|

3. Long-Term

Plan 2024-34

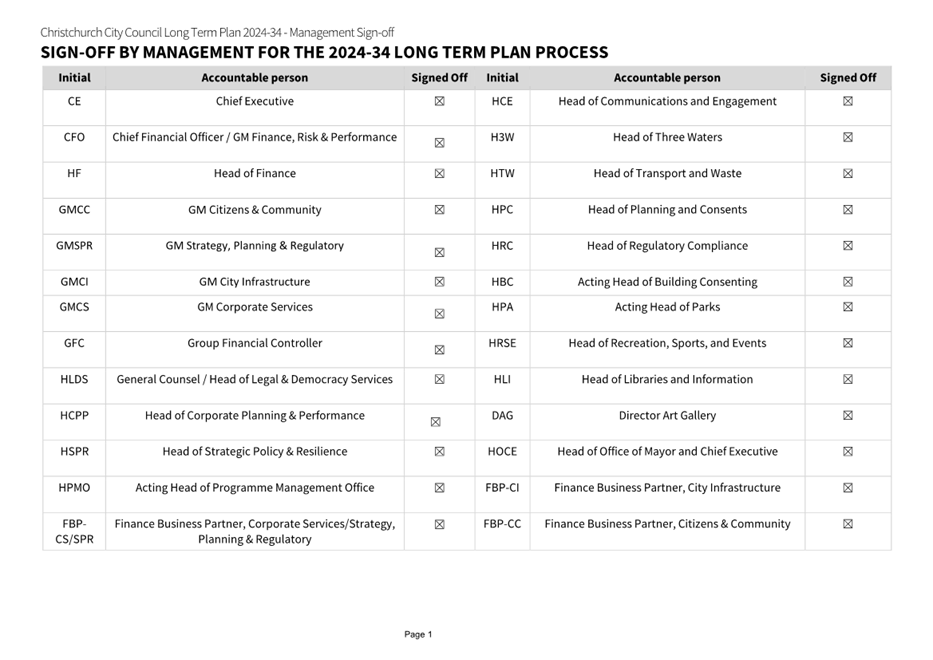

|

|

Reference Te Tohutoro:

|

24/488543

|

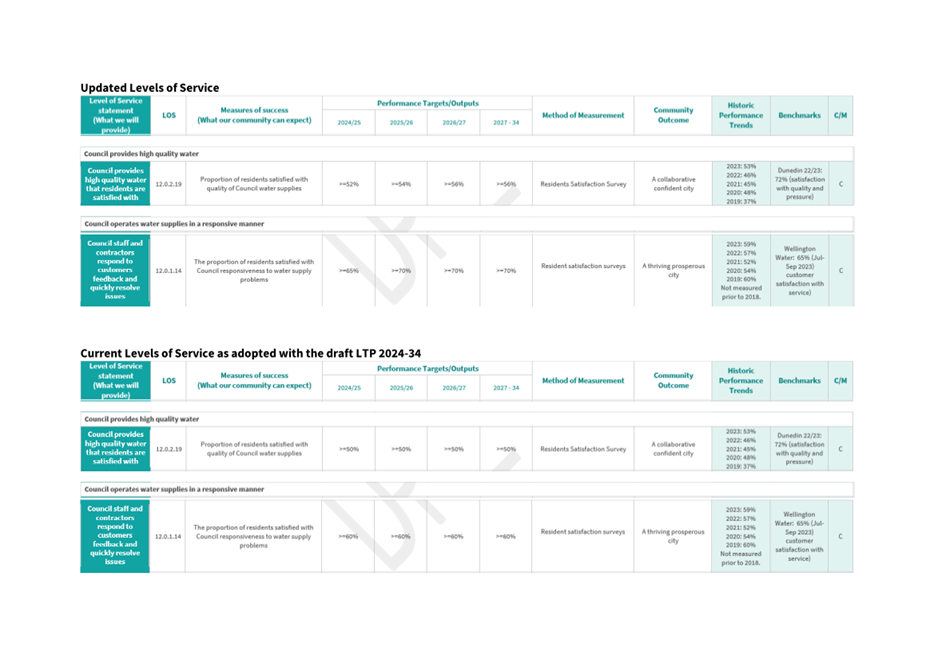

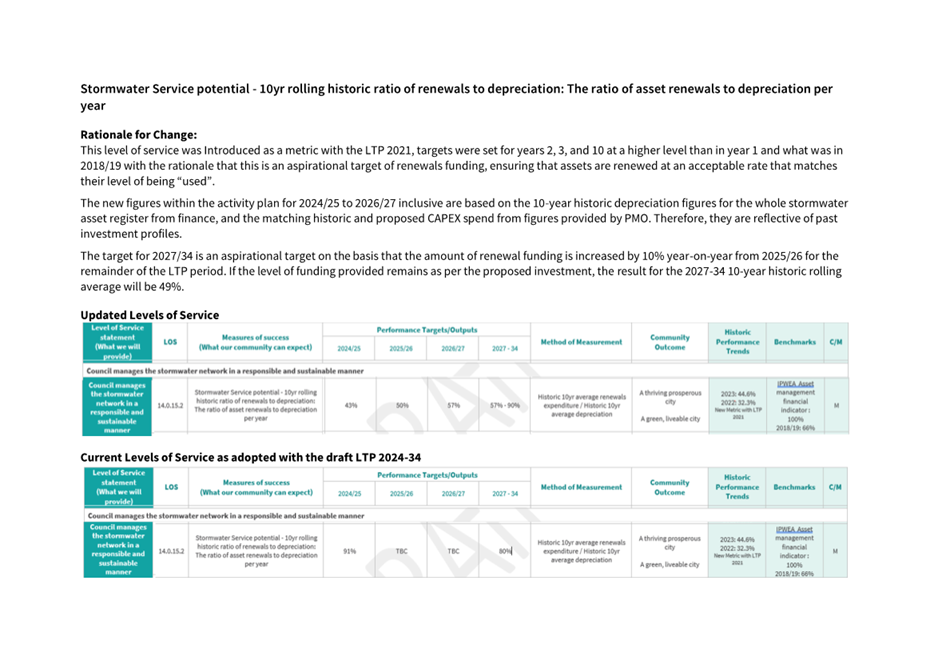

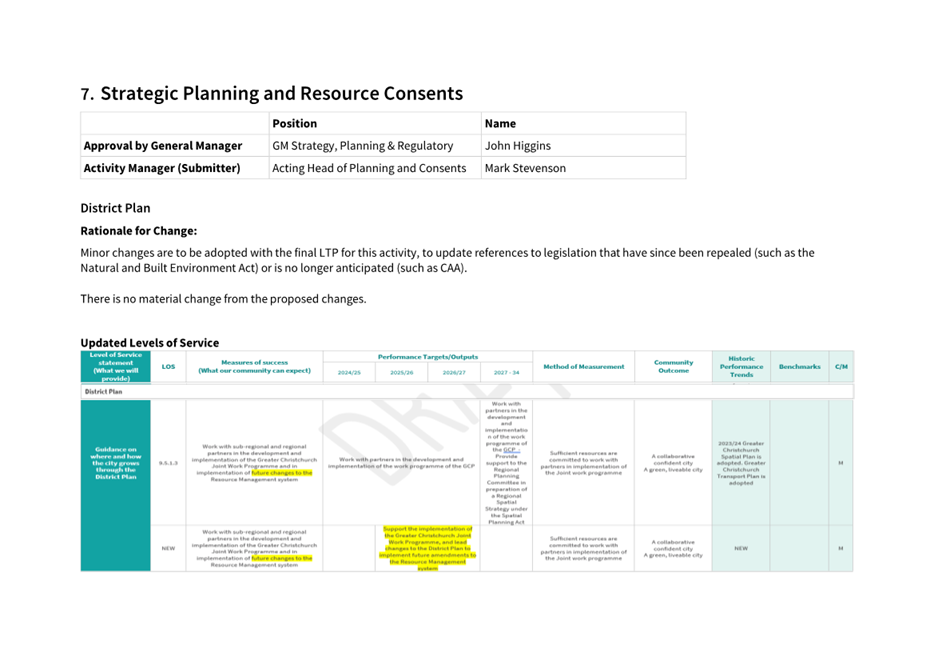

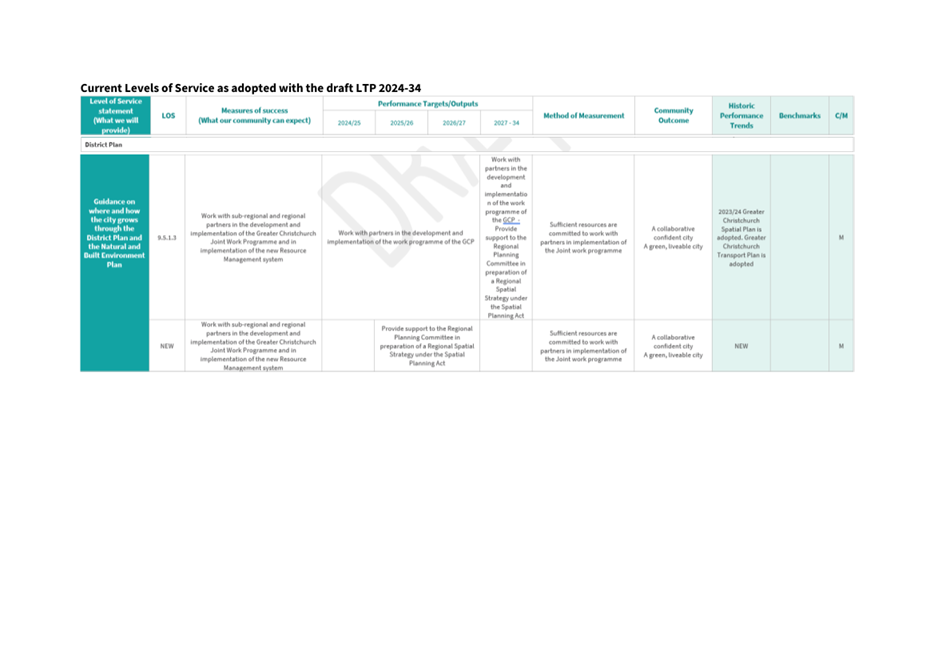

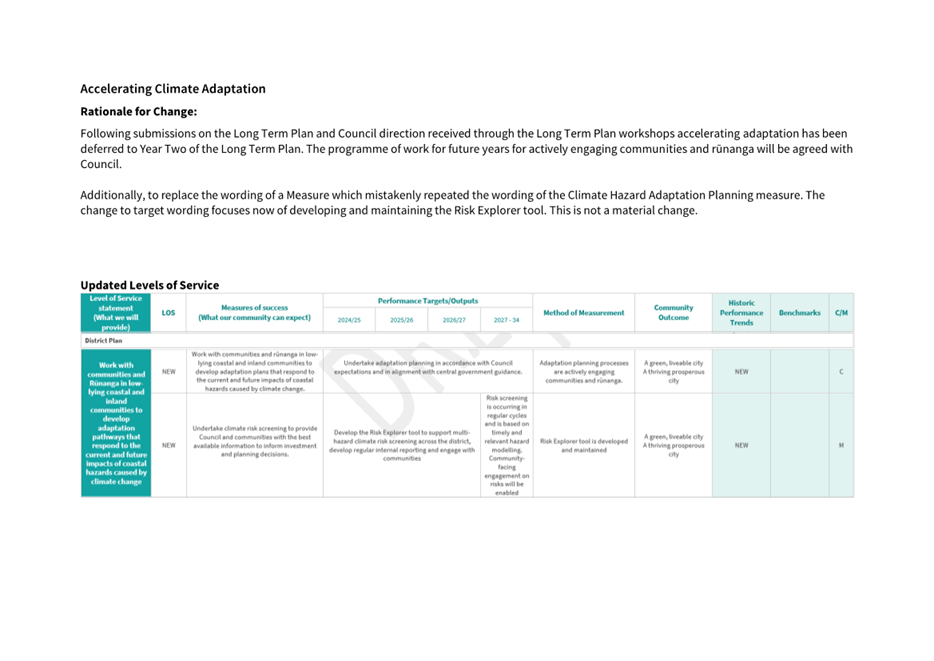

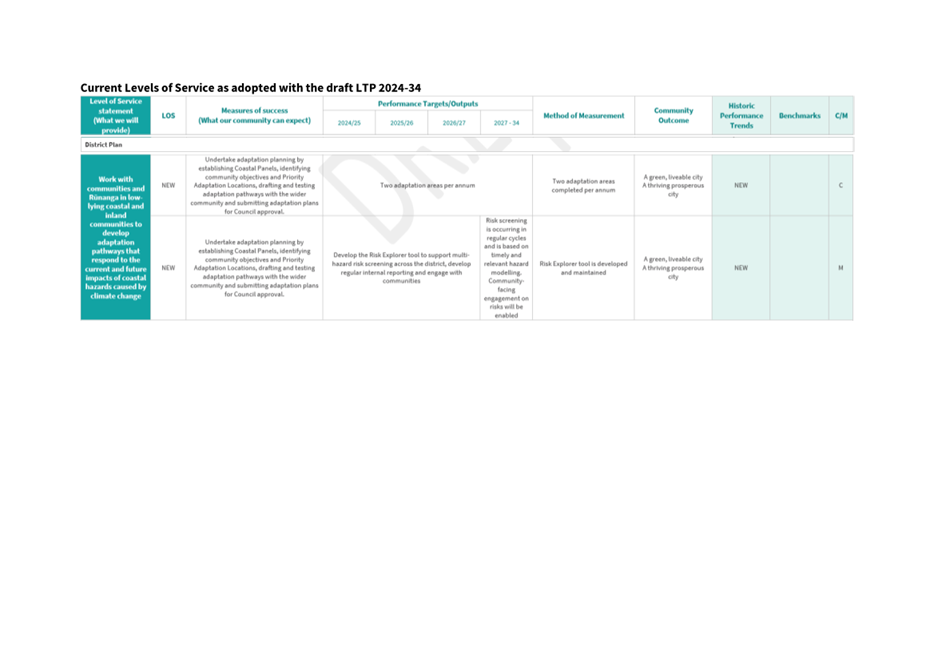

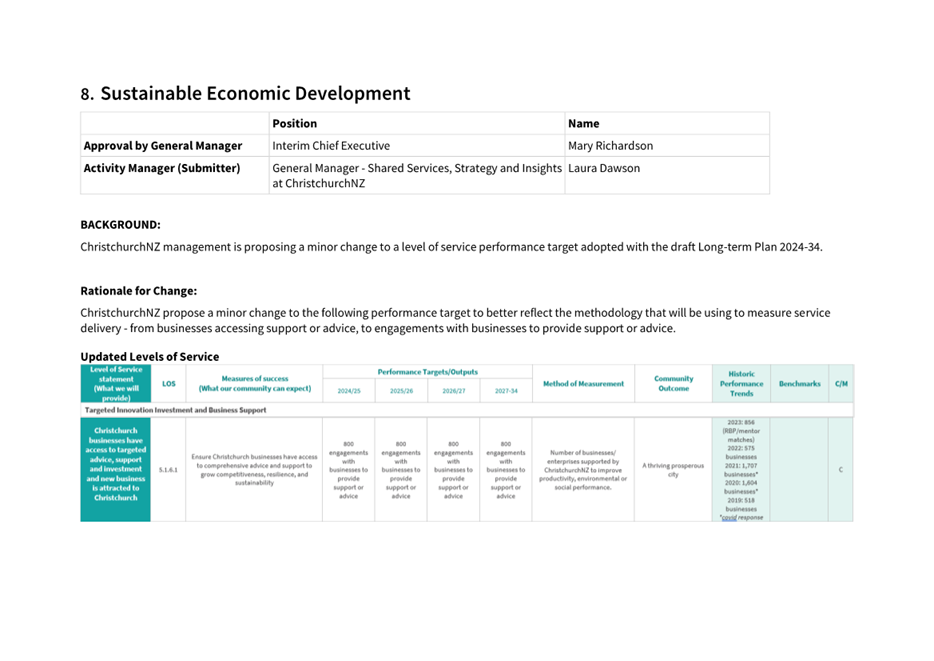

|

Responsible Officer(s) Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance

|

|

Accountable ELT Member Pouwhakarae:

|

Bede

Carran, General Manager Finance, Risk & Performance / Chief Financial

Officer

|

1. Purpose and Origin of the Report Te Pūtake Pūrongo

1.1 The

purpose of this report is to present to the Council:

1.1.1 An

analysis of the submissions made through the 2024-34 Long-Term Plan (LTP

2024-34) consultation process;

1.1.2 The

outcome of the Council’s considerations to date;

1.1.3 Officer

Recommendations for consideration before the Council adopts the LTP 2024-34;

and

1.1.4 Propose

rates to be set for the 2024-25 financial year.

1.2 This

will ensure Council meets its obligations under the Local Government Act (LGA

2002), which requires local authorities to adopt a Long-Term Plan every three

years.

2. Officer Recommendations Ngā

Tūtohu

That the Council:

1. Receives the information in the Long-Term Plan 2024-34 report and the attached documents.

2. Notes that the decision in this report is

assessed as high significance based on the Christchurch City Council’s Significance and

Engagement Policy.

3. Notes the Recommendations of the

Council’s Audit and Risk Management Committee at its meeting on 20 June

2024 (Attachment A – to be provided under separate cover)

4. Receives the Audit report (Attachment B

– to be provided under separate cover) required by s.94(1) of the LGA

2002.

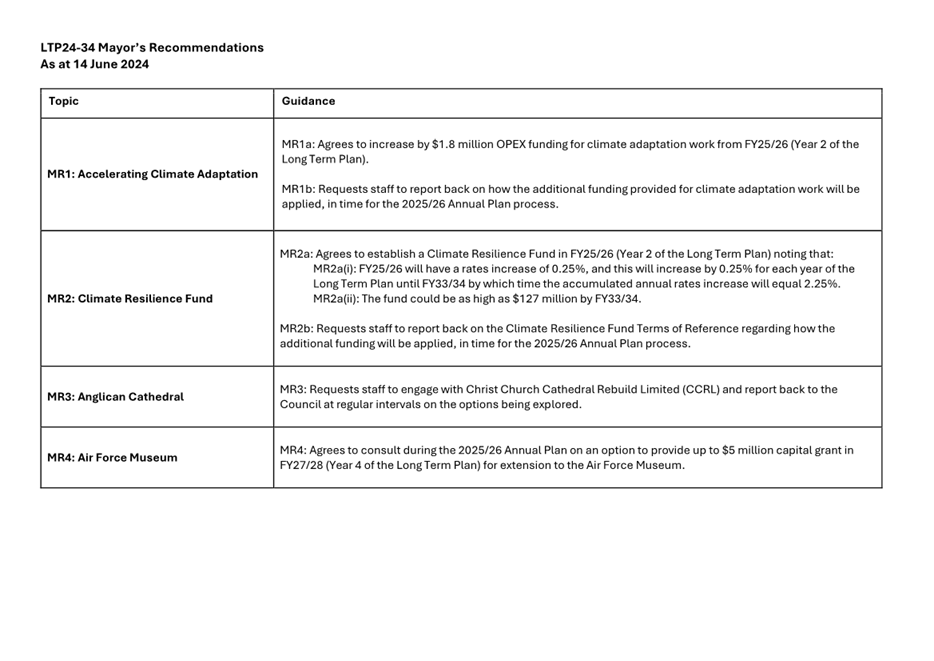

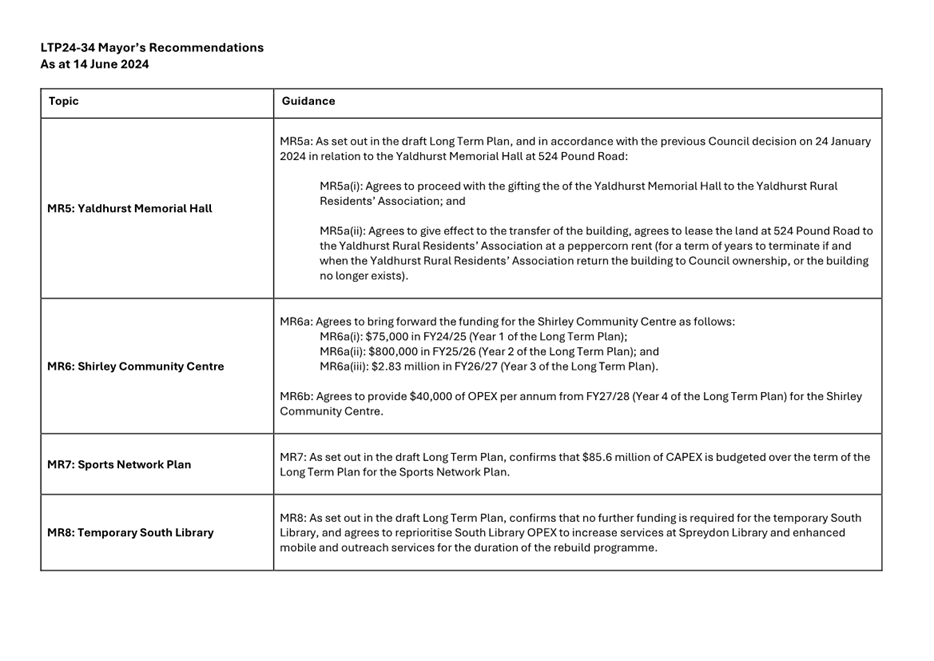

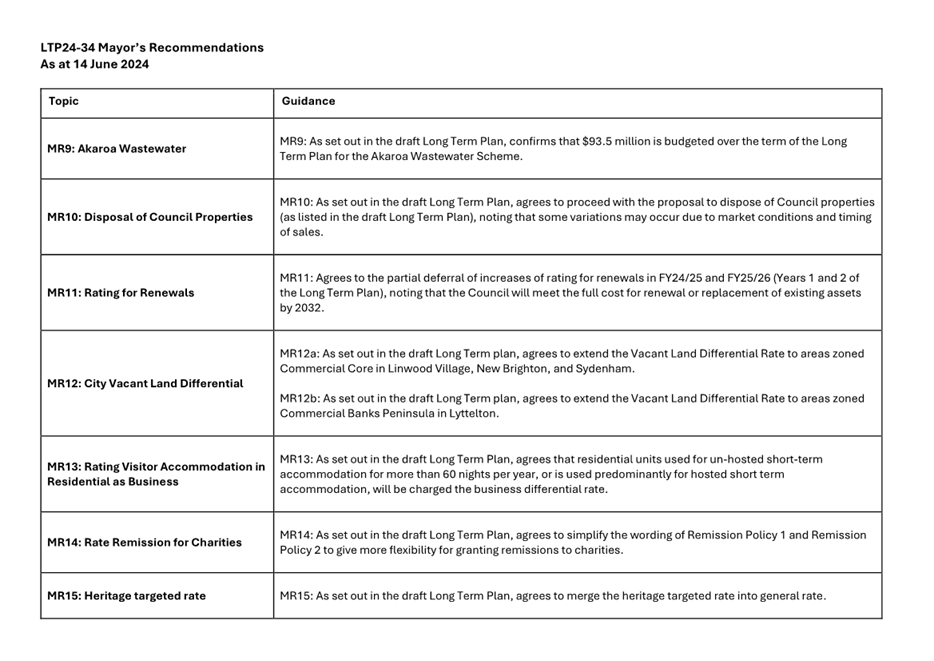

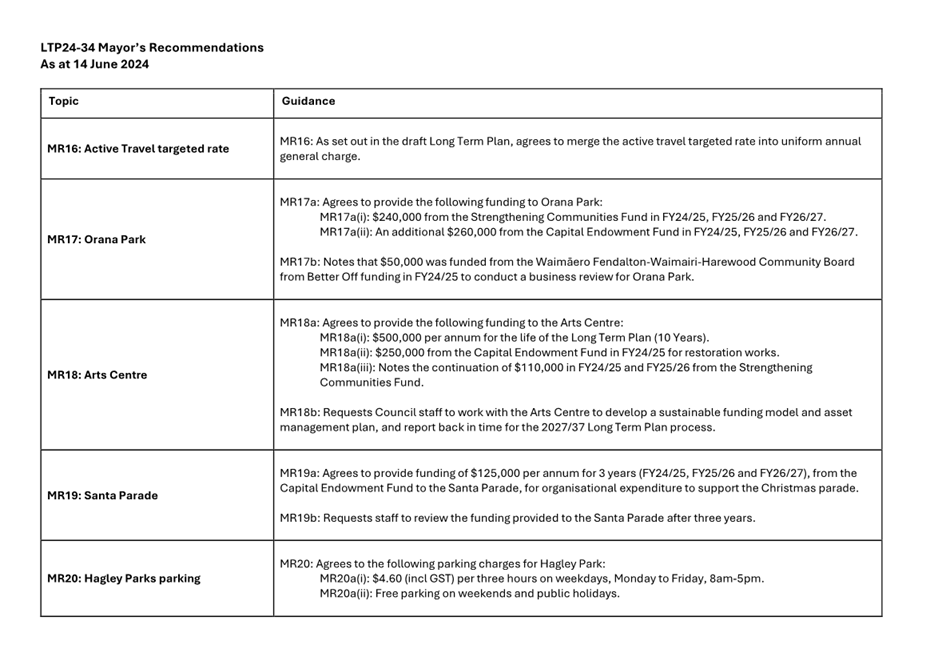

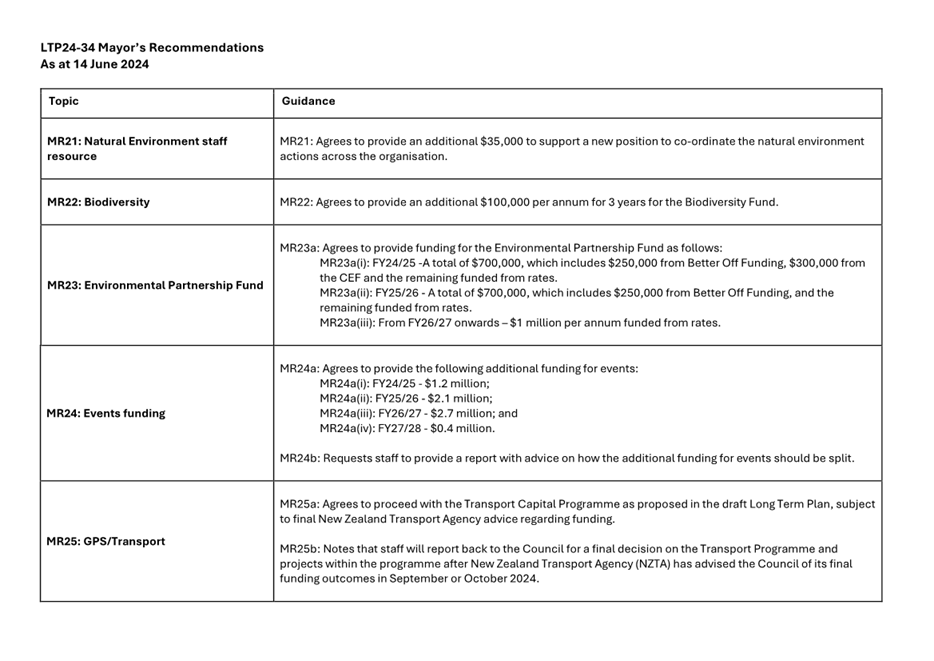

5. Notes the Mayor’s Recommendations and

that these are incorporated into the Funding Impact Statement Attachment C.

6. Adopts the proposed changes to the

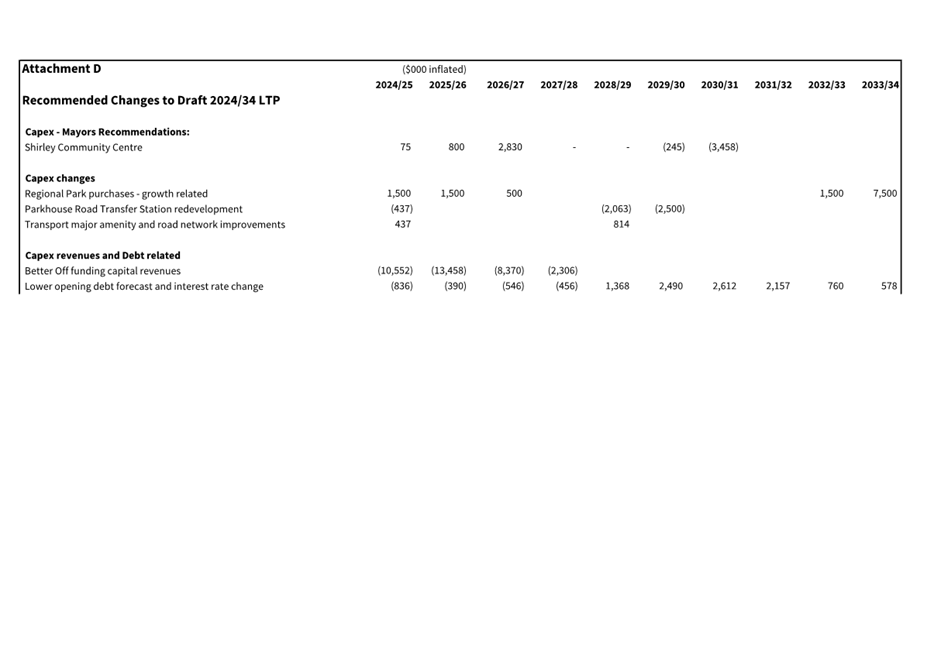

Council’s capital programme set out in Attachment D.

7. Adopts the proposed changes to the

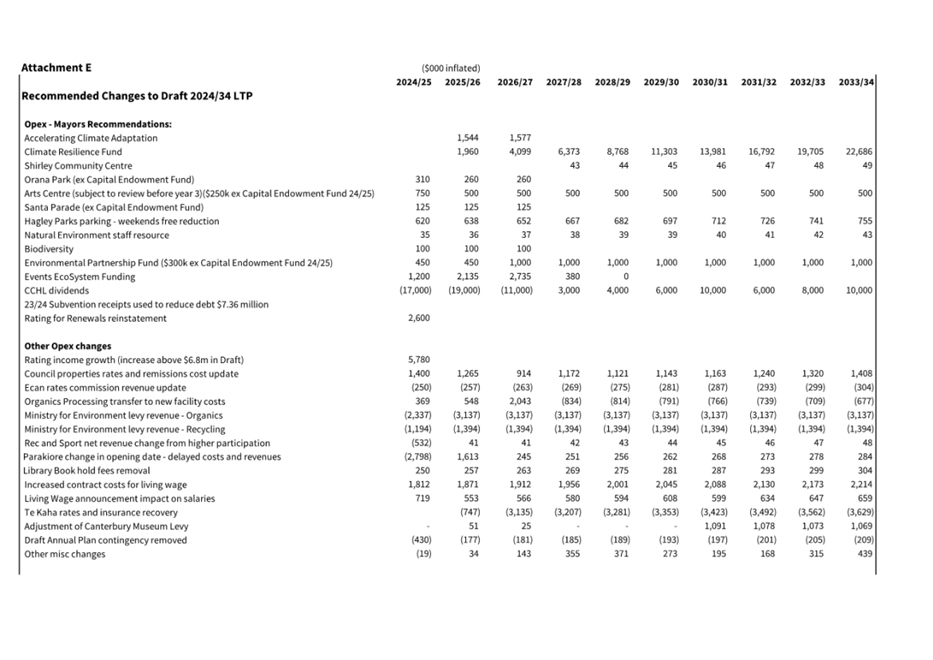

Council’s operating expenditure set out in Attachment E.

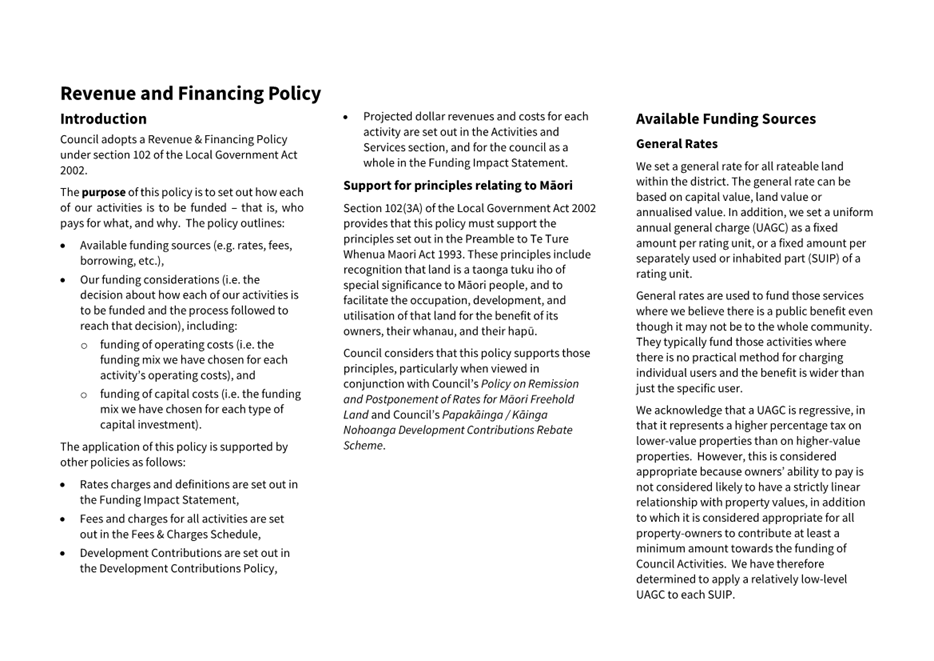

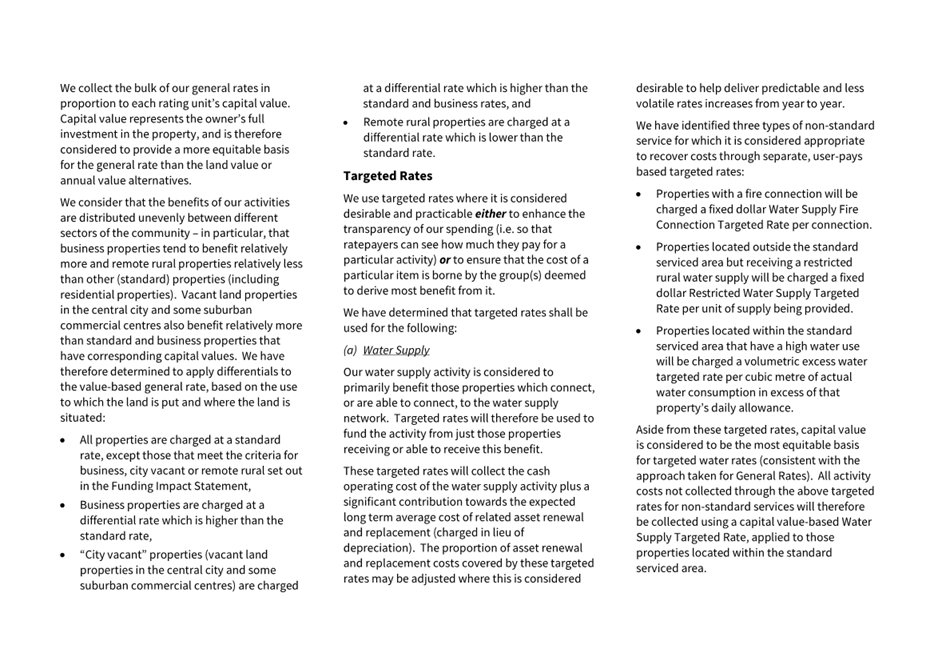

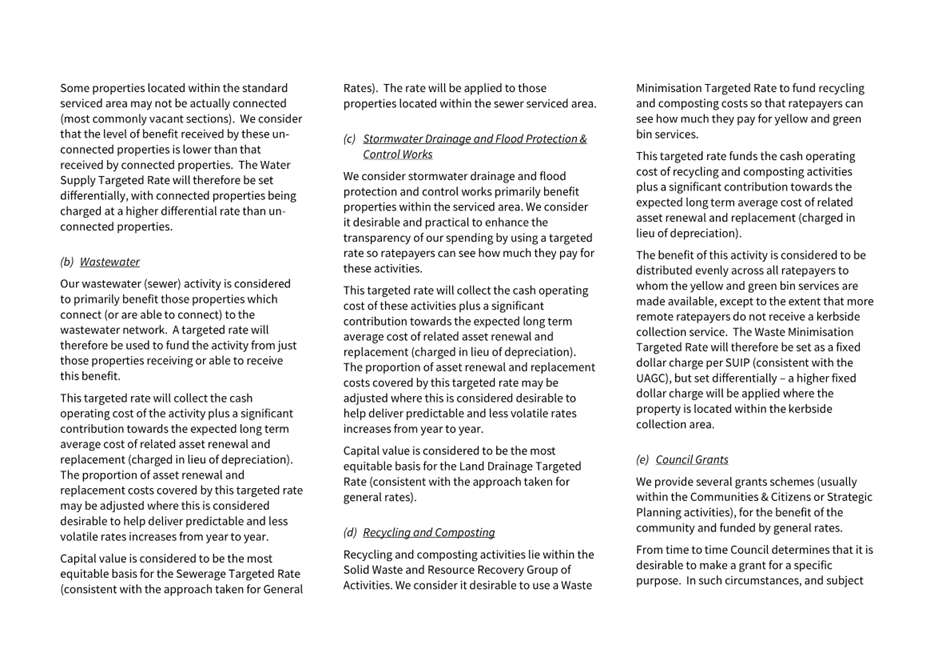

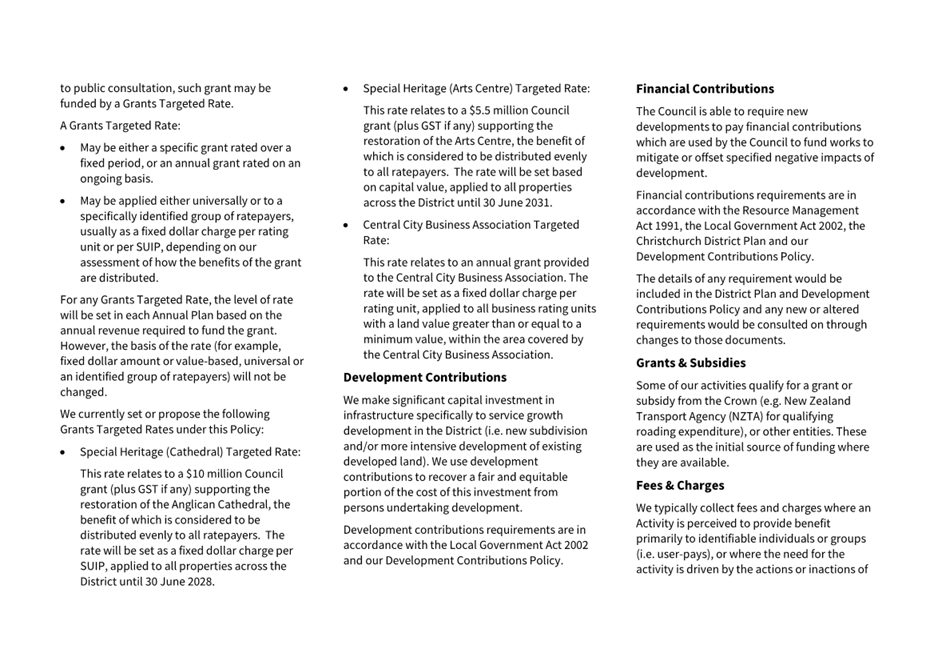

8. Adopts the Revenue and Financing Policy set

out in Attachment F.

9. Adopts the Rates Remission Policy set out in Attachment

G.

10. Adopts the Funding Impact Statement, Financial

Strategy and Infrastructure Strategy set out in Attachments H, I, and J.

11. Adopts minor changes and corrections to levels

of service and fees and charges identified since the publication of the draft

LTP 2024-34, set out in Attachment K.

12. Adopts the supporting information underpinning

the attachments above, including Activity and Asset Plans found at:

https://ccc.govt.nz/the-council/plans-strategies-policies-and-bylaws/plans/long-term-plan-and-annual-plans/long-term-plan-2024-to-2034/draft-activity-and-draft-asset-management-plans/

13. In regards to the Capital Endowment Fund:

a. Resolves to not inflation protect the Capital

Endowment Fund; and

b. Requests this to be reviewed before the next

Long Term Plan 2027-37 (requires 80% majority).

14. Agrees that in accordance with section 100 of

the Local Government Act 2002, it is financially prudent not to set the

Council’s operating revenues at a level sufficient to meet the projected

operating expenses in the financial year 2026-27. Note: the ratio is

forecast to be 99.6% in that year.

15. Notes that the Debt Servicing Financial

Prudence benchmark is breached in all years of the Long Term Plan 2024-34, but there is no concern around Council’s

ability to service the debt.

16. Agrees to continue to provide debt funding to

Christchurch City Holdings Ltd (CCHL) from time to time during the term of the

Long Term Plan 2024-34, and to borrow from the Local Government Funding Agency

(LGFA) for that purpose (back-to-back funding), provided that:

a. CCHL

remains within its existing borrowing covenants.

b. The

borrowing and on-lending is in accordance with the Council’s Liability

Management Policy.

c. Staff

continue to report the amount of such lending in the quarterly corporate

finance report to the Finance and Performance Committee.

17. Adopts the Long Term Plan 2024-34 comprising

the information and underlying documents adopted by the Council at its meeting

dated 14 February 2024 (concluded 14 March 2024), as amended by Resolutions

5-13 above and including the Audit report referred to in Resolution 4.

18. Authorises the Chief Financial Officer to make

the amendments required to ensure the published Long Term Plan 2024-34 aligns

with the Council’s Resolutions of 25 June 2024 and the Audit report, and

to make any other non-material changes that may be required.

19. Authorises the Chief Executive to borrow, in

accordance with the Liability Management Policy, sufficient funds to enable the

Council to meet its funding requirements as set out in the Long Term Plan

2024-34.

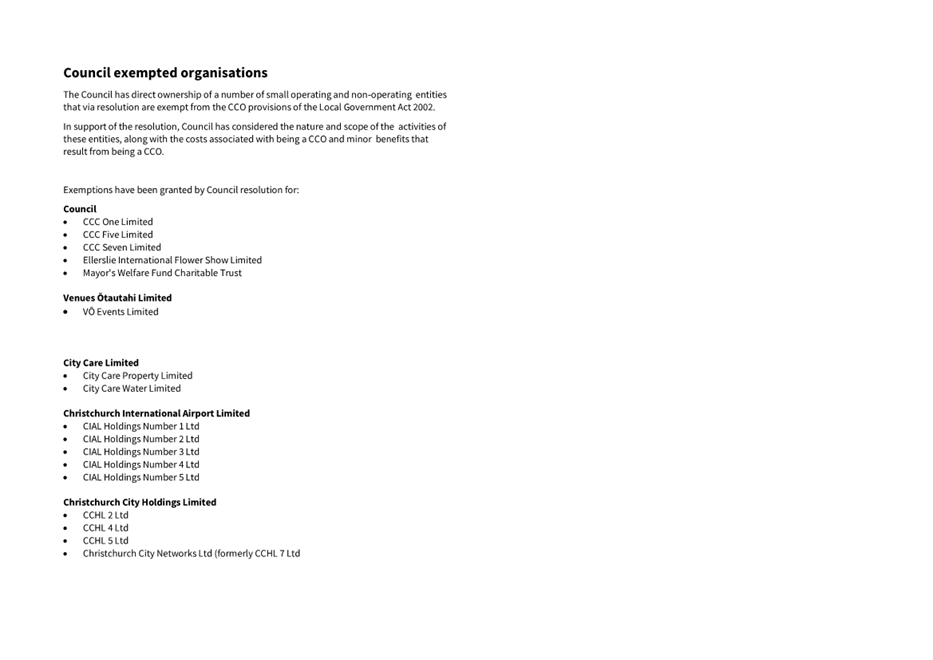

20. Grants an exemption under s.7 of the Local

Government Act 2002 in respect of the Council-Controlled Organisations referred

to in Attachment P.

21. Having set out rates information in the

Funding Impact Statement contained in the Long Term Plan 2024-34, (adopted as Attachment

H by the above Resolutions), resolves to set the following rates under the

Local Government (Rating) Act 2002 for the 2024-25 financial year, commencing

on 1 July 2024 and ending on 30 June 2025 (all statutory references are to the

Local Government (Rating) Act 2002):

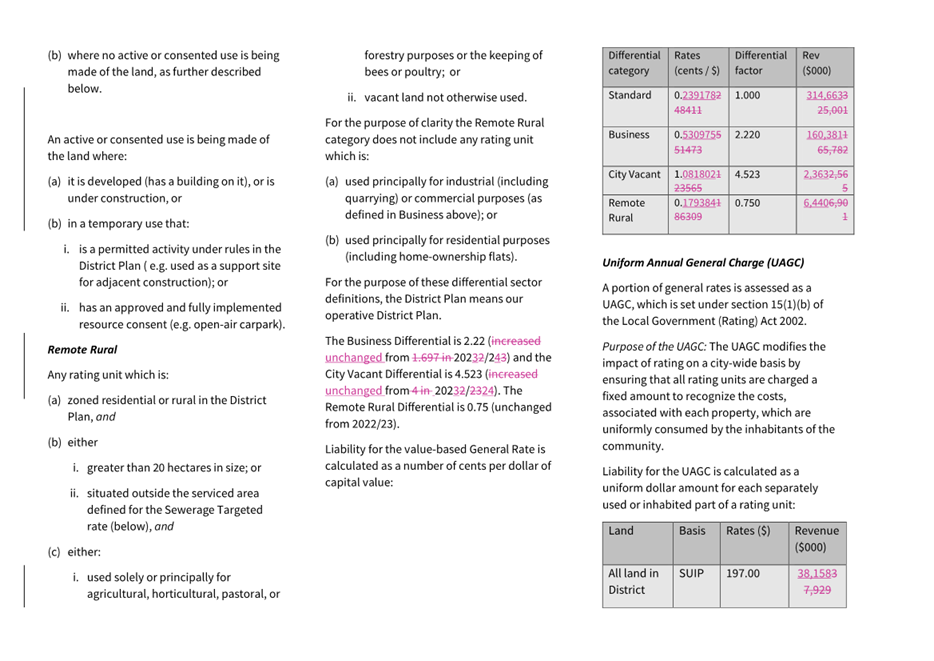

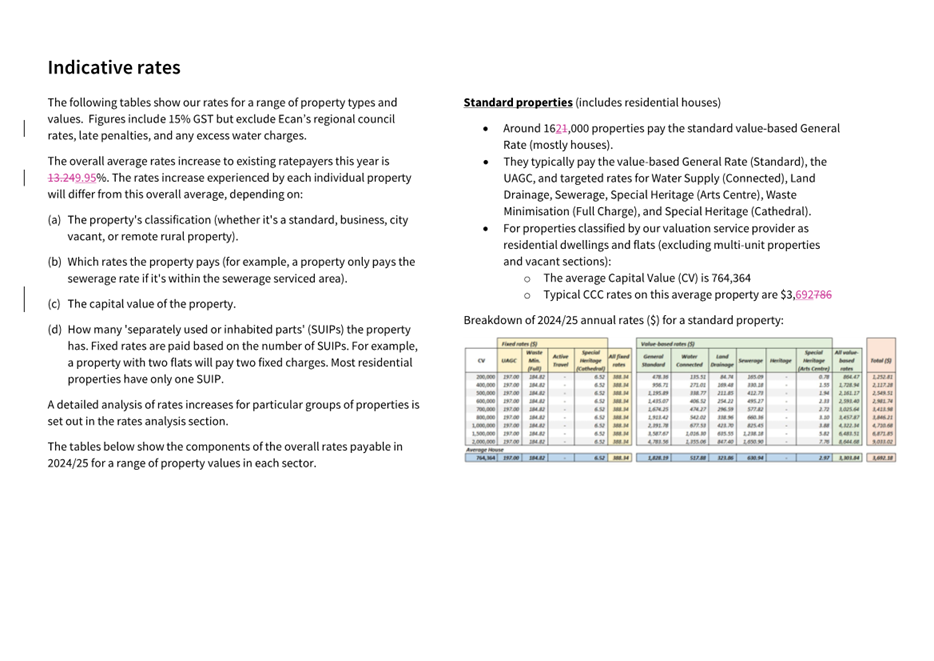

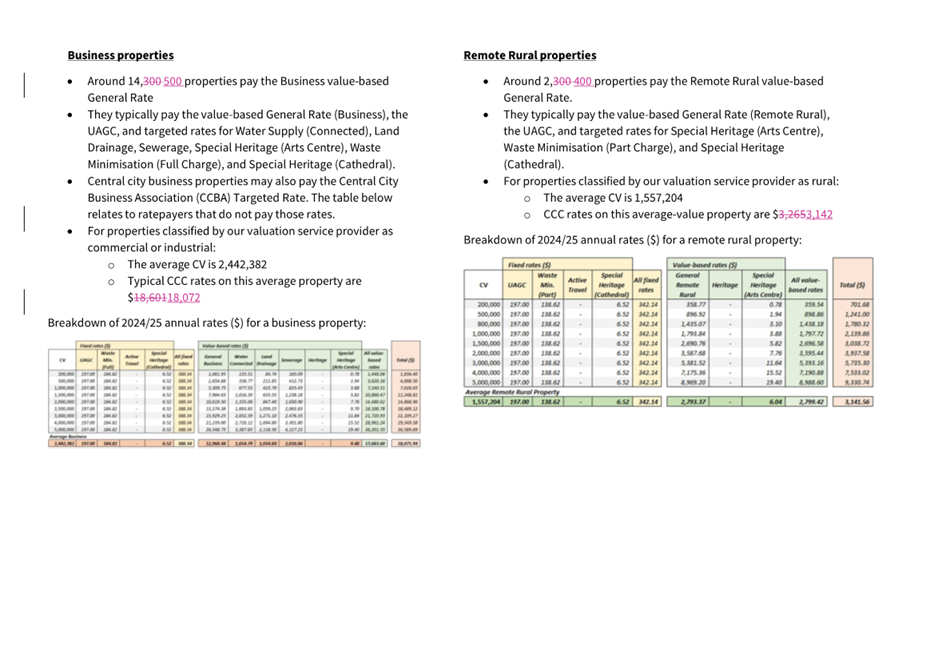

a. a uniform

annual general charge under section 15(1)(b) of $197 (incl. GST) per

separately used or inhabited part of a rating unit;

b. a general

rate under sections 13(2)(b) and 13(3)(a)(ii) set differentially based on

property type, and capital value as follows:

|

Differential

Category

|

Basis for

Liability

|

Rate Factor

(incl. GST) (cents/$ of capital value)

|

|

Standard

|

Capital

Value

|

0.239178

|

|

Business

|

Capital

Value

|

0.530975

|

|

City Vacant

|

Capital

Value

|

1.081802

|

|

Remote

Rural

|

Capital

Value

|

0.179384

|

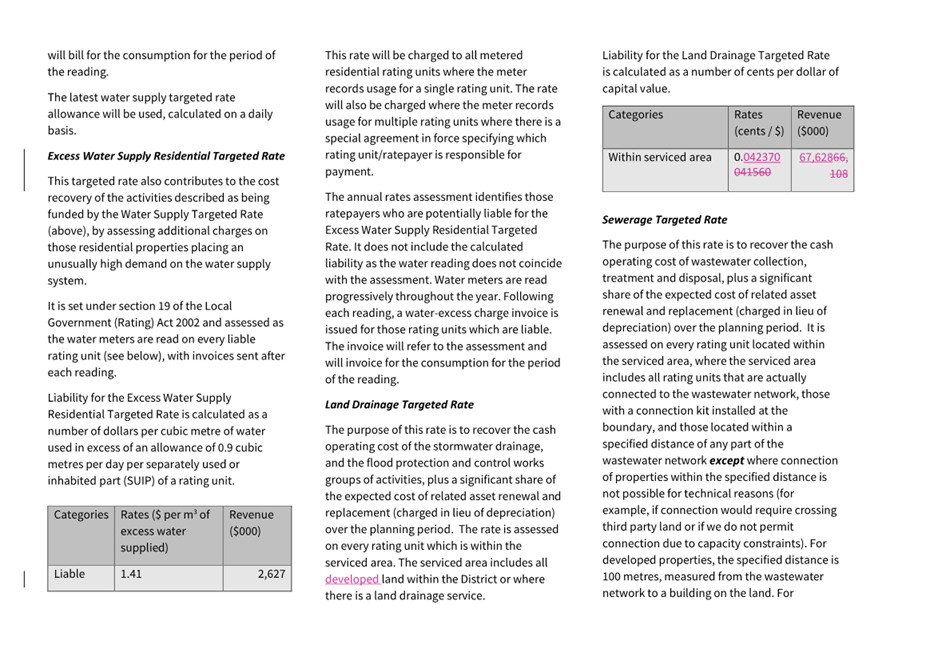

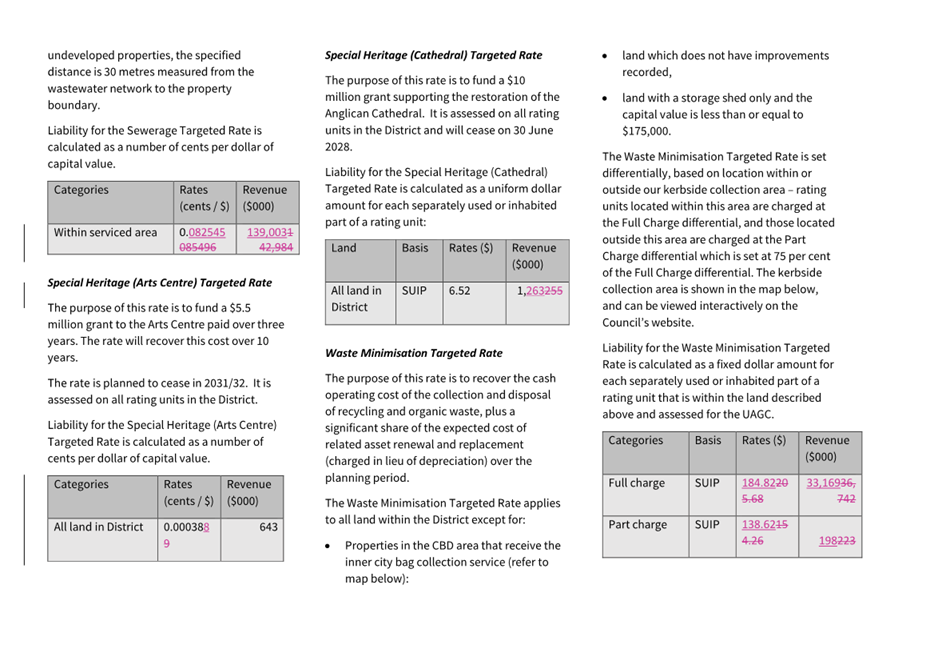

c. a sewerage targeted rate under sections

16(3)(b) and 16(4)(a) on all rating units in the serviced area of 0.082545 cents per dollar of capital value (incl.

GST);

d. a land

drainage targeted rate under sections 16(3)(b) and 16(4)(a) on all rating

units in the serviced area of 0.042370 cents per dollar of capital value (incl.

GST);

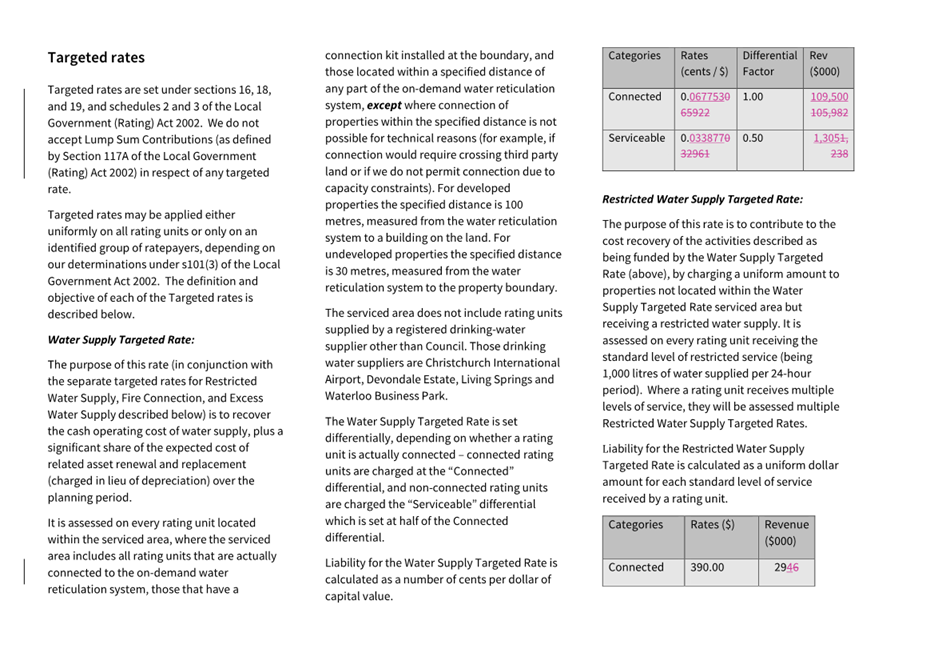

e. a water supply targeted rate under

section 16(3)(b) and 16(4)(b) set differentially depending on whether a

property is connected or capable of connection to the on-demand water

reticulation system, as follows:

|

Differential

Category

|

Basis for

Liability

|

Rate Factor

(incl. GST) (cents/$ of capital value)

|

|

Connected

(full charge)

|

Capital

Value

|

0.067753

|

|

Serviceable

(half charge)

|

Capital

Value

|

0.033877

|

f. a restricted

water supply targeted rate under sections 16(3)(b) and 16(4)(a) on all

rating units with one or more connections to restricted water supply systems of

$390 (incl. GST)

for each standard level of service received by a rating unit;

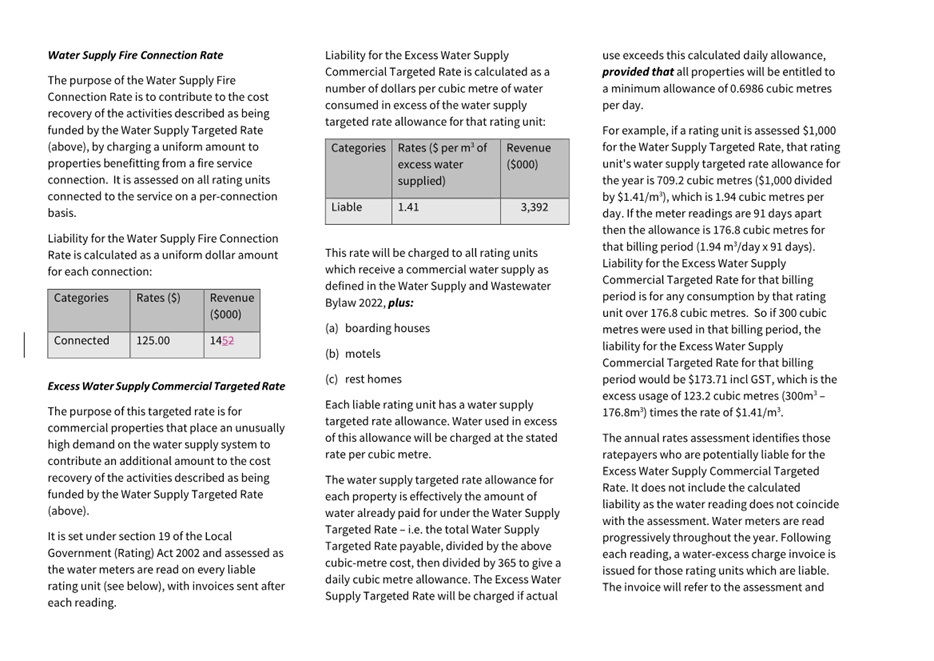

g. a water

supply fire connection targeted rate under sections 16(3)(b)

and 16(4)(a) on all rating units receiving the benefit of a water supply fire

connection of $125 (incl. GST) per connection;

h. an excess

water supply commercial targeted rate under section 19(2)(a) set for all

rating units which receive a commercial water supply as defined in the Water

Supply, Wastewater and Stormwater Bylaw 2022 plus boarding

houses, motels, and rest homes, of $1.41 (incl. GST) per m3

or

any part of a m3 for consumption in

excess of the rating unit’s water supply targeted rate daily allowance:

· where the

rating unit’s water supply targeted rate daily allowance is an amount of

cubic meters per day, calculated as the total amount payable under the water

supply targeted rate (above), divided by the cubic meter cost ($1.41), divided

by 365;

· provided that all

properties will be entitled to a minimum consumption of 0.6986 cubic metres per

day.

i. an excess water supply residential

targeted rate under section 19(2)(a) set for the following:

· all metered residential rating units where the

meter records usage for a single rating unit;

· a rating unit where the meter records usage

for multiple rating units where there is a special agreement in force

specifying which rating unit / ratepayer is responsible for payment,

of $1.41 (incl.

GST) per m3 or any part of a m3 for consumption in excess

of 900 litres per day per separately used or inhabited part of the rating unit;

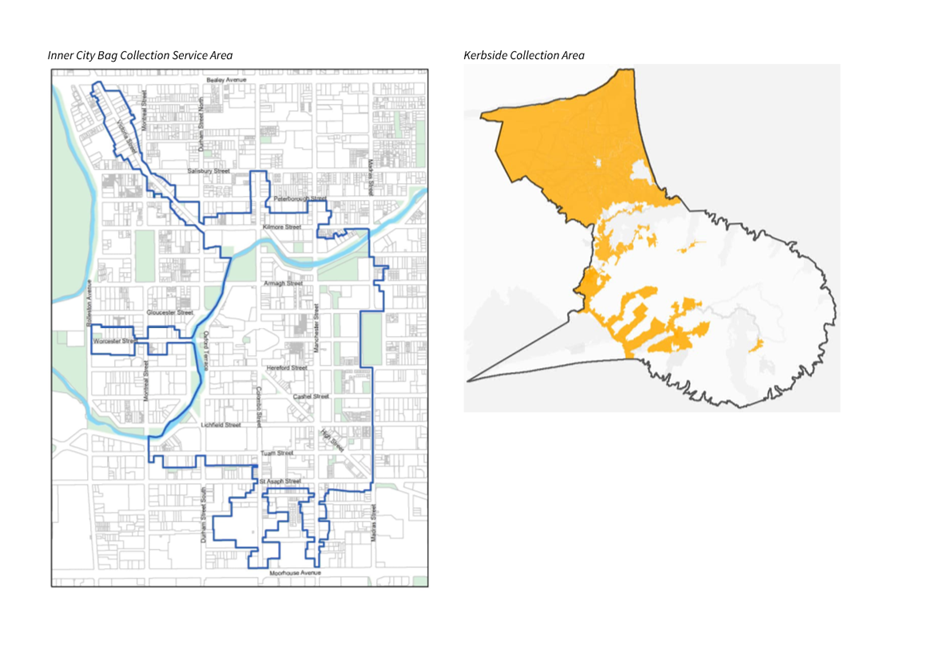

j. a waste

minimisation targeted rate under sections 16(3)(b) and 16(4)(b) set

differentially depending on whether a full or partial service is provided, as

follows:

|

Differential

Category

|

Basis for

Liability

|

Rate Factor

(incl. GST)

|

|

Full

service

|

Per separately used or

inhabited part of a rating unit

|

$184.82

|

|

Partial

service

|

Per separately used or

inhabited part of a rating unit

|

$138.62

|

k. a special

heritage (Cathedral) targeted rate under section 16(3)(a) and 16(4)(a) of

$6.52 (incl. GST) per separately used or inhabited part of a rating unit;

l. a special heritage (Arts Centre)

targeted rate under section 16(3)(a) and 16(4)(a) of 0.000388

cents per dollar of capital value (incl. GST);

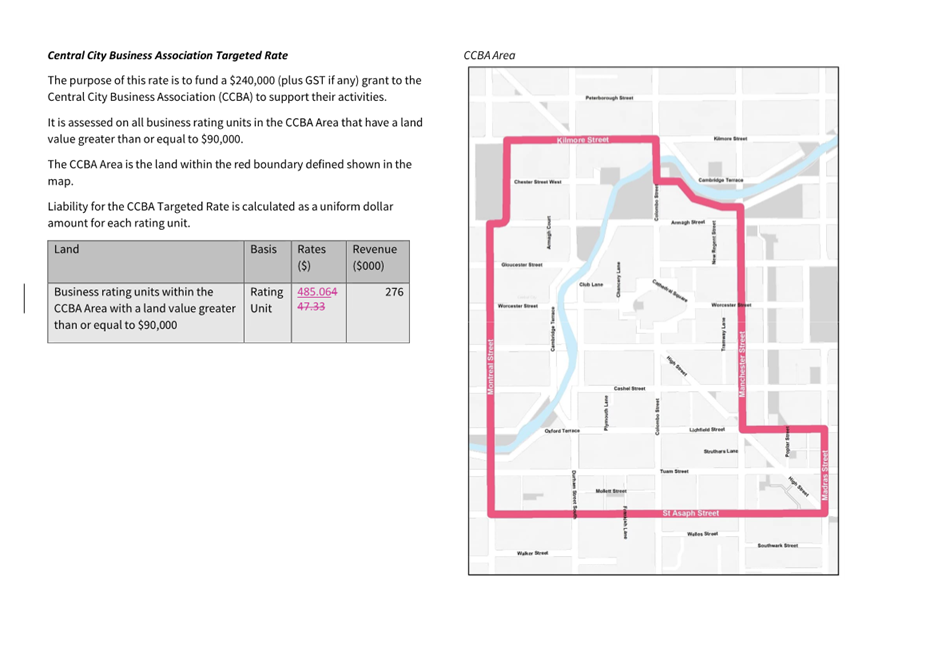

m. a Central City Business Association

targeted rate under section 16(3)(b) and 16(4)(a) of $485.06 (incl.

GST) per business rating unit in the Central City Business Association Area,

where the land value of the rating unit is greater than or equal to $90,000;

22. Resolves that all rates except the excess water supply commercial targeted rate

and the excess water supply residential targeted rate are due in four instalments, and to set the

following due dates for payment:

|

Instalment

|

1

|

2

|

3

|

4

|

|

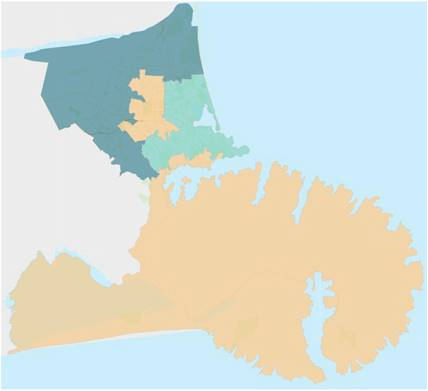

Area 1

|

15 August

2024

|

15 November

2024

|

15 February

2025

|

15 May 2025

|

|

Area 2

|

15

September 2024

|

15 December

2024

|

15 March

2025

|

15 June

2025

|

|

Area 3

|

31 August

2024

|

30 November

2024

|

28 February

2025

|

31 May 2025

|

Where

the Instalment Areas are defined geographically as follows:

|

Area 1

|

Area 2

|

Area 3

|

|

Includes generally the

Central City and the suburbs of St Albans, Merivale, Mairehau, Papanui,

Riccarton, Addington, Spreydon, Sydenham, Beckenham, Opawa and Banks

Peninsula.

|

Includes generally the

suburbs of Shirley, New Brighton, Linwood, Woolston, Mt Pleasant, Sumner,

Cashmere and Heathcote.

|

Includes generally the

suburbs of Belfast, Redwood, Parklands, Harewood, Avonhead, Bishopdale, Ilam,

Fendalton, Hornby, Templeton and Halswell.

|

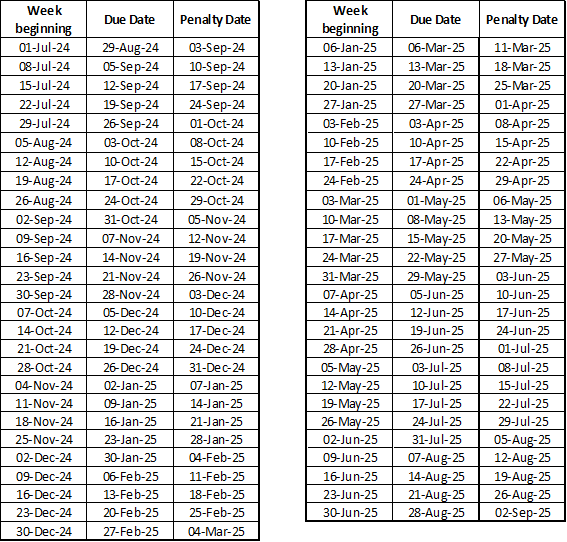

23. Resolves that the excess water supply

commercial targeted rate and the excess water supply residential targeted rate

(together, “excess water charges”) have Due Dates and Penalty Dates

based on the week in which amounts are invoiced, according to the following

table:

24. Resolves to add the following penalties to

unpaid rates:

a. A penalty of 10 per cent will be added to any

portion of an instalment (for rates other than excess water charges) not paid

on or by the due dates set out in paragraph 22 above, to be added on the

following dates:

|

Instalment

|

1

|

2

|

3

|

4

|

|

Area 1

|

20 August

2024

|

21 November

2024

|

20 February

2025

|

20 May 2025

|

|

Area 2

|

17

September 2024

|

19 December

2024

|

20 March

2025

|

19 June

2025

|

|

Area 3

|

05

September 2024

|

05 December

2024

|

05 March

2025

|

06 June

2025

|

b. A penalty of 10 per cent will be added to any

portion of excess water charges not paid on or by the due dates set out in

paragraph 23 above, to be added on the Penalty Dates set out in paragraph 23.

c. For all rates, an additional penalty of 10 per

cent will be added on 01 October 2024 to any rates assessed, and penalties

added, before 01 July 2024 and which remain unpaid on 01 October 2024.

d. For all rates, a further penalty of 10 per

cent will be added if any rates to which a penalty has been added under (c)

above remain unpaid on 01 April 2025.

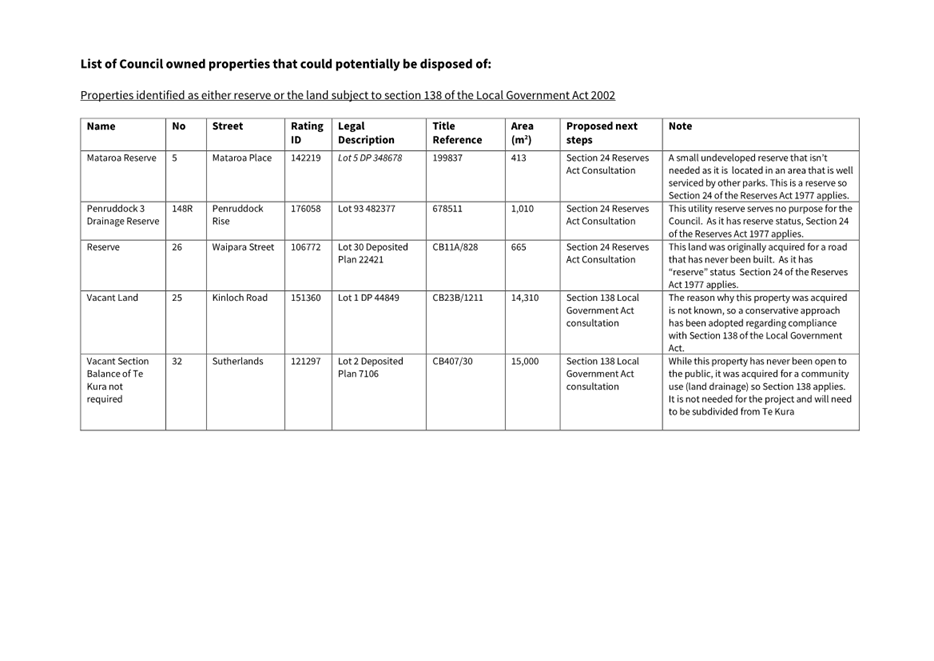

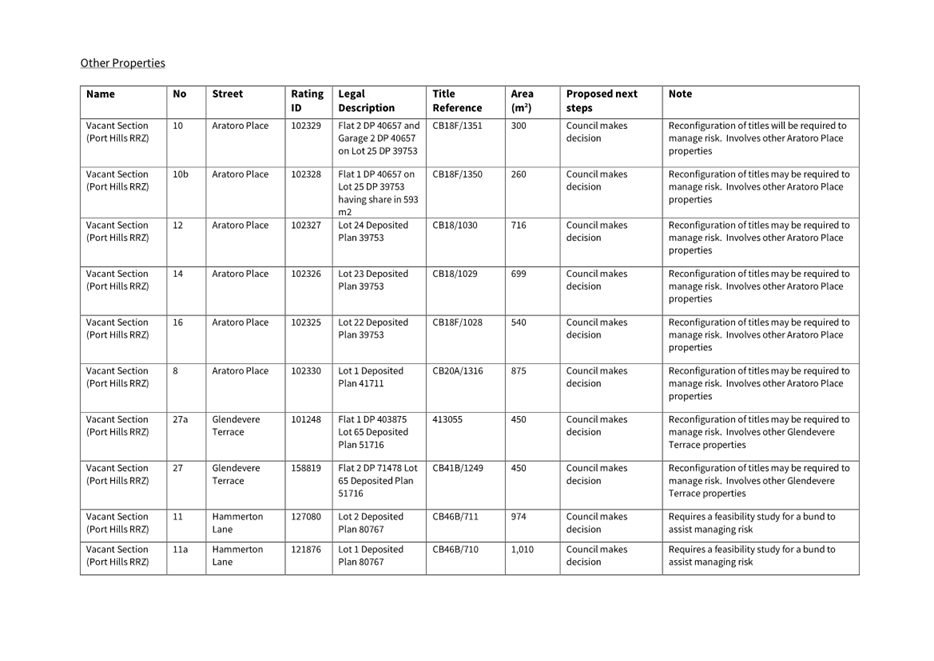

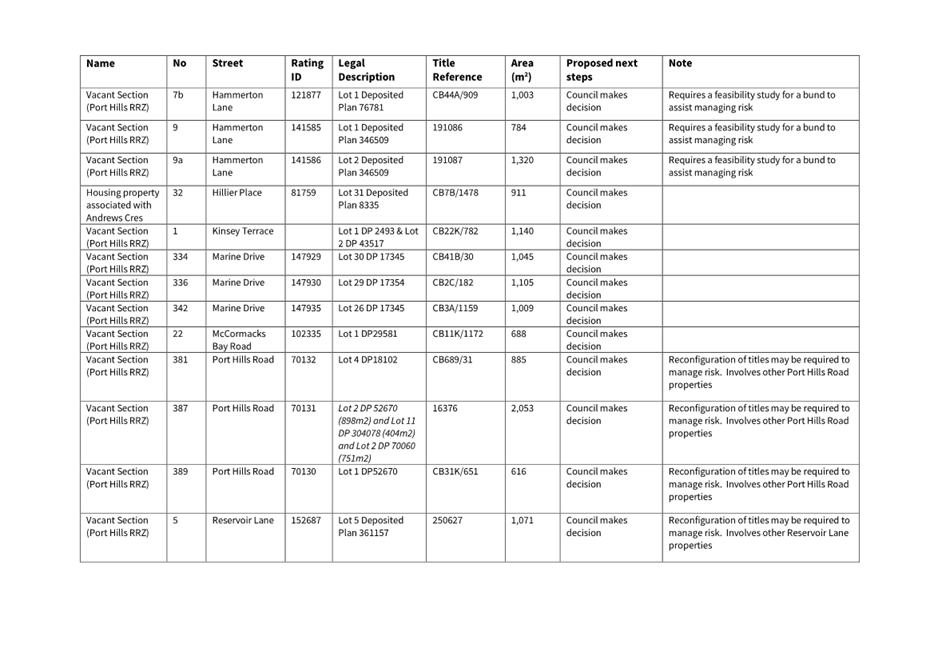

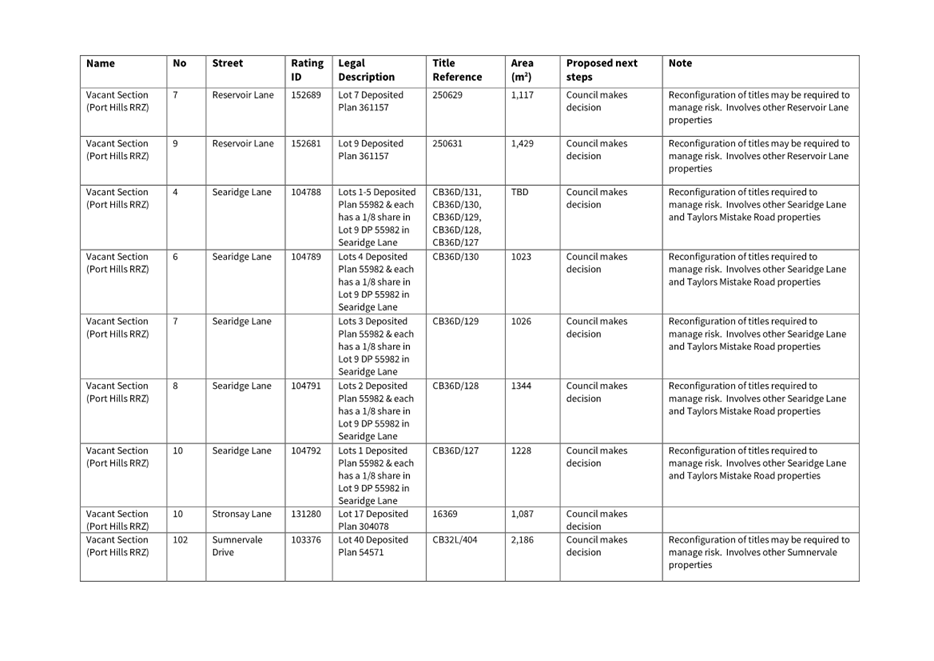

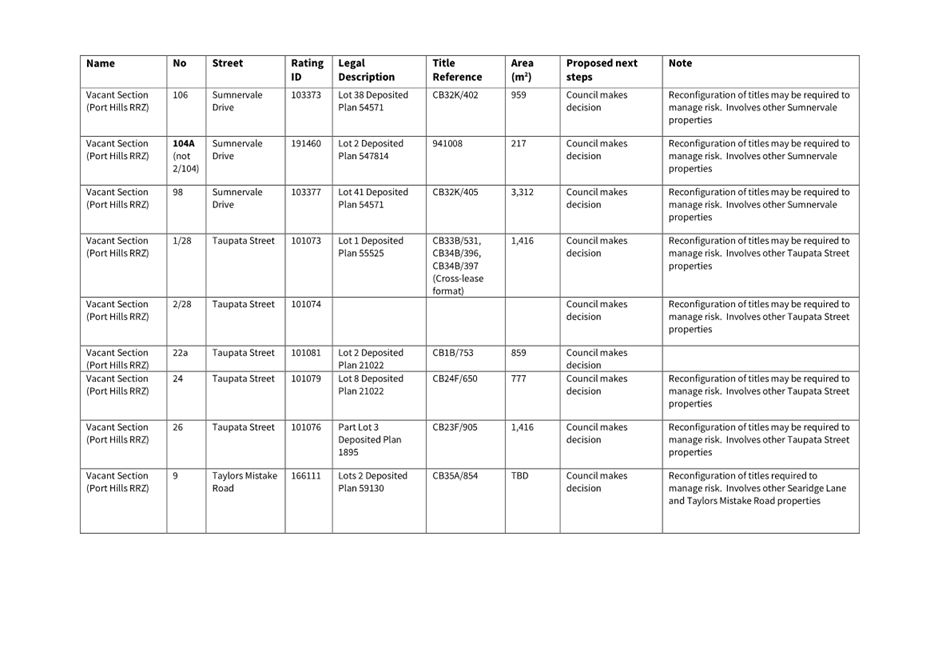

25. In relation to the disposal of Council

properties:

a. Declares the properties in the attached list (Attachment

Q), as consulted upon in the draft Long Term Plan 2024-34, are surplus to

requirements and delegates to the Chief Executive the authority to initiate

their disposal including determining the method of disposal (per second table

of the attachment, “Other Properties”); and

b. Commences formal processes to dispose of the

properties listed in the first table of Attachment Q (“Properties

identified as either reserve or the land subject to section 138 of the Local

Government Act 2002”).

3. Executive Summary Te Whakarāpopoto Matua

3.1 The

2024-34 Long-Term Plan (LTP) process was reviewed by the Council’s Audit

and Risk Management Committee at its meeting on 20 June 2024.

3.2 The

Committee’s opinion will be provided to the Council by way of a memo and

verbal update from the Chair of the Audit and Risk Management Committee at this

Council meeting (25 June 2024). Information establishing that the LTP 2024-34

is supported by appropriate management signoffs is set out in Attachments L

and M.

3.3 The

Mayor and Councillors have received and considered a record number of

submissions (over 7000) made on the Council’s proposed LTP 2024-34 and

heard over 300 verbal submissions from individuals, stakeholders and community

groups through the hearings process which was held from 2 May 2024 to 13 May

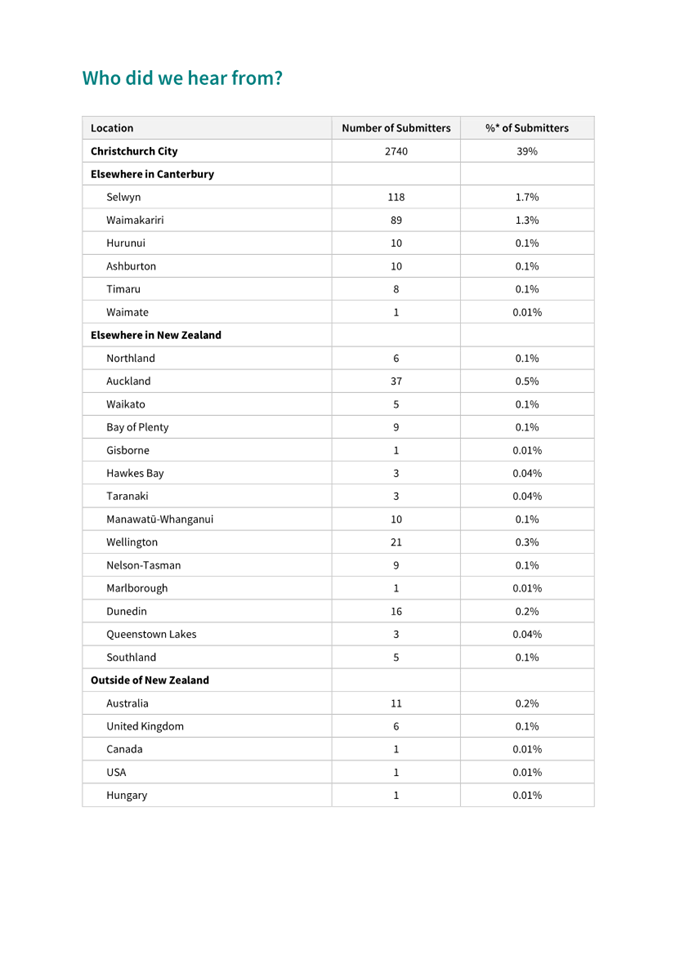

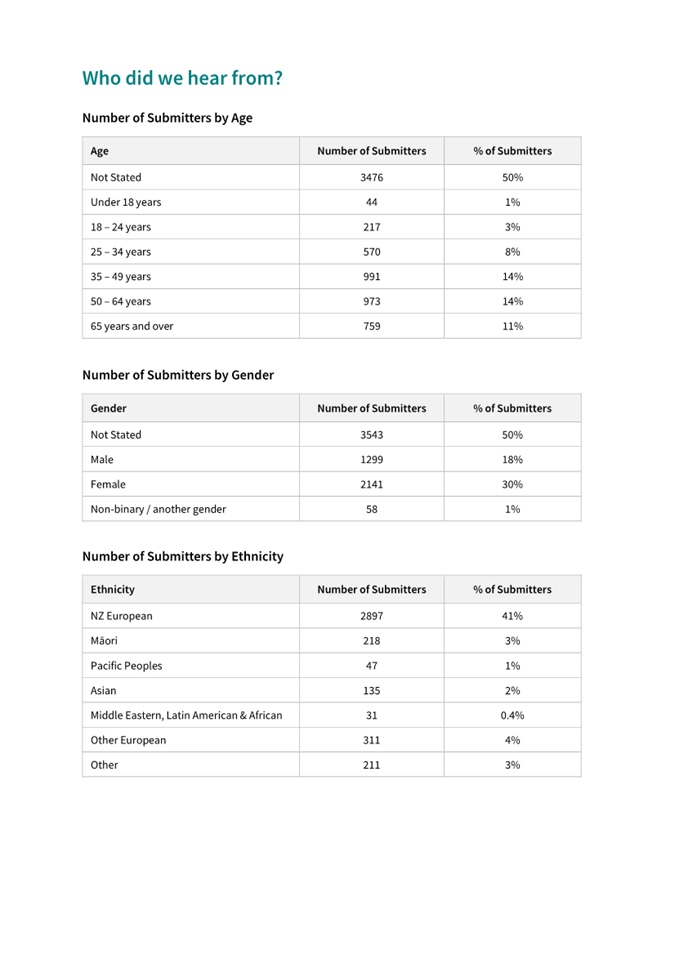

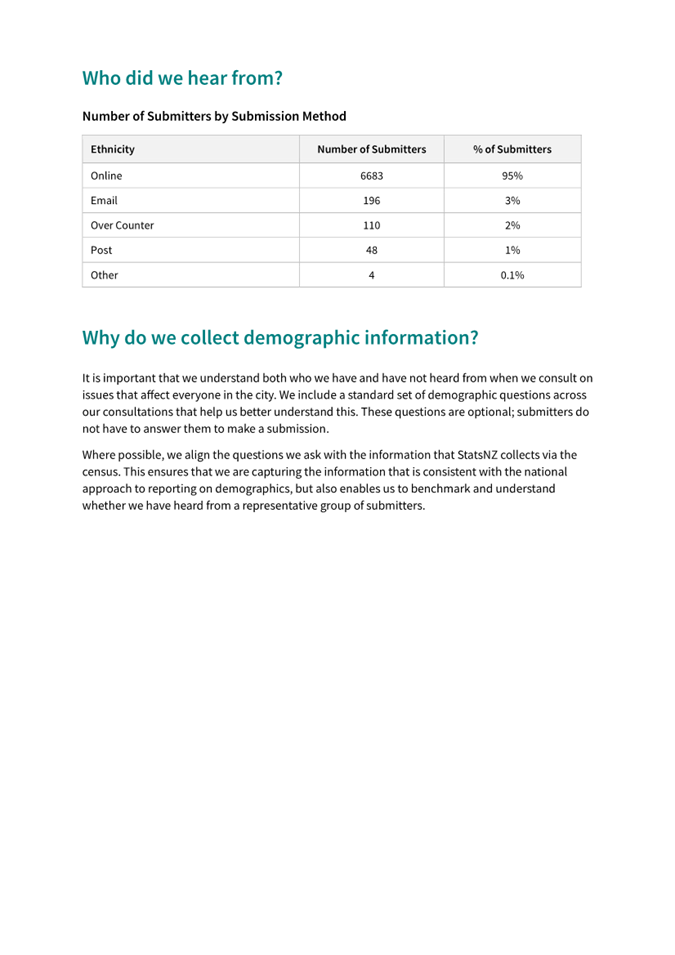

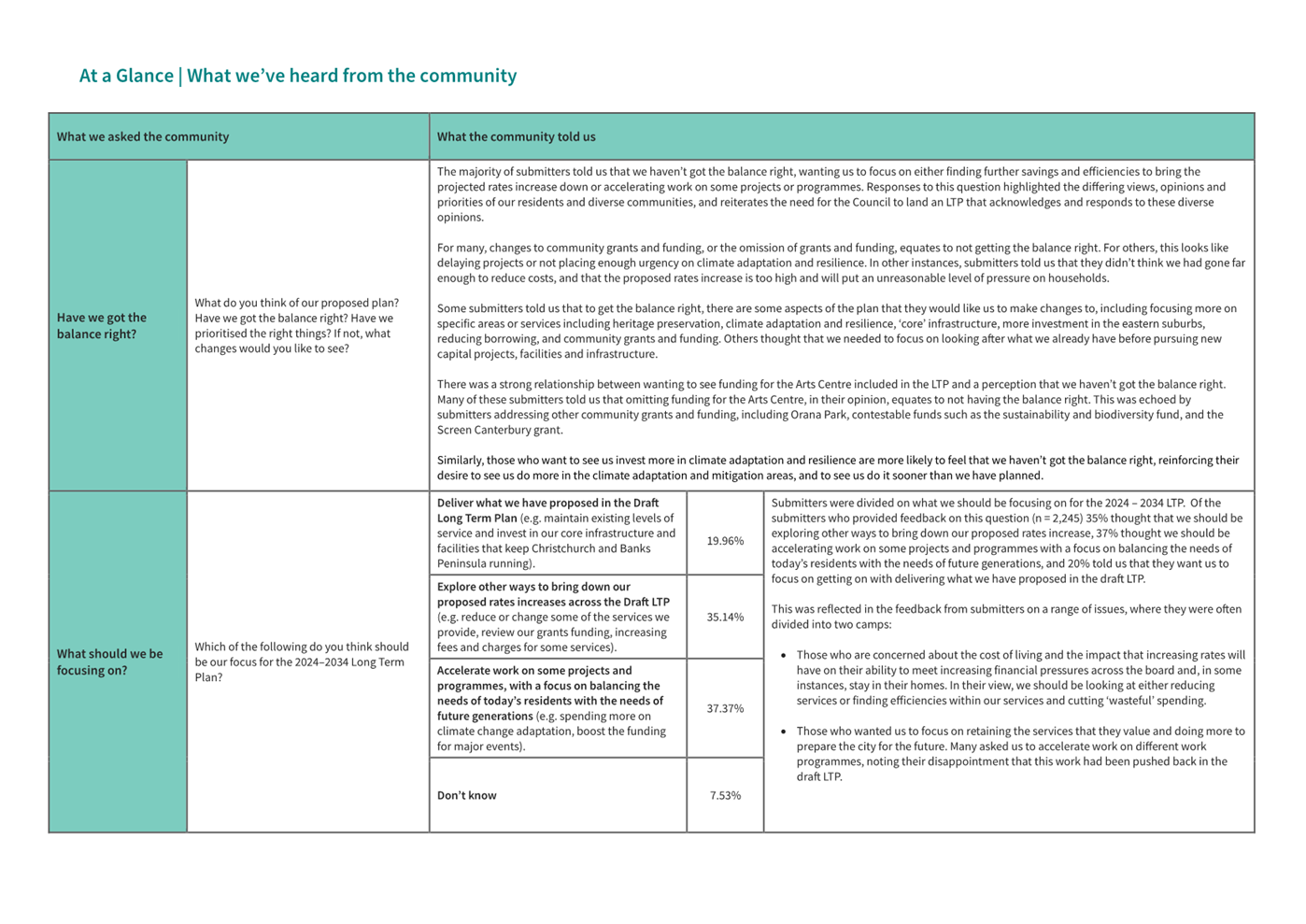

2024. The Thematic Analysis of LTP 2024-34 submissions and hearings is set out

in Attachment O.

3.4 Following

the hearing of verbal submissions, the Council then held a series of Public and

Public Excluded Workshops to discuss the Council’s response to the

community’s views and preferences. The Workshops were held from Monday 20

May to Thursday 30 May 2024.

3.5 Preparing

and adopting an LTP is a matter of high significance. For this reason the

LGA 2002 requires the Council to use the special consultative procedure when

consulting with its community (s.93(2)). The requirements of the SCP are set

out in s.83 of the Act.

3.6 The

consultation process for adoption of the LTP 2024-34 was undertaken in

accordance with the Council’s statutory obligations.

4. Background/Context Te Horopaki

4.1 The

LTP 2024-34 was developed under the direction of the Councillor’s Letter

of Expectation (Attachment N) which set out clear guidelines on both LTP

process and content.

4.2 The

key process expectations were that draft LTP documents would be available for

July 2023, and that a joint development process between Council, staff and

stakeholders would occur July-December 2023 (joint development briefings were

dates where the public could attend (public and live-streamed), with the

release of all briefing recordings, content and briefing notes through LTP 2024-2034 | What matters

most? | Kōrero mai | Let’s talk (ccc.govt.nz).

4.3 The

draft LTP 2024-34 was adopted by the Council on 14 March 2024 (the meeting

commenced from 14 February 2024). The draft LTP was reviewed by Council’s

Audit and Risk Management Committee which concluded it was fit for purpose.

4.4 The

Council then consulted with the community on the draft LTP 2024-34 via a

Consultation Document (CD) and underlying information adopted on 14 March 2024

(the meeting commenced from 14 February 2024.).

4.4.1 The

CD and the underlying information were made publicly available and members of

the public were given the opportunity to present their views and preferences in

response. The CD included an audit report issued by the Auditor General’s

appointed auditor. The audit report provided an opinion that the CD

provided an effective basis for public participation in the Council’s

decision about the proposed content of the LTP and that the information and

assumptions underlying the information in the CD were reasonable. The

consultation was open from 18 March to 21 April 2024. It complied with all

legal requirements.

4.4.2 Opportunity for members of the public to present

at public hearings was available from 2 May to 13 May 2024. These hearings were

recorded and remain publicly available Christchurch City Council Live - YouTube.

4.4.3 All

submissions, written and oral (including those presented at public hearings),

have been analysed to identify the matters raised, the reasons for those

comments and the overall themes that emerged from the consultation process.

4.4.4 The

result of this work was provided to elected members for their workshop of 21

May 2024 to assist with their deliberations. The Thematic Analysis of the LTP

2024-34 Submissions and Hearings is Attachment O of this report.

4.4.5 The

Thematic Analysis provides a summary of key issues identified by a significant

number of submitters in response to the questions asked in the Consultation

Document. The first part of the report provides an overview of the key themes

and messages that have come through in submissions. The latter part of the

report provides detailed submissions analysis for some of the issues that were

most popular with submitters. Also included is a breakdown of the number of

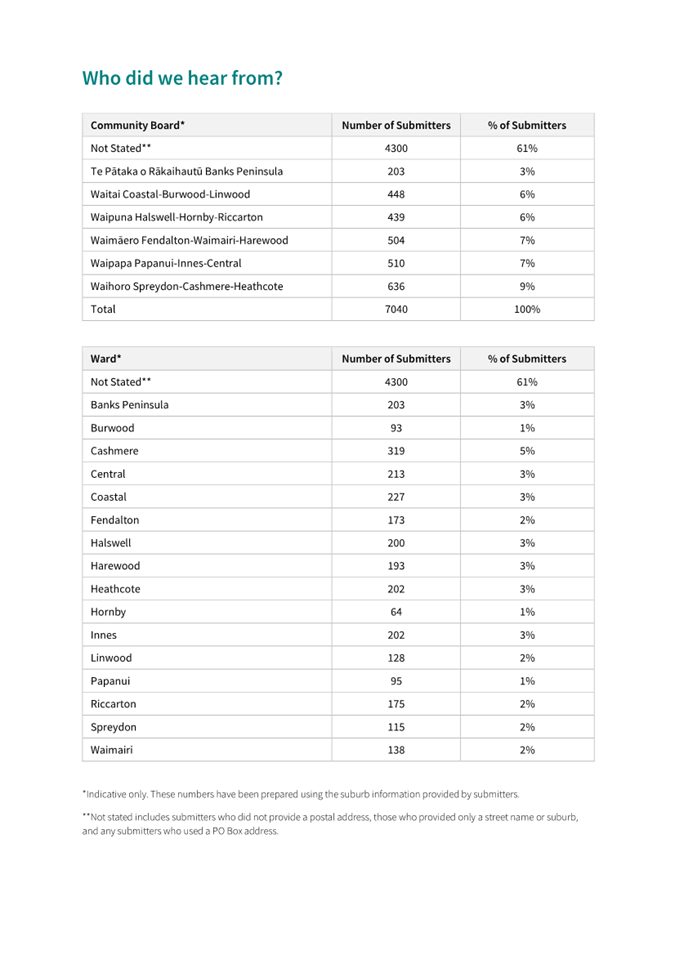

submissions received, by Community Board, age, and gender.

4.5 Since

conclusion of the Hearings, staff have held multiple public and public excluded

Workshops with Councillors (21, 23 [public excluded], 24, 28 and 30 [partially

public excluded] May 2024), provided responses to issues and questions raised,

and received guidance on matters raised. The public workshops were recorded and

remain available Christchurch

City Council Live - YouTube.

4.6 Guidance

was provided by Elected Members via a set of draft Mayor’s

Recommendations (Attachment C.) This guidance was then built into the

LTP 2024-34 adoption documents for Audit NZ review, including expectations for

rates increases.

4.7 The

guidance largely reflects community feedback on the draft LTP, or changes to

the Council’s operating environment since adopting the draft in

February/March 2024.

4.8 The

process for preparing LTP 2024-34 information included a series of detailed

management signoffs, including the Executive Leadership Team, that provide

assurance around compliance with the Council’s relevant statutory,

financial, and legal obligations to the Audit and Risk Management Committee

(ARMC – meeting date 20 June 2024). The management signoffs for Process,

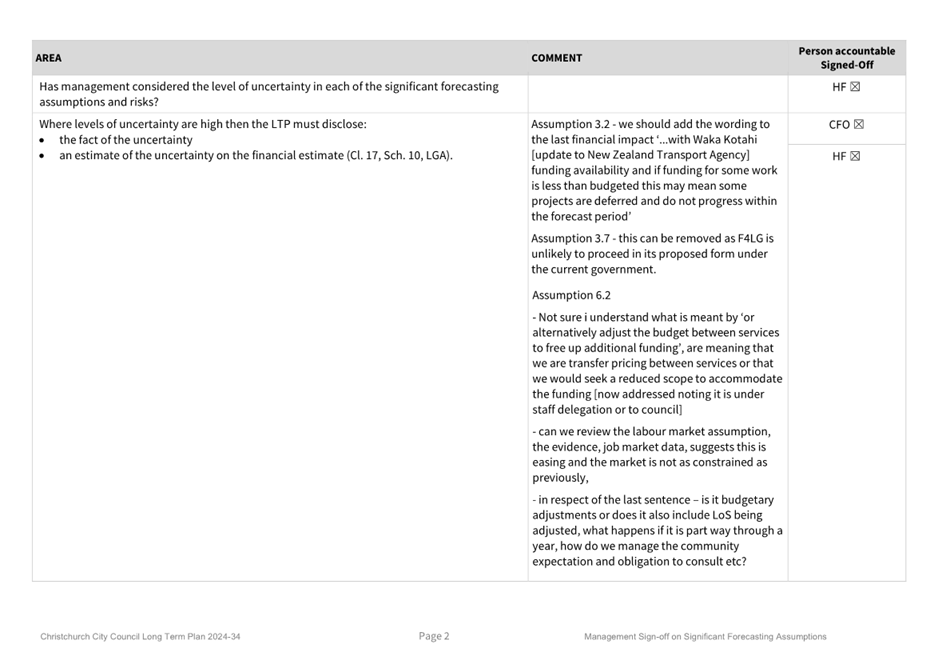

and Significant Assumptions signoffs, form Attachments L and M.

4.9 Audit

New Zealand have agreed to provide a verbal update on their review of the final

LTP 2024-34 at the ARMC meeting of 20 June 2024.

4.10 The

Council meeting to adopt the LTP 2024-34 is scheduled for 25 June 2024, with an

additional available date of 27 June 2024.

4.11 The

LTP 2024-34 is currently on track for adoption by Council on 25/27 June 2024,

provisional upon ARMC and Audit NZ advice.

4.12 Within

one month following adoption of the LTP 2024-34 the Council must make the plan

publicly available. This will include publishing online via our public

website, providing access to hard copies of the plan via our libraries and

services centres, and providing digital and/or hard copy prints to the Mayor

and Councillors, to the National Library of New Zealand, Department of Internal

Affairs, Parliamentary Library, The Auditor General, and Governor General.

4.13 Responses to submitters will be prepared and sent, and the staff

responses to submissions and the Thematic Analysis will be also published on

the public site.

Options Considered Ngā Kōwhiringa Whaiwhakaaro

4.14 The

following key options were considered during the Joint Development Process:

· Early in the process

Councillors provided guidance that Levels of Service would be maintained

wherever possible during the LTP development i.e. minimal service cuts.

· There was clear early

guidance that the capital programme would need to focus closely on

deliverability and affordability, especially in Years 1-3 of the LTP.

4.15 In

December 2023 there was guidance that assets managed by Christchurch City

Holdings Ltd would be managed at ‘Enhanced Status Quo’ rather than

‘Active Portfolio Management.’

4.16 Collectively

this guidance (on maintaining levels of service, a deliverable capital

programme, and management of CCHL assets) formed the overall parameters of the

draft and final LTP.

5. Financial Implications Ngā Hīraunga Rauemi

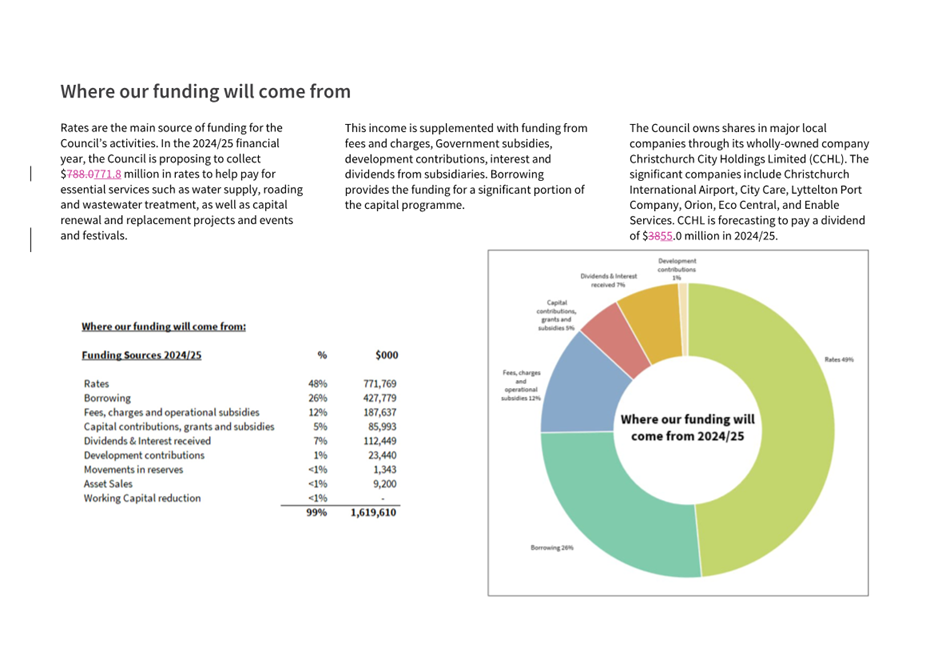

Rates

5.1 The

recommended LTP 2024-34 includes a rates requirement (excl. GST) to be levied

for 2024/25 of $761.2 million.

5.2 The

proposed average rates increase for 2024/25 to all existing ratepayers is

9.95%, lower than the 13.24% forecast in the Draft.

5.3 The

potential 2024/25 increases for the average capital value property in the 3

sectors is:

Residential 9.57%

Business 10.98%

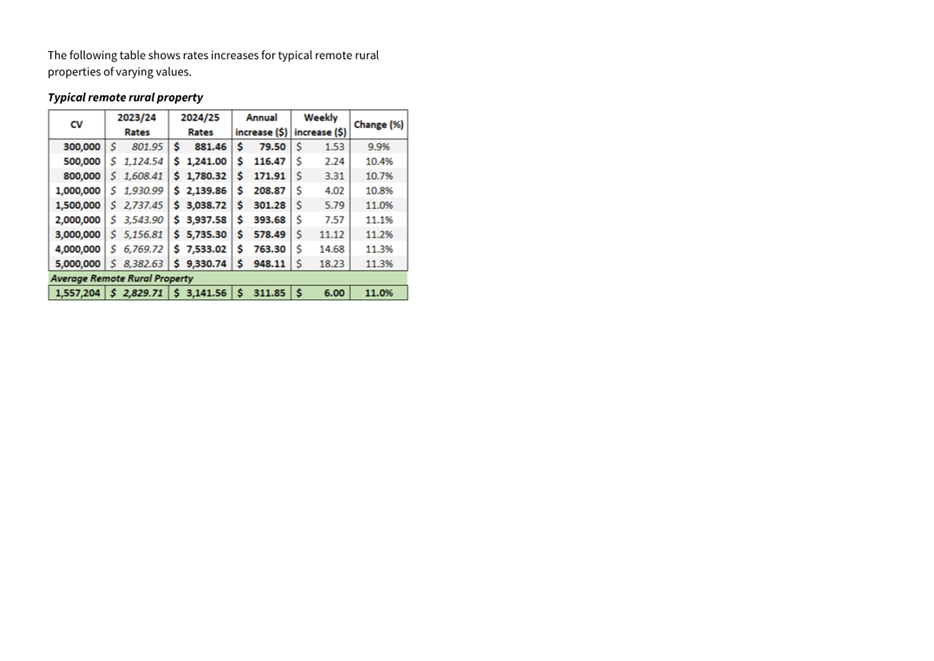

Remote Rural 11.02%

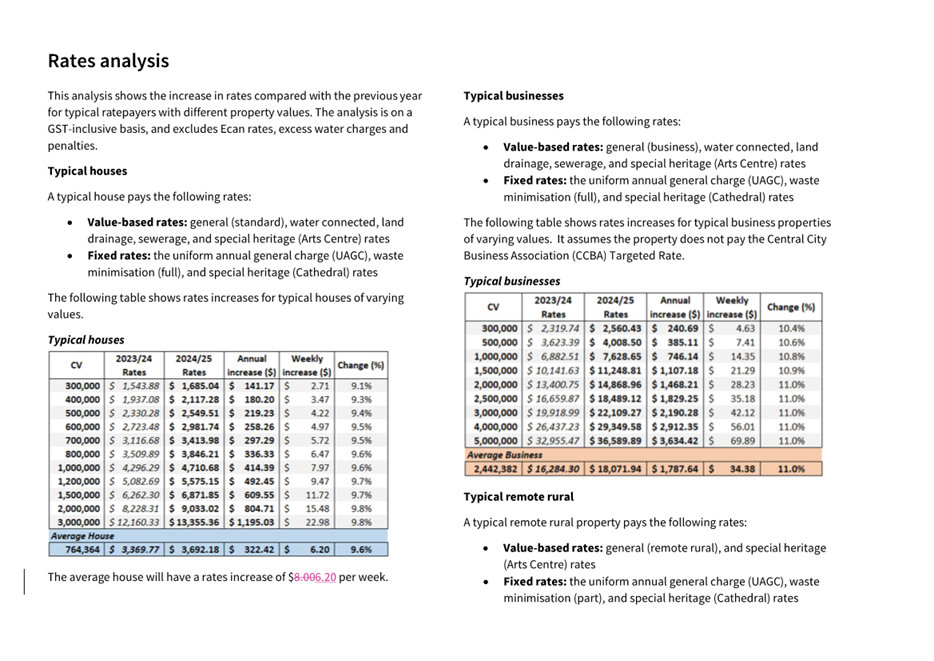

5.4 Based

on the recommended rates requirement noted above, the average house would have

a rates increase of $6.20 (incl GST) per week, down from $8.00 (incl GST) in

the Draft. Full details of rates, including the total rating requirement for

general and targeted rates, and indicative rates for sample properties, are

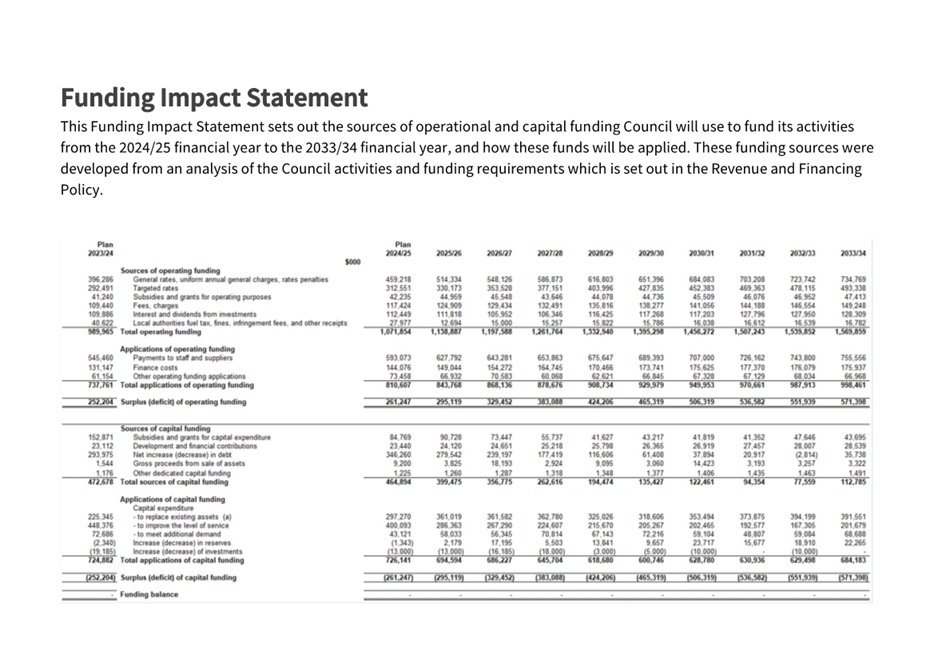

provided in the Funding Impact Statement.

Operating Expenditure

5.5 Operational

expenditure of $7.5 billion is proposed over the 10 years of the LTP, compared

to $7.4 billion in the Draft. The $77 million increase is principally due to:

5.5.1 Increased

contract and salary costs relating to the living wage announcement ($26.4

million),

5.5.2 Updated

cost of rates on Council properties and rates remissions ($12.1 million),

5.5.3 Environmental

partnership fund ($8.9 million),

5.5.4 Bringing

forward increased Events funding ($6.4m)

5.5.5 Arts

Centre funding ($5.25m)

5.5.6 Canterbury

Museum Levy adjustment from 2027/28 ($4.4 million),

5.5.7 Bringing

forward Climate Adaptation expenditure ($3.1 million).

5.6 Interest

costs over the 10 years are $12 million higher than projected in the Draft LTP

2024-34 largely due to slightly higher interest rates in later years.

5.7 Details

of all expenditure and revenue changes from the Draft LTP 2024-34 are shown in Attachment

E.

Revenue

5.8 Total

revenue excluding rates is $4.0 billion over the 10 years of the LTP, compared

to $3.9 billion in the Draft. The $111 million increase is due to:

5.8.1 Additional

Crown levies for organics and recycling ($48.8 million),

5.8.2 Inclusion

of Better Off Funding capital grants ($34.7 million),

5.8.3 Recoveries

of insurance and rates costs from Venue Ōtautahi ($28.8 million),

5.8.4 Additional

interest revenues ($3.2 million),

Partially

offset by:

5.8.5 Lower

Hagley Park revenues due to free weekend parking ($6.9 million).

Surplus, operating

deficits, and sustainability

5.9 The

recommended LTP shows accounting surpluses of $1,095 million before

revaluations over the ten years of the Plan. This is materially higher than the

Draft ($946 million) largely due to rate contributions to the Climate

Resilience Fund. Under accounting standards the Council is required to show all

revenue, including recoveries from central Government and NZ Transport Agency,

as income for the year. However, some of these recoveries reimburse the Council

for capital expenditure. After adjusting for these capital revenues, the

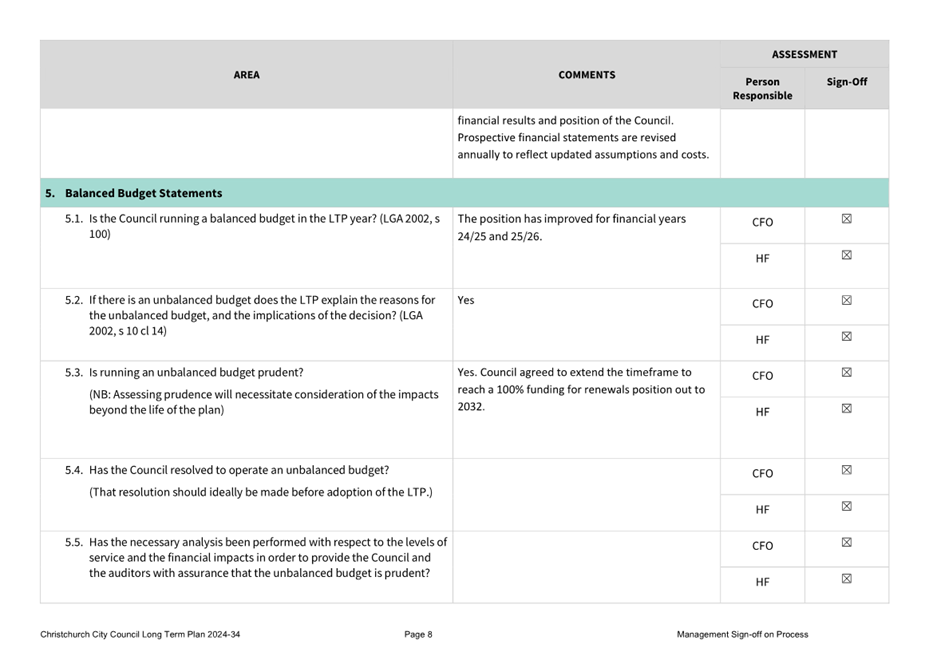

Council is forecasting a balanced budget for each year of the Plan (noting the

financial prudence balanced budget benchmark is a slightly different measure

which is unbalanced in 2026/27).

Capital programme expenditure

5.10 There is minimal change to the

capital programme from the draft. The Council plans to invest a total of $6.5

billion over the 10 years, an increase of $9 million. The changes are shown in Attachment

D.

Capital programme

funding

5.11 The

capital programme is funded by subsidies and grants for capital expenditure,

development contributions, proceeds from asset sales, rates and debt. In

the LTP we rate for $207.3 million of renewals in 2024/25 increasing each year

to $384.3 million in 2033/34.

Borrowing

5.12 The

recommended LTP shows gross debt rising from $2.59 billion at the start to

$3.90 billion at the end of the LTP. Both figures are $0.06 billion lower than

the draft due to an update of the opening LTP position.

5.13 Debt

repayment rises from $68.5 million in 2024/25 to $155 million in 2033/34.

Repayments are in total $21.8 million lower than the Draft.

5.14 In

accordance with our financial strategy we will continue to ensure prudent and

sustainable financial management of our operations and will not borrow beyond

our ability to service and repay that borrowing.

Advances

5.15 The

financial statements incorporate the forgiveness of the $2 million loan to the

Theatre Royal that was due for repayment in 2024/25.

Capex/Opex Ngā Utu Whakahaere

|

|

Recommended Option

|

Option 2 - <enter text>

|

Option 3 - <enter text>

|

|

Cost to Implement

|

Staff costs within existing management

budgets. Final costs for Audit NZ to be confirmed.

|

No alternate options

|

No alternate options

|

|

Maintenance/Ongoing Costs

|

Once the LTP is adopted and published no

maintenance or ongoing costs are anticipated.

|

|

|

|

Funding Source

|

Existing budget per Council's Long-Term

Plan (2021 - 2031)

|

No alternate options

|

No alternate options

|

|

Funding Availability

|

Considerable increase in auditing costs

from Audit NZ. Notified through Letter of Engagement only received early

March 2024. Management considering options for supporting additional cost

through existing budgets.

|

No alternate options

|

No alternate options

|

|

Impact on Rates

|

No anticipated additional impact on

rates.

|

|

|

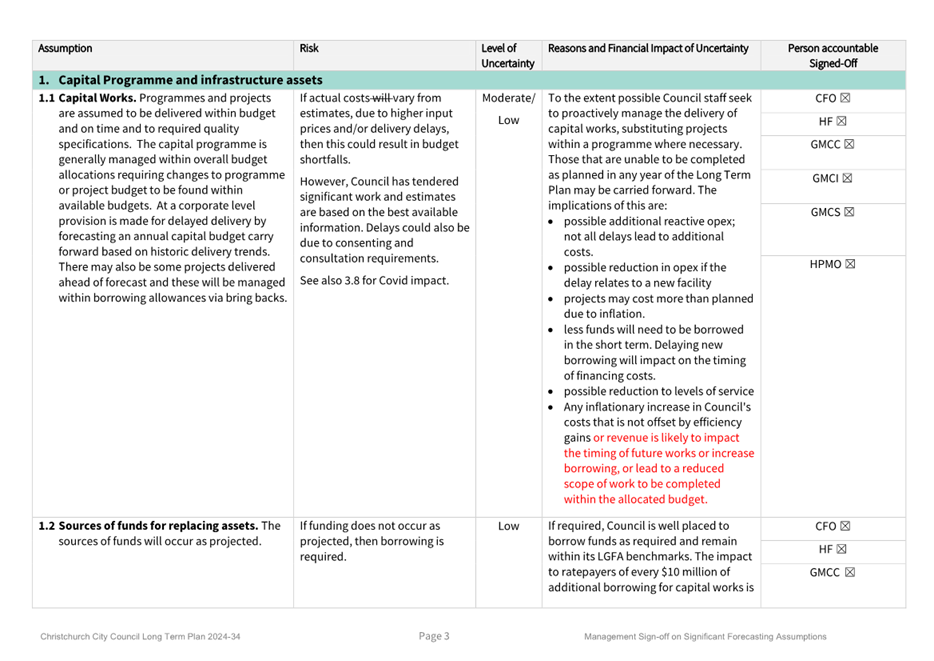

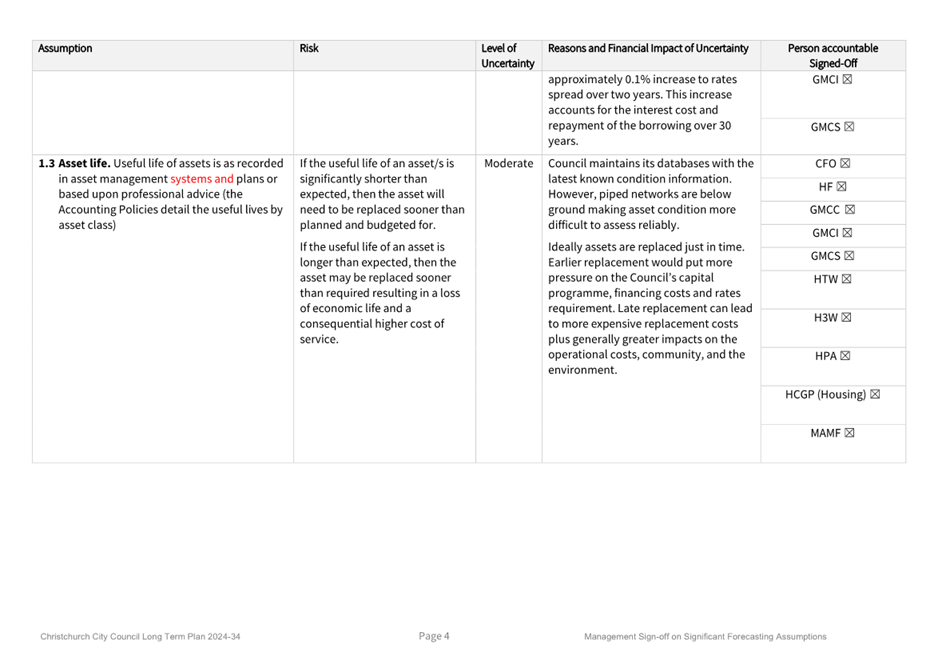

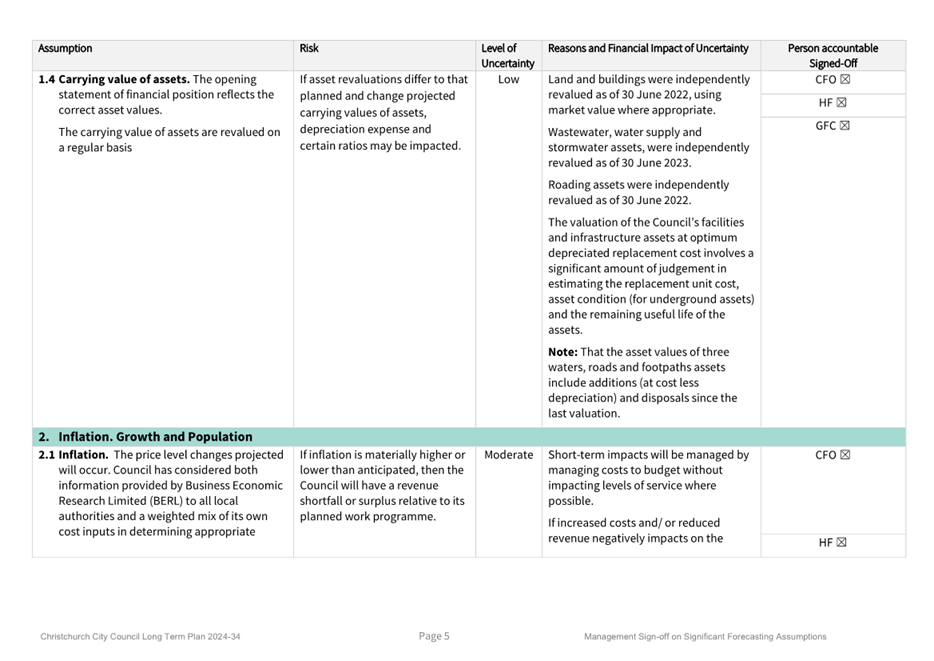

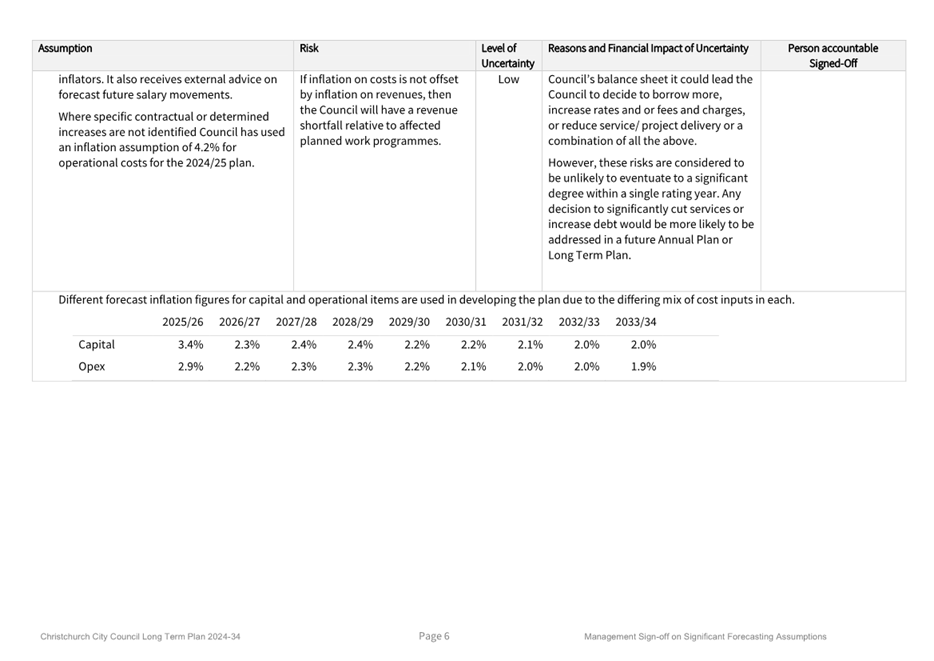

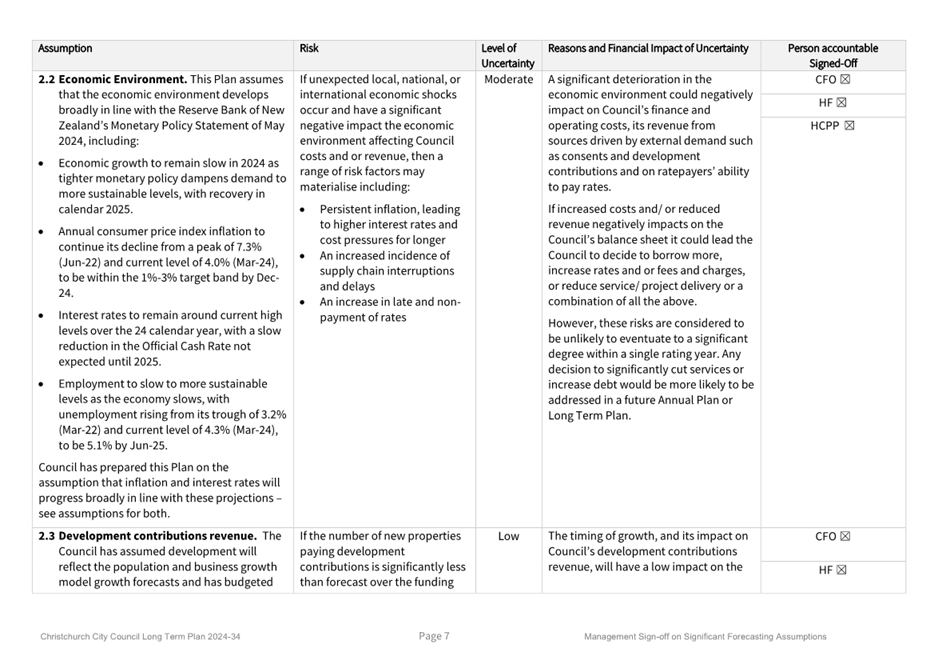

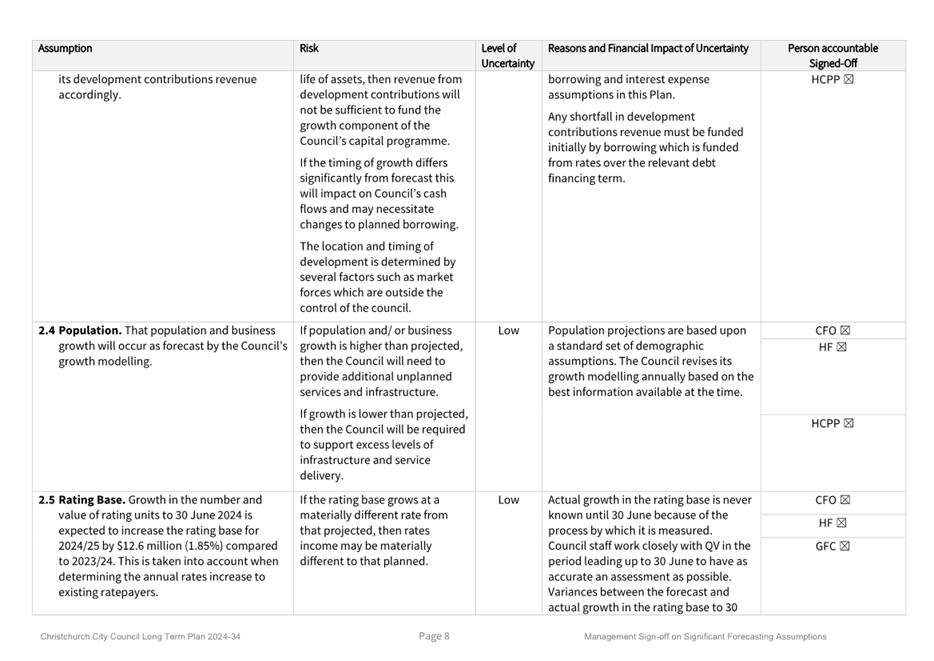

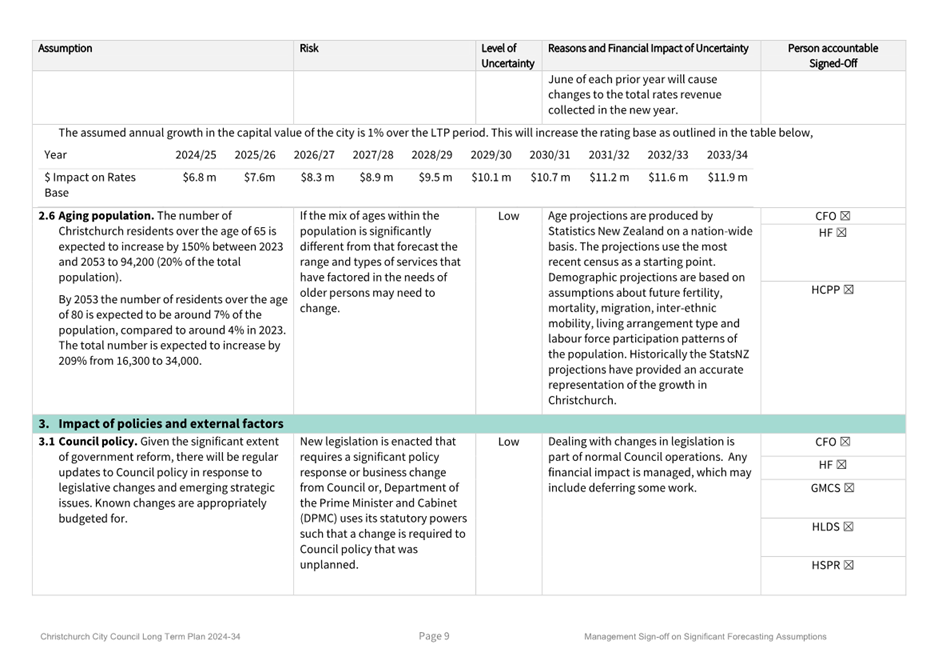

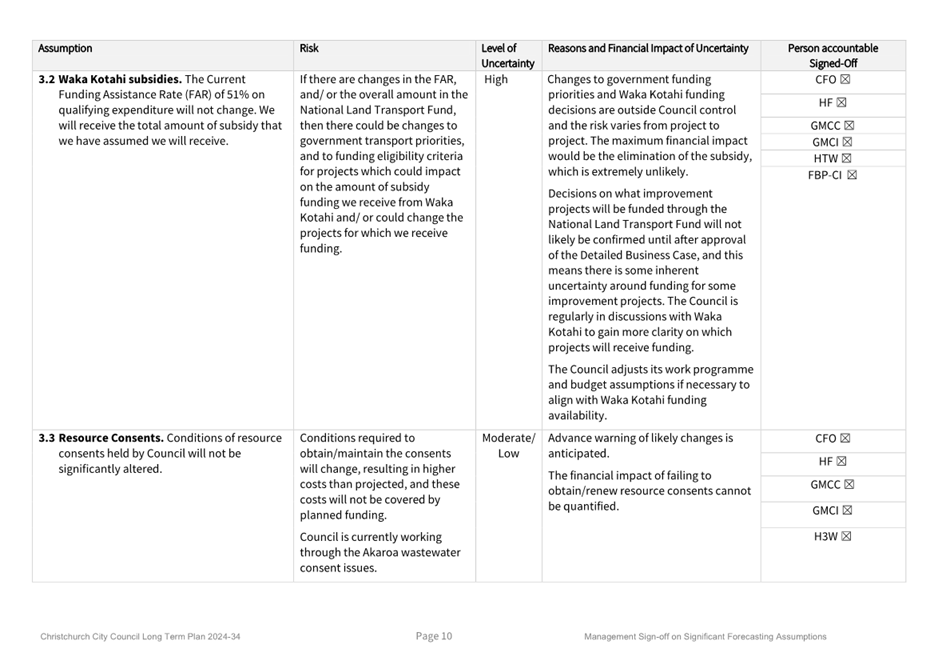

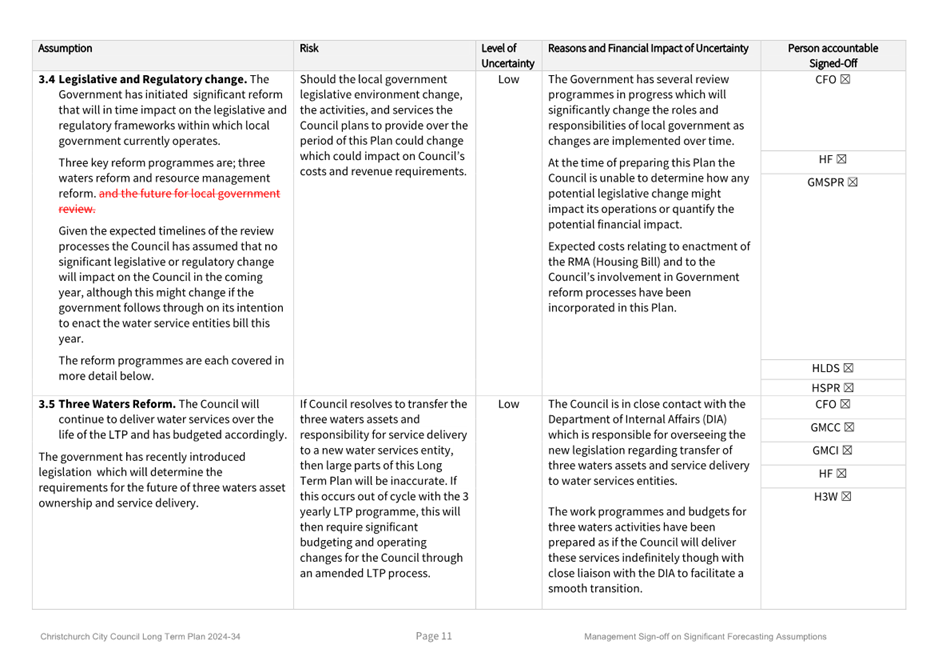

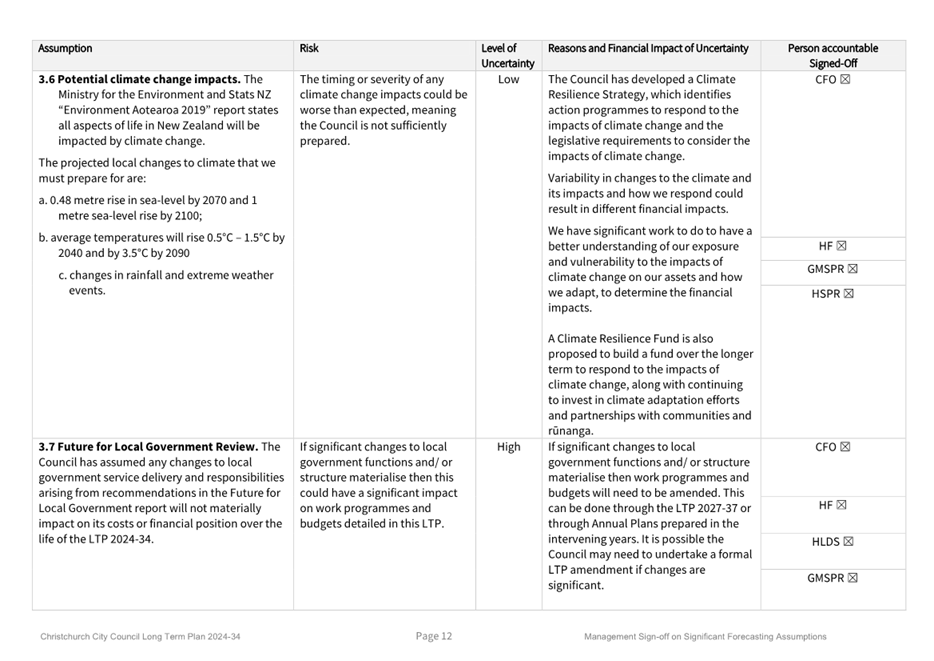

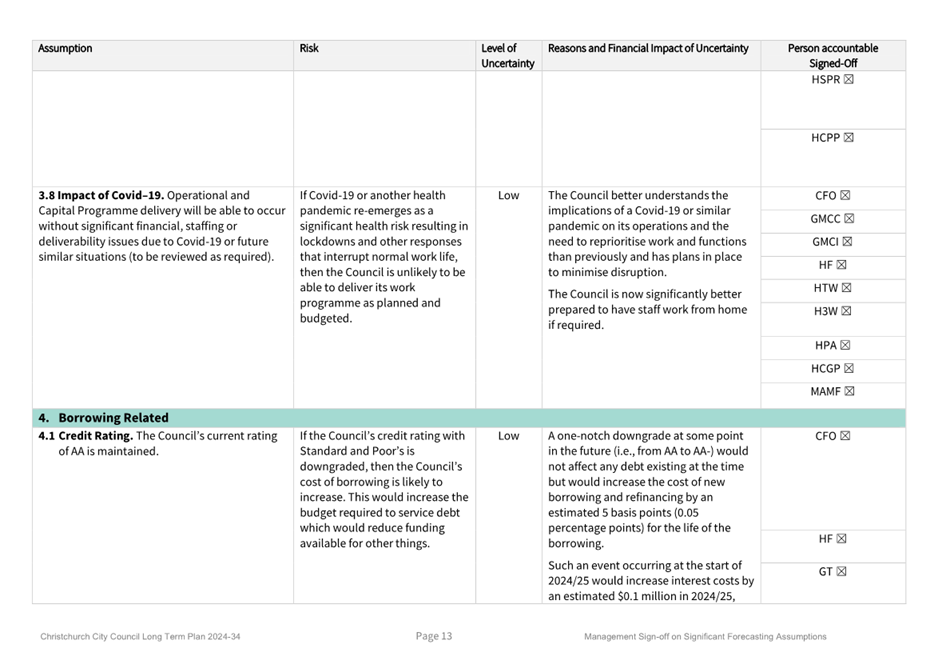

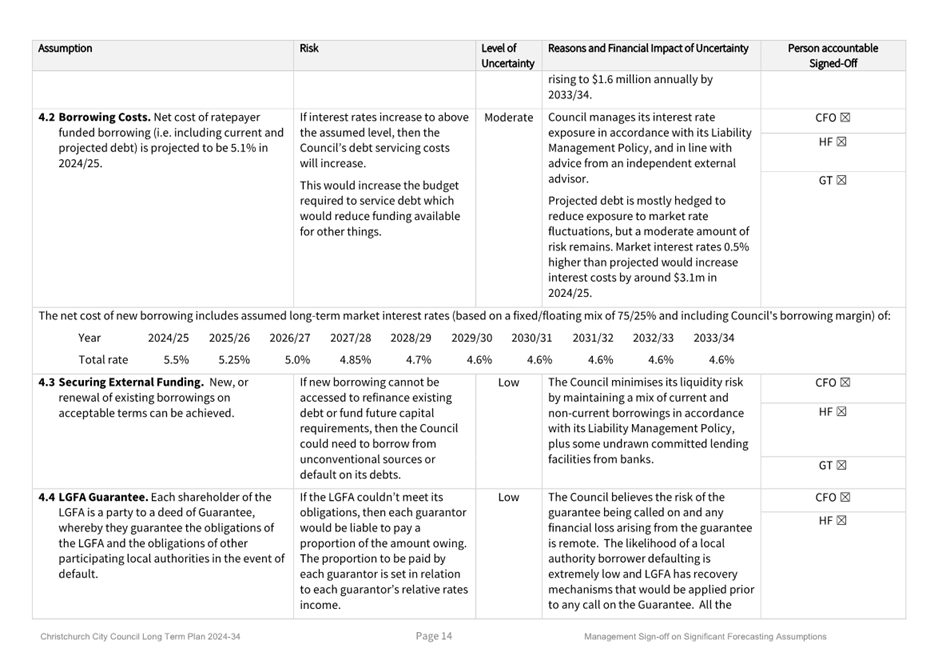

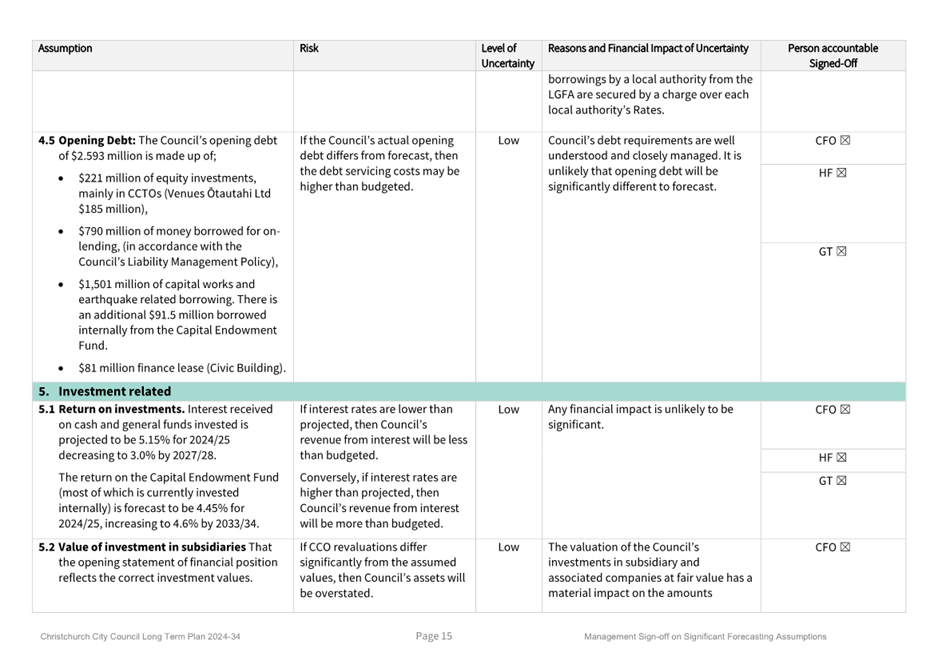

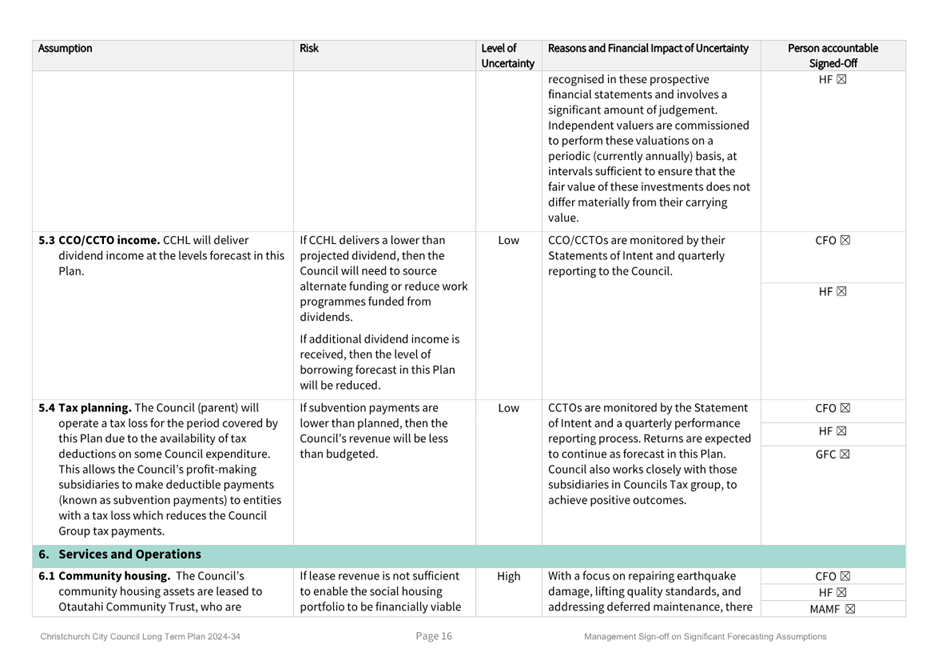

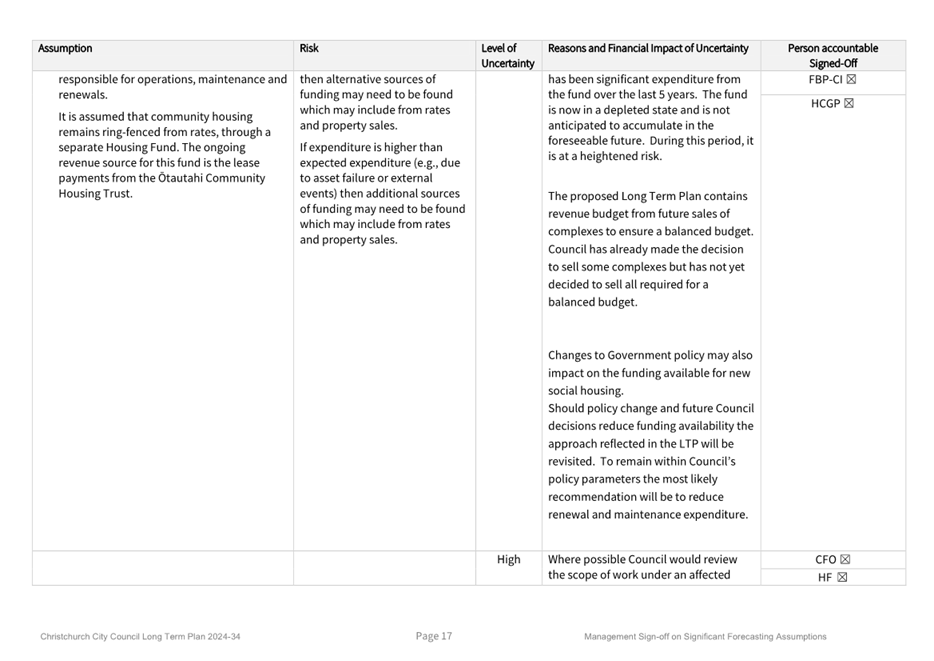

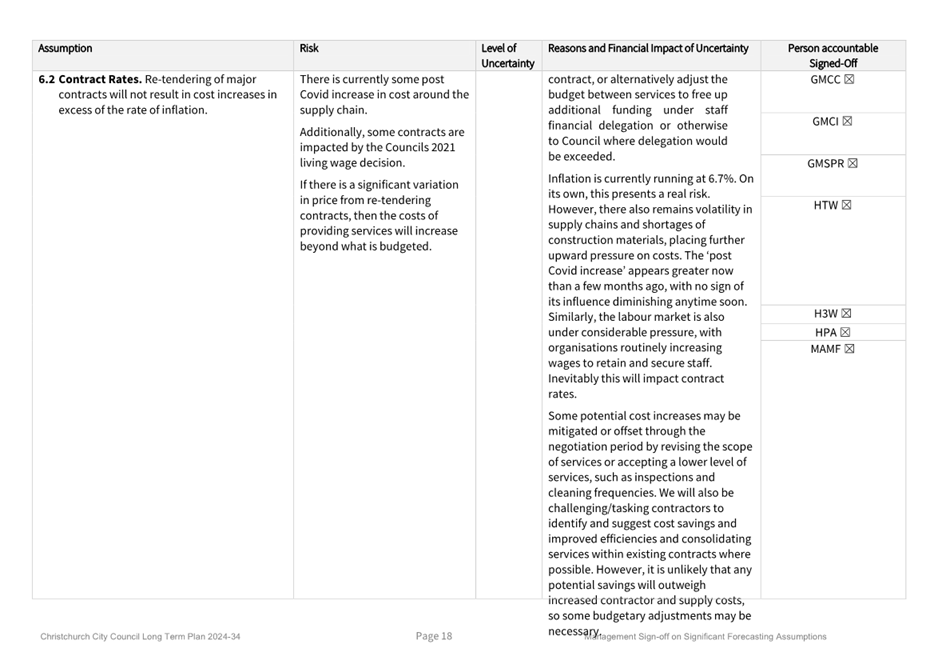

6. Significant Assumptions

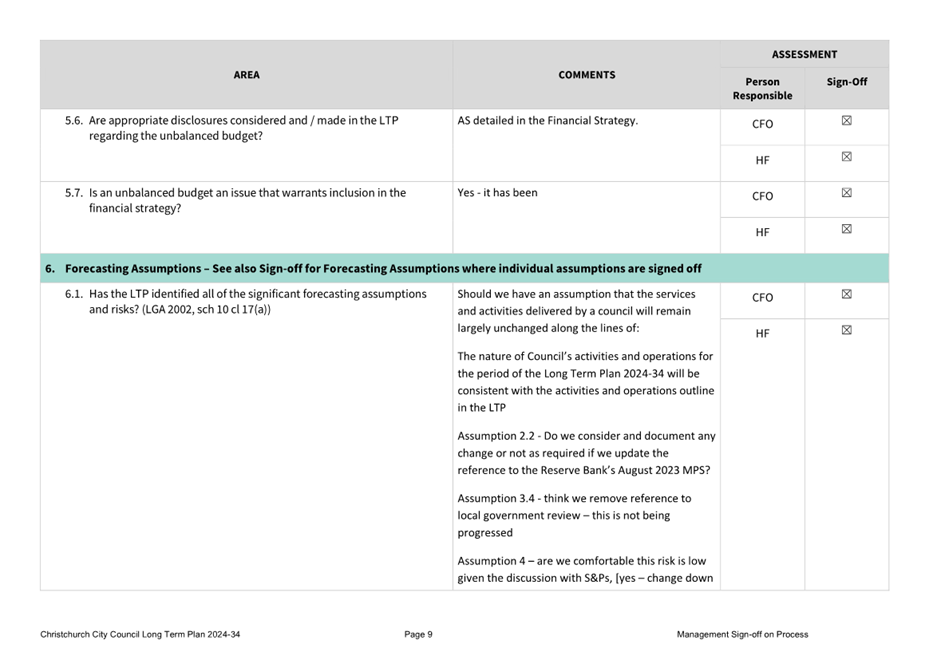

6.1 There

is no significant change from the draft. Assumptions are subject to a rigorous

sign-off process across the Council and results were reviewed by the Audit and

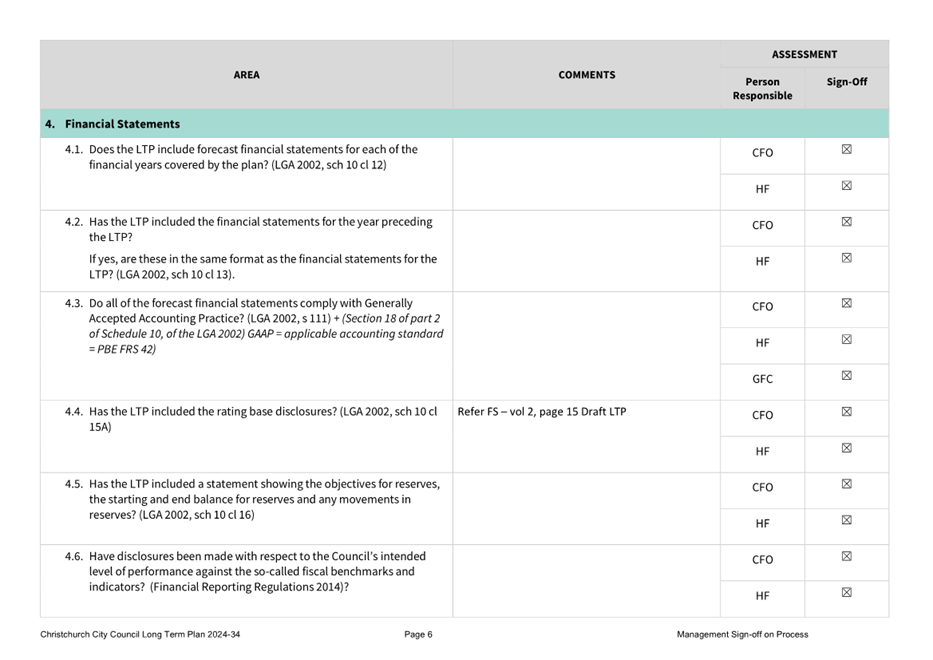

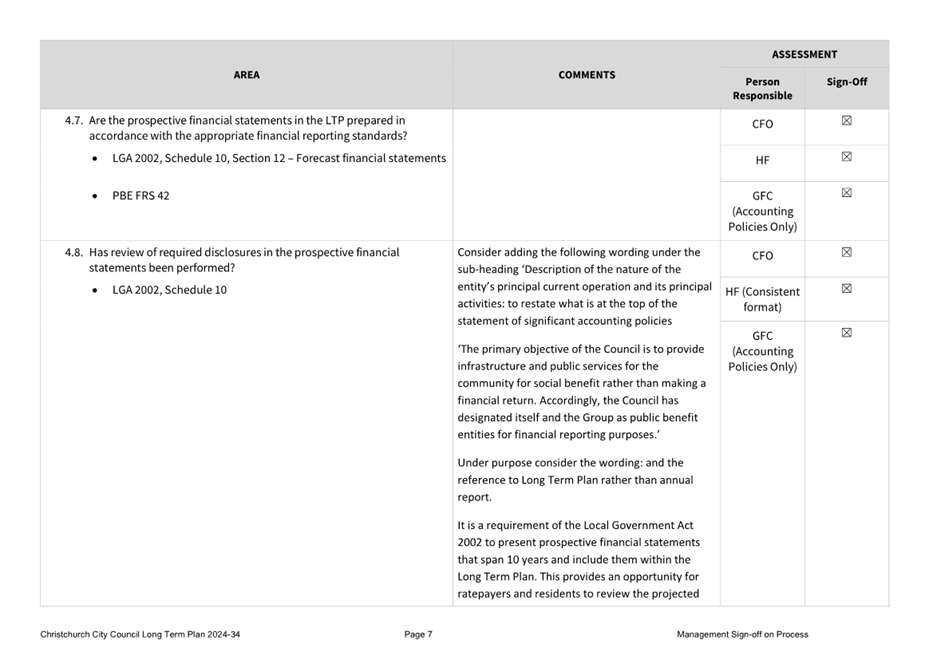

Risk Management Committee (Attachments L and M).

7. Financial Risk Management Strategy

7.1 The

Council’s policies to assist in managing its financial risk, including

liquidity and funding risk management, interest rate exposure and counterparty

credit risk are unchanged from the Draft. An important element in assessing the

value of the Council’s risk management strategy is its five key financial

ratios (two net debt, two interest and one liquidity). All key financial ratios

are expected to be met in all years of the LTP. These are included within the Financial Prudence Benchmarks.

7.2 The

Debt Servicing benchmark (borrowing costs as a percentage of revenue being less

than 10%) is not forecast to be met in any year of the LTP 2024-2034. This is

consistent with the Draft. It is forecast to range between 10.9% and 12.5% due

to projected interest rates, the level of borrowing on-lent to CCHL for

subsidiaries, and the borrowing for Te Kaha. Approximately one third of the

interest cost relates to on-lending to subsidiaries which generates offsetting

interest revenue that the ratio doesn’t consider. There is no concern

around the ability to service the debt.

7.3 The

Balanced Budget benchmark is forecast to be met in all years except 2026/27.

This is an improvement on the Draft which had the first three years unbalanced

due to deferring some of the increase in rating to fund asset renewals.

Councils Financial Strategy outlines the ongoing progress to fully rating for

renewals, ensuring in the medium term this benchmark is met. The LTP forecasts

are considered financially prudent having regard to the matters in section 100

of the LGA.

8. Fees and Charges

8.1 There

are five minor corrections/clarifications from the draft Fees and Changes

schedule outlined in Attachment K.

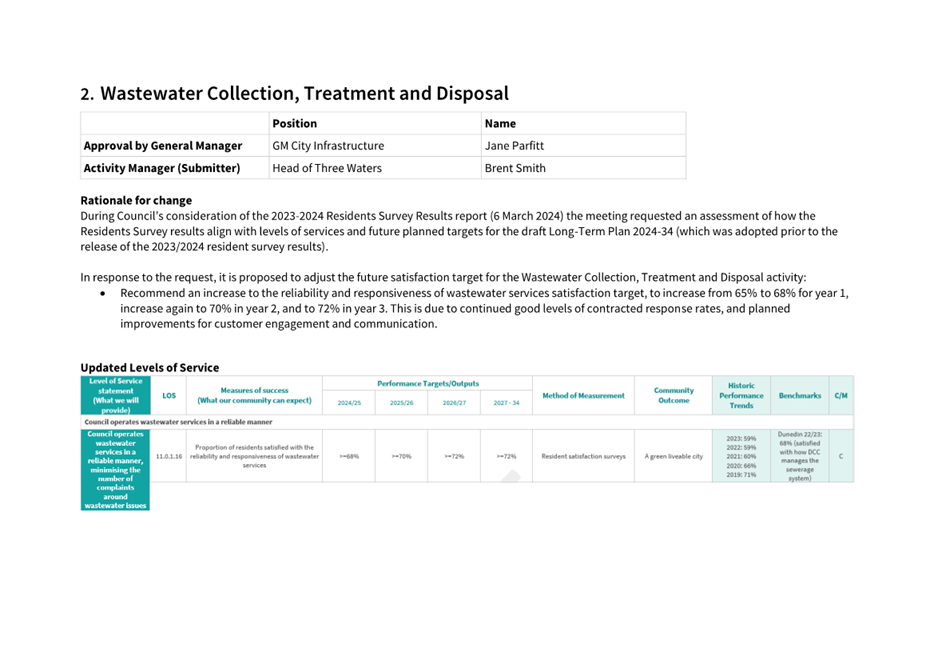

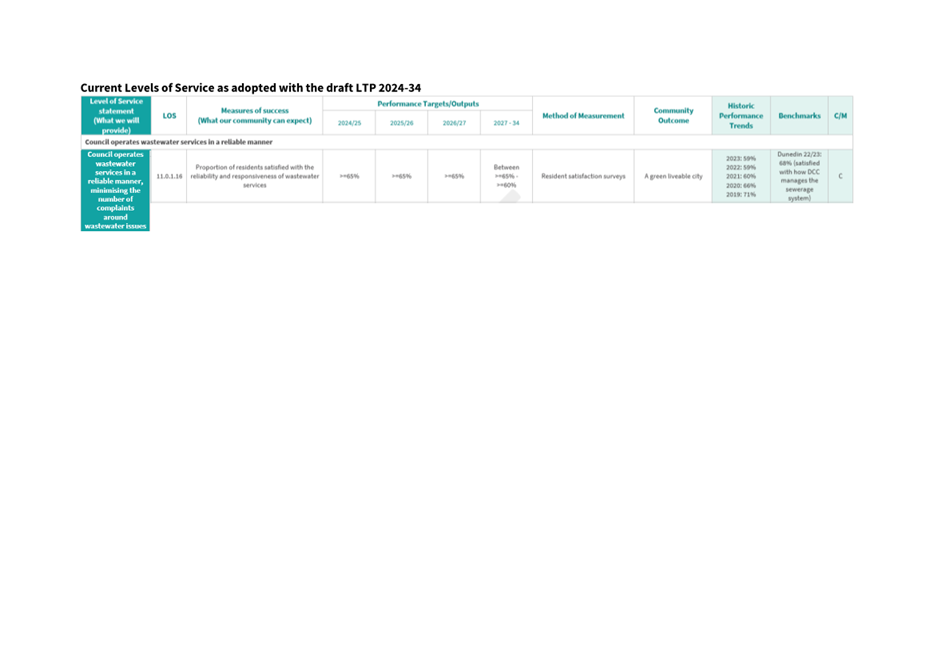

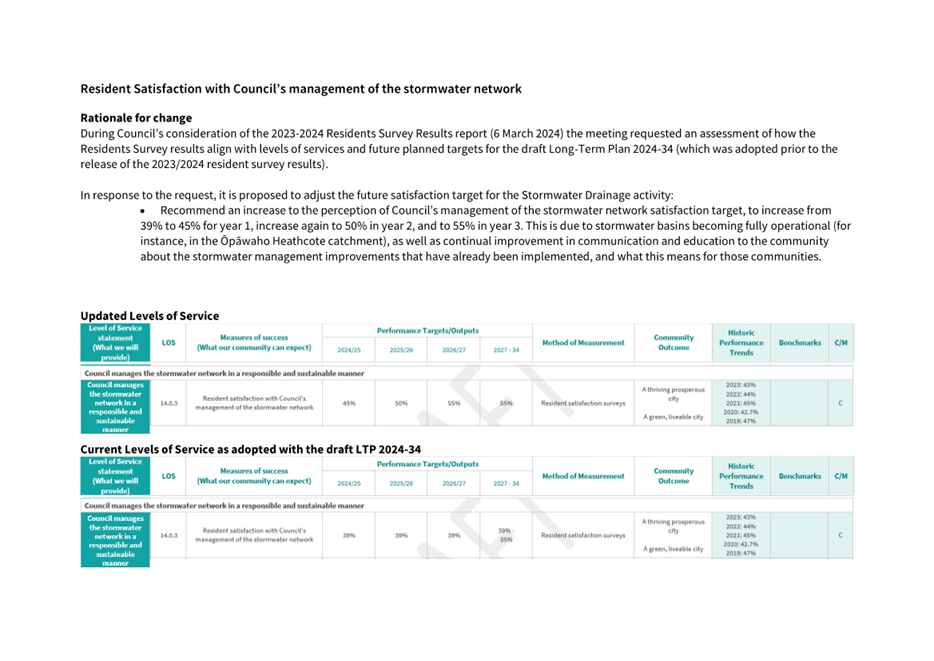

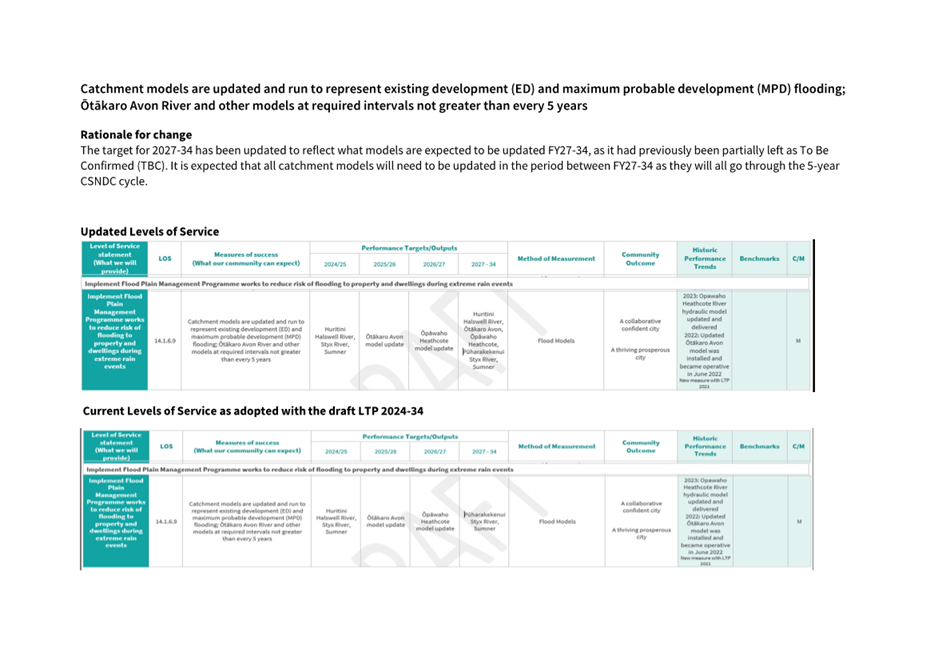

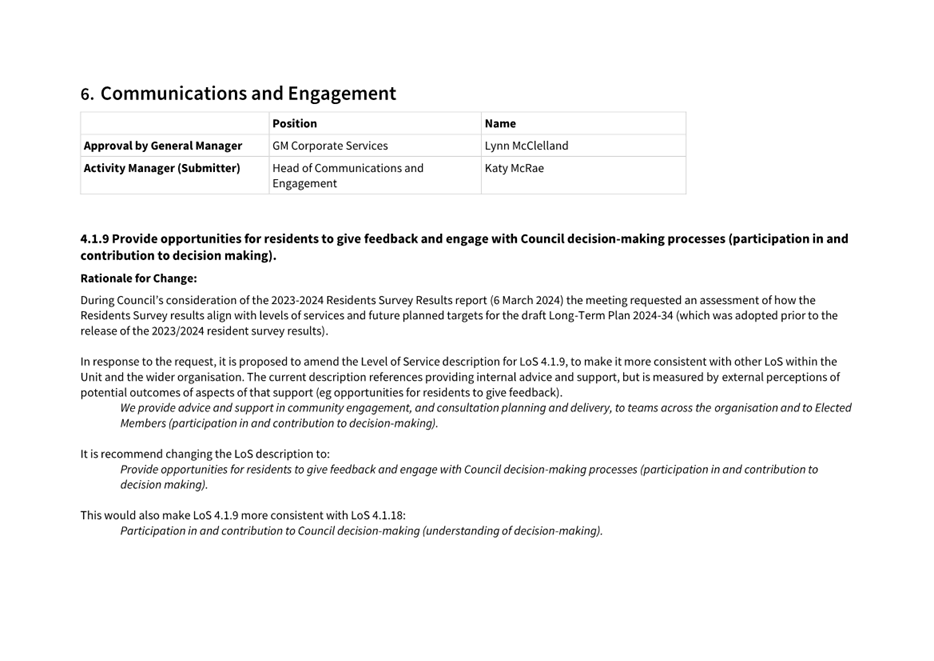

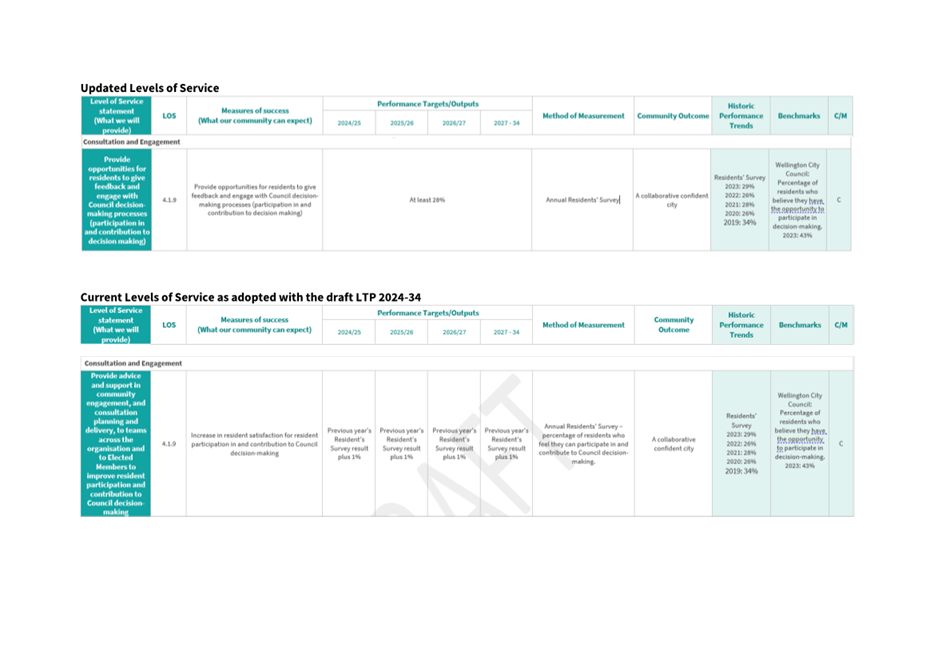

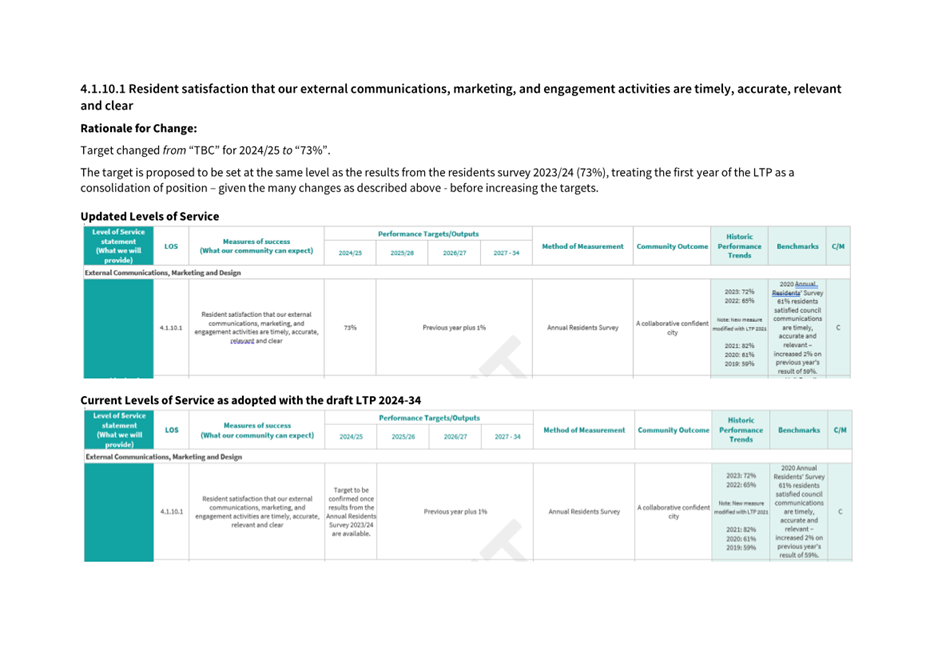

9. Changes to Levels of Service

9.1 Minor

changes and corrections to levels of service identified since the publication

of the draft LTP, including minor technical changes to some asset management

plans, are also set out in Attachment K. These include minor level of

service changes prompted by Council’s

consideration of the 2023-2024 Residents Survey Results report (6 March 2024 -

the meeting requested an assessment of how the Residents Survey results align

with levels of services and future planned targets for the draft LTP 2024-34

adopted prior to the release of the 2023/2024 resident survey results). They

also include updates for any targets marked as to be confirmed (tbc) during the

draft LTP process for which further information is now known.

10. Changes to Revenue, Financing and Rating Policies

10.1 The

following changes to Rating Policies are included in the recommended LTP:

10.1.1 The

definition of “Business” for the purpose of General Rates

differentials is clarified to explicitly include short-term un-hosted

accommodation (such as Air BnB, consistent with Resource Consent requirements),

and predominantly hosted short term accommodation.

10.1.2 The

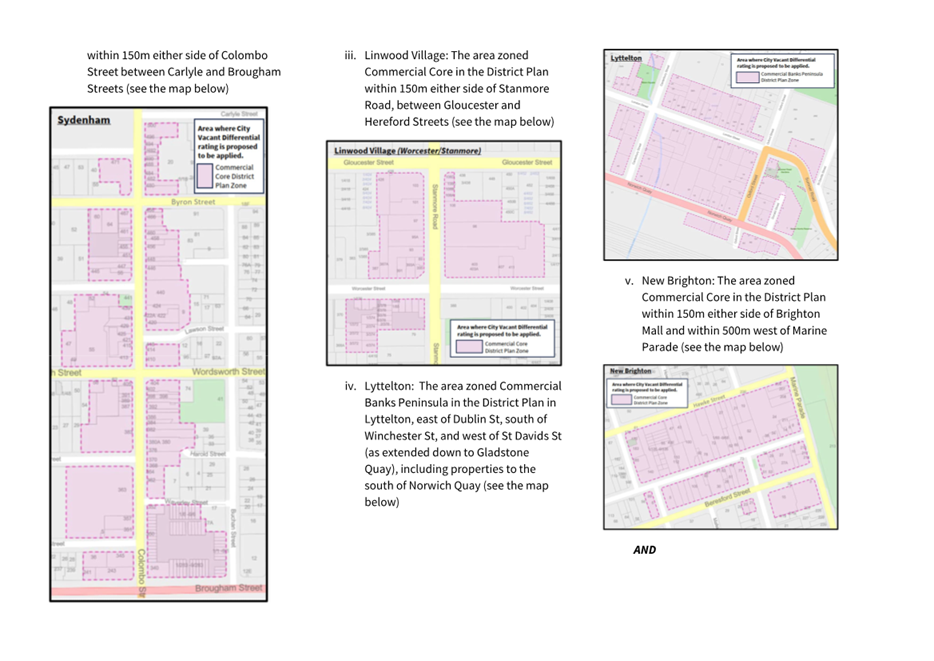

City Vacant differential on the General Rate is expanded to four suburban areas

(Linwood, Sydenham, New Brighton, and Lyttleton) in addition to the current CBD

area.

10.1.3 Active

Travel targeted rate is combined with the Uniform Annual General Charge.

10.1.4 Heritage

targeted rate is removed with funding for the heritage projects now from the

General Rate.

10.1.5 Rates

Remissions for community organisations may now be applied on a sliding scale

(rather than just “full remission or nothing”).

10.1.6 Rates

Postponements will no-longer be available on demand for pensioners (a financial

hardship test will be applied, the same as for younger ratepayers).

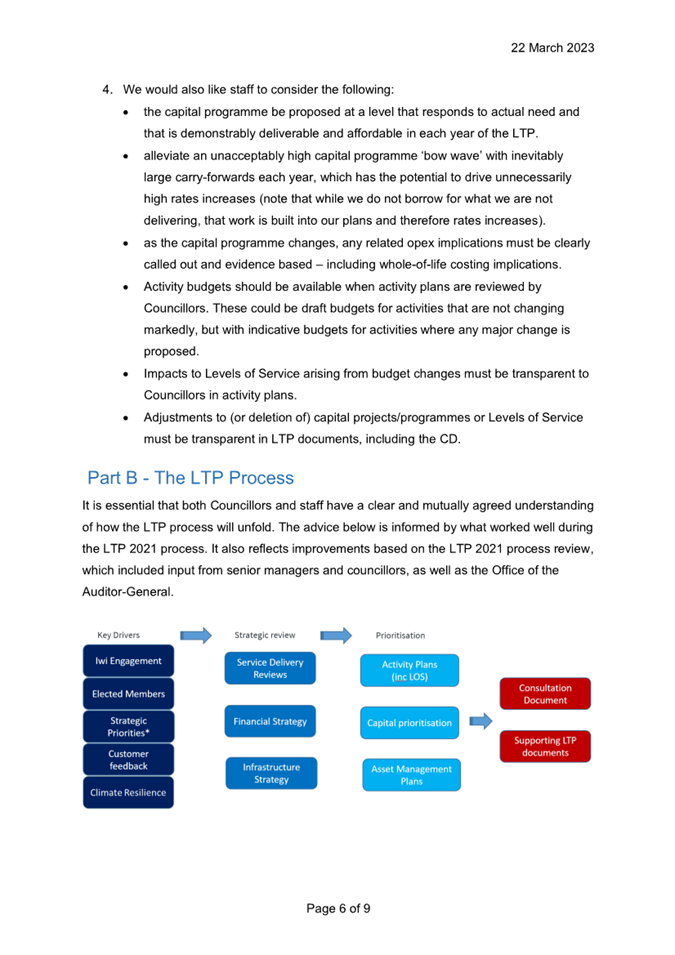

11. Long-term Plan Process

11.1 The

Council is required to prepare and adopt a LTP for each financial year (s.93)

Local Government Act 2002).

12. Considerations Ngā Whai Whakaaro

Risks and Mitigations Ngā Mōrearea me

ngā Whakamātautau

12.1 If

the LTP is not adopted in June 2024 and runs significantly later than planned

there are risks around loss of revenue and reputation. These have been set out

in full in the ARMC report.

Legal Considerations Ngā Hīraunga

ā-Ture

12.2 The

Local Government Act (LGA 2002) requires local authorities to adopt a LTP every

three years (s.93).

Strategy

and Policy Considerations Te

Whai Kaupapa here

12.3 The

required decisions:

12.3.1 Align with the Christchurch

City Council’s Strategic Framework.

12.3.2 Are assessed as

high significance based on the Christchurch City Council’s Significance

and Engagement Policy. The level of significance was determined by the:

· long-term nature of the decisions;

· number of people affected and/or with an interest;

· benefits/opportunities to the Council, ratepayers and wider

community of carrying out the decisions; and

· costs/risks to the Council, ratepayers and wider community

of carrying out the decisions.

12.3.3 The decisions

are consistent with Council’s Plans and Policies.

12.4 This

report supports the Council's

Long Term Plan (2021 - 2031):

12.5 Governance

12.5.1 Activity: Governance and decision-making

· Level of Service: 4.1.18 Participation in and contribution

to Council decision-making - Percentage of respondents who understand how

Council makes decisions: At least 34%

12.6 Internal Services

12.6.1 Activity: Performance Management and Reporting

· Level of Service: 13.1.1 Implement the Long Term Plan and

Annual Plan programme plan - Critical path milestone due dates in

programme plans are met.

Community

Impacts and Views Ngā Mariu ā-Hāpori

12.7 The

decisions affect all wards/Community Board areas.

12.8 The

views of all Community Boards have been considered by the Council.

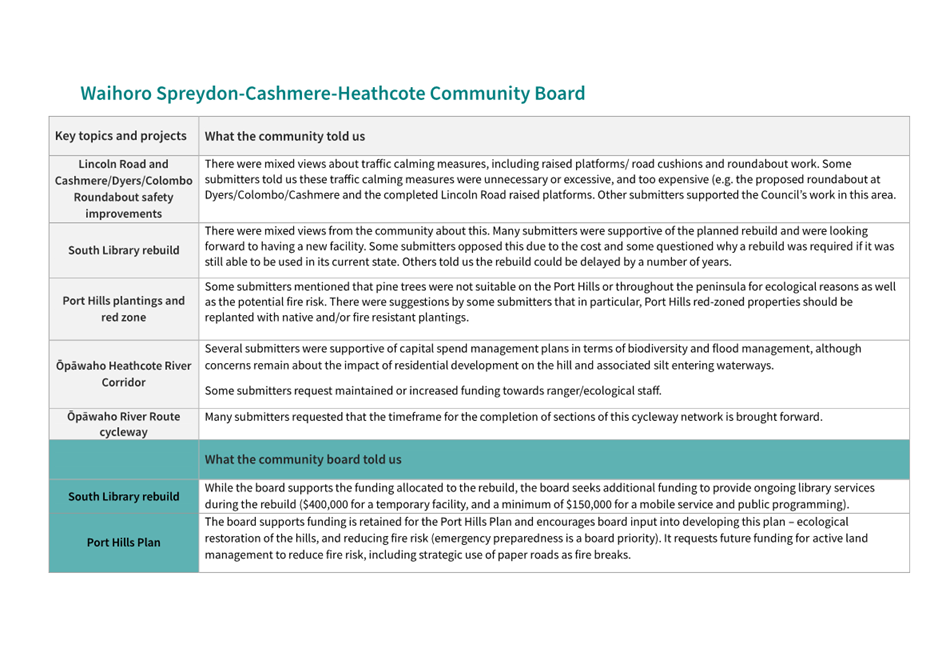

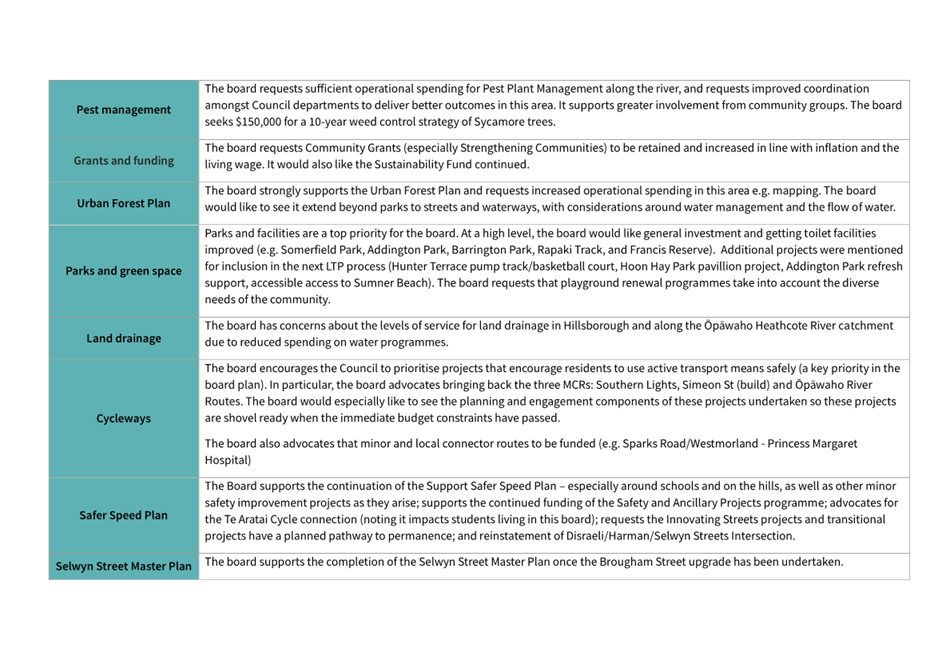

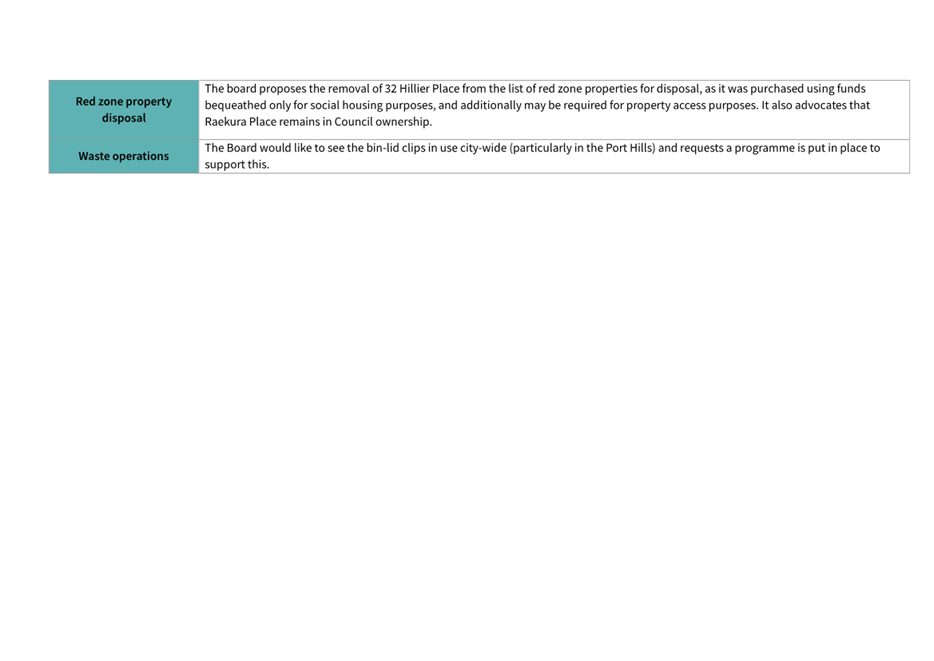

12.9 Each of the six Community Boards finalised a Community Board Plan in

May 2023. Each Plan identified key Community Board priorities that they

wish to achieve in the current electoral term and beyond. The Plans were

made available to Heads of Service to inform the development of Activity Plans.

12.10 Community

Board Chairs identified the top priorities within each Plan that they felt

should be funded in the draft 2024/34 LTP. These were presented to

Council on 11 October 2023. Following this staff undertook to incorporate

as many of the priorities as possible and report back to Community Boards and

Councillors. Staff reported back on 29 November 2023 advising that of the

24 priorities covered, 21 were funded and three were partially funded. A

commitment was made to discuss the partially funded priorities with the

respective Community Board in time to inform Board submissions to make to the

draft LTP.

12.11 Community

Boards submissions were then presented directly to Council at hearings on 2 May

2024, which have informed Council deliberations for the final LTP Christchurch

City Council Live - YouTube

Impact

on Mana Whenua Ngā

Whai Take Mana Whenua

12.12 The

decisions involve matters of interest to Mana Whenua and impact on our agreed

partnership priorities with Ngā Papatipu Rūnanga.

12.13 The Council

directly engages with the Papatipu Rūnanga who fall within the Council

catchment as mana whenua of respective rohe: Te Ngāi Tūāhuriri

Rūnanga, Te Hapū o Ngāti Wheke, Wairewa Rūnanga, Te

Rūnanga o Koukourārata, Ōnuku Rūnanga and Te Taumutu

Rūnanga.

Climate

Change Impact Considerations Ngā Whai Whakaaro mā te Āhuarangi

12.14 The

decisions in this report are likely to:

12.14.1 Contribute

positively to adaptation to the impacts of climate change.

12.14.2 Contribute

positively to emissions reductions.

12.15 The LTP

contains a focus on climate change response, with climate change considerations

embedded throughout the process. This was emphasised in the Mayor and

Councillor’s Letter of Expectation for the LTP and the Council’s

Strategic Priorities and Community Outcomes. Each Activity Plan includes a

description of how that part of Council will respond to climate impacts and

reduce its emissions. Climate change is also part of the Asset Management Plans

and Infrastructure and Financial Strategies. As a result, the LTP has an

emphasis on both mitigation and adaptation, with actions proposed across all

areas of Council.

13. Next Steps Ngā Mahinga ā-muri

13.1 Once

the Council has adopted the final Long Term Plan a local authority must, within

1 month after the adoption of its annual plan, make the plan publicly

available. This includes incorporating the decisions of Council made during

adoption, followed by design, publication and printing.

13.2 The

LTP publications will go on-line, while hard-copies will be distributed to the

National Library of New Zealand, Parliamentary Library, The Auditor General and

Governor General, and to our services centres and libraries.

13.3 Feedback

about the Council’s decisions will be provided to all submitters on the

draft LTP.

13.4 Council

systems will be updated with key content (adopted levels of service and

targets, capital projects, budgets) to enable and support performance reporting

to Finance and Performance Committee (monthly) and Council (Annual Report).

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a

|

LTP Memo from

Audit and Risk Management Committee (Under Separate Cover)

|

|

|

|

b

|

Audit NZ

report (Under Separate Cover)

|

|

|

|

c ⇩

|

The Mayor's

Recommendations

|

24/1036532

|

22

|

|

d ⇩

|

Changes to the

Council's capital programme (24/1041251)

|

24/1042849

|

27

|

|

e ⇩

|

Changes to the

Council's operating expenditure (24/949569)

|

24/1042850

|

28

|

|

f ⇩

|

Revenue and

Financing Policy

|

24/707205

|

29

|

|

g ⇩

|

Rates

Remission Policy

|

24/707238

|

57

|

|

h ⇩

|

Funding Impact

Statement

|

24/1041310

|

62

|

|

i ⇩

|

Financial

Strategy

|

24/262847

|

82

|

|

j ⇩

|

Infrastructure

Strategy

|

24/105908

|

97

|

|

k ⇩

|

Minor changes

to Levels of Service and Fees and Charges

|

24/800132

|

140

|

|

l ⇩

|

LTP 2024-34

Management Sign-offs for Process

|

24/1020591

|

184

|

|

m ⇩

|

LTP 2024-34

Management Sign-offs for Significant Forecasting Assumptions

|

24/1018009

|

199

|

|

n ⇩

|

Councillor's

Letter of Expectation LTP 2024

|

24/140762

|

218

|

|

o ⇩

|

Thematic

Analysis of the 2024-34 LTP submissions and hearings

|

24/894172

|

227

|

|

p ⇩

|

Council-Controlled

Organisations' exemption

|

24/1039104

|

283

|

|

q ⇩

|

LTP 2024-34

List of Properties for Disposal

|

24/1054243

|

284

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Christchurch

City Council Live - YouTube – recordings of all public

hearings/submissions to Council on the LTP 2024-34, held between 2 May and 13

May 2024.

Christchurch

City Council Long-term Plan Joint Development workshops for development of

the Draft LTP 2024-34, held between 25 July 2023 and 14 March 2024:

|

Date

|

Subject

|

|

14/03/24

|

Final Council meeting for adoption of

the Draft LTP 2024-34 and Consultation Document https://christchurch.infocouncil.biz/RedirectToDoc.aspx?URL=Open/2024/03/CLP_20240314_AGN_10191_WEB.htm

|

|

11/03/24

|

Third Council meeting for adoption of

the Draft LTP 2024-34 and Consultation Document https://christchurch.infocouncil.biz/RedirectToDoc.aspx?URL=Open/2024/03/CLP_20240311_AGN_10182_WEB.htm

|

|

27/02/24

|

Secondary Council meeting for adoption

of the Draft LTP 2024-34 & Consultation Document https://christchurch.infocouncil.biz/RedirectToDoc.aspx?URL=Open/2024/02/CLP_20240227_AGN_10161_WEB.htm

|

|

14/02/24

|

Primary Council meeting for adoption of

the Draft LTP 2024-34 and Consultation Document https://christchurch.infocouncil.biz/RedirectToDoc.aspx?URL=Open/2024/02/CLP_20240214_AGN_8503_AT_WEB.htm

|

|

|

Joint development briefings with the

Council held on the following dates:

Long Term Plan 2024-2034 | What matters most? |

Kōrero mai | Let’s talk (ccc.govt.nz)

· 30

and 23 Jan 2024

· 5

and 13 Dec 2023

· 7,

14, 21 and 27 Nov 2023

· 3,

10, 11, 17, 24 and 31 Oct 2023

· 1,

8, 15, 22 and 29 Aug 2023

· 5,

12 and 19 Sept 2023

· 25

July 2023

|

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

Peter Ryan -

Head of Corporate Planning & Performance

Bruce Moher -

Manager Corporate Reporting

Mitchell Shaw

- Reporting Accountant

Ron Lemm -

Manager Legal Service Delivery, Regulatory & Litigation

Steve Ballard

- Group Treasurer

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Bruce Moher -

Manager Corporate Reporting

Bede Carran -

General Manager Finance, Risk & Performance / Chief Financial Officer

Mary

Richardson - Interim Chief Executive

|