|

3. Draft

Annual Plan 2025-26

|

|

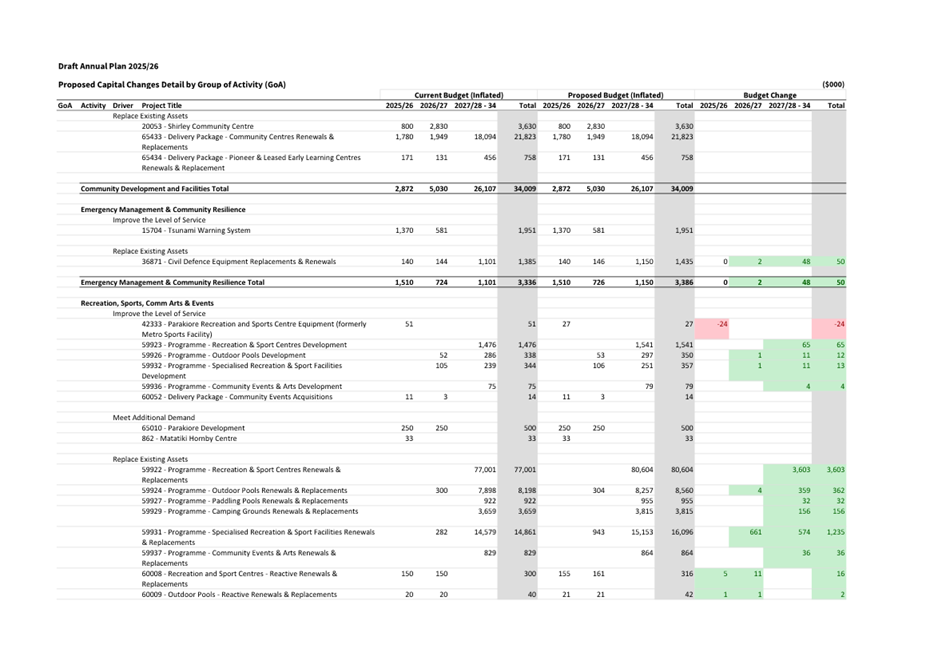

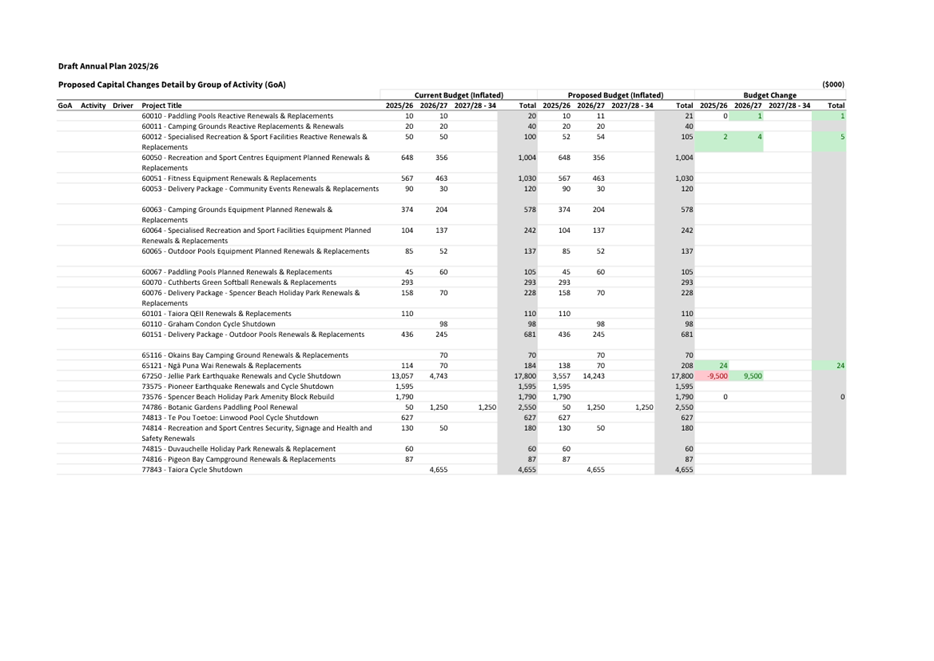

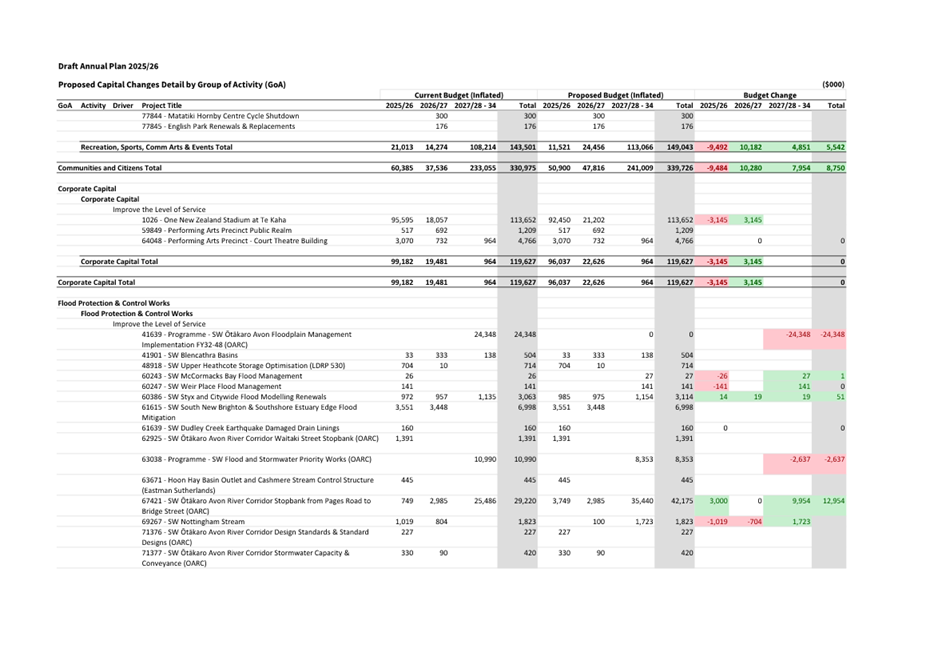

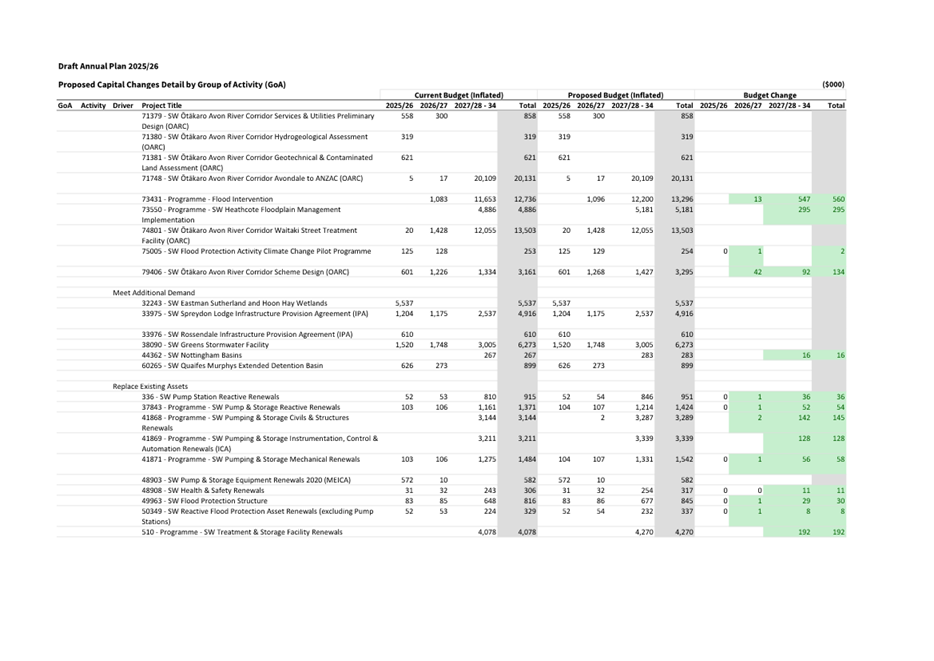

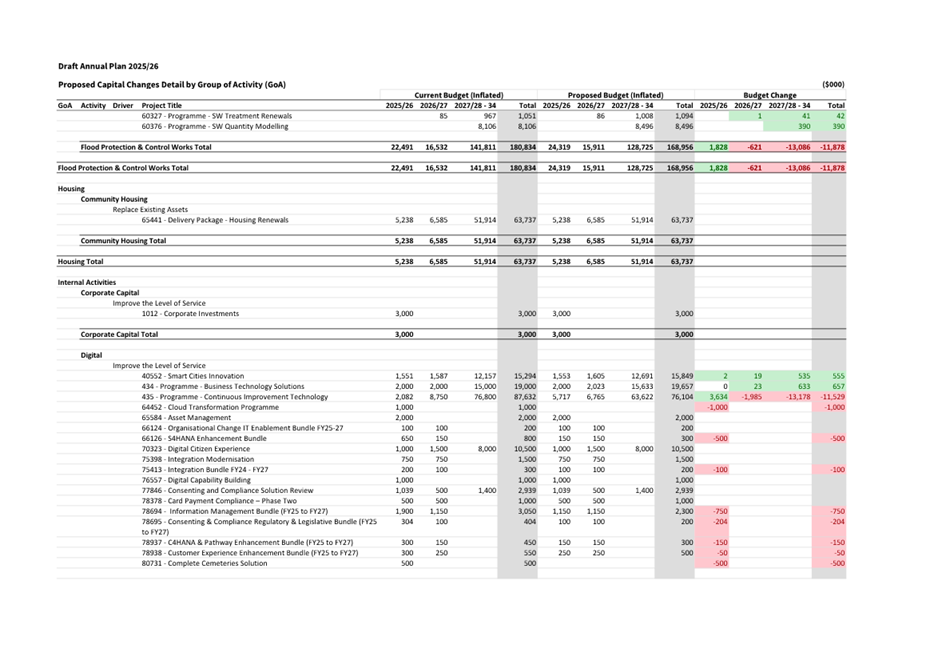

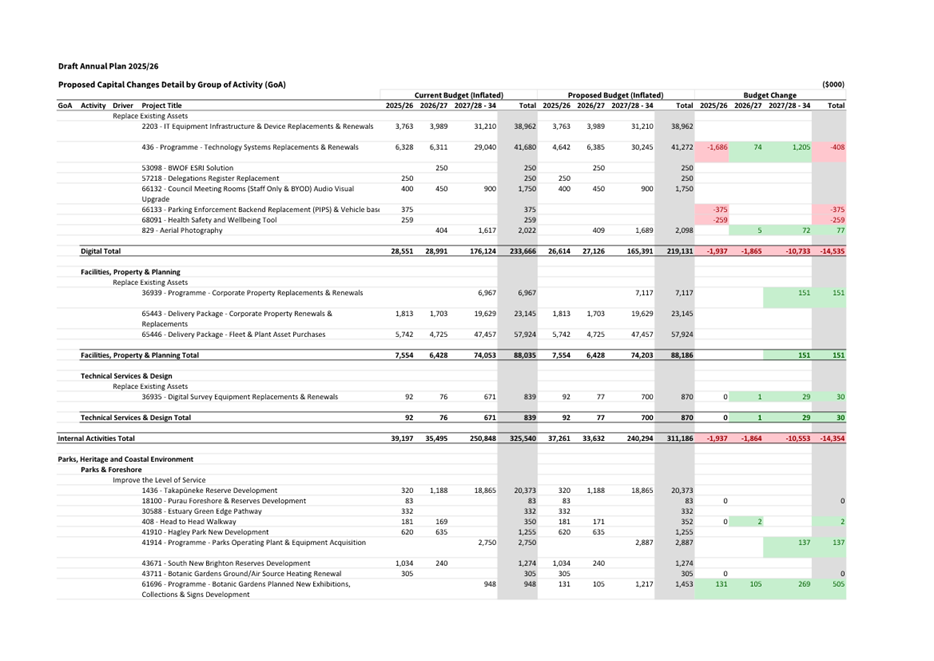

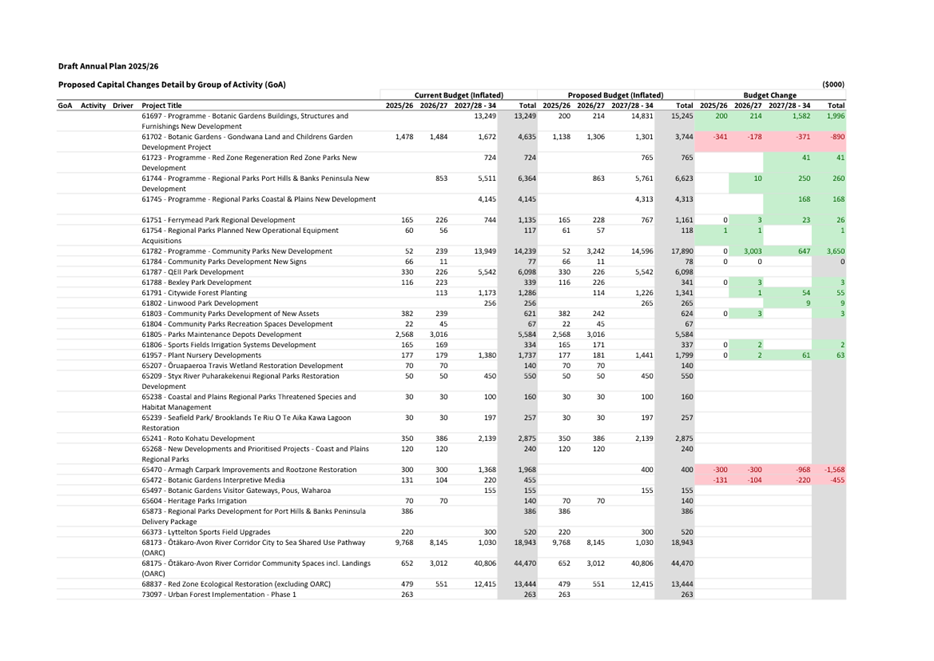

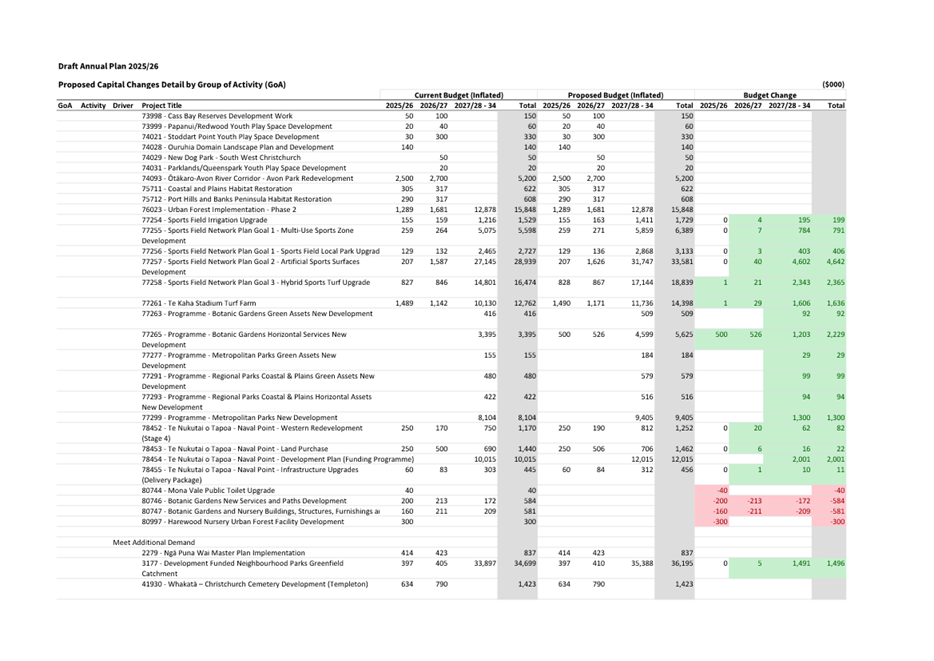

Reference Te Tohutoro:

|

24/2254465

|

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Performance & Planning

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to present to the Council for consideration and

adoption:

· The

Draft 2025/26 Annual Plan, including attached documents;

· The

Draft 2025/26 Annual Plan Consultation Document; and

· The

Draft 2025/26 Annual Plan consultation and engagement process to be undertaken.

1.2 The

Council is required to prepare and adopt an Annual Plan for each financial year

(s.95(1) Local Government Act 2002). The purpose of the plan is to:

· contain

the proposed annual budget and funding impact statement for 2025/26;

· identify

any variation from the financial statements and funding impact statement in the

Council’s Long-Term Plan for 2024-34;

· provide

integrated decision-making and co-ordination of the Council’s resources;

and

· contribute

to the accountability of the Council to the community.

1.3 The

decisions in this report are of high significance in relation to the

Christchurch City Council’s Significance and Engagement Policy. The

Council’s Draft Annual Plan for 2025/26 varies to some degree the

information contained in the Long-Term Plan (LTP) 2024-34 for that year.

Individually, these changes may not be regarded as being significant or

material, however collectively they are significant when the relevant factors

in Council’s Significance and Engagement Policy are considered.

2. Officer Recommendations Ngā

Tūtohu

That the Council:

1. Receives the information in the Draft Annual

Plan 2025-26 report.

2. Notes that the decisions in this report are of

high significance in relation to the Christchurch City Council’s

Significance and Engagement Policy.

3. Notes the Recommendations of the

Council’s Audit and Risk Management Committee at its meeting on 10

February 2025, (Attachment A of this report to be provided under separate

cover).

4. Approves and adopts for consultation the

information contained or referred to in the staff report which provides the

basis for the Draft 2025/26 Annual Plan, together with any amendments made by

resolution at the meeting, and which includes the following attachments of this

report:

a. Financial Overview, including financial

changes to that contained in the Long-Term Plan 2024-2034 (Attachment B).

b. Funding Impact Statement (Attachment C).

c. Rating information (Attachment D)

d. Financial Prudence Benchmarks (Attachment E).

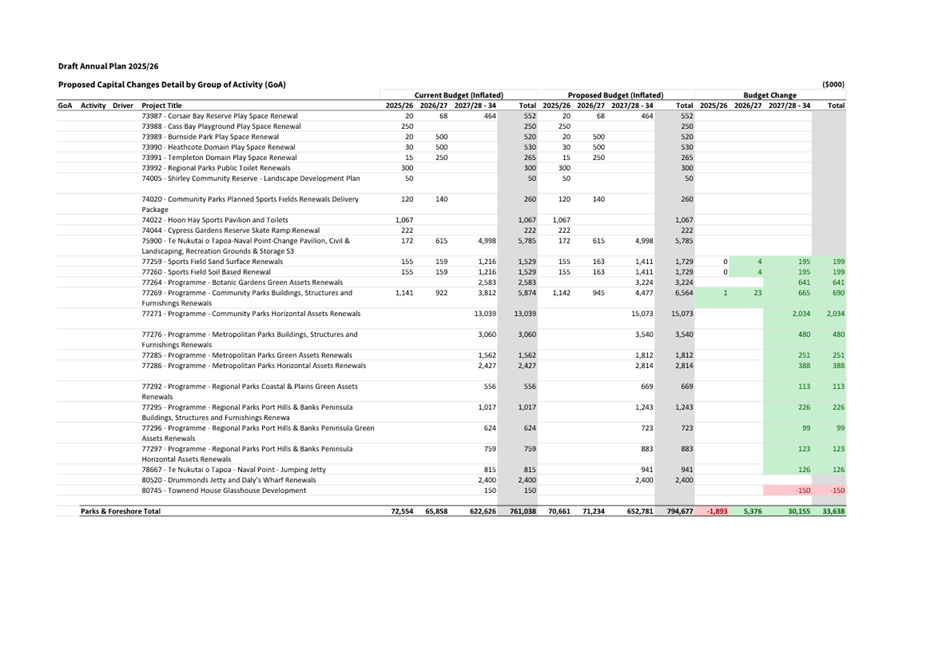

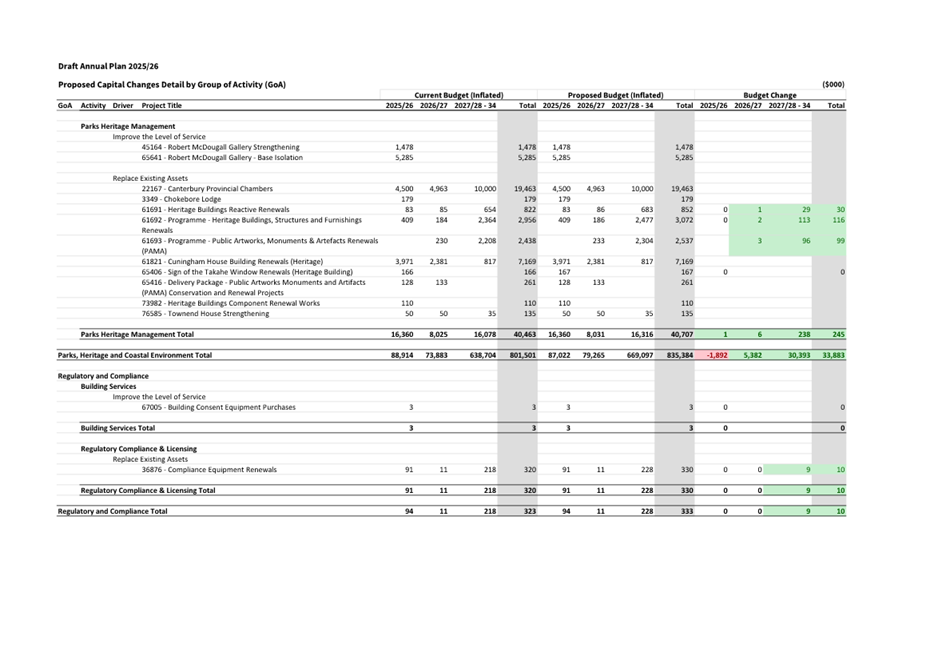

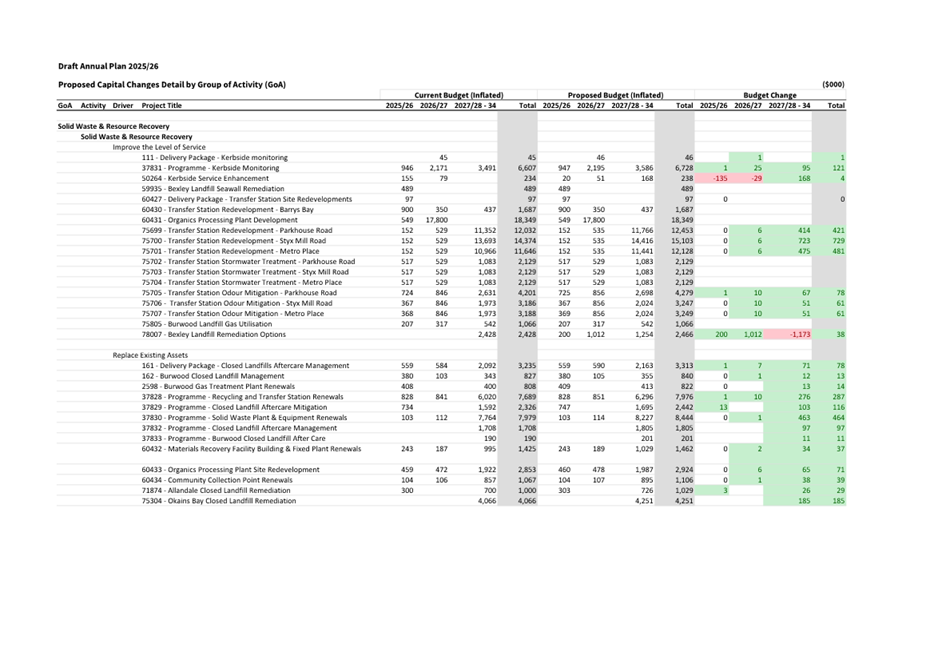

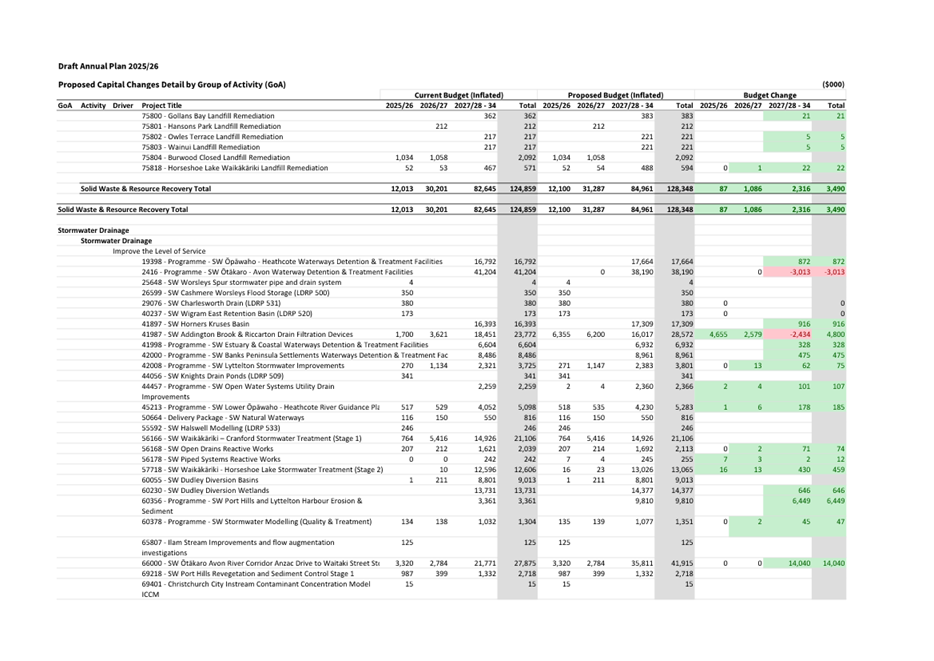

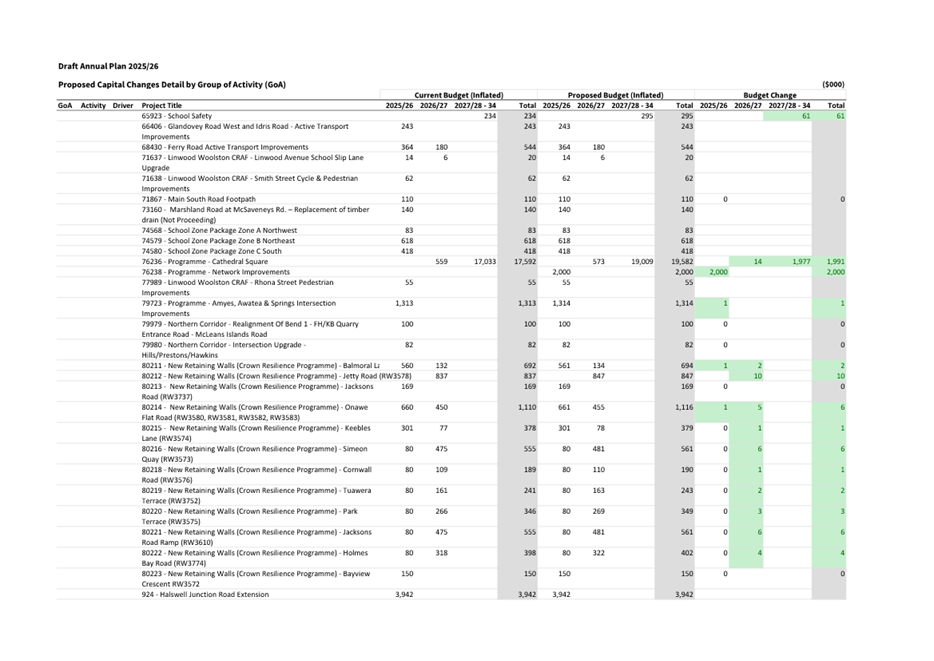

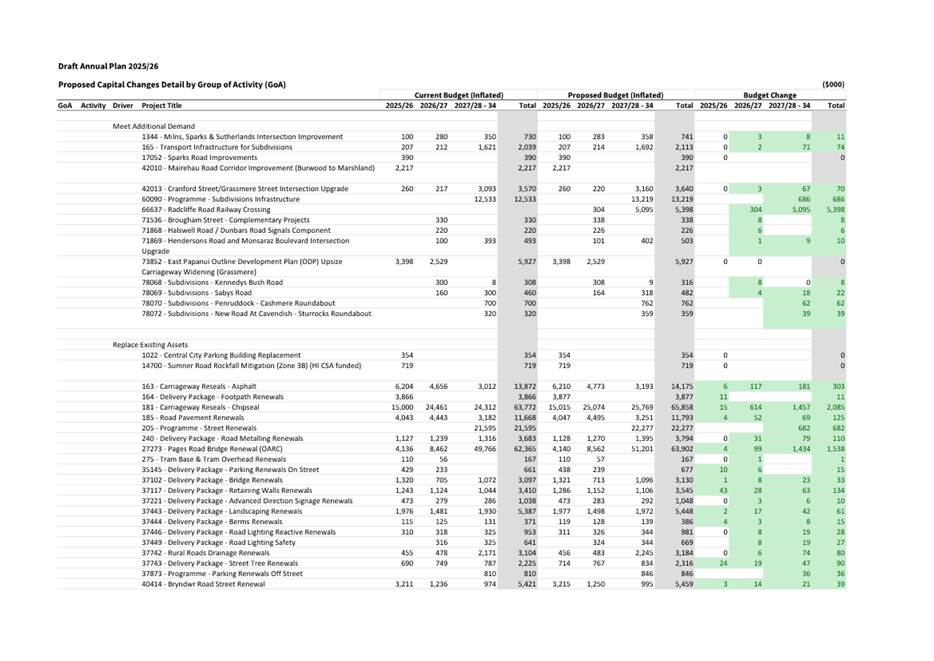

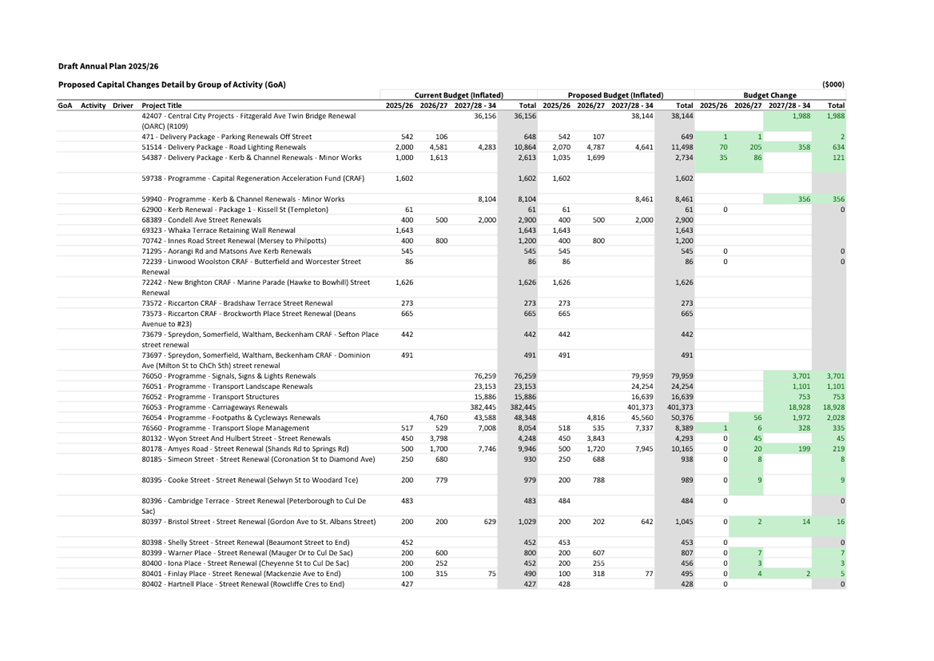

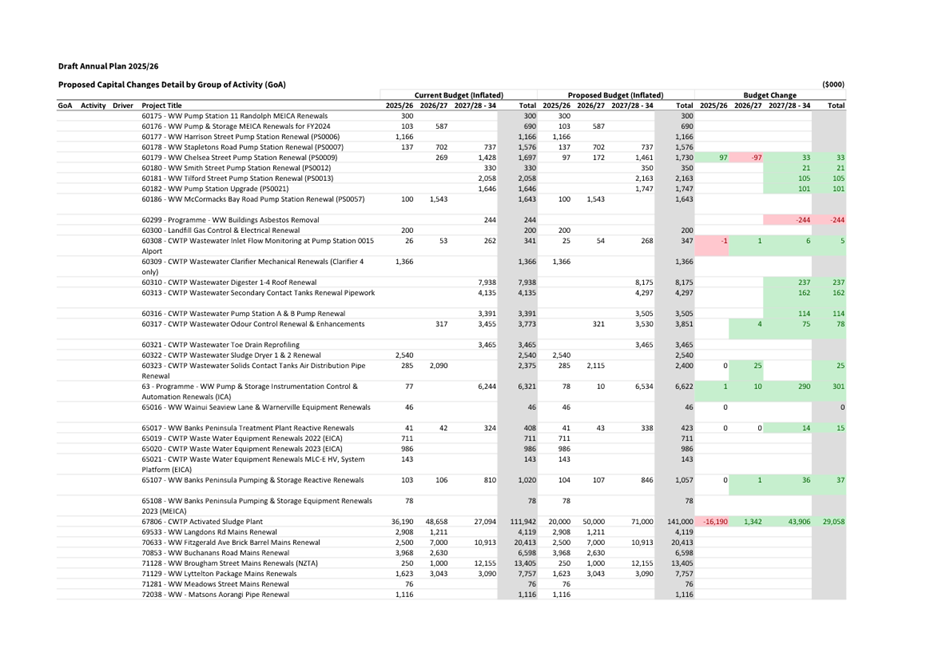

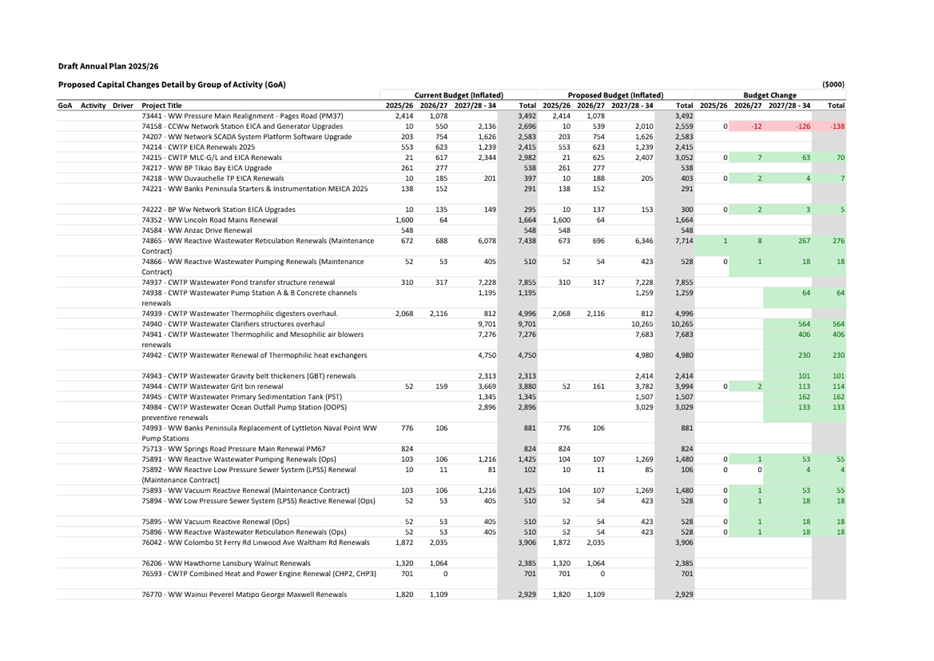

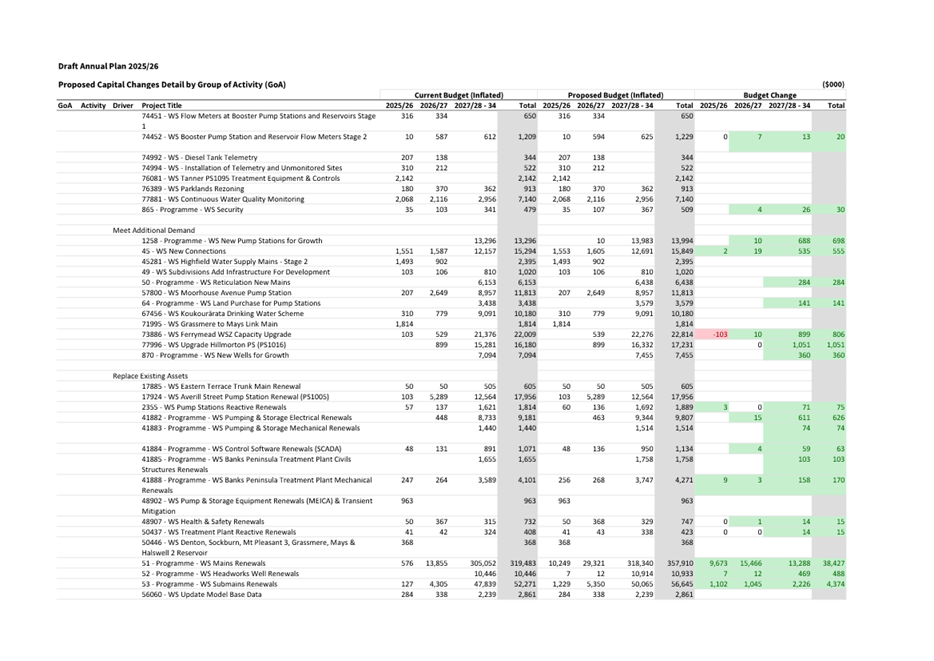

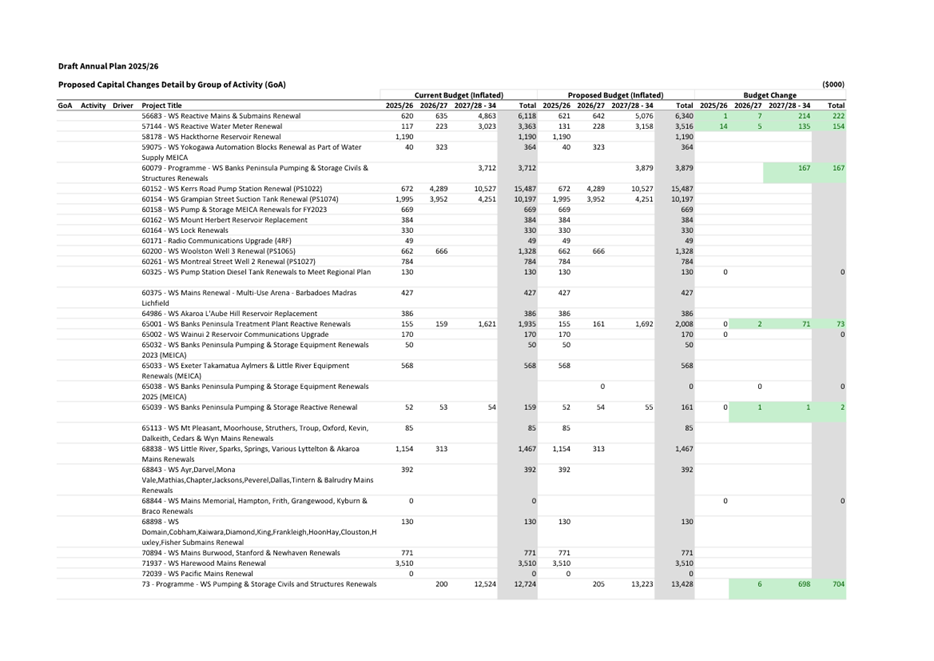

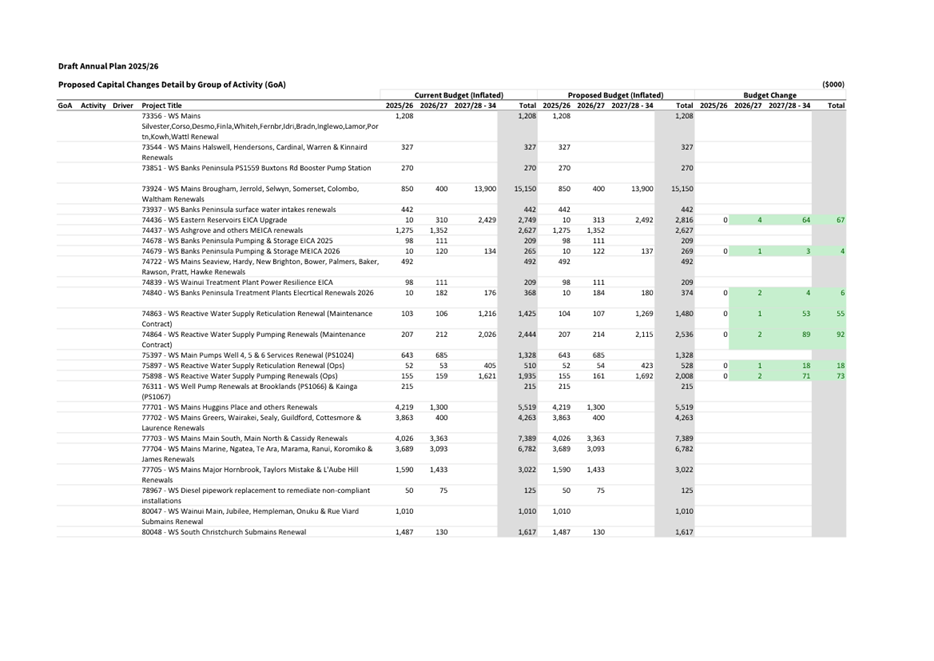

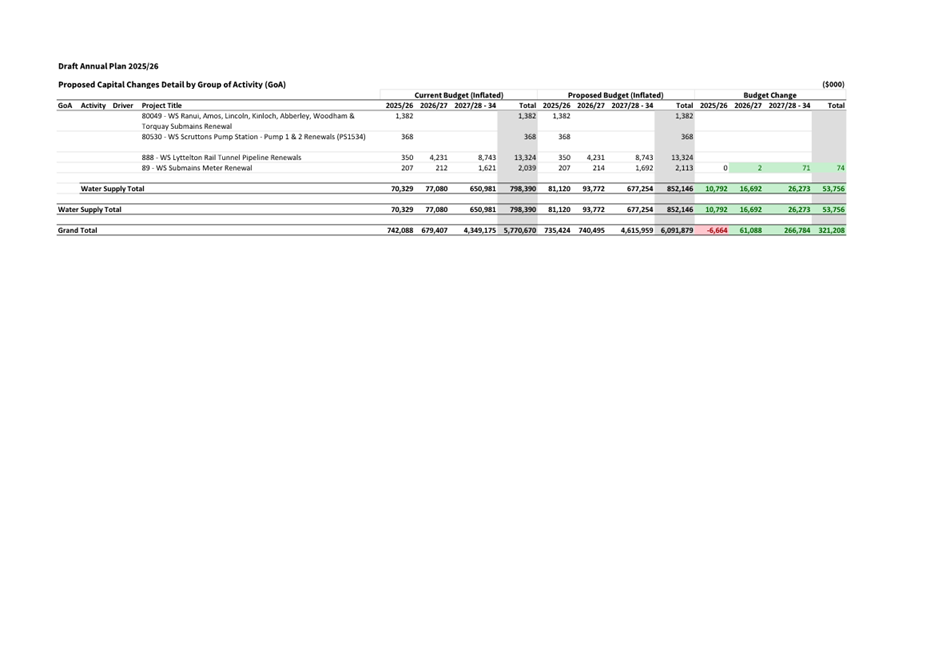

e. Proposed Capital Programme, including schedule

of changes to LTP (Attachment F).

f. Proposed minor changes to Levels of Service

(Attachment G).

g. Proposed Fees and Charges (Attachment H).

h. Prospective Financial Statements (Attachment

I).

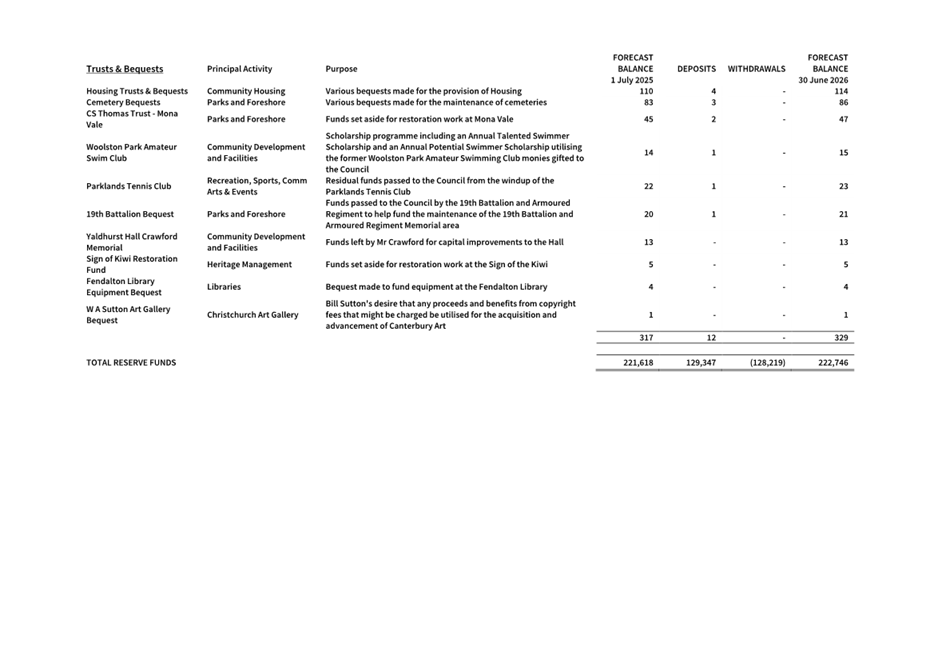

i. Reserves and Trust Funds (Attachment J).

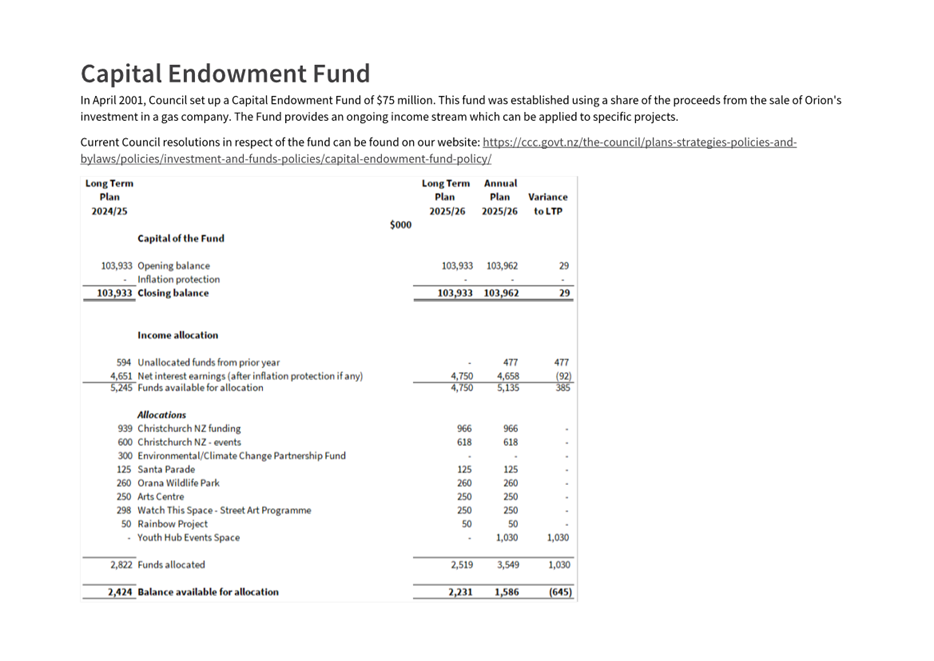

j. Capital Endowment Fund (Attachment K).

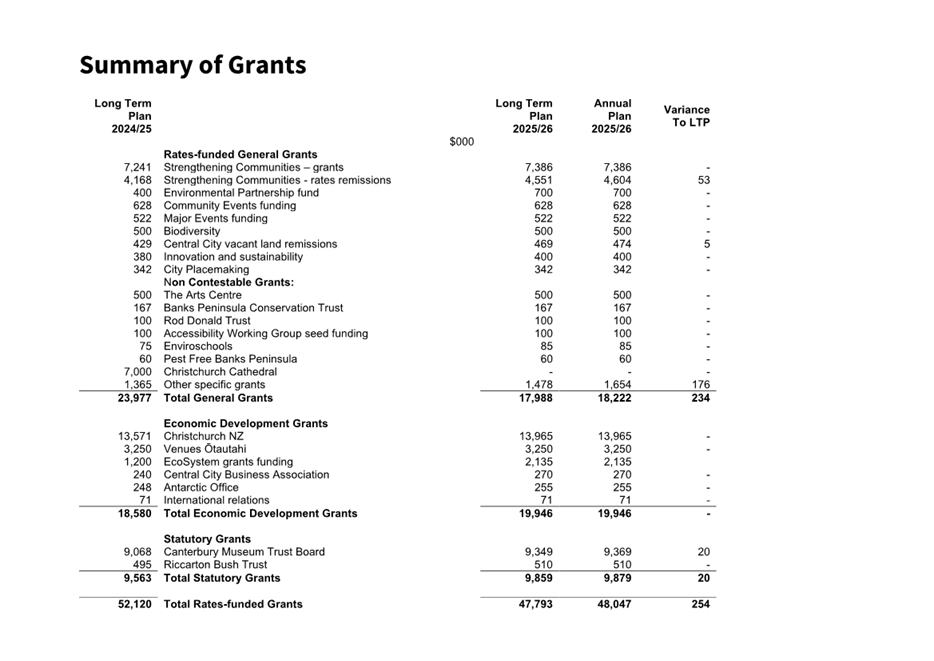

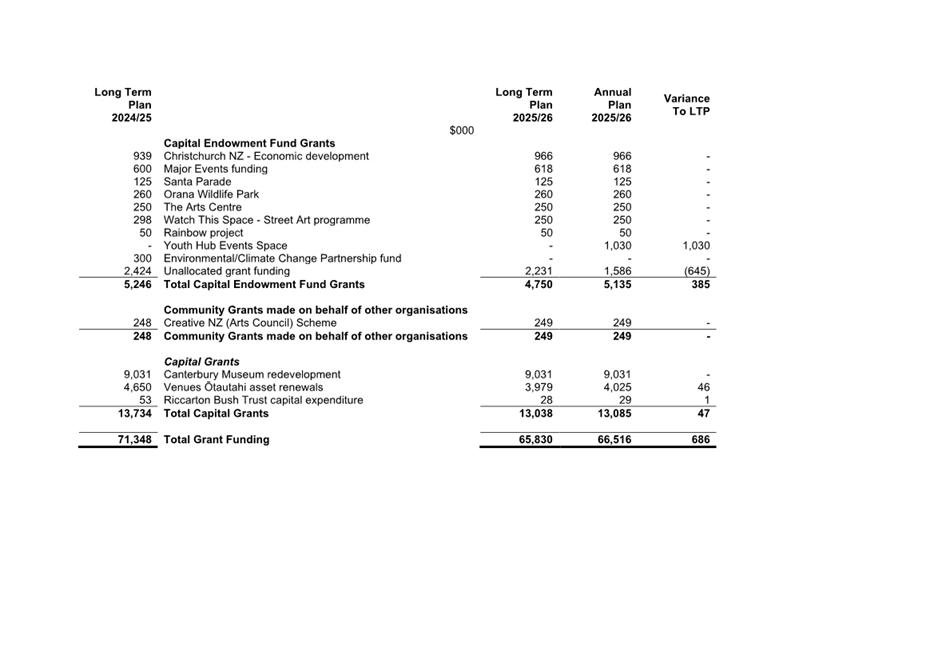

k. Summary of Grants (Attachment L).

l. List of properties for seeking the community

views and preferences as to their future use (Attachment M).

5. Approves and adopts for public consultation

the Consultation Document for the Draft 2025/26 Annual Plan (Attachment N of

this report to be provided under separate cover).

6. Approves the following process for the Draft

2025/26 Annual Plan consultation:

a. All relevant information and documents,

including the Consultation Document, be made available on the Council’s

website from 26 February 2025.

b. Hard copy information and documents to be made

available at Council libraries and service centres from 26 February 2025

onwards.

c. The period for making submissions will run

from 26 February 2025 to 11:59pm on 28 March 2025.

d. For people who indicate they wish to present

oral submissions, hearings will be held in in April 2025 (exact dates will be

confirmed and communicated to those submitters closer to the time).

7. Authorises the General Manager Finance, Risk

and Performance/CFO to make any non-material changes to the Draft 2025/26

Annual Plan documents and/or information attached to or referred to in the

staff report.

8. Notes that the Council will meet on 26 June

2025 to adopt the final Annual Plan 2025/26.

3. Executive Summary Te Whakarāpopoto Matua

3.1 Annual

Plan workshops were held from August through to December 2024. These workshops,

(many publicly live-streamed), sought guidance from the Council by presenting

issues and options around proposed changes to major infrastructure activities,

(Three Waters, Parks, Transport, as well as other activities), and the

financial position and financial changes / impacts since the Long-Term Plan

2024-34 (LTP) was approved in June 2024.

3.2 Information

and staff advice on a variety of proposals carried forward from the LTP process

were presented at the workshops. Guidance was received and has been

incorporated into the preparation of the Draft Annual Plan.

3.3 At

its meeting on 10 December 2024, the Council confirmed the framework, direction

and specific content of the Draft 2025/26 Annual Plan. This included:

3.3.1 An

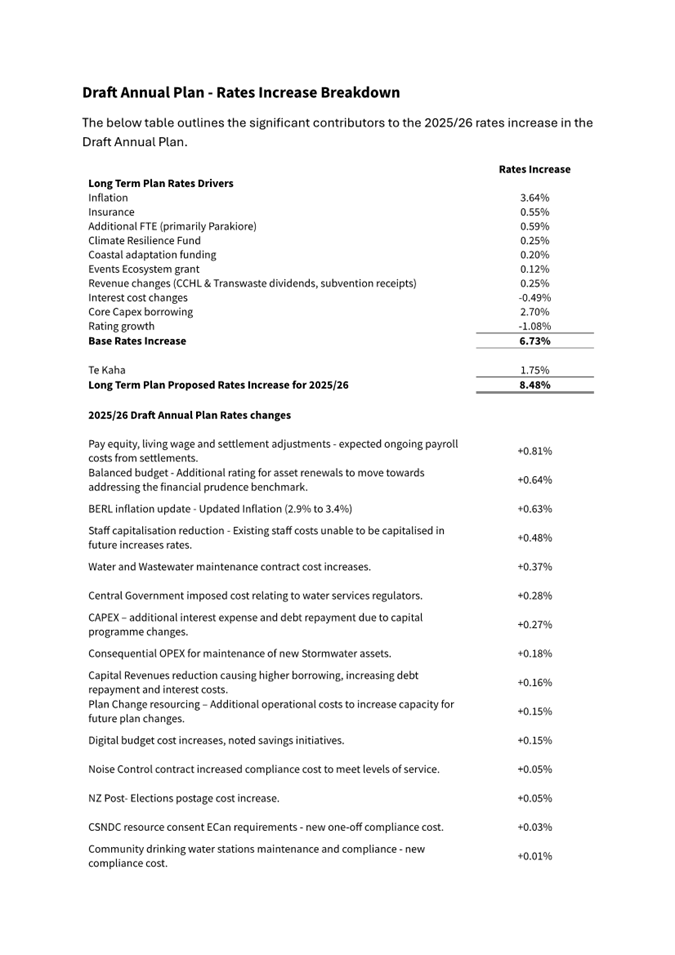

overall rates increase of 8.93%

3.3.2 Using

$6 million of subvention receipts to reduce the rates increases

3.3.3 Using

$6 million of forecast current year (2024/25) operating surplus to reduce the

rates increases and reduce debt

3.3.4 Adding

$1.1 million to enable district plan changes

3.3.5 Inclusion

of additional rating of $5/10/15 million (plus inflation) over three years to

help meet the balanced budget benchmark by 2027/28

3.4 Further

and full details of the outcomes of the 10 December meeting follow in this

report.

3.5 Since

that date, staff have collated Council feedback in creating the Draft Annual

Plan documents presented in this report.

4. Background/Context Te Horopaki

4.1 In

accordance with the Local Government Act 2002 (LGA), the Council adopted its

LTP 2024-34 in June 2024. The LTP sets out service delivery and associated

levels of service, capital programmes and budgets over that ten-year period.

The LTP was based on several key Council directions including:

· That levels of service

would not be reduced.

· That the core capital

programme (excluding One New Zealand Stadium at Te Kaha) would increase from

$483 million in 2023/24 to $668 million 2026/27.

· That the One New Zealand

Stadium at Te Kaha would be completed and hosting events by the beginning of

the 2026/27 financial year.

· Staff would be recruited

for the new Parakiore Recreation and Sports Centre.

· Asset renewals would be

sustainable.

· That a variety of climate

resilience and environmental initiatives / grants would be funded.

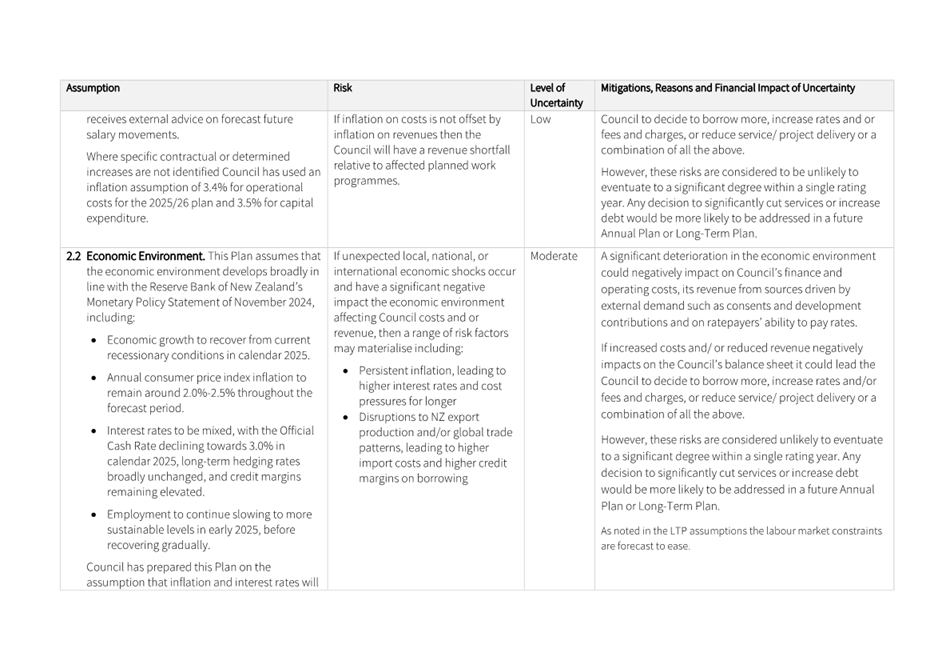

4.2 The LTP also factored in inflation (at 3.64%) based on BERL

forecasts (BERL being the Cost Price Index (CPI) for local authorities).

4.3 The

purpose of an Annual Plan is to provide a one-year schedule of updates to the

LTP, if any are required by changing circumstances. Further points to

note in respect of an Annual Plan are:

4.3.1 Annual

Plans are not designed as a mechanism to revisit the entire LTP. That requires

an amendment to the LTP, which also requires (among other matters) that the

amended LTP be audited.

4.3.2 Where

that list of updates is not material (as is sometimes the case in the first

year after an LTP is adopted) a local authority may opt to not consult on its

Annual Plan.

4.3.3 Annual

Plans, being limited in scope relative to an LTP, are not required to be

audited.

4.4 Development

of the Draft Annual Plan 2025/26 included addressing the following matters:

4.4.1 Fluctuations and

revisions of the BERL inflation forecasts.

4.4.2 The settlement of the

Christchurch Wastewater Treatment Plant (CWTP) fire insurance.

4.4.3 Decrease in insurance

premium costs.

4.4.4 Increases in general

operating costs.

4.4.5 Increases in staffing

costs.

4.4.6 Changes in various

other financial charges since the adoption of the LTP.

4.4.7 Proposed

Taumata Arowai and Commerce Commission levies to be introduced to enable

regulatory oversight of water services.

4.5 On

27 August 2024, the first Council workshop on the Annual Plan process was held.

A range of options were presented that included amending the LTP (which is a

significant undertaking including an audit), an annual plan that incorporated

only minor changes to the LTP necessary to keep it current along with some

limited additional initiatives, or an Annual Plan that had only minor changes

necessary to keep it current and not requiring consultation. The

following guidance/direction was given:

4.5.1 That levels of

service would be maintained.

4.5.2 There

would be no amended LTP process (which at its full extent can involve amending

the Financial and Infrastructure Strategies from the LTP, as well as levels of

service, projects and budgets for the remaining nine-year period).

4.5.3 That the Annual Plan

reflect the minor changes to the Long-term Plan as agreed on 27 June 2024.

4.5.4 That

consultation on those changes would be carried out.

4.6 It was also noted at the workshop on 27 August 2024 that no budget

has been set aside for a second (additional) LTP audit process to take place,

particularly given the LTP 2024-34 had been adopted only some months earlier. A

full audit typically costs approximately $300,000 (plus GST).

4.7 Nine

subsequent Council workshops, both public and public-excluded, were held on the

following dates: 24 September, 1 October, 15 October, 22 October, 29 October, 5

November, 12 November, 19 November, and 26 November 2024. These workshops are

not formal meetings of Council, and no decisions

were made.

4.8 At

these workshops, staff received guidance from Council on topics covering:

4.8.1 Incorporation of LTP

carryover actions in the Annual Plan.

4.8.2 Changes to the

Capital Programme – primarily for Parks, Three Waters, and Transport.

4.8.3 The likely rates

increase for 2025/26.

4.8.4 Options to reduce

rate increases.

4.8.5 Updates on financial

position.

4.8.6 Properties proposed

for disposal, for seeking the community views and preferences

as to their future use.

4.9 Additionally,

the following topics came up at several times during the Workshops, but

following direction from Council, have been excluded from consideration for the

Annual Plan:

4.9.1 Reducing

Levels of Service (LoS) - During the development of the LTP, the city-wide, What

Matters Most, survey identified a clear preference from the community for

Council services to be maintained. This is consistent with the strong community

views received when level of service cuts have been proposed and consulted upon

in previous LTPs, noting:

· This became clear

guidance from a majority of councillors during an LTP workshop and was

subsequently reflected and formally adopted in the LTP.

· Altering

significantly levels of service for a significant activity triggers amendments

to the LTP (there is a range up to fully amending the whole LTP), and Council

provided clear guidance on process at its workshop of 27 August 2024 that

explicitly ruled out using the Annual Plan as a mechanism for significant

amendment of the LTP or triggering an audit process.

· Non-front line

levels of service (around finance, procurement and related internal functions)

have been heavily rationalised in several previous LTPs and Annual Plans.

· That material

savings to offset the proposed rates increase are most likely to come from

changes to significant Levels of Service for significant activities, which

triggers an LTP amendment, and, conversely, changes to non-significant Levels

of Service are unlikely to yield material savings.

· That, as a result,

materially reducing Levels of Service has not been looked at as a viable

cost-saving measure in the context of developing an Annual Plan that does not

trigger a costly amendment of the LTP 2024-34.

4.9.2 Delaying renewal and

replacement programmes (‘sweating the assets’) – a resolution

at the 10 December 2024 meeting was for advice on putting a hold on all

non-essential maintenance/renewals in council facilities (i.e. painting,

carpet, kitchen and bathroom fit outs etc). Staff understand that when

necessary repairs and maintenance are undertaken, it is an opportunity for

minor cosmetic replacements to be undertaken at a marginal and minor cost and

this is looked at on a case-by-case basis.

4.10 Taking

all the above information into consideration, at its meeting on 10 December

2024, the Council made decisions about what to include in the framework of the

Draft Annual Plan, including:

4.10.1 A rates

increase of 8.93%, comprising 8.48% as per year 2 of the 2024-34 Long-Term

Plan, a further 0.28% being Central Government imposed costs for water services

regulators, 0.15% for increased capacity to support amendments to the District

Plan and several minor changes.

4.10.2 The use of $6

million of subvention receipts to reduce the rates increases; and

4.10.3 The use of $6

million of the forecast current year (2024/25) operating surplus to reduce the

rates increases ($3.35 million) and reduce debt ($2.65 million).

4.10.4 Acknowledgement

of a breach of the balanced budget financial prudence benchmark for 2025/26

(and 2026/27, as indicated in the LTP).

4.10.5 Inclusion of

additional rating of $5/10/15 million (plus inflation) over the next three

years to enable the balanced budget benchmark to be met by 2027/28. While the

LTP showed the 2026/27 benchmark as not met, latest modelling shows that

without this increase the next four years are at risk. The additional rates

will be applied to funding asset renewals in lieu of borrowing to reduce

interest and debt repayment costs. It should be noted that the balanced budget

benchmark is one of a number of regulatory measures that indicates financial

prudence.

4.10.6 Other material

variations to the LTP can be found in section 5 of the Report.

4.11 It was also

decided that the following topics would be explored further/consulted upon as

part of the consultation process:

4.11.1 Cathedral Targeted Rate - given the Cathedral’s reinstatement project being paused,

the draft Annual Plan proposes pausing the collection of the remaining three

years of the Cathedral targeted rate (a fixed charge of $6.52 per annum per

separately used or inhabited property). The existing ringfenced funds will be

held and continue to earn interest in the interim. As previously advised,

the community should be consulted about the proposed change to the Cathedral

targeted rate.

4.11.2 Postponing the

completion of the Wheels to Wings cycleway in favour of implementing selected

portions of the project.

5. Financial Implications Ngā Hīraunga Rauemi

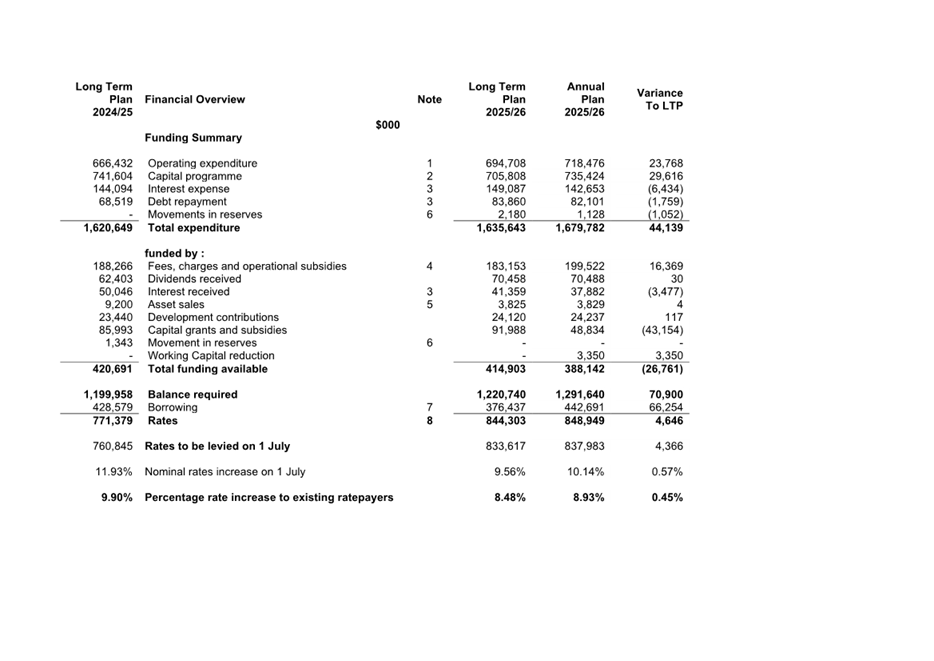

Rates

5.1 The

Draft Annual Plan includes a rates requirement (excl GST) to be levied of $838

million.

5.2 The

proposed average rates increase to all existing ratepayers of 8.93% is slightly

higher than the 8.48% forecast in the 2024-34 Long Term Plan. Details of the

makeup of the rates increase is shown in Attachment O.

5.3 The

increases for the average property based on capital value in the three sectors

is:

· Residential 8.64%

· Business

9.88%

· Remote Rural 10.63%

5.4 The

average house will have a proposed rates increase of $6.59 per week. Full

details of rates, including the total rating requirement for general and

targeted rates, and indicative rates for sample properties, are provided in the

Funding Impact Statement (Attachment C).

5.5 Ratepayers

will be able to see a forecast of the 2025/26 rates for their specific property

by visiting Council's website using the "rates search" tab from 26

February 2025 (the date for opening of consultation).

5.6 The

proposed Uniform Annual General Charge is $197 (incl GST). It has increased

from $177 based on the average increase in general rates. The proportion of

total rates revenue to be collected from fixed charges (rather than based on

capital value) will decrease from 8.40% to 8.05%. Full details of rates

information are shown in Attachment D.

Expenditure

5.7 Operational

expenditure of $718.5 million is $23.8 million above the level forecast in the

LTP principally due to:

5.7.1 An

increase in staff salaries and wages costs of $8.0 million, due to pay equity,

living wage and contract settlement adjustments resulting in increased payroll

costs. It should be noted that (excluding pay equity and the positions

requested by Council) the majority of the increases have been offset by

additional revenues or budget reductions.

5.7.2 Additional

inflation over that provided for in the LTP ($6.5 million).

5.7.3 Additional

water services maintenance costs identified, primarily as a result of contract

rates increases greater than inflation provided for, and additional capital

projects being completed, which will result in consequential operational costs

to maintain ($4.1 million).

5.7.4 Higher

Burwood Landfill operating costs ($4.8 million) due to an extension of the

consent, allowing operations to continue longer than planned in the LTP (offset

by increased revenues).

5.7.5 Reduction

in staff cost capitalisation of $3.7 million following a review of costs that

can be capitalised, primarily relating to software development.

5.7.6 Proposed

Taumata Arowai ($1.6 million) and Commerce Commission ($0.5 million) levies to

be introduced to enable regulatory oversight of water services.

5.7.7 Additional

digital contract and software cost increases over and above inflation ($1.1

million).

5.7.8 Additional

$1.1 million of resourcing, internal staff and external commissioners, to

enable district plan changes.

5.7.9 Additional

service allowance costs ($0.4 million) due to a change in terms for the staff

salary & wages collective agreement and an increased number of staff on the

collective agreement.

5.7.10 Additional

postage costs of $0.4 million for the 2025/26 local government elections due to

price increases over and above inflation.

5.7.11 Additional

noise control contract costs of $0.4 million for additional resources due to

levels of service not being met with existing resourcing.

5.8 These

proposed increases are partially offset by a reduction in insurance premiums of

$9.2 million, following representations to insurance brokers.

5.9 Gross

interest costs are $6.4 million lower than projected in the LTP due to lower

interest rates and debt levels, noting $3.5 million of this decrease relates to

on-lending to subsidiaries which is recovered as interest revenue.

Revenue

5.10 Total

revenue (excluding rates) of $381.0 million is $30.1 million lower than that

projected in the LTP. The revenue changes from the LTP are:

5.10.1 Reduced

interest revenues, due to lower interest rates ($3.5 million).

5.10.2 Reduced Waka

Kotahi capital subsidies ($11.2 million) due to an overstatement in the LTP.

5.10.3 Reduced Shovel

Ready and MCR capital funding ($32.0 million) due to an overstatement the LTP.

5.11 The

reductions in revenue have been partially offset by:

5.11.1 Additional Solid

Waste revenue of $6.8 million.

5.11.2 An additional

planned $6.0 million of subvention receipts.

5.11.3 An additional

$1.6 million of regulatory compliance revenues, relating to resource management

consents ($0.9 million), building consents & inspections ($0.3 million) and

Food Safety & Health ($0.4 million).

5.11.4 An additional

revenue from other activities of $2.2 million.

Surplus, operating

deficits, and sustainability

5.12 The

Draft Annual Plan for 2025/26 shows an accounting surplus of $227.3 million

before revaluations, and includes vesting assets of $245.7 million which

includes Parakiore. After adjusting for capital revenues, which fund capital

expenditure and taking into account rating for renewals rather than

depreciation, the Draft Annual Plan is based on a balanced funding budget,

effectively ensuring cash operating costs are met from operating revenue.

5.13 The

operating surplus for the current financial year (2024/25) is forecast (as at

31 December 2024) to be $19.8 greater than budget. Of this $6.0 million,

primarily as a result of savings in insurance costs, has been identified as

being available to be carried forward. The Draft Annual Plan proposes applying

this portion of the forecast operating surplus in the following way:

5.13.1 $2.65 million

used to reduce current year borrowing, thereby reducing the opening debt

position and lowering future interest costs and debt repayment and therefore

rates.

5.13.2 $3.35 million

applied to reduce rates in the 2025/26 financial year.

5.13.3 Staff will

provide advice to Council, so direction can be given, on the balance of any

actual operating surplus at year end.

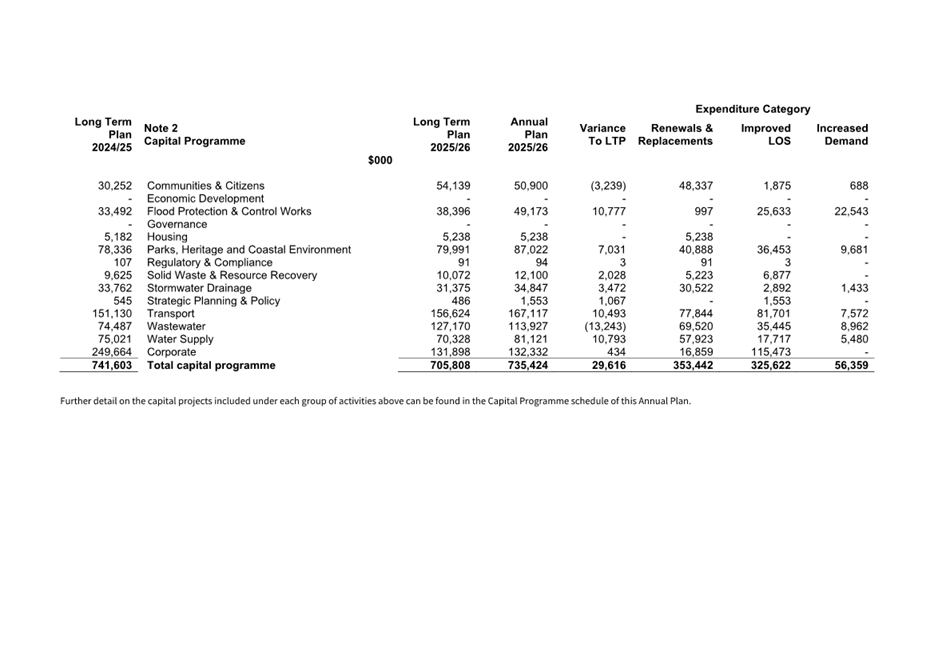

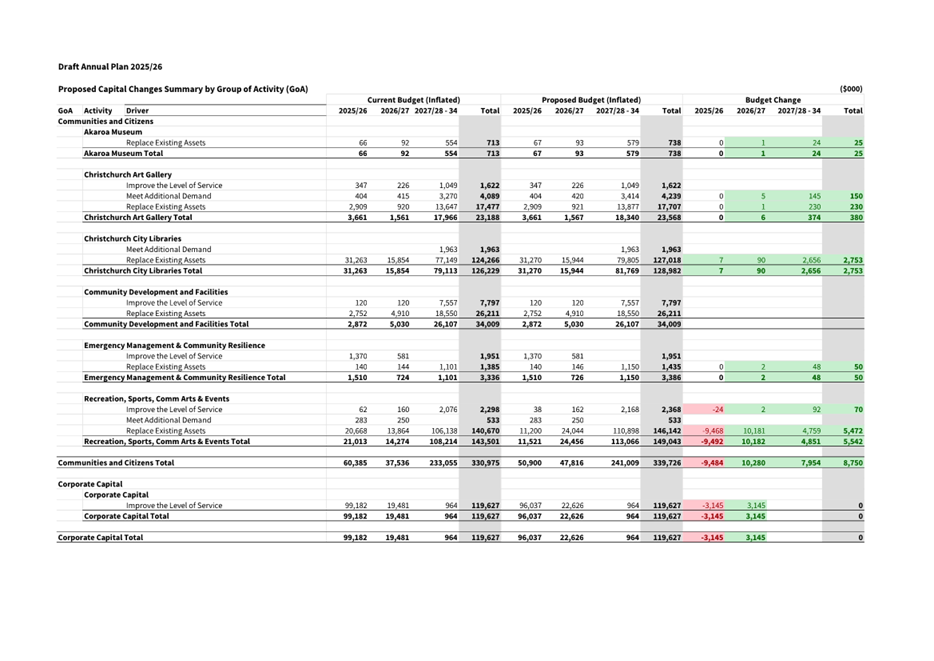

Capital programme expenditure

5.14 Council

plans to invest $735.4 million in the capital programme in 2025/26, an increase

of $29.6 million from that shown in the LTP.

5.15 The

capital programme has been reviewed with a focus on deliverability, to ensure

ratepayers are not levied in advance of funds being required. Key factors taken

into account when considering deliverability were:

· Supply chain

issues – including resources, materials and labour.

· Cost

escalation/inflationary pressure.

· Human resource

availability (internal and external).

5.16 The

additional capital programme expenditure proposed in 2025/26 compared to the

LTP mainly relates to the following:

Community Facilities

· An additional

$75,000 opex for a feasibility assessment for a skate park upgrade including a

potential vert ramp at Washington Skatepark or an alternative venue, so in the

future Ōtautahi Christchurch may be able to host national or international

skate events.

· Re-timing of

$9.5 million of Jellie Park renewals to 2026/27.

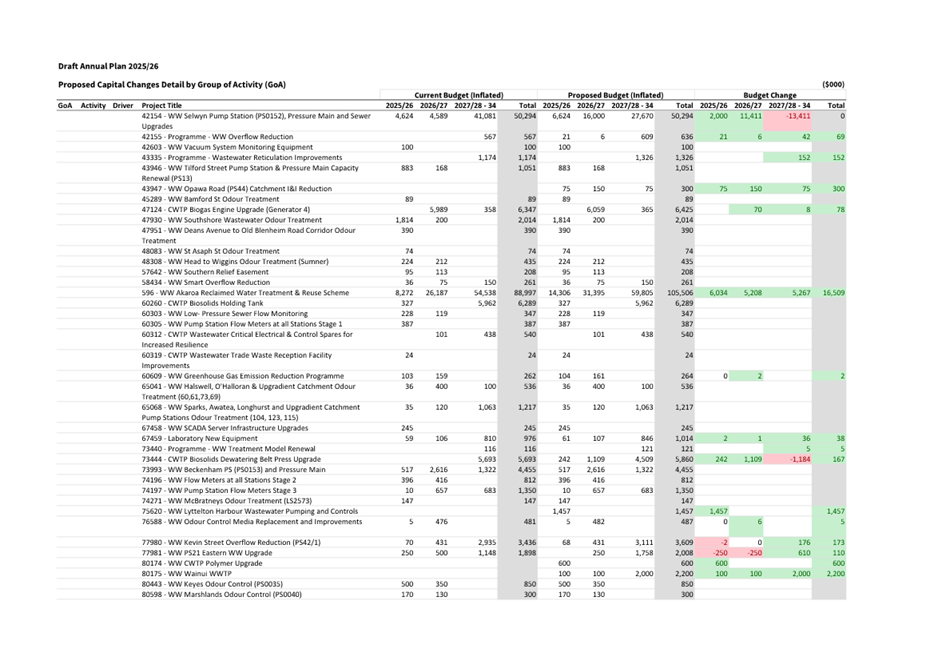

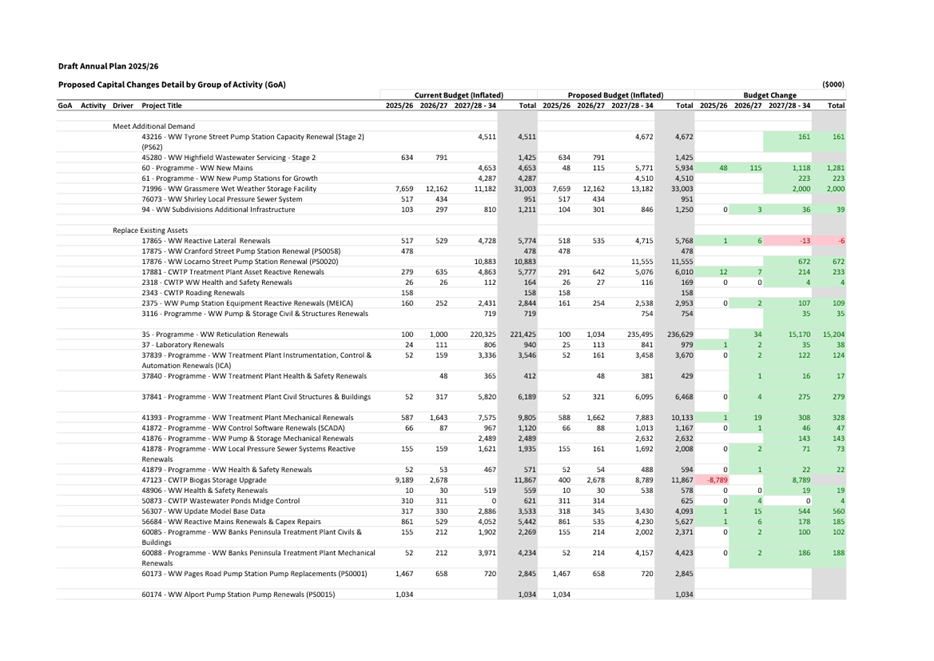

Three Waters

· Additional

$10.2 million of water supply mains renewals programme works.

· Re-timing

of $6.0 million for the Akaroa wastewater treatment plant from 2025/26.

· Reprioritisation

of the Addington Brook Filtration Devices bringing $5.0 million budget forward

from 2030/31.

· Reprioritisation

of the Highsted Styx Mill Reserve Wetland bringing $3.4m budget forward from

2028/29.

· Re-phasing

to 2026/27 of $16.2 million for the Christchurch Wastewater Treatment Plant

activated sludge plant.

· Re-phasing to 2027/29 of $8.8

million for the Christchurch Wastewater Treatment Plant biogas storage upgrade.

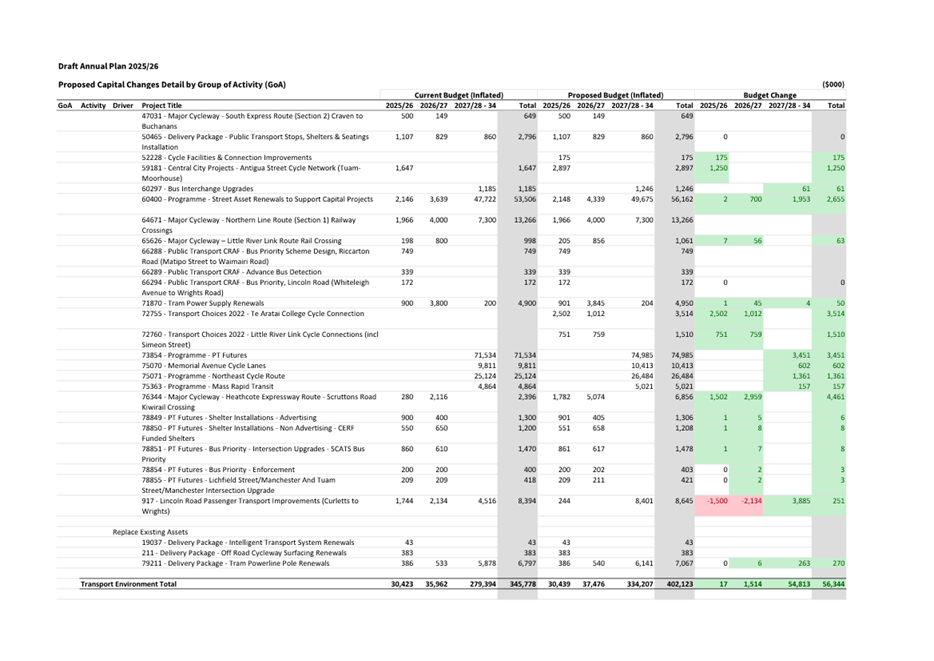

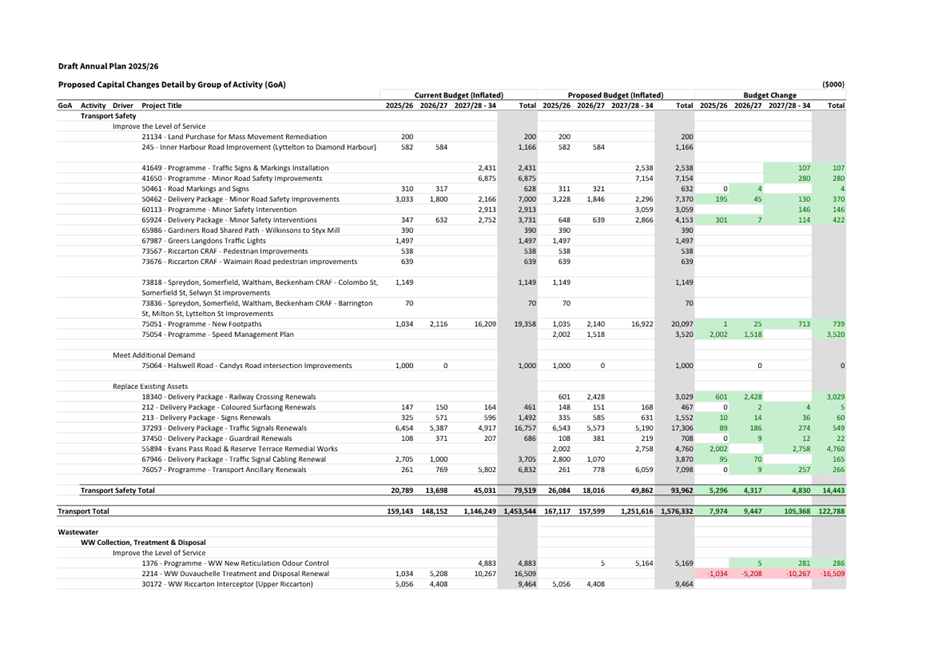

Transport

· Proposing to stage the delivery of the Papanui

ki Waiwhetū Wheels to Wings major cycle route which includes:

- linking

the Te Ara O-Rakipaoa Nor'West Arc and Puari ki Pū-harakeke-nui Northern

Line major cycle routes, and installing a signalised pedestrian crossing

on Harewood Road, between Matsons Avenue and Chapel Street ($4.2M);

- Installing

traffic lights at the Harewood Road, Gardiners Road and Breens Road

intersection, and installing a signalised pedestrian crossing on Harewood Road

at Harewood School ($5.5M); and

- Noting

that the remaining construction programme is yet to be finalised and will be

confirmed through future Annual Plans or Long-Term Plan processes.

· Proposing to defer the Lincoln Road Public Transport

project while working on a business case for NTZA funding from 2026 – 28

to 2029 - 30.

· An

additional $2.5 million has been added in to 2025/26 and $1 million into

2026/27 to enable us to complete the Te Aratai Cycle Connection

project.

· An

additional $1.5 M has been allocated across 2025/26 and 2026/27 to enable us to

complete the Simeon Street Cycle Connection Project.

Capital programme

funding

5.17 The

capital programme is funded by; subsidies and grants for capital expenditure,

development contributions, proceeds from sales of surplus land, rates and debt.

In 2025/26 Council will rate for $221 million of renewals which is consistent

with the Financial Strategy.

Borrowing

5.18 Council’s

borrowing at 1 July 2025 is forecast to be $119 million lower than forecast in

the LTP. The Draft Annual Plan proposes to include new borrowing in

2025/26 of $442.7 million, an increase of $66.3 million on the LTP, largely

reflecting lower capital revenues.

5.19 Debt

repayment at $82.1 million is $1.8 million lower than the LTP due to lower

capital programme borrowing in 2024/25. The reduction in borrowing arose

primarily from receipt of the insurance settlement for the Christchurch

Wastewater Treatment Plant.

5.20 Gross

debt as 30 June 2026 is expected to be $3.17 billion, $52 million lower than

planned in the LTP as a result of the opening position and movements noted

above.

5.21 In

accordance with Council’s financial strategy, the Draft Annual Plan

ensures prudent and sustainable financial management of Council’s

operations including that it will not borrow beyond its ability to service and

repay that borrowing.

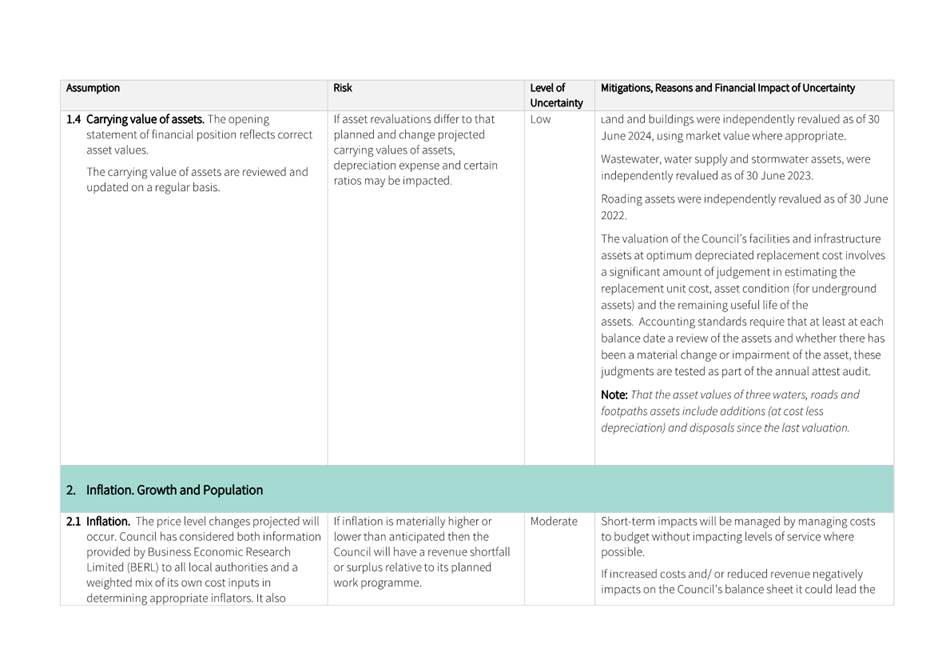

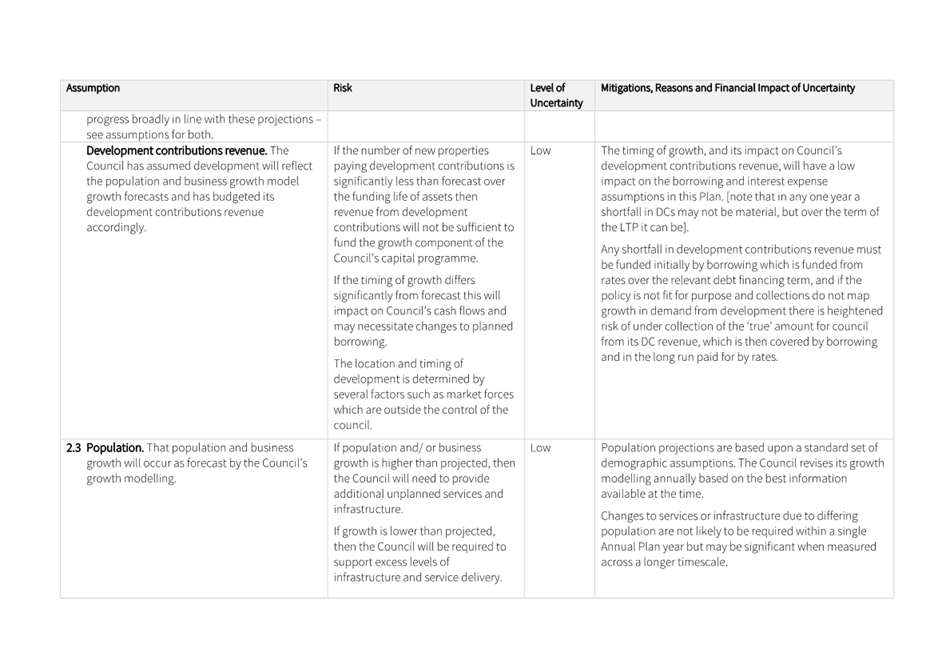

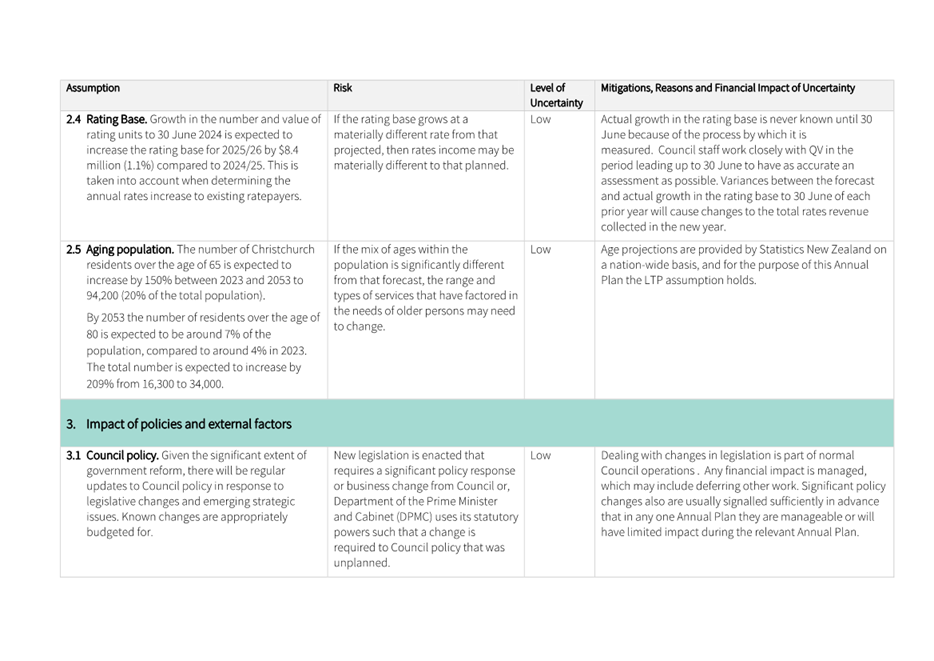

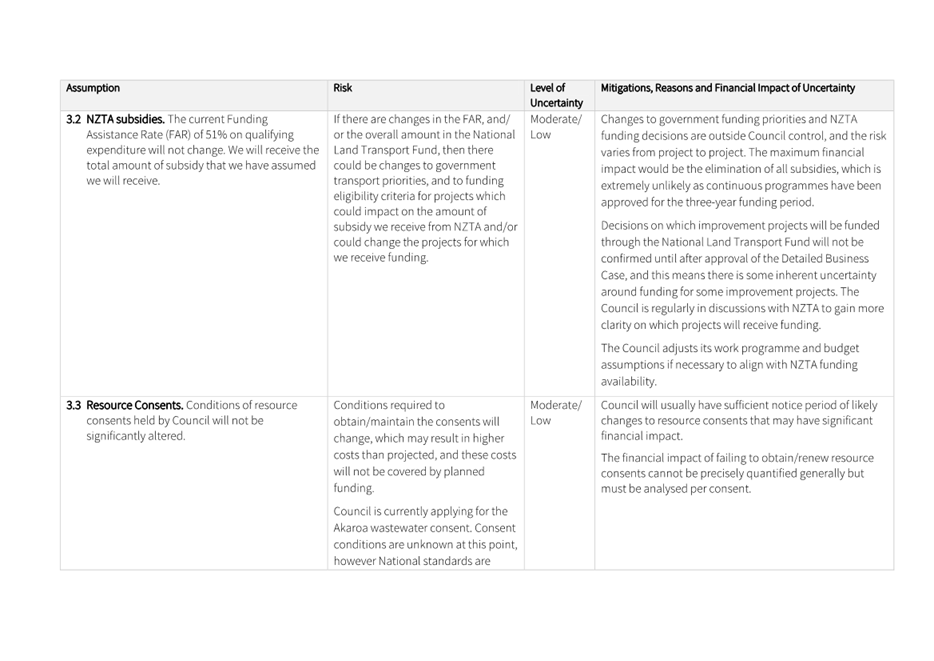

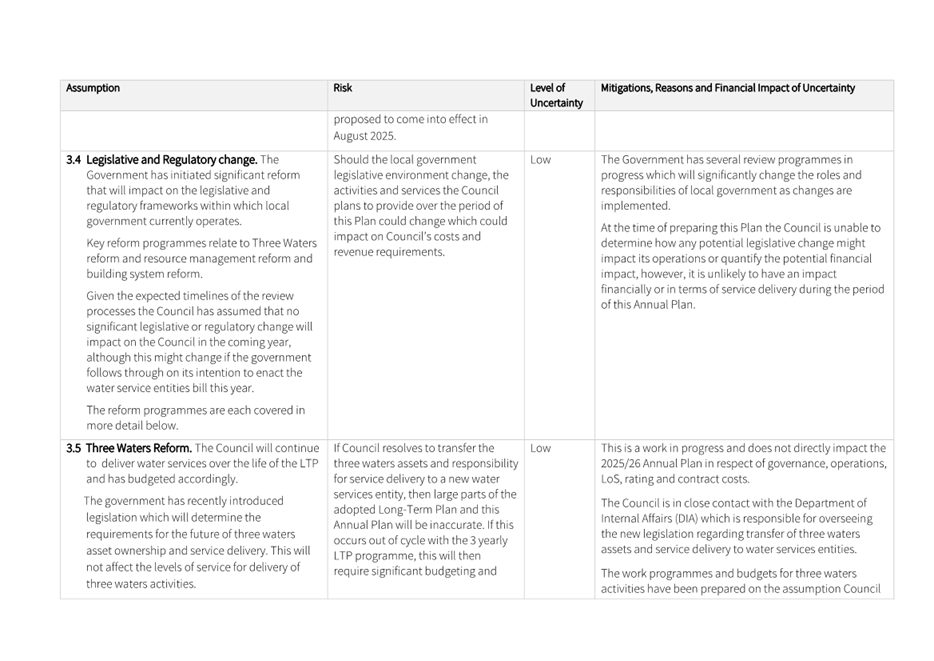

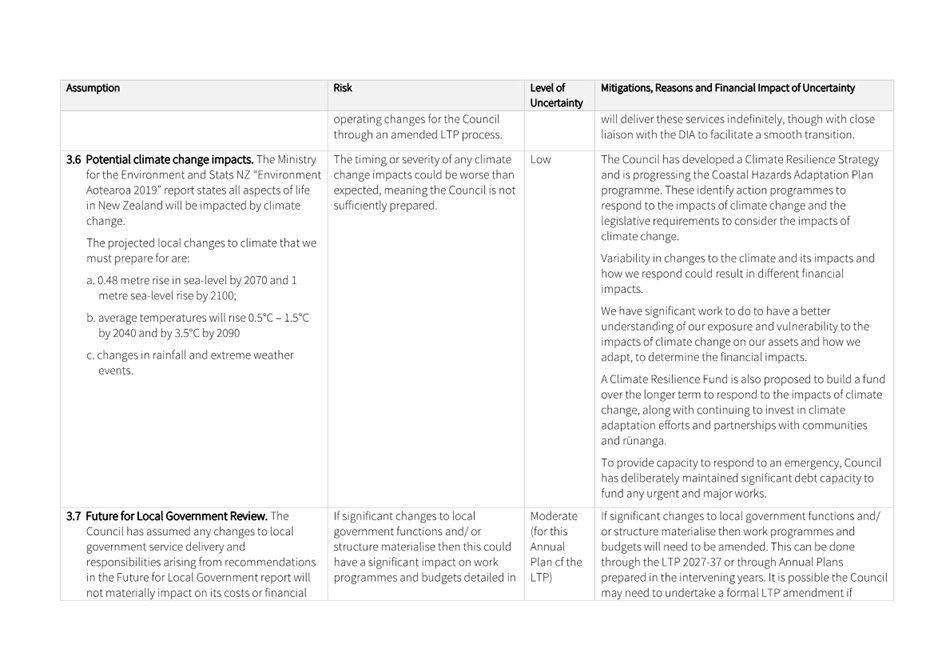

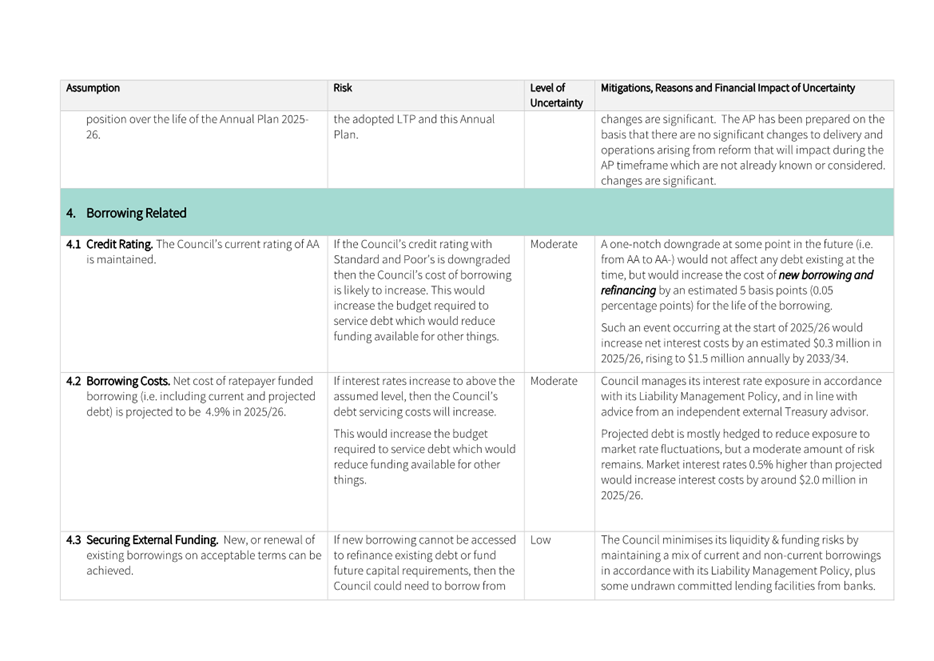

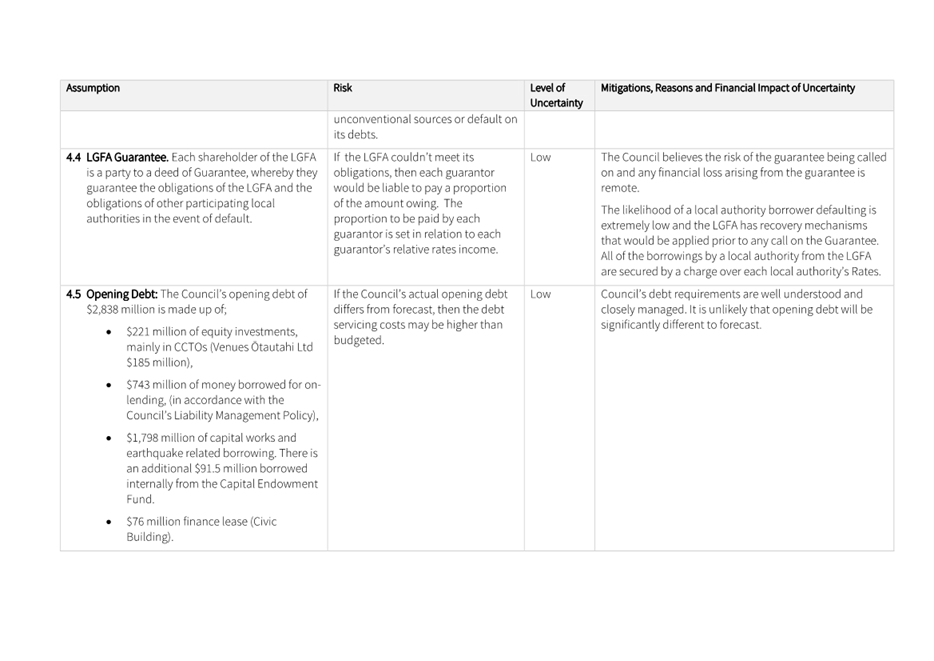

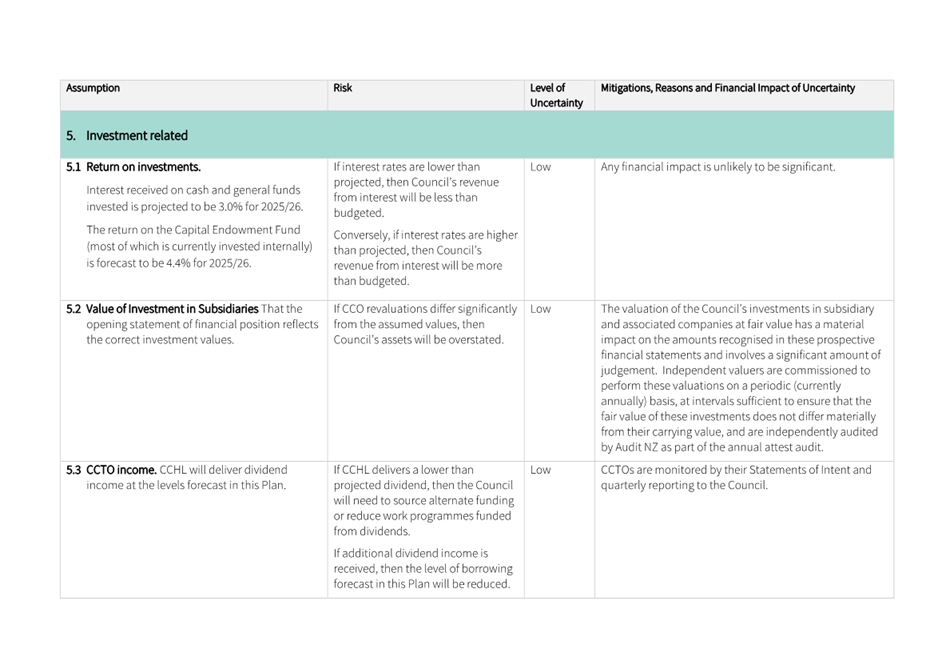

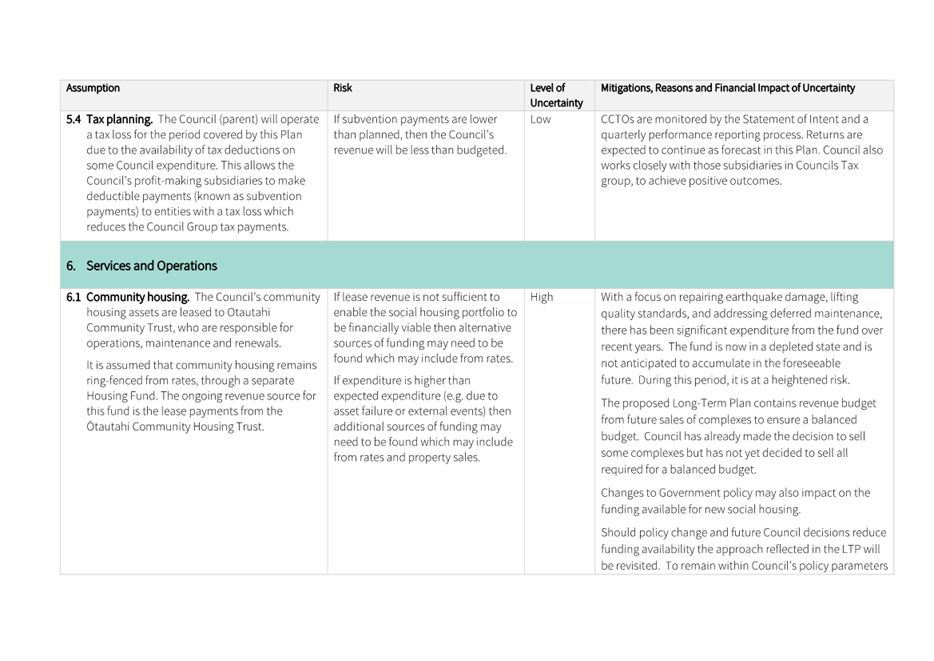

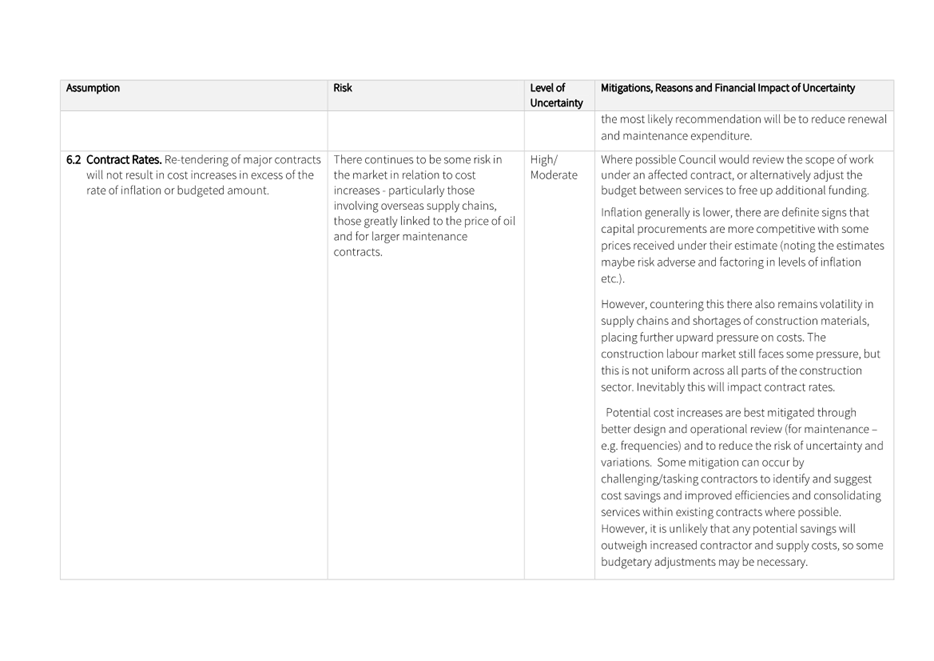

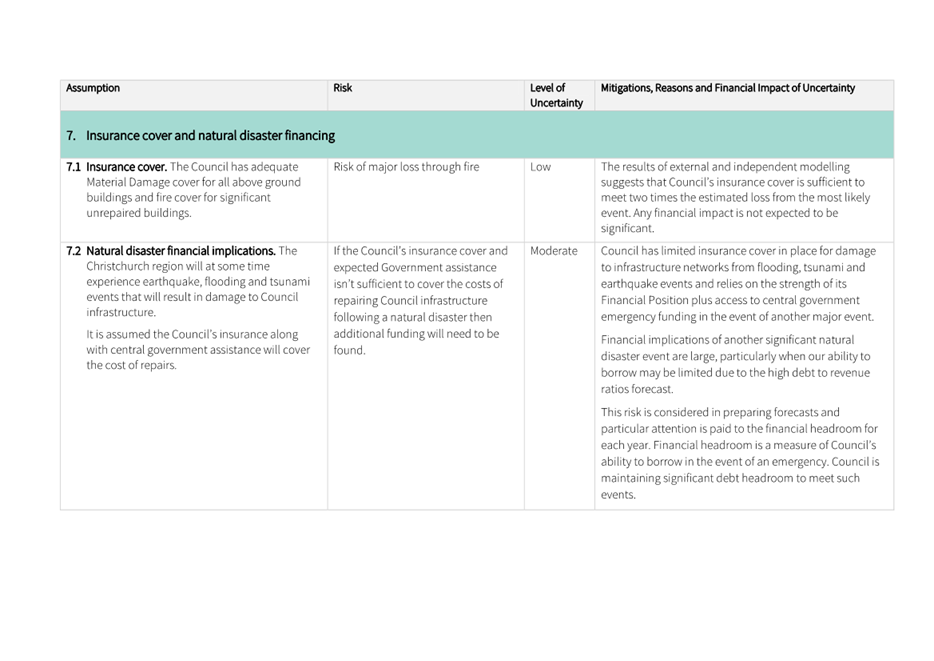

6. Significant Assumptions

6.1 Significant assumptions used to develop and inform the LTP

were reviewed to ensure they remained current and applicable. There are

no significant changes to assumptions used in developing the LTP. The level of

uncertainty on a number of assumptions is lower than the LTP due to the

one-year focus of the Annual Plan.

7. Financial Risk Management Strategy

7.1 The

Council’s financial strategy and related policies applied in this Draft

Annual Plan establish the framework for decision making to manage financial

risks, including liquidity and funding, interest rate exposure and counterparty

credit risk. They remain unchanged from the financial strategy and

policies developed and approved as part of the LTP.

7.2 An

important element in assessing the value of the Council’s risk management

strategy are its five key financial ratios (two net debt, two interest and one

liquidity). All key financial ratios are expected to be met in 2025/26. These

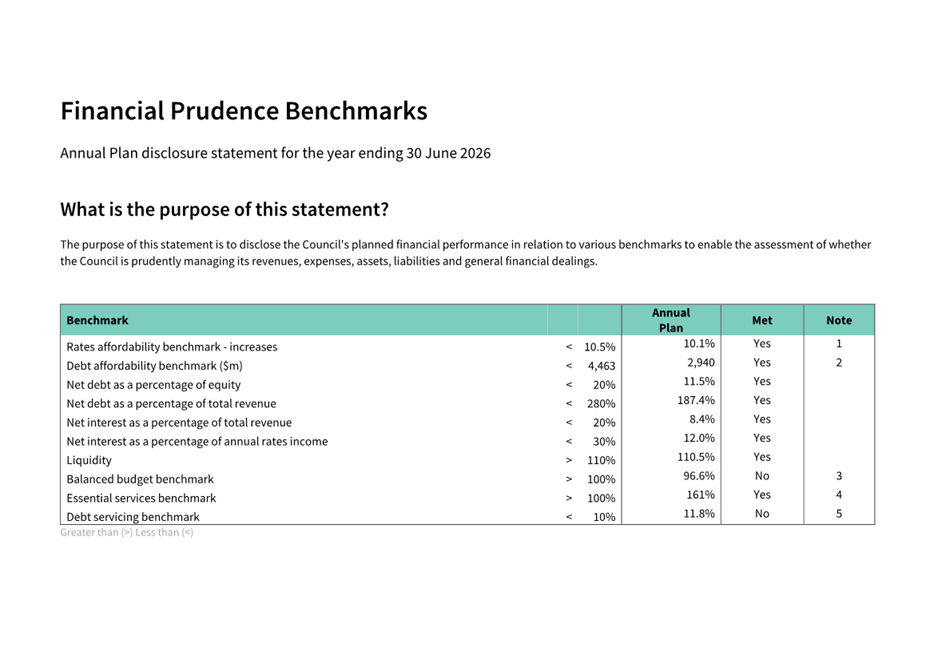

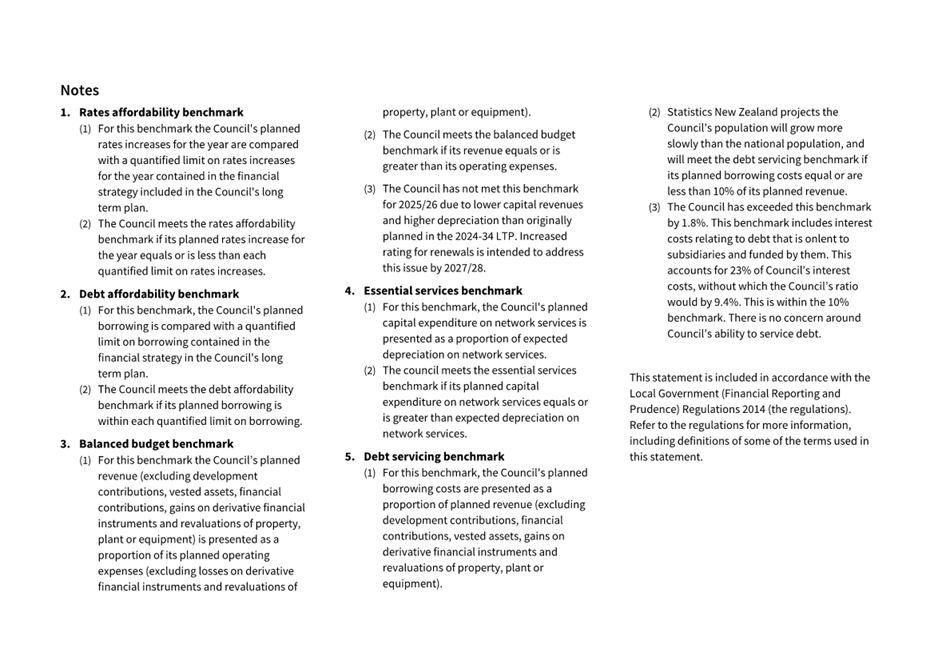

are included within the Financial Prudence Benchmarks (Attachment E).

7.3 There

are two Financial Prudence benchmarks not expected to be met in 2025/26; the

Balanced Budget benchmark and the Debt Servicing benchmark.

7.4 The

Balanced Budget benchmark measures if revenue is equal to or greater than

operating expenses. It is forecast to now not be met in 2025/26 due to

significantly lower capital revenues than were planned in the LTP. The

underlying reason for the benchmark not being met is that rates do not fully

fund asset renewals until 2032, noting that the Council’s financial

strategy forecasts that rates will not fully fund renewals until near the end

of the LTP period.

7.5 The

Debt Servicing benchmark (borrowing costs as a percentage of revenue being less

than 10%) is forecast to not be met for 2025/26. It is forecast to be 11.8%. This benchmark includes interest costs relating to debt that is

on-lent to subsidiaries and funded by them. This accounts for 23% of

Council’s interest costs. If an adjustment is made that reverses

out the effect of the back-to-back loans with subsidiaries (primarily

Christchurch City Holdings Ltd), Council’s ratio would by 9.4%. This is

within the 10% benchmark. There is no concern around

the ability of any of the subsidiaries to service the debt.

7.6 Staff

note that Council remains comfortably within the parameters of its financial

strategy and the Draft Annual Plan does not depart in any significant way from

what was forecast for Year 2 of the LTP.

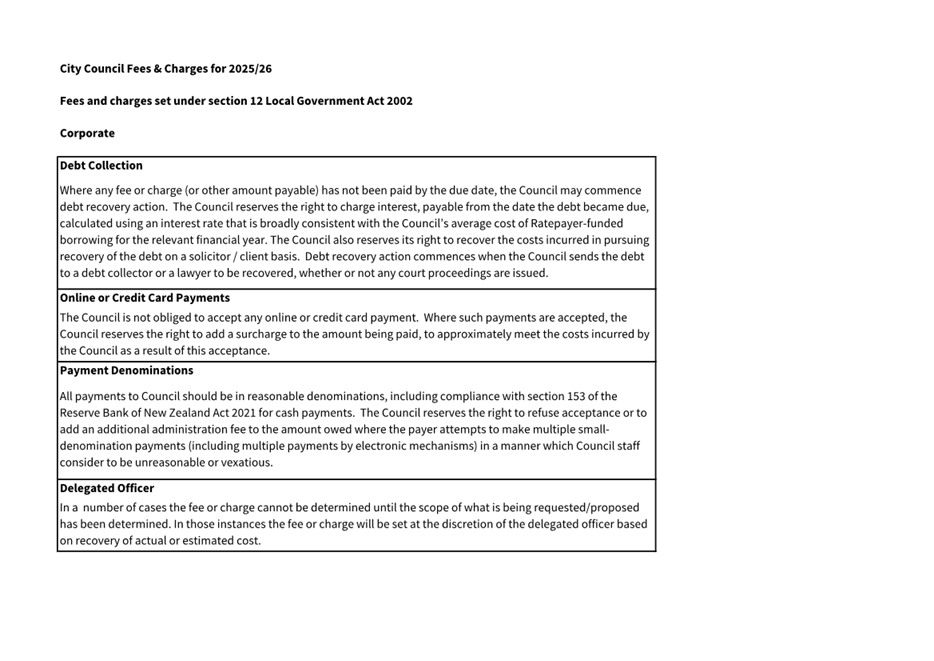

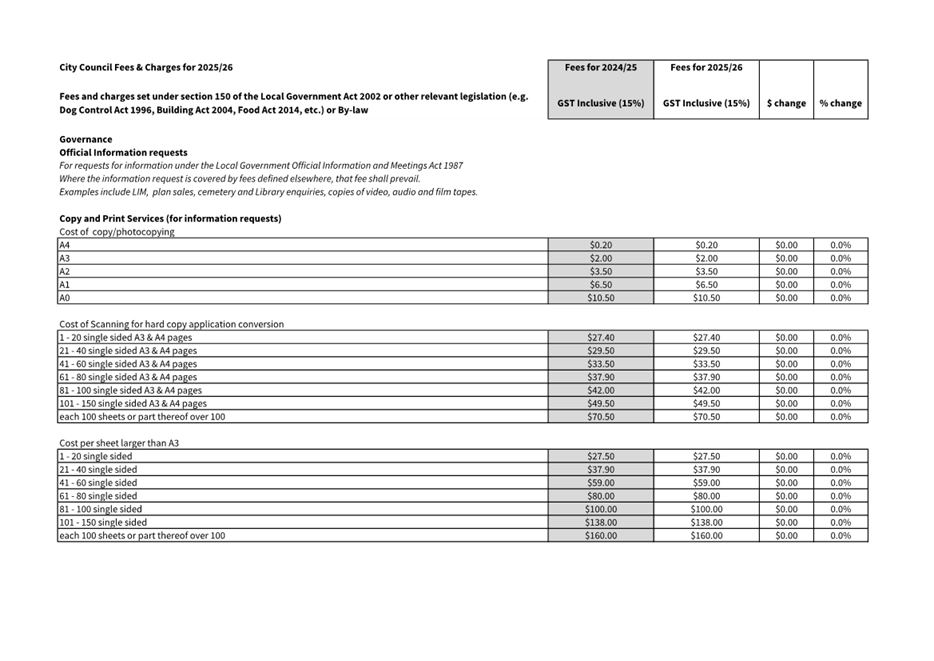

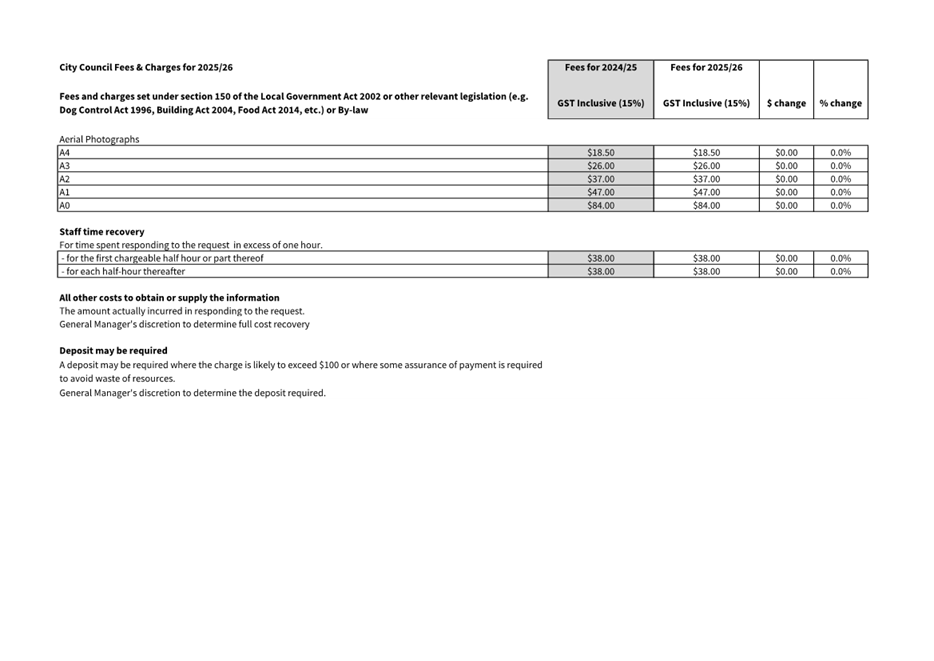

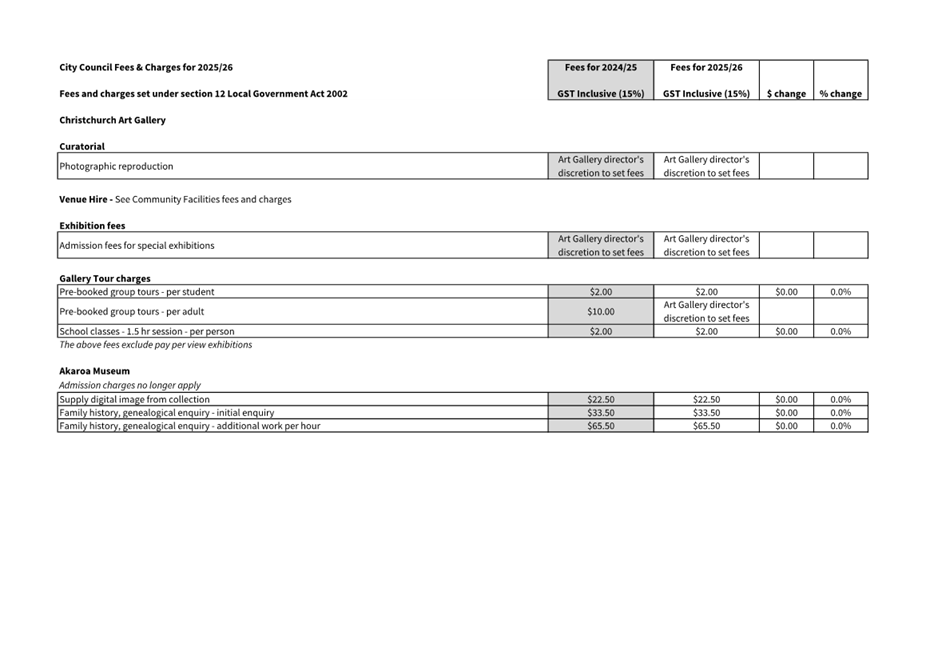

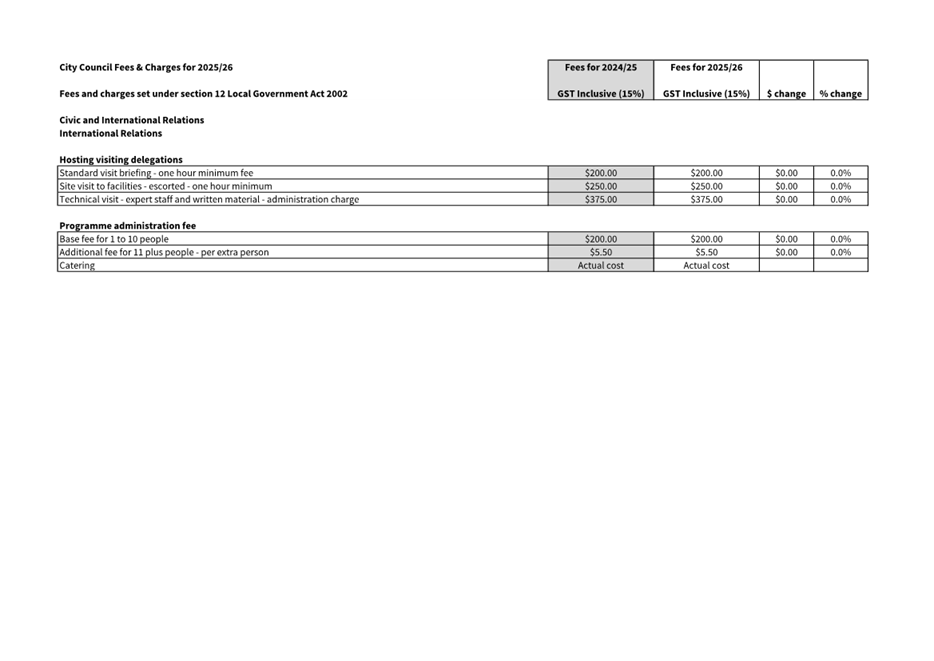

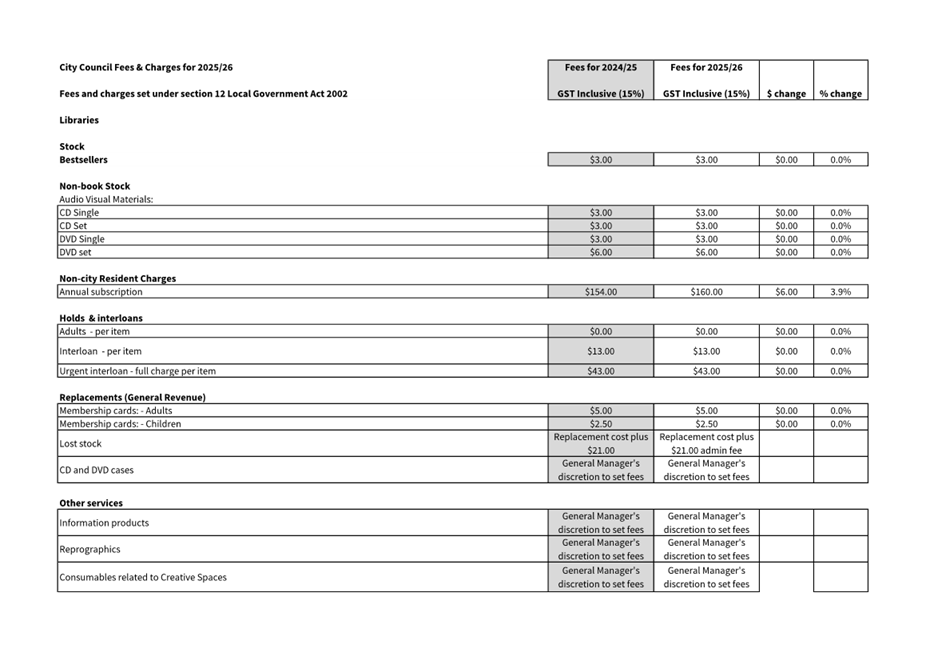

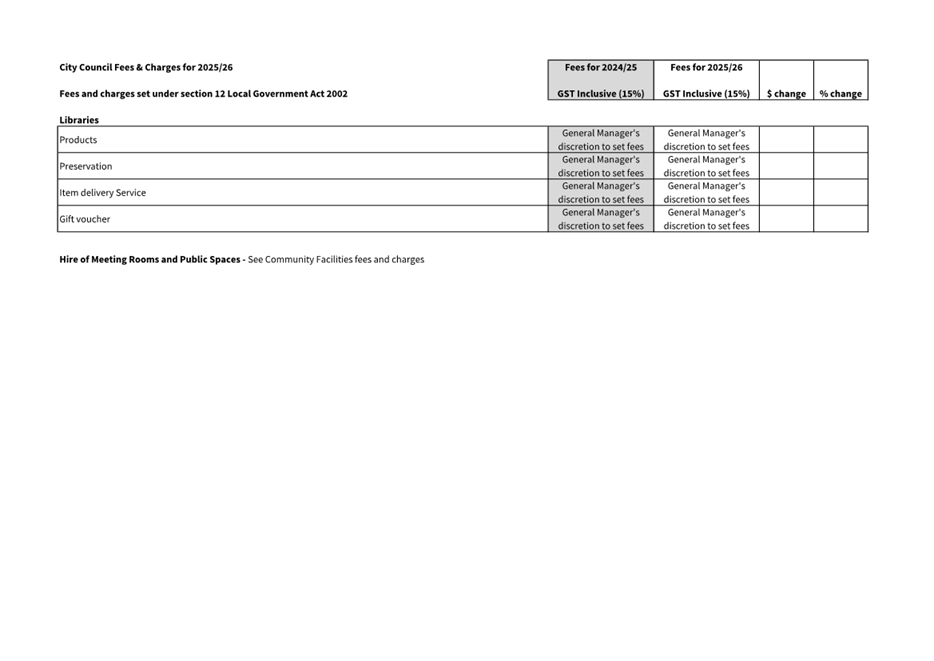

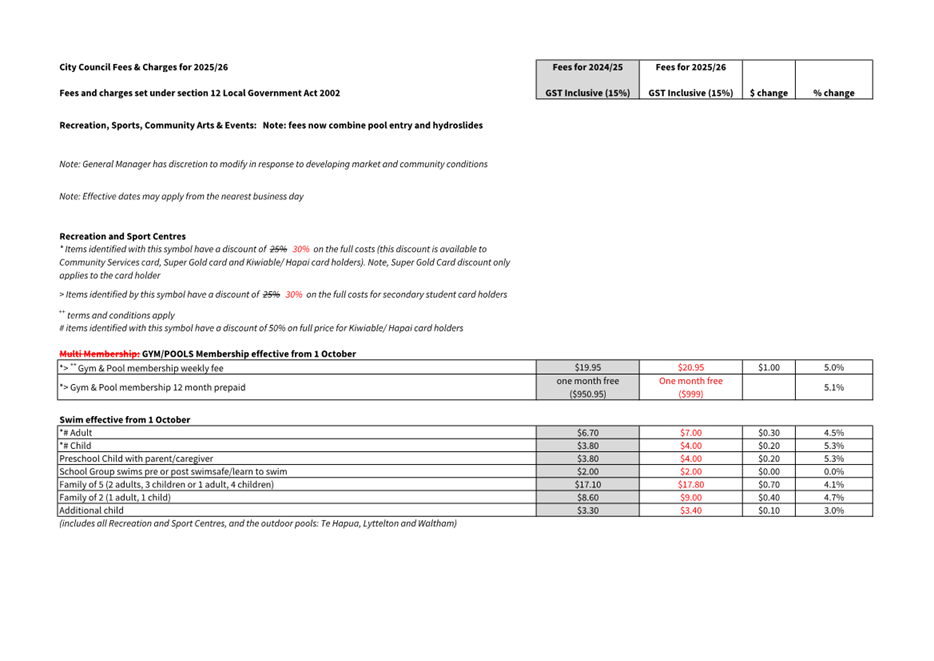

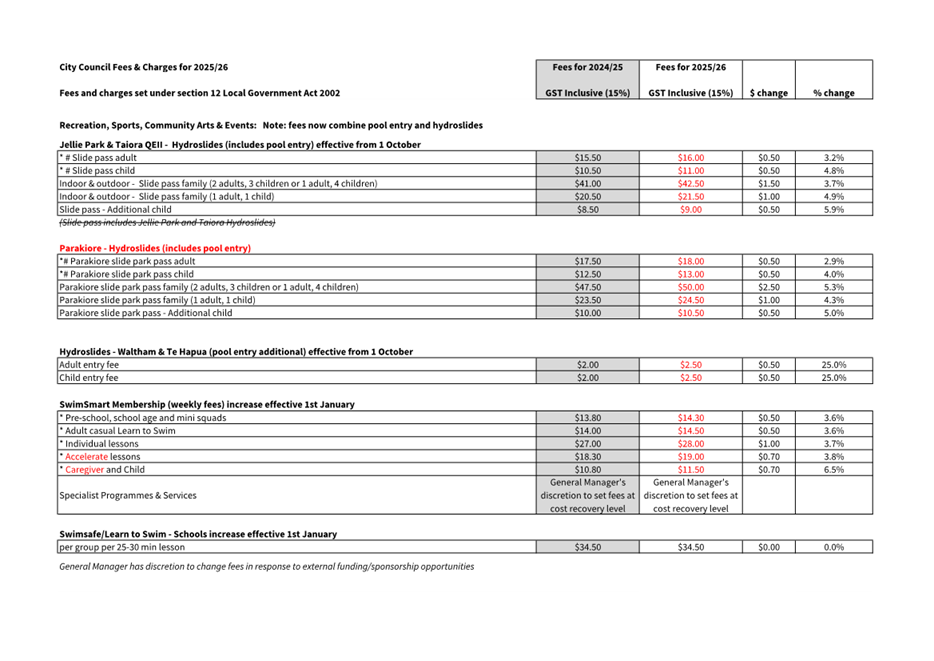

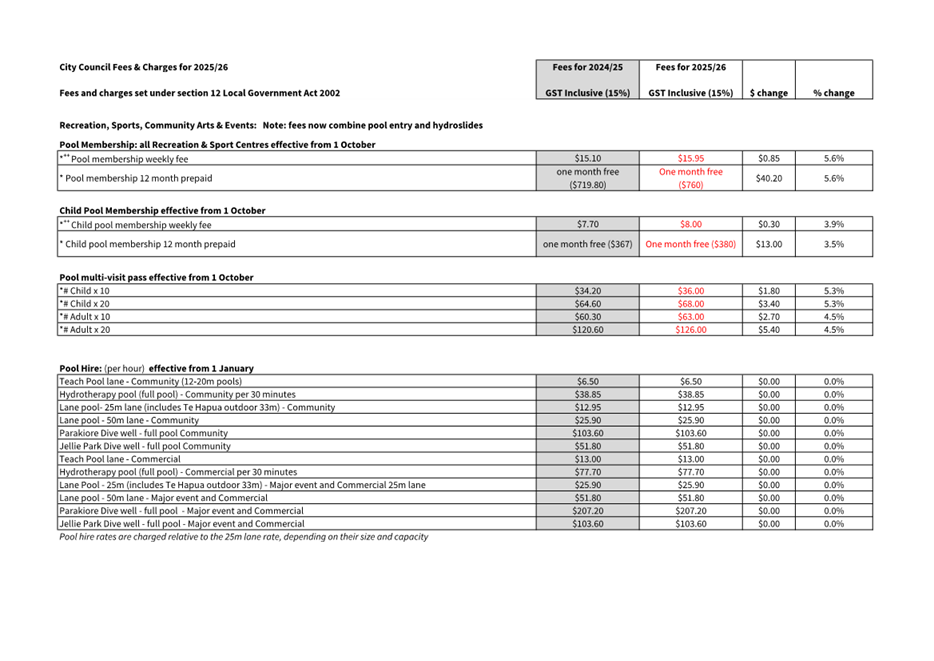

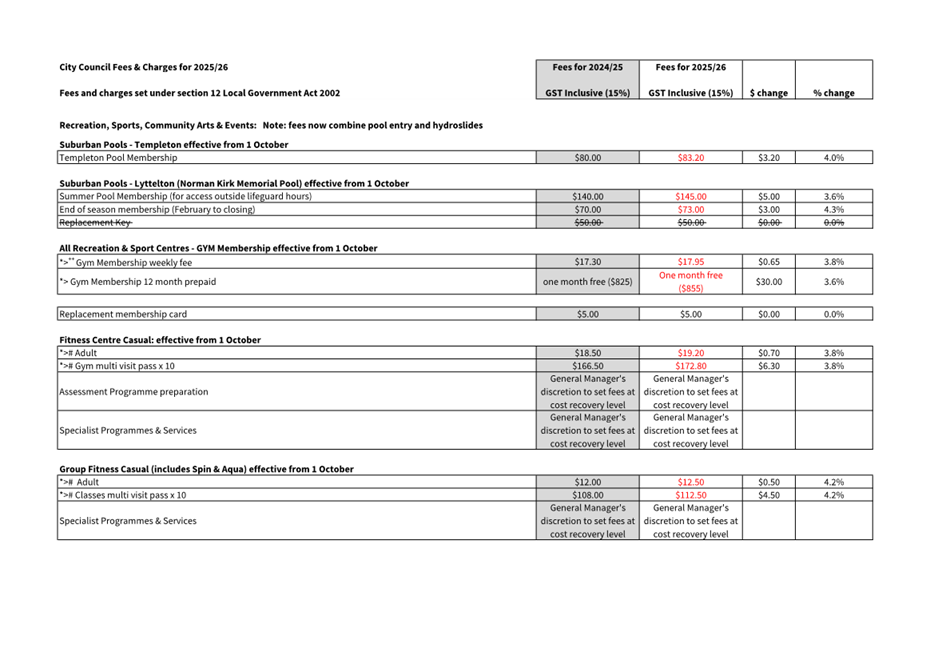

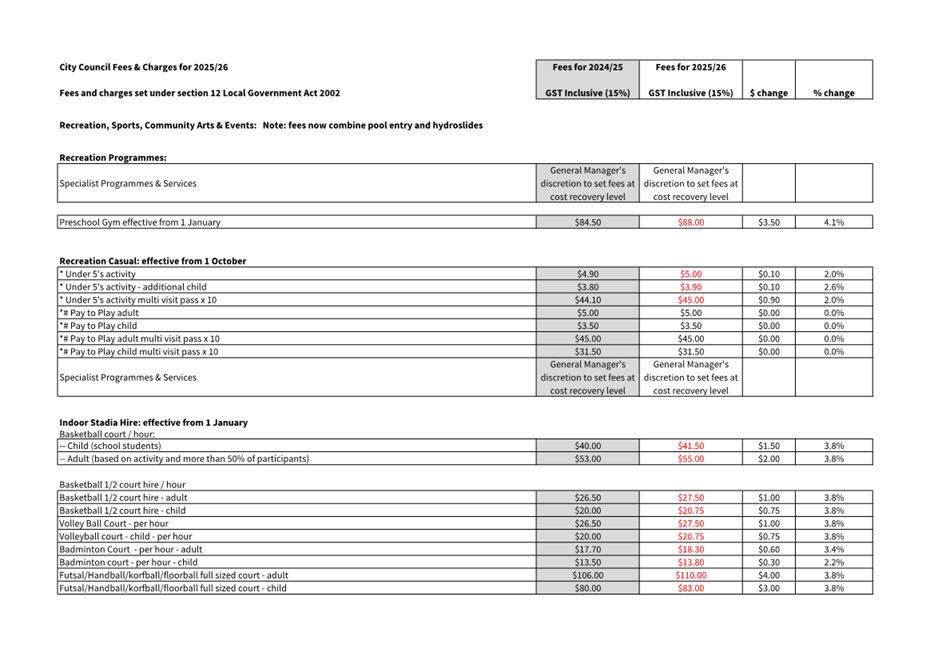

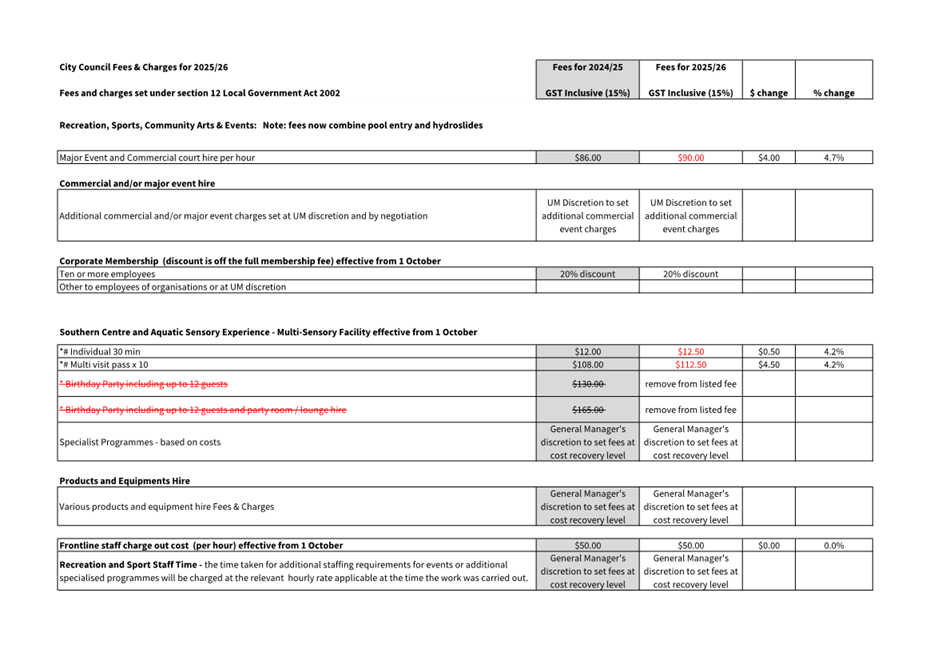

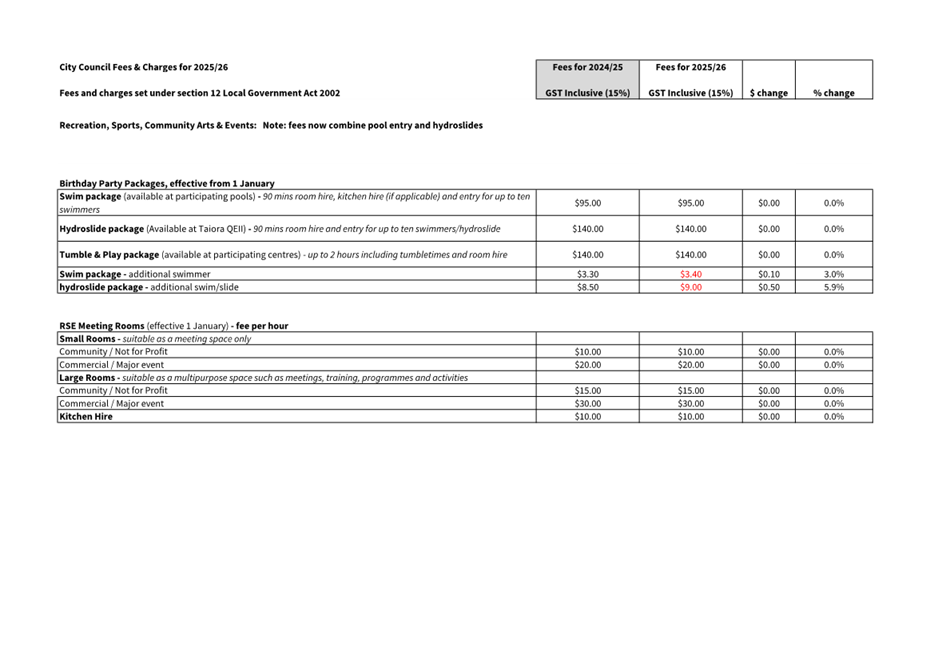

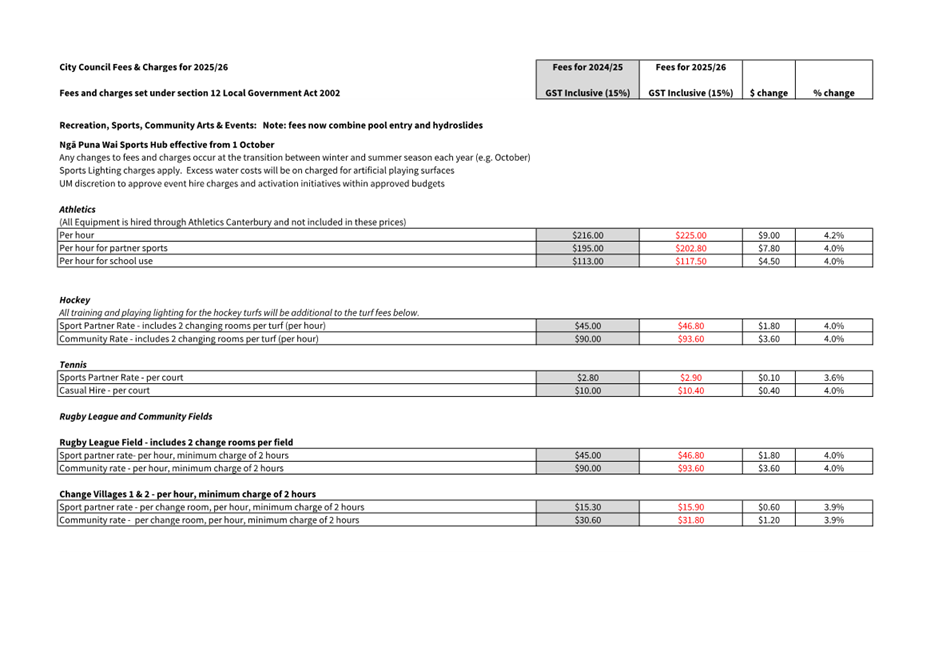

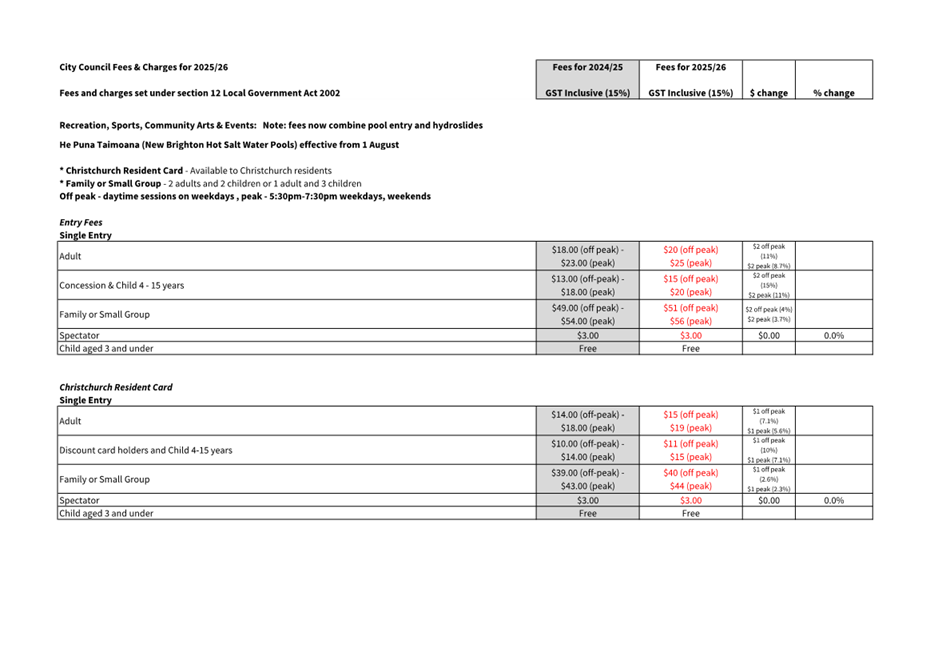

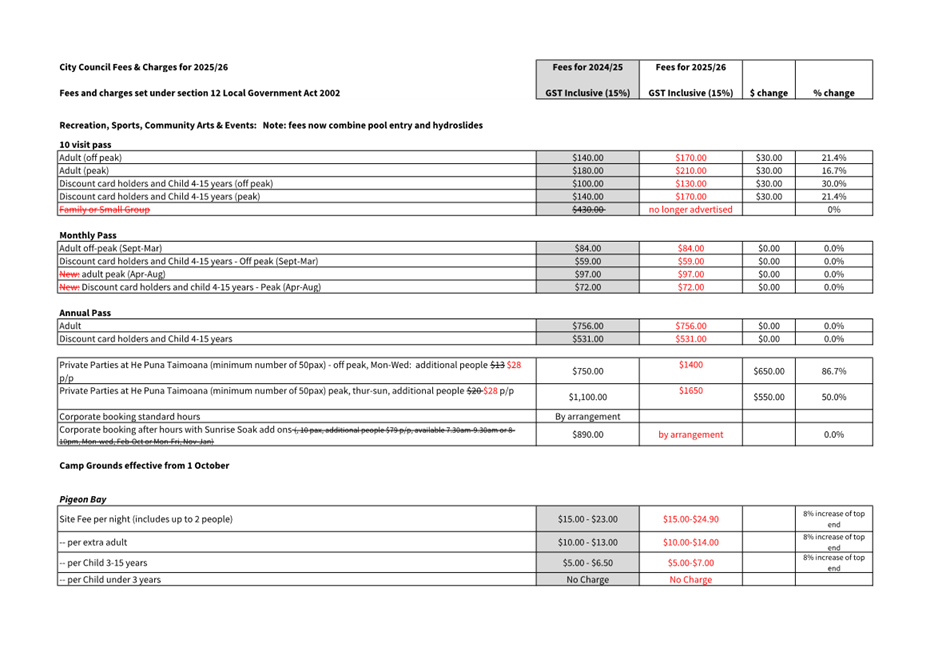

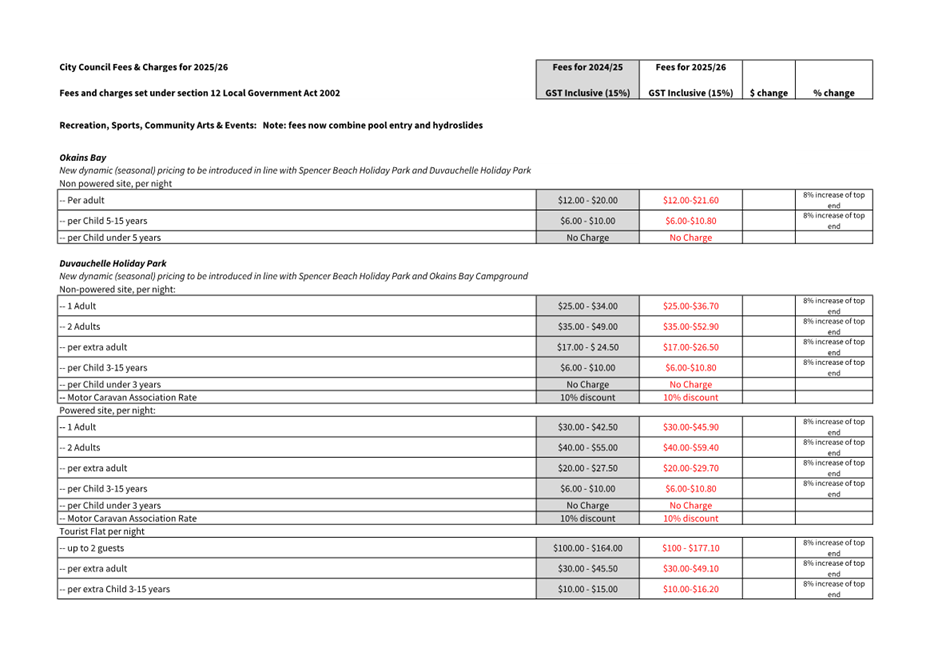

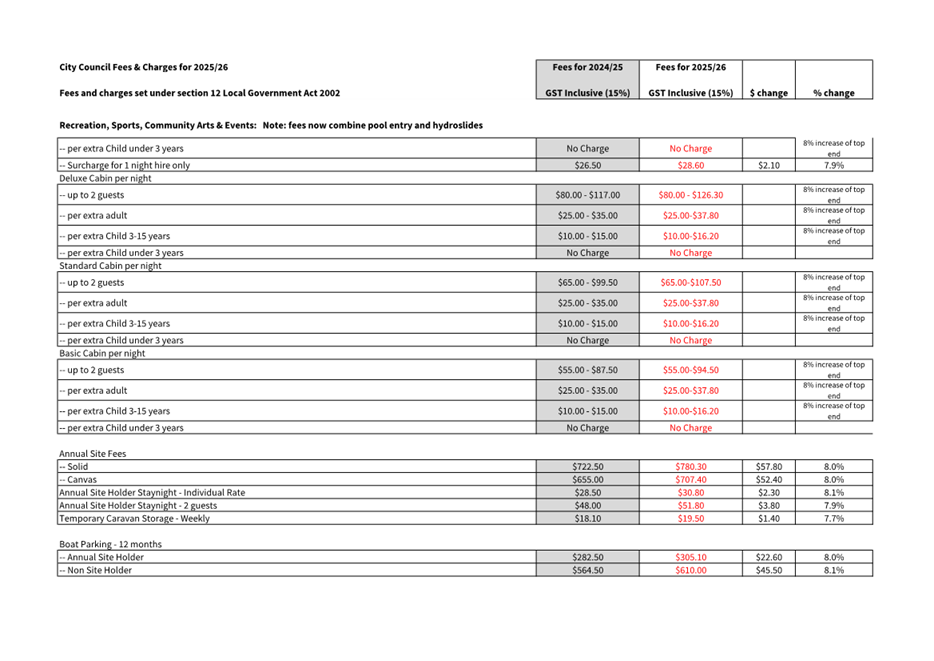

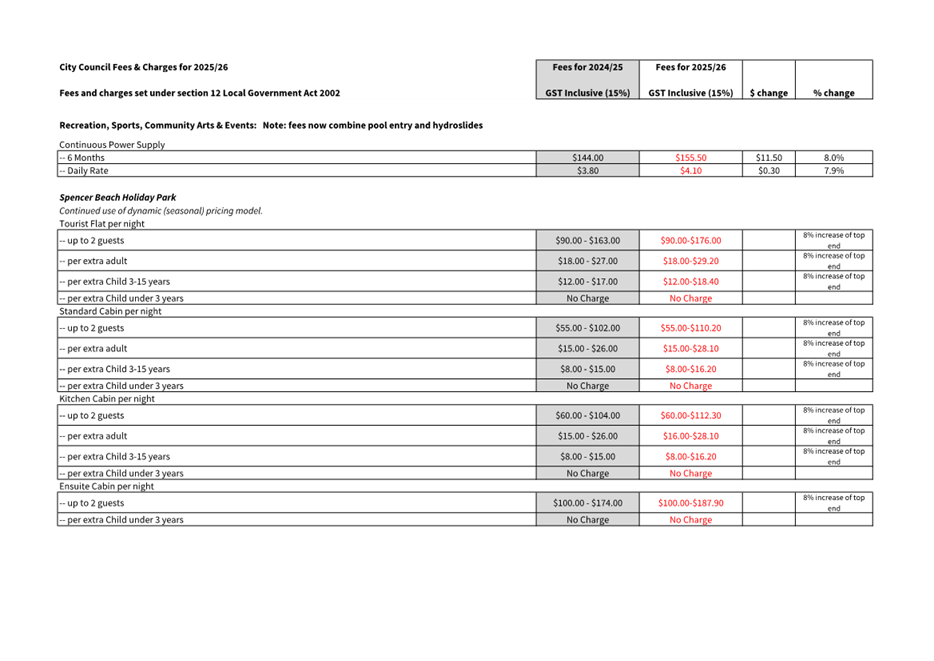

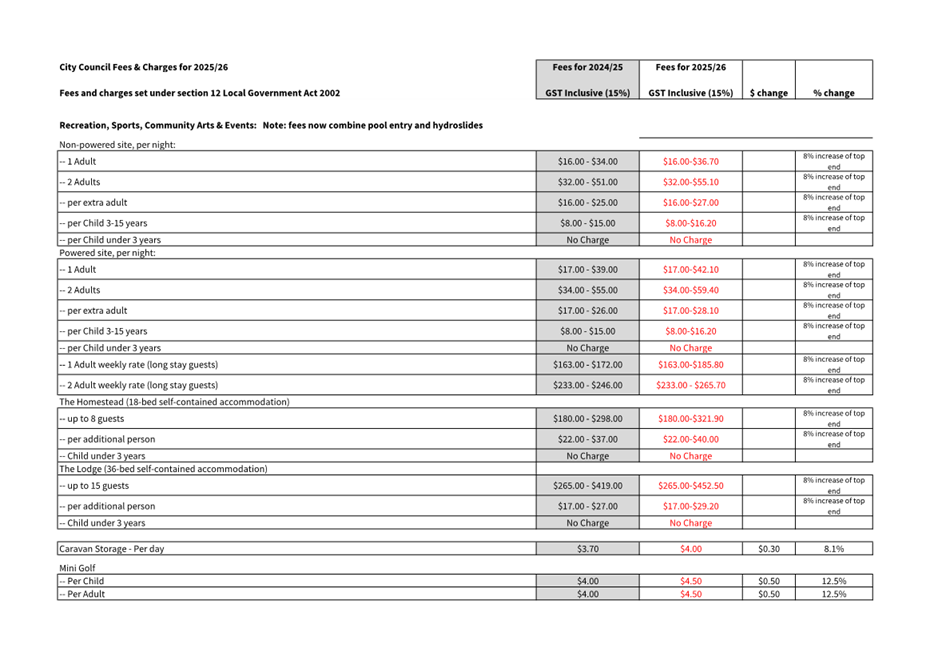

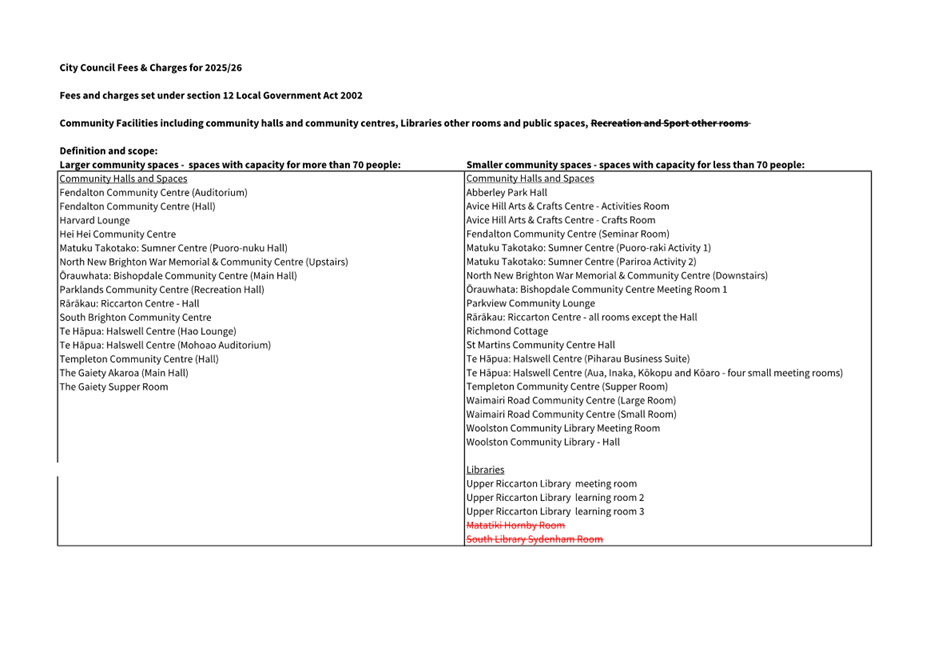

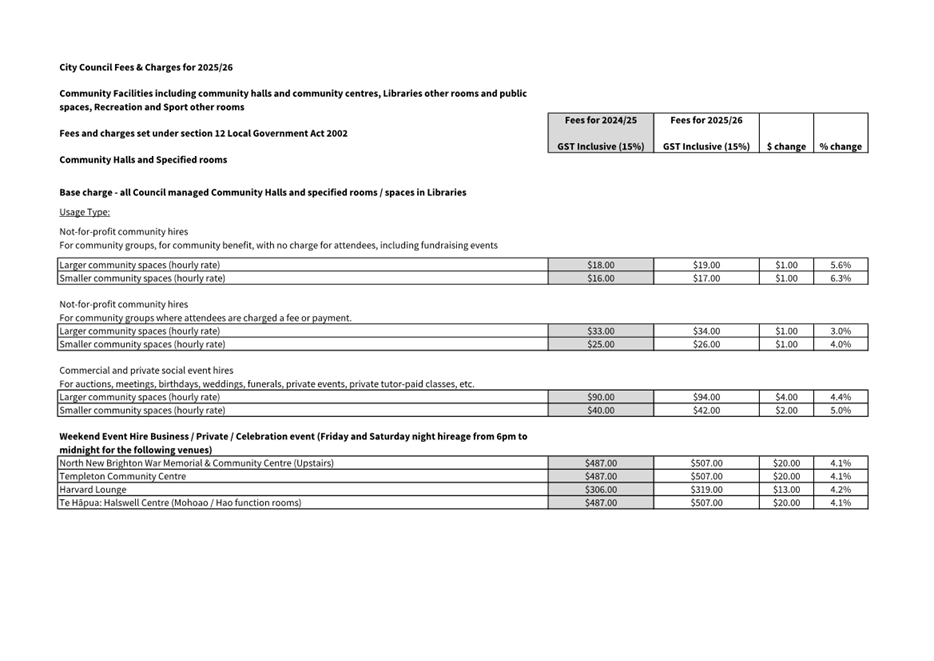

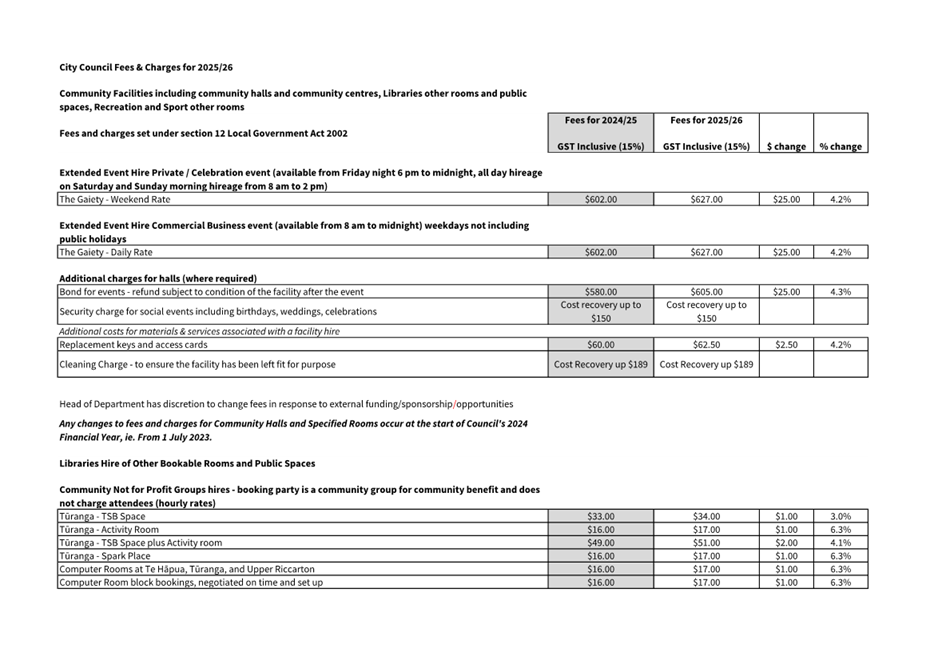

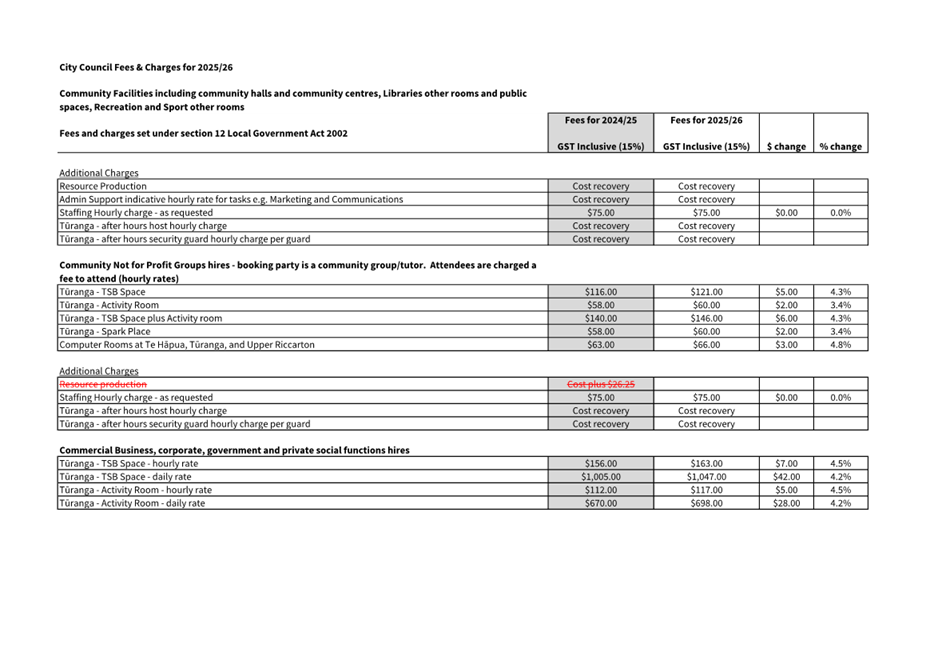

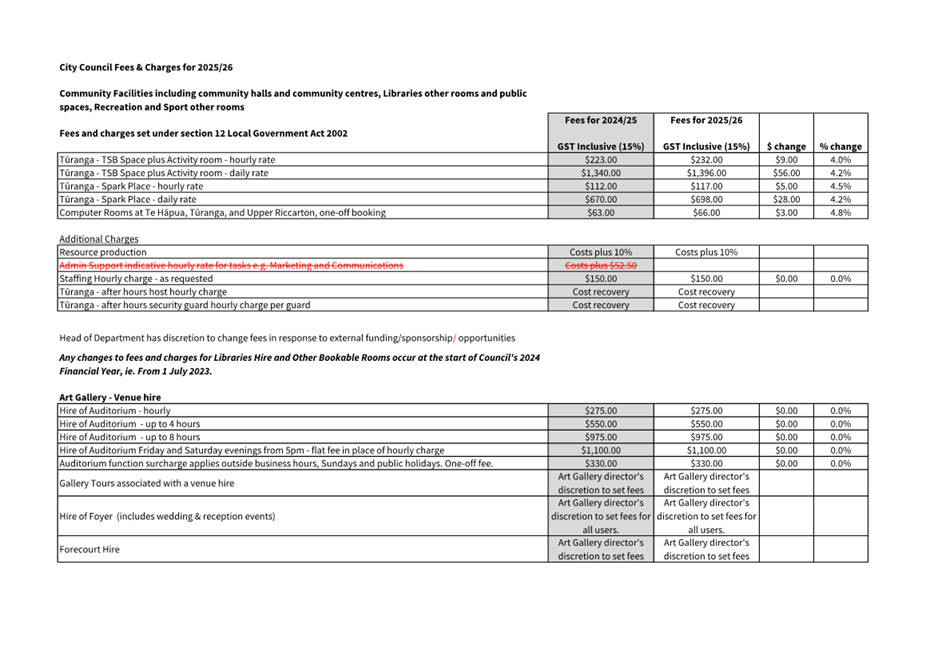

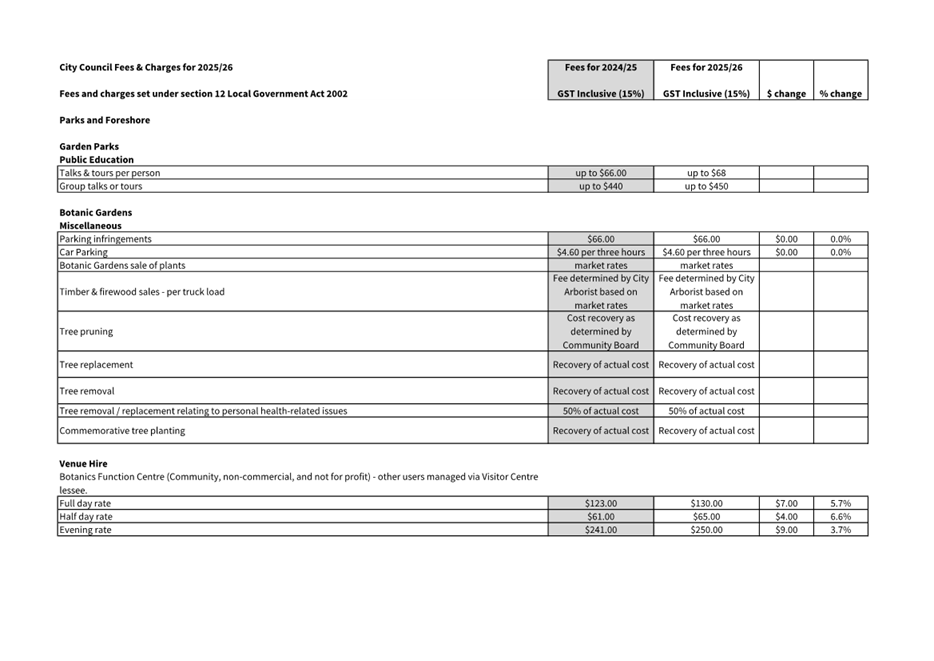

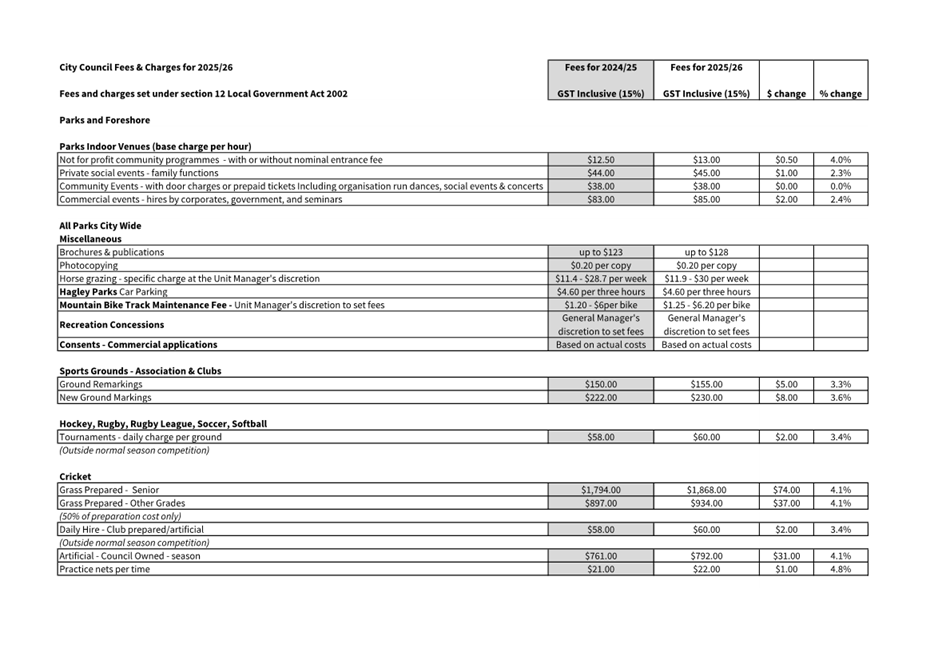

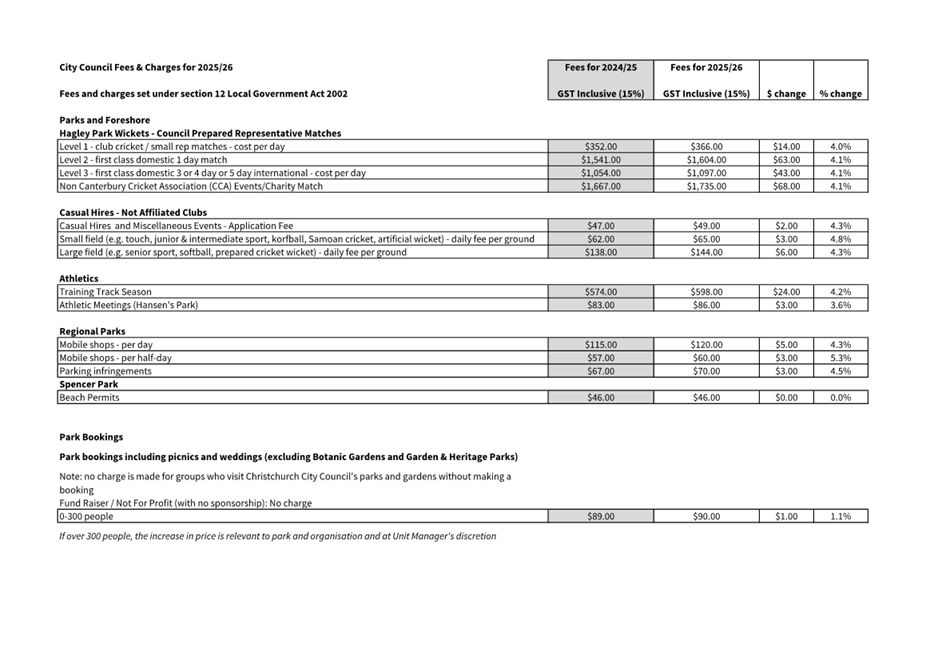

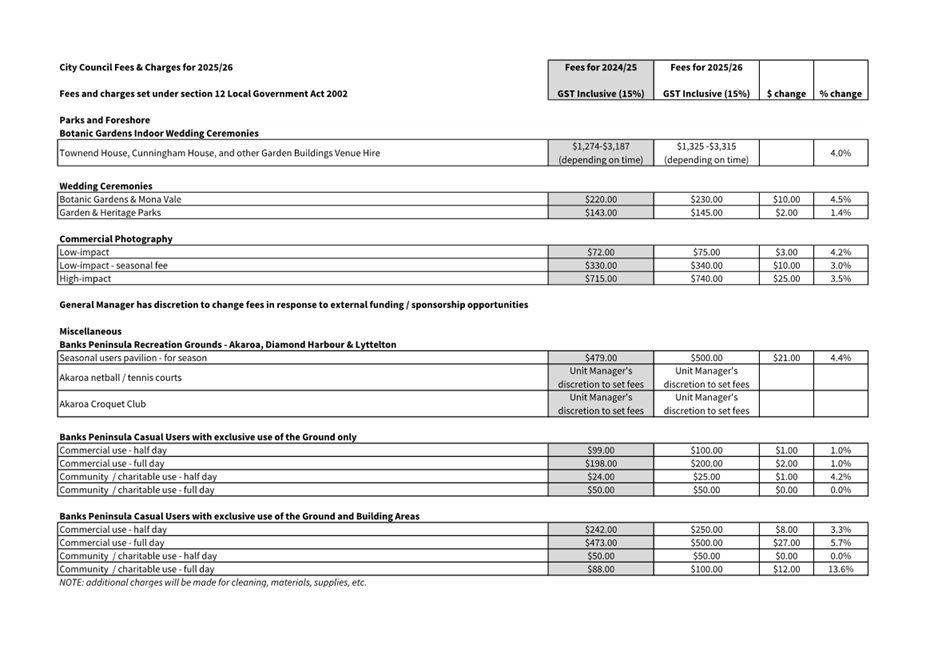

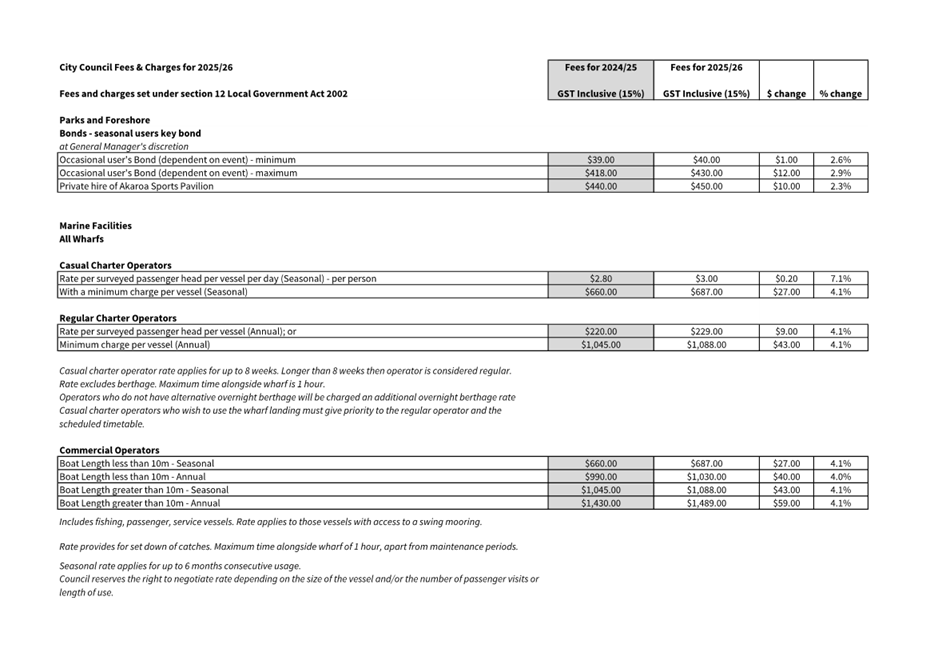

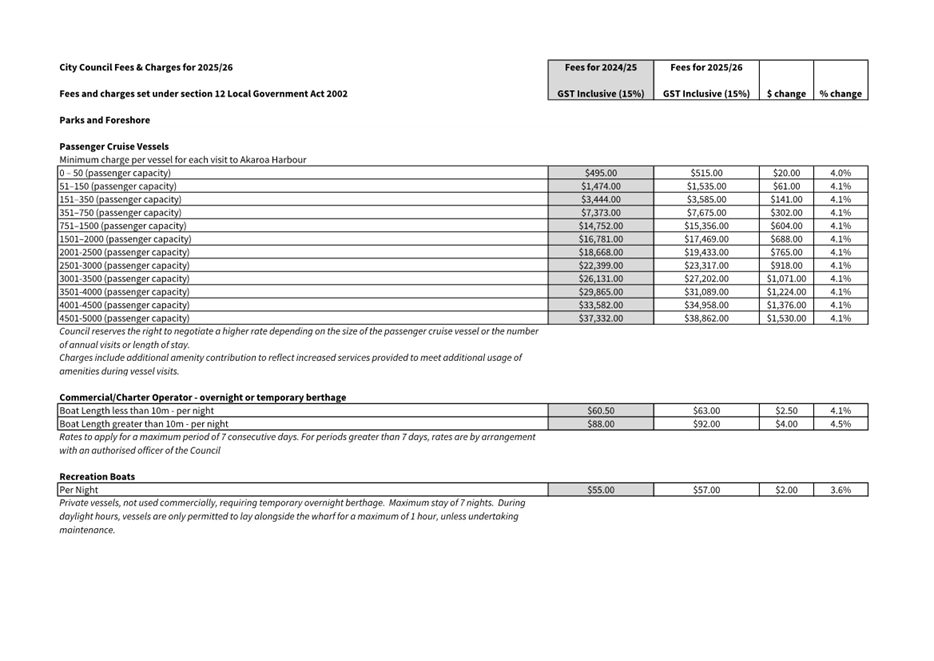

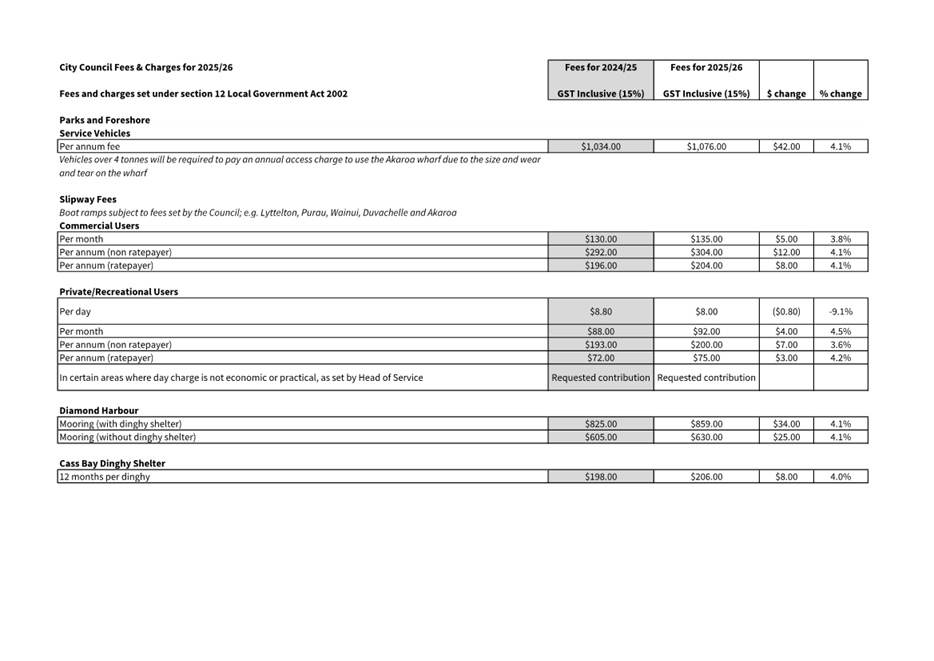

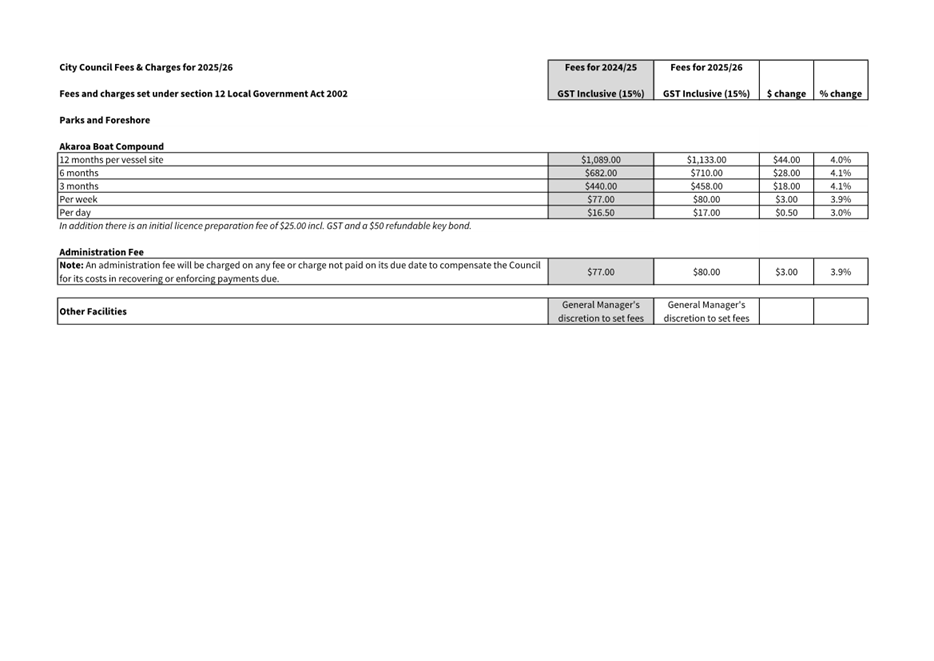

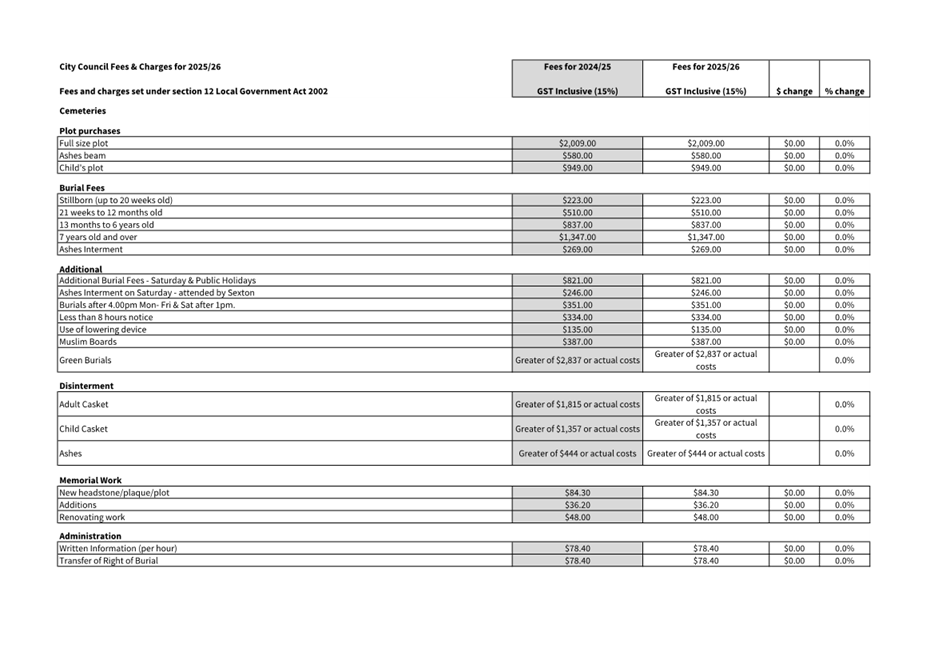

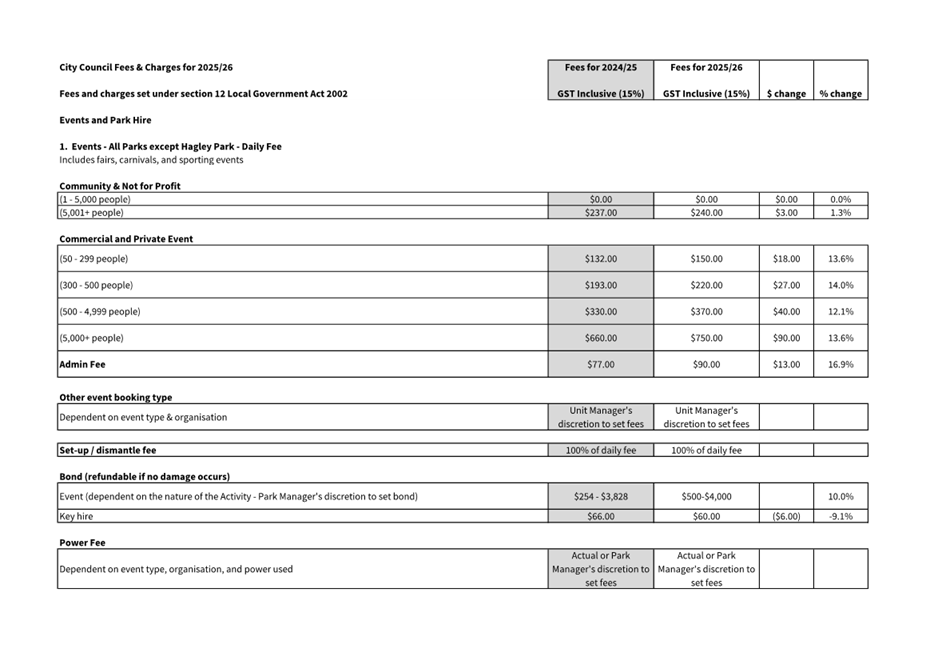

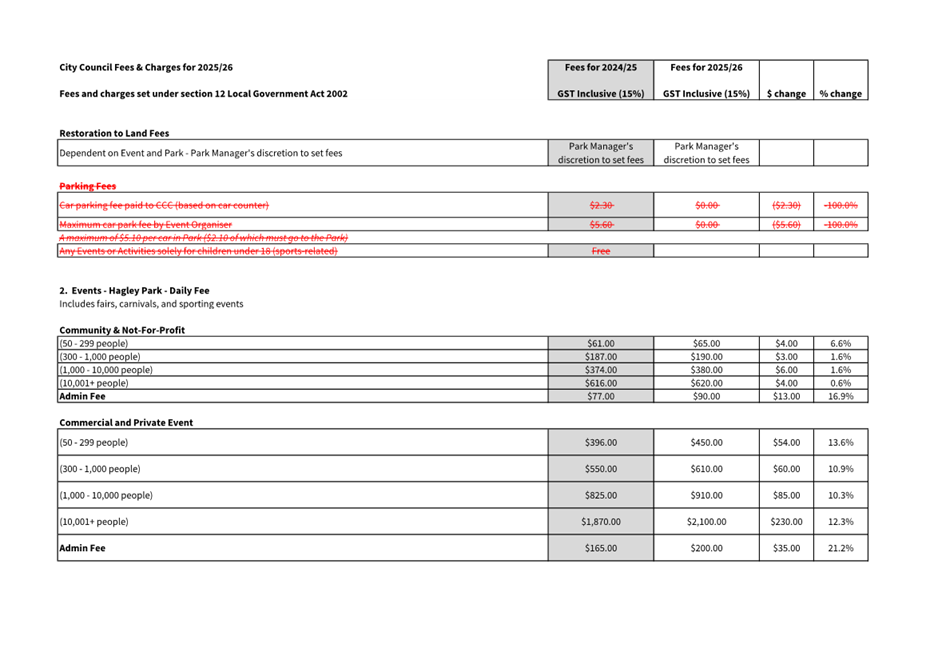

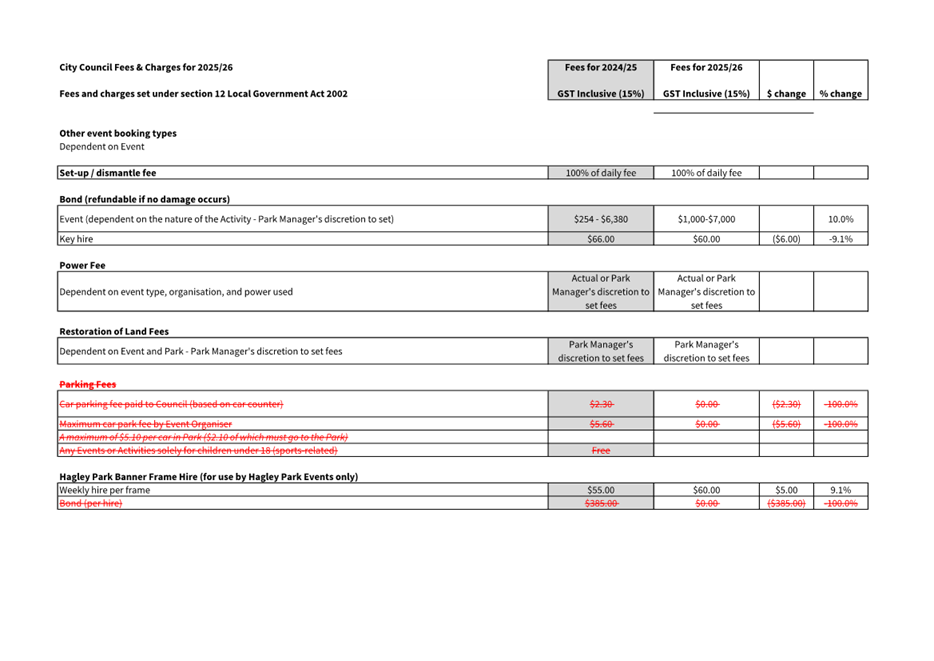

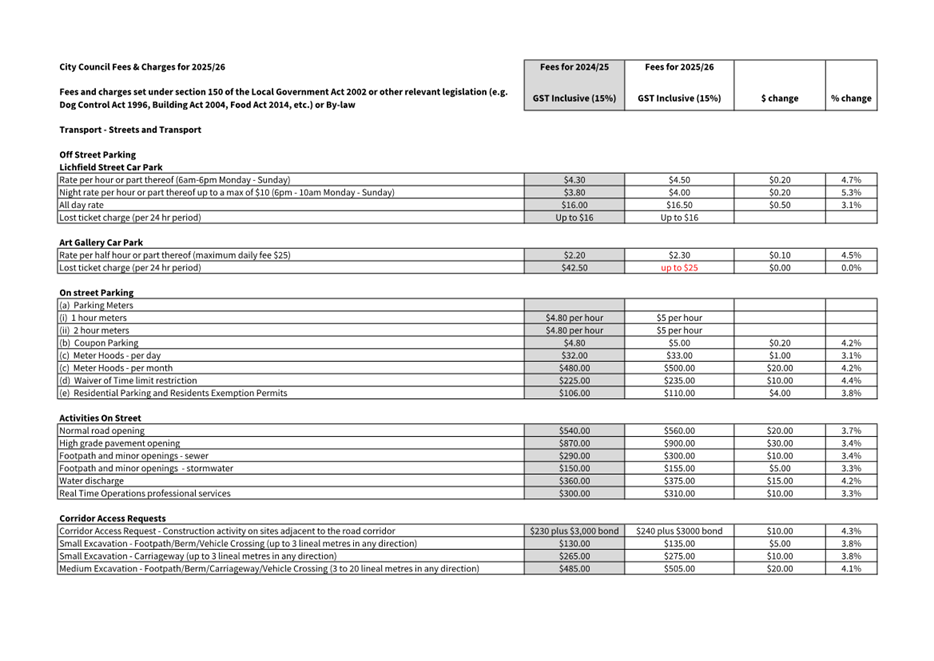

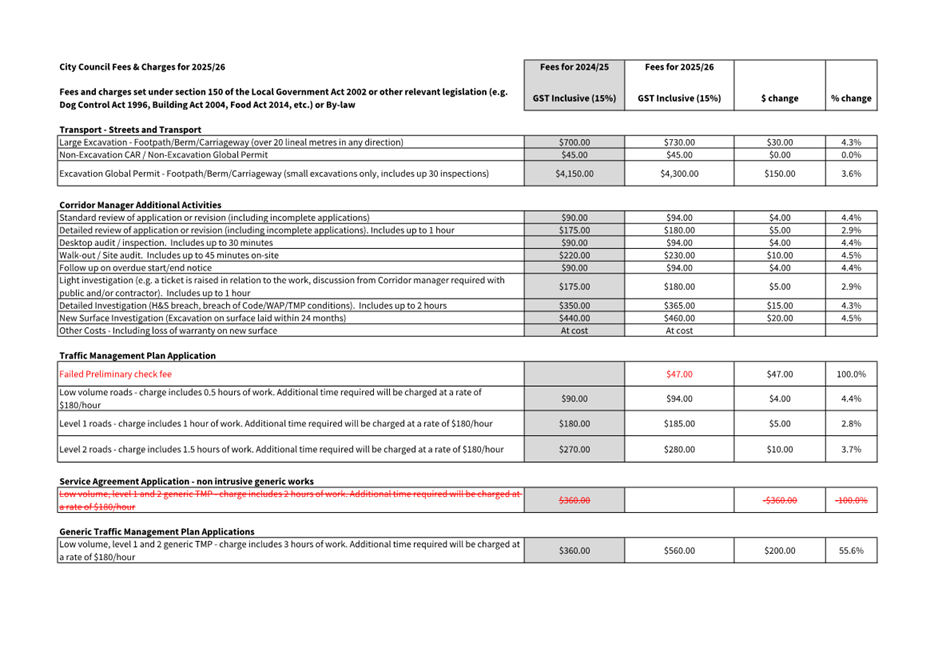

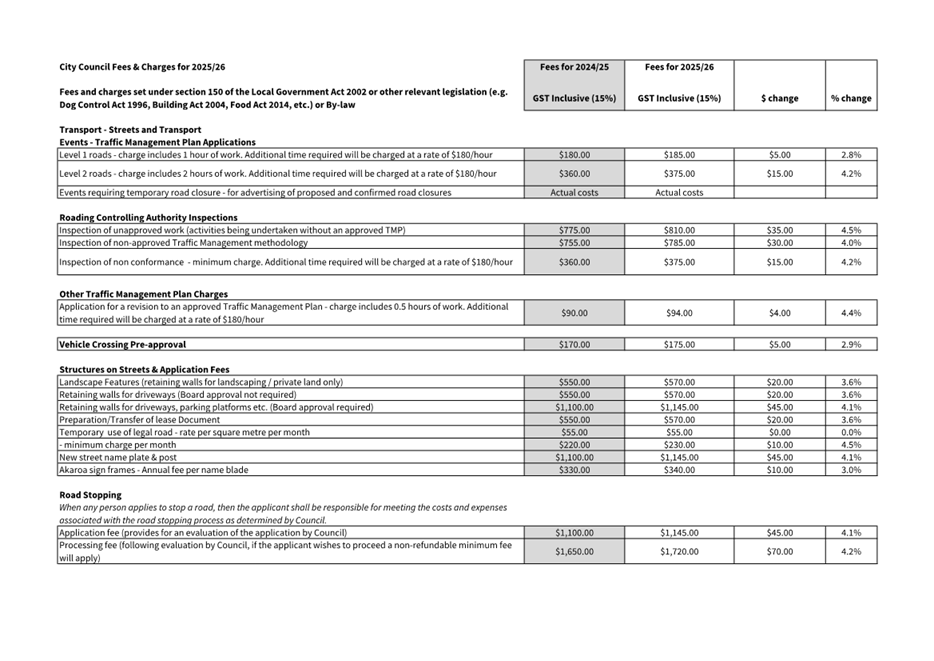

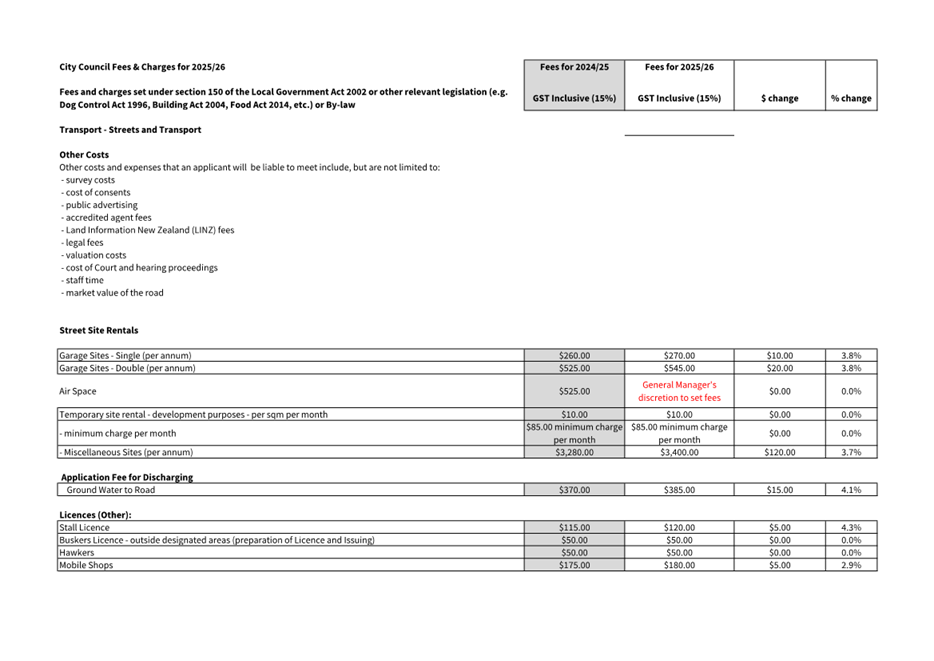

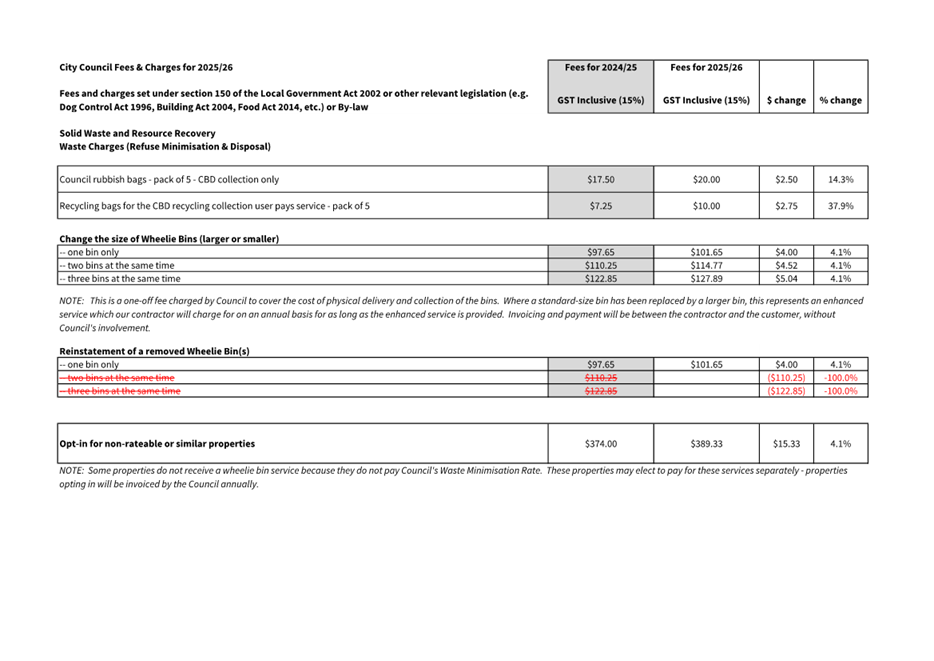

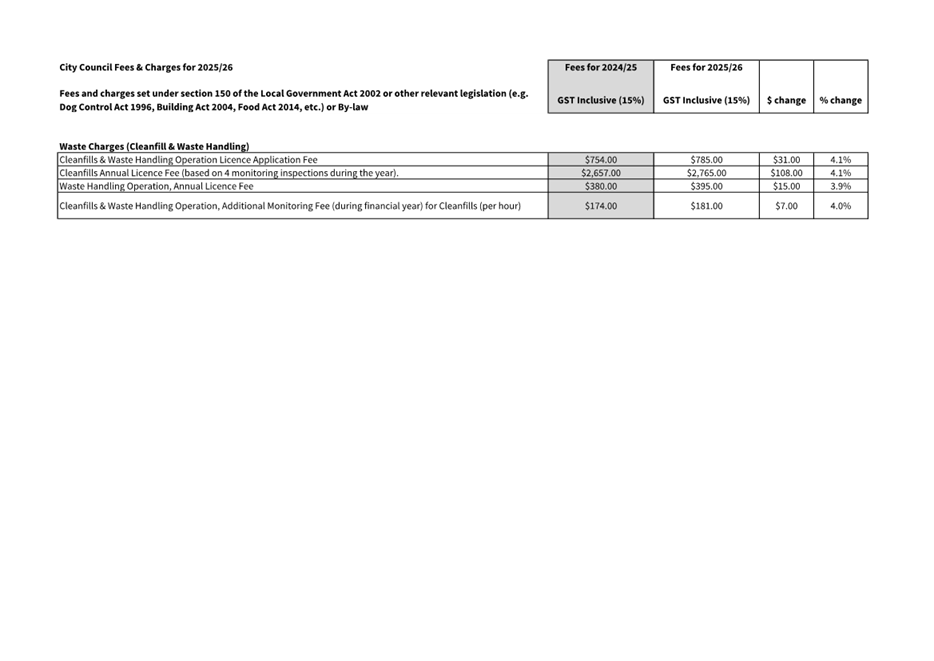

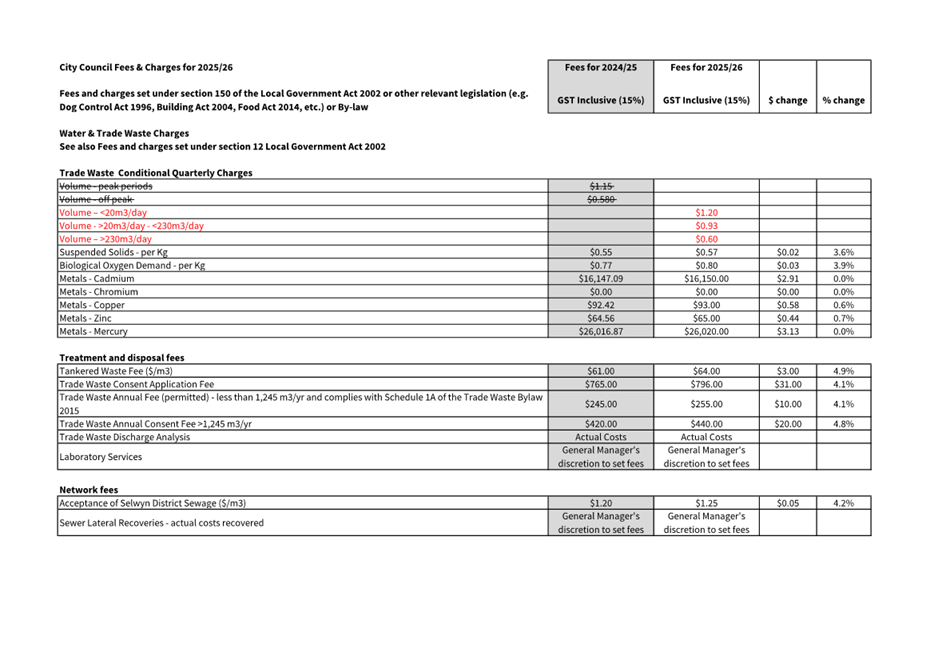

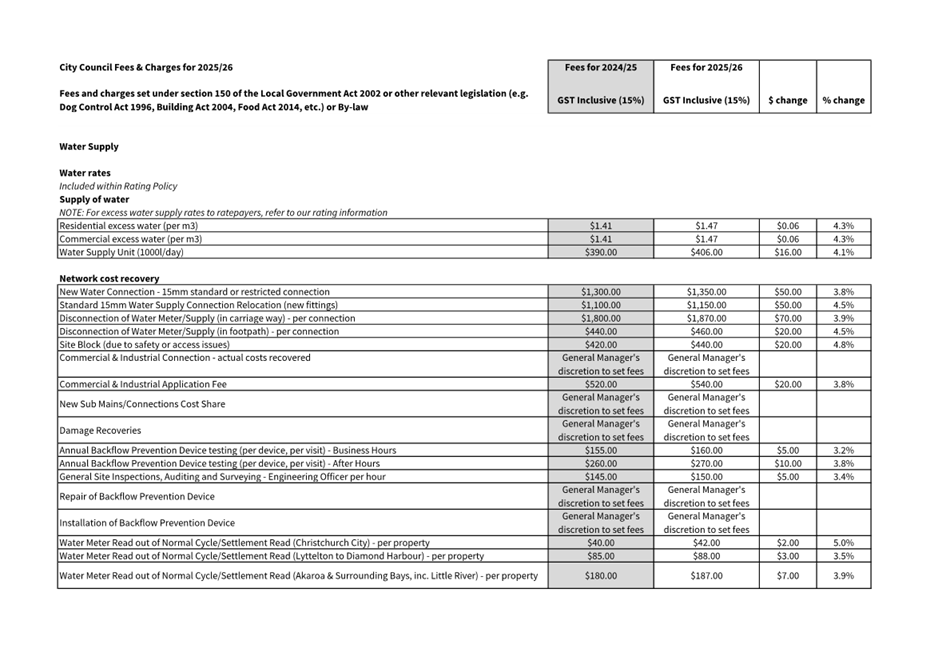

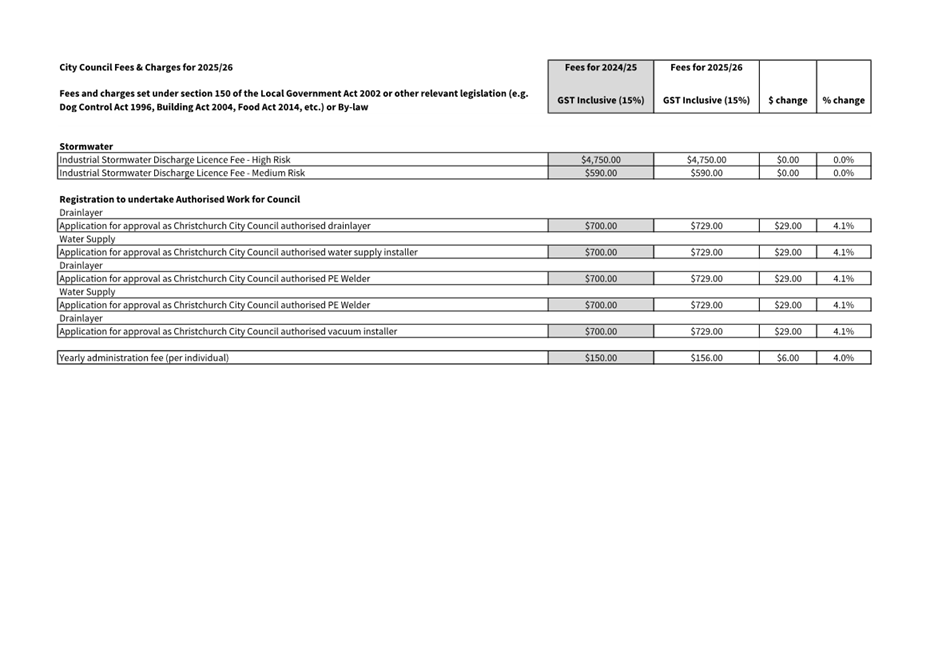

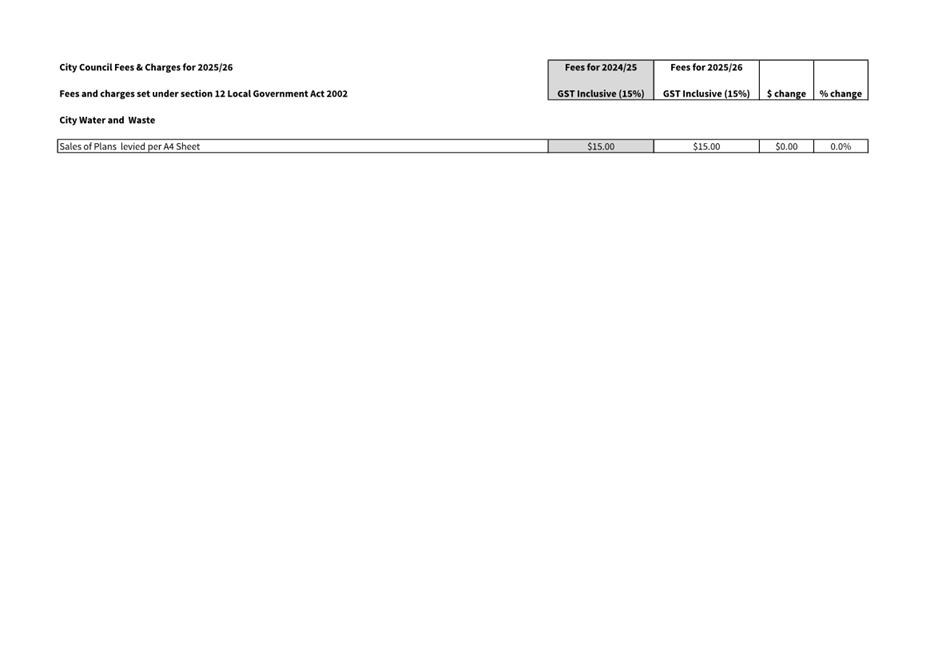

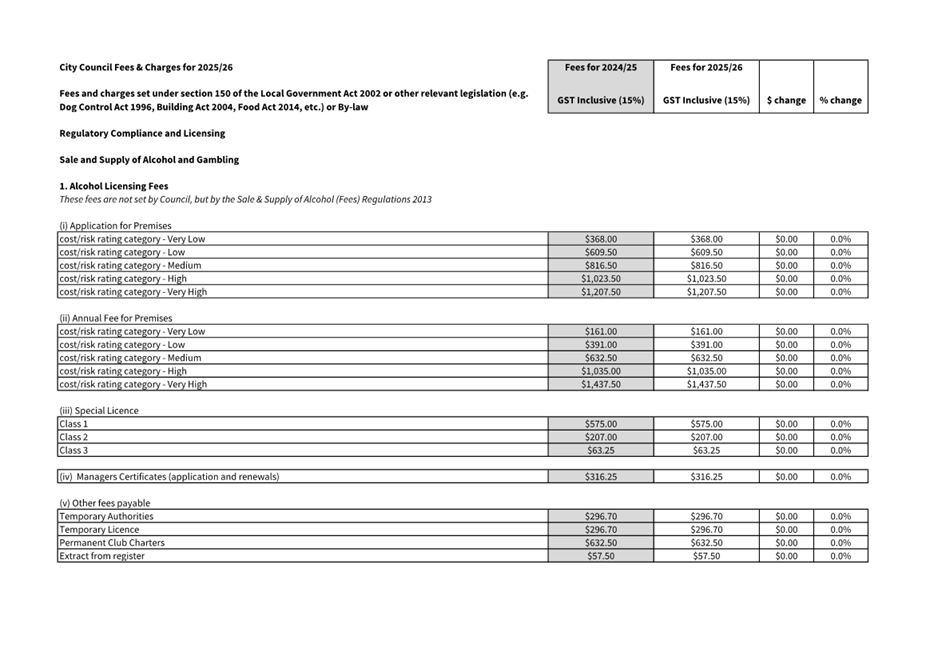

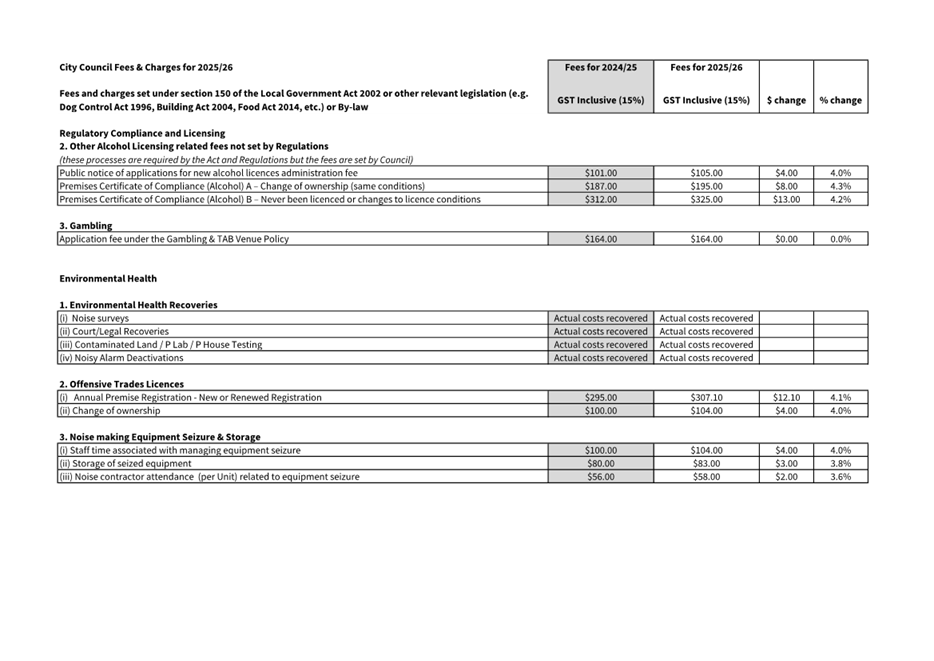

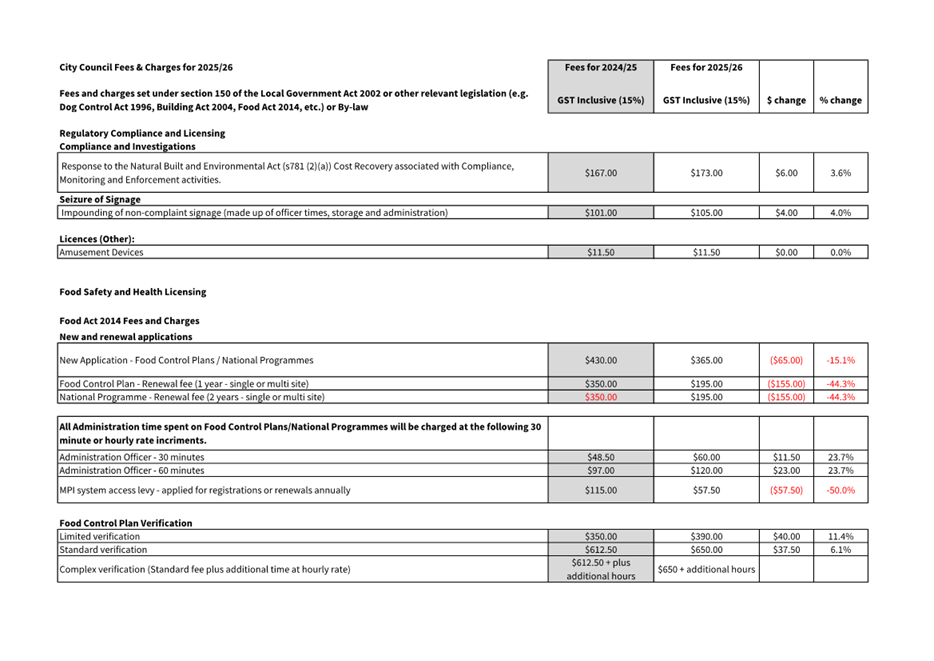

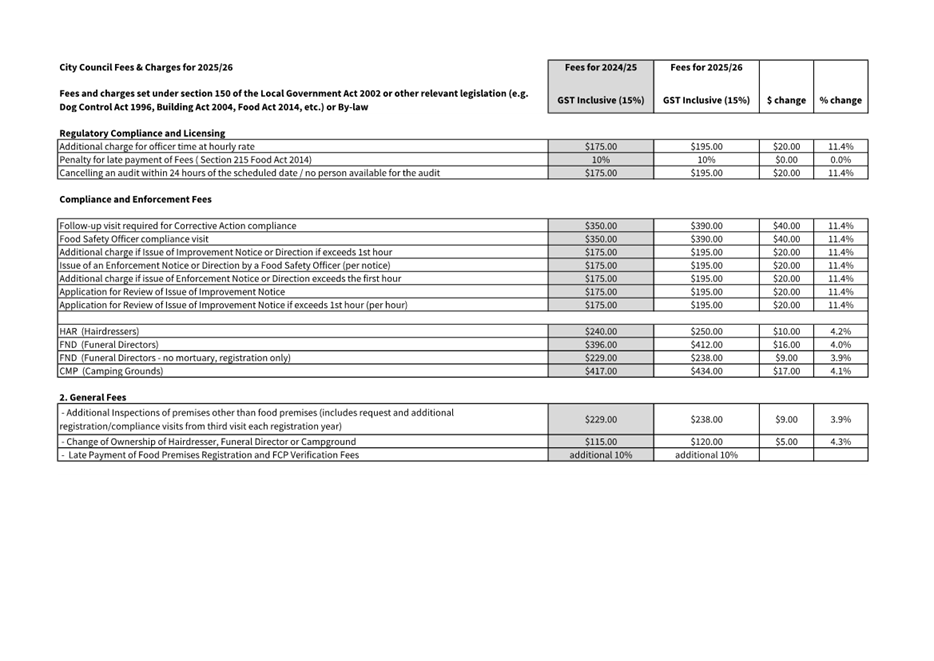

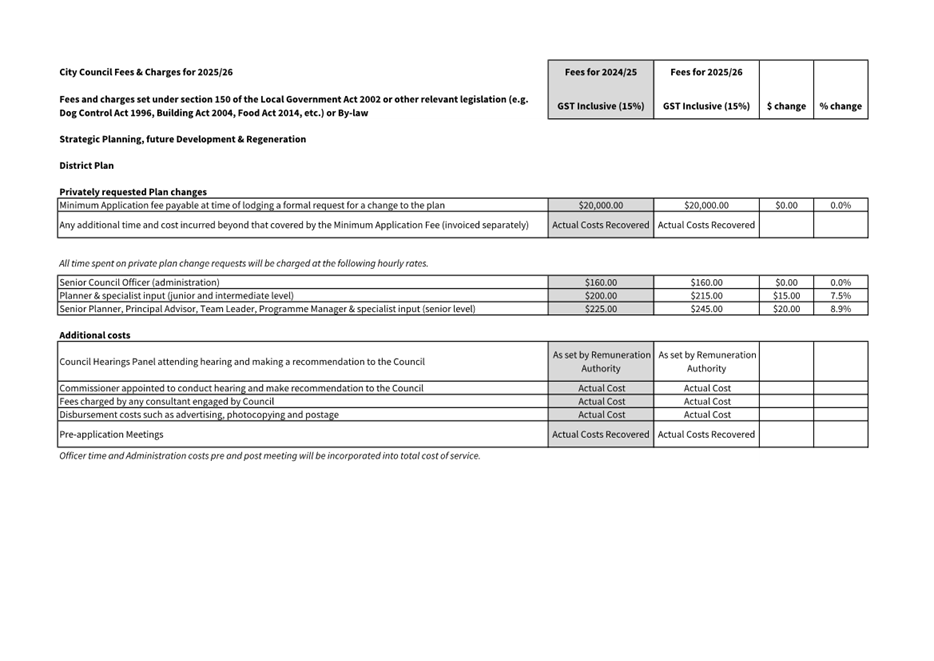

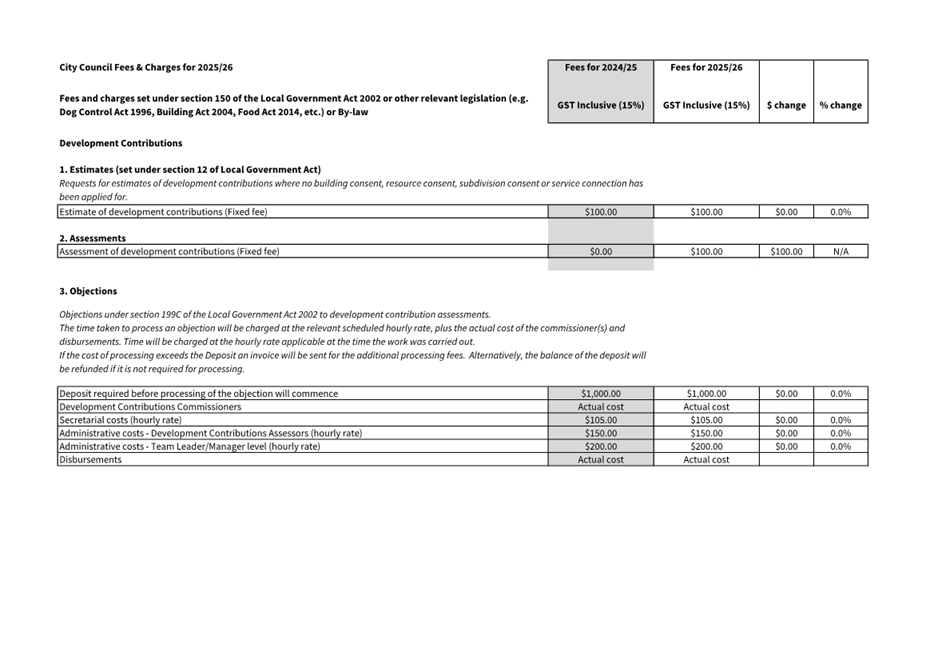

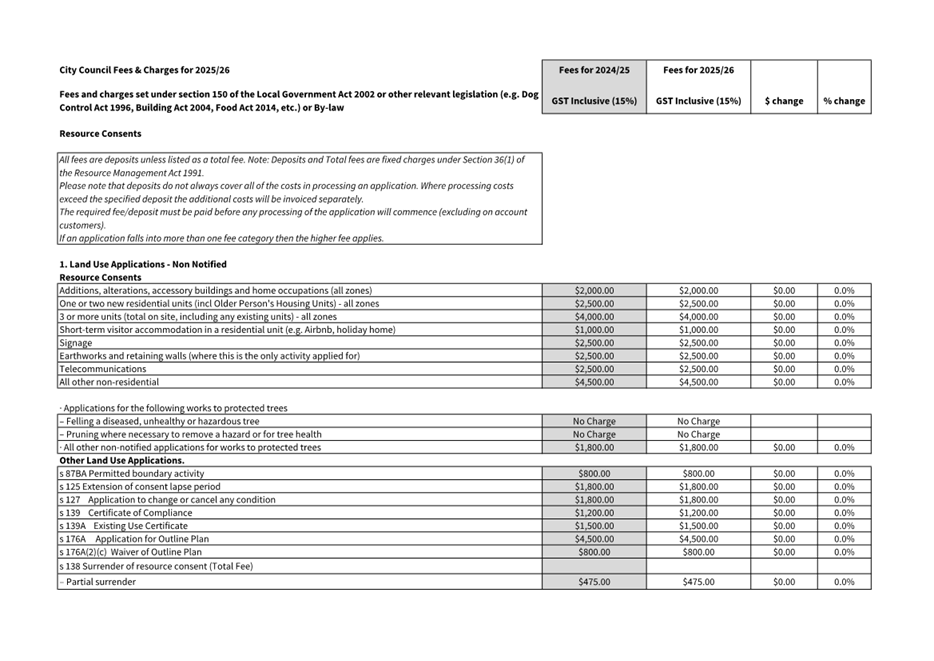

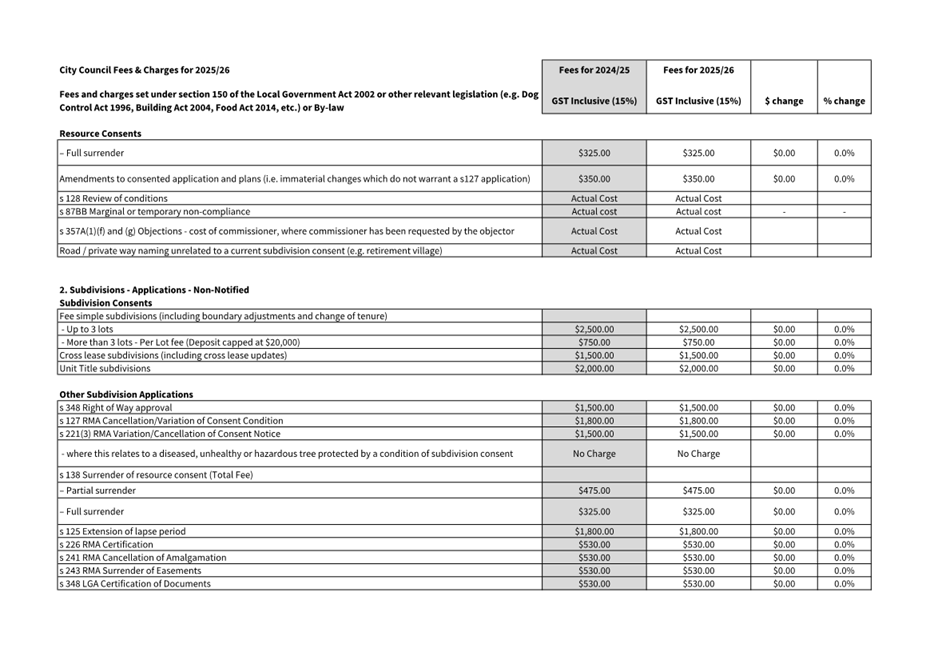

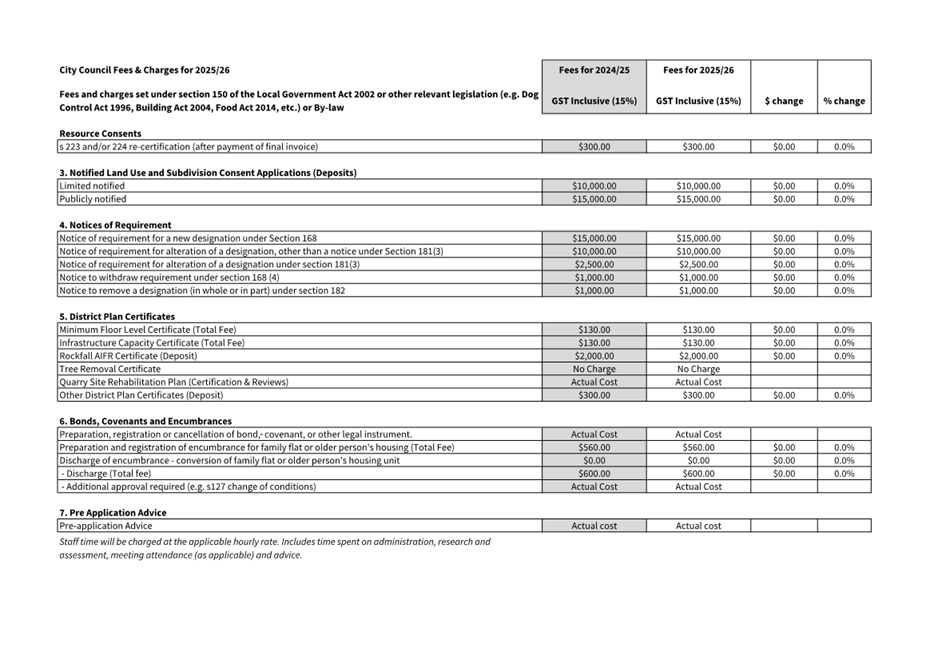

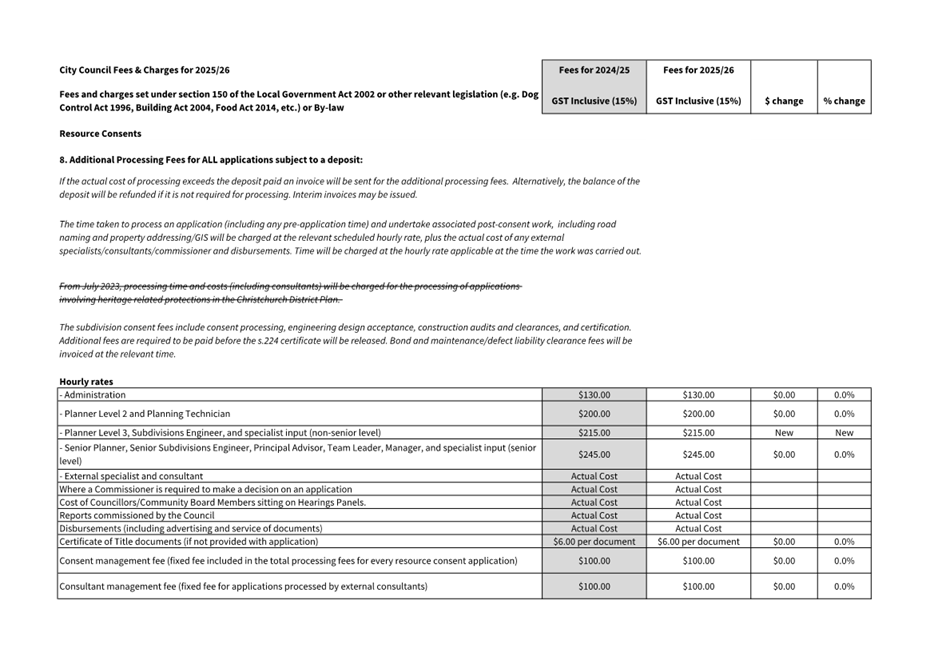

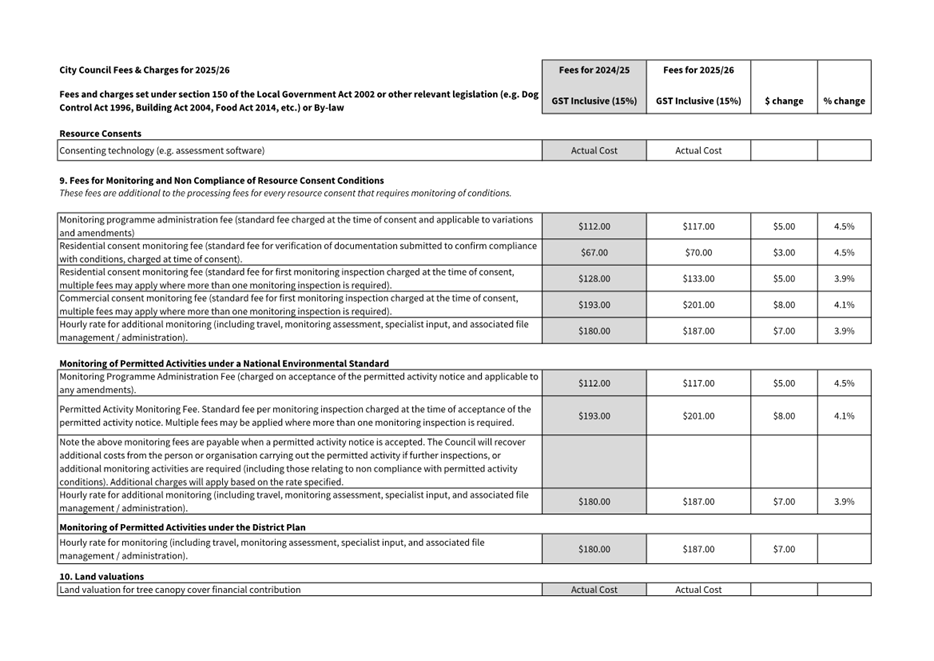

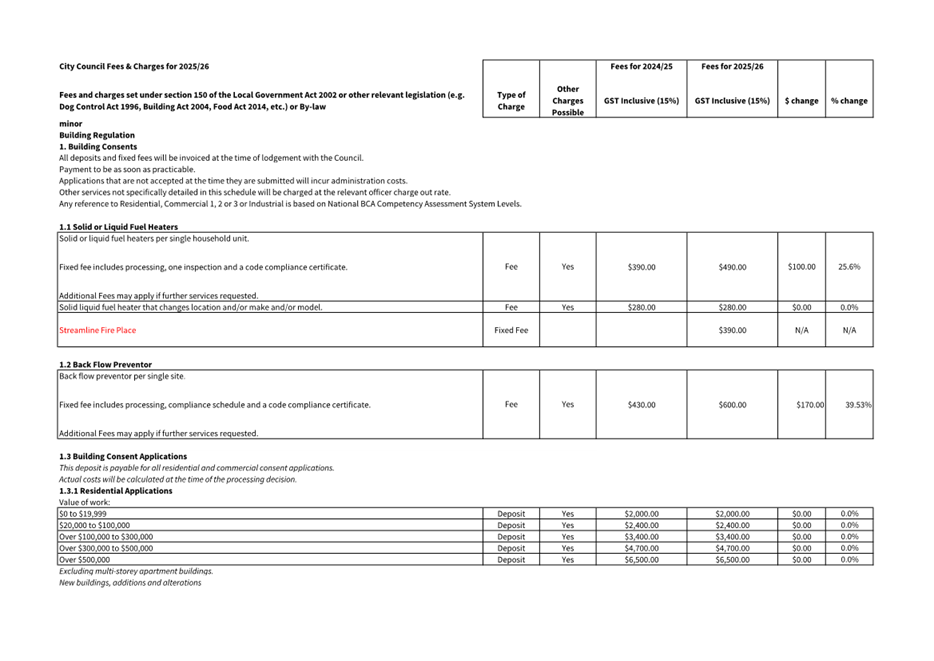

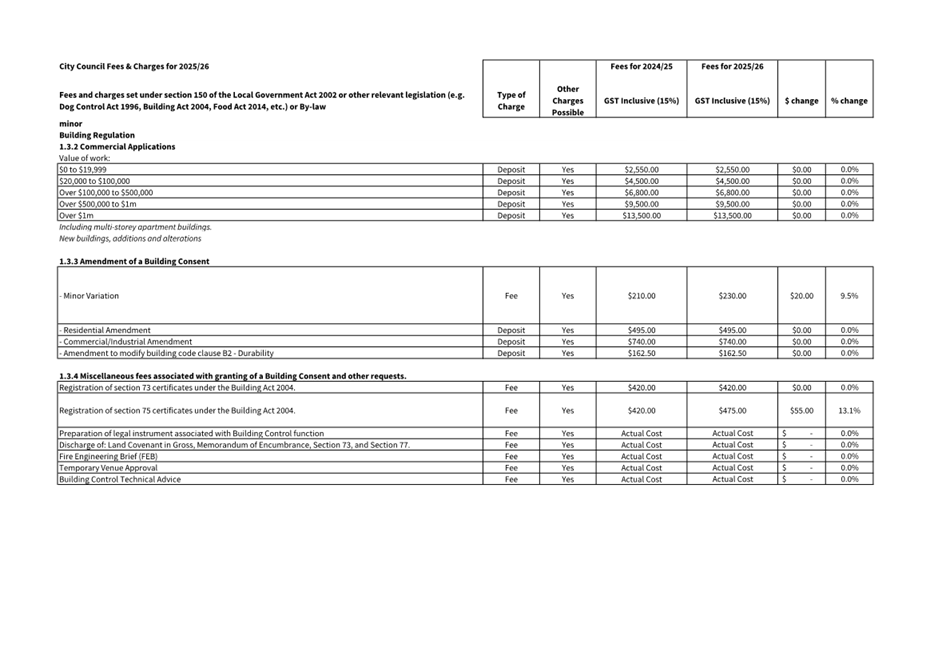

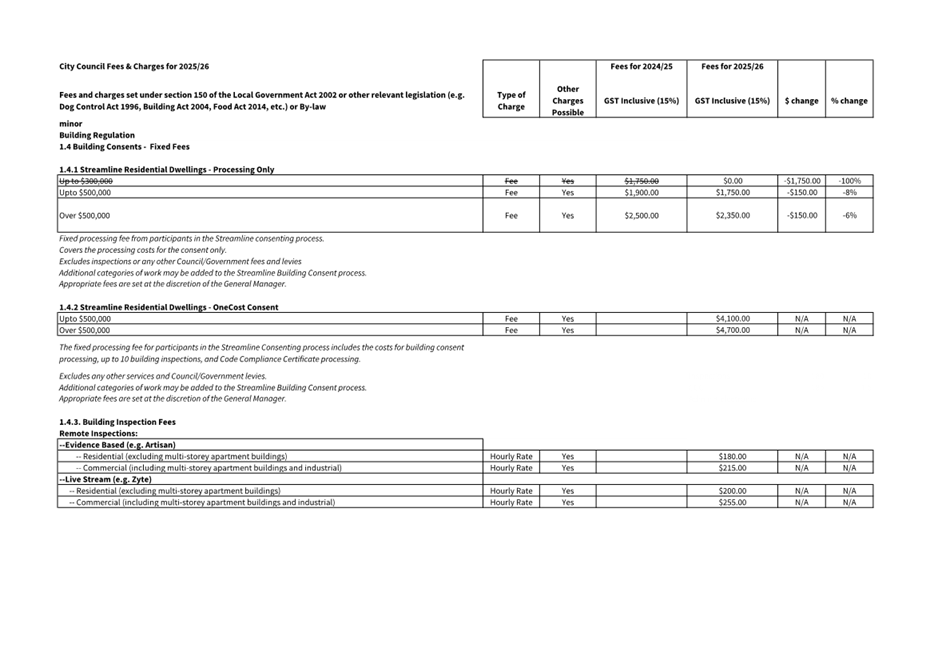

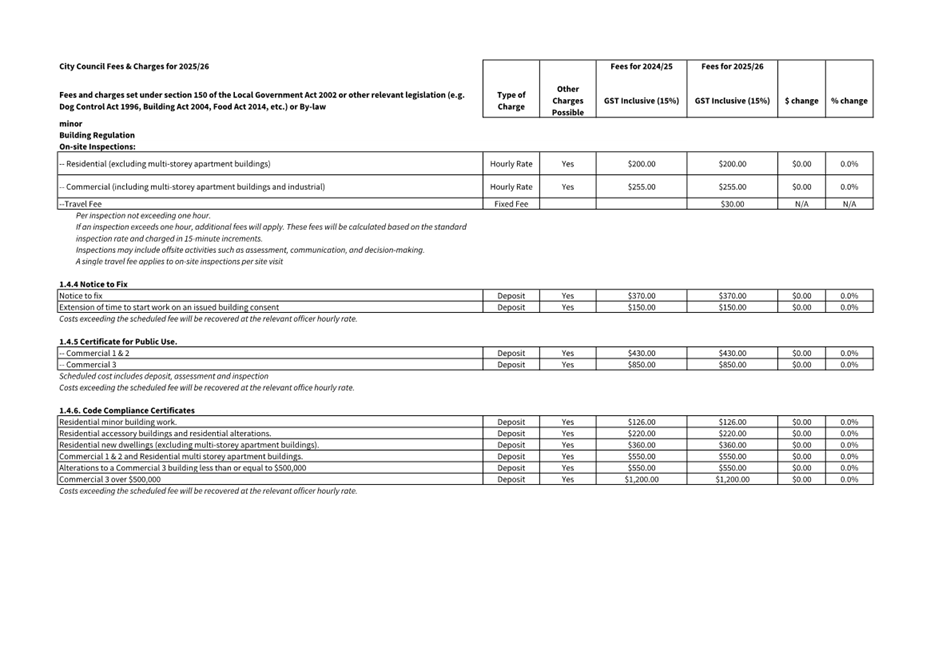

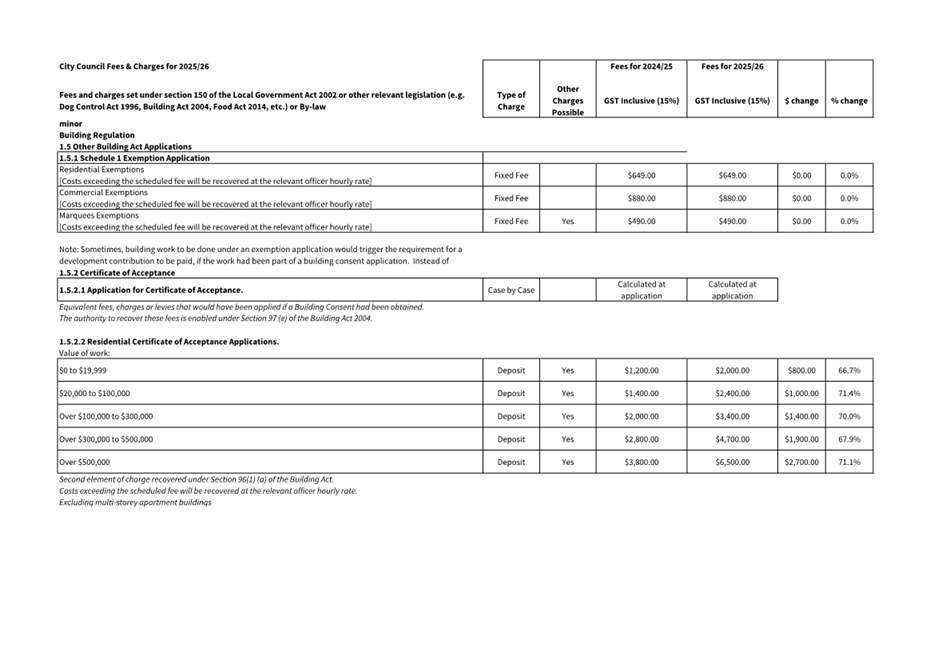

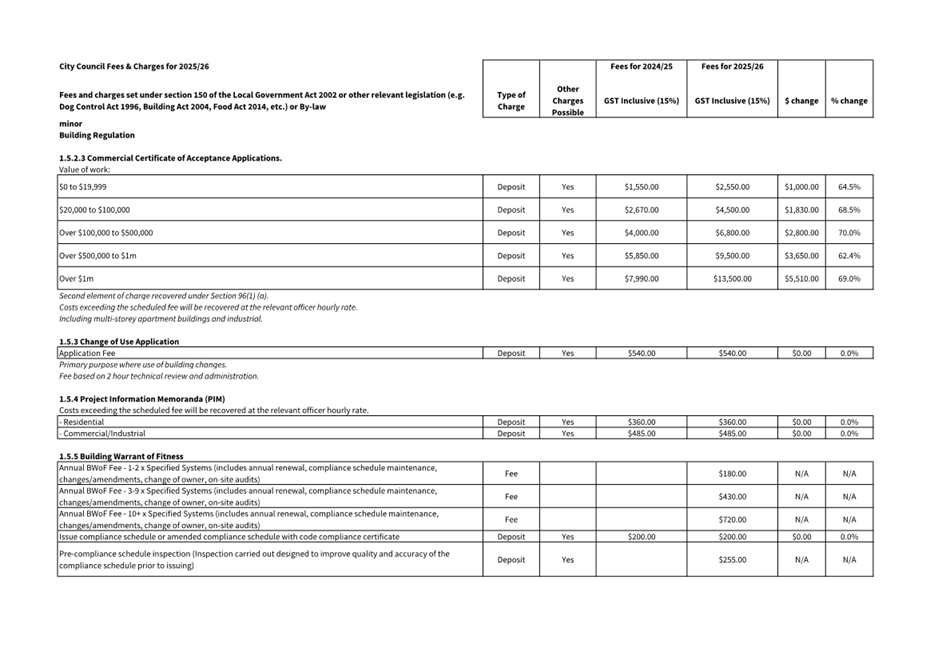

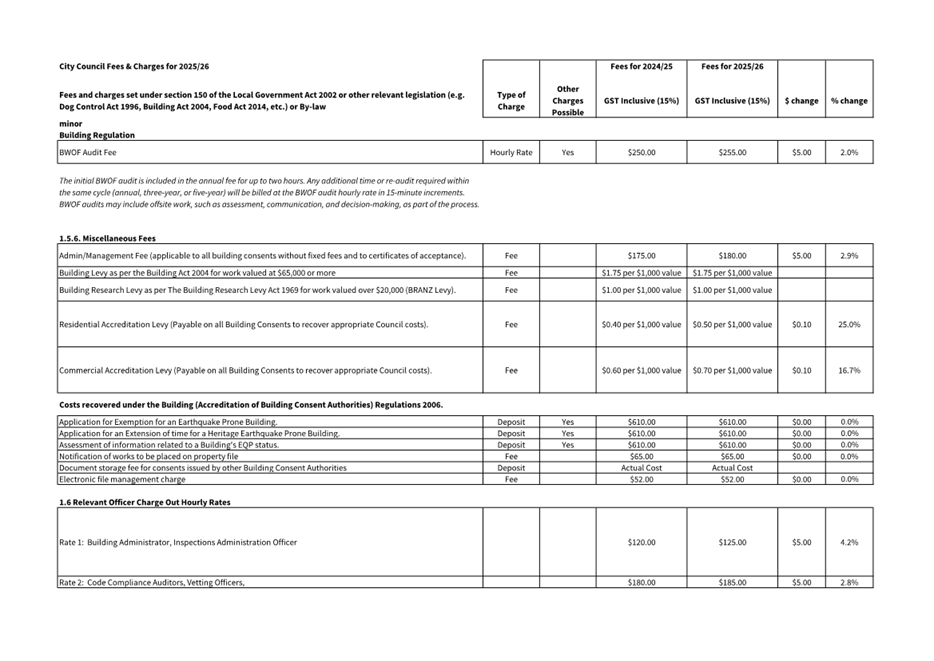

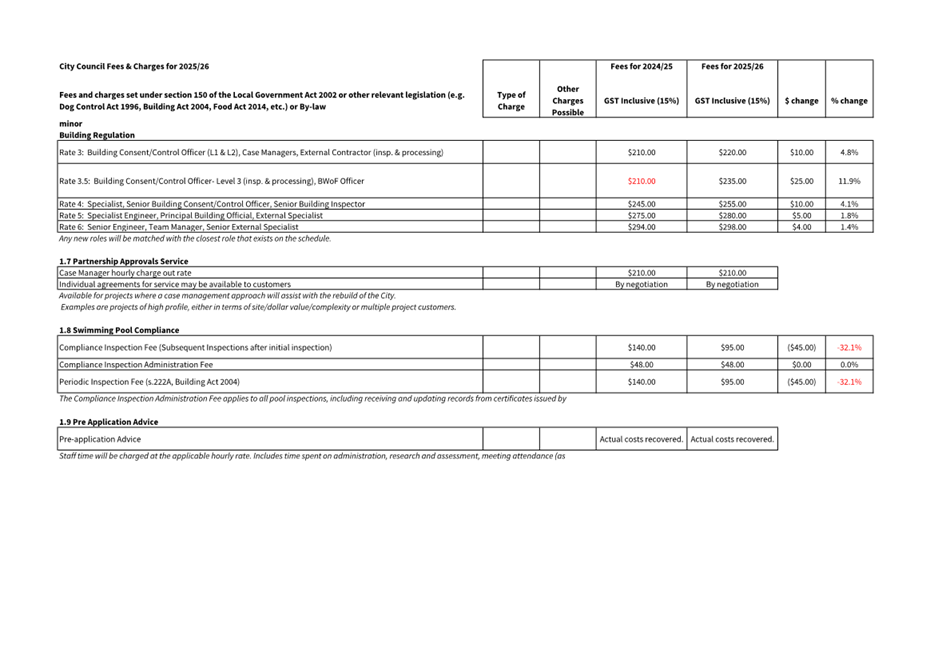

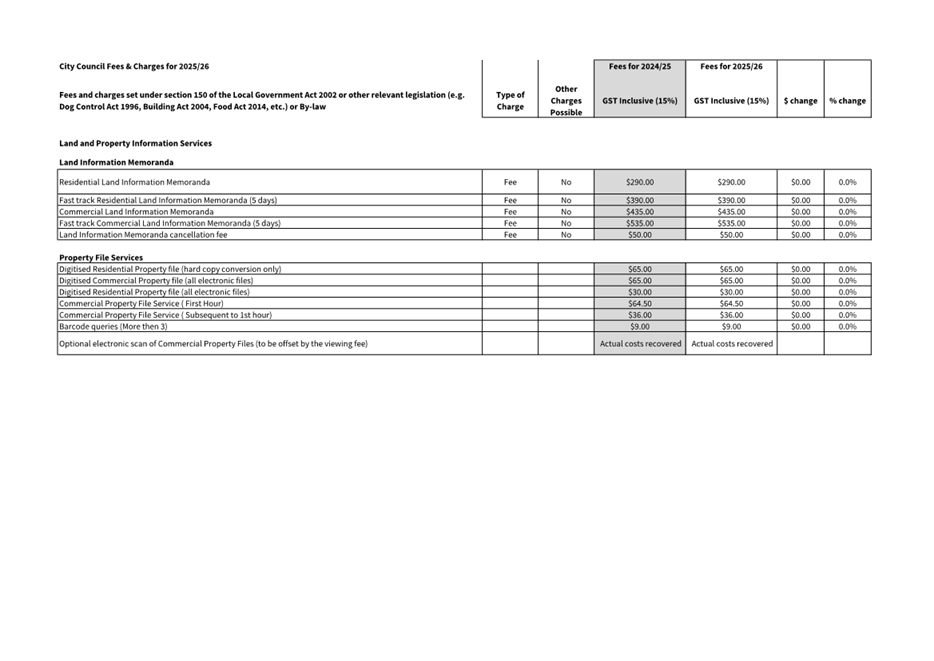

8. Fees and Charges

8.1 A schedule of proposed Fees and Charges is included (refer Attachment

H). In recommending the proposed fees, staff have been conscious of the

financial pressure on residents and ratepayers and have attempted to avoid

increases that would create a barrier to the community’s utilisation of

Council’s services.

8.2 As a result of the above, limitations imposed by the

market, and the varying inflationary impacts on costs and limits on cost

recovery, fee increases proposed for 2025/26 vary but generally align to

expected Council inflation of 4.1%.

8.3 Proposed Trade Waste charges contain a change in

methodology that is being consulted on.

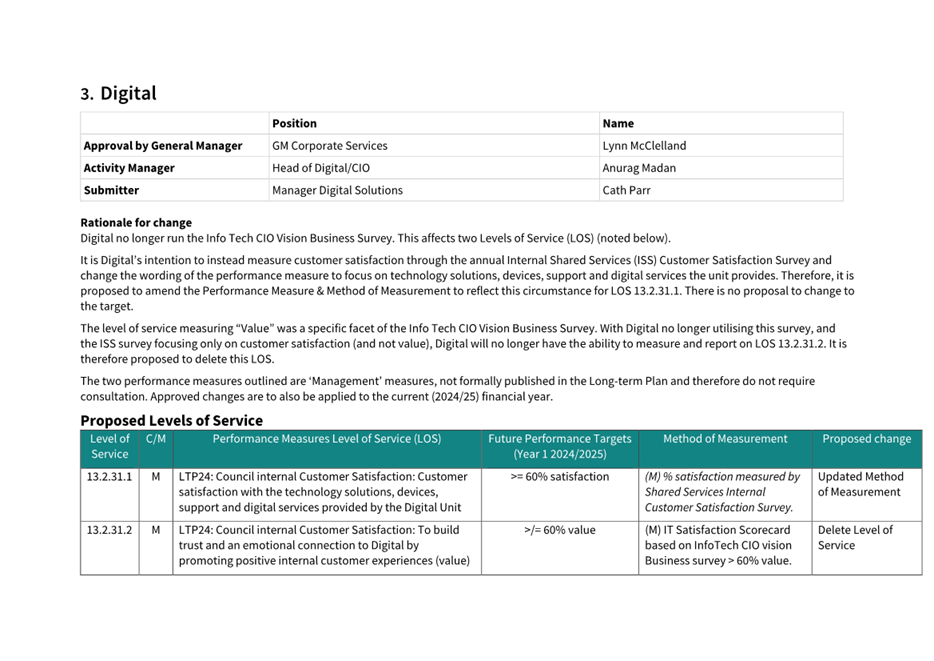

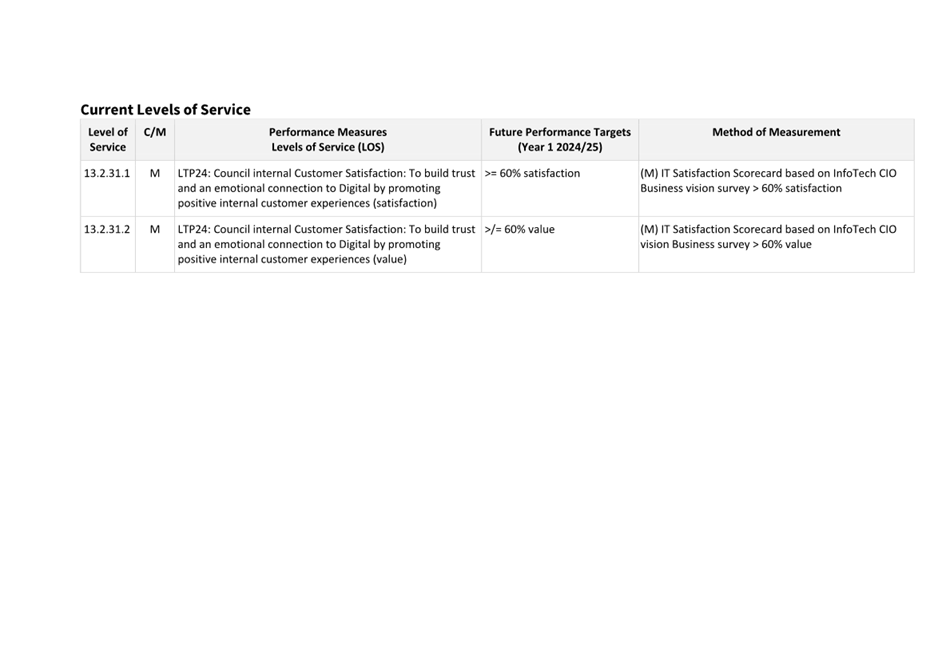

9. Changes to Levels of Service

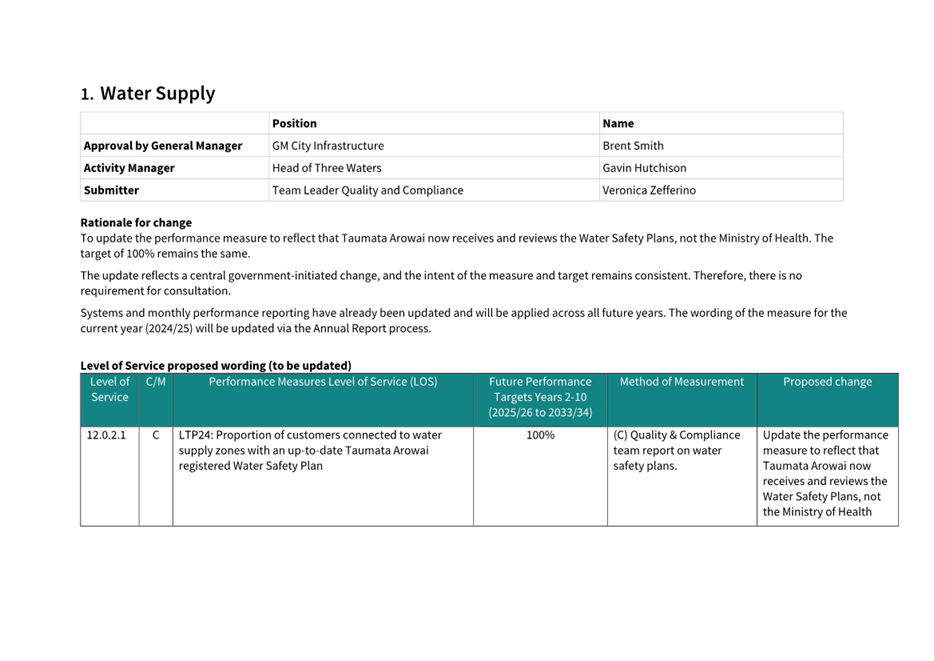

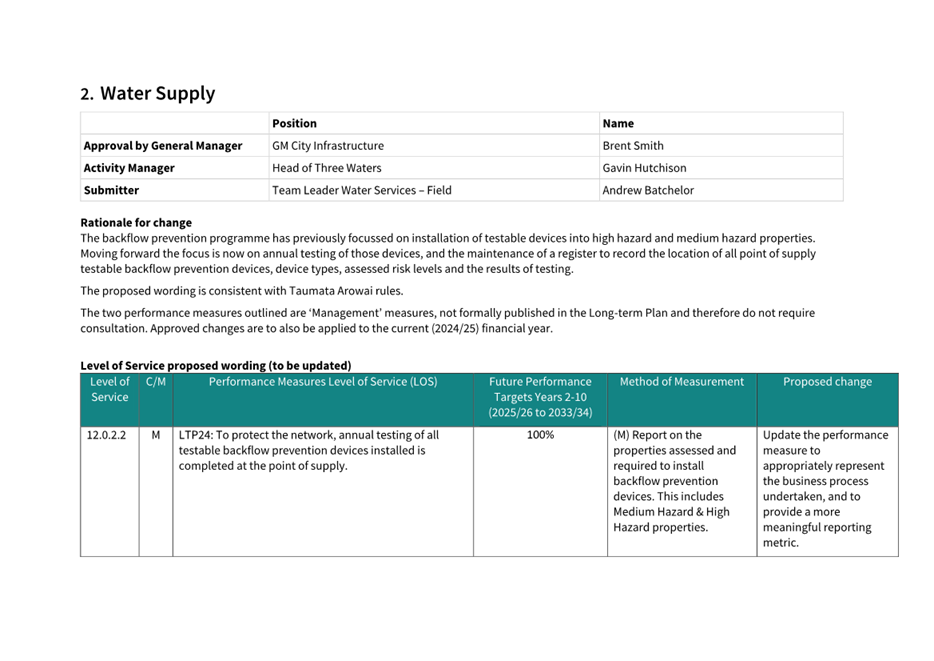

9.1 There are proposed minor changes to five Measures of

Success and targets (levels of service) accompanied by rationale (refer Attachment

G).

9.2 In summary the changes are;

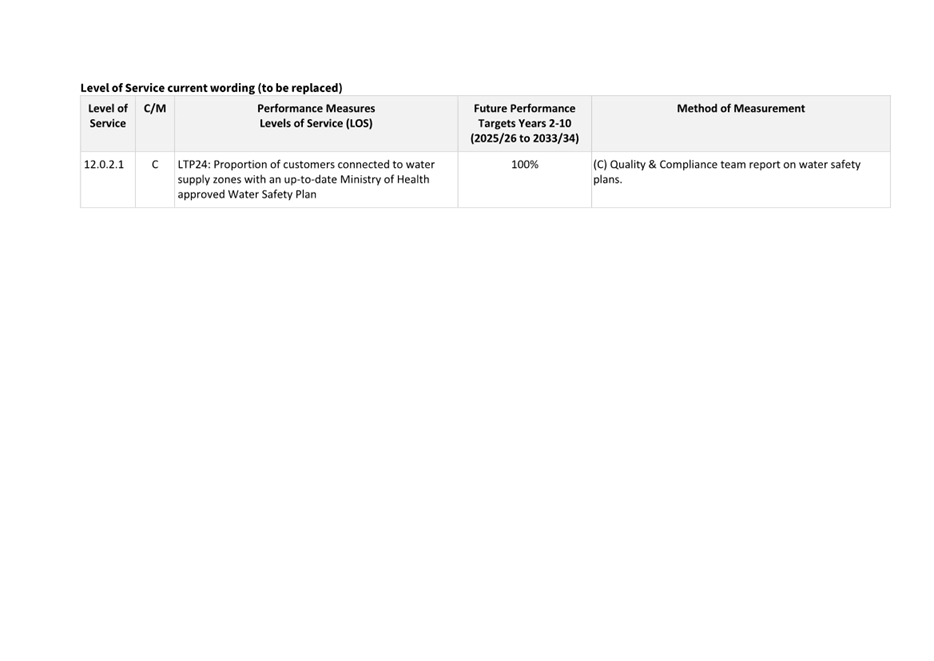

9.2.1 Water Supply (1): to reflect that Taumata

Arowai now receives and reviews the Water Safety Plans,

not the Ministry of Health.

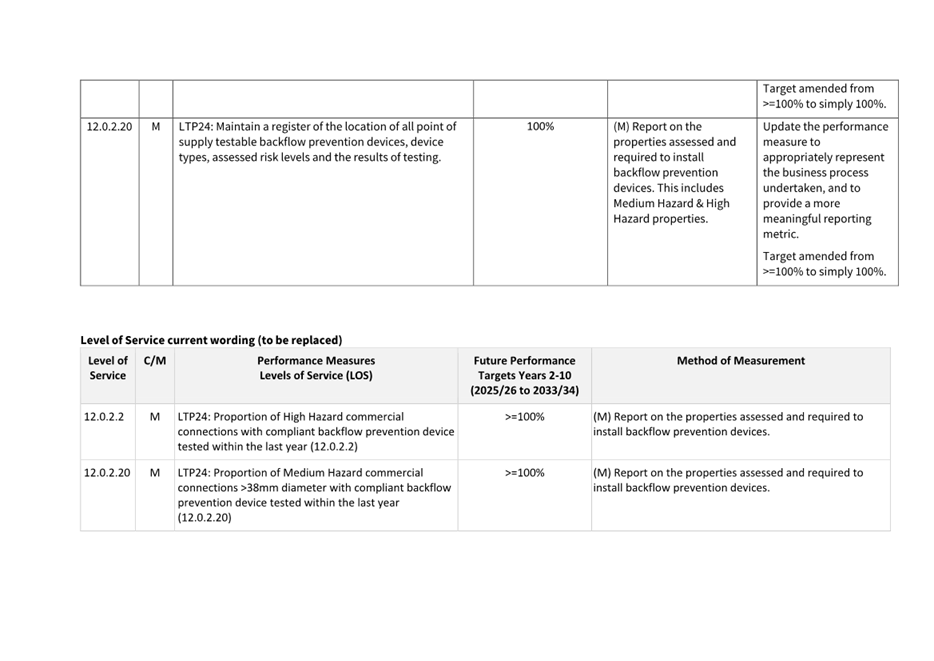

9.2.2 Water Supply (2): Measures of Success previously focussed on

installation of testable devices into high hazard and medium hazard properties.

Focus will now be on annual testing of the backflow prevention devices, and the

maintenance of a register to record the location of all

point of supply testable backflow prevention devices, device types,

assessed risk levels and the results of testing.

9.2.3 Digital

(2): to reflect a change in the method of survey for measuring internal

customer satisfaction, and discontinuation of a Measure

of Success monitoring internal business value perceptions.

9.3 The

minor changes are for administrative purposes and do not require consultation

with the community.

10. Changes to Revenue, Financing and Rating

Policies

10.1 There

are no policy changes proposed to the Revenue, Financing and Rating Policies as

part of the Draft Annual Plan.

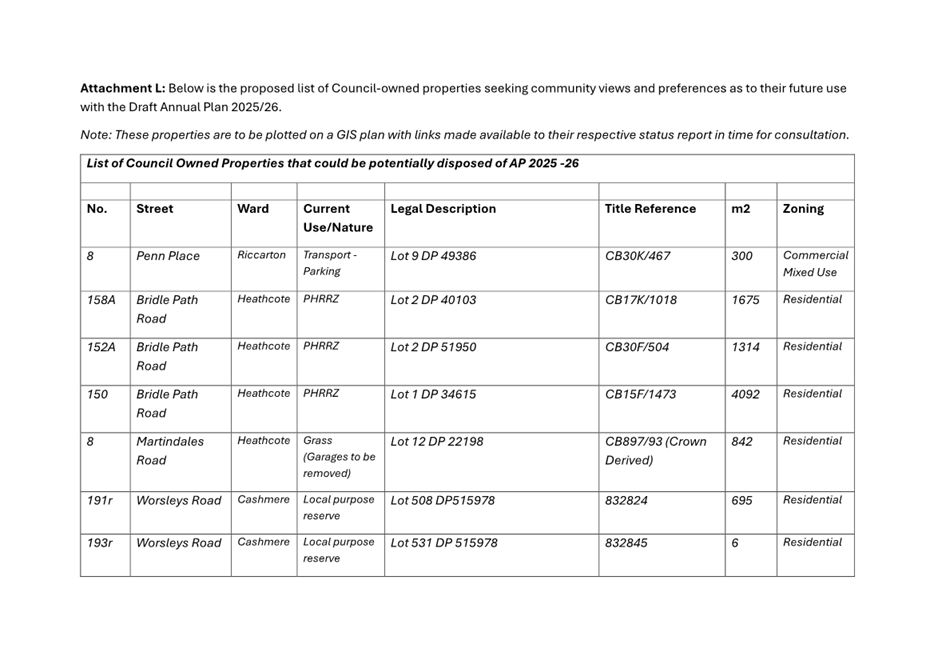

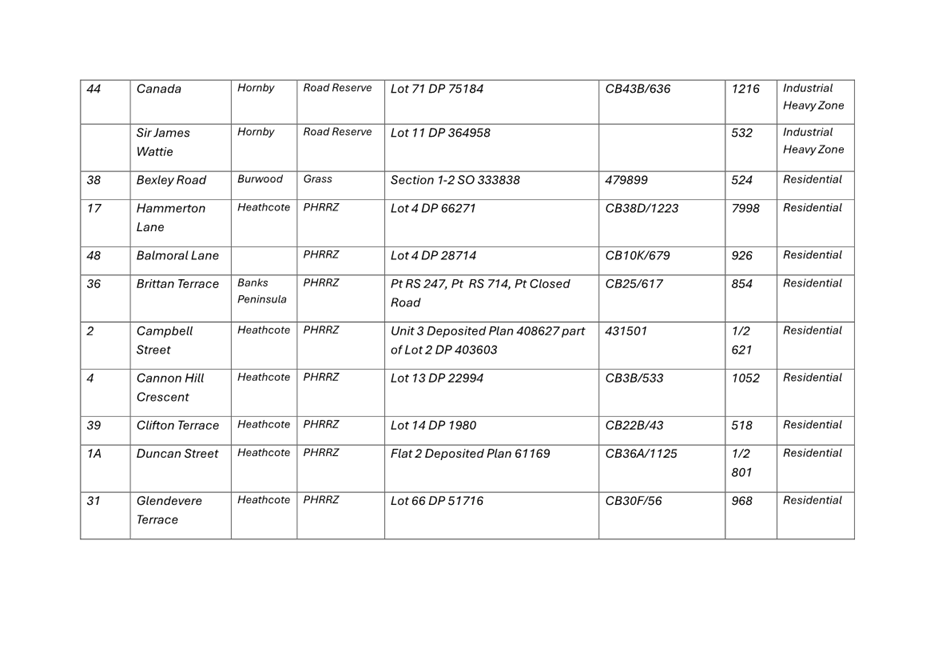

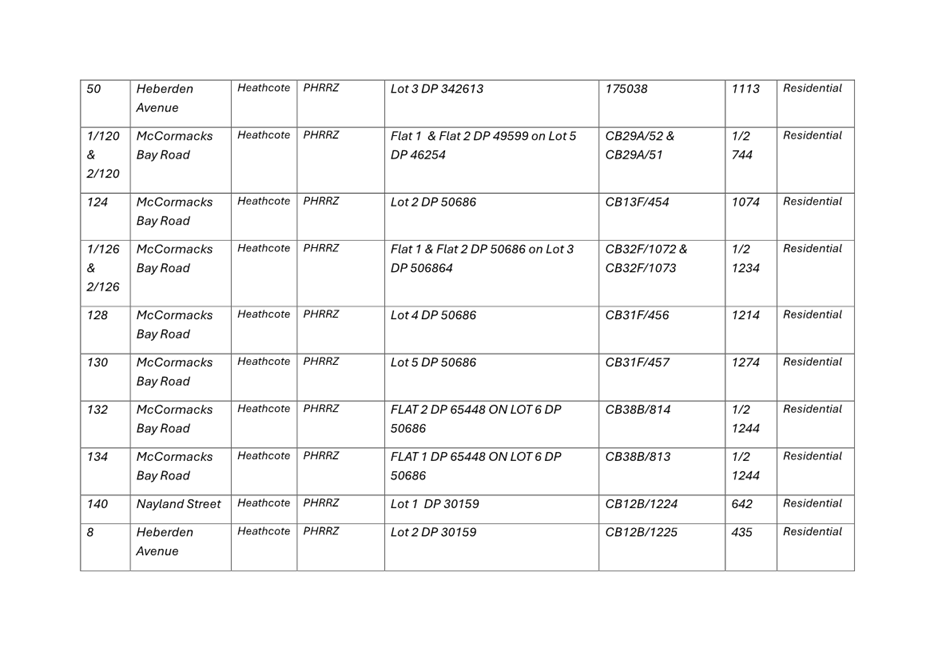

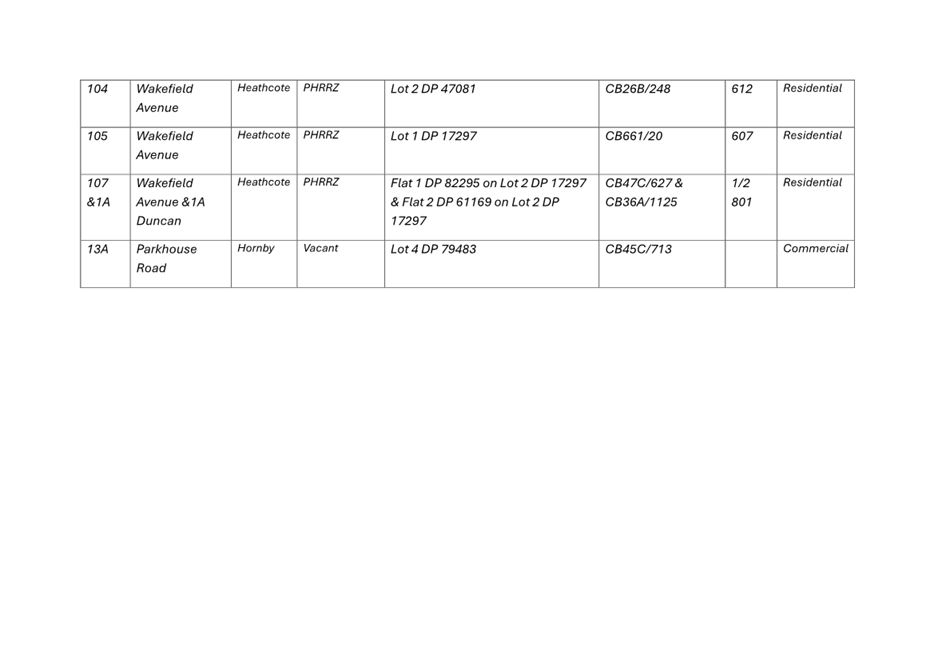

11. Potential Disposal of Council Owned Properties

11.1 The

Council owns many types of properties of varying configurations and sizes.

Owning property comes at a cost, and it is good financial practice to

frequently review the portfolio to ensure it remains fit for purpose. If a

property is no longer fit for purpose, then Council should decide whether to

keep it or release its value for community benefit.

11.2 Since

2021 the Council has when appropriate included in its draft LTPs and Annual

Plans a small portfolio of properties to be considered for disposal. The

properties have been put forward for consideration on the basis they were no

longer delivering the original activity or service for which they were

purchased.

11.3 It

is intended to replicate the process in this Annual Plan for a small number of

properties which have been identified as no longer used for the purpose for

which they were originally acquired. These have been assessed against and are

considered to meet the following criteria adopted by the Council at its meeting

of 10 December 2021:

11.3.1 Is the full

property still required for the purpose for which it was originally acquired?

11.3.2 Does the

property have special cultural, heritage or environmental values that can only

be protected through public ownership?

11.3.3 Is there an

immediate identified alternative public use / work / activity in a policy, plan

or strategy?

11.3.4 Are there any

strategic, non-service delivery needs that the property meets and that can only

be met through public ownership?

11.3.5 Are there any

identified unmet needs, which the Council might normally address, that the

property could be used to solve? And is there a reasonable pathway to funding

the unmet need?

11.4 A

list of those properties considered suitable to be put forward for

incorporation in this draft Annual Plan for consultation purposes can be seen

at Attachment M.

12. Funding of Asset Renewals (Rating for Renewals)

12.1 At its meeting on 10 December 2024 Council

resolved to consider increasing the amount rated for renewals as part of the

consultation for this draft Annual Plan.

12.2 The purpose of this resolution is to consider

how much of the renewals work is funded by rates, which has a direct impact on

the rates increase, and how much is funded by long-term debt, which spreads the

cost over many years. For completeness, one point to note, is that

increasing the rates collected for renewals does not increase the level of

renewals. The discussion on rating for renewals is essentially a funding

issue that addresses the proportion of the renewal work that is funded by either

rates or debt.

12.3 Council currently borrows some of the cost of its annual asset

renewal programme, approximately $125 million. Since

2015 Council has been on a trajectory to fully fund its renewals from rates by

2031. The rationale for fully funding renewals is that current ratepayers will

be meeting the full cost of renewing or replacing existing assets and are not

passing that cost on to future generations.

12.4 To reduce the rates increase in last year’s LTP, Council

reduced the level of rating for asset renewals in the first two years of the

LTP. That meant Council would now not reach its target of fully funding

renewals from rates until 2032, a year later than originally planned.

12.5 While extending the time frame for fully funding renewals from rates

has the effect of reducing rates in the current year, there are also longer

term effects. Any amount not rated for renewals is funded by borrowings.

Over the remaining period of the LTP net borrowings will increase by $93

million through to 2031, which results in an additional $19 million in interest

costs during that period. It also contributes to Council having an unbalanced

budget for the next four years when combined with the reduction in capital

revenues which were overstated in the LTP.

12.6 To reduce the unbalanced budget period to two years, additional

rating for renewals into proposed plans over the next three years (approx. $5,

10, 15 million inflated) has been budgeted. The recommended Draft Annual Plan

2025/26 includes the $5 million. This is forecast to enable a balanced budget

from 2027/28. If the increased rating for renewal is then flatlined to

2031 the additional borrowing is effectively eliminated. Additional interest

costs are reduced to approximately $6 million and are due to extending the

period to fully funding renewal from 2031 to 2032. While this causes slightly higher rates increases through to

2027/28, staff advice is that this is consistent with the financial

strategy.

12.7 In

the alternative, if Council is considering additional rating for renewals, $1

million of additional rating will reduce borrowing by $1 million and have the

following financial impact between 2026 and 2031:

|

Change in

Rates

|

|

$ Impact

over 2026 - 2031

|

|

$1 million

increase in each of the 6 years to 2031

Rates impact

0.13% in 2025/26

|

Interest

saved

Debt

repayment avoided

Overall rates

saving

|

0.81 million

0.5 million

1.31 million

|

|

$1 million

increase 2025/26 only

Rates impact

0.13% in 2025/26 reversed in 2026/27

|

Interest

saved

Debt

repayment avoided

Overall rates

saving

|

0.25 million

0.16 million

0.41 million

|

13. Considerations Ngā Whai Whakaaro

Risks and Mitigations Ngā Mōrearea me

ngā Whakamātautau

13.1 Key

risks for the deliverability of the finalised Annual Plan are as follows:

13.1.1 Significant

amendments or modifications of the Annual Plan at a late stage, preventing

timely advice on proposed amendments being provided and all reasonable options

being considered, and a risk that any significant changes will require an

amendment to the LTP.

13.1.2 Deliverability

of the capital programme.

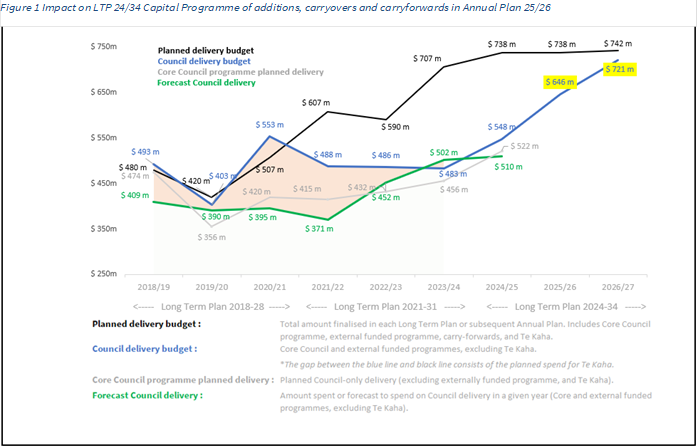

· The LTP process generated debate on the capital programme ‘bow

wave’ in local government and the deliverability of the core (non-Te

Kaha) capital programme. This was finalised in the LTP at a core capital

programme of $610 million for 2025/26.

· In the months

since the LTP was adopted, carry-forwards (capital works not done in 2023/24)

have been added ($36 million) and a variety of capital works have been

‘brought back’ from outer years. Actions carried over from

the LTP added $4.5 million, boosting the current 2025/26 Annual Plan proposal

by approximately $40 million.

· The graph

below shows the actual capital delivery trend line (in green) with delivery of

capital works at year end 2024/25 forecast to be $510 million, an historic

high.

· It also shows

the currently proposed Annual Plan core capital programme budget for 2025/26 at

$646 million (in blue).

· The Project

Management Office (PMO) forecasts also currently show a projected carry-forward

of potentially $20 million into 2025/26 (ie a further net increase in the

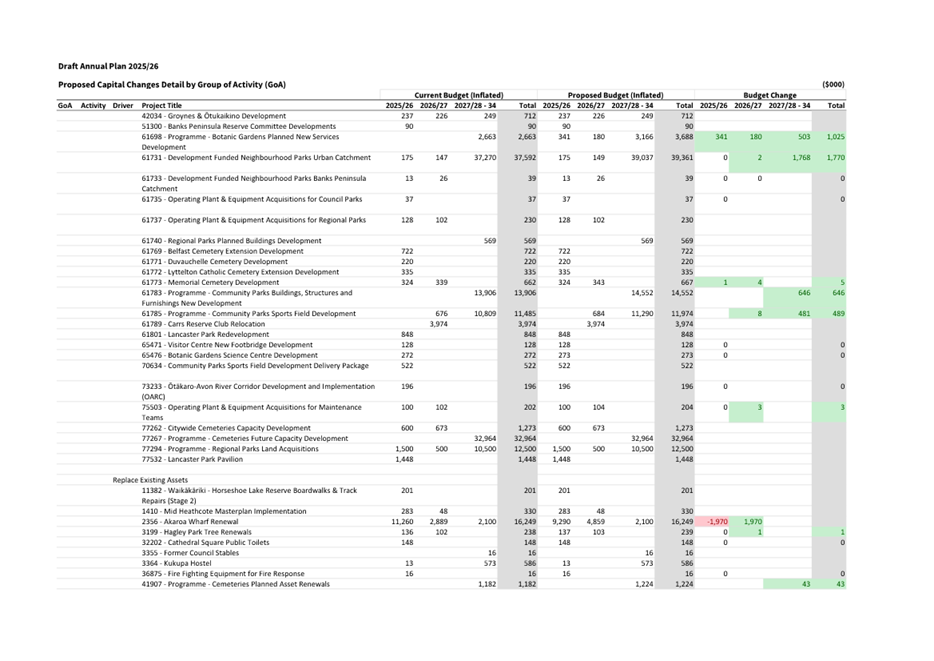

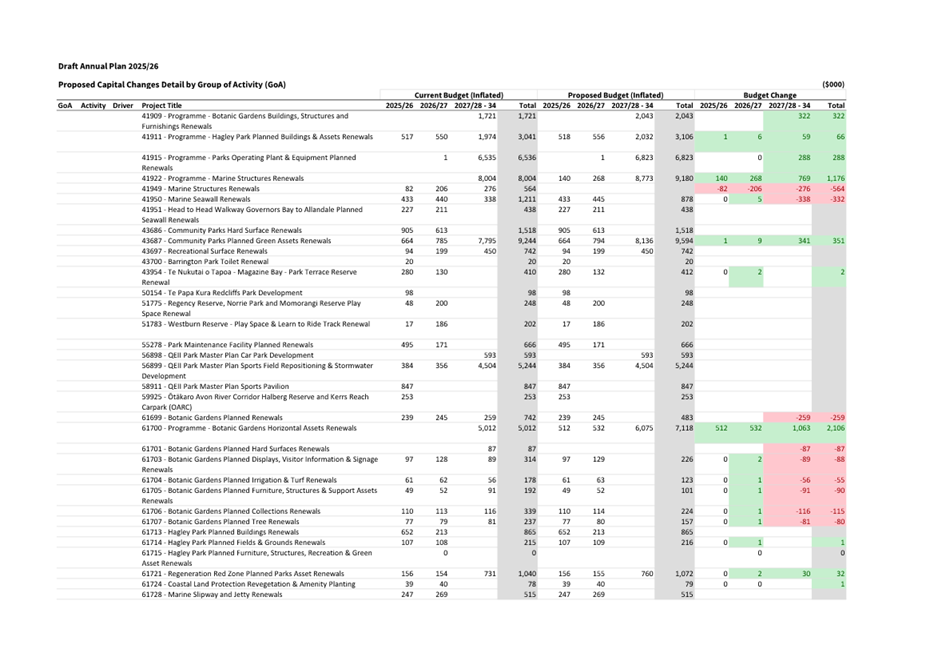

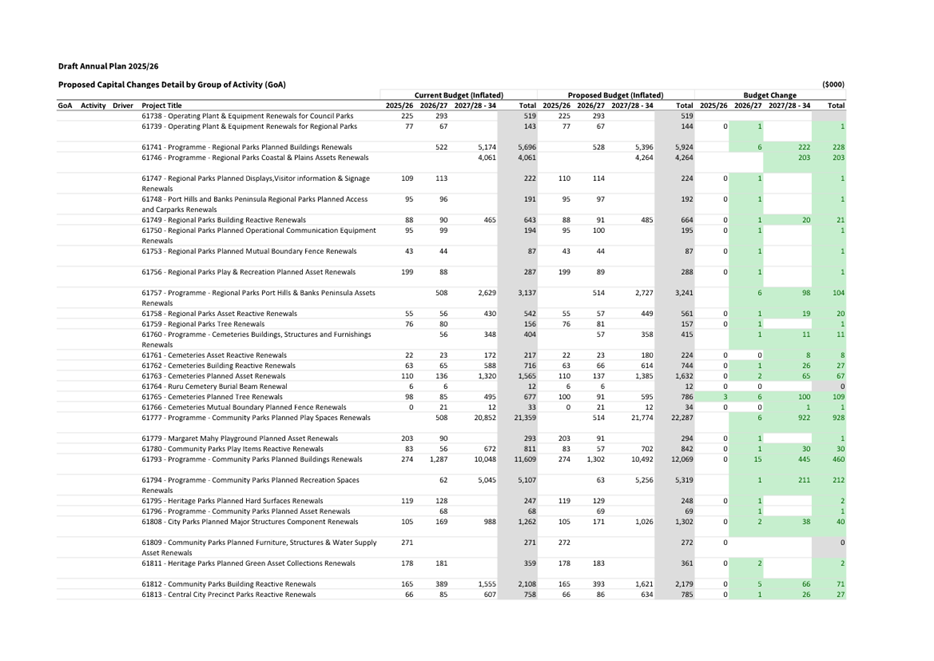

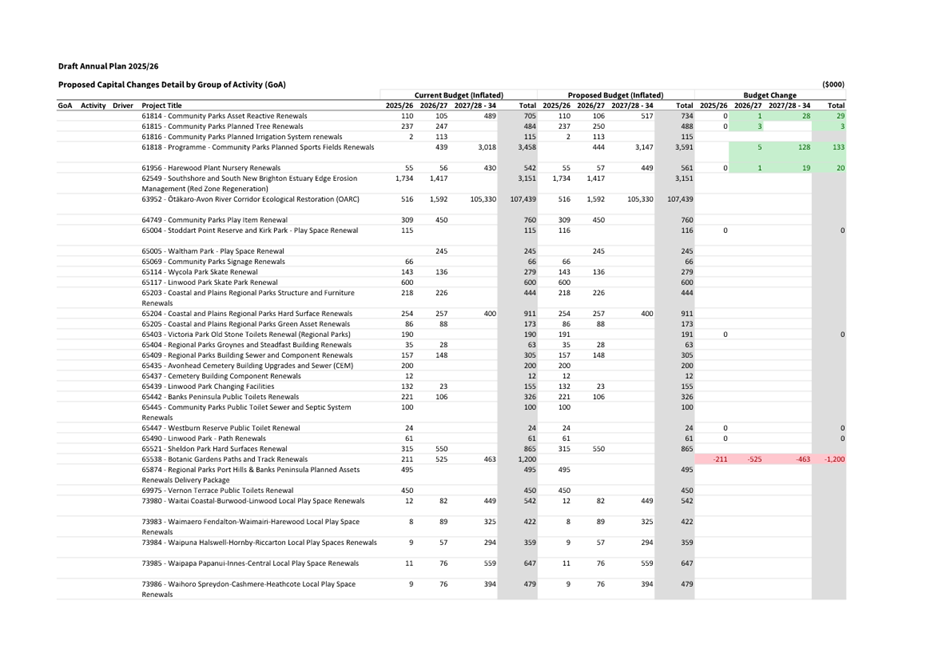

capital programme of approximately $20 million).

·

The assumption that delivery can lift by at least $136 million

over the course of a single year carries risk, especially if further capital

works are added via the Annual Plan.

13.2 The

Project Management Office (PMO) is currently leading a body of work on capital

programme deliverability. This is in response to questions from the Finance

& Performance Committee on the issue of deliverability of the capital

programme. The purpose of the work is to provide clear evidence on

deliverability for Council.

13.3 The

above risks have been identified by the Project Team and are being managed

through the general checklists and sign-offs by management, including

significant forecasting assumptions, reviewed by the Audit and Risk Management

Committee.

Legal Considerations Ngā Hīraunga

ā-Ture

13.4 Statutory

and/or delegated authority to undertake proposals in the report:

13.4.1 The Council must, at all times, have an LTP / Annual Plan in place

(sections 93 and 95 of the LGA). The Annual Plan is required to be

adopted prior to the year to which it relates (section 95(3) of the LGA).

13.5 Other Legal Implications:

13.5.1 The Council has

a legal duty to ensure that each years projected operating expenses are set to

achieve a balanced budget (section 100(1) of the Local Government Act 2002

(LGA)). Council can approve an unbalanced budget (in final Annual Plan adoption

of June 2025) provided it resolves that it is financially prudent to do so,

having regard to the relevant criteria set out in section 100(2) of the

LGA.

13.5.2 As the current

Christ Church Cathedral Targeted Rate (Targeted Rate) has been signalled in the

funding impact statement and collected for a specific purpose ceasing to levy

for the Targeted Rate is a valid approach subject to the appropriate

consultation with the community.

13.5.3 There is

no additional legal context, issue or implication relevant to this decision.

Strategy

and Policy Considerations Te

Whai Kaupapa here

13.6 The

required decision aligns with the Strategic Framework adopted with the

Long-Term Plan 2024-34.

13.7 This

report supports the Council's Long Term Plan (2024 -

2034):

13.8 Internal Activities

13.8.1 Activity: Performance, Finance, and Procurement

· Level of Service: 13.1.1 Implement the Long-Term Plan and

Annual Plan programme plan - Critical path milestone due dates in programme

plans are met

Community

Impacts and Views Ngā Mariu ā-Hāpori

13.9 This

decision affects all residents and ratepayers of Christchurch, and has

implications for current and future residents, ratepayers.

13.10 The

decision affects all wards/Community Board areas. Pre-engagement with the

Annual Plan process has occurred across all Community Boards.

13.11 Consultation

on the Draft Annual Plan will commence on 26 February 2025.

Impact

on Mana Whenua Ngā

Whai Take Mana Whenua

13.12 The LTP

2024–34 saw consultation and engagement with Ngā Papatipu

Rūnanga, which resulted in a wide range of initiatives being undertaken in

the LTP. Those undertakings remain intact and are not proposed to be affected

by the Annual Plan.

13.13 The

decision will not impact on Council’s agreed partnership priorities with Ngā Papatipu Rūnanga.

Climate

Change Impact Considerations Ngā Whai Whakaaro mā te Āhuarangi

13.14 The

decisions in this report do not affect climate impact considerations made as

part of the Long Term Plan 2024-34.

13.14.1 Climate change

and environmental initiatives were proposed and consulted on as part of

developing the LTP 2024-34. Responding to feedback from submitters Council

decided on several initiatives which are all being implemented.

13.14.2 Those

undertakings remain intact and are not proposed to be affected by the Annual

Plan.

14. Next Steps Ngā Mahinga ā-muri

14.1 After

the draft adoption, consultation with the community will commence, on the basis

of the Consultation Document (Attachment N), beginning on 26 February

2025 and running until 11:59 pm on 28 March 2025.

14.2 At

the completion of consultation, hearings will follow and are planned to be held

in April 2025.

14.3 Following

the Hearings, the results of the consultation feedback and hearings will be

collated to inform Council Information Sessions/Workshops in May/June 2025.

14.4 Adjustments

and changes resulting from consultation, hearings and workshops will be

incorporated into the Annual Plan to be presented to Council for its adoptions,

which is proposed to be at a meeting of the Christchurch City Council on 26

June 2025.

14.5 If

there are delays, for any reason, to the timetable this is likely to put at

significant risk the Annual Plan’s adoption before the end of June.

The effect of this is to prevent striking the proposed rates for the 2025/26

financial year. This would result in a significant revenue gap, loss of

revenue and risks reputational damage until the new Annual Plan can be adopted.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a

|

Audit and Risk

Management Committee Recommendations - 10 February 2025 (Under Separate

Cover)

|

|

|

|

b ⇩

|

Financial

Overview, including financial changes to that contained in the Long-Term Plan

2024-2034

|

24/1355975

|

21

|

|

c ⇩

|

Funding Impact

Statement

|

24/1355999

|

32

|

|

d ⇩

|

Rating

Information

|

25/31519

|

36

|

|

e ⇩

|

Financial

Prudence Benchmarks

|

24/1365417

|

53

|

|

f ⇩

|

Proposed

Capital Programme, including changes

|

25/181876

|

55

|

|

g ⇩

|

Proposed Minor

Changes to Levels of Service

|

24/2320443

|

96

|

|

h ⇩

|

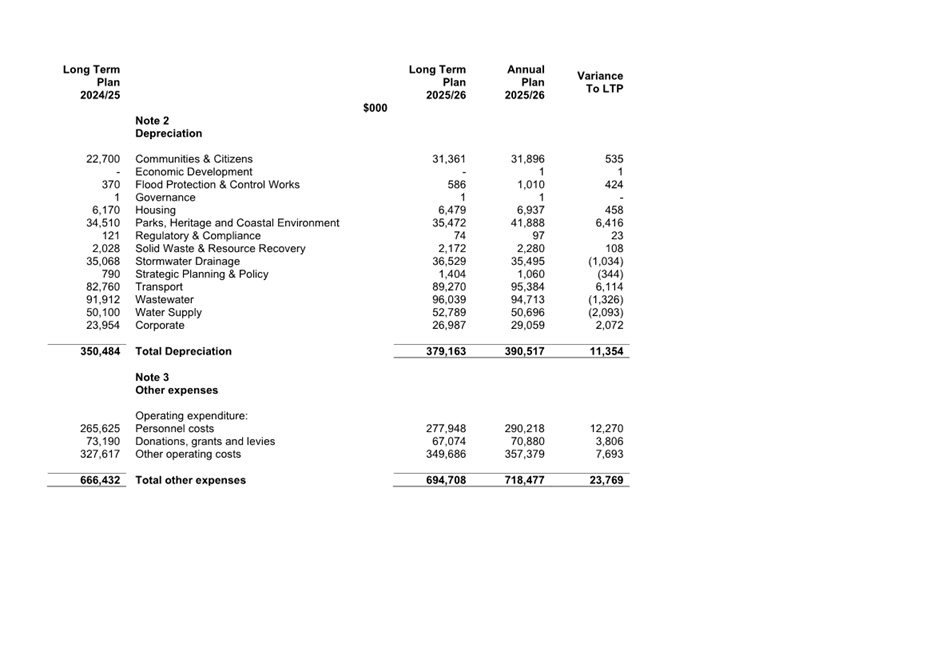

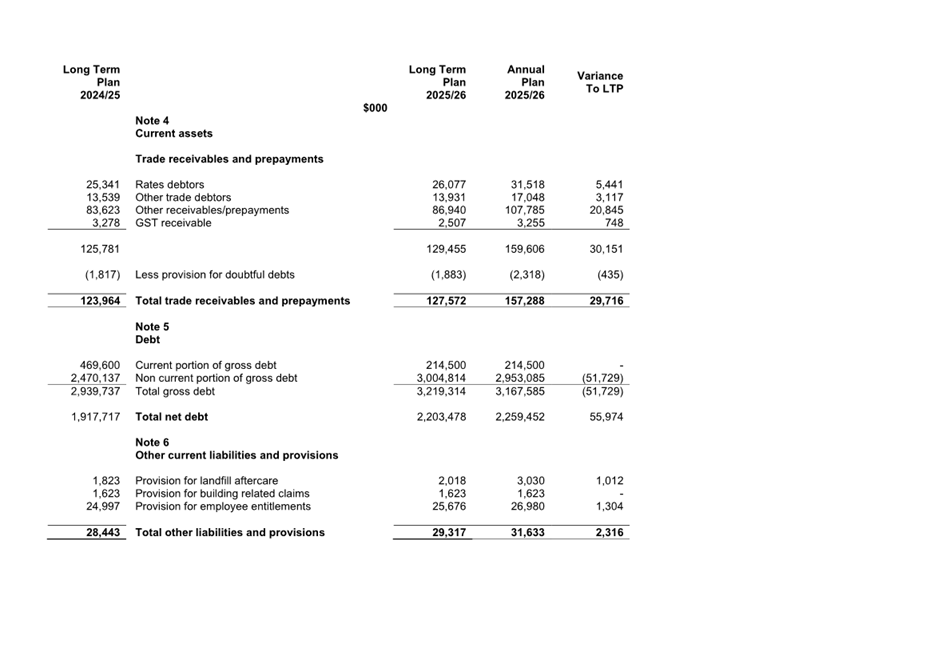

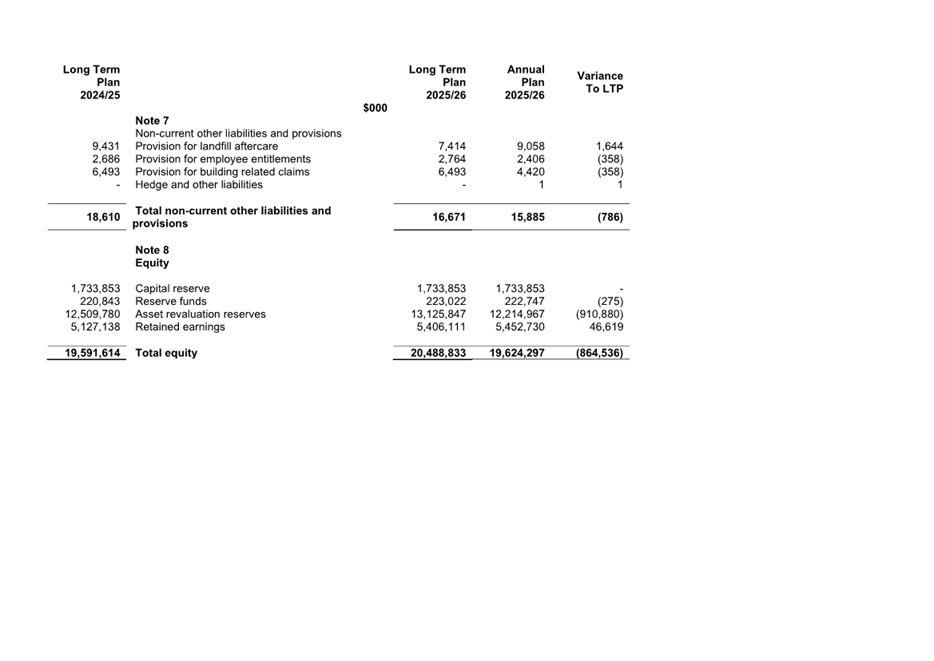

Prospective

Financial Statements incl Accounting Policies and Significant Assumptions

|

25/177999

|

103

|

|

i ⇩

|

Proposed Fees

and Charges, including changes

|

25/128877

|

142

|

|

j ⇩

|

Reserves and

Trust Funds

|

24/1365598

|

211

|

|

k ⇩

|

Capital Endowment

Fund

|

24/1365679

|

214

|

|

l ⇩

|

Grants Summary

|

24/1365736

|

215

|

|

m ⇩

|

List of

properties for consultation seeking the community views and preferences as to

their future use

|

25/95038

|

217

|

|

n

|

Draft AP

2025/26 Consultation Document (Under Separate Cover)

|

|

|

|

o ⇩

|

Rates Increase

Breakdown for Draft Annual Plan 2025/26

|

25/83705

|

222

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Tim Ward -

Senior Corporate Planning & Performance Analyst

Bruce Moher -

Manager Corporate Reporting

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Russell Holden

- Head of Finance

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

Mary

Richardson - Chief Executive

|