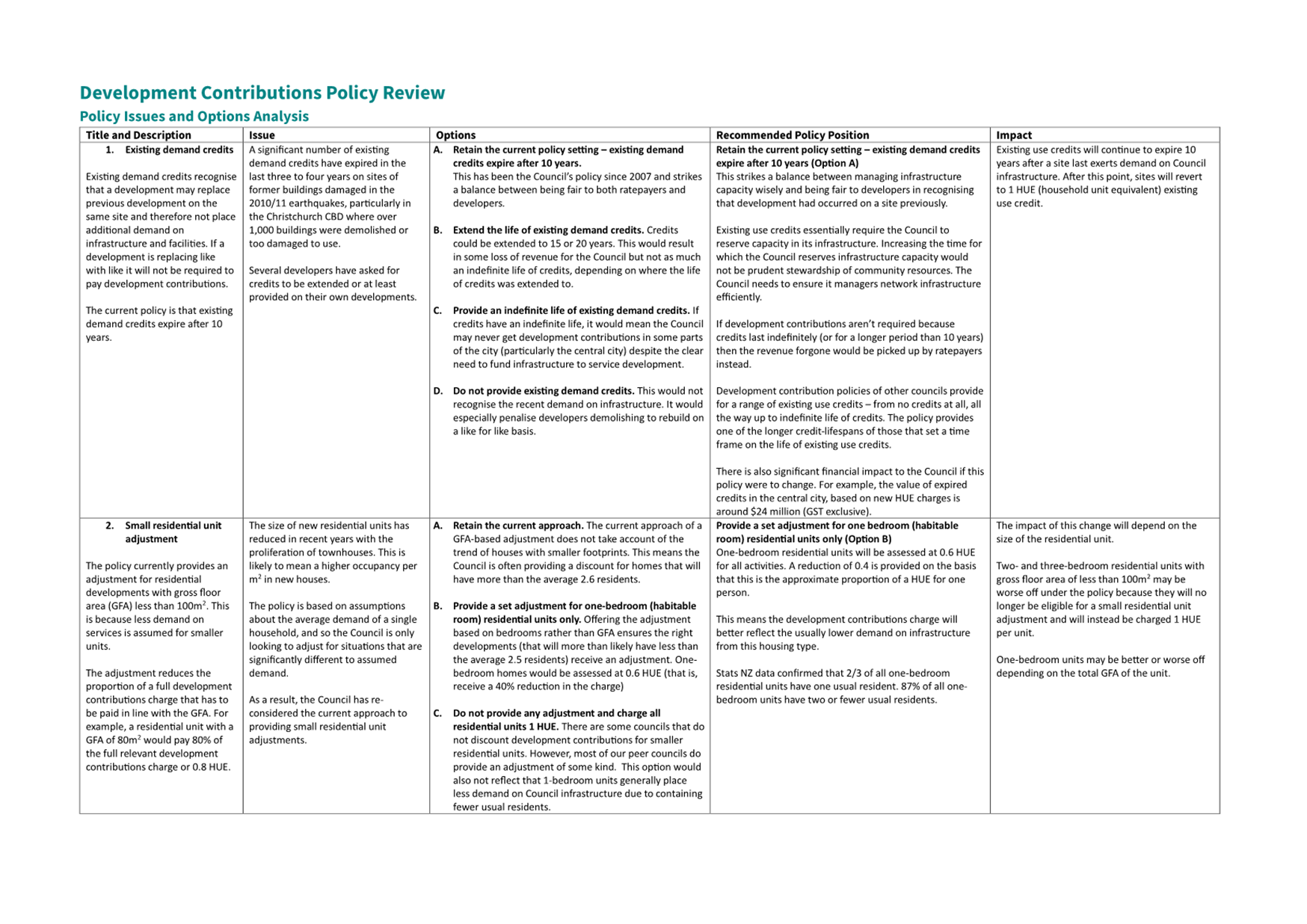

Life of

existing use credits

5.2 Issue:

The Council position has been to limit the life of existing use credits to

ten years from when the site last exerted demand on Council infrastructure.

Many credits have expired in the last three years on buildings and sites of

former buildings damaged in the 2010/11 earthquakes – particularly in the

Christchurch CBD where over 1000 buildings were demolished or too damaged to

use. This issue was considered as part of the 2021 policy review and staff have

reconsidered as part of this review.

5.3 Recommendation:

Retain the current policy setting, where existing demand credits

expire after 10 years. This strikes a balance between managing infrastructure

capacity wisely, being fair to ratepayers in that a liability to provide

infrastructure to service these lots is not in place forever and being fair to

developer in recognising that development has occurred on a site previously.

5.4 There

is also significant financial impact to the Council if this policy were to

change. The value of expired credits in the central city, based on new

household unit equivalent (HUE) charges is around $24 million (GST exclusive).

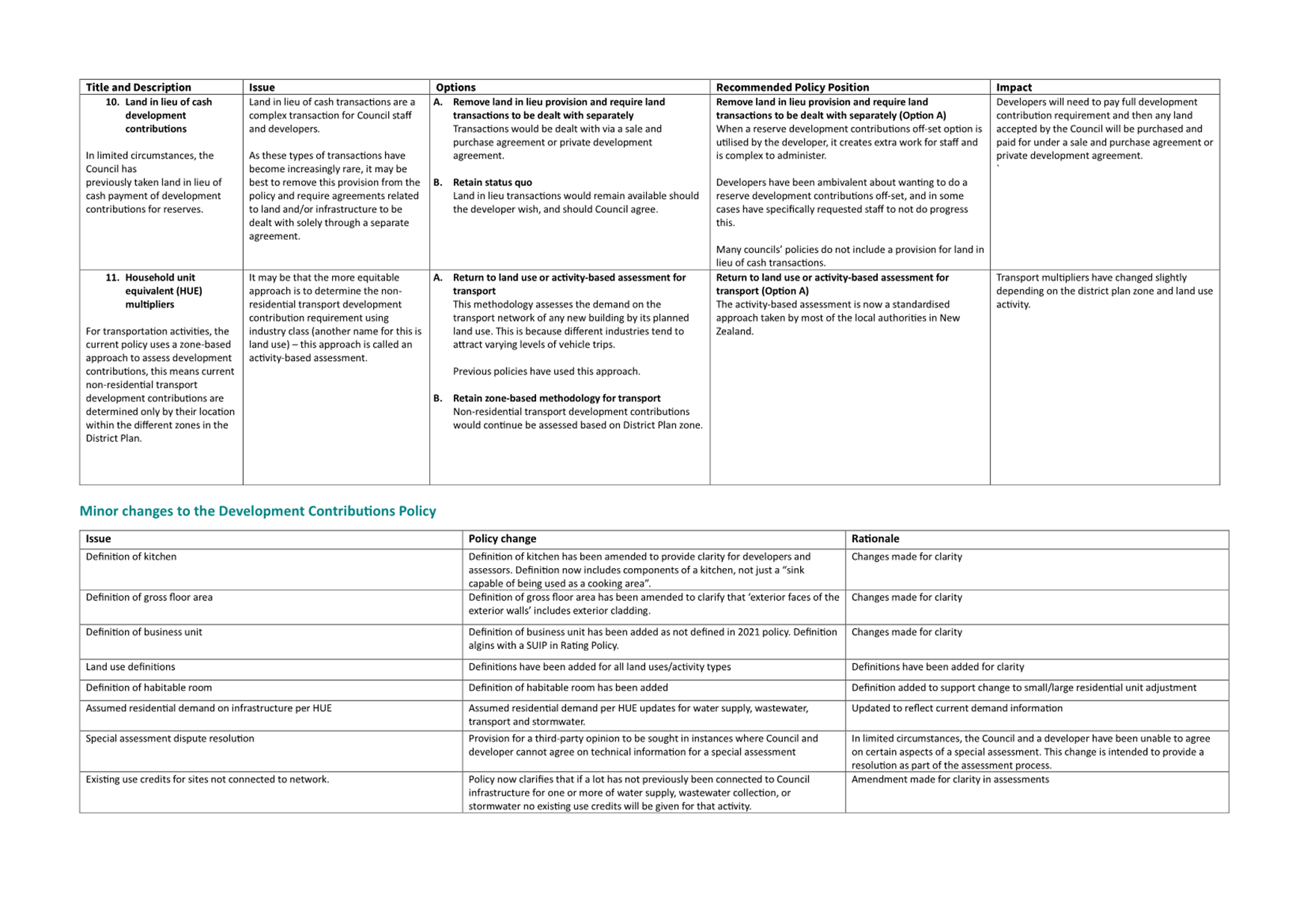

Small

residential unit adjustment

5.5 Issue: The Council currently reduces development

contributions charges for residential development for dwellings with a gross

floor area (GFA) less than 100m2 including garaging and potentially

habitable accessory buildings. The reduction is in line with the floor area,

for example a unit with 80m2 gross floor area is assessed at 0.8 HUE

or 80% of the full development contributions charge

5.6 In the last 10 years houses have got significantly smaller. In 2023,

45% of building consents in Christchurch were for homes less than 100m2,

24% were for less than 80m2 and 6% were for less than 60m2.This

means the Council is providing a discount for close to half of all new homes.

However, the policy is based on assumptions and averages and the Council is

only looking to adjust for situations that are significantly different to

assumed demand. Using GFA is no longer an accurate reflection of the demand a residential

unit places on Council infrastructure.

5.7 Recommendation: Staff recommend moving

to a residential unit adjustment based on bedrooms and keeping a small unit

adjustment for one-bedroom homes. This will ensure that the Council is only

making adjustments for developments that fall outside the assumptions built

into the policy.

5.8 Data from Statistics New Zealand confirms that 66% of one-bedroom residential

units have one person living in them and 87% of have two or fewer. The average

household is 2.6 people, so it is reasonable to assume these homes have half

the assumed demand of what is built into the policy.

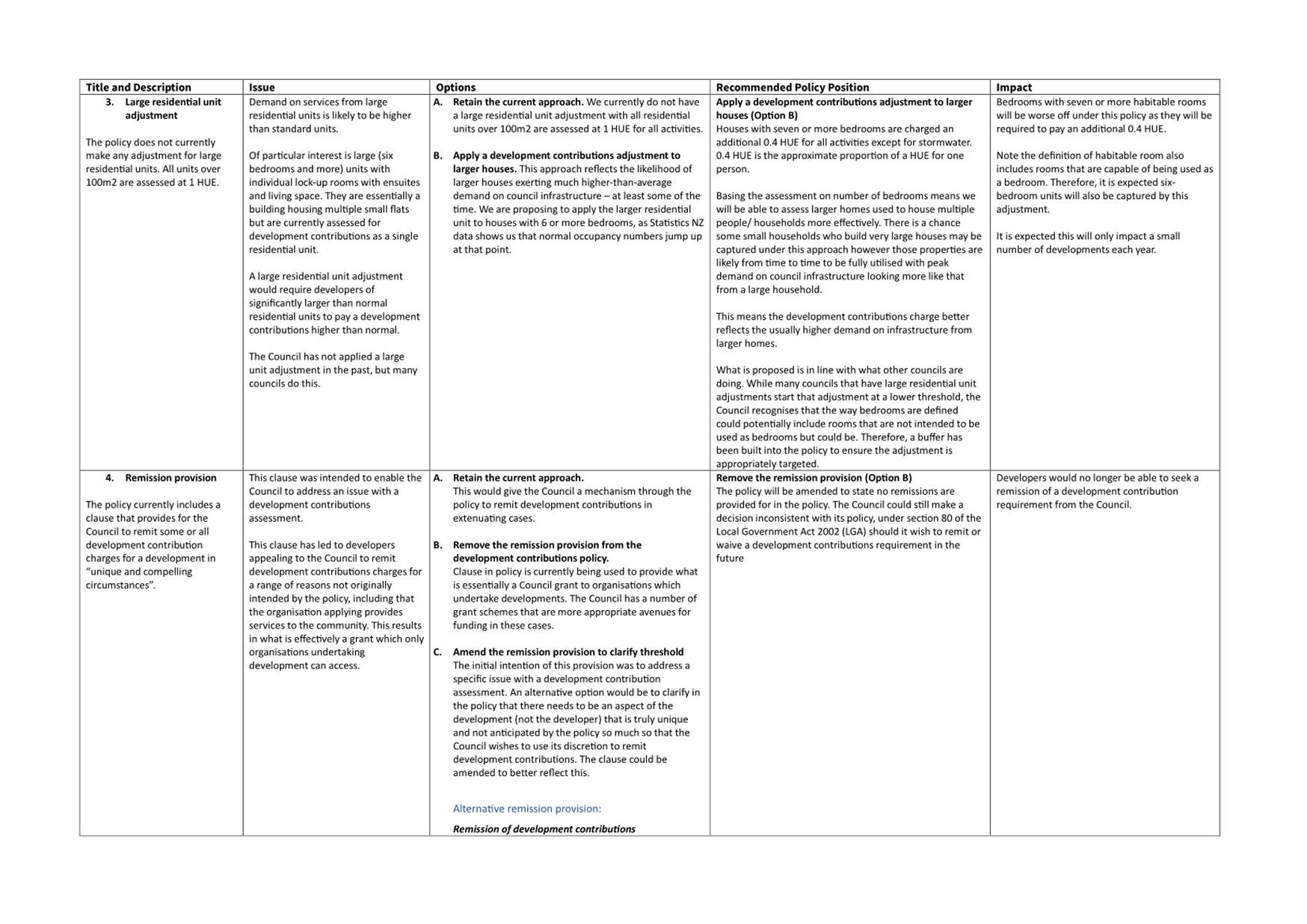

Large

residential unit adjustment

5.9 Issue: The

policy does not currently have a provision relating to large residential units.

Many councils’ policies have a large residential unit adjustment on the

basis that the greater the number of bedrooms in a residential

unit the more usual residents it likely has.

5.10 The Council is noticing an increasing

number of multiple tenancy housing developments with lock-up rooms with an

ensuite and shared kitchen lounge. Under current policy

provisions, there are currently assessed as a single household unit.

5.11 Recommendation: Staff

recommend providing a large residential unit adjustment. Developments with

seven or more bedrooms assessed at 1.4 HUE. This means the

development contribution charge better reflects the usually higher demand on

infrastructure from larger homes.

5.12 While many

councils that have large residential unit adjustments start their adjustment at

a lower threshold, the Council recognises that the way bedrooms are defined

could potentially include rooms that are not intended to be used as bedrooms

but could be. Therefore, a buffer has been built into the policy to ensure the

adjustment is appropriately targeted.

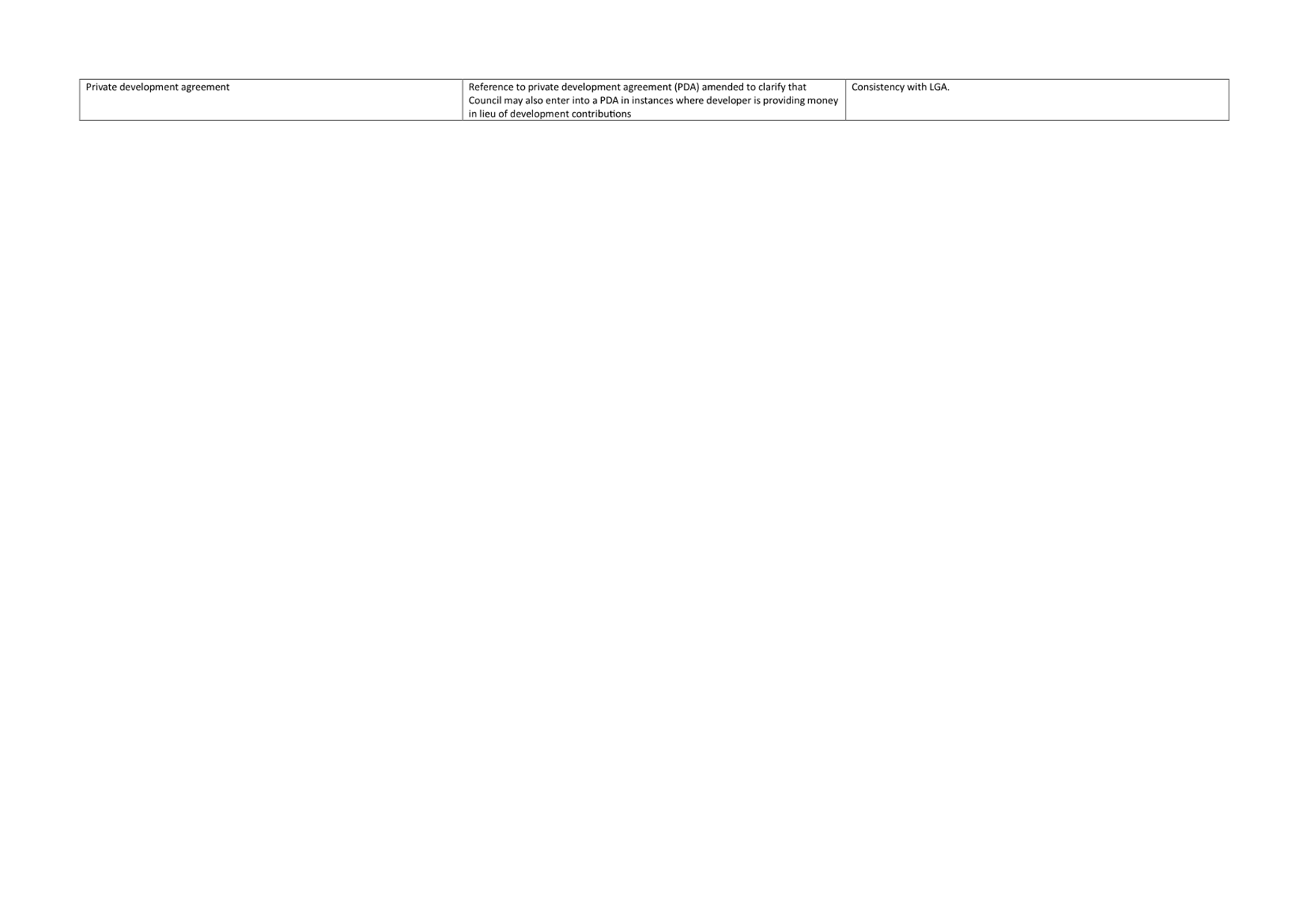

Remission

provision

5.13 Issue: The

policy currently includes a clause that provides for the Council to remit some

or all development contribution charges for a development in “unique and

compelling circumstance”. The original intent of this clause was

to allow for the Council to address a matter directly associated with the development

contributions charge. The clause is being used more widely

with developers appealing to the Council to remit development contributions

charges for a range of reasons including that the organisation applying

provides services to the community.

5.14 Recommendation:

The remission provision has been removed from the policy and replace with a

statement that the policy does not provide for remissions. The Council could

still opt to make decisions in certain circumstances that are inconsistent with

the Council’s policy, under section 80 of the LGA. Staff propose to

include a specific question on this in the consultation.

5.15 An alternative remission

provision has also been drafted and is included in Attachment B. The

alternative clause clarifies that it is the development itself (not the

developer or future occupier of the site) that must be unique and that the

development must be sufficiently distinct from other developments that

remitting a development contribution requirement does not create a new

precedent. Staff will include this as part of community consultation.

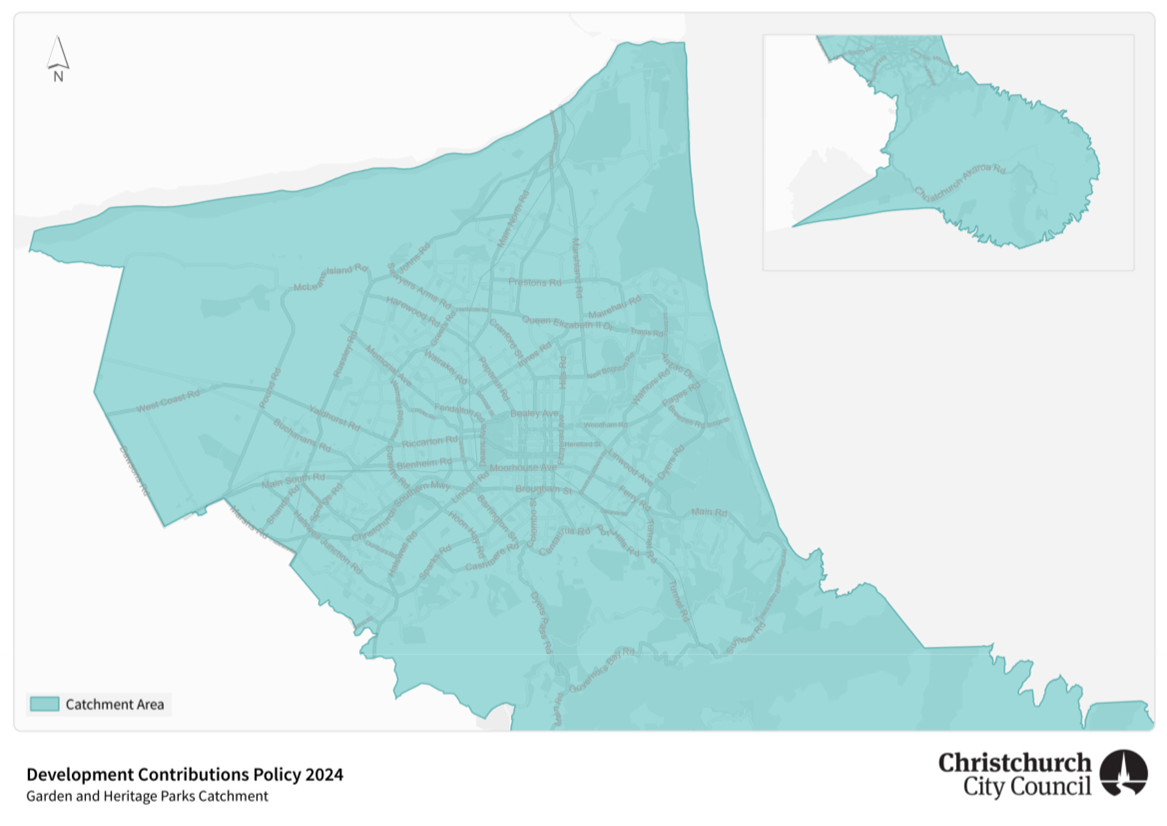

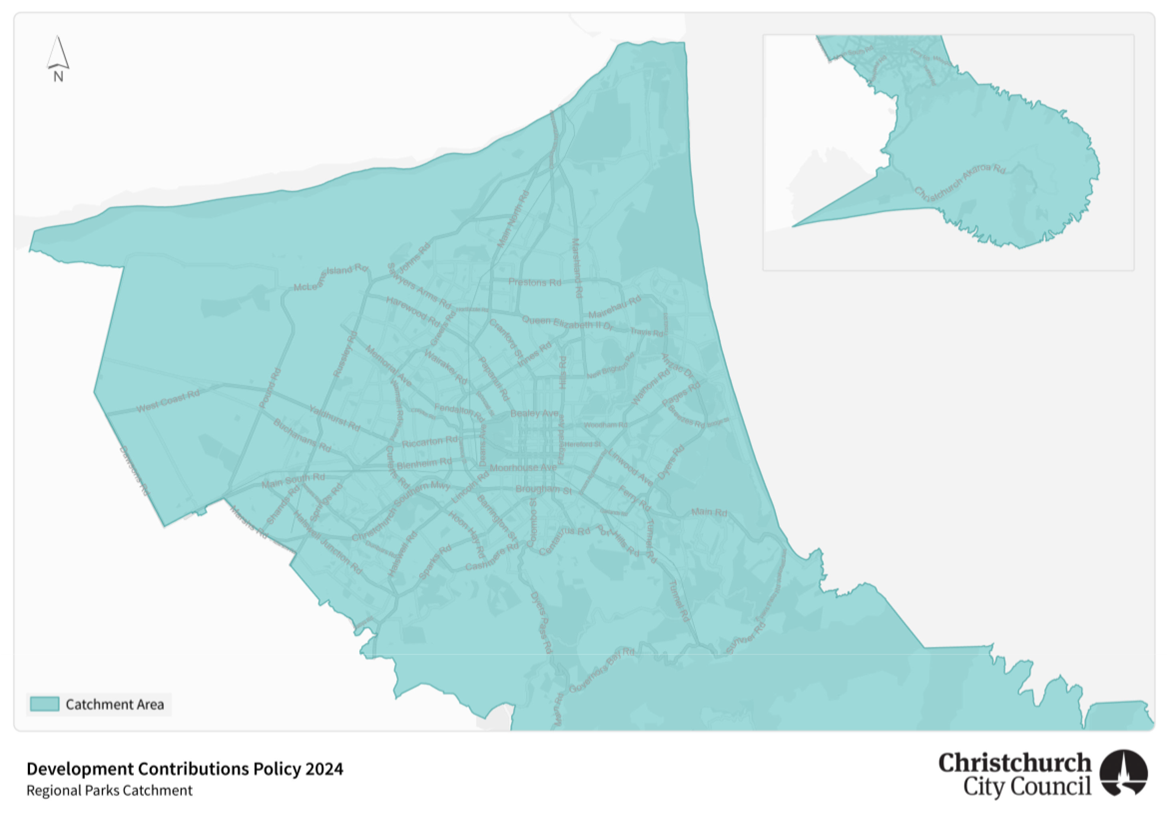

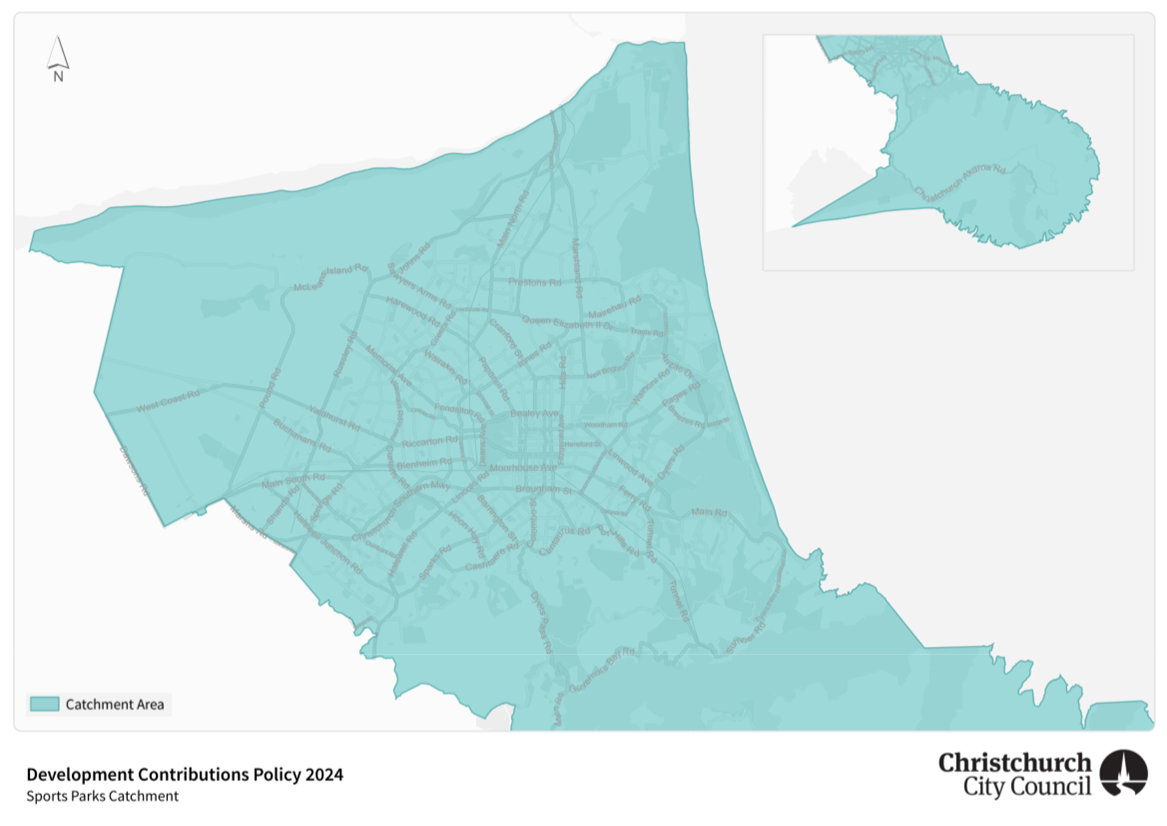

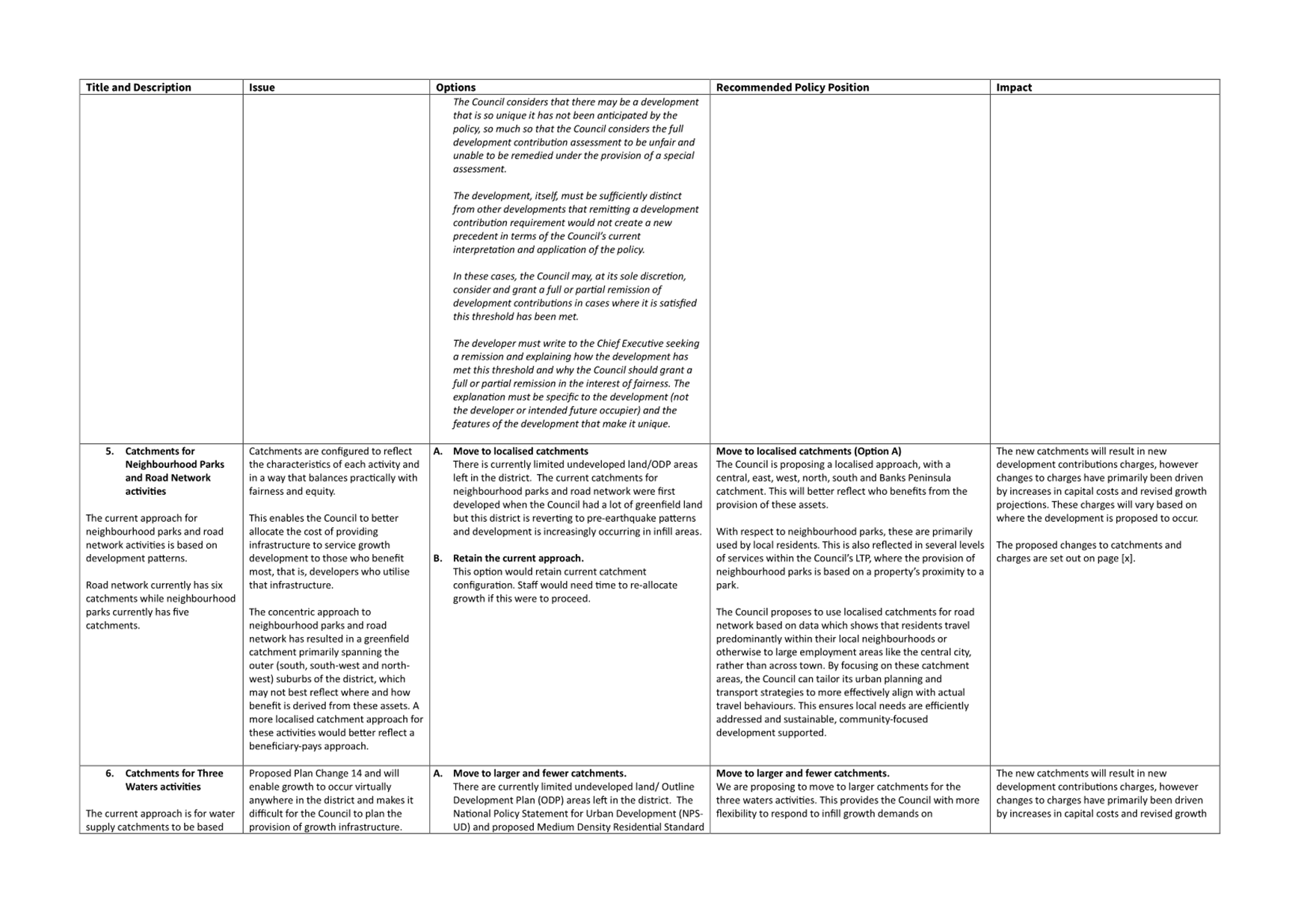

Catchments

for road network and neighbourhood parks activities

5.16 Issue:

The concentric approach the Council currently takes for neighbourhood parks

and road network has resulted in a greenfield catchment primarily spanning the

outer (south, south-west and north-west) suburbs of the district. These

catchments were first developed when the Council had a lot of greenfield land but

as Christchurch reverts to pre-earthquake patterns, development is increasingly

occurring in infill areas there is less rationale for a greenfield catchment.

5.17 Concentric

catchments means that it is possible developments are currently contributing to

the provision of parks and roads that are not necessarily local to the

neighbourhood where the development is occurring. The catchments could

be better configured to ensure a development contributions for neighbourhood

parks and roads are paid for by developments that most often use and benefit

from them.

5.18 Recommendation: Staff propose to move to more localised catchments for

neighbourhood parks and road network. This will better reflect who benefits

from the provision of these assets.

5.19 With respect to neighbourhood

parks, these are primarily used by local residents. This is also reflected in

several levels of services within the Council’s (Long

Term Plan) LTP, where the provision of neighbourhood parks is based on a

property’s proximity to a park.

5.20 The Council proposes to use

localised catchments for road network based on data which shows that residents

travel predominantly within their local neighbourhoods or otherwise to large

employment areas like the central city, rather than across town. By focusing on

these catchment areas, urban planning and transport strategies can be tailored

to align more effectively with actual travel behaviours. This ensures the

Council continues to address local needs efficiently and support sustainable,

community-focused development.

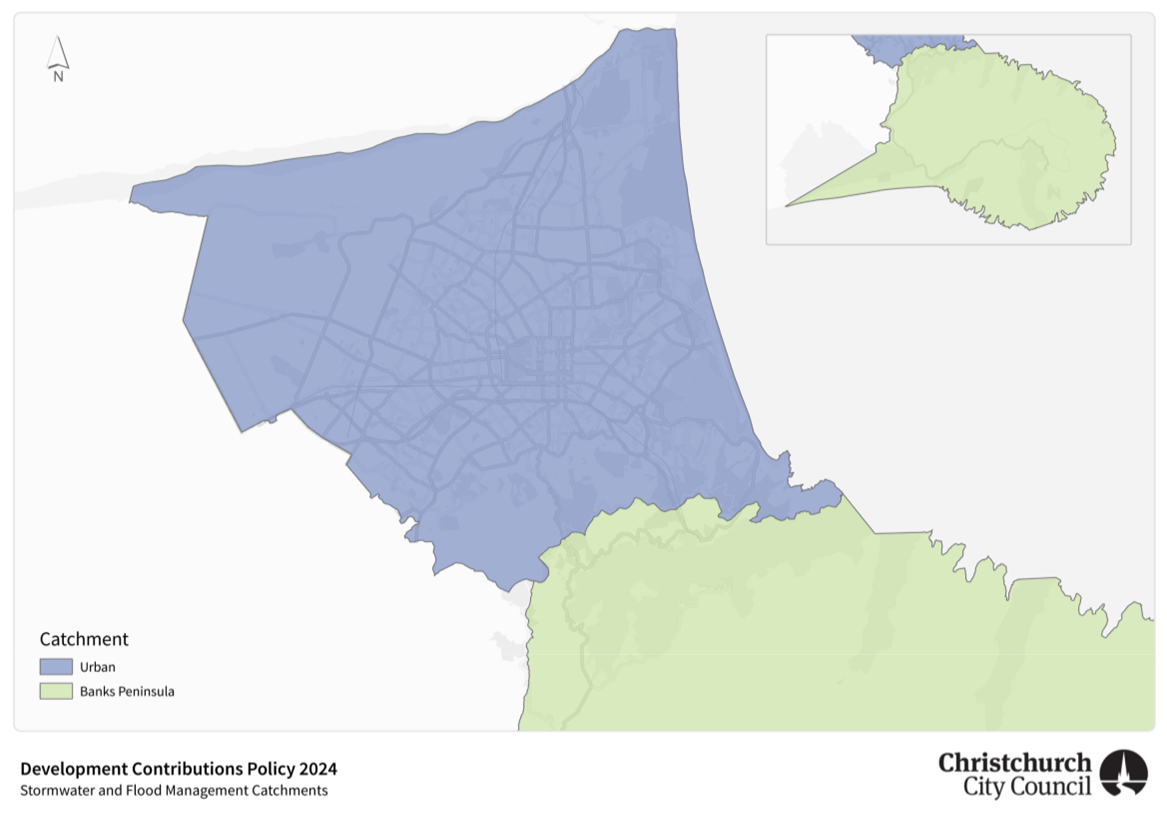

Catchments

for three waters activities

5.21 Issue:

Proposed Plan Change 14 and National Policy Statement on Urban Development (NPS-UD)

will enable growth to occur virtually anywhere in the district and makes it

difficult for the Council to plan the provision of growth infrastructure. The

Council requires a flexible whole of city response to three waters

infrastructure requirements to service growth which the current catchments do

not support. The number of catchments that we currently have is also

administratively complex.

5.22 Recommendation: Staff propose

return to larger, fewer catchments for water wastewater and stormwater, which

will also better reflect the integrated nature of the Council’s approach

to the delivery of these assets. This is administratively simpler and reflects

the Council’s integrated delivery of three waters services. Furthermore, because infrastructure plans are not fully aligned with

the LTP funding period, there may be misalignment between LTP provision and the

development triggering the required upgrades. This approach will allow the

Council to be more flexible in responding to growth – particularly where

there is uncertainty with where that growth with occur.

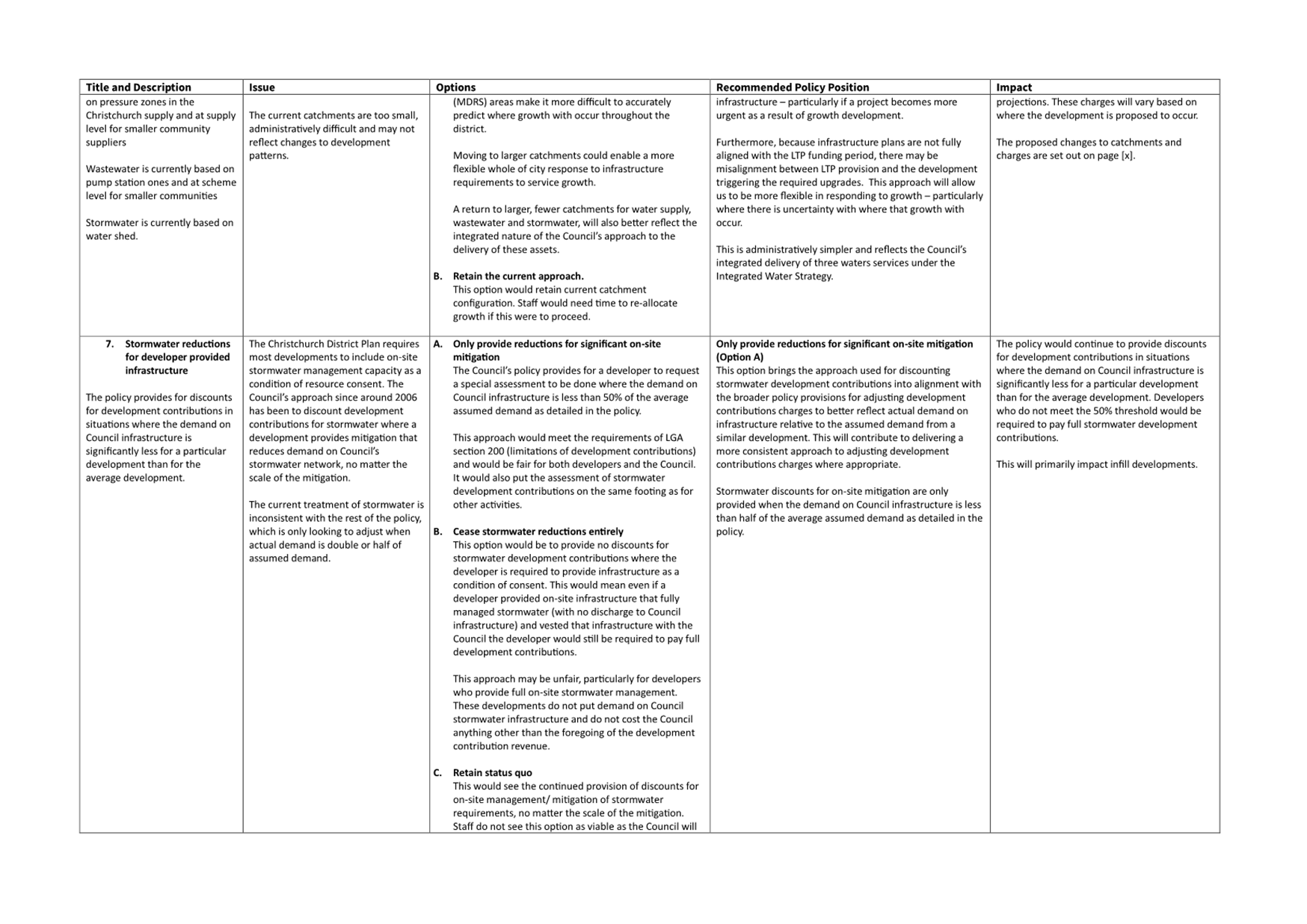

Stormwater

reductions for developer provided infrastructure

5.23 Issue:

The Council’s policy provides for discounts for development contributions

in situations where the demand on Council infrastructure is significantly less

for a particular development than for the average development. The Christchurch

District Plan requires most developments to include on-site stormwater

management capacity as a condition of resource consent.

5.24 The

Council’s approach since around 2006 has been to discount development

contributions for stormwater where a development provides mitigation that

reduces demand on Council’s stormwater network. However, this is

inconsistent with the rest of the policy, which is to only provide adjustments

when actual demand is double or half of assumed demand.

5.25 Recommendation: Stormwater

discounts for on-site mitigation are only provided when the

demand on Council infrastructure is less than half of the average assumed

demand as detailed in the policy. This would see relatively minor adjustments

(such as for the installation of a rainwater tank) cease.

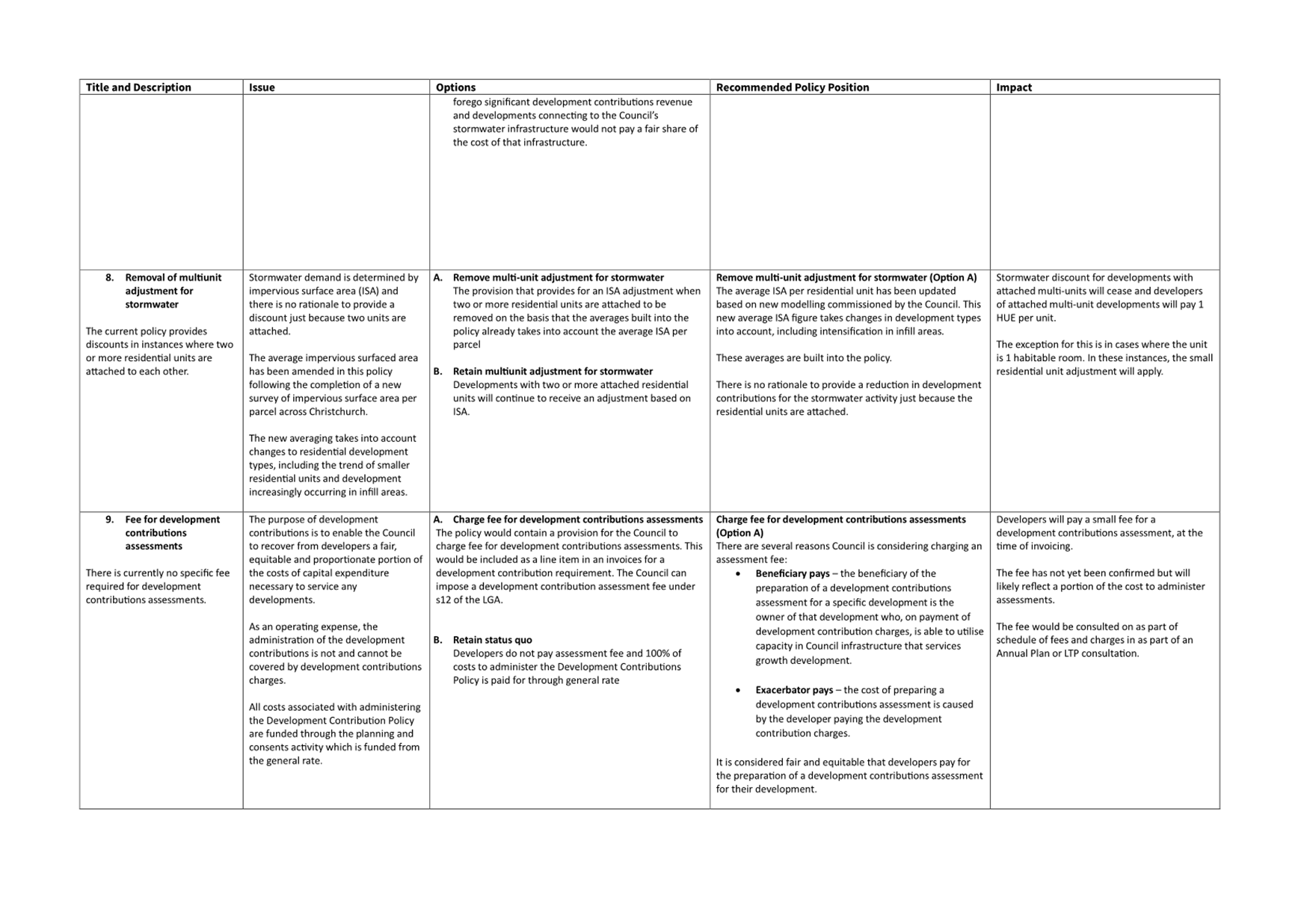

Multi-unit stormwater

adjustments

5.26 Issue: The current policy

provides discounts in instances where two or more residential units are

attached to each other. Stormwater demand is determined by impervious surface

area and there is no rationale to provide a discount just because two units are

attached.

5.27 The average impervious surfaced

area has been amended in this policy following the completion of a new survey

of impervious surface area per parcel across Christchurch. The new averaging

takes into account changes to residential development types, including the

trend of smaller residential units and development increasingly occurring in

infill areas.

5.28 Recommendation: Stormwater

discount for developments with attached multi-units will cease on this basis

that the averages built into the policy already take into account smaller

residential units and because impervious surface area determines demand for

stormwater activity,

Fee for

development contributions assessments

5.29 Issue: Ratepayers current fund the development contribution assessment

function via the general rate.

5.30 Recommendation: Provision for the Council to charge fee for development

contributions assessment. It is fair that the cost of

preparing a development contributions assessment is funded by the developer because

they both benefit from the assessment of their development and cause the

assessment to be required through submitting their development for consent. The

exact charge will be consulted on separately.

6. Financial Implications Ngā Hīraunga Rauemi

Capex/Opex Ngā Utu Whakahaere

6.1 Cost

to Implement – The cost of preparing the draft policy and community

engagement is funded through existing operational budgets. This work has been

undertaken over more than one year and is funded as a general cost of business

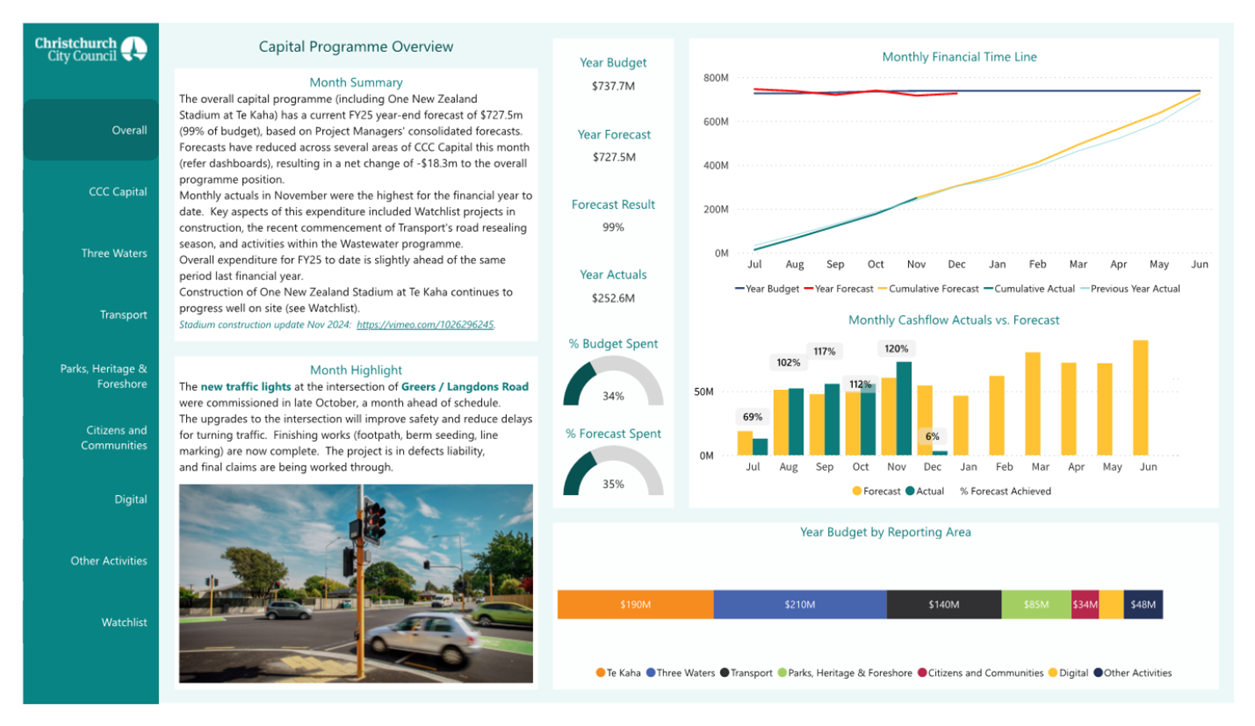

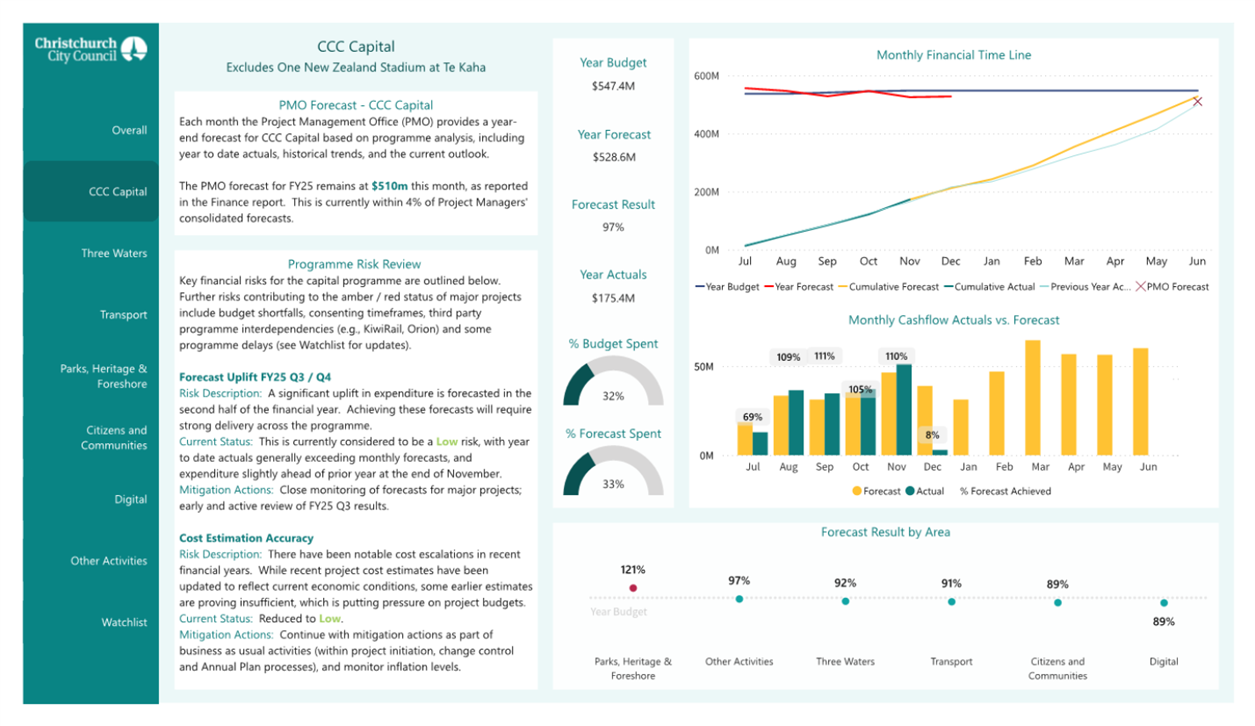

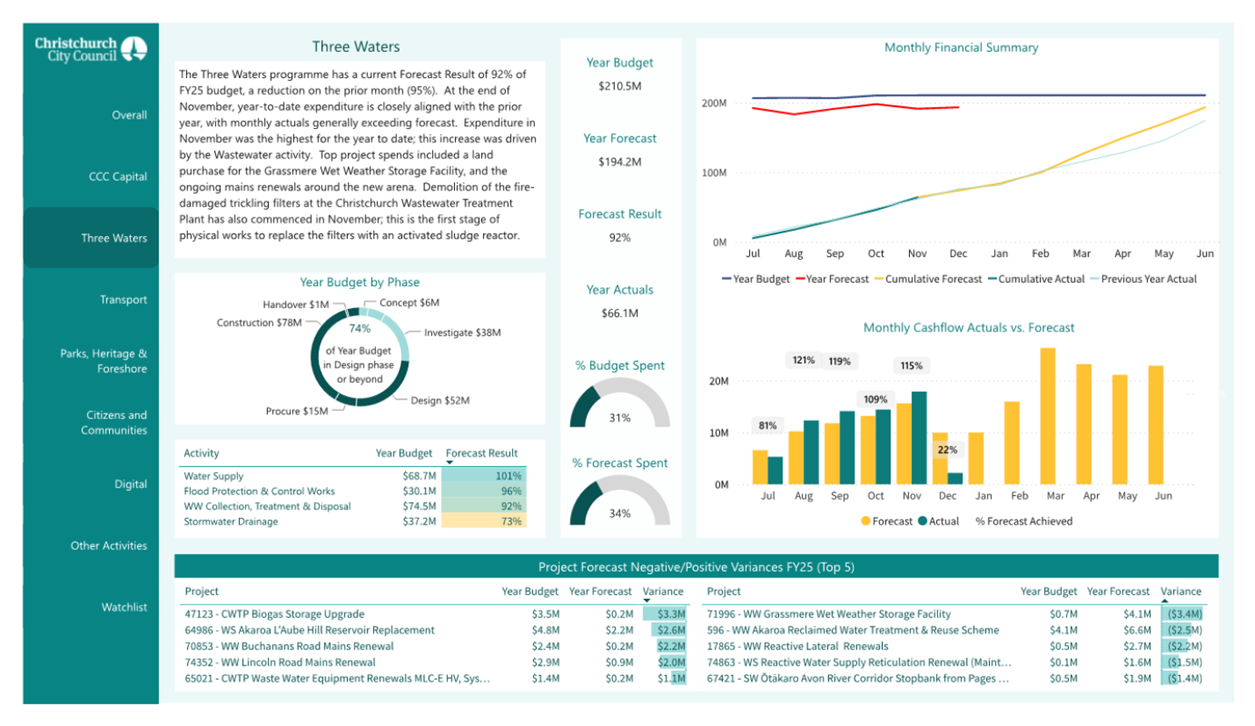

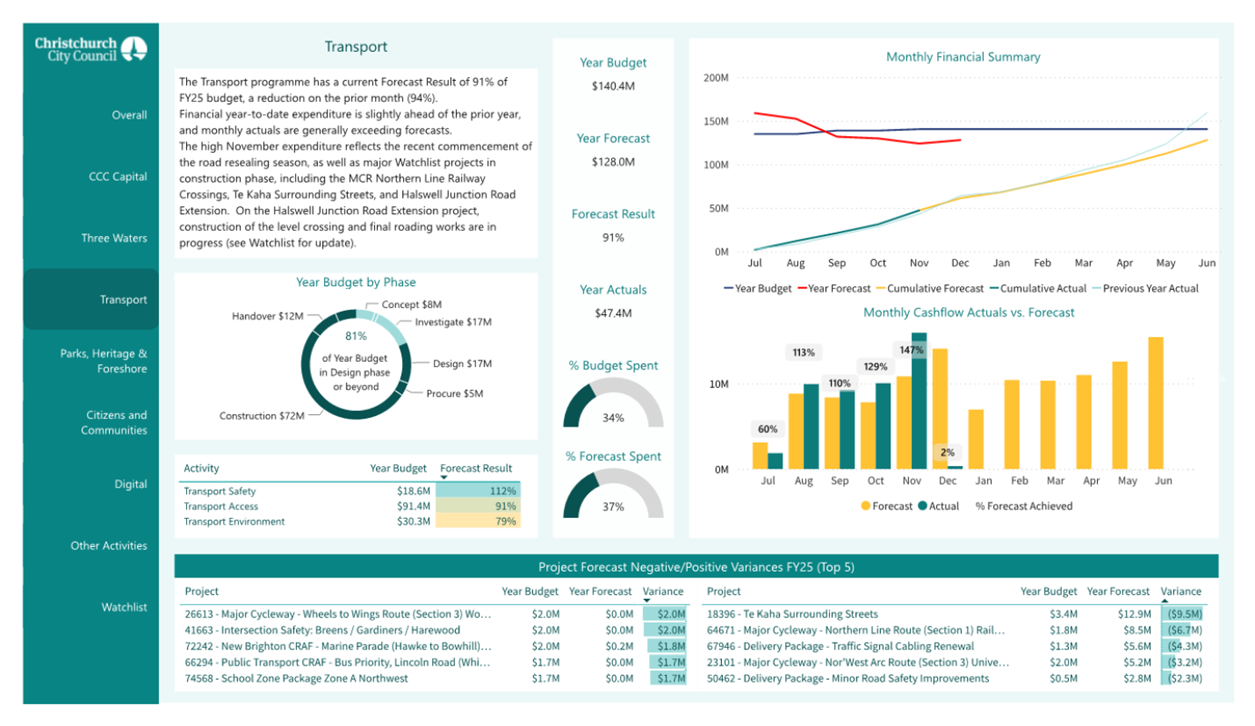

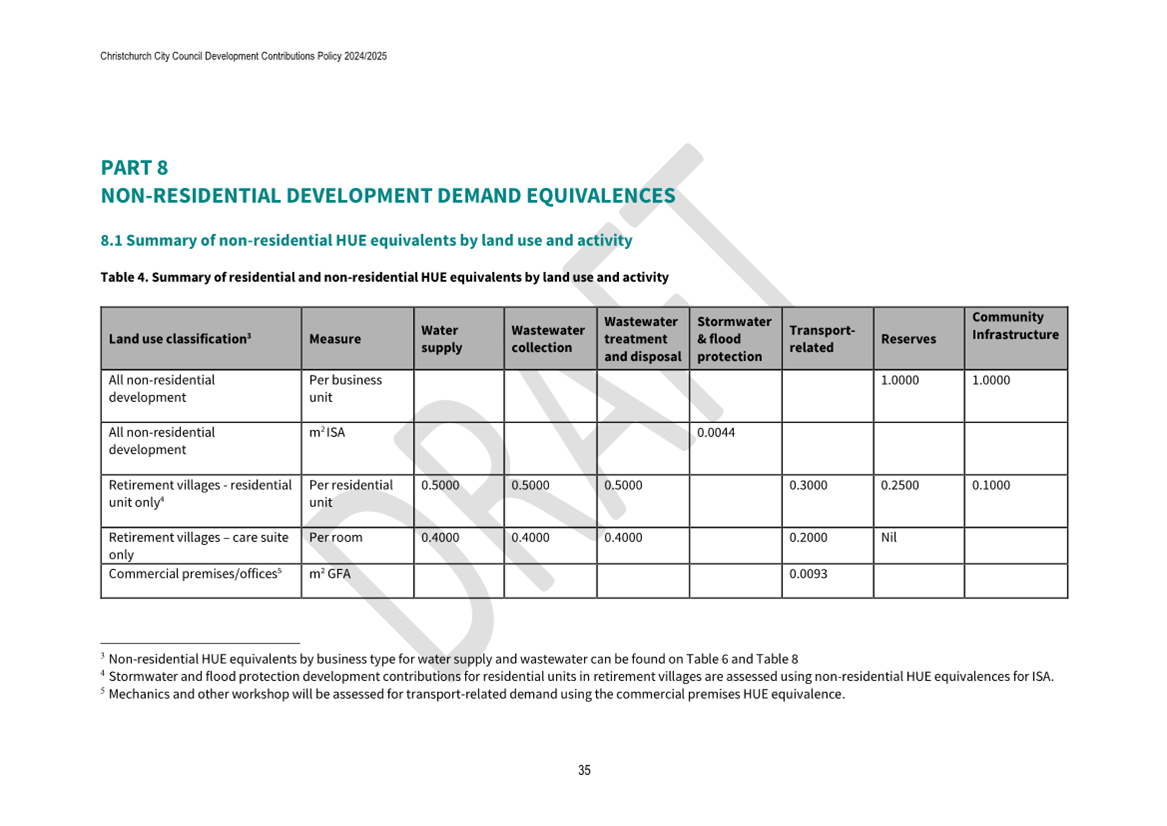

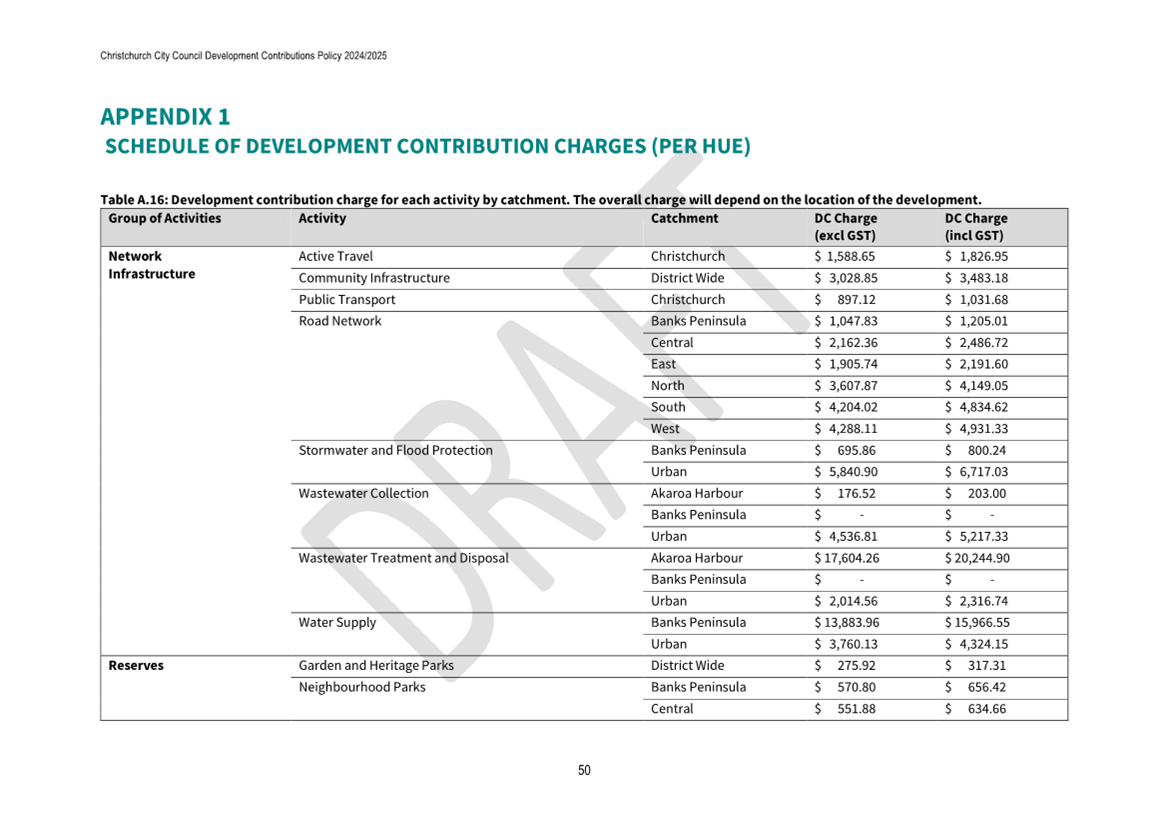

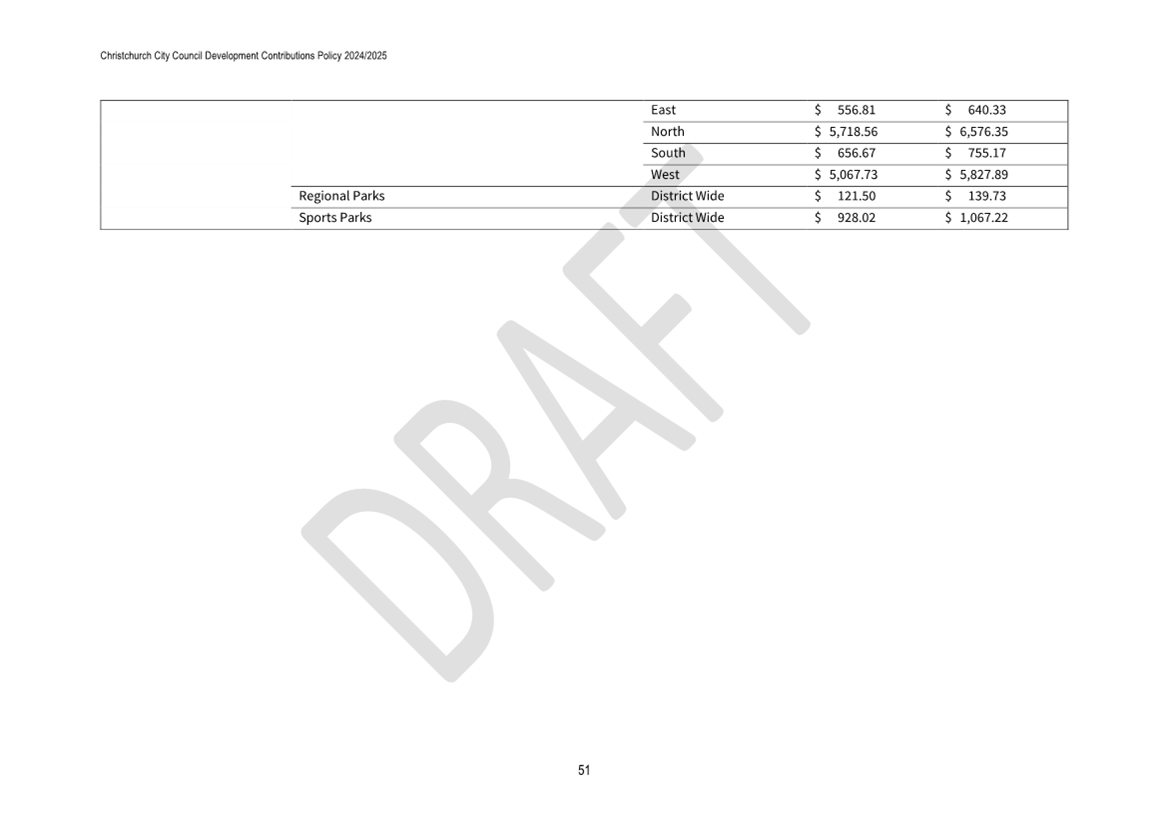

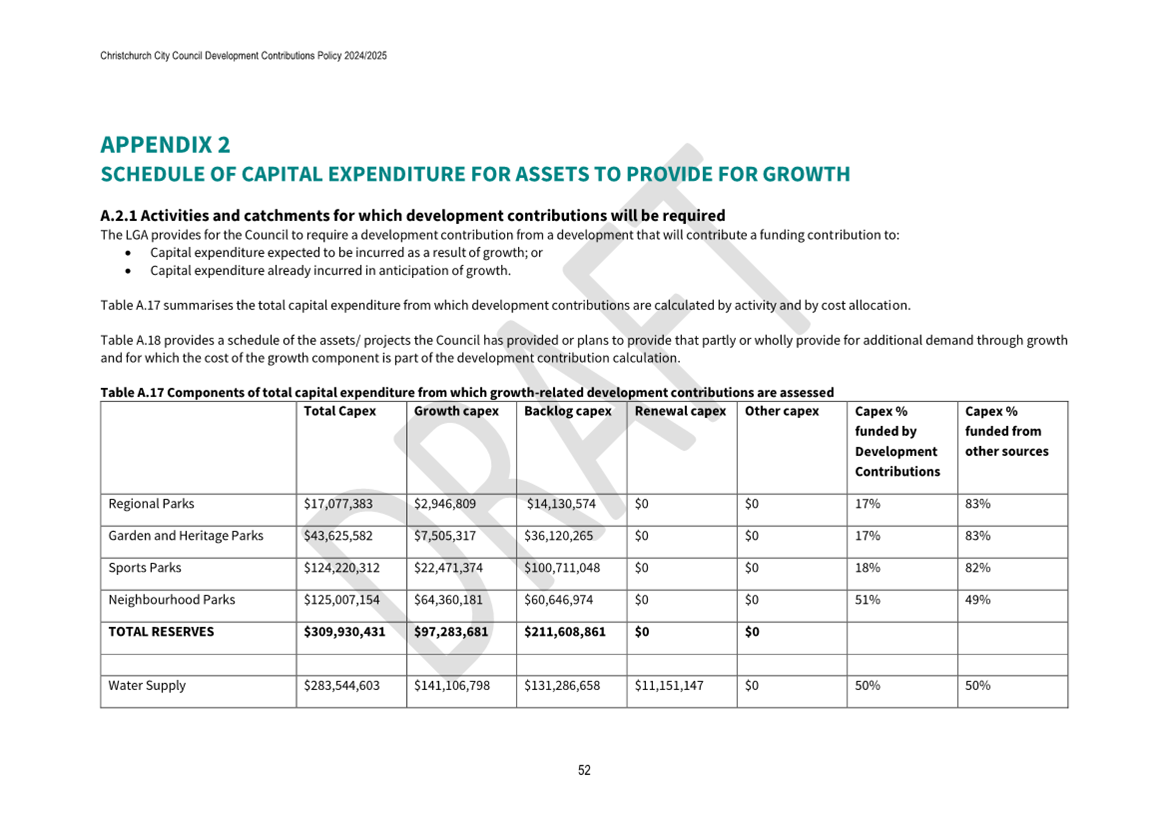

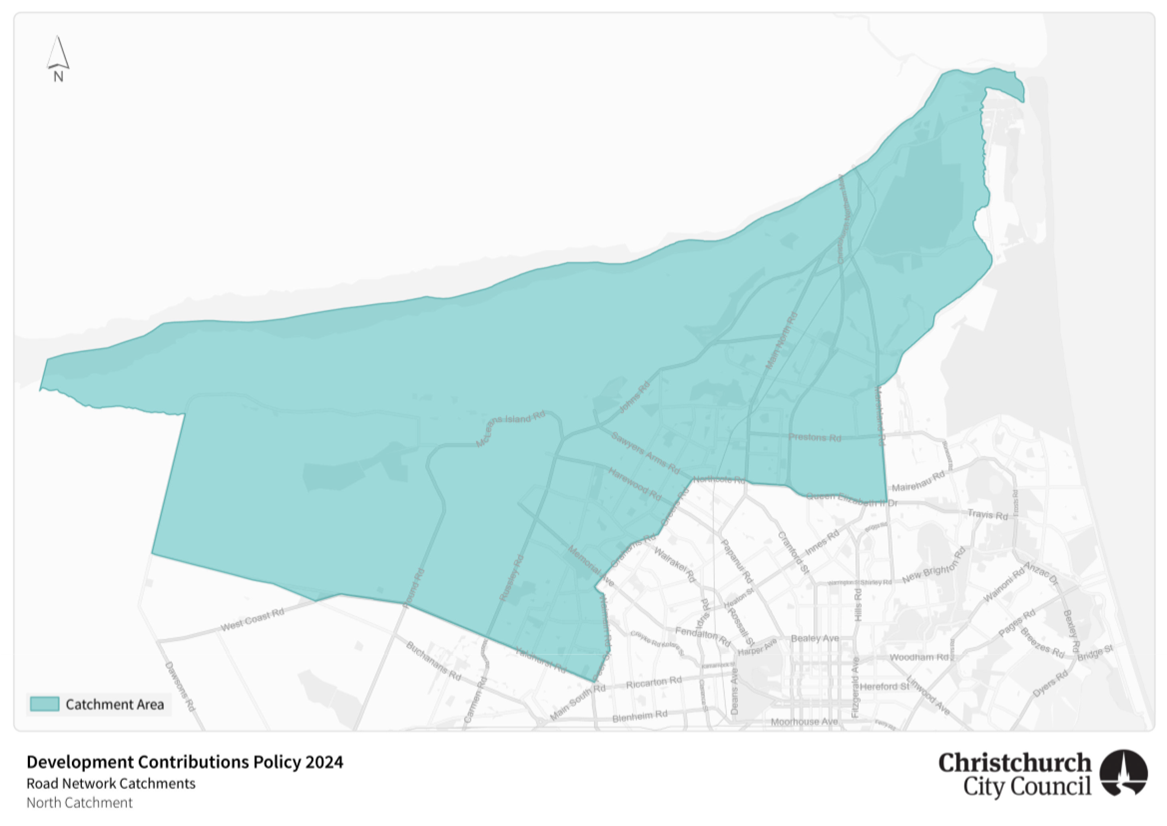

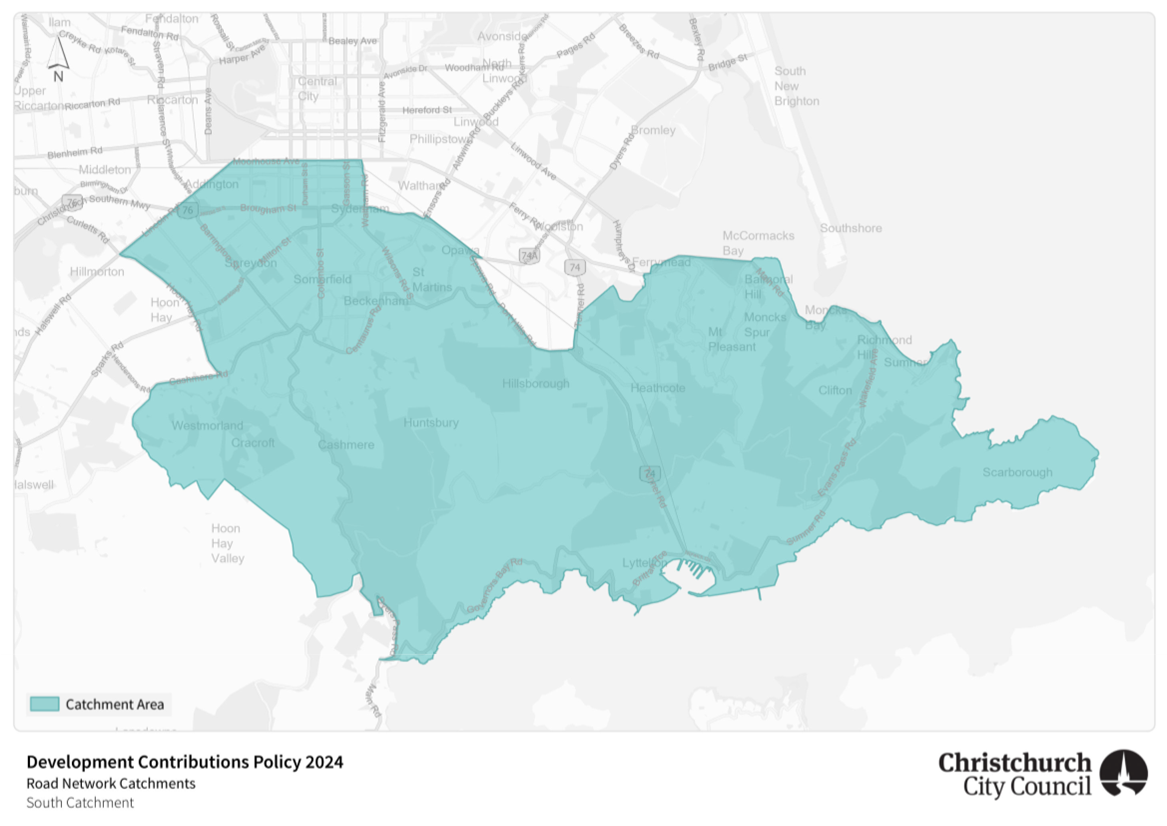

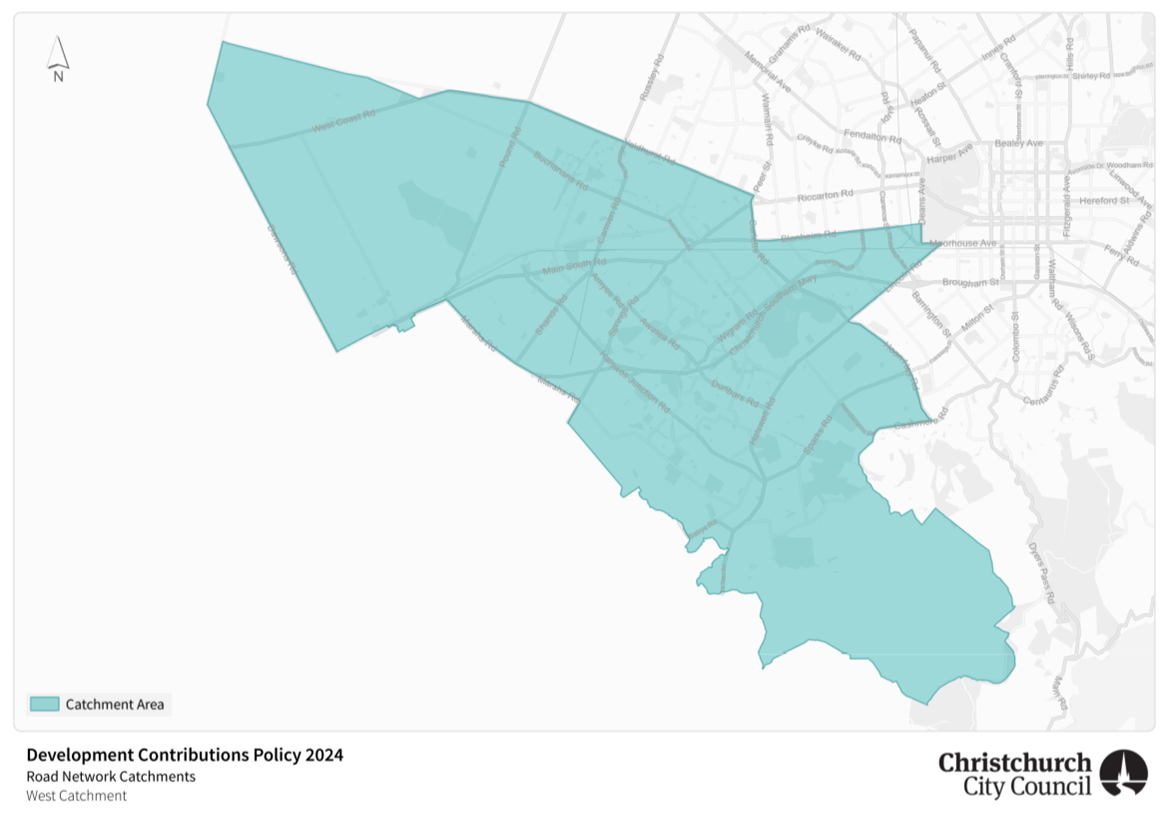

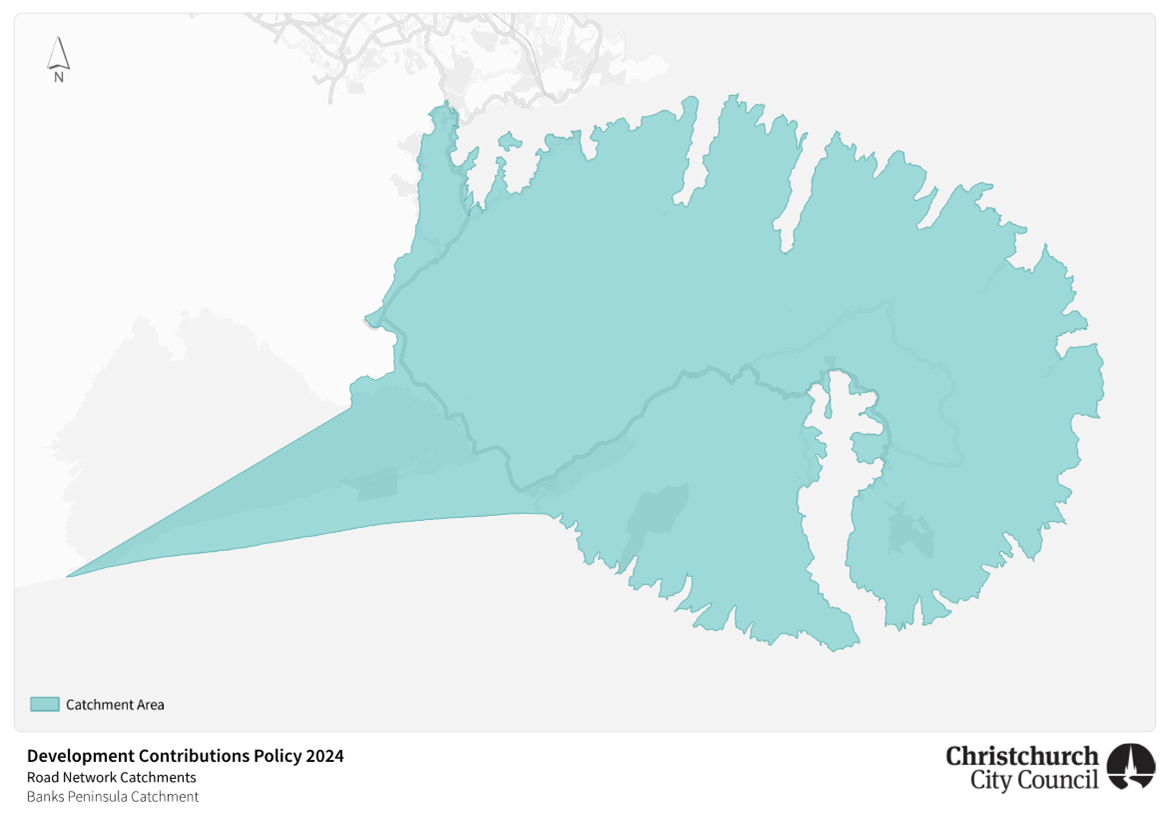

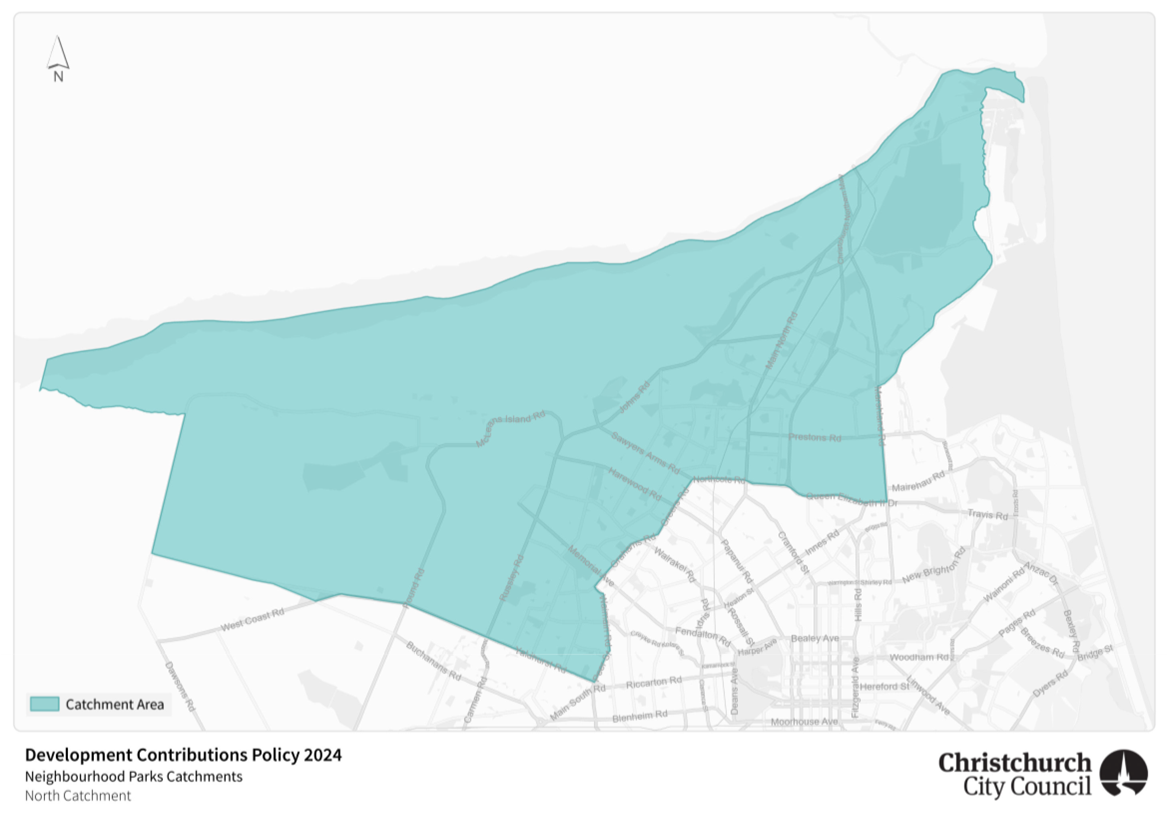

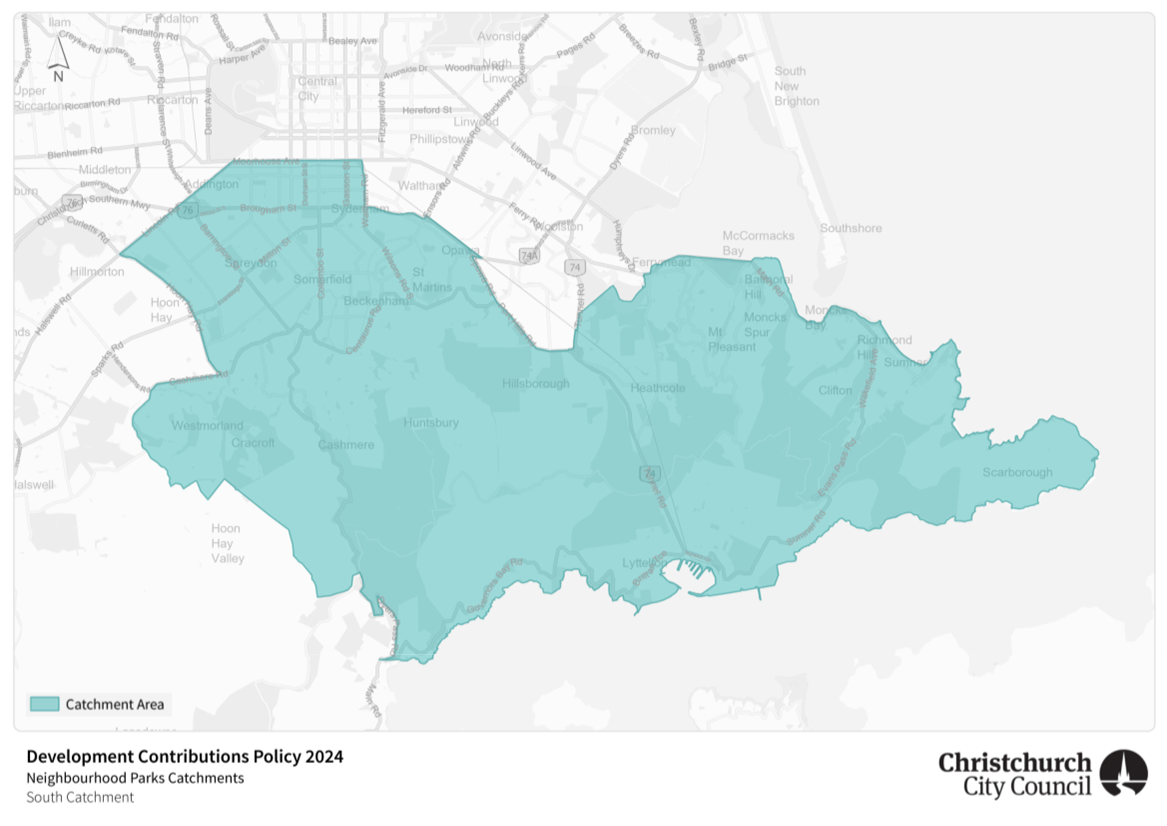

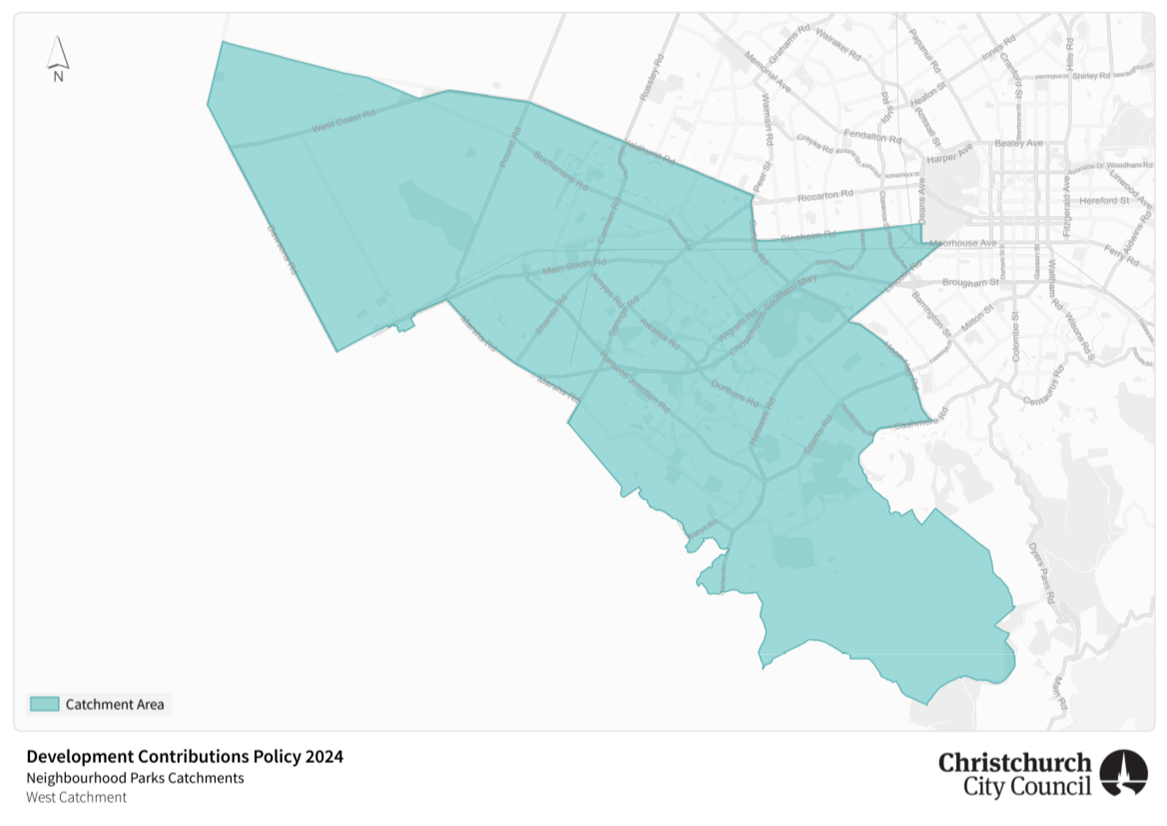

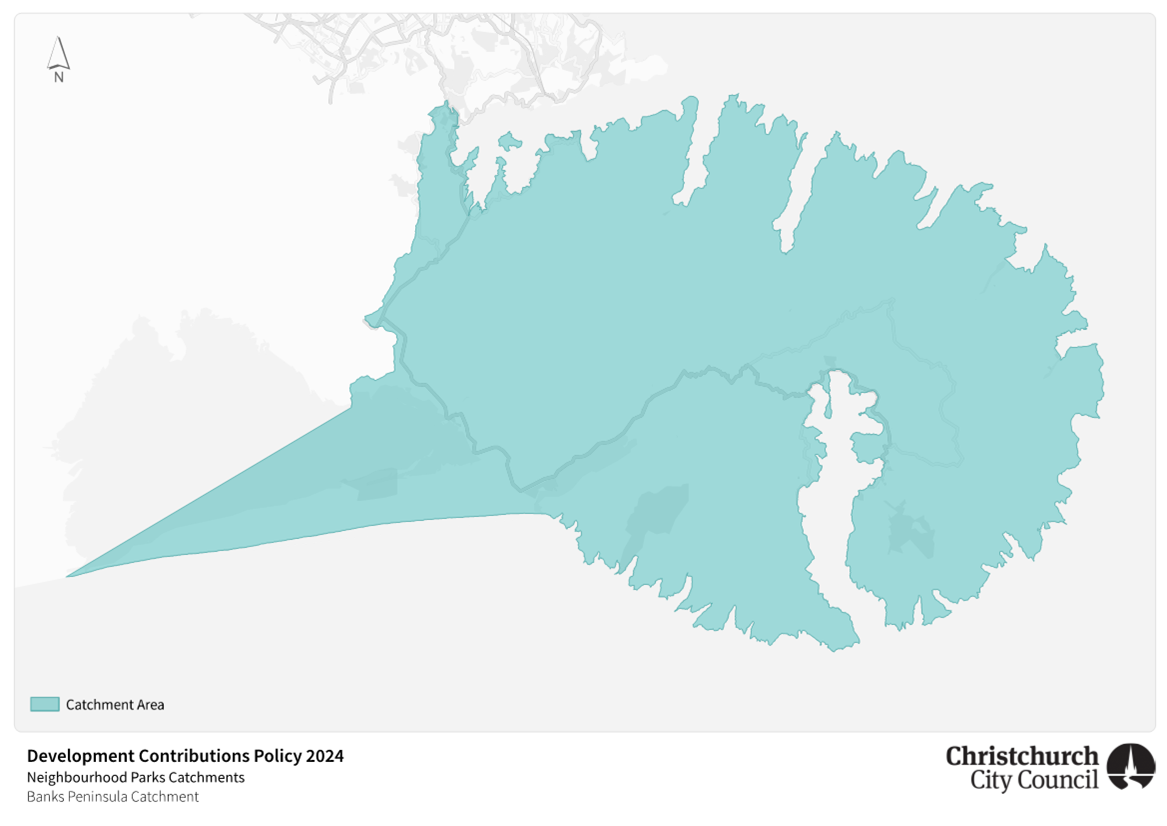

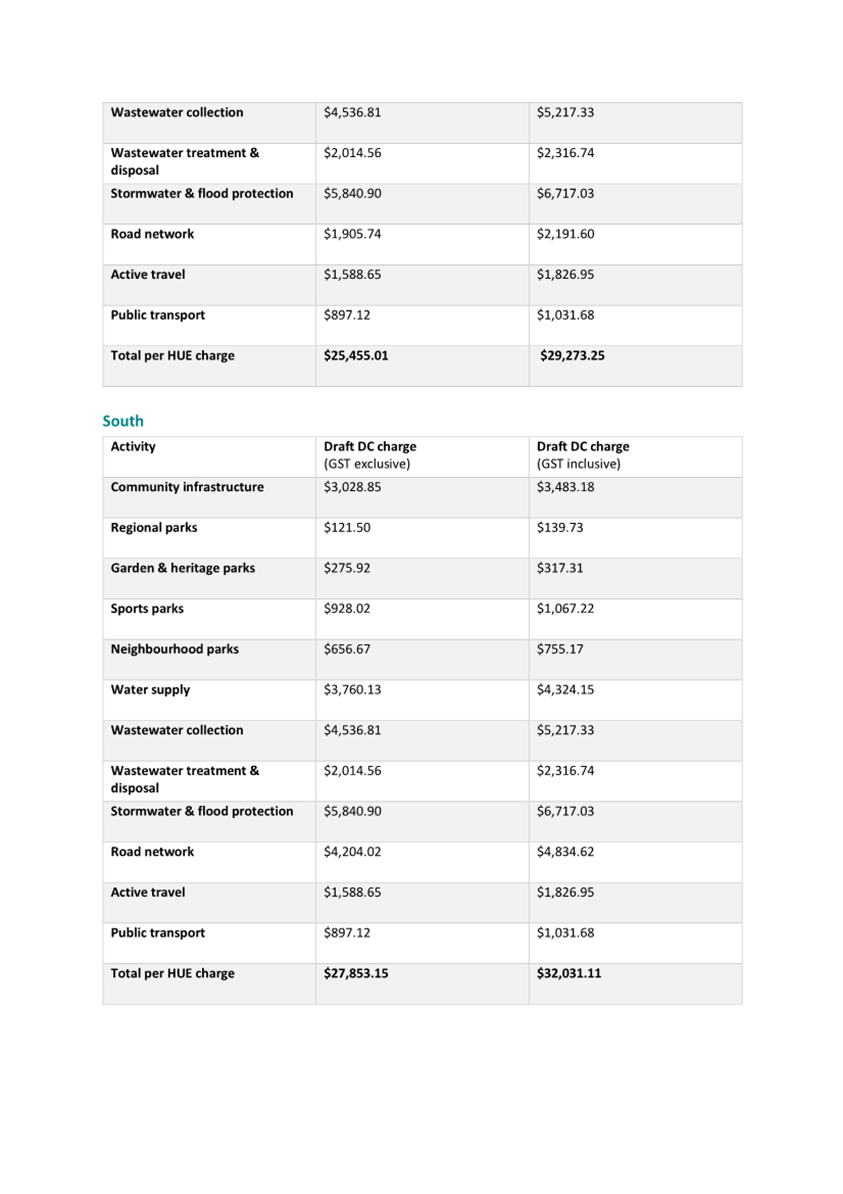

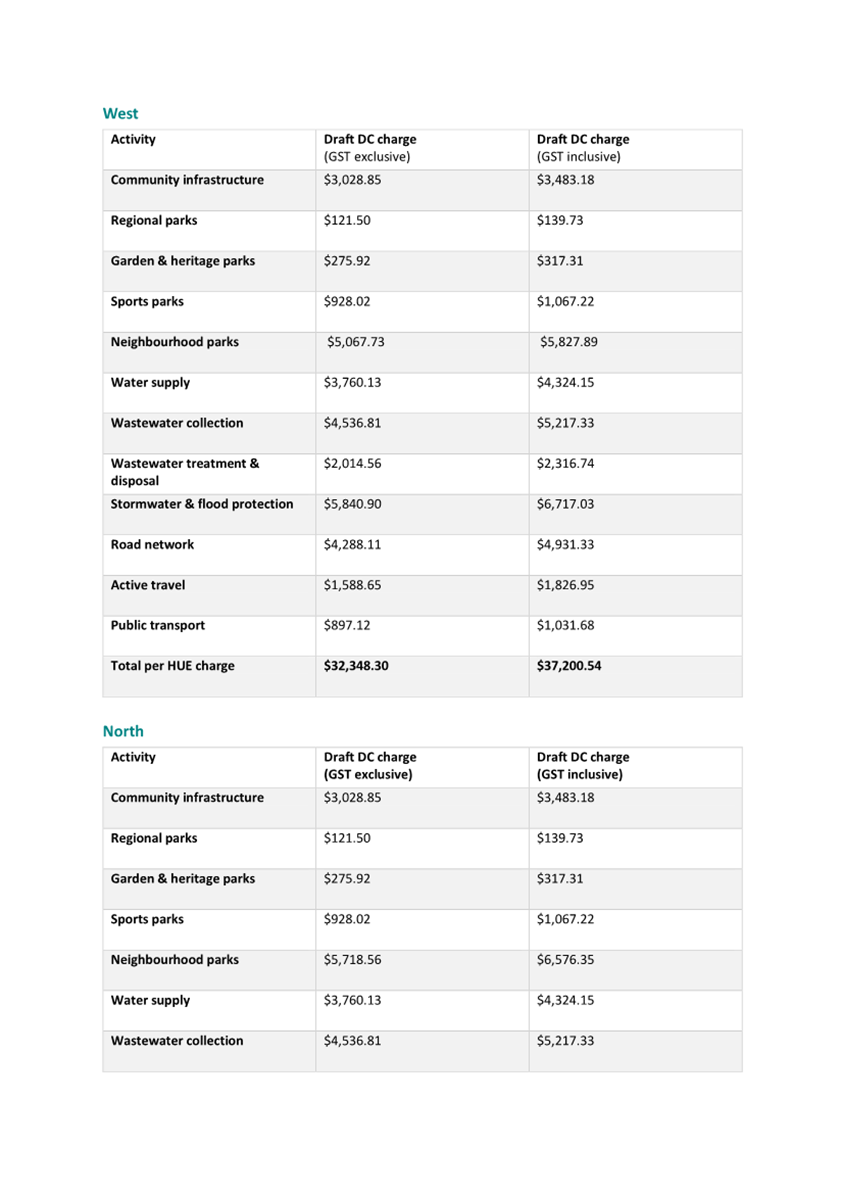

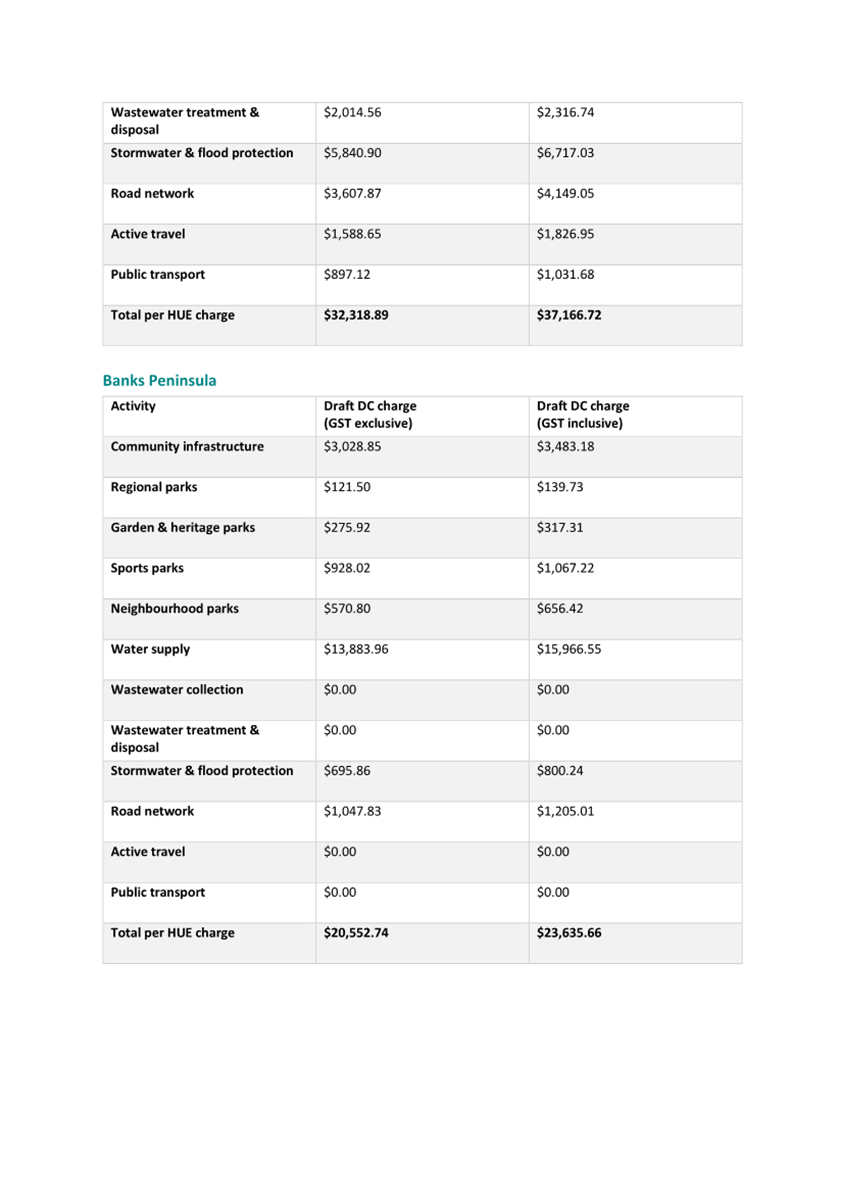

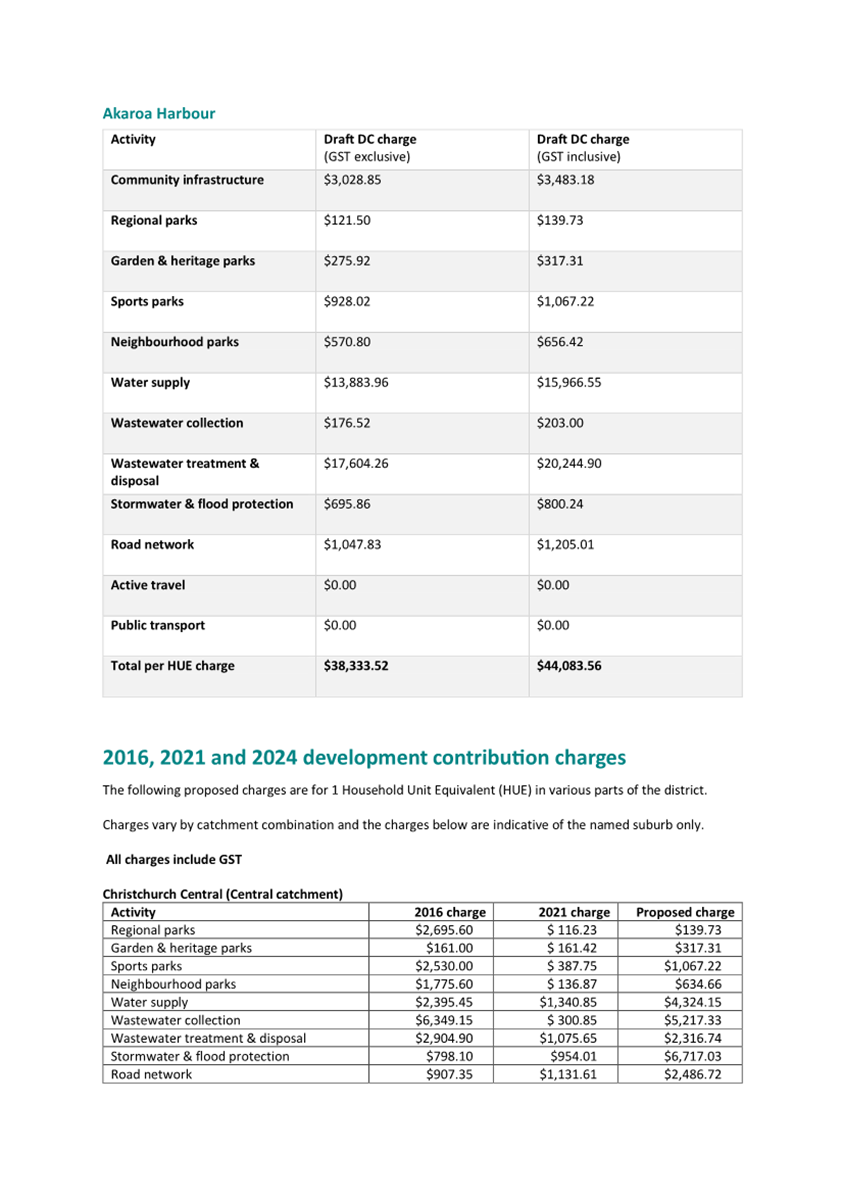

rather than a discrete cost attributed to the project.