Audit and Risk Management Committee

Agenda

Notice of Meeting:

An ordinary meeting of the Audit and Risk

Management Committee will be held on:

Date: Thursday 8 February 2024

Time: 9.30 am

Venue: Committee Room 1, Level 2, Civic Offices,

53 Hereford Street, Christchurch

Membership

|

Chairperson

Deputy Chairperson

Members

|

Mr Michael Wilkes

Councillor Jake McLellan

Councillor Tyrone Fields

Councillor Sam MacDonald

Councillor Tim Scandrett

Mrs Hilary Walton

|

2 February 2024

|

|

|

Principal Advisor

Jane Parfitt

Interim General Manager Infrastructure

Planning & Regulatory

Tel: 941 8999

|

Luke Smeele

Democratic Services Advisor

941 6374

luke.smeele@ccc.govt.nz

www.ccc.govt.nz

|

Audit and Risk Management Committee

08 February 2024

|

|

Audit

and Risk Management Committee - Terms of Reference Ngā Ārahina Mahinga

|

Chair

|

Mr

Michael Wilkes (Independent)

|

|

Deputy Chair

|

Councillor

McLellan

|

|

Membership

|

Councillor Fields

Councillor MacDonald

Councillor Scandrett

External Members:

Mrs Hilary Walton

Ms Jacqueline Robertson Cheyne

|

|

Quorum

|

Half of the members if the

number of members (including vacancies) is even, or a majority of members if

the number of members (including vacancies) is odd.

|

|

Meeting

Cycle

|

Quarterly and

as required

|

|

Reports

To

|

Council

|

Purpose

To assist the Council to discharge

its responsibility to exercise

due care, diligence and skill in relation to the oversight of:

·

the robustness of the internal control framework;

·

the integrity and appropriateness of external reporting, and

accountability arrangements within the organisation for these functions;

·

the robustness of risk management systems, process and practices;

·

internal and external audit;

·

accounting policy and practice;

·

compliance with applicable laws, regulations, standards and best

practice guidelines for public entities; and

·

the establishment and maintenance of controls to safeguard the

Council’s financial and non-financial assets.

The foundations on which this

Committee operates, and as reflected in this Terms of Reference, includes:

independence; clarity of purpose; competence; open and effective relationships

and no surprises approach.

Procedure

·

In order to give effect to its advice the Committee should make recommendations to the Council and to

Management.

·

The Committee should meet the internal and the external auditors

without Management present as a standing agenda item at each meeting where

external reporting is approved, and at other meetings if requested by any of

the parties.

·

The external auditors,

the internal audit manager and the co-sourced internal audit firm should meet

outside of formal meetings as appropriate with the Committee Chair.

·

The Committee Chair

will meet with relevant members of Management before each Committee meeting and

at other times as required.

Responsibilities

Internal Control Framework

·

Consider the adequacy and effectiveness of internal controls and

the internal control framework including overseeing privacy and cyber security.

·

Enquire as to the steps management has taken to embed a culture

that is committed to probity and ethical behaviour.

·

Review the processes or systems in place to capture and

effectively investigate fraud or material litigation should it be required.

·

Seek confirmation annually and as necessary from internal and

external auditors, attending Councillors, and management, regarding the

completeness, quality and appropriateness of financial and operational

information that is provided to the Council.

Risk Management

·

Review and consider Management’s risk management framework

in line with Council’s risk appetite, which includes policies and

procedures to effectively identify, treat and monitor significant risks, and

regular reporting to the Council.

·

Assist the Council to determine its appetite for risk.

·

Review the principal risks that are determined by Council and

Management, and consider whether appropriate action is being taken by

management to treat Council’s significant risks. Assess the effectiveness

of, and monitor compliance with, the risk management framework.

·

Consider emerging significant risks and report these to Council

where appropriate.

Internal Audit

·

Review and approve the annual internal audit plan, such plan to

be based on the Council’s risk framework. Monitor performance against the

plan at each regular quarterly meeting.

·

Monitor all internal audit reports and the adequacy of

management’s response to internal audit recommendations.

·

Review six monthly fraud reporting and confirm fraud issues are

disclosed to the external auditor.

·

Provide a functional reporting line for internal audit and ensure

objectivity of internal audit.

·

Oversee and monitor the performance and independence of internal

auditors, both internal and co-sourced. Review the range of services provided

by the co-sourced partner and make recommendations to Council regarding the

conduct of the internal audit function.

·

Monitor compliance with the delegations policy.

External Reporting and

Accountability

·

Consider the appropriateness of the Council’s existing

accounting policies and practices and approve any changes as appropriate.

·

Contribute to improve the quality, credibility and objectivity of

the accounting processes, including financial reporting.

·

Consider and review the draft annual financial statements and any

other financial reports that are to be publicly released, make recommendations

to Management.

·

Consider the underlying quality of the external financial

reporting, changes in accounting policy and practice, any significant

accounting estimates and judgements, accounting implications of new and

significant transactions, management practices and any significant

disagreements between Management and the external auditors, the propriety of

any related party transactions and compliance with applicable New Zealand and

international accounting standards and legislative requirements.

·

Consider whether the external reporting is consistent with

Committee members’ information and knowledge and whether it is adequate

for stakeholder needs.

·

Recommend to Council the adoption of the Financial Statements and

Reports and the Statement of Service Performance and the signing of the Letter

of Representation to the Auditors by the Mayor and the Chief Executive.

·

Enquire of external auditors for any information that affects the

quality and clarity of the Council’s financial statements, and assess

whether appropriate action has been taken by management.

·

Request visibility of appropriate management signoff on the

financial reporting and on the adequacy of the systems of internal control;

including certification from the Chief Executive, the Chief Financial Officer

and the General Manager Corporate Services that risk management and internal

control systems are operating effectively;

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

·

Review and consider the Summary Financial Statements for

consistency with the Annual Report.

External Audit

·

Annually review the independence and confirm the terms of the

audit engagement with the external auditor appointed by the Office of the

Auditor General. Including the adequacy of the nature and scope of the audit,

and the timetable and fees.

·

Review all external audit reporting, discuss with the auditors

and review action to be taken by management on significant issues and

recommendations and report to Council as appropriate.

·

The external audit reporting should describe: Council’s

internal control procedures relating to external financial reporting, findings

from the most recent external audit and any steps taken to deal with such

findings, all relationships between the Council and the external auditor,

Critical accounting policies used by Council, alternative treatments of

financial information within Generally Accepted Accounting Practice that have

been discussed with Management, the ramifications of these treatments and the treatment

preferred by the external auditor.

·

Ensure that the lead audit engagement and concurring audit

directors are rotated in accordance with best practice and NZ Auditing

Standards.

Compliance with Legislation,

Standards and Best Practice Guidelines

·

Review the effectiveness of the system for monitoring the

Council’s compliance with laws (including governance legislation,

regulations and associated government policies), with Council’s own

standards, and Best Practice Guidelines.

Appointment of Independent Members

·

Identify skills required for Independent Members of the Audit and

Risk Management Committee. Appointment panels will include the Mayor or

Deputy Mayor, Chair of Finance & Performance Committee and Chair of Audit

& Risk Management Committee. Council approval is required for all

Independent Member appointments.

·

The term of the Independent members should be for three

years. (It is recommended that the term for independent members begins on

1 April following the Triennial elections and ends 31 March three years

later. Note the term being from April to March provides continuity for

the committee over the initial months of a new Council.)

·

Independent members are eligible for re-appointment to a maximum

of two terms. By exception the Council may approve a third term to ensure continuity

of knowledge.

Long Term Plan Activities

·

Consider and review the Long Term and Annual Plans before

adoption by the Council. Apply similar levels of enquiry, consideration,

review and management sign off as are required above for external financial

reporting.

Audit and Risk Management Committee

Forward Work Programme 2024

|

2023

|

Feb

|

Apr

|

Jun

|

Aug

|

Oct

|

Dec

|

|

Update Reports

|

·

LTP

Process Update

|

·

Risk

and Assurance

·

Procurement

·

Cyber

Security

·

Health

and Safety

|

· Risk and Assurance

· Major Litigation

· Health and Safety

|

· Risk and Assurance

· Procurement

|

· Risk and Assurance

· Cyber Security

· Health and Safety

|

· Risk and Assurance

· Procurement

· Major Litigation

· Health and Safety

|

|

Other Reports

|

|

· Te Kaha

|

· CCHL

|

|

|

|

|

Annual Report

|

·

Audit NZ Management

Report

|

·

External

Reporting and Audit Programme for 2023/24 Update

|

·

Audit

NZ Management Letter for current year interim audit

|

|

· Financial Statements and Annual Report

·

Update on critical

judgments, estimates & assumptions

|

|

|

Annual Plan

|

·

Draft

LTP

|

|

·

Final LTP

|

|

|

|

|

Audit and Risk Management Committee

08 February 2024

|

|

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

TABLE OF CONTENTS NGĀ IHIRANGI

C 1. Apologies Ngā Whakapāha.......................................................................... 9

B 2. Declarations of Interest Ngā Whakapuaki Aronga........................................... 9

C 3. Confirmation of Previous Minutes Te Whakaāe o te

hui o mua.......................... 9

B 4. Public Forum Te Huinga Whānui.................................................................. 9

B 5. Deputations by Appointment Ngā Huinga

Whakaritenga................................. 9

B 6. Presentation

of Petitions Ngā

Pākikitanga.................................................... 9

Staff Reports

C 7. LTP

2024-34 Update................................................................................. 15

C 8. Consideration

of the Council's Draft Long-term Plan LTP 2024-34 process....... 21

C 9. Resolution

to Exclude the Public................................................................ 70

|

Audit and Risk Management Committee

08 February 2024

|

|

1. Apologies Ngā Whakapāha

At the close of

the agenda no apologies had been received.

2. Declarations of Interest Ngā

Whakapuaki Aronga

Members are

reminded of the need to be vigilant and to stand aside from decision making

when a conflict arises between their role as an elected representative and any

private or other external interest they might have.

3. Confirmation of Previous Minutes Te

Whakaāe o te hui o mua

That the

minutes of the Audit and Risk Management Committee meeting held on Thursday, 7 December 2023 be

confirmed (refer page 10).

4. Public Forum Te Huinga Whānui

A period of up

to 30 minutes may be available for people to speak for up to five minutes on

any issue that is not the subject of a separate hearings process.

It is intended

that the public forum session will be held at <Approximate Time>

There were no public forum requests

received at the time the agenda was prepared

5. Deputations by Appointment Ngā Huinga

Whakaritenga

There were no

deputations by appointment at the time the agenda was prepared.

6. Petitions Ngā Pākikitanga

There were no

petitions received at the time the agenda was prepared.

|

Audit and Risk Management Committee

08 February 2024

|

|

Audit and Risk Management Committee

Open Minutes

Date: Thursday 7 December 2023

Time: 2.01pm

Venue: Council Chambers, Level 2, Civic Offices,

53 Hereford Street, Christchurch

Present

|

Chairperson

Members

|

Mr Michael Wilkes

Councillor Tyrone Fields

Councillor Sam MacDonald

Councillor Tim Scandrett

Mrs Hilary Walton

|

|

|

|

Principal Advisor

Russell Holden

Acting General Manager - Resources / CFO

Tel: 941 8999

|

Luke Smeele

Democratic Services Advisor

941 6374

luke.smeele@ccc.govt.nz

www.ccc.govt.nz

Part A Matters

Requiring a Council Decision

Part B Reports

for Information

Part C Decisions

Under Delegation

The agenda was dealt with in the following

order.

1. Apologies

Ngā Whakapāha

Part C

|

Committee Resolved ARCM/2023/00021

That the apologies received from

Jacqueline Robertson for absence and Councillor McLellan for lateness be

accepted.

Councillor

MacDonald/Councillor Fields Carried

|

|

Secretarial

Note: Councillor McLellan did not attend the

Meeting.

|

2. Declarations

of Interest Ngā Whakapuaki Aronga

Part B

There were no

declarations of interest recorded.

3. Confirmation

of Previous Minutes Te Whakaāe o te hui o mua

Part C

|

Committee Resolved ARCM/2023/00022

That the

minutes of the Audit and Risk Management Committee meeting held on Monday, 16

October 2023 be confirmed.

Councillor

MacDonald/Mrs Walton Carried

|

4. Public

Forum Te Huinga Whānui

Part B

There were no public forum presentations.

5. Deputations

by Appointment Ngā Huinga Whakaritenga

Part B

There were no deputations by appointment.

6. Presentation

of Petitions Ngā Pākikitanga

Part B

There was no presentation of petitions.

|

7. LTP

2024-34 Update

|

|

|

Committee Resolved ARCM/2023/00023

Officer Recommendation

Accepted without Change

Part C

That the Audit

and Risk Management Committee:

1. Receive the information in the LTP

2024-34 Update Report.

Councillor

MacDonald/Councillor Scandrett Carried

|

|

8. Procurement

and Contracts Unit FY24 Q1 Report

|

|

|

Committee Resolved ARCM/2023/00024

Officer Recommendation Accepted without

Change

Part C

That the Audit

and Risk Management Committee:

1. Receive the information in the Quarterly Procurement Report for

the months of July, August, September 2023 (FY2024 Q1 Report).

Mrs

Walton/Councillor Fields Carried

|

The public were re-admitted to the meeting

at 3.37pm.

Meeting

concluded at 3.38pm.

CONFIRMED

THIS 8th

DAY OF FEBRUARY 2023

Michael Wilkes

Chairperson

|

Audit and Risk Management Committee

08 February 2024

|

|

|

7. LTP

2024-34 Update

|

|

Reference / Te Tohutoro:

|

23/1667998

|

|

Report of / Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance

|

|

Senior Manager / Pouwhakarae:

|

Lynn

McClelland, Assistant Chief Executive Strategic Policy and Performance

(lynn.mcclelland@ccc.govt.nz)

|

1. Purpose and Origin of Report Te Pūtake Pūrongo

1.1 The purpose of this report is to provide an update on

progress against the approved LTP work programme to the Audit and Risk

Management Committee (ARMC), including any enterprise-level risks or

impediments to the project and its key workstreams.

1.2 Consideration and review of the Long Term and Annual Plan

processes before adoption by the Council is specified in the ARMC Terms

of Reference.

2. Officer Recommendations Ngā Tūtohu

That the Audit and Risk

Management Committee:

1. Receive the information in the Long Term Plan 2024-34

Update Report.

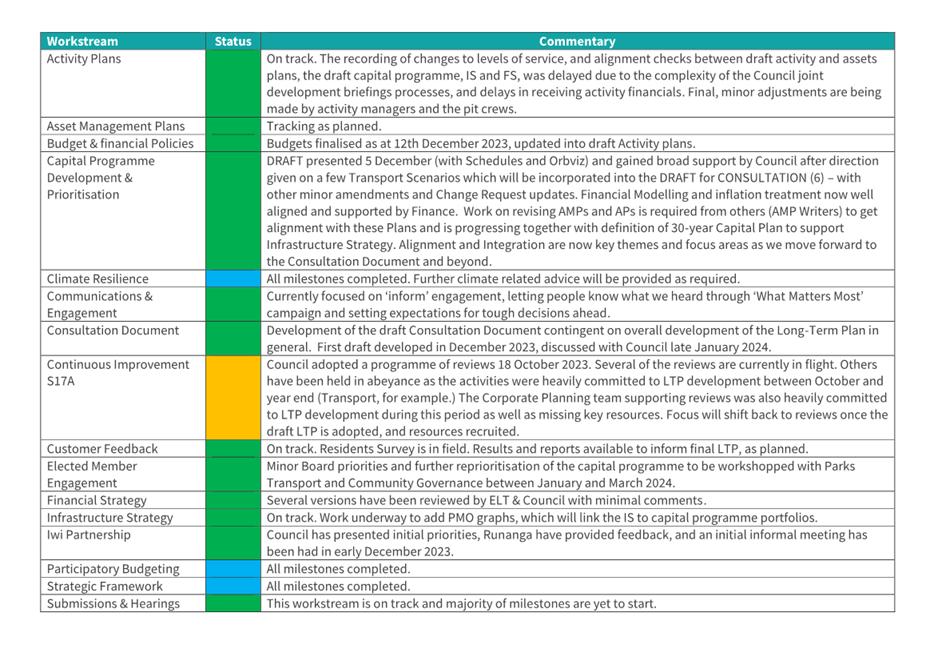

3. Brief Summary

3.1 The

ARMC has requested updates on the implementation of the

LTP 2024-34 development project plan workstreams, including an update on

key risks including mitigations (Attachment A).

4. Background Information Te Horopaki

4.1 Under

the Local Government Act 2002 a local authority must have an LTP in place at

all times. The structure, timing, information provided, and consultation

processes are defined by the legislation. LTPs are audited by the Office of the

Auditor-General through Audit NZ, and both draft and final LTPs are published

with the audit opinion.

4.2 The

flagship document of the LTP is the Consultation document (CD) which must set

out the challenges facing the city as well as the options and recommendations

of the Council for community consultation. This is the key document from

resident’s point of view.

4.3 It

is supported by Infrastructure and Financial Strategies that must have a

minimum horizon of 30 years. These too must set out the challenges, options and

recommendations that inform the LTP, as well as guiding the development of the

capital programme.

4.4 Supporting

these are technical documents (activity and asset management plans) that span

the Council’s services.

4.5 The

ARMC has requested regular updates on the implementation of the Long-term Plan

(LTP) 2024-34 development project plan.

4.6 At

the previous meeting of 7th December 2023 ARMC received:

4.6.1 LTP

2024-34 Project Update;

4.6.2 LTP

2024-34 Project risks, including how these are reported and managed.

4.7 This

latest LTP 2024 progress report (Attachment A) summarises (at a high level)

risks to the overall project work streams, as well as risks to specific work

streams. Enterprise-level risks are further underpinned by a suite of

operational risk assessments (management signoffs, significant assumptions

signoffs, and operational risks).

4.8 Each

work stream is led by an accountable Head of Service, and Heads of Service have

provided the information in these attachments. They will be available at the

ARMC meeting for further information as required.

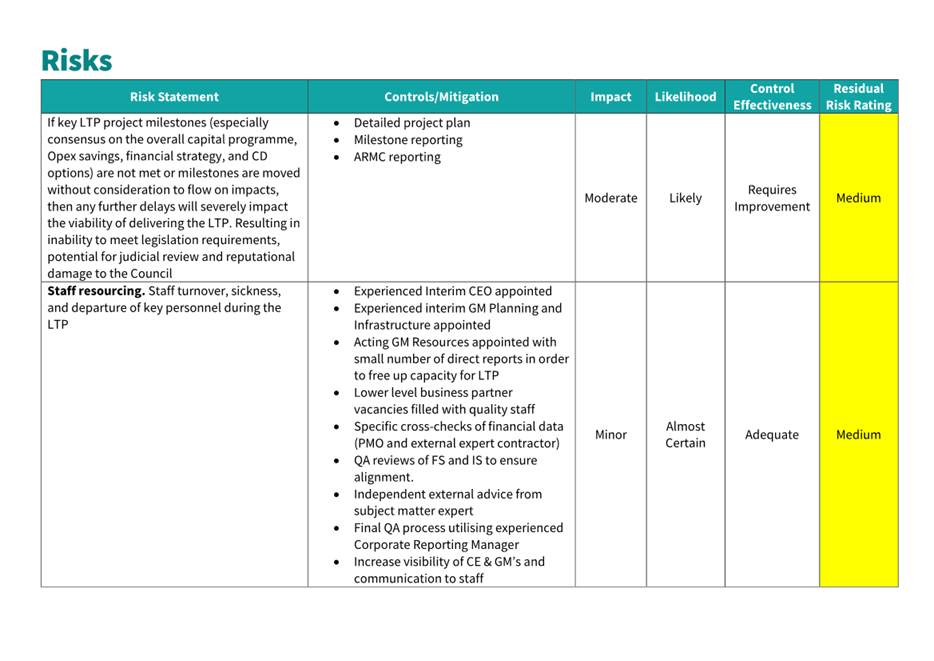

4.9 Project

risks have been identified that if realised will have significant impact on a

successful delivery of the LTP.

4.10 During

the development phase of the LTP the focus is naturally on content risk. The

areas of greatest risk lie (as they normally do) finding the optimum balance

between service delivery, capital programme delivery, and rates increases.

4.11 To

achieve this, it is essential to develop a Financial Strategy (FS) that is

aligned with the Infrastructure Strategy (IS) and activity plan budgets.

4.12 Alignment

of the FS with a significant savings opex programme and an

affordable/deliverable capital programme is also critical.

4.13 Finally,

the FS informs the way in which options for community consultation should occur

in the Consultation document.

4.14 Framing

these options in a way that can be easily understood by the community (and

which clearly set out the implications of those options) is critical to the

success of the LTP, and to minimise the risk of criticism or (successful)

challenge to the LTP process.

4.15 Operational

risk areas include confidence around asset condition and performance data, and

ability to meet the project milestones and timeline.

4.16 As

these issues are resolved (or substantively resolved), focus will move to

alignment risks.

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a ⇩

|

LTP 2024-34

Project Update

|

24/173554

|

18

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Confirmation of Statutory

Compliance Te Whakatūturutanga ā-Ture

|

Compliance with Statutory Decision-making

Requirements (ss 76 - 81 Local Government Act 2002).

(a) This report contains:

(i) sufficient information about all reasonably practicable

options identified and assessed in terms of their advantages and

disadvantages; and

(ii) adequate consideration of the views and preferences of

affected and interested persons bearing in mind any proposed or previous

community engagement.

(b) The information reflects the level of significance of the

matters covered by the report, as determined in accordance with the Council's

significance and engagement policy.

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Amber Tait -

Performance Analyst

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Lynn

McClelland - Assistant Chief Executive Strategic Policy and Performance

|

|

Audit and Risk Management Committee

08 February 2024

|

|

|

Audit and Risk Management Committee

08 February 2024

|

|

|

8. Consideration of the Council's

Draft Long-term Plan LTP 2024-34 process

|

|

Reference / Te Tohutoro:

|

24/96357

|

|

Report of / Te Pou Matua:

|

Peter

Ryan, Head of Corporate Planning & Performance

|

|

Senior Manager / Pouwhakarae:

|

Lynn

McClelland, Assistant Chief Executive Strategic Policy and Performance

(lynn.mcclelland@ccc.govt.nz)

|

1. Purpose and Origin of Report Te Pūtake Pūrongo

1.1 To enable ARMC to review, and provide advice to Council on,

the process and supporting documentation for preparation of the draft LTP

2024-34.

1.2 Consideration and review of the Long Term and Annual Plan

processes before adoption by the Council is specified in the ARMC Terms of

Reference.

2. Officer Recommendations Ngā

Tūtohu

That the Audit and

Risk Management Committee:

1. Notes it has reviewed key documentation in

respect of the information that provides the basis for adoption of the Draft Long-term Plan (LTP) 2024-34 by Council, including drafts of the:

a. Consultation Document;

b. Financial Strategy;

c. Infrastructure Strategy;

d. General checklists and sign-offs by

management, including significant forecasting assumptions; and

e. An early (work in progress) draft of the Draft

LTP 2024-34 adoption report to Council. This must remain public excluded until

the Council agenda goes live on 9 February 2024.

2. Recommends to the Council that in the

Committee’s opinion an appropriate process has been followed in the

preparation of Long-Term Plan 2024-34 information.

3. Reason for Report Recommendations Ngā Take mō te

Whakatau

3.1 Under

the Local Government Act 2002 a local authority must have an LTP in place at

all times. The structure, timing, information provided, and consultation

processes are defined by the legislation. LTPs are usually audited by the

Office of the Auditor-General through Audit NZ, and both draft (usually) and

final LTPs are published with the audit opinion.

3.2 It

should be noted that due to the change in central government and its revised

approach to Three Waters reform, councils across NZ have been offered the

option of not having their Consultation Documents contain a formal audit

opinion. This is an attempt to avoid complexity while the revision of Three

Waters legislation occurs. CCC has opted to utilise this provision. Oversight

and auditing of the LTP will still occur as usual, but adoption of the CD will

not depend on receipt of an audit opinion on that document.

3.3 The

flagship document of the LTP is the Consultation Document (CD) which must set

out the challenges facing the city as well as the options and recommendations

of the Council for community consultation. This is the key document from

residents’ point of view.

3.4 It

is supported by Infrastructure and Financial Strategies that must have a

minimum horizon of 30 years. These too must set out the challenges, options and

recommendations that inform the LTP, as well as guiding the development of the

capital programme.

3.5 Supporting

these are technical documents (activity and asset management plans) that span

the Council’s services.

3.6 Regular

updates have been provided to the Finance & Performance Committee and the Audit

& Risk Management Committee (ARMC) on the risks to and implementation of

the LTP 2024-34 development project plan (the most recent to ARMC being 7

December 2023) on both the process and draft content of the developing LTP.

(See next LTP Update report going to this same ARMC meeting.)

3.7 The

purpose of this report is to enable the Audit & Risk Management Committee

to review the process and all documentation for preparation of the Draft LTP

2024-34, to recommend to Council that an appropriate process has been followed

in the preparation of the information.

3.8 This

draft LTP has been developed to meet the requirements of the Mayor and

Councillors as set out in the Letter of Expectation to staff (Attachment G)

which set out priorities to be addressed, as well as defining the LTP 2024-34

process. The letter and other key project information was originally received

by ARMC at the meeting of 20 June 2023.

3.9 The

LTP project team is chaired by the Assistant Chief Executive. The LTP process

was reviewed with Councillors, other stakeholders and key staff at the

conclusion of the LTP 2021-31 and subsequent Annual Plans and agreed

improvements have been included into the latest process (received by ARMC). The

process has also been tested against Taituarā (industry best-practice)

guidance and through regular briefings with other councils, as well as guided

by the councillor’s Letter of Expectation, which is highly specific on

process.

3.10 In

line with the Letter, Council staff held a series of joint development

workshops with the Mayor and Councillors to obtain overall direction as well as

fine-tuning specific details. These commenced in March 2023 and concluded in

January 2024.

3.11 One

key improvement identified from previous processes was to make these LTP joint

development briefings accessible to the public. This was achieved through

advertising key joint development briefing dates where the public could attend

(public and live-streamed), and the recording and releasing of all briefing

recordings, content and briefing notes - made available through Long

Term Plan 2024-2034 | What matters most? | Kōrero mai | Let’s talk

(ccc.govt.nz)

3.12 These

briefings provided opportunities for Councillors to discuss their priorities

for the draft Long-term Plan 2024 and their expectations for matters such as

rates increases, level of debt, financial headroom, the capital works

programme, levels of service and detailed savings options.

3.13 The

guidance received from Council during these briefings crossed all services, but

the key guidance was around an acceptable range of rates increase, to maintain

levels of service, and to ensure that the capital programme is deliverable

across all years of the LTP.

3.14 Having

obtained specific guidance and advice from Councillors, staff proceeded to

build a report and attachments for the adoption of the Draft Long-term Plan

2024-34. The process for preparing the information has been the subject of a

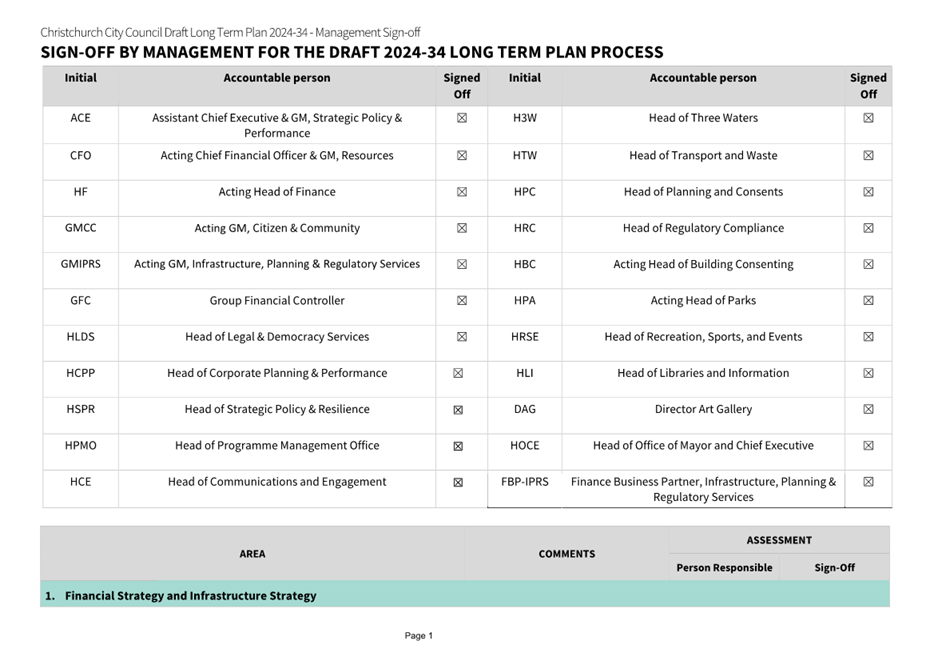

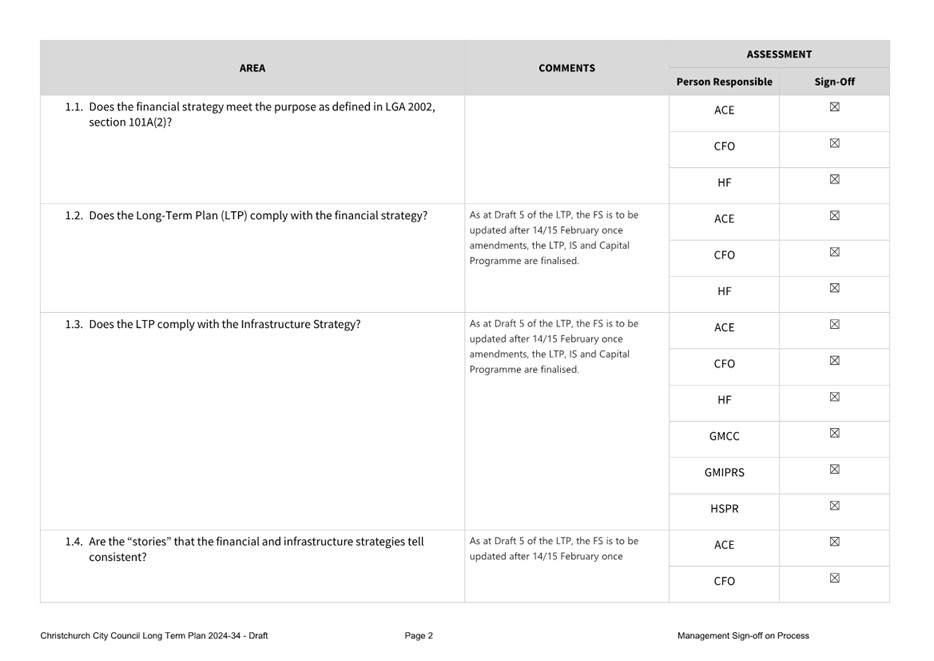

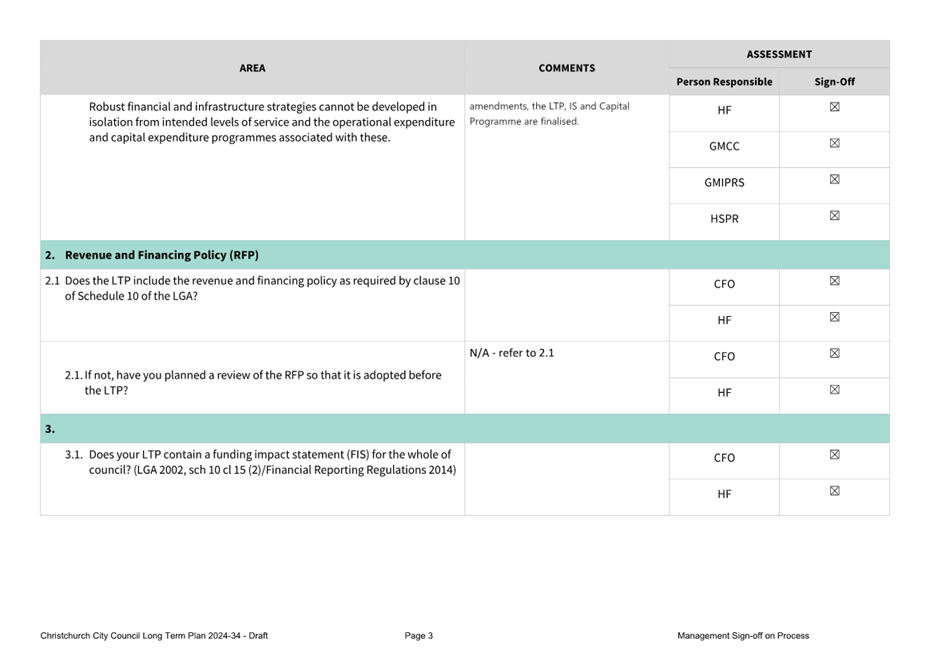

detailed series of management sign offs – including signoffs by members

of the Executive Leadership Team - that demonstrate compliance with the

Council’s statutory, financial, and legal obligations.

3.15 The

management and significant assumptions checklists and sign-off schedules are

attached to this report (Attachments D and E, respectively).

3.16 Also

as part of LTP development, Audit NZ recommended completion of their LTP

Self-Assessment review (results supplied to ARMC to the meeting of 16 October

2023.)

3.17 Early,

in-development drafts of key Long-term Plan content and the draft adoption

report are attached. These work-in-progress drafts must remain public-excluded

until the Draft Long-term Plan 2024-34 adoption report agenda to Council is

formally released on 9 February 2024.

3.17.1 Draft

Consultation document – Attachment A

3.17.2 Draft

Financial Strategy – Attachment B

3.17.3 Draft

Infrastructure Strategy – Attachment C

3.17.4 Early

draft of the Draft LTP 2024-34 adoption report to Council (all other supporting

documentation is to be attached or linked to from the Council report in time

for agenda release, noting a link to the public web will not go live until 9

February 2024) – Attachment F.

3.18 Staff

do not anticipate any significant or material changes between the release of

the ARMC agenda and attachments for this meeting of 8 February and the release

of the Council LTP agenda for their meeting of 14 February 2024.

3.19 Council

will meet to consider and adopt the Draft Long-term Plan on 14 February 2024,

to be followed by community consultation. (For further key project dates see

10.2 below.) The Consultation Document is the primary mechanism for this and

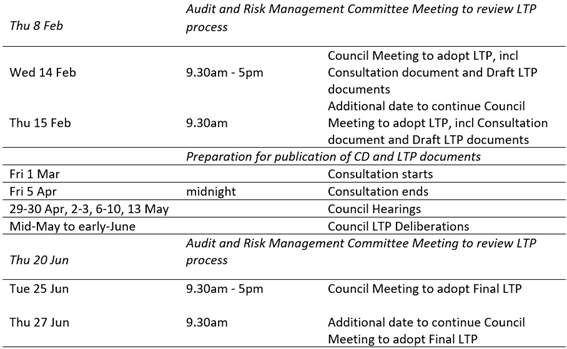

will reflect the decisions of Council made on 14 February 2024.

3.20 Consultation

will include a submissions process as well as feedback generated on social

media. There will also be an opportunity for members of the community to

present directly to Councillors.

4. Alternative Options Considered Ētahi atu Kōwhiringa

4.1 No

alternative options are proposed.

5. Detail Te Whakamahuki

5.1 As

the Draft Long-term Plan evolved between election of Council (October 2022) and

January 2024, Council staff held a series of workshops with the Mayor and

Councillors, and Community Board members, all of whom have had the opportunity

to contribute to the preparation of the plan.

5.2 Decisions in the Draft LTP 2024-34 adoption report affect the

following wards/Community Board areas:

5.2.1 All wards, Community Board areas.

6. Policy Framework Implications Ngā Hīraunga ā- Kaupapa here

Strategic

Alignment Te Rautaki

Tīaroaro

6.1 The Council must, at all times, have a long-term

plan; must use the special consultative procedure in adopting a long-term plan;

the long-term plan must be adopted before the commencement of the first year to

which it relates, and continue in force until the close of the third

consecutive year to which it relates (s.93(1-3)) Local Government Act 2002).

6.2 This report supports the Council's

Long Term Plan (2021 - 2031):

6.3 Internal Services

6.3.1 Activity: Performance Management and

Reporting

· Level of Service: 13.1.1 Implement the Long Term

Plan and Annual Plan programme plan - Critical path milestone due dates

in programme plans are met.

Policy

Consistency Te Whai

Kaupapa here

6.4 The

decision is consistent with Council’s Plans and

Policies.

Impact

on Mana Whenua Ngā

Whai Take Mana Whenua

6.1 The

decision involves a matter of interest to Mana Whenua

and could impact on our agreed partnership priorities with Ngā Papatipu Rūnanga.

6.2 Through the Te Hononga Committee the Council directly engages with

iwi – Te Rūnanga o Ngāi Tahu, and six of the Papatipu

Rūnanga who fall within the Council catchment as mana whenua of respective

rohe: Te Ngāi Tūāhuriri Rūnanga, Te Hapū o Ngāti

Wheke, Wairewa Rūnanga, Te Rūnanga o Koukourārata, Ōnuku

Rūnanga and Te Taumutu Rūnanga.

Climate

Change Impact Considerations Ngā Whai Whakaaro mā te Āhuarangi

6.3 The decisions in this report are likely to:

6.6.1 Contribute positively to adaptation to the

impacts of climate change.

6.6.2 Contribute positively to emissions reductions.

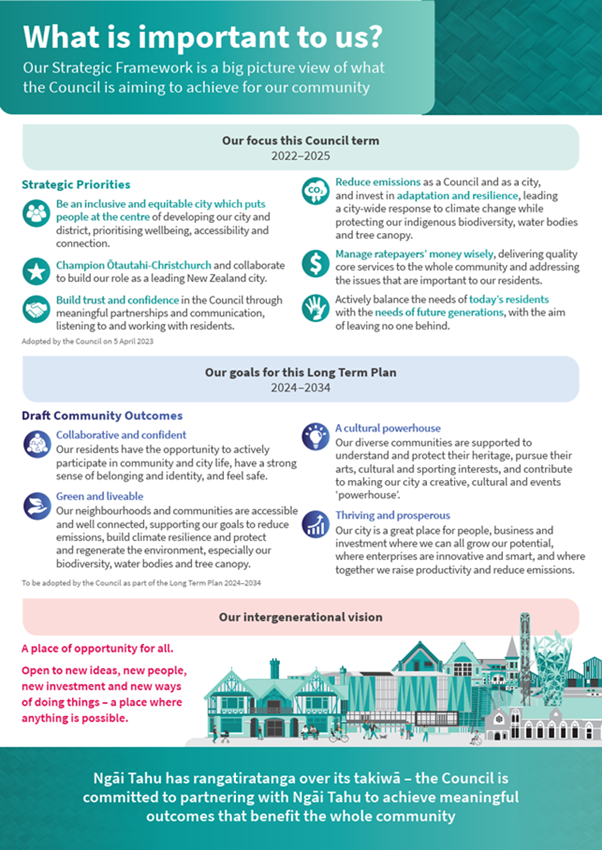

6.4 The LTP contains a focus on climate change response, with climate

change considerations embedded throughout the process. This is emphasised in

the Mayor’s Letter of Expectation for the LTP and the Council’s

Strategic Priorities and Community Outcomes. Each Activity Plan includes a

description of how that part of Council will respond to climate impacts and

reduce its emissions. Climate change is also part of the Asset Management

Plans, Infrastructure and Financial Strategies and Capital Programme.

6.5 As a result, the LTP has an emphasis on both mitigation and

adaptation, with actions proposed across all areas of Council. Pre-engagement

consultation undertaken with the community on the LTP asked ‘What Matters

Most?’

6.6 This engagement found that climate change is a top priority for

Christchurch residents across all different ages, ethnicities, and areas of our

community. The Consultation Document expands on this by providing further

climate action options for our community to consider.

Accessibility

Considerations Ngā

Whai Whakaaro mā te Hunga Hauā

6.10 N/A

7. Resource Implications Ngā Hīraunga Rauemi

Capex/Opex Ngā Utu Whakahaere

7.1 Cost

to Implement – unclear. The Letter of

Engagement has yet to be received from Audit NZ (it is pending advice from the

Office of the Auditor-General) so costs of the LTP audit are not known.

7.2 Maintenance/Ongoing

costs - within existing budget.

7.3 Funding

Source - existing budget per Council's Long-term Plan

(2021 - 2031).

Other He mea anō

7.4 None

8. Legal Implications Ngā Hīraunga ā-Ture

Statutory power to undertake proposals in the report

Te Manatū Whakahaere Kaupapa

8.1 The Council must, at all times, have a long-term plan; must

use the special consultative procedure in adopting a long-term plan; the

long-term plan must be adopted before the commencement of the first year to

which it relates, and continue in force until the close of the third

consecutive year to which it relates (s.93(1-3)) Local Government Act 2002).

Other Legal Implications Ētahi atu

Hīraunga-ā-Ture

8.2 There is no legal context, issue or implication relevant to

this decision, other than that which has been considered as part of the Draft

Long-term Plan management process and sign-offs.

9. Risk Management Implications Ngā Hīraunga Tūraru

9.1 Risks have been identified and managed through regular LTP

Project Update reporting to the project team, ELT and ARMC. This is underpinned

by a suite of four risk management tools, managed in partnership with the Risk

and Assurance Unit – an enterprise-level risk register, detailed

management signoffs, significant assumptions sign-offs, and operational risk

register.

10. Next Steps Ngā Mahinga ā-muri

10.1 The

Council will meet on 14 February 2024 to consider and formally adopt the

Consultation document and draft Long-term Plan 2024-2034 for consultation.

10.2 The

remaining key project milestones for the LTP 2024 are summarised as follows:

Attachments Ngā Tāpirihanga

|

No.

|

Title

|

Reference

|

Page

|

|

a

|

Draft

Consultation document (Under Separate Cover) - Confidential

|

24/172760

|

|

|

b

|

Draft

Financial Strategy (Under Separate Cover) - Confidential

|

23/2048736

|

|

|

c

|

Draft

Infrastructure Strategy (Under Separate Cover) - Confidential

|

24/105908

|

|

|

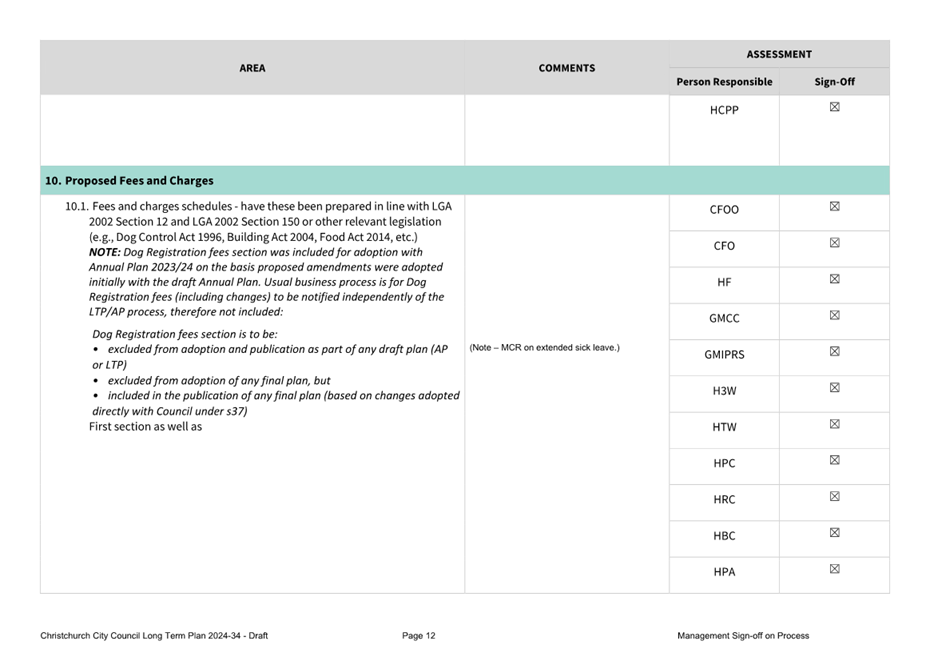

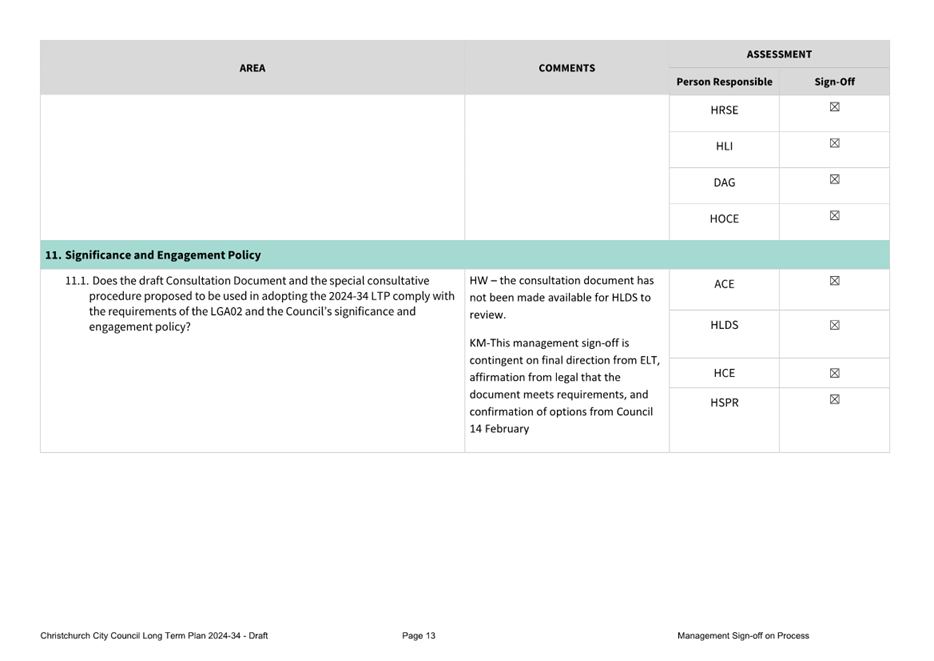

d ⇩

|

Draft LTP

2024-34 - Management Sign-off for Process

|

24/171782

|

28

|

|

e ⇩

|

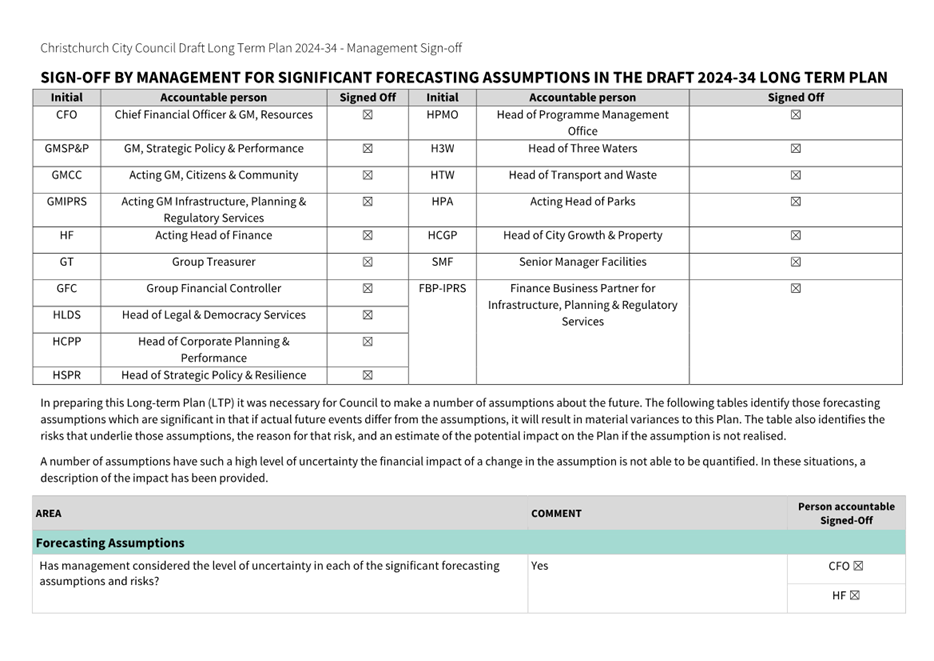

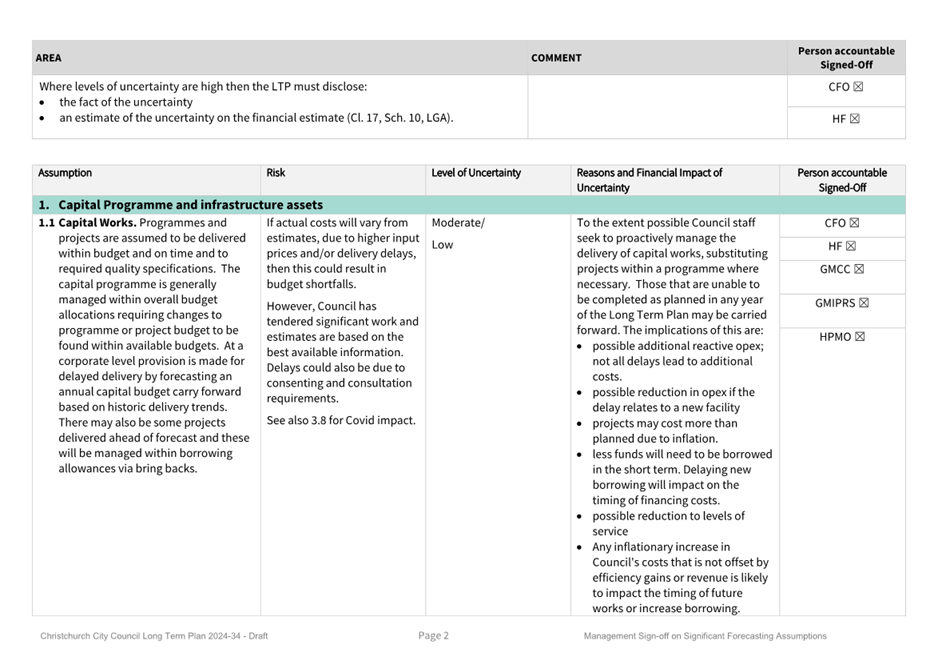

Draft LTP

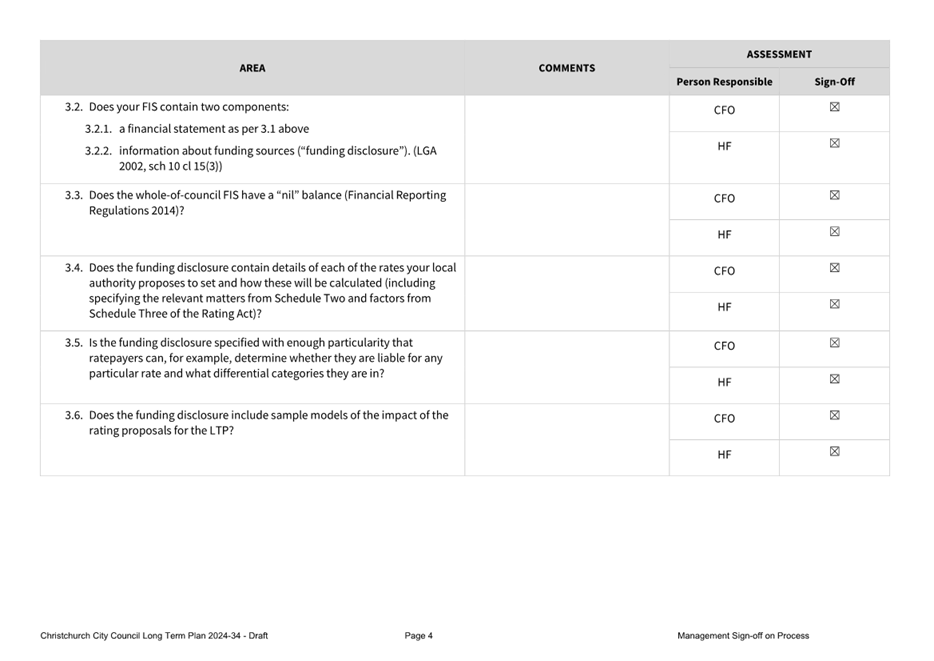

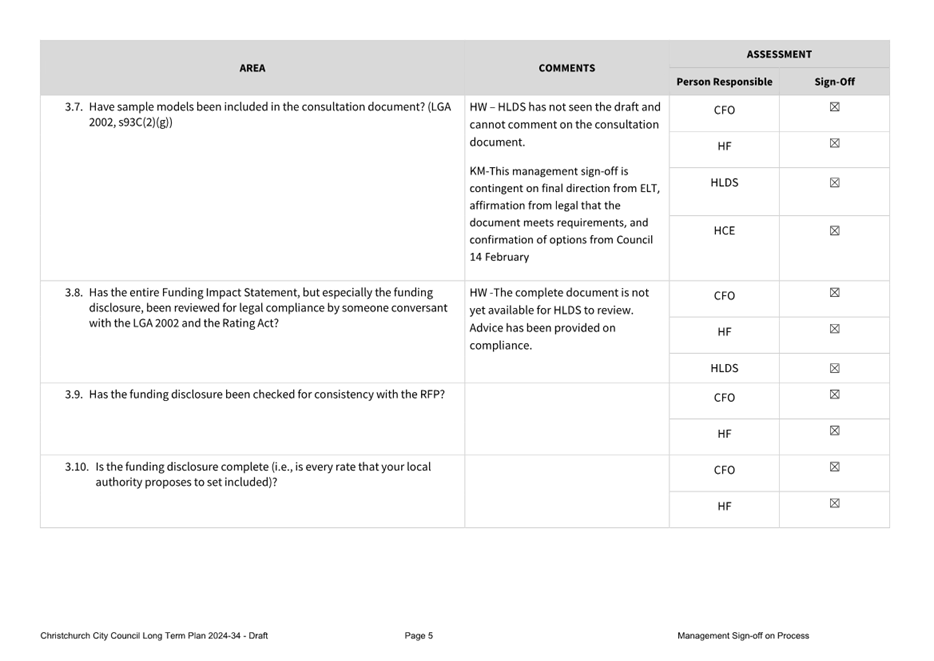

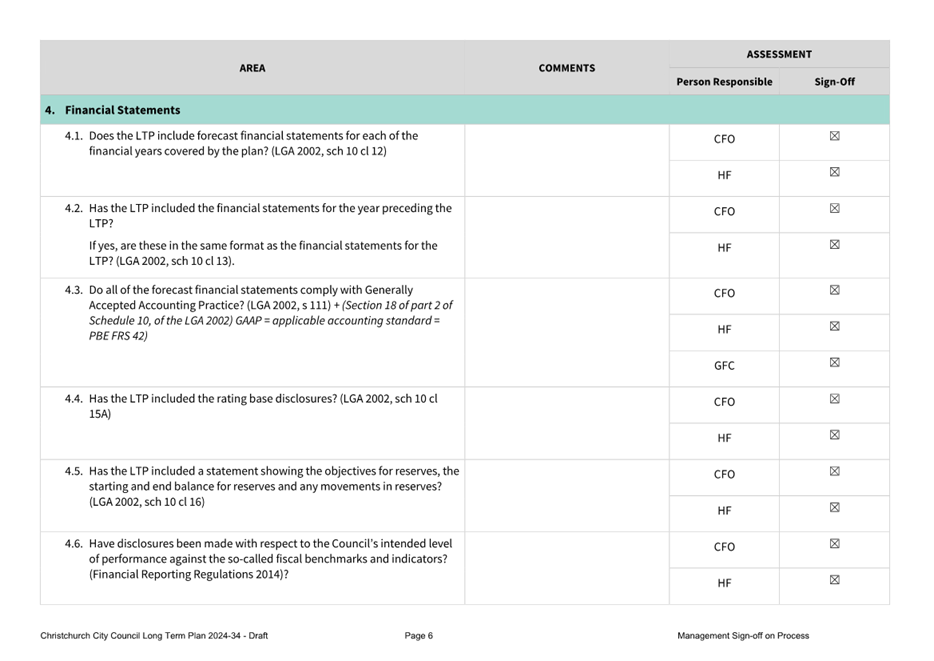

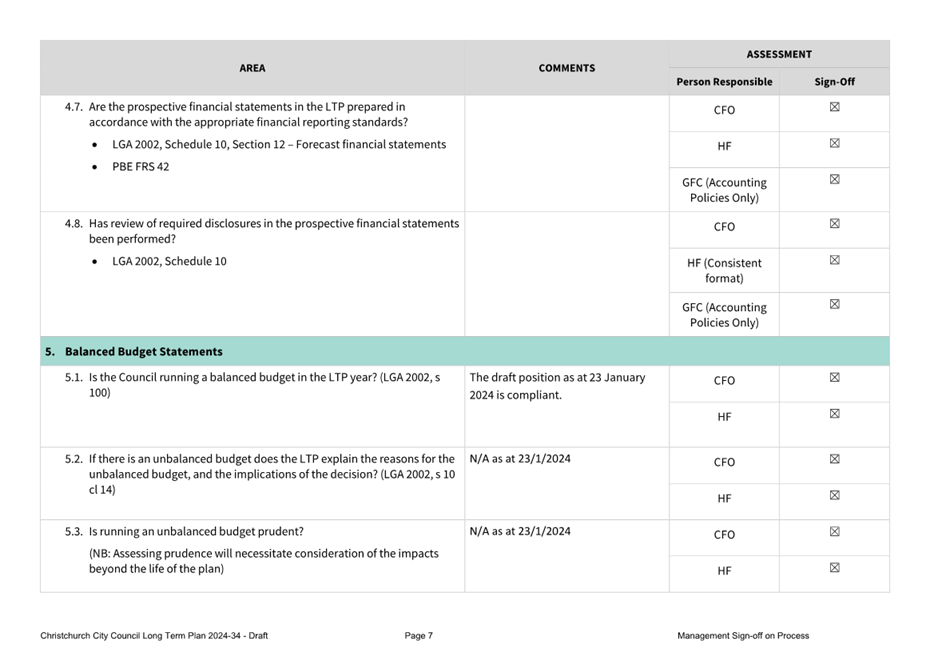

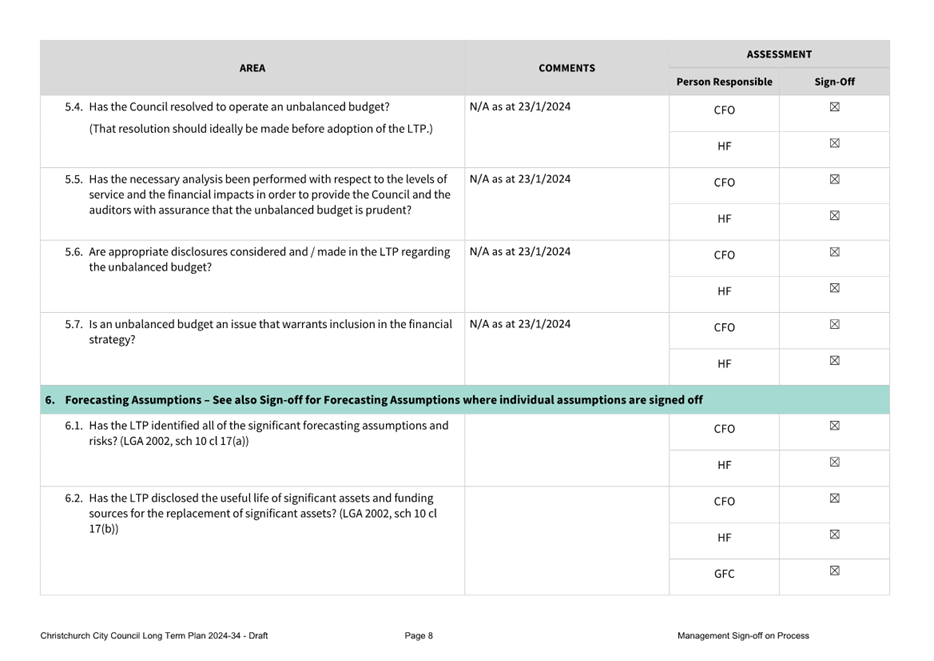

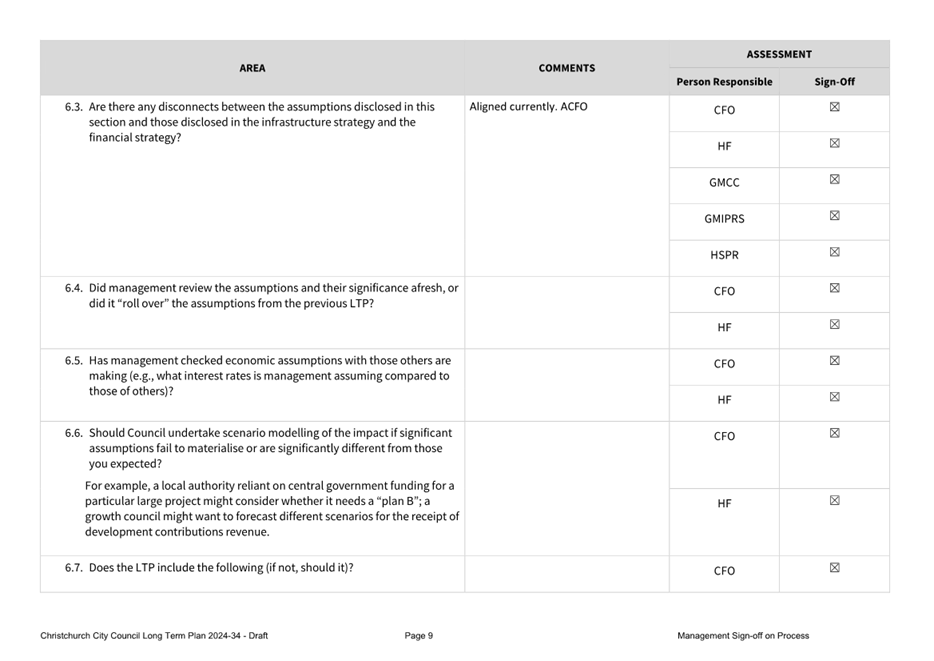

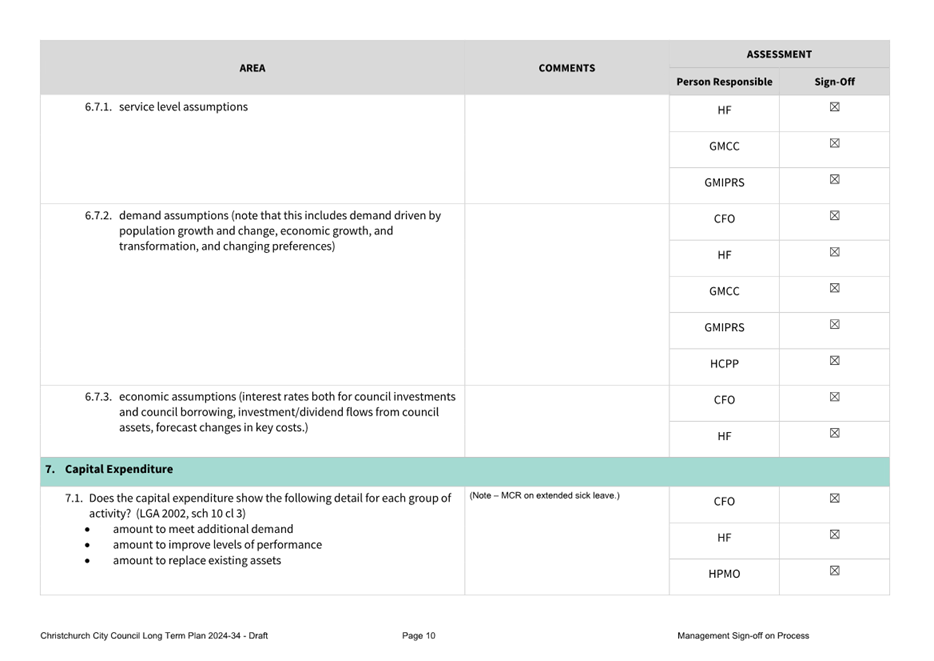

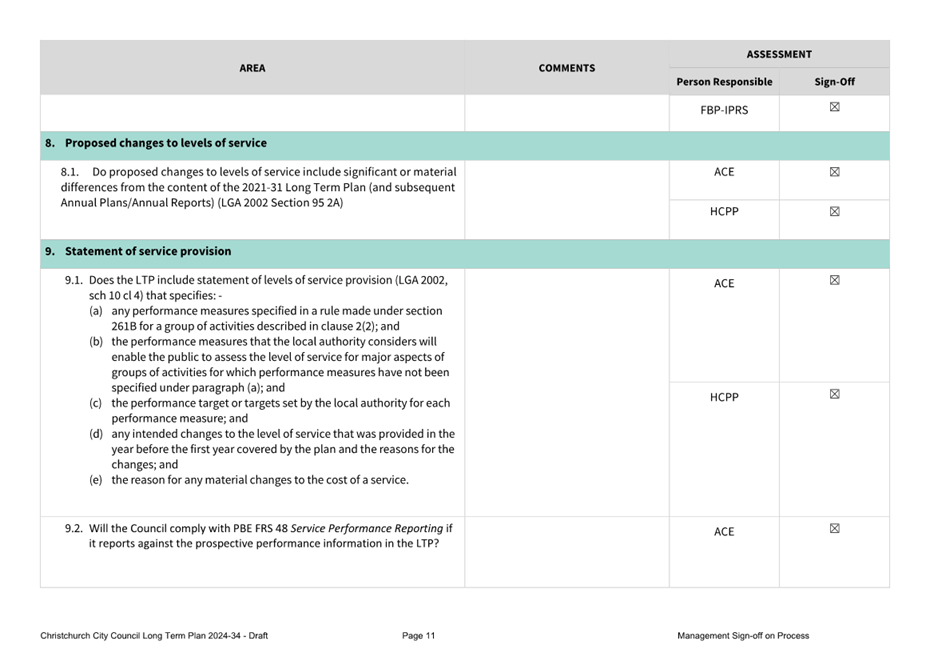

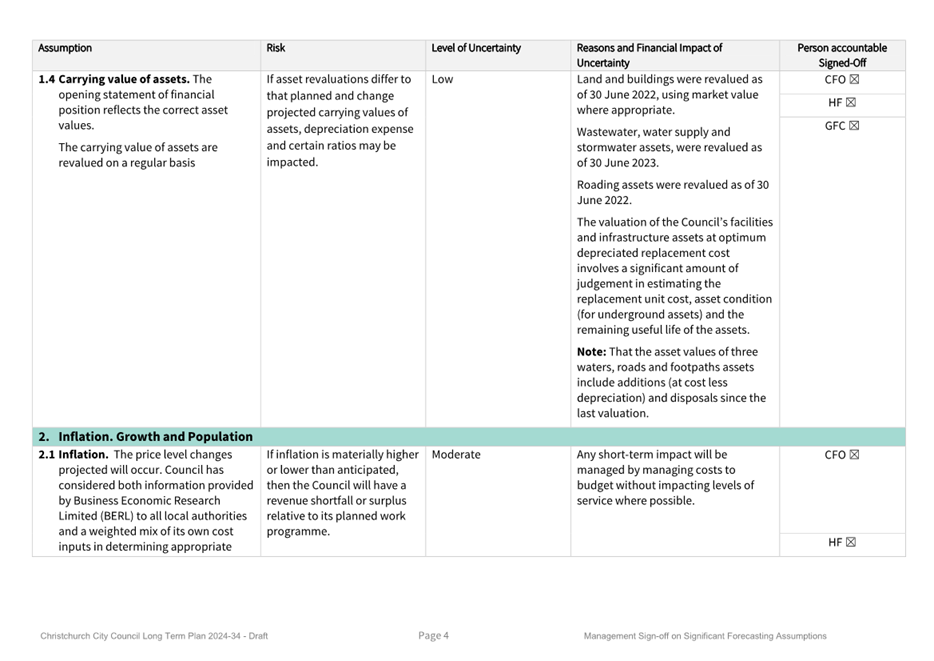

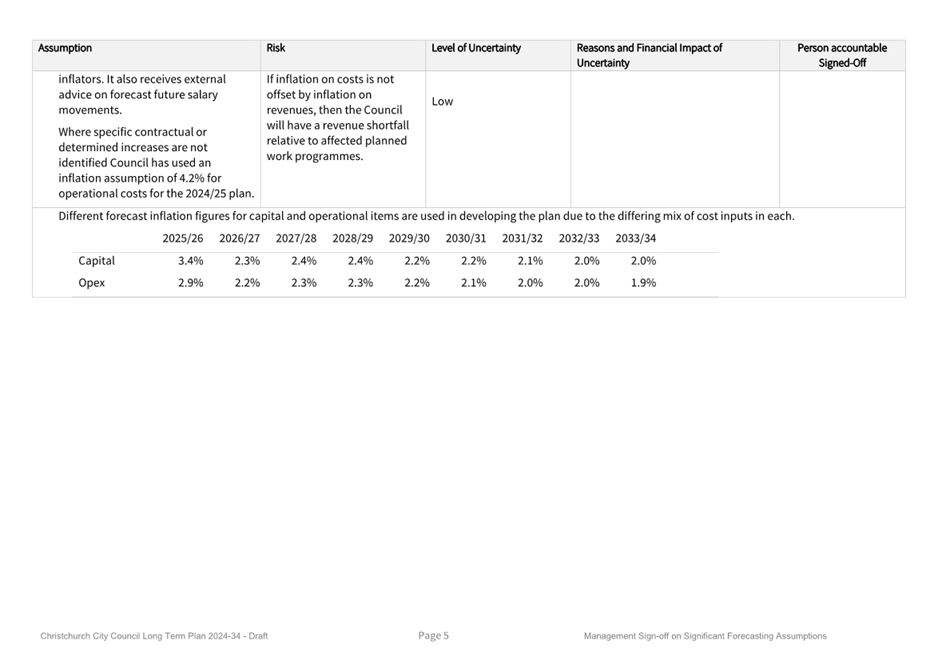

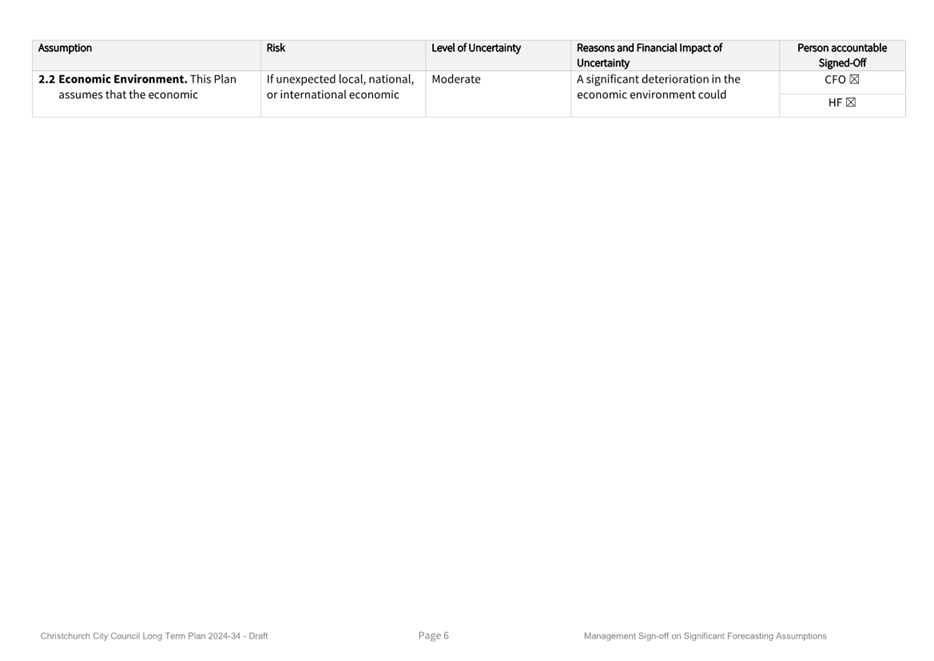

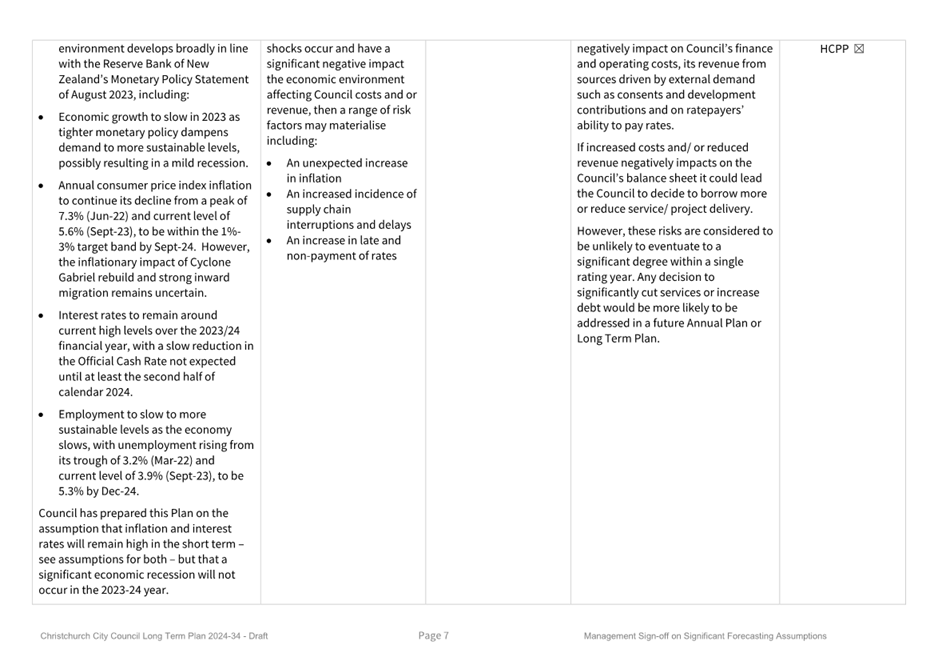

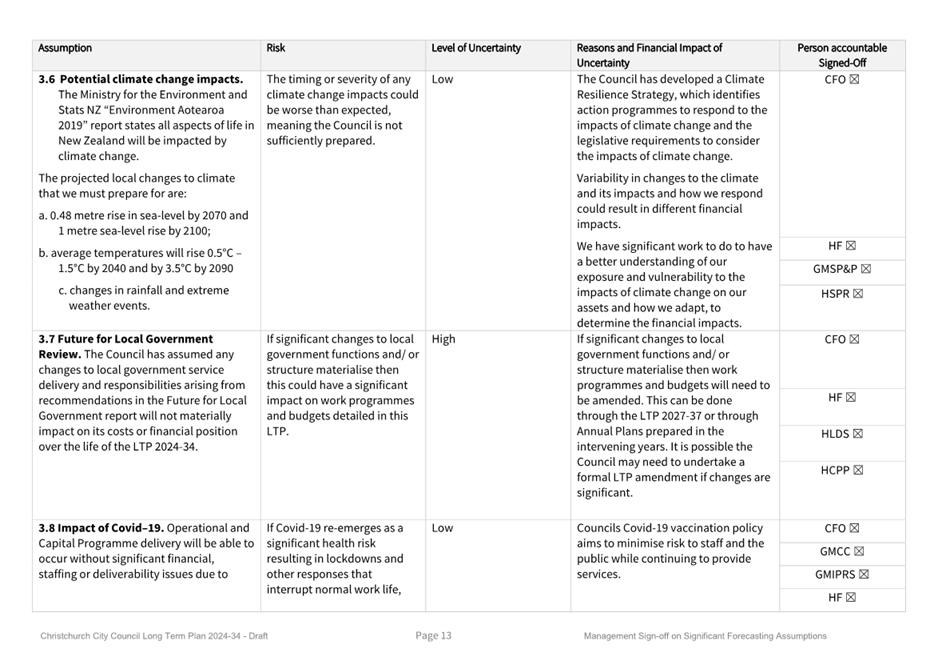

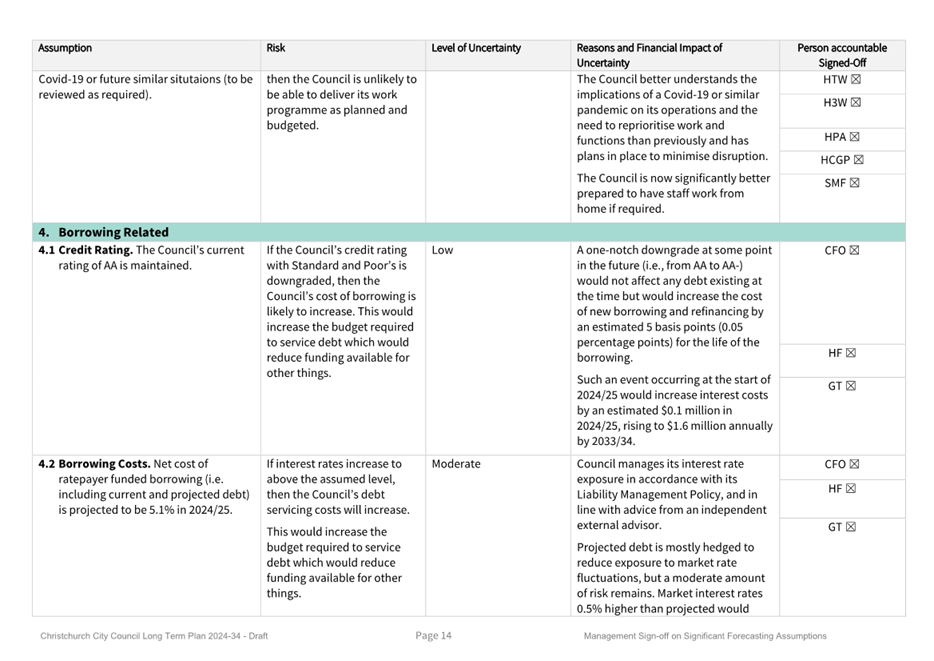

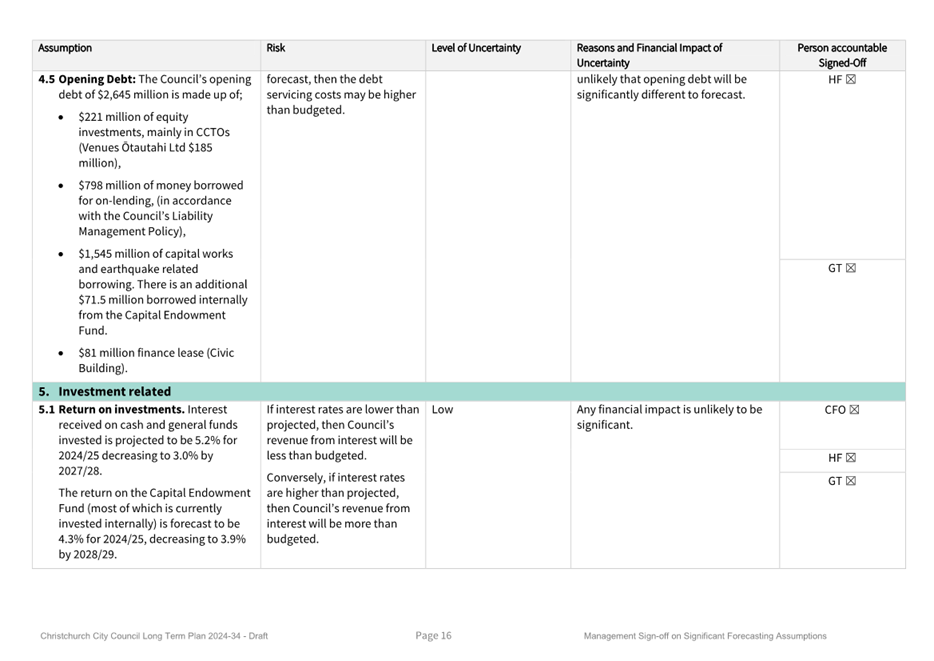

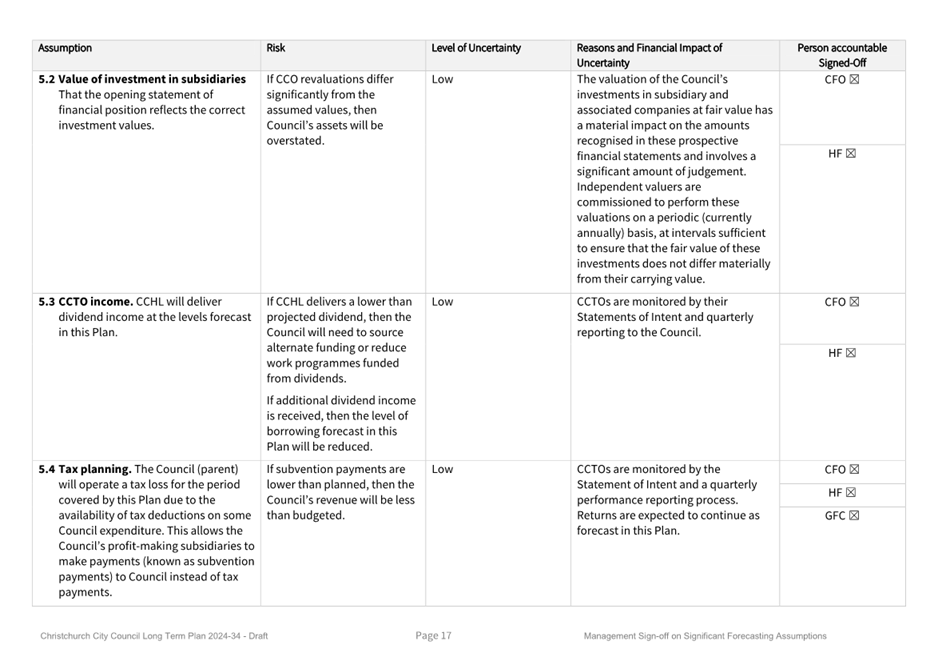

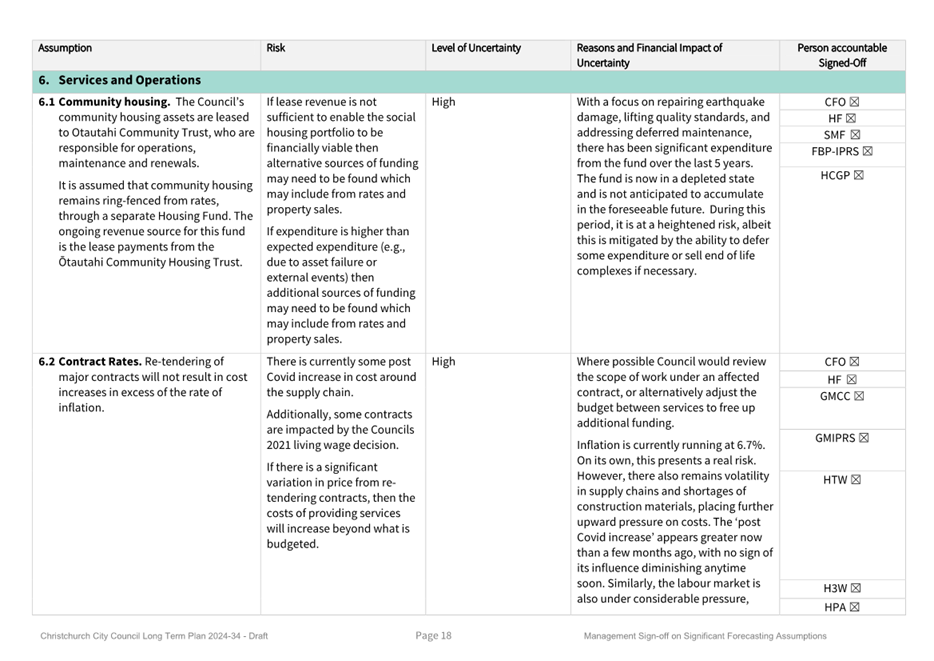

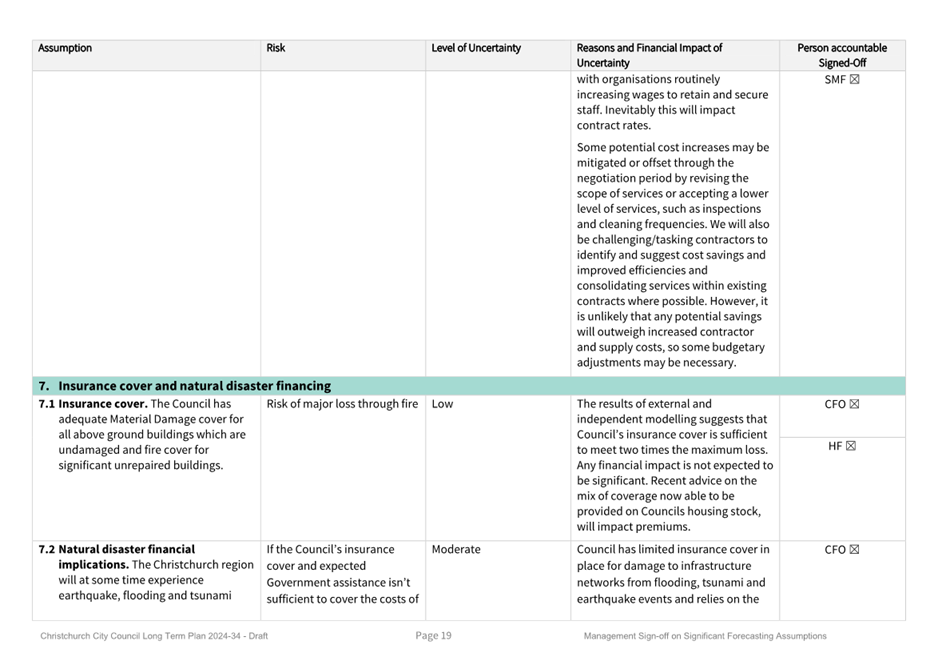

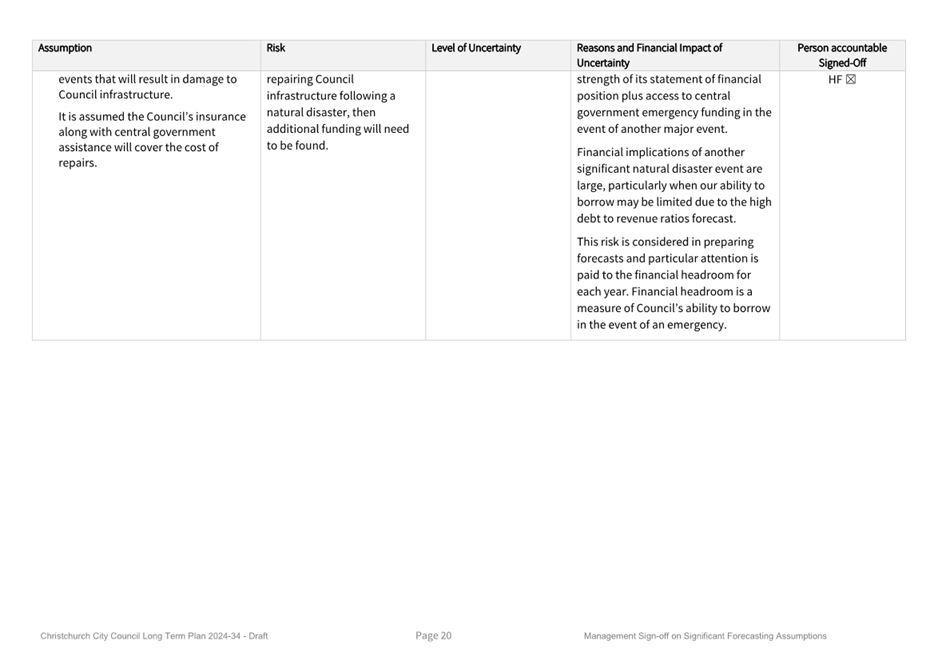

2024-34 - Management Sign-off for Significant Assumptions

|

24/171052

|

41

|

|

f

|

Early draft of

the draft LTP 2024-34 adoption report to Council (Under Separate Cover) - Confidential

|

23/2098528

|

|

|

g ⇩

|

LTP 2024-34

Letter of Expectation

|

24/140762

|

61

|

In addition to the attached documents, the following background

information is available:

|

Document

Name – Location / File Link

|

|

Not

applicable

|

Confirmation of Statutory

Compliance Te Whakatūturutanga ā-Ture

|

Compliance with Statutory Decision-making

Requirements (ss 76 - 81 Local Government Act 2002).

(a) This report contains:

(i) sufficient information about all reasonably practicable

options identified and assessed in terms of their advantages and

disadvantages; and

(ii) adequate consideration of the views and preferences of

affected and interested persons bearing in mind any proposed or previous

community engagement.

(b) The information reflects the level of significance of the

matters covered by the report, as determined in accordance with the Council's

significance and engagement policy.

|

Signatories Ngā Kaiwaitohu

|

Authors

|

Boyd Kedzlie -

Senior Corporate Planning & Performance Analyst

Peter Ryan -

Head of Corporate Planning & Performance

|

|

Approved By

|

Peter Ryan -

Head of Corporate Planning & Performance

Russell Holden

- Acting General Manager Resources/Chief Financial Officer

Lynn

McClelland - Assistant Chief Executive Strategic Policy and Performance

Jane Parfitt -

Interim General Manager Infrastructure, Planning and Regulatory Services

Mary

Richardson - Interim Chief Executive

|

|

Audit and Risk Management Committee

08 February 2024

|

|

|

Audit and Risk Management Committee

08 February 2024

|

|

|

Audit and Risk Management Committee

08 February 2024

|

|

|

Audit and Risk Management Committee

08 February 2024

|

|

|

9. Resolution to Exclude the Public

|

Section 48, Local Government Official

Information and Meetings Act 1987.

I move that the public be excluded from the

following parts of the proceedings of this meeting, namely items listed

overleaf.

Reason for passing this resolution: good

reason to withhold exists under section 7.

Specific grounds under section 48(1) for

the passing of this resolution: Section 48(1)(a)

Note

Section 48(4) of the Local Government

Official Information and Meetings Act 1987 provides as follows:

“(4) Every resolution to exclude the

public shall be put at a time when the meeting is open to the public, and the

text of that resolution (or copies thereof):

(a) Shall

be available to any member of the public who is present; and

(b) Shall

form part of the minutes of the local authority.”

This resolution is made in reliance on

Section 48(1)(a) of the Local Government Official Information and Meetings Act

1987 and the particular interest or interests protected by Section 6 or Section

7 of that Act which would be prejudiced by the holding of the whole or relevant

part of the proceedings of the meeting in public are as follows:

|

Audit and Risk Management Committee

08 February 2024

|

|

|

ITEM NO.

|

GENERAL SUBJECT OF EACH MATTER TO BE CONSIDERED

|

SECTION

|

SUBCLAUSE AND REASON UNDER THE ACT

|

PLAIN ENGLISH REASON

|

WHEN REPORTS CAN BE REVIEWED FOR POTENTIAL RELEASE

|

|

8.

|

Consideration of the Council's Draft Long-term Plan LTP 2024-34

process

|

|

|

|

|

|

|

Attachment a - Draft Consultation document

|

s7(2)(b)(ii)

|

Prejudice Commercial Position

|

Council report and key attachments will be released on the public

agenda on the 9 February 2024 for adoption meeting of the 14 February 2024.

|

14 February 2024

Council adoption meeting.

|

|

|

Attachment b - Draft Financial Strategy

|

s7(2)(b)(ii)

|

Prejudice Commercial Position

|

Council report and key attachments will be released on the public

agenda on the 9 February 2024 for adoption meeting of the 14 February 2024.

|

14 February 2024

Council adoption meeting.

|

|

|

Attachment c - Draft Infrastructure Strategy

|

s7(2)(b)(ii)

|

Prejudice Commercial Position

|

Council report and key attachments will be released on the public

agenda on the 9 February 2024 for adoption meeting of the 14 February 2024.

|

14 February 2024

Council adoption meeting.

|

|

|

Attachment f - Early draft of the draft LTP

2024-34 adoption report to Council

|

s7(2)(b)(ii)

|

Prejudice Commercial Position

|

Council report and key attachments will be released on the public

agenda on the 9 February 2024 for adoption meeting of the 14 February 2024.

|

14 February 2024

Council adoption meeting.

|

|

10.

|

Public Excluded Audit and Risk Management

Committee Minutes - 7 December 2023

|

|

|

Refer to the previous public excluded reason in the agendas for

these meetings.

|

|

|

11.

|

Audit Management Report 2023

|

s7(2)(c)(i)

|

Protection of Source of Information

|

Information on CCC internal systems are disclosed within this

report.

|

10 February 2025

Conclusion of the review of CCC internal systems.

|