Audit and Risk Management Committee

Agenda

Notice of Meeting:

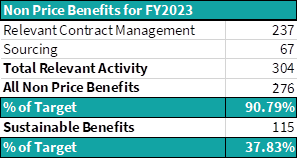

An ordinary meeting of the Audit and Risk

Management Committee will be held on:

Date: Monday 16 October 2023

Time: 9:30am

Venue: Council Chambers, Level 2, Civic Offices,

53 Hereford Street, Christchurch

Membership

|

Chairperson

Deputy Chairperson

Members

|

Mr Michael Wilkes

Councillor Jake McLellan

Councillor Tyrone Fields

Councillor Sam MacDonald

Councillor Tim Scandrett

Ms Jacqueline Robertson Cheyne

Mrs Hilary Walton

|

11 October 2023

|

|

|

Principal Advisor

Leah Scales

General Manager - Resources / CFO

Tel: 941 8999

|

Luke Smeele

Democratic Services Advisor

941 6374

luke.smeele@ccc.govt.nz

www.ccc.govt.nz

|

Audit and Risk Management Committee

16 October 2023

|

|

Audit

and Risk Management Committee - Terms of Reference Ngā Ārahina Mahinga

|

Chair

|

Mr

Michael Wilkes (Independent)

|

|

Deputy Chair

|

Councillor

McLellan

|

|

Membership

|

Councillor Fields

Councillor MacDonald

Councillor Scandrett

External Members:

Mrs Hilary Walton

Ms Jacqueline Robertson Cheyne

|

|

Quorum

|

Half of the members if the

number of members (including vacancies) is even, or a majority of members if

the number of members (including vacancies) is odd.

|

|

Meeting

Cycle

|

Quarterly and

as required

|

|

Reports

To

|

Council

|

Purpose

To assist the Council to discharge

its responsibility to exercise

due care, diligence and skill in relation to the oversight of:

·

the robustness of the internal control framework;

·

the integrity and appropriateness of external reporting, and

accountability arrangements within the organisation for these functions;

·

the robustness of risk management systems, process and practices;

·

internal and external audit;

·

accounting policy and practice;

·

compliance with applicable laws, regulations, standards and best

practice guidelines for public entities; and

·

the establishment and maintenance of controls to safeguard the

Council’s financial and non-financial assets.

The foundations on which this

Committee operates, and as reflected in this Terms of Reference, includes:

independence; clarity of purpose; competence; open and effective relationships

and no surprises approach.

Procedure

·

In order to give effect to its advice the Committee should make recommendations to the Council and to

Management.

·

The Committee should meet the internal and the external auditors

without Management present as a standing agenda item at each meeting where

external reporting is approved, and at other meetings if requested by any of

the parties.

·

The external auditors,

the internal audit manager and the co-sourced internal audit firm should meet

outside of formal meetings as appropriate with the Committee Chair.

·

The Committee Chair

will meet with relevant members of Management before each Committee meeting and

at other times as required.

Responsibilities

Internal Control Framework

·

Consider the adequacy and effectiveness of internal controls and

the internal control framework including overseeing privacy and cyber security.

·

Enquire as to the steps management has taken to embed a culture

that is committed to probity and ethical behaviour.

·

Review the processes or systems in place to capture and

effectively investigate fraud or material litigation should it be required.

·

Seek confirmation annually and as necessary from internal and

external auditors, attending Councillors, and management, regarding the

completeness, quality and appropriateness of financial and operational

information that is provided to the Council.

Risk Management

·

Review and consider Management’s risk management framework

in line with Council’s risk appetite, which includes policies and

procedures to effectively identify, treat and monitor significant risks, and

regular reporting to the Council.

·

Assist the Council to determine its appetite for risk.

·

Review the principal risks that are determined by Council and

Management, and consider whether appropriate action is being taken by

management to treat Council’s significant risks. Assess the effectiveness

of, and monitor compliance with, the risk management framework.

·

Consider emerging significant risks and report these to Council

where appropriate.

Internal Audit

·

Review and approve the annual internal audit plan, such plan to

be based on the Council’s risk framework. Monitor performance against the

plan at each regular quarterly meeting.

·

Monitor all internal audit reports and the adequacy of

management’s response to internal audit recommendations.

·

Review six monthly fraud reporting and confirm fraud issues are

disclosed to the external auditor.

·

Provide a functional reporting line for internal audit and ensure

objectivity of internal audit.

·

Oversee and monitor the performance and independence of internal

auditors, both internal and co-sourced. Review the range of services provided

by the co-sourced partner and make recommendations to Council regarding the

conduct of the internal audit function.

·

Monitor compliance with the delegations policy.

External Reporting and

Accountability

·

Consider the appropriateness of the Council’s existing

accounting policies and practices and approve any changes as appropriate.

·

Contribute to improve the quality, credibility and objectivity of

the accounting processes, including financial reporting.

·

Consider and review the draft annual financial statements and any

other financial reports that are to be publicly released, make recommendations

to Management.

·

Consider the underlying quality of the external financial

reporting, changes in accounting policy and practice, any significant

accounting estimates and judgements, accounting implications of new and

significant transactions, management practices and any significant

disagreements between Management and the external auditors, the propriety of

any related party transactions and compliance with applicable New Zealand and

international accounting standards and legislative requirements.

·

Consider whether the external reporting is consistent with

Committee members’ information and knowledge and whether it is adequate

for stakeholder needs.

·

Recommend to Council the adoption of the Financial Statements and

Reports and the Statement of Service Performance and the signing of the Letter

of Representation to the Auditors by the Mayor and the Chief Executive.

·

Enquire of external auditors for any information that affects the

quality and clarity of the Council’s financial statements, and assess

whether appropriate action has been taken by management.

·

Request visibility of appropriate management signoff on the

financial reporting and on the adequacy of the systems of internal control;

including certification from the Chief Executive, the Chief Financial Officer

and the General Manager Corporate Services that risk management and internal

control systems are operating effectively;

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

·

Review and consider the Summary Financial Statements for consistency

with the Annual Report.

External Audit

·

Annually review the independence and confirm the terms of the

audit engagement with the external auditor appointed by the Office of the

Auditor General. Including the adequacy of the nature and scope of the audit,

and the timetable and fees.

·

Review all external audit reporting, discuss with the auditors

and review action to be taken by management on significant issues and

recommendations and report to Council as appropriate.

·

The external audit reporting should describe: Council’s

internal control procedures relating to external financial reporting, findings

from the most recent external audit and any steps taken to deal with such

findings, all relationships between the Council and the external auditor,

Critical accounting policies used by Council, alternative treatments of

financial information within Generally Accepted Accounting Practice that have

been discussed with Management, the ramifications of these treatments and the

treatment preferred by the external auditor.

·

Ensure that the lead audit engagement and concurring audit

directors are rotated in accordance with best practice and NZ Auditing

Standards.

Compliance with Legislation,

Standards and Best Practice Guidelines

·

Review the effectiveness of the system for monitoring the

Council’s compliance with laws (including governance legislation,

regulations and associated government policies), with Council’s own

standards, and Best Practice Guidelines.

Appointment of Independent Members

·

Identify skills required for Independent Members of the Audit and

Risk Management Committee. Appointment panels will include the Mayor or

Deputy Mayor, Chair of Finance & Performance Committee and Chair of Audit

& Risk Management Committee. Council approval is required for all

Independent Member appointments.

·

The term of the Independent members should be for three

years. (It is recommended that the term for independent members begins on

1 April following the Triennial elections and ends 31 March three years

later. Note the term being from April to March provides continuity for

the committee over the initial months of a new Council.)

·

Independent members are eligible for re-appointment to a maximum

of two terms. By exception the Council may approve a third term to ensure continuity

of knowledge.

Long Term Plan Activities

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

Audit and Risk Management

Committee Forward Work Programme 2023

|

2023

|

Feb

|

Apr

|

Jun

|

Aug

|

Annual Report Oct

|

Dec

|

|

Update Reports

|

·

Risk

and Assurance

·

Procurement

|

·

Risk

and Assurance

·

Cyber

Security

|

· Risk and Assurance

· Procurement

· Major Litigation Report

|

· Major Litigation Report

|

·

Cyber Security

·

Risk and Assurance

·

LTP Update

·

Procurement

|

· Risk and Assurance

· Procurement

· Te Kaha

|

|

Other Reports

|

·

Holidays

Act Remediation Programme Completion

·

Christchurch City Holdings

|

· Te Kaha

|

· LTP Process

· Cyber Security Report

· Parakiore

· Report to Governors FY22

|

·

Situational

Safety Report

|

·

CCHL

·

Audit

Fees Proposal

·

Conflict

of Interest and Gift Declaration

|

·

Changes

to Procurement Framework

|

|

Annual Report

|

|

·

External

Reporting and Audit Programme for 2022/23 Update

|

|

· Update on critical judgments, estimates

& assumptions

· Financial Statements Update - Valuations

|

· Financial Statements and Annual Report

|

· Debenture trust audit report

·

Audit NZ Management

Letter from prior year’s audit

|

|

Annual Plan

|

·

Draft

Annual Plan

|

|

·

Final Annual Plan

|

|

|

|

|

Audit and Risk Management Committee

16 October 2023

|

|

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

TABLE OF CONTENTS NGĀ IHIRANGI

C 1. Apologies Ngā Whakapāha.......................................................................... 9

B 2. Declarations of Interest Ngā Whakapuaki Aronga........................................... 9

C 3. Confirmation of Previous Minutes Te Whakaāe o te

hui o mua.......................... 9

B 4. Public Forum Te Huinga Whānui.................................................................. 9

B 5. Deputations by Appointment Ngā Huinga

Whakaritenga................................. 9

B 6. Presentation

of Petitions Ngā

Pākikitanga.................................................... 9

Staff Reports

C 7. Procurement

and Contracts Unit FY23 Q4 Report......................................... 13

C 8. Conflict

of Interest and Gift Declaration...................................................... 17

C 9. LTP

2024-34 Update................................................................................. 19

C 10. Audit and

Risk Quarterly Update................................................................ 61

C 11. Resolution

to Exclude the Public................................................................ 65

|

Audit and Risk Management Committee

16 October 2023

|

|

1. Apologies Ngā Whakapāha

At the close of

the agenda no apologies had been received.

2. Declarations of Interest Ngā

Whakapuaki Aronga

Members are

reminded of the need to be vigilant and to stand aside from decision making

when a conflict arises between their role as an elected representative and any

private or other external interest they might have.

3. Confirmation of Previous Minutes Te

Whakaāe o te hui o mua

That the

minutes of the Audit and Risk Management Committee meeting held on Thursday, 3 August 2023 be confirmed

(refer page 10).

4. Public Forum Te Huinga Whānui

There were no public forum requests

received at the time the agenda was prepared

5. Deputations by Appointment Ngā Huinga

Whakaritenga

There were no

deputations by appointment at the time the agenda was prepared.

6. Petitions Ngā Pākikitanga

There were no

petitions received at the time the agenda was prepared.

|

Audit and Risk Management Committee

16 October 2023

|

|

Audit and Risk Management Committee

Open Minutes

Date: Thursday 3 August 2023

Time: 2:02pm

Venue: Council Chambers, Level 2, Civic Offices,

53 Hereford Street, Christchurch

Present

|

Chairperson

Deputy Chairperson

Members

|

Mr Michael Wilkes

Councillor Jake McLellan

Councillor Tyrone Fields

Councillor Sam MacDonald

Mrs Hilary Walton

|

|

|

|

Principal Advisor

Leah Scales

General Manager - Resources / CFO

Tel: 941 8999

|

Luke Smeele

Committee & Hearings Advisor

941 6374

luke.smeele@ccc.govt.nz

www.ccc.govt.nz

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

The agenda was dealt with in the following

order.

1. Apologies

Ngā Whakapāha

Part C

|

Committee Resolved ARCM/2023/00009

That the apologies received from

Jacqueline Robertson Cheyne and Tim Scandrett be accepted.

Councillor

MacDonald/Councillor McLellan Carried

|

2. Declarations

of Interest Ngā Whakapuaki Aronga

Part B

There were no

declarations of interest recorded.

3. Confirmation

of Previous Minutes Te Whakaāe o te hui o mua

Part C

|

Committee Resolved ARCM/2023/00010

That the

minutes of the Audit and Risk Management Committee meeting held on Tuesday,

20 June 2023 be confirmed.

Councillor

MacDonald/Councillor McLellan Carried

|

4. Public

Forum Te Huinga Whānui

Part B

There were no public forum presentations.

5. Deputations

by Appointment Ngā Huinga Whakaritenga

Part B

There were no deputations by appointment.

6. Presentation

of Petitions Ngā Pākikitanga

Part B

There was no presentation of petitions.

|

7. Resolution

to Exclude the Public

|

|

|

Committee Resolved ARCM/2023/00011

Part C

That Chantelle Gernetzky and Debbie Bradfield of Audit New

Zealand, remain after the public have been excluded and Scott McClay of

Deloitte can remain for item number 9 of the public excluded agenda as they

have knowledge that is relevant to those items and will assist the Council.

AND

That at 2:04pm the resolution to exclude the public set out on

pages 15 to 17 of the agenda be adopted.

Councillor

Fields/Councillor McLellan Carried

|

The public were re-admitted to the meeting

at 4:18pm.

Meeting

concluded at 4:18pm.

CONFIRMED THIS 16th DAY

OF OCTOBER 2023

Michael Wilkes

Chairperson

|

Audit and Risk Management Committee

16 October 2023

|

|

|

7. Procurement

and Contracts Unit FY23 Q4 Report

|

|

Reference / Te Tohutoro:

|

23/337302

|

|

Report of / Te Pou Matua:

|

Paul

Cateriano, Head of Procurement and Contracts

(paul.cateriano@ccc.govt.nz)

|

|

General Manager / Pouwhakarae:

|

Leah

Scales, General Manager Resources/Chief Financial Officer

(Leah.Scales@ccc.govt.nz)

|

1. Nature of Information Update and Report Origin

1.1 Quarterly Audit and Risk Management Committee Report.

1.2 Procurement and Contract Management Compliance Monitoring

and Reporting.

Report to Audit and Risk Management Committee every quarter on monitoring

compliance.

2. Officer Recommendations Ngā Tūtohu

That the Audit and

Risk Management Committee:

1. Receive the information in the Quarterly

Procurement Report for the months of April, May and June 2023 (FY2023 Q4

Report).

3. Long Term Plan Activity Reports

3.1 LTP/AP22: 13.1.21.1 Procurement and Contract Management is managed as a shared service

delivery - Performance.

Return on Investment (ROI) = total Cost

Reduction/Avoidance

3.1.1 Total

commercial benefits for the Procurement and Contracts Unit on FY23 is

$18,346,800. This includes a mix of both Capex and Opex cost reduction and avoidance.

3.1.2 As

total cost of the Procurement and Contracts Unit in FY22/23 was $2,602,600, the

Return on Investment (ROI) for the Unit for FY22/23 is 7. Expectation of the

Unit is to have an ROI of 3.

3.1.3 For

a detailed breakdown of all the Financial Benefits please refer to Attachment A – Financial Benefits FY23.

3.1.4 Below

a summary of the final financial benefits for FY23.

3.1.5 Project

actual savings are an average of all projects completed in FY23 to date and are

calculated as per the below:

· A cost reduction is when

the awarded amount is lower than the pre-tender estimate.

· A cost avoidance is when

the awarded amount is larger than the estimated amount, but lower than the

tendered amount.

3.2 LTP/AP22: 13.1.21.2 Procurement

and Contract Management is managed as a shared service delivery

Non-financial return through procurement activity - 85% of sourcing activity

and contract management activity to achieve Non-Financial outcomes annually.

Sustainable return through procurement

activity - 85% of sourcing activity and contract management activity to achieve

sustainable outcomes annually.

3.2.1 Non-Financial

return through procurement activity for FY23 was 90.79%. This includes a mix of

multiple non-financial benefits such as Process Improvement initiatives, Risk

Mitigation, KPI Improvement, amongst others.

3.2.2 Sustainable

return through procurement activity for FY23 was 37.83%. This includes only

Social, Environmental and Economic benefits reported through a Procurement

activity.

3.2.3 The

Procurement and Contracts Leadership Team is developing a training module for

all REPC Unit staff on how to properly capture and report on sustainable

benefits as 100% of our sourcing activities should be achieving this target now

that it is a mandatory requirement for all tenders.

3.2.4 See

below a summary of the Non-Financial and Sustainable return through Procurement

for FY23. For a detailed breakdown of the benefits please refer to Attachment

B - Non-Financial Benefits for FY23.

3.3 LTP/AP22:

13.1.22.1 Procurement and Contract Management is managed as a shared

service delivery.

95% of all procurement activity more than $100k (Excl. GST) put to market

through RFP/T.

3.3.1 100%

of all the procurement activity over $100k in FY23 followed the Council

Procurement Framework and was put to marked through a Request for Proposal

(RFP) or a Request for Tender (RFT). A total of 32% of all of that activity was

over $100k.

3.3.2 The

table below shows a summary of the procurement activity in FY23.

3.4 LTP/AP22: 13.1.22.3

Procurement and Contract Management is managed as a shared service delivery -

Conformance.

100% of Procurement & Contract recommended Departures have valid

procurement plans/strategies and risk assessment.

3.4.1 There

were 25 departures submitted this quarter. 100% of all Departures submitted had

a valid procurement plan and a risk assessment.

3.4.2 The

rationale for not going to market is justified based on the Office of the

Auditor General Procurement Guidance for Public Entities.

4. Other Council Procurement

Information

4.1 Off-Contract

Spend.

4.1.1 There

has been a decrease of $1.17M in Off-Contract spend compared to previous

reporting period. Current off contract spend represents 13.73% of total spend.

We expect to see a reduction in off-contract spend even further, as the

Procurement and Contract Units together with Finance, are currently carrying

out multiple in-person trainings across all Council Units.

4.2 Purchase

Orders raised after Invoice.

4.2.1 There

has been a decrease in purchase orders raised after invoice of 3.9% compared to

the last reporting period. Approximately 8.87% of Purchase Orders created have

been created after receiving the invoice.

4.2.2 We

expect to drive this number close to zero as we are currently making a process

change due to the SAP Improvement Programme that all Purchase Order will need

to be linked to an active Contract. Invoices without a Purchase Order number

will not be able to be paid under the new Accounts Payable process, unless it

is related to an emergency procurement. Internal and external communication to

all our stakeholders and suppliers about this change has already commenced in

September 2023.

Attachments / Ngā

Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a

|

Attachment A -

Financial Benefits FY23 (Under Separate Cover) - Confidential

|

23/1586948

|

|

|

b

|

Attachment B -

Non-Financial Benefits for FY23 (Under Separate Cover) - Confidential

|

23/1586950

|

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Confirmation of Statutory

Compliance / Te Whakatūturutanga ā-Ture

|

Compliance with Statutory Decision-making

Requirements (ss 76 - 81 Local Government Act 2002).

(a) This report contains:

(i) sufficient information about all reasonably practicable

options identified and assessed in terms of their advantages and

disadvantages; and

(ii) adequate consideration of the views and preferences of

affected and interested persons bearing in mind any proposed or previous

community engagement.

(b) The information reflects the level of significance of the

matters covered by the report, as determined in accordance with the Council's

significance and engagement policy.

|

Signatories / Ngā Kaiwaitohu

|

Authors

|

Paul Cateriano

- Head of Procurement & Contracts

Jo van den

Heever - Principal Advisor Procurement

Elizabeth

Espin - Team Leader Procurement Special Projects

Chris Banks -

Senior Procurement Reporting Analyst

Luke Stevens -

Manager Procurement

|

|

Approved By

|

Russell Holden

- Acting General Manager Resources/Chief Financial Officer

|

|

Audit and Risk Management Committee

16 October 2023

|

|

|

8. Conflict of Interest and Gift

Declaration

|

|

Reference / Te Tohutoro:

|

22/1523345

|

|

Report of / Te Pou Matua:

|

Wade

Morris, Legal Counsel

|

|

General Manager / Pouwhakarae:

|

Lynn

McClelland, Assistant Chief Executive Strategic Policy and Performance

(lynn.mcclelland@ccc.govt.nz)

|

1. Nature of Information Update and Report Origin

1.1 The purpose of this report is to provide an update on outstanding

action ARMC/2020/00039.

1.2 On 2 December 2020, the Audit and Risk Management Committee

resolved that staff investigate the improvement opportunities noted at

paragraph 3.1 and report back to the Committee.

2. Officer Recommendations Ngā Tūtohu

That the Audit and

Risk Management Committee:

1. Receive the information in the Conflict of

Interest and Gift Declaration Report.

2. Note the support available to Elected Members

to support compliance with conflict-of-interest obligations.

3. Brief Summary

3.1 In

a report to the Audit and Risk Committee in 2020 staff noted the following

improvement opportunities with respect to Elected Members’ interests:

3.1.1 Update

and finalise Elected Members’ Code of Conduct.

3.1.2 Development

of a clear, centralised Conflict of Interest policy/procedure document for the

Mayor and Councillors. Such a policy would cover gifts and hospitality and may

extend to Community Board Members.

3.1.3 Update

and simplify the Councillors’ register of interest and requirement

documents and process.

3.1.4 Update

the Council’s Conflict of Interest standing agenda item.

3.1.5 Update

Elected Member induction material/process and Big Tin Can folders to improve

ease of location reference and coverage of Conflicts of Interest.

3.1.6 Consider

how interests and gifts can be more effectively administered, via a system/web

tool.

3.2 In

the intervening period, all but one of the improvement opportunities noted

above have been implemented or are underway. The Code of Conduct is the

matter that has not been fully implemented at the time of writing this report,

but a revised version is in development and Councillors have been briefed on

it. We anticipate adoption of the revised version by December 2023.

3.3 The

outstanding improvement opportunity originally identified is the development of

a conflict-of-interest policy.

3.4 Staff

consider that a specific conflict of interest policy is superfluous given:

3.4.1 The

implementation of the other actions;

3.4.2 Processes

around conflicts of interest are well provided for in the Code of Conduct

applicable to elected members;

3.4.3 Elected

members are provided with conflict-of-interest training at the beginning of

each term;

3.4.4 Advice

has been circulated from an external legal services provider in relation to

conflicts that apply for councillors who are appointed to council-controlled

and council organisations.

3.4.5 Elected

members can request advice concerning conflicts of interests from

Council’s Legal & Democratic Services;

3.4.6 The

changes to the Local Government Act 2002 in relation to pecuniary interests,

which included the provision of further guidance and advice to support

compliance; and

3.4.7 The

inability to enforce a policy.

Attachments / Ngā Tāpirihanga

There are no

attachments to this report.

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Confirmation of Statutory

Compliance / Te Whakatūturutanga ā-Ture

|

Compliance with Statutory Decision-making

Requirements (ss 76 - 81 Local Government Act 2002).

(a) This report contains:

(i) sufficient information about all reasonably practicable

options identified and assessed in terms of their advantages and

disadvantages; and

(ii) adequate consideration of the views and preferences of

affected and interested persons bearing in mind any proposed or previous

community engagement.

(b) The information reflects the level of significance of the

matters covered by the report, as determined in accordance with the Council's

significance and engagement policy.

|

Signatories / Ngā Kaiwaitohu

|

Author

|

Wade Morris -

Legal Counsel

|

|

Approved By

|

Helen White -

Head of Legal & Democratic Services

Lynn

McClelland - Assistant Chief Executive Strategic Policy and Performance

|

|

Audit and Risk Management Committee

16 October 2023

|

|

|

9. LTP 2024-34 Update

|

|

Reference / Te Tohutoro:

|

23/1545492

|

|

Report of / Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance

|

|

Senior Manager / Pouwhakarae:

|

Lynn

McClelland, Assistant Chief Executive Strategic Policy and Performance

(lynn.mcclelland@ccc.govt.nz)

|

1. Purpose and Origin of Report Te Pūtake Pūrongo

1.1 The purpose of this report is to provide an update on

progress against the approved LTP work programme to the Audit and Risk

Management Committee (ARMC), including any risks or impediments to the project and

its key workstreams.

1.2 Consideration and review of the Long Term and Annual Plans

before adoption by the Council is specified in the ARMC Terms of Reference.

2. Officer Recommendations Ngā Tūtohu

That the Audit and

Risk Management Committee:

1. Receive the information in the LTP 2024-34 Update Report.

2. Note the LTP 2024-34 project update and Audit NZ Self-Assessment.

3. Brief Summary

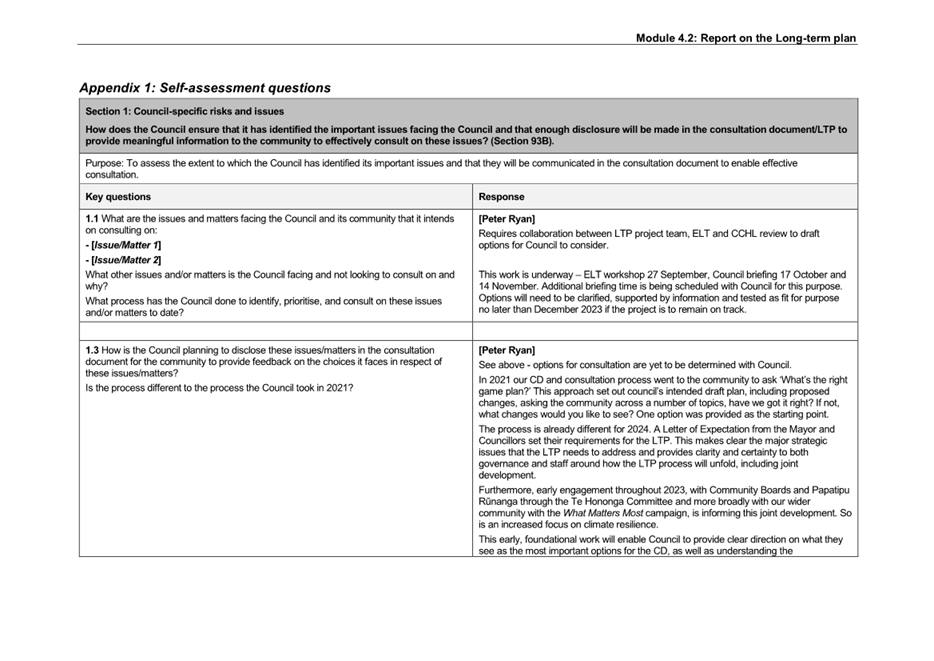

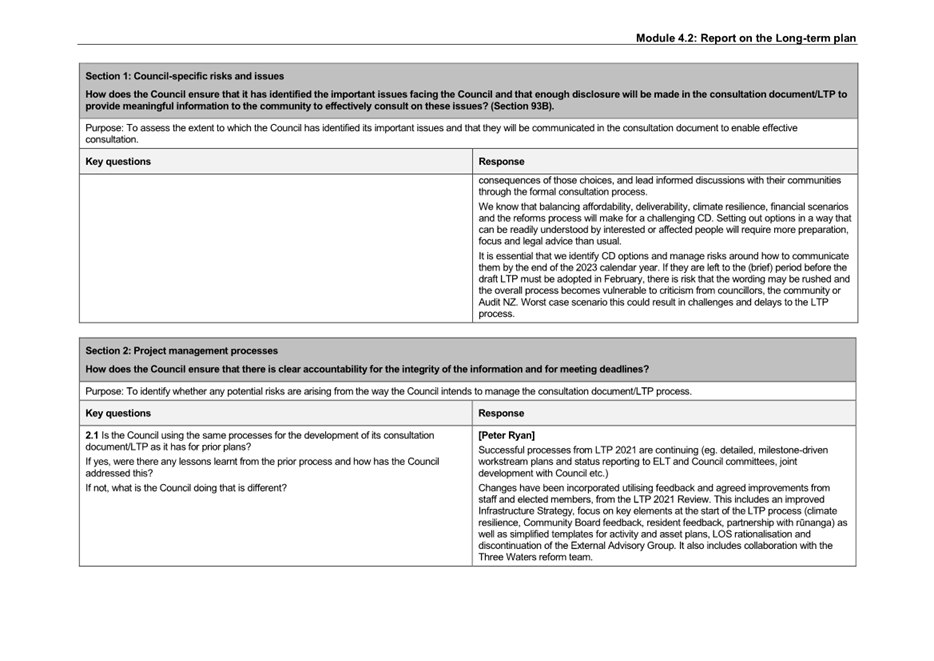

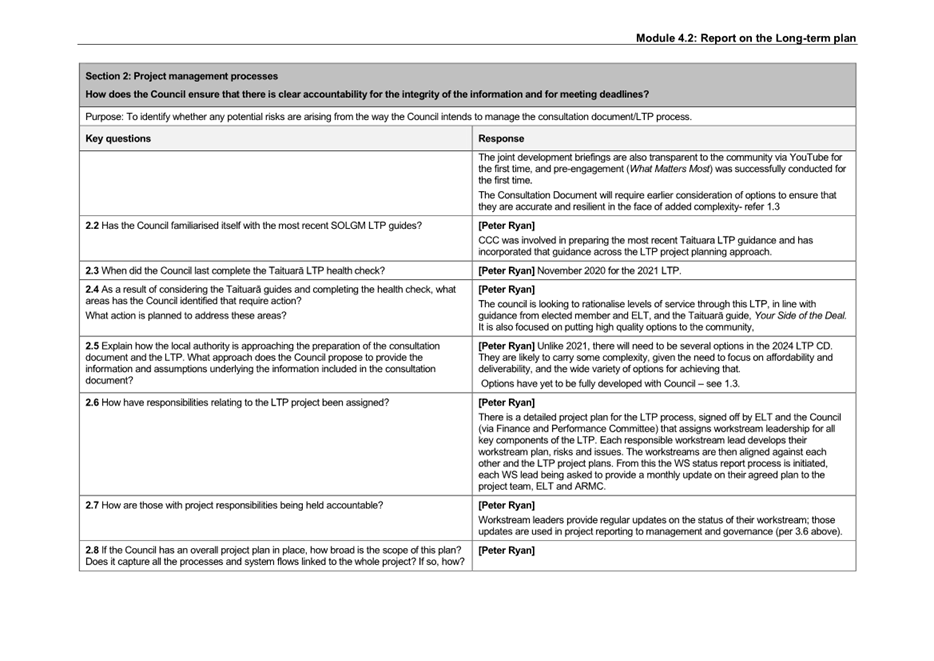

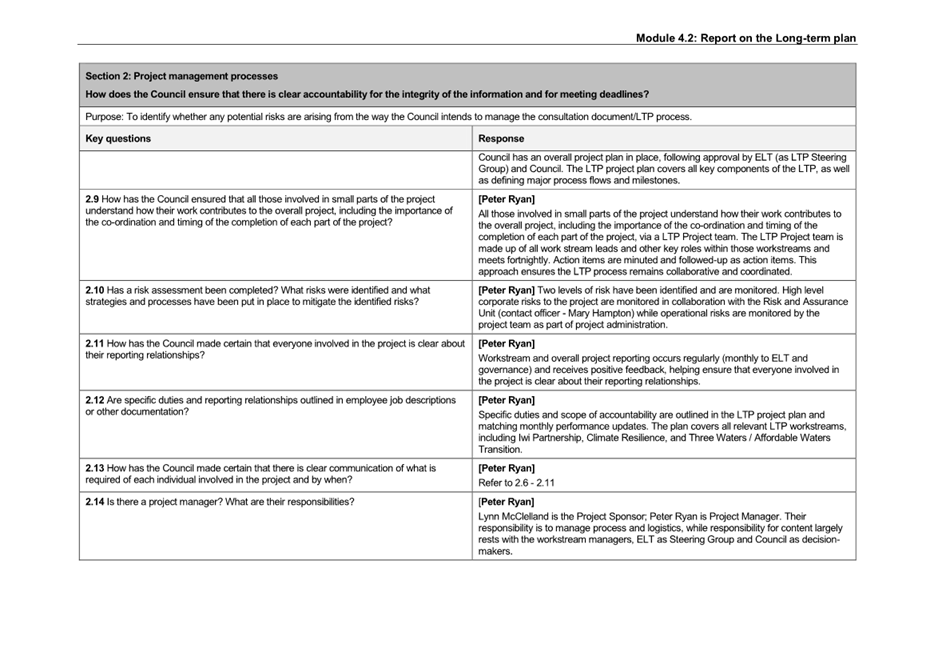

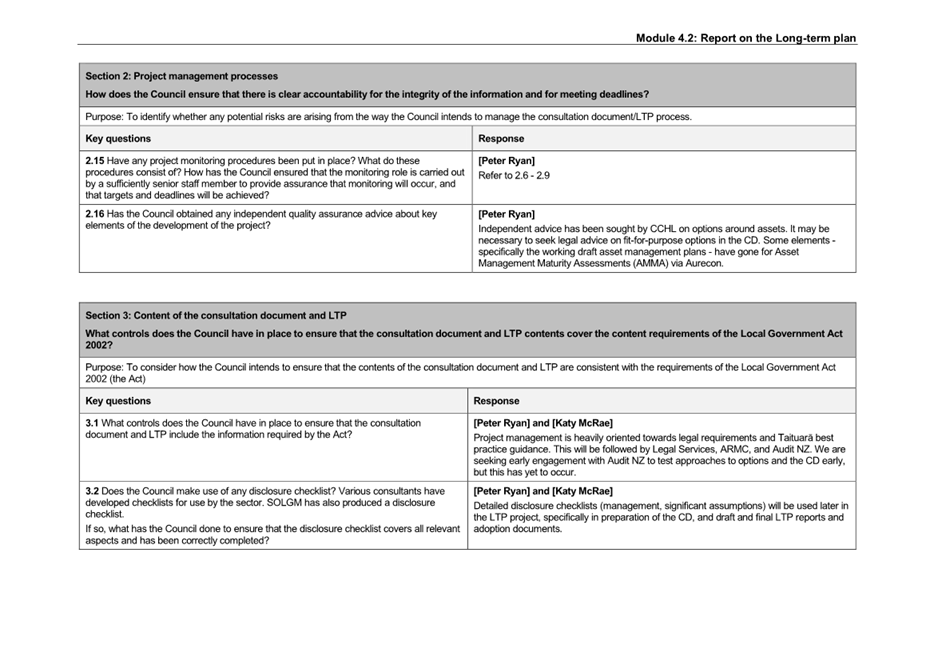

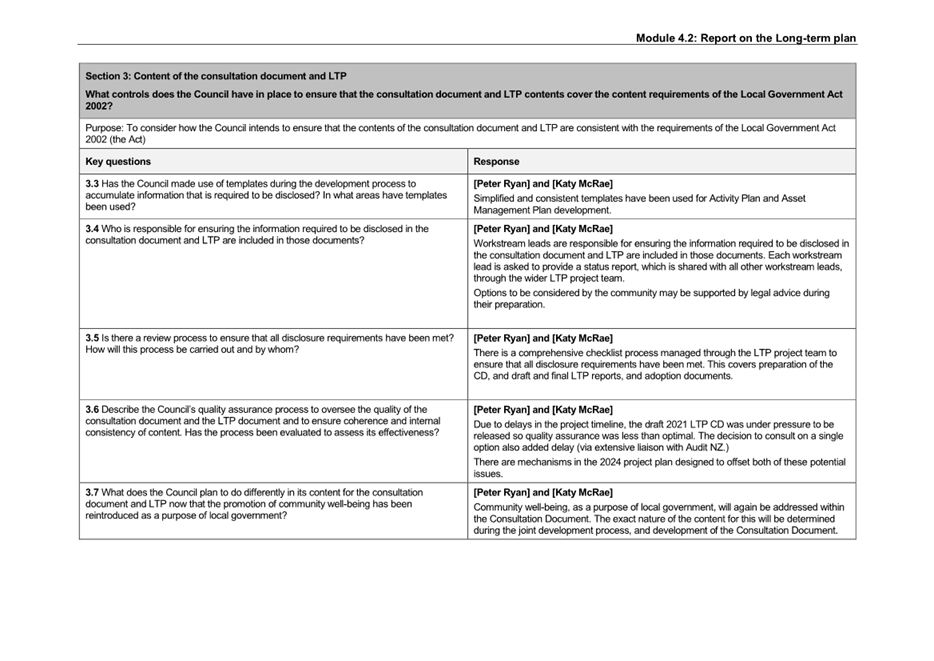

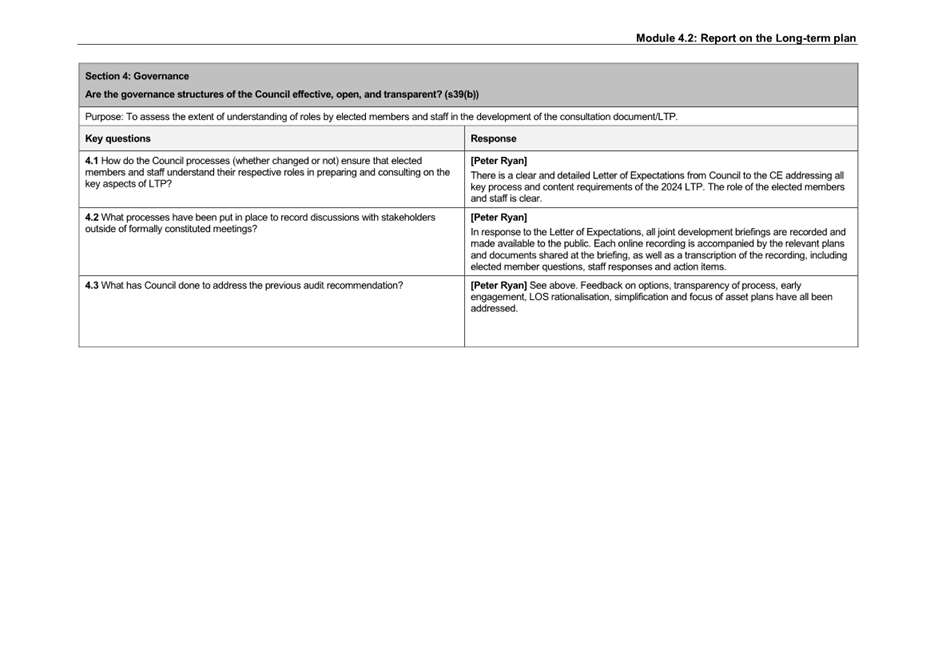

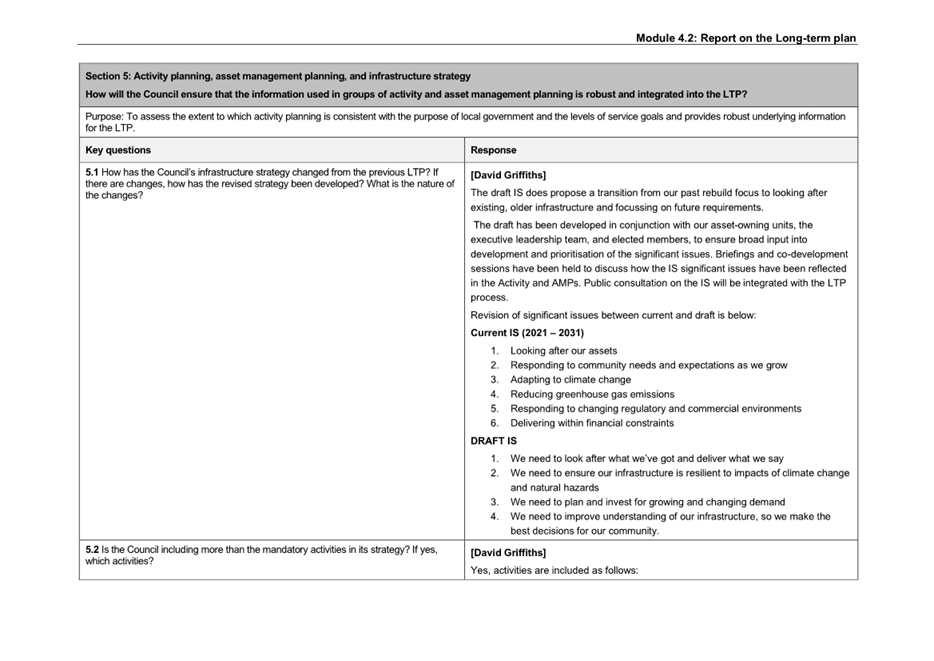

3.1 The

ARMC has requested updates on the implementation of the LTP 2024-34 development

project plan workstreams (Attachment A).

3.2 As

part of LTP development, Audit NZ recommend completion of their LTP

Self-Assessment review (Attachment B.)

4. Background Information Te Horopaki

4.1 Under

the Local Government Act 2002 a local authority must have an LTP in place at

all times. The structure, timing, information provided, and consultation

processes are defined by the legislation. LTPs are audited by the Office of the

Auditor-General through Audit NZ, and both draft and final LTPs are published

with the audit opinion.

4.2 The

flagship document of the LTP is the Consultation document (CD) which must set

out the challenges facing the city as well as the options and recommendations

of the Council for community consultation. This is the key document from

resident’s point of view.

4.3 It

is supported by Infrastructure and Financial Strategies that must have a

minimum horizon of 30 years. These too must set out the challenges, options and

recommendations that inform the LTP, as well as guiding the development of the

capital programme.

4.4 Supporting

these are technical documents (activity and asset management plans) that span

the Council’s services.

4.5 The

ARMC has requested regular updates on the implementation of the Long-term Plan

(LTP) 2024-34 development project plan.

4.6 At

the previous meeting of 20 June 2023 ARMC received:

4.6.1 the Letter of

Expectation from the Mayor and Council to staff, which sets out priorities to

be addressed as well as defining the LTP 2024-34 process;

4.6.2 confirmation of

governance structure for the LTP; Council is the decision-making body, the

Executive Leadership Team acts as the Steering Group, supported by an

operational Programme Management Group;

4.6.3 the adopted draft

Strategic Framework, and how Climate Resilience is being embedded in the LTP

2024;

4.6.4 information regarding

the high-level phasing and timings for the project;

4.6.5 an outline of the

individual workstreams within the project, including progress updates to that

point;

4.6.6 key risks, including

how these are reported and managed.

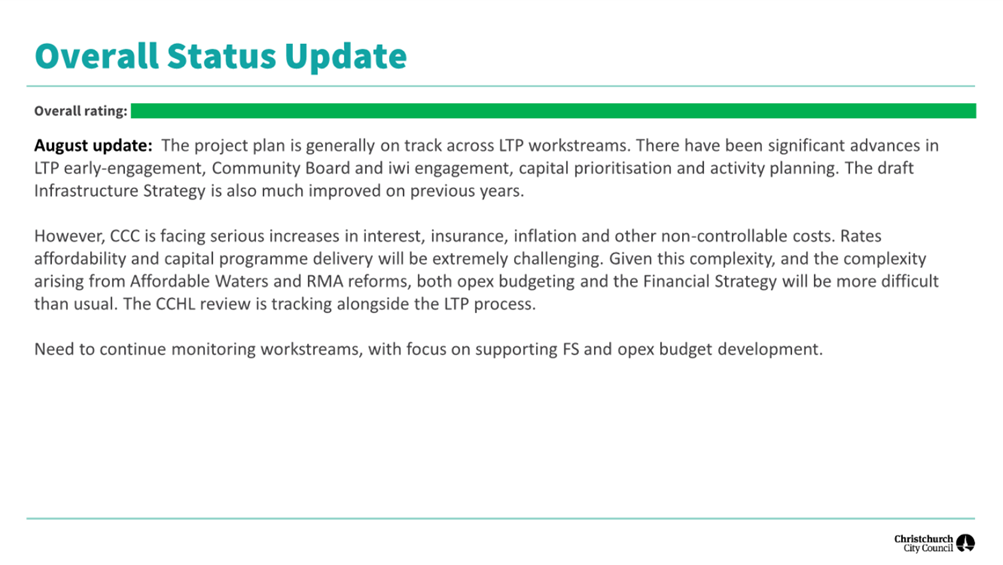

4.7 This

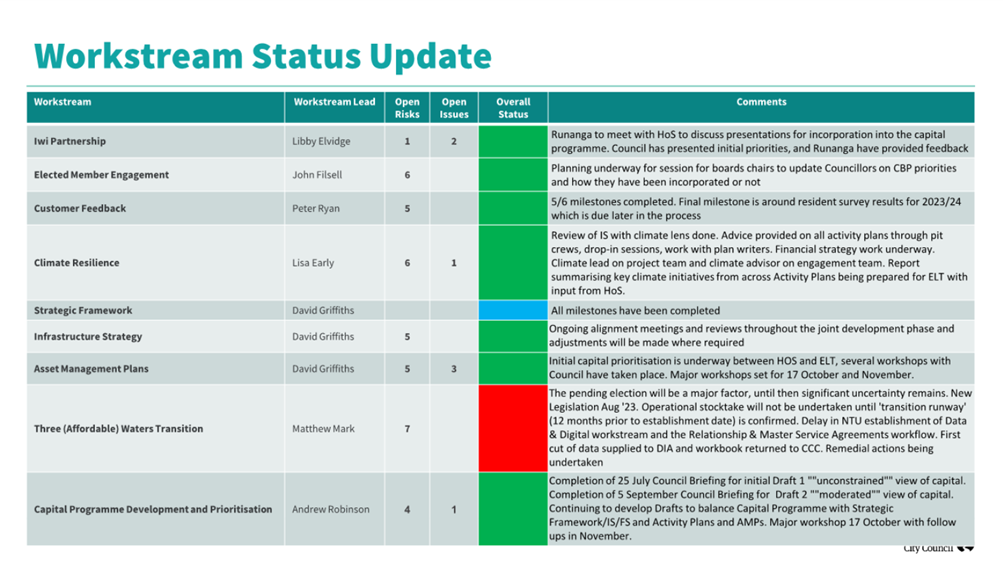

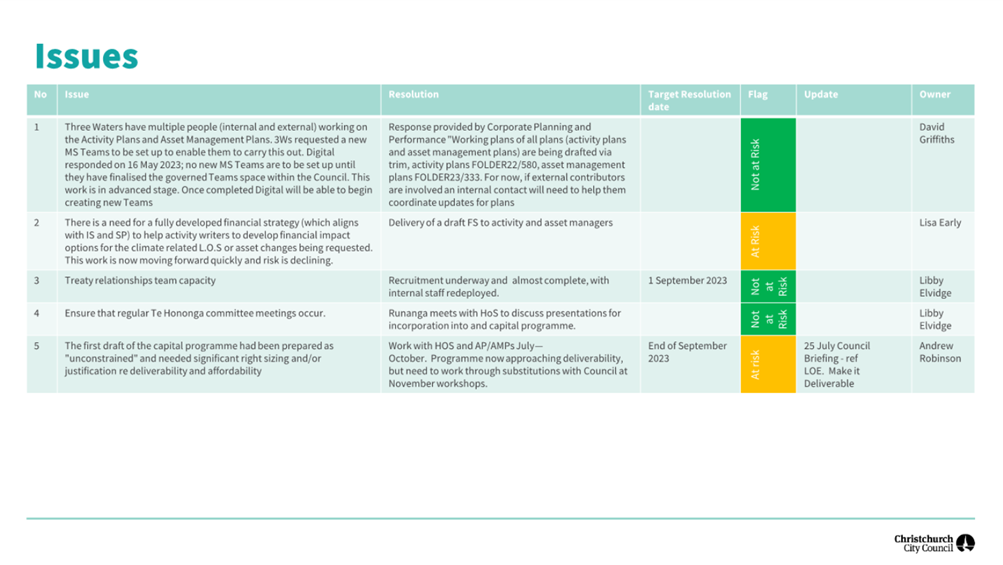

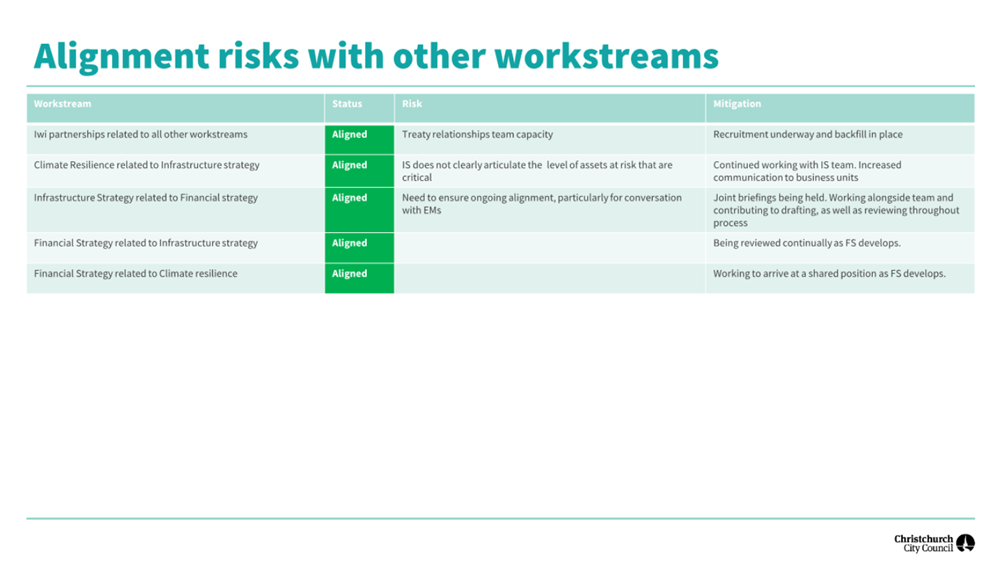

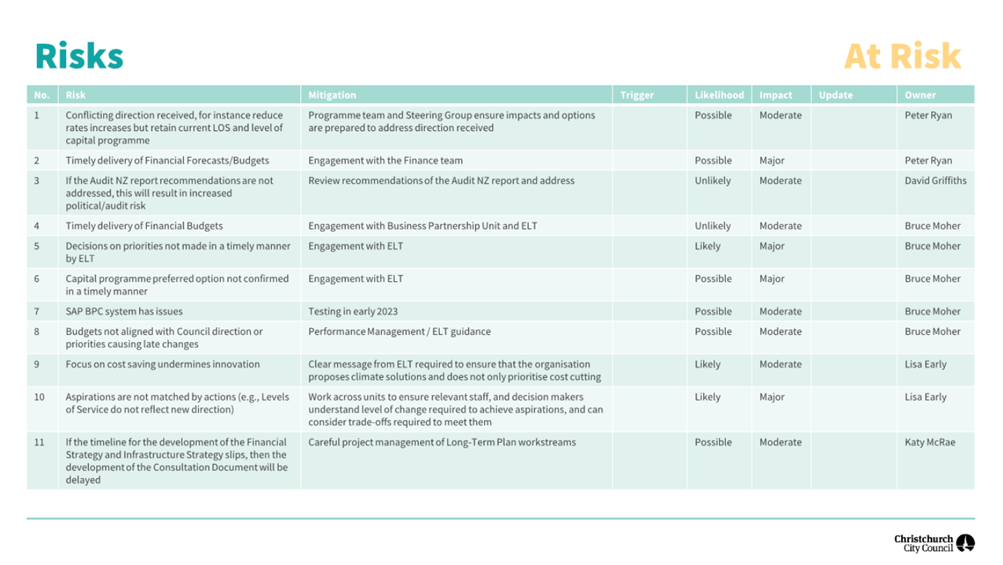

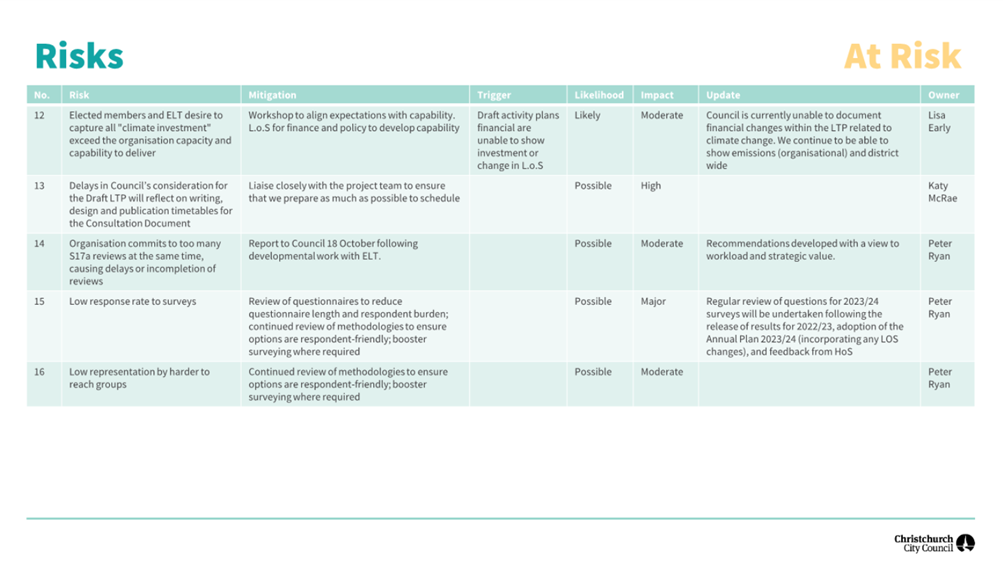

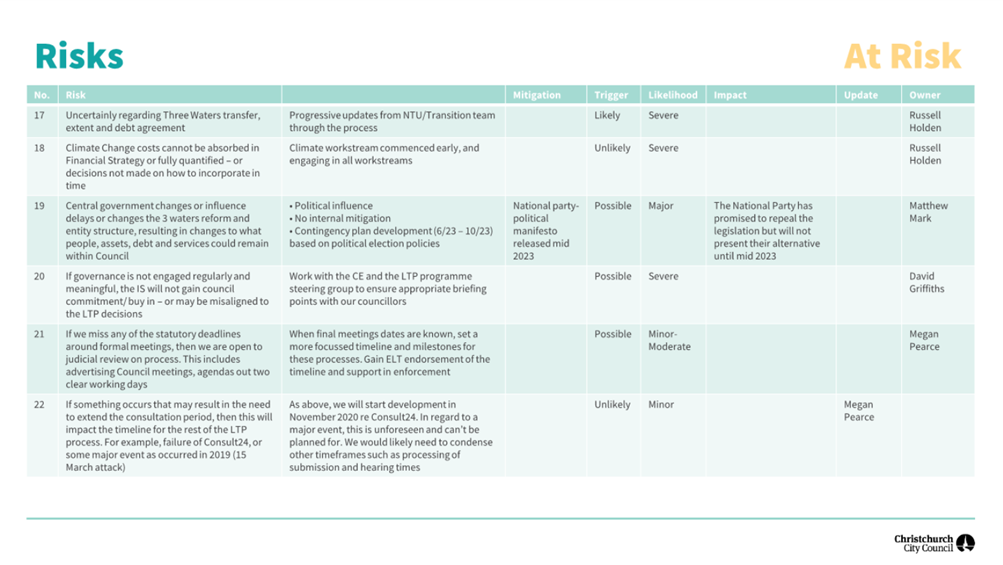

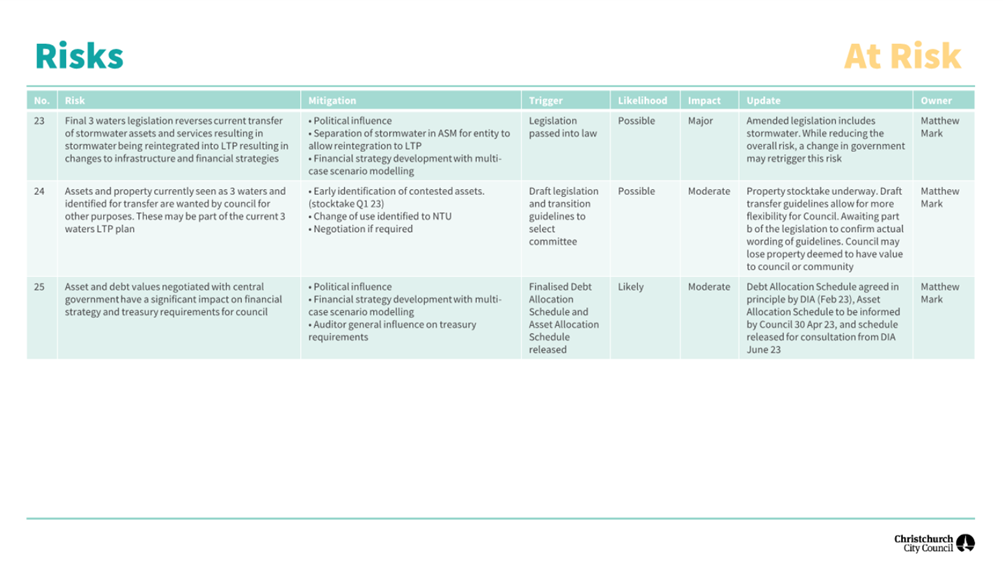

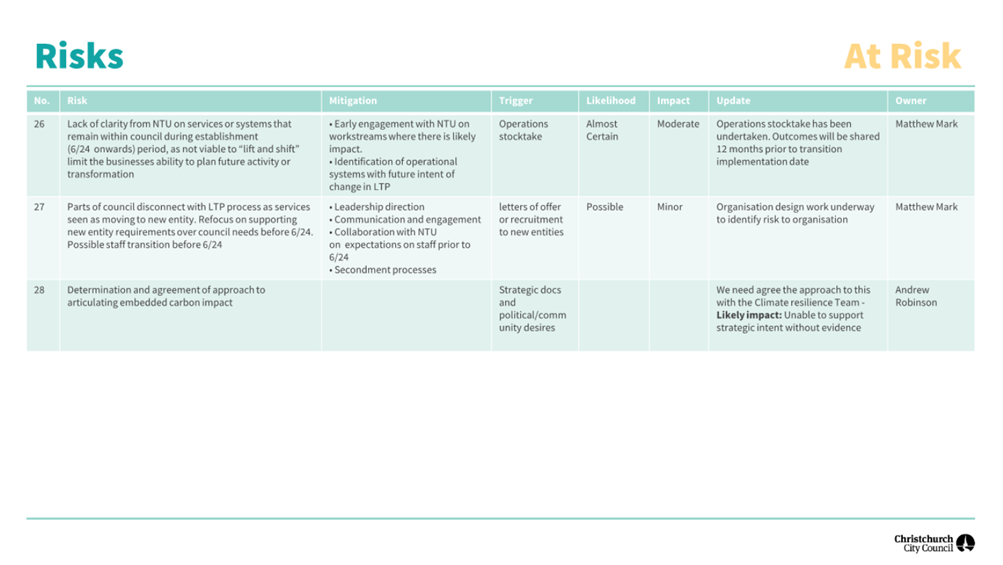

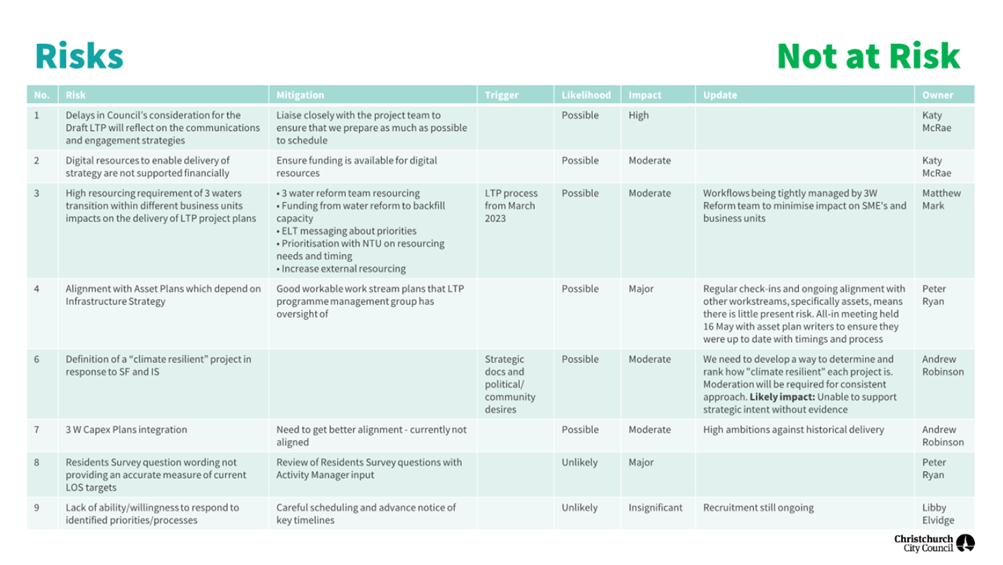

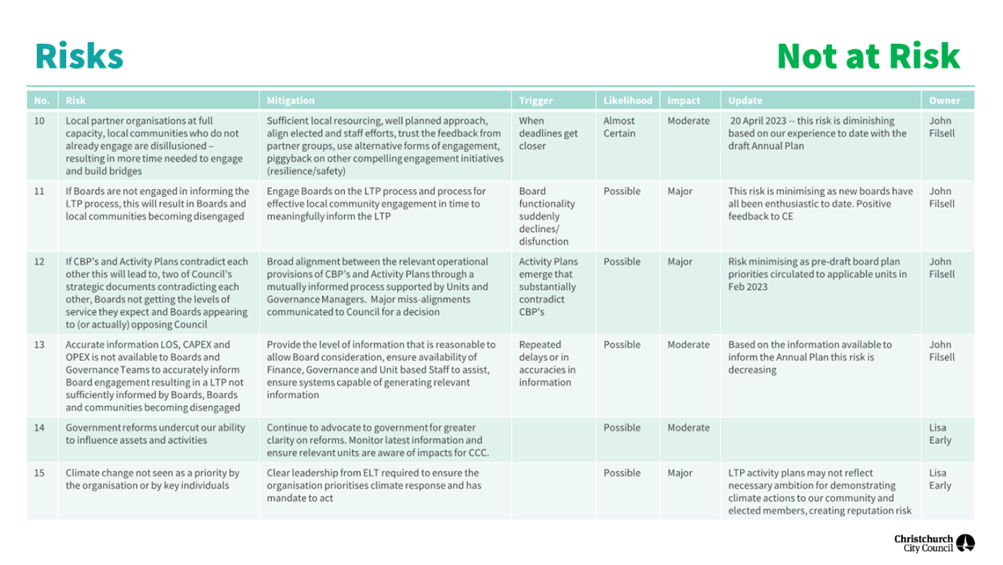

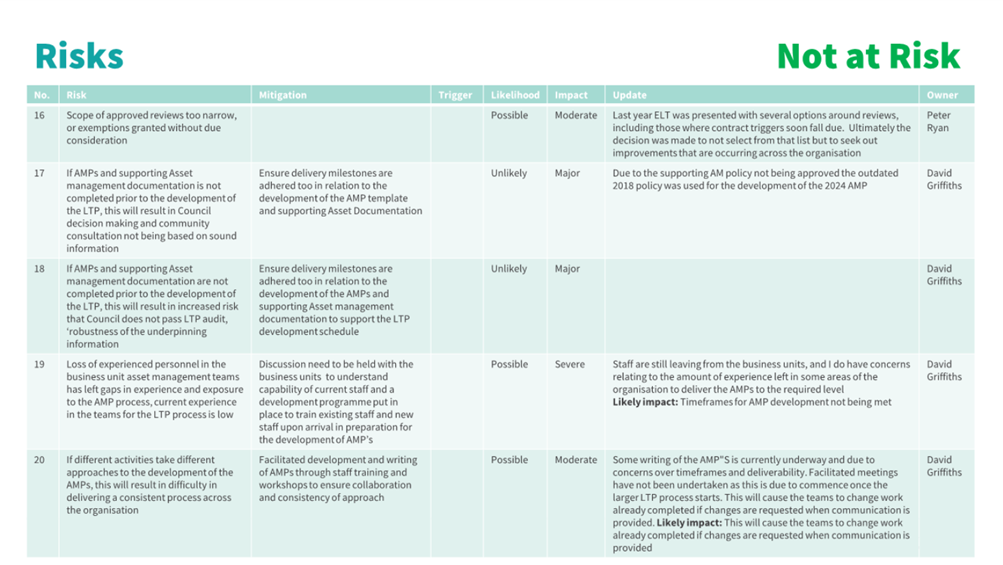

latest LTP 2024 progress report (Attachment A) summarises (at a high level)

risks to the overall project work streams, as well as risks to specific work

streams.

4.8 Each

work stream is led by an accountable Head of Service, and Heads of Service have

provided the information in these attachments. They will be available at the

ARMC meeting for further information as required.

4.9 Audit

NZ has previously supplied a detailed self-assessment tool to gauge readiness and

progress for the LTP and have confirmed this tool remains suitable for use with

some small adjustment. The Self-Assessment for LTP 2024-34 (Attachment B) has

been reviewed by the Executive Leadership Team.

4.10 Risks fall into

two types – content risk (in terms of the accuracy and timeliness of

content within a workstream) and alignment risk (in terms of consistency

between workstreams i.e., the Financial Strategy, the Infrastructure Strategy,

capital programme and asset plans).

4.11 During the

development phase of the LTP the focus is naturally on content risk. The areas

of greatest risk lie (as they normally do) finding the optimum balance between

service delivery, capital programme delivery, and rates increases.

4.12 To achieve this,

it is essential to develop a Financial Strategy that is aligned with the

Infrastructure Strategy and activity plan budgets.

4.13 Alignment of the

FS with a significant savings opex programme and an affordable/deliverable capital

programme is also critical.

4.14 Finally, the FS

informs the way in which options for community consultation should occur in the

Consultation Document.

4.15 Framing these

options in a way that can be easily understood by the community (and which

clearly set out the implications of those options) is critical to the success

of the LTP, and to minimise the risk of criticism or (successful) challenge to

the LTP process.

4.16 Other key risk

areas include confidence around asset condition and performance data, and

ability to meet the project milestones and timeline.

4.17 As these issues

are resolved (or substantively resolved), focus will move to alignment risks.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

LTP 2024-34

Project Update

|

23/1602401

|

22

|

|

b ⇩

|

CCC LTP Self

Assessment (Audit NZ)

|

23/1621140

|

35

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Confirmation of Statutory

Compliance Te Whakatūturutanga ā-Ture

|

Compliance with Statutory Decision-making

Requirements (ss 76 - 81 Local Government Act 2002).

(a) This report contains:

(i) sufficient information about all reasonably practicable

options identified and assessed in terms of their advantages and

disadvantages; and

(ii) adequate consideration of the views and preferences of

affected and interested persons bearing in mind any proposed or previous

community engagement.

(b) The information reflects the level of significance of the

matters covered by the report, as determined in accordance with the Council's

significance and engagement policy.

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Amber Tait -

Performance Analyst

Boyd Kedzlie -

Senior Business Analyst

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Lynn

McClelland - Assistant Chief Executive Strategic Policy and Performance

|

|

Audit and Risk Management Committee

16 October 2023

|

|

|

Audit and Risk Management Committee

16 October 2023

|

|

|

Audit and Risk Management Committee

16 October 2023

|

|

|

10. Audit and Risk Quarterly Update

|

|

Reference / Te Tohutoro:

|

23/1539528

|

|

Report of / Te Pou Matua:

|

Nicholas

Hill, Head of Risk and Assurance (Nicholas.Hill@ccc.govt.nz)

|

|

Senior Manager / Pouwhakarae:

|

Leah

Scales, General Manager Resources/Chief Financial Officer

(Leah.Scales@ccc.govt.nz)

|

1. Purpose and Origin of Report Te Pūtake Pūrongo

1.1 Risk and Assurance regularly supports management across a

range of matters that may be relevant to the Committee. Progress reporting to

the Committee about improving the maturity of the Council's risk and assurance

related systems.

1.2 Council Risk and Assurance Unit.

2. Officer Recommendations Ngā Tūtohu

That the Audit and

Risk Management Committee:

1. Receive the information in the Risk and Assurance Update Report.

3. Risk Management Update

Risk Assurance Statement

3.2 During

the reporting period the Protected Disclosure Officer received three (3) separate

disclosures of concerns around serious wrongdoing. The disclosures have been

reviewed and communicated with the Chief Executive for decision on further

action.

Activity

during the quarter

3.1 The risk function

has supported the Long-Term Planning Project Team with refreshing the risk

associated with the project. The aim of this process was to ensure that all

risks are still relevant and to identify any new or emerging risks.

3.2 The Risk and

Assurance unit ran an hour-long risk workshop with the Executive Leadership

Team (ELT). The workshop covered the perceived understanding of the current

working environment. The workshop was also an opportunity to introduce new

staff members to the ELT and prepare for the Councillor Risk Workshop.

3.3 The risk function

ran a risk workshop with Councillors, Executive Leadership Team and independent

ARMC members. The workshop covered risk 101 and explored their risk appetite

against the draft strategic priorities. The workshop was well received by those

who attended.

3.4 The implementation

of agreed actions from the internal fraud audit continues. We have developed

two eLearning packages: Fraud and Corruption Prevention and Protected

Disclosures. These trainings cover essential definitions, interactive knowledge

checks and how staff can report concerns within and outside the Council.

Activity planned for the next

quarter

3.5 The

risk function will work alongside People and Culture to develop an improvement

work program focusing on the conflict-of-interest process at the Council.

3.6 The

risk function will continue to implement and embed the internal fraud audit

recommendations.

Situational safety risk assessment

3.7 In

response to a request from ARMC, the Risk and Assurance team have developed a

high-level risk assessment around the situational safety of elected members and

high-profile senior staff. Although high-level, the risk assessment has

reviewed several keys areas as outlined below.

3.8 Staff

feeling – a survey was sent to both senior and high-profile staff asking

some basic questions around perceived risk and how high profile they believed

they were. Results of the survey were analysed and factored into the risk

assessment.

3.9 Climate

Activism - Climate Activism in New Zealand, is

diverse and dynamic, with various groups and individuals pushing for climate

action at different levels of society. The movement is characterized by a sense

of urgency and a commitment to holding both the government and private sector

accountable for addressing climate change.

3.10 Physical threats

- refer to actions or circumstances that pose a direct danger or harm to a

person's physical well-being, safety, or bodily integrity. These threats can

manifest in various forms, including violence, assault, accidents, or natural

disasters, and may result in physical injuries or harm.

3.11 Psychological

threats - involve situations or actions that can harm an individual's mental or

emotional well-being. These threats can encompass various forms of stress, manipulation,

intimidation, Harassment, or emotional abuse, and may lead to psychological

distress, anxiety, or trauma.

3.12 Reputational

threats – such a scandal, in fighting, negative media coverage, social

media attacks, hacking, data breaches, or online harassment all contribute to

reputational damage. The Council and its staff are under constant

scrutiny, in the name of being held accountable by the people of Christchurch

City. Any mistake or perceived mistake is analysed, publicised, and dissected

by media and self-appointed watchdogs. These agencies or individuals

often see it as their responsibility to call out anything they disagree with

using both the mainstream and social media as a platform.

3.13 A Vulnerability

Assessment has also been undertaken as part of the risk assessment.

Physical, Cyber and Reputational Vulnerability were analysed, and relevant

controls identified and assessed for effectiveness.

3.14 WorkSafe

guidelines have also been reviewed to ensure we are in line with best practice around

controls for key areas such as architectural/layout, policies and procedures,

training, emergency process and other security measures.

3.15 The risk

assessment is complete; however, the report and recommendations are still being

compiled. The report will be presented and discussed with ELT in the next

two weeks and presented to ARMC at the next appropriate opportunity.

4. Internal Audit Update

Internal Audit Statement

4.1 Internal

Audit continues to provide independent review and support to the other business

units as necessary. While several discussions have been held with various

business units over the quarter, there are no matters of material significance

that needs to be reported.

Activity during the quarter

4.2 The primary focus

for the Internal Audit team during the quarter has been the finalisation and

assisting in management response to the independent review of the Christchurch

Wastewater Treatment Plant fire and recovery response.

4.2.1 The review primarily focuses on how the

Council responded to the fire, and how the Council communicated key decisions

and concerns to the wider community.

4.2.2 The final report has been received and

endorsed by the ELT.

4.2.3 The management action plan has been

completed as collaboration between a number of business units that are involved

in the key processes. The management action plan has also been endorsed by the

ELT.

4.2.4 The final

report along with the management action plan will be presented to the Council

in the next Council meeting on 18 October.

4.3 Internal

Audit team also assisted in finalising the management action plan in response

to the independent FTE controls review. This matter is discussed as a separate

agenda item for the ARMC meeting.

4.4 Internal Audit has reviewed and updated the Internal Audit Plan to

reflect the risks currently relevant to the Council. The Audit Plan has gone

through multiple internal quality assurance reviews and have been reviewed by

the Council’s Internal Audit Partner, KPMG for reasonableness. The Internal

Audit Plan will need to be discussed with the ARMC Chair initially before it is

presented to the ARMC for feedback and endorsement.

4.5 Internal Audit is also in process of planning and developing the

Council’s assurance mapping based on identified strategic risks. The

assurance mapping is intended to provide a snapshot view of the Council’s

strategic risks and captures both the gross risk scores prior to any assurance

and controls and the net risk score post all assurance. This tool will assist

to determine whether assurance is required, and whether internal audit review

is required.

4.6 To gain coverage and assurance over wider business operations and

risks, the Internal Audit team are working on developing and establishing

methodology for speed analysis reviews. Whilst the speed analysis review will

not be replacing the traditional audit reviews which are more complex in

nature, the speed analysis review is planned to be completed on a rotational

basis along with the traditional audit reviews. The traditional audits are more

detailed and complex, which are inherently more time consuming. The speed

analysis review intends to review a specific pain spot within a process to

provide audit recommendations in a more time efficient manner.

Activity planned for the next quarter

4.7 Internal

Audit will continue to work through planned and unplanned work based on

priority and risk. Due to high volume of high-risk unplanned work, there is

backlog of planned work and this will be addressed accordingly.

4.8 Internal

Audit will finalise the Internal Audit Plan subsequent to review and

endorsement from the relevant stakeholders.

4.9 Internal

Audit will work towards finalising the assurance mapping and speed analysis

review methodology.

4.10 Internal Audit

will continue to support other business units with independent review and

support as necessary.

Attachments Ngā Tāpirihanga

There are no

attachments to this report.

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Confirmation of Statutory

Compliance Te Whakatūturutanga ā-Ture

|

Compliance with Statutory Decision-making

Requirements (ss 76 - 81 Local Government Act 2002).

(a) This report contains:

(i) sufficient information about all reasonably practicable

options identified and assessed in terms of their advantages and

disadvantages; and

(ii) adequate consideration of the views and preferences of

affected and interested persons bearing in mind any proposed or previous

community engagement.

(b) The information reflects the level of significance of the

matters covered by the report, as determined in accordance with the Council's

significance and engagement policy.

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Min Jang -

Senior Internal Auditor

Nicholas Hill

- Head of Risk & Assurance

Mary Hampton -

Senior Risk Advisor

Mike Marr -

Manager Internal Audit

|

|

Approved By

|

Russell Holden

- Acting General Manager Resources/Chief Financial Officer

|

|

Audit and Risk Management Committee

16 October 2023

|

|

|

11. Resolution to Exclude the Public

|

Section 48, Local Government Official

Information and Meetings Act 1987.

I move that the public be excluded from the

following parts of the proceedings of this meeting, namely items listed

overleaf.

Reason for passing this resolution: good

reason to withhold exists under section 7.

Specific grounds under section 48(1) for

the passing of this resolution: Section 48(1)(a)

Note

Section 48(4) of the Local Government

Official Information and Meetings Act 1987 provides as follows:

“(4) Every resolution to exclude the

public shall be put at a time when the meeting is open to the public, and the

text of that resolution (or copies thereof):

(a) Shall

be available to any member of the public who is present; and

(b) Shall

form part of the minutes of the local authority.”

This resolution is made in reliance on

Section 48(1)(a) of the Local Government Official Information and Meetings Act

1987 and the particular interest or interests protected by Section 6 or Section

7 of that Act which would be prejudiced by the holding of the whole or relevant

part of the proceedings of the meeting in public are as follows:

|

Audit and Risk Management Committee

16 October 2023

|

|

|

ITEM NO.

|

GENERAL SUBJECT OF EACH MATTER TO BE CONSIDERED

|

SECTION

|

SUBCLAUSE AND REASON UNDER THE ACT

|

PLAIN ENGLISH REASON

|

WHEN REPORTS CAN BE RELEASED

|

|

7.

|

Procurement and Contracts Unit FY23 Q4 Report

|

|

|

|

|

|

|

Attachment a - Attachment A - Financial

Benefits FY23

|

s7(2)(b)(ii), s7(2)(h), s7(2)(j)

|

Prejudice Commercial Position, Commercial Activities, Prevention

of Improper Advantage

|

Terms negotiated with suppliers that could prejudice their

commercial position

|

27 September 2024

On review of Head of Procurement and Contracts

|

|

|

Attachment b - Attachment B - Non-Financial

Benefits for FY23

|

s7(2)(b)(ii), s7(2)(h), s7(2)(j)

|

Prejudice Commercial Position, Commercial Activities, Prevention

of Improper Advantage

|

Terms negotiated with suppliers that could prejudice their

commercial position

|

27 September 2024

On review of Head of Procurement and Contracts

|

|

12.

|

Public Excluded Audit and Risk Management

Committee Minutes - 3 August 2023

|

|

|

Refer to the previous public excluded reason in the agendas for

these meetings.

|

|

|

13.

|

Cyber Security Programme Update and Report

|

s7(2)(c)(i)

|

Protection of Source of Information

|

Disclosure of our approach to cyber security will increase the

risk of Council being a target, resulting in potential service disruptions

and / or information breaches that will not be in the public interest.

|

This report may only be released if the Chief Executive has

determined that there are no longer any reasons under the Local Government

Official Information and meeting Act to withhold the information.

|

|

14.

|

Audit Engagement Letter and Fees Proposal

Update

|

s7(2)(h)

|

Commercial Activities

|

Negotiations on the level and structure of the fee proposals are

in discussion.

|

When a suitable audit fees agreement has been reached with Audit

New Zealand and confirmed to by the Audit and Risk Management Committee.

|

|

15.

|

Council Draft Annual Report for the year

ended 30 June 2023

|

s7(2)(b)(ii), s7(2)(h)

|

Prejudice Commercial Position, Commercial Activities

|

The information to be used as the basis for the finalisation of

the Council's 2023 Annual Report remains subject to change. The Committee has

a responsibility to consider and review the annual report before adoption by the

Council and to hold it in confidence before it is finalised for adoption, and

it is in the public interest that the committee can review the annual report

before it is publicly available.

|

31 October 2023

The information included in, and attached to, the staff report

will be available on the public agenda for the 31 October 2023 meeting of the

Council.

|

|

16.

|

FTE Controls Review

|

s7(2)(a), s7(2)(b)(ii)

|

Protection of Privacy of Natural Persons, Prejudice Commercial

Position

|

To protect the privacy of individuals.

|

On reveiw and appropriate redaction of the report by the Official

Information team and by the Head of Legal and Democratic Services and then

approved by the appropriate delegates.

|

|

17.

|

Christchurch City Holdings Ltd - FY23 Update

to ARMC Report

|

s7(2)(b)(ii)

|

Prejudice Commercial Position

|

The release of the internal control system review would prejudice

the commerical position of CCHL.

|

That the Report may only be released if the Chief Executive has

determined that there are no longer any reasons under the Local Government

Official Information and Meetings Act to withhold the information.

|